wind and water power program wind energy cost, performance and

TRANSCRIPT

Energy Efficiency & Renewable Energy eere.energy.gov

1

Program Name or Ancillary Text eere.energy.gov

WIND AND WATER POWER PROGRAM

1

Wind Energy Cost, Performance and Pricing Trends: Past & Future

Ryan Wiser Lawrence Berkeley

National Laboratory

2013 National Summit on RPS

November 6, 2013

WIND AND WATER POWER PROGRAM

2

• 13.1 GW of wind added in 2012, more than 90% higher than 2011

• $25 billion invested in wind power project additions

• Cumulative wind power capacity up by 28%, bringing total to 60 GW

Wind Power Additions Hit a New Record in 2012, in Part Driven By the Then-Planned Expiration of Federal Tax Incentives

0

5

10

15

20

25

30

35

40

45

50

55

60

65

70

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Annual U.S. Capacity (left scale)

Cumulative U.S. Capacity (right scale)

Cu

mu

lati

ve

Ca

pa

cit

y (

GW

)

An

nu

al

Ca

pa

cit

y (

GW

)

WIND AND WATER POWER PROGRAM

3

Wind Power Was the Largest Source of U.S. Generating Capacity Additions in 2012

• Wind was, for the first time, the largest resource added in terms of gross capacity, despite persistently low natural gas prices

0%

10%

20%

30%

40%

50%

0

20

40

60

80

100

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

To

tal A

nnual

Cap

acity A

dd

itio

ns (G

W)

Wind Other Renewable Gas

Coal Other Non-Renewable Wind (% of Total)

Win

d C

apac

ity

Ad

dit

ion

s(%

of T

ota

l An

nu

al C

apac

ity

Ad

dit

ion

s)

WIND AND WATER POWER PROGRAM

4

• Past deployment substantially impacted by wind

technology improvement, and impacts on:

Cost trends

Performance trends

Pricing trends

• Future deployment may be impacted to an even

greater degree, given policy uncertainty at

Federal and State levels

• Presentation focused on past and near-term

trends, limited to land-based wind

WIND AND WATER POWER PROGRAM

5

Past Trends: Cost

WIND AND WATER POWER PROGRAM

6

Wind Turbine Prices Remain Well Below the Levels Seen Several Years Ago

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

Jan-9

7

Jan-9

8

Jan-9

9

Jan-0

0

Jan-0

1

Jan-0

2

Jan-0

3

Jan-0

4

Jan-0

5

Jan-0

6

Jan-0

7

Jan-0

8

Jan-0

9

Jan-1

0

Jan-1

1

Jan-1

2

Jan-1

3

Announcement Date

U.S. Orders <5 MW

U.S. Orders from 5 - 100 MW

U.S. Orders >100 MW

Vestas Global Average

Polynomial Trend Line for Orders

Turb

ine T

ransa

ctio

n P

rice

(2012$

/kW

)

Recently reported global

average prices

Figure depicts reported transaction prices from 102 U.S. wind turbine orders totaling 27 GW

Escalation in turbine prices from 2003 through 2008: rising

commodity prices; increased labor costs; improved

manufacturer profitability; turbine up-scaling

WIND AND WATER POWER PROGRAM

7

Reported Installed Project Costs Continue to Trend Lower

0

1,000

2,000

3,000

4,000

5,000

6,000

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Inst

all

ed

Pro

ject

Co

st (

20

12

$/k

W)

Commercial Operation Date

Individual Project Cost (689 projects totaling 49,414 MW)

Capacity-Weighted Average Project Cost

Whereas turbine prices peaked in 2008/2009, project-level installed costs peaked in

2009/2010, reflecting the normal passage of time between when a turbine supply

agreement is signed and when those turbines are actually installed

2012 average:

$1,940/kW,

down $200/kW

from 2011;

down $300/kW

from peak

WIND AND WATER POWER PROGRAM

8

Some Regional Differences in Average Wind Power Project Costs Are Apparent

Different permitting/development costs may play a role at both ends of spectrum: it’s easier/cheaper to build in the US interior and harder/more expensive along the coasts

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Interior42 projects3,827 MW

Northeast29 projects1,101 MW

Great Lakes21 projects1,529 MW

West25 projects2,938 MW

Southeast1 project19 MW

Inst

alle

d P

roje

ct C

ost

(2

01

2 $

/kW

)

Capacity-Weighted Average Project Cost

Individual Project Cost

Capacity-Weighted Average Cost, Total U.S.

Sample includes projects built in 2012

WIND AND WATER POWER PROGRAM

9

Past Trends: Performance

WIND AND WATER POWER PROGRAM

10

Regional Variations in Capacity Factor Reflect the Strength of the Wind Resource

0%

10%

20%

30%

40%

50%

60%

Southeast4 projects308 MW

Northeast6 projects289 MW

West37 projects2,452 MW

Great Lakes15 projects2,077 MW

Interior48 projects5,430 MW

Generation-Weighted Average (by region)

Generation-Weighted Average (total U.S.)

Individual Project (by region)

20

12

Ca

pa

city

Fa

cto

r

Sample includes 110 projects built in 2010 or 2011 and totaling 10.6 GW

WIND AND WATER POWER PROGRAM

Average Hub Height and Rotor Diameter Have Increased Dramatically: Would Expect Capacity Factor Increases to Follow

• Two periods of rapid scaling: 1998-2006 and 2009-present

• 2007-2008 mostly stagnant, as OEMs focused on meeting demand

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

0

10

20

30

40

50

60

70

80

90

100

1998-99 2000-01 2002-03 2004-05 2006 2007 2008 2009 2010 2011 2012

Commercial Operation Year

Average Nameplate Capacity (right scale)

Average Rotor Diameter (left scale)

Average Tower Height (left scale)

Mete

rs

MW

11

WIND AND WATER POWER PROGRAM

As Dominant Turbine OEM in the US, GE Provides a Useful Example of the Evolution of Turbine Design

2.60

m2/kW

3.10

m2/kW

3.30

m2/kW

4.85

m2/kW

4.85

m2/kW

2002 2010 2012- (standard) 2012- (lower wind speed) 12

WIND AND WATER POWER PROGRAM

However, Trends in Sample-Wide Capacity Factors Were Impacted by Curtailment and Inter-Year Wind Resource Variability…

The wind resource index is compiled from NextEra Energy Resources reports. The pre-2007 portion of the index is adjusted to

approximate the conversion from wind speed to generation (this adjustment is unnecessary starting in 2007). 13

0.00

0.15

0.30

0.45

0.60

0.75

0.90

1.05

1.20

0%

5%

10%

15%

20%

25%

30%

35%

40%

200010

591

200130

943

200273

2,682

200384

3,128

2004106

4,500

2005129

5,142

2006153

7,967

2007196

9,951

2008240

14,926

2009339

23,617

2010452

33,381

2011516

38,561

2012446

42,844

Lon

g-Term

Win

d R

eso

urce

Ind

ex

Sam

ple

-Wid

e C

apac

ity

Fact

or

Capacity Factor Based on Estimated Generation (if no curtailment in subset of regions)

Capacity Factor Based on Actual Generation (with curtailment)

Wind Resource Index (right scale)

# MW:

# Projects:Year:

WIND AND WATER POWER PROGRAM

And… Despite Turbine Scaling that Should Boost Capacity Factors, Project Build-Out in Lower-Quality Wind Resource Areas Has Pushed the Other Way

14

275

305

335

365

395

425

75

80

85

90

95

100

1998-99 2000-01 2002-03 2004-05 2006 2007 2008 2009 2010 2011 2012

Commercial Operation Date

Average 80m Wind Resource Quality Among Built Projects (left scale)

Average Specific Power Among Built Projects (right scale)

Ind

ex

of

Win

d R

eso

urc

e Q

ua

lity

at

80

m (

19

98

-99

=1

00

)

Sp

eci

fic

Po

we

r (W

/m^

2 )

WIND AND WATER POWER PROGRAM

15

Past Trends: Wind Power Price

WIND AND WATER POWER PROGRAM

16

Sample of Wind Power Prices

• Berkeley Lab collects data on historical wind power sales prices, and long-term PPA prices

• PPA sample includes 302 contracts from projects built from 1998-2012, totaling 24,626 MW (42% of all wind capacity added in that period, and 70% of all capacity added that is sold under bundled PPAs)

• Prices reflect the bundled price of electricity and RECs as sold by the project owner under a power purchase agreement

– Dataset excludes merchant plants and projects that sell renewable energy certificates (RECs) separately

– Prices reflect receipt of state and federal incentives (e.g., the PTC or Treasury grant), as well as various local policy and market influences; as a result, prices do not reflect wind energy generation costs

WIND AND WATER POWER PROGRAM

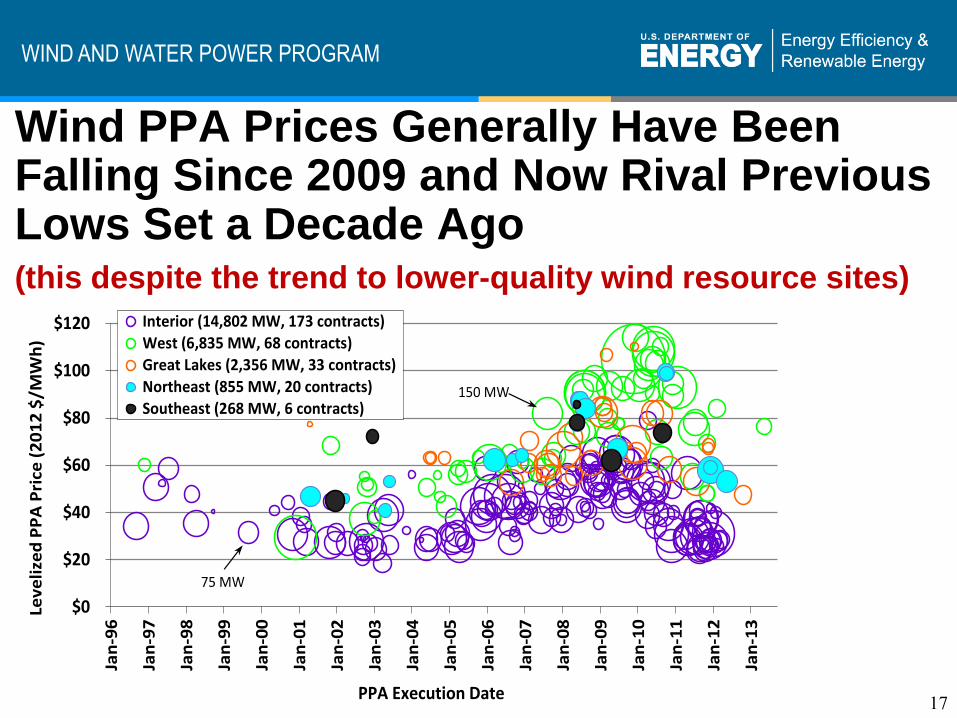

Wind PPA Prices Generally Have Been Falling Since 2009 and Now Rival Previous Lows Set a Decade Ago

(this despite the trend to lower-quality wind resource sites)

17

$0

$20

$40

$60

$80

$100

$120

Jan

-96

Jan

-97

Jan

-98

Jan

-99

Jan

-00

Jan

-01

Jan

-02

Jan

-03

Jan

-04

Jan

-05

Jan

-06

Jan

-07

Jan

-08

Jan

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

PPA Execution Date

Interior (14,802 MW, 173 contracts)

West (6,835 MW, 68 contracts)

Great Lakes (2,356 MW, 33 contracts)

Northeast (855 MW, 20 contracts)

Southeast (268 MW, 6 contracts)

Lev

eli

zed

PP

A P

rice

(2

01

2 $

/MW

h)

75 MW

150 MW

WIND AND WATER POWER PROGRAM

A Smoother Look at the Time Trend Shows Steep Recent Decline in Pricing; Especially Low Pricing in Interior Region

18

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

1996-9910

553

2000-0117

1,249

2002-0324

1,382

2004-0530

2,190

200630

2,311

200726

1,781

200839

3,465

200947

3,982

201040

3,999

201134

3,533

20128

630

Ave

rag

e L

eve

lize

d P

PA

Pri

ce (

Re

al

20

12

$/M

Wh

)

Nationwide Interior

Great Lakes West

Northeast

PPA Year:Contracts:

MW:

WIND AND WATER POWER PROGRAM

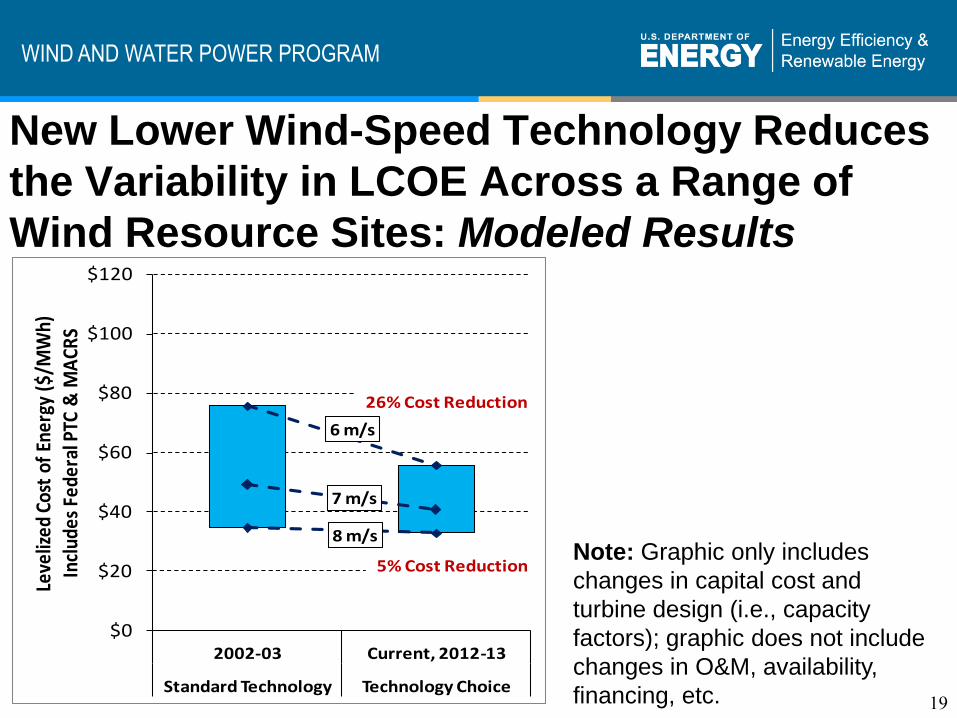

New Lower Wind-Speed Technology Reduces

the Variability in LCOE Across a Range of

Wind Resource Sites: Modeled Results

8 m/s

7 m/s

6 m/s

$0

$20

$40

$60

$80

$100

$120

2002-03 Current, 2012-13

Standard Technology Technology Choice

Leve

lized

Cos

t of

Ene

rgy

($/M

Wh)

Incl

udes

Fed

eral

PTC

& M

ACR

S

26% Cost Reduction

5% Cost Reduction

19

Note: Graphic only includes

changes in capital cost and

turbine design (i.e., capacity

factors); graphic does not include

changes in O&M, availability,

financing, etc.

WIND AND WATER POWER PROGRAM

Available Land Area Exceeding LCOE

Thresholds Has Increased: Modeled Results

2002-03:Standard Technology

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

$30 $40 $50 $60 $70 $80 $90

Ava

ilab

le L

and

Are

a (k

m2)

Levelized Cost of Energy ($/MWh)

2012-13:Lowest CostTech Choice

w/: PTC/MACRS

w/o: PTC/MACRS $57 $67 $77 $89 $99 $110 $121

Percentage Increase Since 2002-2003:

< $35/MWh w/ PTC & MACRS: 42%

< $55/MWh w/ PTC & MACRS: 48%

< $75/MWh w/ PTC & MACRS: 25%

20

WIND AND WATER POWER PROGRAM

21

Current and Future Trends

WIND AND WATER POWER PROGRAM

22

Areas of Continued Wind Power Technology Advancement

Land-based wind technology is relatively mature,

but continued advancement opportunities include:

• Plant-level design and management to maximize production

• Advanced control systems for turbines and plants to increase

energy production, reduce loads

• Improved numerical methods for understanding wind resource

• Blade innovations to increase performance, reduce loads & noise

• Multiple drivetrain technologies, with increase reliability

• Enhanced reliability & robustness among all components & systems

• Continued turbine scaling, especially low to mid wind speed sites

WIND AND WATER POWER PROGRAM

Most Projections for Land-Based Wind

Plant LCOE Anticipate Further Reductions

Note: Projections included here were derived from a variety of methods including

learning curves, expert elicitation, and engineering-based models 23

WIND AND WATER POWER PROGRAM

Focusing on Projects Installed from 2009-2012 (to control for resource quality) and on Capacity Factor in First Six Months of 2013 (to include 2012 installations) Shows Technology Evolution

24

Specific Power < 260 = recent, lower wind-speed models such as GE 1.6 MW / 100m rotor;

Siemens 2.3/108; Vestas 1.8/100; Nordex 2.4/117; Specific Power < 220 = GE 1.6/100

Note: Very small

sample size exists

for some of these

categories

WIND AND WATER POWER PROGRAM

25

Recent PPA Trends Suggest Further Price Reductions (and capacity factor increases) • Xcel (SPS; 700 MW proposed to regulator):

• 5700 MW of bids < $30/MWh w/ RECs [RECs value <$2.5/MWh]

• Mammoth -- 199 MW, OK, 57.1% CF: $22/MWh energy only

• Palo Duro -- 249 MW, TX, 54.1% CF: $23/MWh energy only

• Roosevelt -- 250 MW, NM, 48.4% CF: $23/MWh energy only

• Xcel (CO, MN; 1200 MW total): $25-35/MWh

"It works out to a very good levelized cost for our customers," Xcel CEO Fowke

said. "These prices are so compelling, the energy [cost] associated with it is

less than you can do locking in a 20-year gas strip.” Xcel expects the wind

projects to save its customers about $800 million in fuel costs over 20 years.

• AEP-PSO (OK; 600 MW): 50.6% expected capacity factor

• OPPD (NE; 400 MW): 50% expected capacity factor

WIND AND WATER POWER PROGRAM

26

Though Low Wholesale Electricity Prices Have Challenged the Relative Economics of Wind Power in Recent Years…

0

10

20

30

40

50

60

70

80

90

100

Interior28 projects2,969 MW

Great Lakes4 projects219 MW

Northeast3 projects210 MW

West7 projects766 MW

Total US42 projects4,163 MW

Average 2012 Wholesale Power Price Range

Individual Project Levelized Wind PPA Price

Generation-Weighted Average Levelized Wind PPA Price

Wind project sample includes projects with PPAs signed in 2011 or 2012

2012

$/M

Wh

Wind PPA prices are most competitive with wholesale prices in the Interior

region (where PPAs signed in 2011/2012 generally ranged from $20-40/MWh)

WIND AND WATER POWER PROGRAM

Uncertainties in Future Natural Gas Prices Are Substantial, and Upwards Trajectory in Prices Is Anticipated

Source: LBNL compilation of forecasts and data from the Energy Information Administration

3

4

5

6

7

8

9

10

11

19

97

19

99

20

01

20

03

20

05

20

07

20

09

20

11

20

13

20

15

20

17

20

19

20

21

20

23

20

25

20

27

20

29

20

31

20

33

20

35

20

37

20

39

Nat

ura

l Gas

Pri

ce D

eliv

ere

d t

o E

lect

rici

ty

Ge

ne

rato

rs (

20

12

$/M

MB

tu)

1998-2001

2008

2009 2010

2012

2011

2013(Ref)

2002

2005

2006-07

2004

2003

Actual

2013(High)

2013(Low)

Actual versus AEO Projections

27

WIND AND WATER POWER PROGRAM

Recent Wind PPAs Can Compete on a Long-Term Basis, and Many Very Recent PPAs Can Compete in Short Term; PTC Plays a Key Role in this Competitiveness

Note: Wind is modeled as “fuel saver” – i.e., assumed to offset only fuel costs of gas generation (no credit for capacity value, etc.)

*Fuel cost projections are translated from $/MMBtu into $/MWh terms using average heat rates implied in the NEMS modeling output

0

20

40

60

80

100

120

140

19

99

20

01

20

03

20

05

200

7

20

09

20

11

20

13

20

15

20

17

20

19

202

1

20

23

20

25

20

27

20

29

20

31

20

33

203

5

20

37

20

39

20

41

20

43

20

45

No

min

al $

/MW

h

Range of recent EIA gas scenarios* AEO11 reference gas AEO12 reference gas AEO13 reference gas Historical gas Wind PPA sample Wind PPA sample (no PTC)

+$23/MWh if no PTC

Wind PPA sample includes only those signed in 2011 or 2012: 38 PPAs totaling 3,876 MW

28

Many current PPAs in Interior

WIND AND WATER POWER PROGRAM

29

Conclusions

WIND AND WATER POWER PROGRAM

30

Current Low Prices for Wind Energy Can Compete with Only the Operating Cost of Natural Gas Plants in Some Areas, and May Support Higher Growth in the Future, but Other Pricing Headwinds Include…

• Lack of clarity about fate of federal tax incentives

• Continued low natural gas and wholesale electricity prices

• Growing competition from solar in some regions

WIND AND WATER POWER PROGRAM

31

Regional Definitions Based on Combination of Geography and Wind Resource

Interior

GreatLakes

West

Southeast

Northeast