who wins in offshoring? · pdf filewho wins in offshoring? ... lan-zzy396-20031015-5408-zzy 1...

TRANSCRIPT

LAN-ZZY396-20031015-5408-ZZY

Who Wins in Offshoring?Who Wins in Offshoring?

McKinsey Global InstituteMcKinsey Global InstituteFebruary 4, 2004February 4, 2004

LAN-ZZY396-20031015-5408-ZZY

1

McKinsey Global Institute

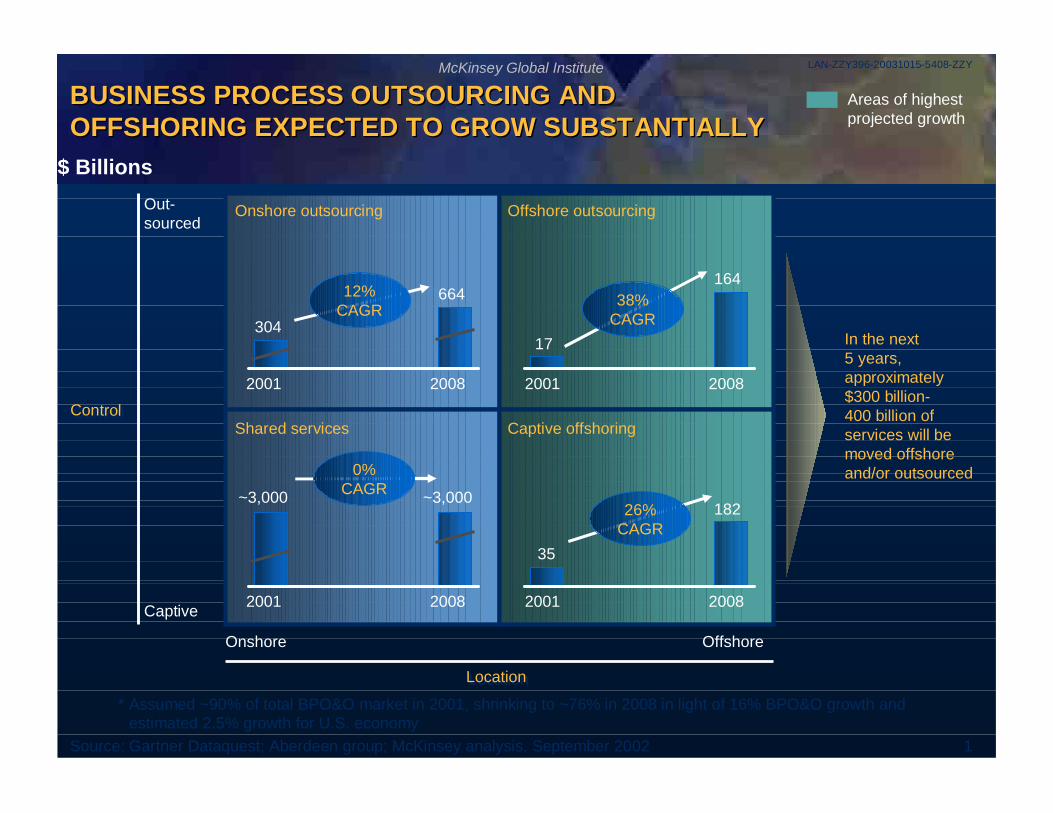

BUSINESS PROCESS OUTSOURCING ANDOFFSHORING EXPECTED TO GROW SUBSTANTIALLYBUSINESS PROCESS OUTSOURCING ANDOFFSHORING EXPECTED TO GROW SUBSTANTIALLY

* Assumed ~90% of total BPO&O market in 2001, shrinking to ~76% in 2008 in light of 16% BPO&O growth andestimated 2.5% growth for U.S. economy

Source: Gartner Dataquest; Aberdeen group; McKinsey analysis, September 2002

ControlControl

In the next5 years,approximately$300 billion-400 billion ofservices will bemoved offshoreand/or outsourced

LocationLocation

Onshore Offshore

Out-sourced

Captive

Onshore outsourcing Offshore outsourcing

Captive offshoringShared services

2001 2008

304

664

2001 2008

17

164

2001 2008

~3,000 ~3,000

2001 2008

35

182

12%CAGR 38%

CAGR

0%CAGR

26%CAGR

Areas of highestprojected growth

$ Billions

LAN-ZZY396-20031015-5408-ZZY

2

McKinsey Global Institute

Australia

0.4

Mexico

0.5

EasternEurope

0.4Russia

0.2

China

1.1

Philippines0.3

0.05Thailand

India

7.7

South Africa0.01

Israel

3.0Ireland

8.3

Canada

3.7

INDIA IS A DOMINANT PLAYER IN OFFSHORINGINDIA IS A DOMINANT PLAYER IN OFFSHORING

Offshored services market size$ Billions, 2001

* Includes Poland, Romania, Hungary, and Czech Republic** Primarily composed of MNC captives

Source: Software Associations; U.S country commercial reports; press articles; McKinsey analysis; Gartner; IDC; Countrygovernment websites; Ministry of Information Technology for various countries; Enterprise Ireland; NASSCOM

LAN-ZZY396-20031015-5408-ZZY

3

McKinsey Global Institute

OFFSHORING OPPORTUNITIES CUT ACROSSTHE ORGANIZATIONOFFSHORING OPPORTUNITIES CUT ACROSSTHE ORGANIZATION

Source: Press releases and news; expert interviews; team analysis

Samplefunctions

Samplecompanies

Increasingly complex transactionsIncreasingly complex transactions• Basic data

entry– Application

forms– Data

conversion• Transaction

processing• Document

management

• Customerrelations– Call centers

(inboundandoutbound)

– On-linecustomerservice

• Telemarketing• Collections

• Sharedcorporateservices– Finance/

accounting– HR– Procurement– IT

• Help desk• Maintenance• Infrastructure• Applications

development

• Researchservices

• Customeranalysis

• Portfolioanalysis

• Claimsprocessing

• Riskmanagement– Credit

underwriting

• Contentdevelopment,engineeringand design

• New productdesign– Design

specs– Pilot/

prototypes– Testing– Production

design andoptimization

Back officeBack office CustomerCustomercontactcontact

CommonCommoncorporatecorporatefunctionsfunctions

KnowledgeKnowledgeservices andservices anddecision analysisdecision analysis

Research andResearch anddevelopmentdevelopment

Access to highlyskilled labor pool

Low-cost labor

LAN-ZZY396-20031015-5408-ZZY

4

McKinsey Global Institute

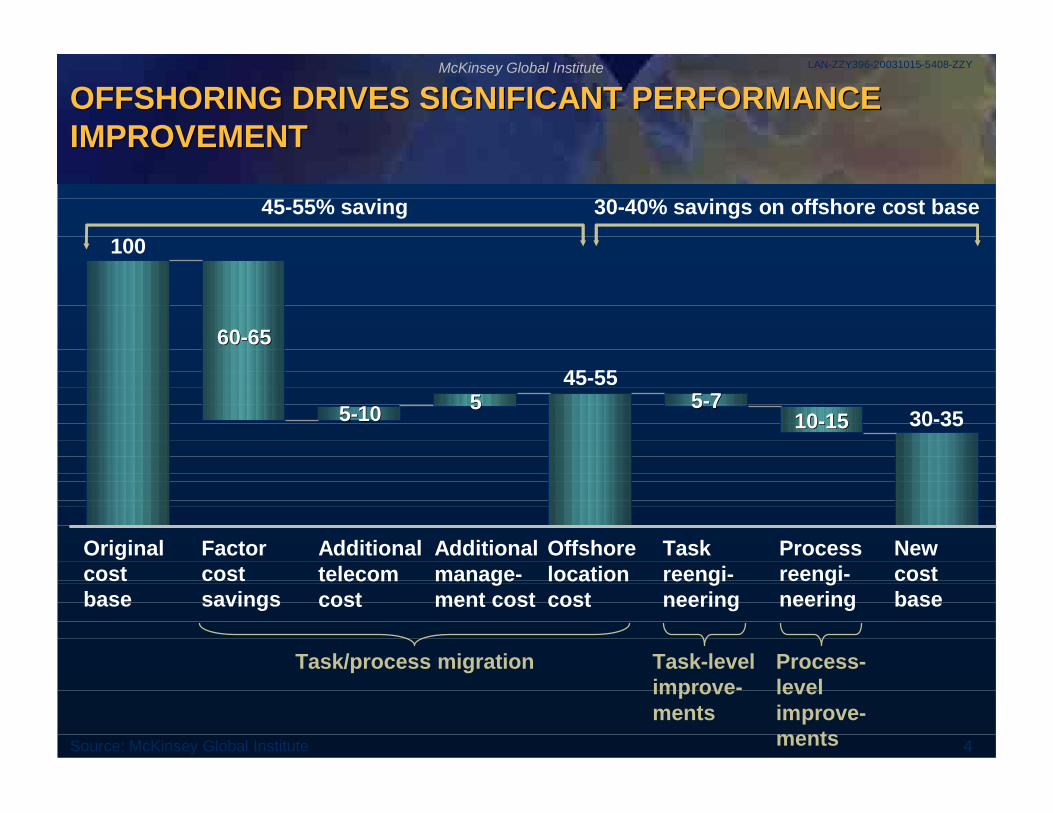

Source: McKinsey Global Institute

OFFSHORING DRIVES SIGNIFICANT PERFORMANCEIMPROVEMENTOFFSHORING DRIVES SIGNIFICANT PERFORMANCEIMPROVEMENT

Originalcostbase

Factorcostsavings

Additionaltelecomcost

Additionalmanage-ment cost

Offshorelocationcost

Taskreengi-neering

Processreengi-neering

Newcostbase

Task/process migration Task-levelimprove-ments

Process-levelimprove-ments

45-55% saving 30-40% savings on offshore cost base

100

6060--6565

55--1010 5545-55

55--771010--1515 30-35

LAN-ZZY396-20031015-5408-ZZY

5

McKinsey Global Institute

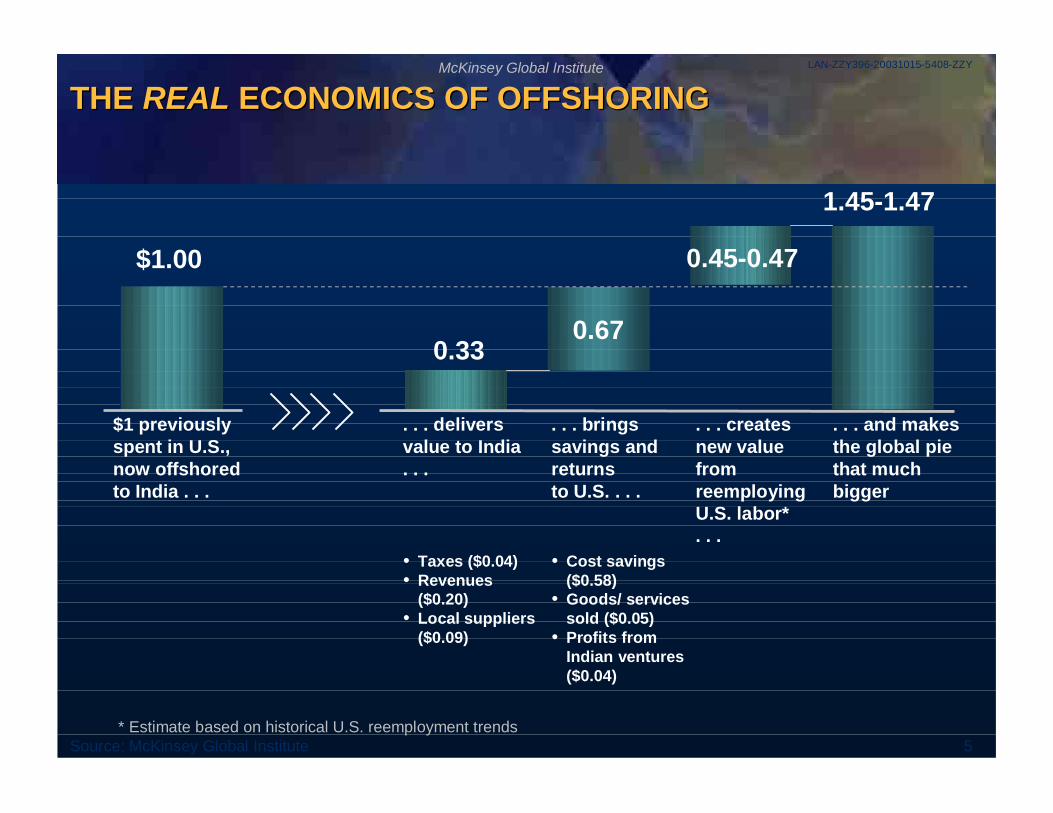

0.33

* Estimate based on historical U.S. reemployment trendsSource: McKinsey Global Institute

THE REAL ECONOMICS OF OFFSHORINGTHE REAL ECONOMICS OF OFFSHORING

• Taxes ($0.04)• Revenues

($0.20)• Local suppliers

($0.09)

. . . deliversvalue to India. . .

0.67

• Cost savings($0.58)

• Goods/ servicessold ($0.05)

• Profits fromIndian ventures($0.04)

. . . bringssavings andreturnsto U.S. . . .

1.45-1.47

. . . and makesthe global piethat muchbigger

0.45-0.47

. . . createsnew valuefromreemployingU.S. labor*. . .

$1 previouslyspent in U.S.,now offshoredto India . . .

$1.00

LAN-ZZY396-20031015-5408-ZZY

6

McKinsey Global Institute

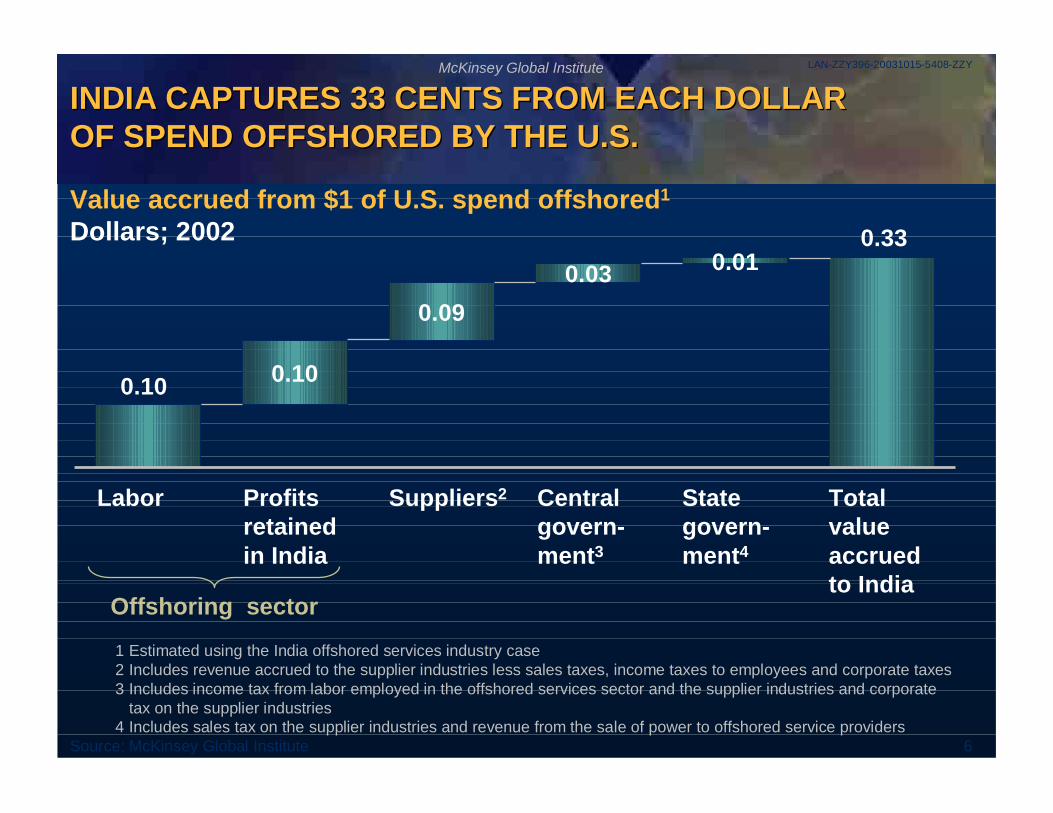

0.030.33

0.10

0.09

0.10

0.01

Profitsretainedin India

INDIA CAPTURES 33 CENTS FROM EACH DOLLAROF SPEND OFFSHORED BY THE U.S.INDIA CAPTURES 33 CENTS FROM EACH DOLLAROF SPEND OFFSHORED BY THE U.S.

Value accrued from $1 of U.S. spend offshored1

Dollars; 2002

Centralgovern-ment3

Stategovern-ment4

Totalvalueaccruedto India

Labor Suppliers2

Offshoring sector

1 Estimated using the India offshored services industry case2 Includes revenue accrued to the supplier industries less sales taxes, income taxes to employees and corporate taxes3 Includes income tax from labor employed in the offshored services sector and the supplier industries and corporate

tax on the supplier industries4 Includes sales tax on the supplier industries and revenue from the sale of power to offshored service providers

Source: McKinsey Global Institute

LAN-ZZY396-20031015-5408-ZZY

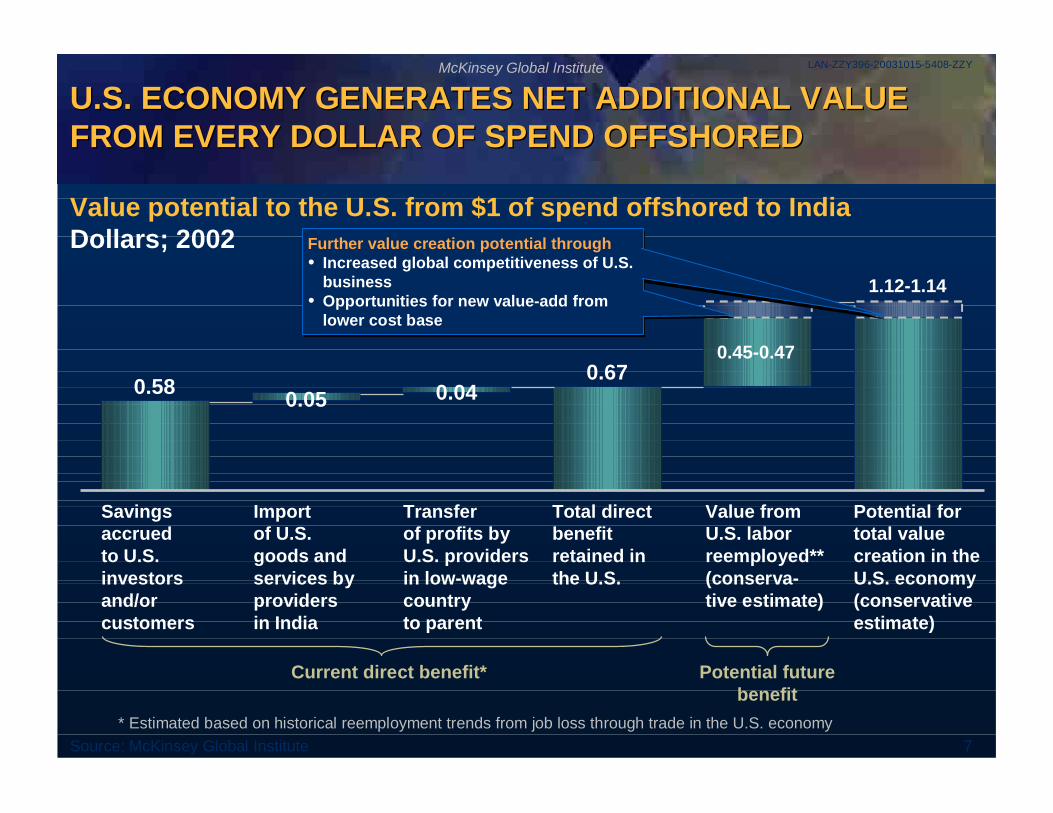

7

McKinsey Global Institute

0.45-0.47

0.05 0.040.58

1.12-1.14

0.67

U.S. ECONOMY GENERATES NET ADDITIONAL VALUEFROM EVERY DOLLAR OF SPEND OFFSHOREDU.S. ECONOMY GENERATES NET ADDITIONAL VALUEFROM EVERY DOLLAR OF SPEND OFFSHORED

Savingsaccruedto U.S.investorsand/orcustomers

Importof U.S.goods andservices byprovidersin India

Transferof profits byU.S. providersin low-wagecountryto parent

Value potential to the U.S. from $1 of spend offshored to IndiaDollars; 2002

Total directbenefitretained inthe U.S.

Value fromU.S. laborreemployed**(conserva-tive estimate)

Potential fortotal valuecreation in theU.S. economy(conservativeestimate)

Current direct benefit* Potential futurebenefit

* Estimated based on historical reemployment trends from job loss through trade in the U.S. economySource: McKinsey Global Institute

Further value creation potential through• Increased global competitiveness of U.S.

business• Opportunities for new value-add from

lower cost base

Further value creation potential through• Increased global competitiveness of U.S.

business• Opportunities for new value-add from

lower cost base

LAN-ZZY396-20031015-5408-ZZY

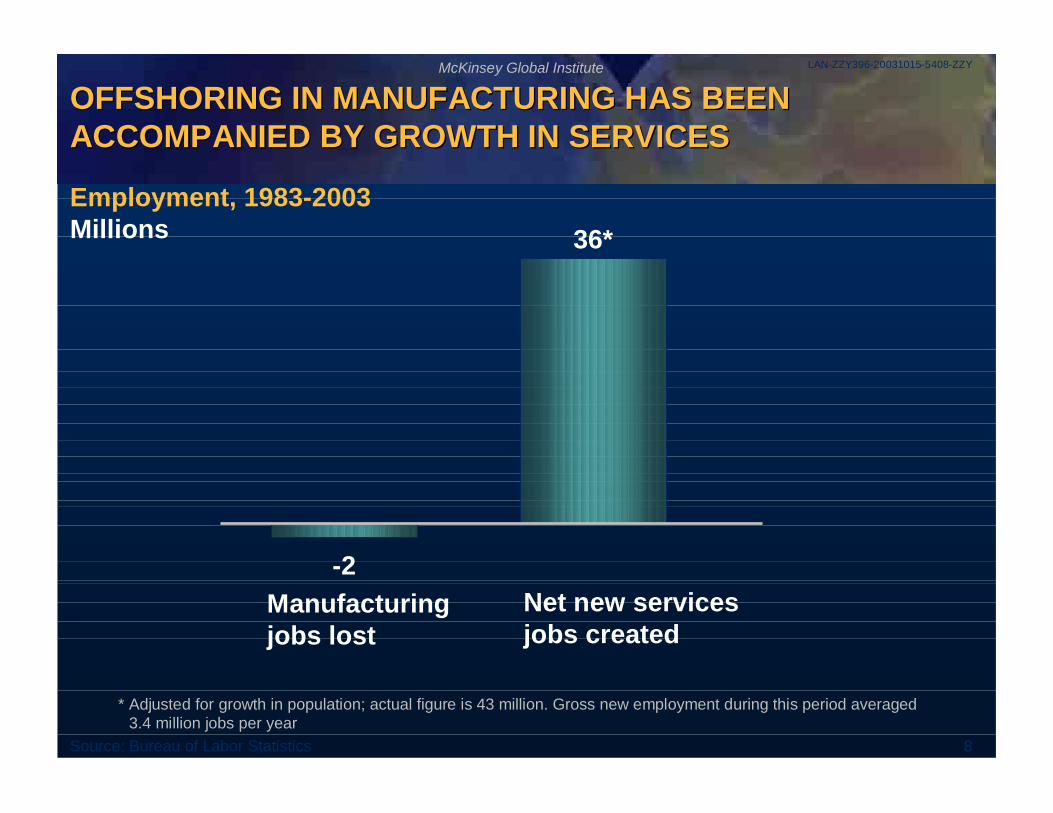

8

McKinsey Global Institute

OFFSHORING IN MANUFACTURING HAS BEENACCOMPANIED BY GROWTH IN SERVICESOFFSHORING IN MANUFACTURING HAS BEENACCOMPANIED BY GROWTH IN SERVICES

* Adjusted for growth in population; actual figure is 43 million. Gross new employment during this period averaged3.4 million jobs per year

Source: Bureau of Labor Statistics

Employment, 1983-2003Millions

-2

36*

Manufacturingjobs lost

Net new servicesjobs created

LAN-ZZY396-20031015-5408-ZZY

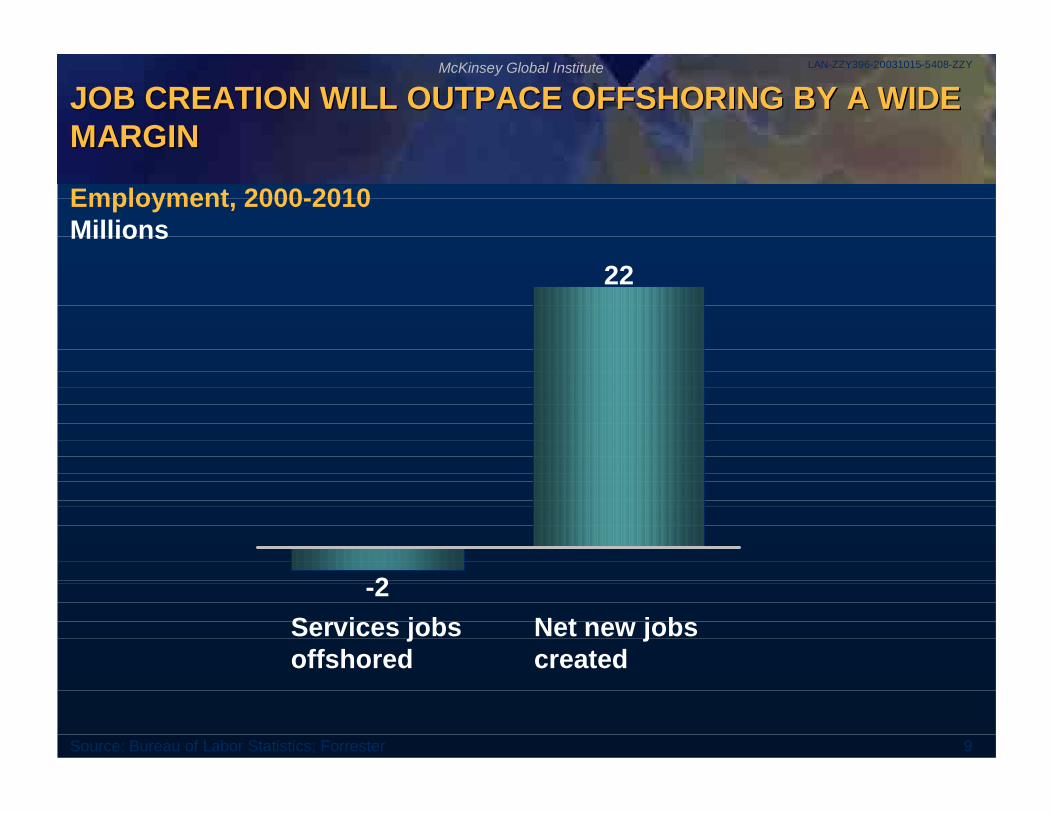

9

McKinsey Global Institute

JOB CREATION WILL OUTPACE OFFSHORING BY A WIDEMARGINJOB CREATION WILL OUTPACE OFFSHORING BY A WIDEMARGIN

Source: Bureau of Labor Statistics; Forrester

22

-2

Employment, 2000-2010Millions

Services jobsoffshored

Net new jobscreated

LAN-ZZY396-20031015-5408-ZZY

10

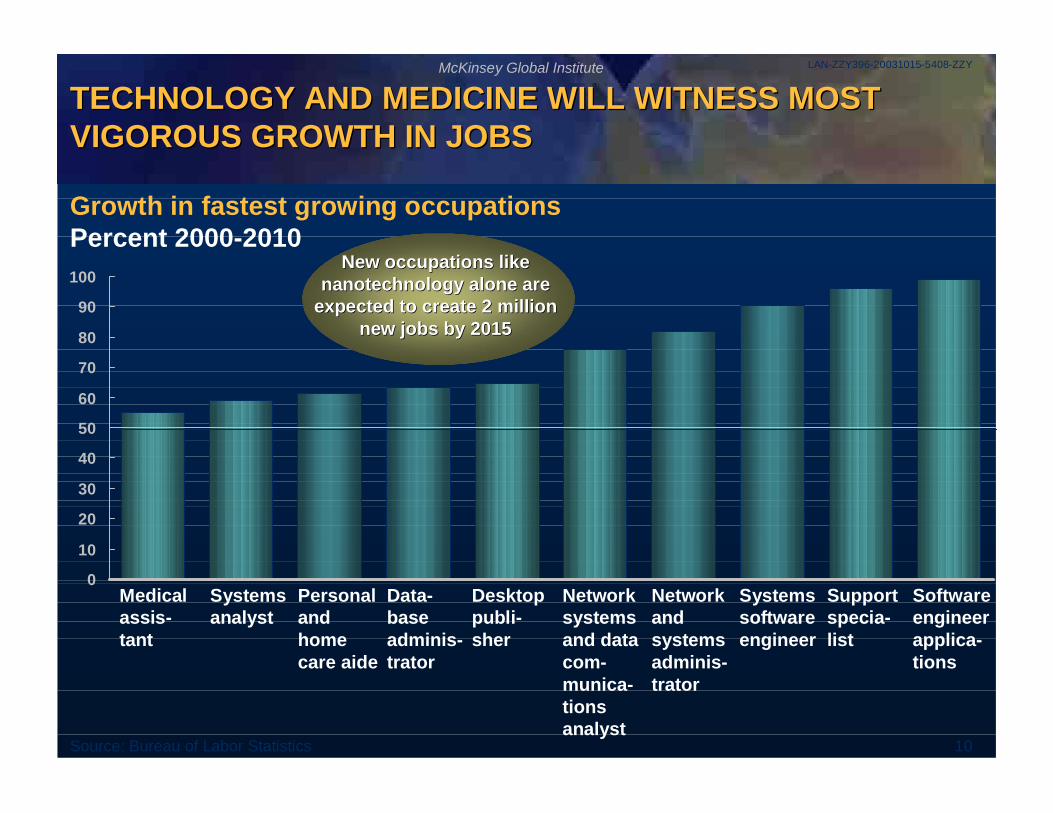

McKinsey Global Institute

0

10

20

30

40

50

60

70

80

90

100

TECHNOLOGY AND MEDICINE WILL WITNESS MOSTVIGOROUS GROWTH IN JOBSTECHNOLOGY AND MEDICINE WILL WITNESS MOSTVIGOROUS GROWTH IN JOBS

Source: Bureau of Labor Statistics

Growth in fastest growing occupationsPercent 2000-2010

New occupations likeNew occupations likenanotechnology alone arenanotechnology alone are

expected to create 2expected to create 2 millionmillionnew jobs by 2015new jobs by 2015

Medicalassis-tant

Systemsanalyst

Personalandhomecare aide

Data-baseadminis-trator

Desktoppubli-sher

Networksystemsand datacom-munica-tionsanalyst

Networkandsystemsadminis-trator

Systemssoftwareengineer

Supportspecia-list

Softwareengineerapplica-tions

LAN-ZZY396-20031015-5408-ZZY

11

McKinsey Global Institute

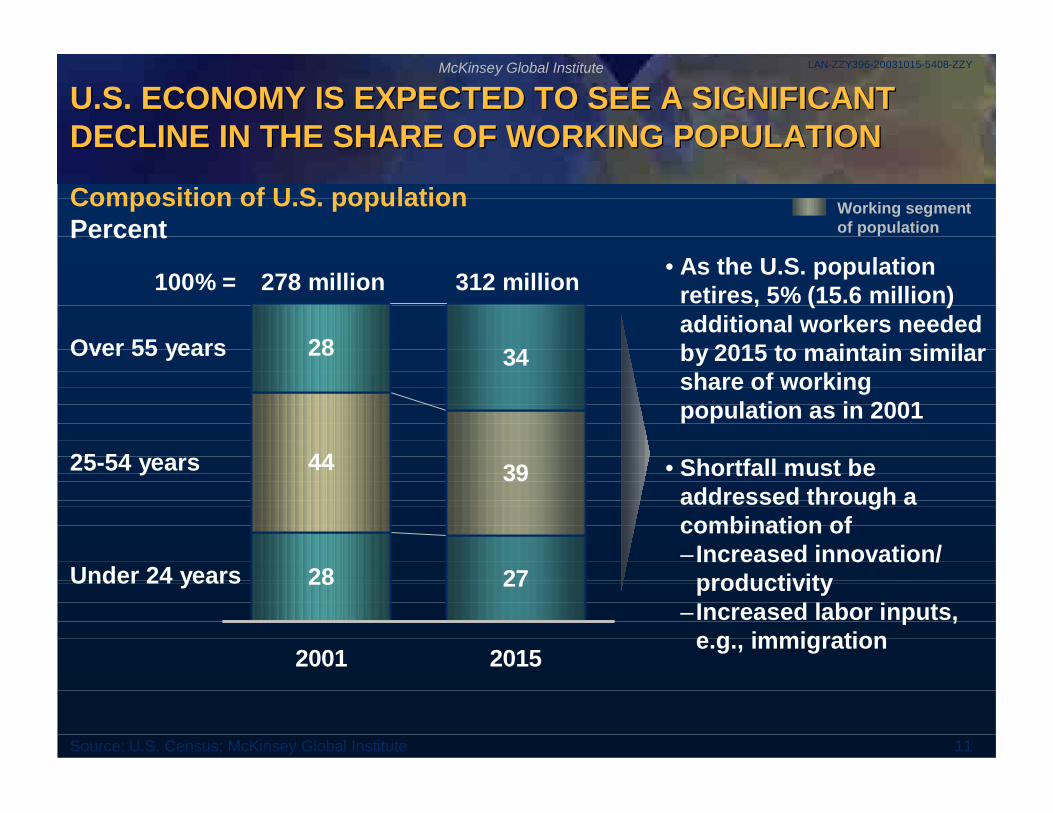

U.S. ECONOMY IS EXPECTED TO SEE A SIGNIFICANTDECLINE IN THE SHARE OF WORKING POPULATIONU.S. ECONOMY IS EXPECTED TO SEE A SIGNIFICANTDECLINE IN THE SHARE OF WORKING POPULATION

Composition of U.S. populationPercent

Source: U.S. Census; McKinsey Global Institute

28 27

44 39

28 34

2001 2015

100% = 278 million 312 million

Over 55 years

25-54 years

Under 24 years

• As the U.S. populationretires, 5% (15.6 million)additional workers neededby 2015 to maintain similarshare of workingpopulation as in 2001

• Shortfall must beaddressed through acombination of– Increased innovation/

productivity– Increased labor inputs,

e.g., immigration

Working segmentof population

LAN-ZZY396-20031015-5408-ZZY

12

McKinsey Global Institute

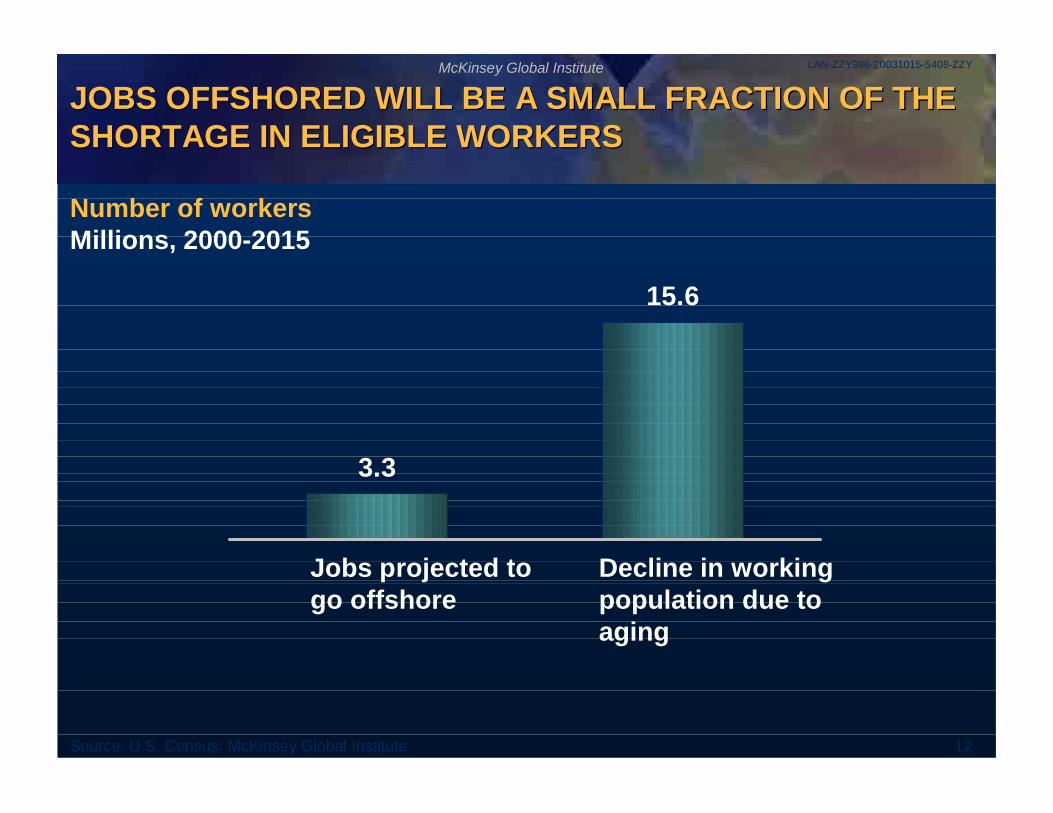

JOBS OFFSHORED WILL BE A SMALL FRACTION OF THESHORTAGE IN ELIGIBLE WORKERSJOBS OFFSHORED WILL BE A SMALL FRACTION OF THESHORTAGE IN ELIGIBLE WORKERS

Number of workersMillions, 2000-2015

Source: U.S. Census; McKinsey Global Institute

3.3

15.6

Jobs projected togo offshore

Decline in workingpopulation due toaging

LAN-ZZY396-20031015-5408-ZZY

13

McKinsey Global Institute

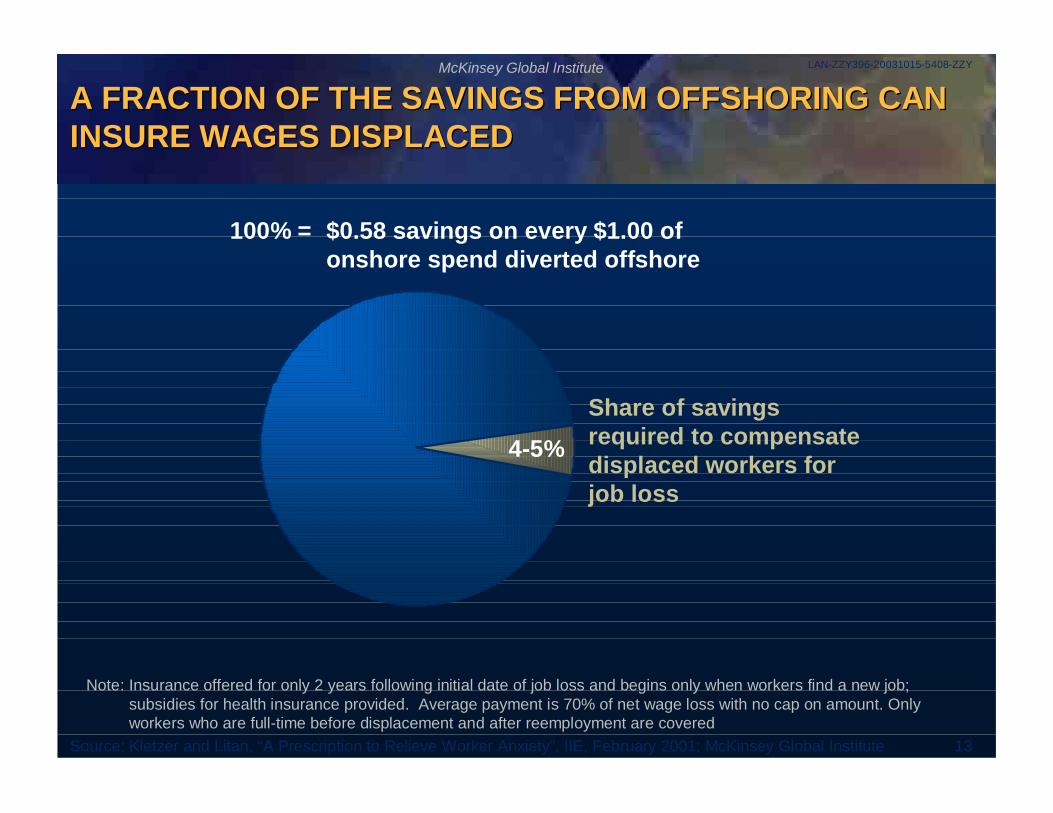

A FRACTION OF THE SAVINGS FROM OFFSHORING CANINSURE WAGES DISPLACEDA FRACTION OF THE SAVINGS FROM OFFSHORING CANINSURE WAGES DISPLACED

100% = $0.58 savings on every $1.00 ofonshore spend diverted offshore

Share of savingsrequired to compensatedisplaced workers forjob loss

4-5%

Note: Insurance offered for only 2 years following initial date of job loss and begins only when workers find a new job;subsidies for health insurance provided. Average payment is 70% of net wage loss with no cap on amount. Onlyworkers who are full-time before displacement and after reemployment are covered

Source: Kletzer and Litan, “A Prescription to Relieve Worker Anxiety”, IIE, February 2001; McKinsey Global Institute

LAN-ZZY396-20031015-5408-ZZY

McKinsey Global InstituteMcKinsey Global Institutewww.www.mckinseymckinsey.com/.com/mgimgi