where is european private equity heading? - 2005 european private equity statistics gemma...

TRANSCRIPT

Where is European Private Equity Heading?Where is European Private Equity Heading?

- 2005 - 2005 European Private Equity StatisticsEuropean Private Equity Statistics

Gemma Postlethwaite, Thomson Financial

16 March 2006

2

Investment Activity Methodology

Data collected from GPs via survey questionnaires, response rate 62.3% for 1,450 PE firms

Europe is defined as location of the PE fund

Fundraising – only formal closings included

Investments – based on completion date, only equity value (debt only if provided by PE fund)

Divestments – at cost, and at time of divestment by PE firm

3

2.4

5.25.7

7.4

9.6

9.26.8 5.4 5.1

17.9

1.8

5.04.9

4.7

10.7

10.2

4.3 4.9 4.5

14.9

3.3

3.4

5.7

4.7

3.6 2.8

7.2

5.0

4.6

3.4 4.2 3.2

3.4

2.2

0

10

20

30

40

50

60

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

€ billionCapital Markets

Academic I nstitutions

Fund of FundsI nsurance Companies

Pension Funds

Banks

Government Agencies

Private I ndividuals

Corporate I nvestorsRealised Capital Gains

Others/Not Available

8.0

20.0 20.3

25.4

48.0

40.0

27.5 27.0 27.5

59.5

A fund raising all-time record at €60bn

Source: EVCA/Thomson Financial/ PricewaterhouseCoopers

Sustainable level?

77% of funds raised in 2005 allocated to buyout, vs. 65% in 2004

Banks are back – why?

Pension funds invest massively –baby boomers with a pension shortfall

US fund raising also a record with $173bn, but second to 2000

European Private Equity Funds Raised

4

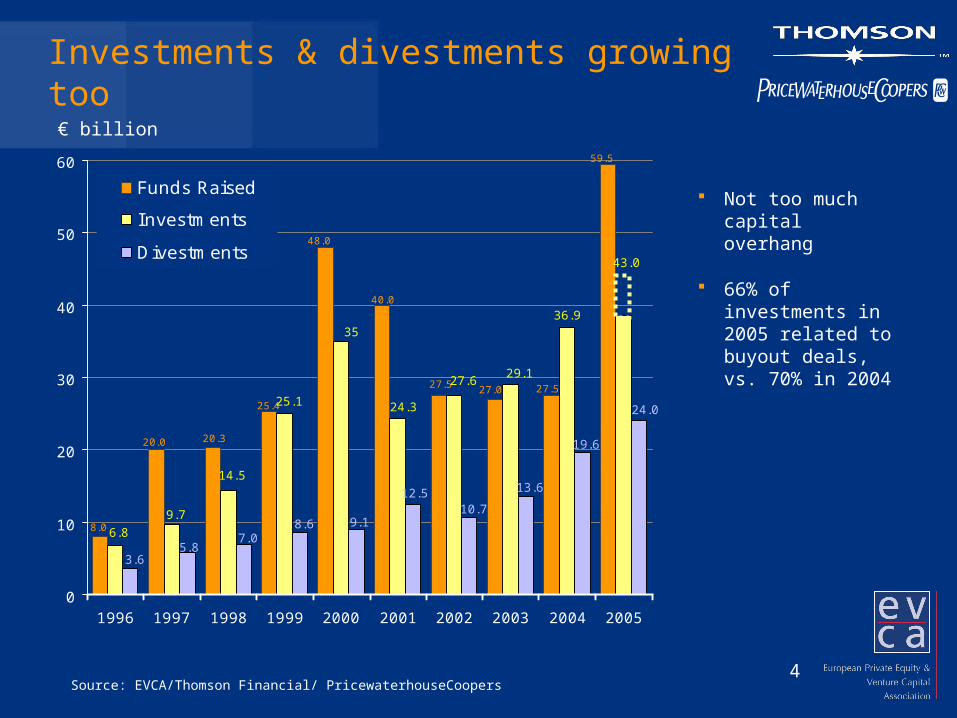

Investments & divestments growing too

€ billion

Source: EVCA/Thomson Financial/ PricewaterhouseCoopers

59.5

8.0

48.0

27.0 27.5

20.0 20.3

25.4

27.5

40.0

36.9

6.8

14.5

9.7

25.1

35

24.3

27.629.1

43.0

13.6

19.6

10.712.5

9.18.6

24.0

7.0

3.65.8

0

10

20

30

40

50

60

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Funds Raised

Investments

Divestments

Not too much capital overhang

66% of investments in 2005 related to buyout deals, vs. 70% in 2004

5

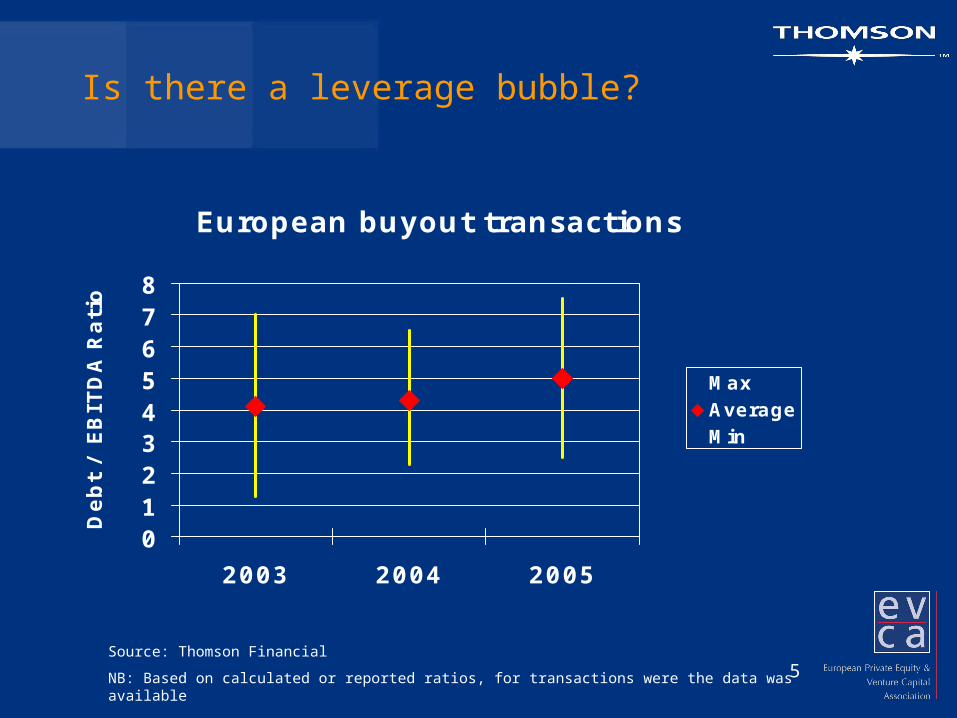

Is there a leverage bubble?

European buyout transactions

012345678

2003 2004 2005

Deb

t /

EB

ITD

A R

ati

o

MaxAverageMin

Source: Thomson Financial

NB: Based on calculated or reported ratios, for transactions were the data was available

6

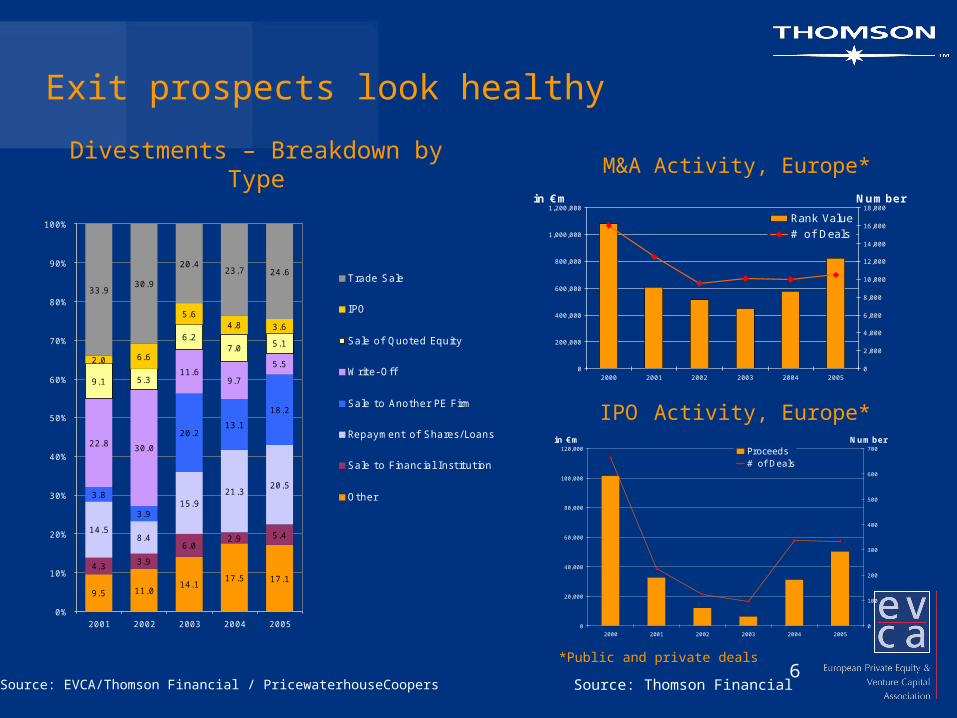

Exit prospects look healthy

9.5 11.014.1

17.5 17.14.3 3.9

6.02.9 5.4

14.58.4

15.921.3

20.53.8

3.9

20.213.1

18.2

22.8 30.0

11.69.7

5.5

9.1 5.3

6.27.0

2.0 6.6

5.64.8 3.6

33.930.9

20.423.7 24.6

5.1

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2001 2002 2003 2004 2005

Trade Sale

IPO

Sale of Quoted Equity

Write- Off

Sale to Another PE Firm

Repayment of Shares/ Loans

Sale to Financial Institution

Other

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

2000 2001 2002 2003 2004 2005

in €m

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000Number

Rank Value# of Deals

Source: EVCA/Thomson Financial / PricewaterhouseCoopers

Divestments – Breakdown by Type

0

20,000

40,000

60,000

80,000

100,000

120,000

2000 2001 2002 2003 2004 2005

in €m

0

100

200

300

400

500

600

700

Number

Proceeds# of Deals

M&A Activity, Europe*

IPO Activity, Europe*

Source: Thomson Financial

*Public and private deals

7

Performance Methodology

Data collected from GPs and LPs historically for 1000+ European funds

Returns calculated at fund level, and net of management fees and carried interest

All calculations done by Thomson based on actual cash flows

Pooled IRR: IRR of a group of funds where cash flows have been aggregated together before IRR calculation

Investment horizon return: IRR calculated with Net Asset Value as capital outflow at beginning of period, Net Asset Value at end of period, and actual cash flow in between

DPI: Distribution (in cash or stock) divided by Paid-In capital (‘realised’ ratio)

RVPI: Residual Value divided by Paid-In capital (‘unrealised’ ratio)

TVPI: Total Value divided by Paid-In, sum of DPI and RVPI

8

Investment Benchmarks European Sample

Report Year No. Funds Committed €Bn.

1996 278 20.6

1997 384 39.8 1998 438 51.4 1999 511 68.8 2000 573 87.6 2001 665 108.8 2002 774 135.4 2003 881 158.7 2004 949 159.4 2005 1007 192.4

9

European Private Equity Funds Formed 1980-2005Net IRRs to Investors, Investment Horizon Return as of 31-Dec-2005

Stage 1 YR 3 YR 5 YR 10 YR 20 YR

All Venture 25.4 0.6 -4.0 5.3 5.7

Buyouts 20.9 7.9 5.0 12.6 12.4

Generalist 51.2 1.2 -4.8 9.7 8.6

All Private Equity 24.1 5.2 1.2 10.2 9.6

Source: Thomson Financial / EVCA

Short term indicators show good performance

10

3-year venture IRR moves into positive territory

-10

0

10

20

30

40

Rolli

ng I

RR

s (%

)

10-year IRR5-year IRR3-year IRR

+0.6%

+5.3%

Source: Thomson Financial / EVCA

European Venture 3-,5-,10-Year Rolling IRRs

-4.0%

11

All horizon IRRs in positive territory for buyouts and climbing

-10

0

10

20

30

40

Rolli

ng I

RR

s (%

)

10-year IRR5-year IRR3-year IRR

+7.9%

+12.6%

Source: Thomson Financial / EVCA

European Buyouts3-,5-,10-Year Rolling IRRs

+5.0%

12

Top quarter funds return 23%

Stage PooledIRR

Minimum value Top Quarter

Pooled IRRTop

Quarter

All Venture 5.6 6.1 23.9

Buyouts 12.4 17.1 35.3

Generalist 8.6 8.1 12.4

All Private Equity 9.6 10.4 23.0

Source: Thomson Financial / EVCA

European Private Equity Funds Formed 1980-2005

0

25

50

75

100

2005

+23.0%

+9.5%

3rd quarter

4th quarter

10.4%

Quarter IRR

Top QuartileI RR

Ranking

13

Where is performance coming from?

Stage DPI RVPI TVPI

All Venture 0.60 0.61 1.21

Buyouts 0.80 0.60 1.40

Generalist 0.97 0.40 1.37

All Private Equity 0.78 0.57 1.35

Source: Thomson Financial / EVCA

European Private Equity Funds Formed 1980-2005

14

Conclusion: Record Activity

Fundraising record at €59.5bn Pension funds and banks - main investors with 57.5%

2005 investments steady at €38.5bn, expected to go above €43bn on final data set Buyouts represent 65.8% by amount invested

Venture represent 72.6% by number of investments

Divestments up 23% at €24.0 billion Trade sale continues to be the most popular exit route with 24.6% of the

total amount divested

Write-offs reduced to 5.5% of total amount divested

15

Conclusion: Improved Performance

Long-term performance Stays constant at around 10% net IRR

Robust returns for top quarter funds: 35.3% for buyout and 23.9% for venture funds.

Shorter-term performance Overall 3-year rolling IRR moves up to 5.2% IRR with both buyout and venture

returns in positive territory

1-year rolling IRR is an impressive 20.9% for buyout and 25.4% for venture funds

16

Contact the Thomson Research Specialists:

Performance: Cornelia Andersson [email protected] +44 20 7014 1202

Investment activity: Margherita Del Bianco [email protected] +44 20 7566 1934

How to contribute data?