will container shipping sail or sink

DESCRIPTION

Outlook for Container Shipping Industry in 2013TRANSCRIPT

WILL GLOBAL CONTAINER SHIPPING SAIL OR SINK? Jefferies Asia Pacific : Cross-Thinking Summit Hong Kong/Singapore 10/13 July 2012

The worldwide reference in liner shipping

Important Disclosure: Any views or opinions expressed by the third party experts are solely those of the speaker, not Jefferies, and this does not represent an endorsement by Jefferies of the view or opinions expressed.

Turnaround play but recovery remains fragile ► 2009-2012 has been the most volatile period in industry history ► Despite the recovery in 2012, outlook remains weak and tentative

(c) Alphaliner 2011 2

‐16% ‐16% ‐16% ‐10%

0%

9%

15%

7%

‐1% ‐5%

‐7% ‐10%

‐11%

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

Average Ca

rrier O

peratin

g Margin

Average of APL, CMA CGM, CCNI, CSAV, CSCL, EMC, Hanjin, HMM, Hapag‐Lloyd, KL, Maersk, MOL, NYK, RCL, SITC, STX Pan Ocean, WHL, YML, Zim

Potential

“negative to neutral” results for full year

Demand contraction Excess supply

Demand recovery Discipline or desperation??

Market forecasts 1Q 2012 results below market forecast

First - the Good News! ► Breakeven by some lines in April-May ► June should be profitable for most carriers ► 2Q cashflow remains tight but 3Q liquidity will improve

(c) Alphaliner 2011 3

Freight rates up sharply

0

200

400

600

800

1,000

1,200

1,400

1,600

Jan‐98

Jan‐99

Jan‐00

Jan‐01

Jan‐02

Jan‐03

Jan‐04

Jan‐05

Jan‐06

Jan‐07

Jan‐08

Jan‐09

Jan‐10

Jan‐11

Jan‐12

CCFI In

dex (Jan

1998=1,00

0)

CCFI

0

200

400

600

800

1,000

1,200

1,400

1,600

Jan‐98

Jan‐99

Jan‐00

Jan‐01

Jan‐02

Jan‐03

Jan‐04

Jan‐05

Jan‐06

Jan‐07

Jan‐08

Jan‐09

Jan‐10

Jan‐11

Jan‐12

CCFI In

dex (Jan

1998=1,00

0)

CCFI

Fuel Adjusted Freight Index

(both gross & adjusted)

0

200

400

600

800

1000

1200

1400

1600

Jan‐98

Jan‐99

Jan‐00

Jan‐01

Jan‐02

Jan‐03

Jan‐04

Jan‐05

Jan‐06

Jan‐07

Jan‐08

Jan‐09

Jan‐10

Jan‐11

Jan‐12

CCFI In

dex (Jan

1998=1,000)

FO $/tonCCFIFuel Adjusted Freight Index

Bunker costs down 20% ~ 4-5% margin improvement

Rates increased despite moderate load factors ► 2012 rate increases unusual - sharp jump achieved despite lacklustre

load factors 85-90% ► Historically, rate increases sustainable only when load factors > 95%

4

Demand outlook remains week ► 2012 rate recovery is not driven by demand growth

(c) Alphaliner 2011 5

2009 2010 2011 2012(F) FE‐Europe ‐14.8% 17.3% 4.7% 0.2% FE‐US ‐14.9% 16.9% ‐0.8% 3.3%

Can carriers live with lower load factors? ► Other asset-heavy industries can live with lower utilisation levels

(c) Alphaliner 2011 6

Container shipping as a commodity ► Fragmented/overcrowded industry; no M&A impetus ► Lower prices needed to win – Market leadership mainly by price ► Differentiation extremely difficult ► Contestable markets intense competition

(c) Alphaliner 2011 7

Few innovations in the industry Daily Maersk – launched Sep 2011

Competitors response:- CSCL : up to 10 sailings/wk CKYH : up to 9 sailings/wk Evergreen : up to 9 sailings/wk CMA CGM : 7 sailings/wk G6 : 6 sailings/wk

Forward rates trending down ► Rates in backwardation - trending down in 2H 2012 ► Forward rates suggests peak season expected to be brief

(c) Alphaliner 2011 8

Rate recovery has been tentative with significant rate volatility expected over the next 6 months In absence of space crunch, rates can only be held up with pricing discipline. Such discipline has only been exhibited in the past only when lines are in negative cashflow situations

Significant new deliveries committed ► High level of new vessel deliveries amongst Top 20 carriers in 2012

… will continue into 2013 ► Actions of a few carriers could disrupt market

(c) Alphaliner 2011 9

2013 Scheduled Deliveries

2012 Actual and Scheduled Deliveries (1 Jul 2012)

Total deliveries for main carriers in 2012 = 1.30 Mteu

Total deliveries for main carriers in 2013 = 1.38 Mteu

Already delivered

Scrapping is insufficient to redress balance ► 1H 2012 Deliveries YTD 805,000 teu ► 1H 2012 Scrapping YTD 169,000 teu ► New deliveries vs scrapping ratio : 5-to-1

(c) Alphaliner 2011 10

‐50,000

0

50,000

100,000

150,000

200,000

250,000

2008

Jan Jul

2009

Jan Jul

2010

Jan Jul

2011

Jan Jul

2012

Jan

Capa

city in

TEU

TEU ScrappedTEU deliveredNet Increase

Scrap candidates are limited ► Relatively young containership fleet ► Average TEU-weighted age is only 8 years

(c) Alphaliner 2011 11

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

2012

2011

2010

2009

2008

2007

2006

2005

2004

2003

2002

2001

2000

1999

1998

1997

1996

1995

1994

1993

1992

1991

1990

1989

1988

1987

1986

Pre‐19

86

TEU

Millions

Year Built

Size Range (TEU) >10,000 teu7,500‐10,000 teu5,100‐7,500 teu4,000‐5,100 teu3,000‐4,000 teu2,000‐3,000 teu1,000‐2,000 teu<1,000 teu

Ships built 1992 or earlier (20 years and above) represent only 5.3% of current fleet

Carriers fleet have different age profiles ► MSC – 12% of current fleet are potential scrap candidates ► APL, Maersk, Evergreen - Not many ships to scrap

(c) Alphaliner 2011 12

2%

12%

1%

4%

2%

9%

6%

5%

3%

0%

0%

0% 2%

0%

5%

0%

6%

2%

0%

1%

5%

0%

2%

4%

6%

8%

10%

12%

14%

0

50,000

100,000

150,000

200,000

250,000

300,000AP

M‐M

aersk

MSC

CMA CG

MCO

SCON

Evergreen

Hapag‐Lloyd APL

CSCL

Hanjin Shg

MOL

OOCL

NYK

Ham

burg Süd

Yang

Ming

HMM

K Line Zim PIL

CSAV

UAS

CWan

Hai

TEU

Ships ≥ 20 years As % of fleet (1 Jul 2012)

Chartered tonnage mismatch ► Chartered tonnage redeliveries would not solve carriers’

overcapacity challenge ► Size mismatch between vessels for redelivery vs new ships

(c) Alphaliner 2011 13

461

196

65 70

29 9

43

5 17

33

15 54

0

50

100

150

200

250

300

350

400

450

500

1000‐2000 2000‐3000 3000‐4000 4000‐5000 5000‐7500 above 7500

Units fo

r delivery

Size Range in TEU

Charter redeliveries vs New ship deliveries Jun‐Dec 2012

Charter redeliveries

New ship deliveries

Vessel Delivery Schedule ► High levels of new ship deliveries to continue in 2013

(c) Alphaliner 2011 14

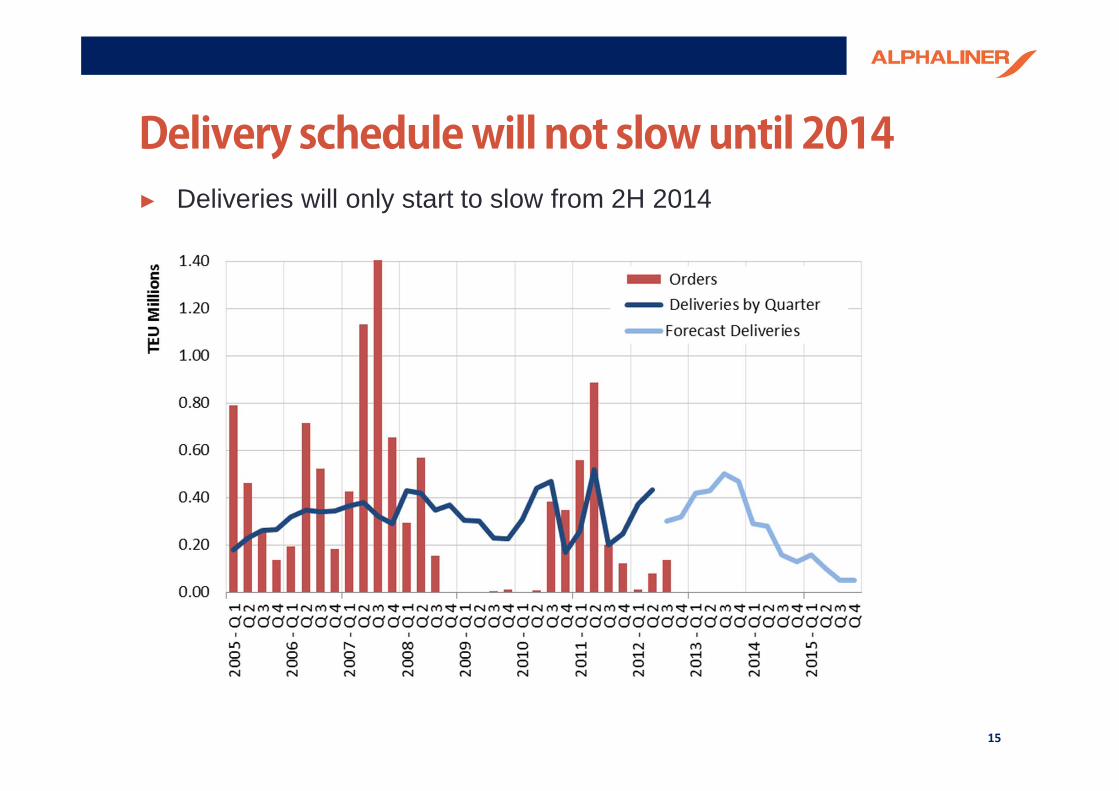

Delivery schedule will not slow until 2014 ► Deliveries will only start to slow from 2H 2014

(c) Alphaliner 2011 15

Big ships are coming … ► Maersk ‘EEE’ class ships delivery to begin mid-2013

(c) Alphaliner 2011 16

2013 remains challenging ► 2013 will see over 100 units of new VLCS deliveries ► Pace of deliveries will only slow in 2014

(c) Alphaliner 2011 17

Capacity discipline is key ► Rise in idle tonnage in 1Q 2012 sign of capacity discipline and key

driver of successful rate increase implementation in Jan-Apr ► But idle capacity has halved from 915,000 teu in March to 430,000

teu at end June

(c) Alphaliner 2011 18

Capacity creeping back ► Carriers have reintroduced 9% of capacity on FE-Europe and 10%

on FE-US routes since March ► Capacity restraint could be coming to an end – cascade of ULCS to

secondary trades are not optimal ► Further capacity in August could jeopardise rate recovery

(c) Alphaliner 2011 19

Slow Steaming not the cure-all But going slower does not … ►Slow steaming from 23 knots to 18 knots cuts FO consumption by 100 tons/day

►Super slow steaming from 18 knots to 13 knots cuts FO consumption by 55 tons/day

(c) Alphaliner 2011 20

Source : Maersk 2012

Conclusions ► Cycle has turned up but coming off a very weak 2011, while

earnings outlook is uncertain ► Liquidity remains a concern, especially for those with weak

capitalisation ► Positive 3Q results could provide relief and short-term positive

catalyst for equities but rate gains may not last into 4Q ► 2013 will still be a challenging year with supply-demand balance

likely only in 2014 ► Key indicators to track:-

► SCFI/CCFI – spot vs forward rates ► Capacity utilisation – space crunch as catalyst for sustained rate increase ► Idle capacity/Capacity deployment in main trades – indicator of carrier

discipline ► Port handling volumes – indicator of demand growth

(c) Alphaliner 2011 21

Speaker Bio ► Tan Hua Joo is Executive Consultant with Alphaliner – a leading market

research service provider for the container shipping industry. He has over fifteen years experience in the shipping industry and has held senior positions in leading container shipping, container leasing and shipowning companies.

► Mr. Tan graduated with a BA in Politics, Philosophy and Economics from Oxford University and holds an MBA from Stanford University.

(c) Alphaliner 2011

Tel : (65) 96479147 Email : [email protected]

Website : www.alphaliner.com

22