weekly credit update - danske...

TRANSCRIPT

Weekly Credit Update

20 September 2016

Important disclosures and certifications are contained from page 36 of this report

Investment Researchwww.danskebank.com/CI

This document is intended for institutional investors and is not subject to all the independence and disclosure standards applicable to debt research reports prepared for retail investors.

Analysts

Brian Børsting+45 45 12 85 [email protected]

Katrine Jensen+45 45 12 80 [email protected]

22

- General credit market news and current themes

- Credit indicators

- Scandi investment grade

Contents

- Coverage universe, credit ratings and recommendations

- Scandi high yield/unrated

33Source: Bloomberg, Danske Bank Markets (both charts)

What’s on our minds

General credit market news

• The European credit indices widened slightly during last week as iTraxx Main ended at index 71 – up from 68 last week - and iTraxx Crossover widened some 15bp to 330 on the back of increased volatility in the equity market.

• The main event this week will be the September FOMC meeting. Danske Bank’s view is that the Fed will not raise the federal funds target range this year, in light of sluggish growth and continued labour market slack. For further information on our view please see 10 reasons why we believe the Fed will not hike this year, 14 September.

• New data from BIS shows that more than 90% of the new issuance in Q2 16 from euro-area based non-financial companies was EUR-denominated. At the beginning of 2016 the number was close to 50%! The impact of ECB’s decision to purchase EUR investment grade non-financial corporate bonds is clearly visible in the new issue market.

• The direct impact on business activity following the British EU referendum has been fairly limited up until now. However, this week UK facility management company Mitie issued a significant profit warning that made its stock price decline some 25%. We cover some peer group companies like ISS (OW), G4S (MW) and Securitas (MW). We believe the Mitie profit warning is mainly related to Mitie’s operations that have significant exposure to the UK public sector. However, we will monitor a potential worsening of general market conditions in the UK closely.

44

Weekly purchase volumes Purchased issues, split by country of risk

Source: ECB, Danske Bank Markets Source: ECB, Danske Bank Markets

CSPP UpdatePurchases of EUR2.7bn in the week ending 16 September

Buy NOKIA 2019 USD, trading at wide margin to Nokia 2019 EUR

Published on 23 May 2016

• The weekly purchase volume continued to climb last week to a monthly run-rate of a substantial EUR11.7bn. This is the highest week so far. In total the ECB has now purchased bonds under the CSPP totalling EUR25.6bn.

• In relation to total purchased volume, the average holding of each ISIN (dividing the total purchased amount by the number of ISINs held) has continued to rise to EUR42bn per ISIN.

• See table on the right for newly purchased issues. Interestingly, a number of the new issues were new issues in the market, indicating a number of primary participations by the ECB.

• In terms of the split of purchases so far, bonds from German issuers represent a much larger share of purchased issues than the ECB’s benchmark would imply, based on outstanding market volumes. Over time, the purchases should reflect the market benchmark.

AT BE

DE

EE

ES

FIFR

IE

IT

LU

NL

PTSISKGBUSCH

Bond

Remaining

tenor

Z-

spread

Δ since

announcement*

GLENLN 1 7/8 09/13/23 7,0 216,39 New issue

ELIASO 3 04/07/29 12,6 41,83 -44,48

HENKEL 0 09/13/18 2,0 12,13 New issue

HENKEL 0 09/13/21 5,0 14,48 New issue

DT 2 10/30/19 3,1 14,12 -6,86

ANNGR 0 7/8 06/10/22 5,7 52,03 n/a

EVKGR 0 3/8 09/07/24 8,0 40,64 n/a

EVKGR 0 3/4 09/07/28 12,0 49,60 n/a

EVKGR 0 03/08/21 4,5 23,90 n/a

SANFP 2 1/2 11/14/23 7,2 15,31 -25,72

VIEFP 1.59 01/10/28 11,3 33,68 -58,58

ADPFP 1 1/2 07/24/23 6,8 15,89 -34,83

SANFP 0 01/13/20 3,3 16,76 New issue

SANFP 0 09/13/22 6,0 16,39 New issue

SANFP 0 1/2 01/13/27 10,3 30,92 New issue

PRE 1 1/4 09/15/26 10,0 95,39 New issue

Purchased issues last week

0

5

10

15

20

25

30

35

40

45

0

500

1000

1500

2000

2500

3000

17/06/2016 17/07/2016 17/08/2016

Weekly purchase volume Volume held per ISIN

* Spread change since announcement of CSPP in March

Source: ECB, Bloomberg, Danske Bank Markets

5

Scandi HY/unrated

66

Chart 1. Relative value, indicative mid spreads Chart 2. Twelve month credit spread development vs BBB index

Source: Bloomberg, Danske Bank Markets Source: Bloomberg, Danske Bank Markets

Low credit risk – Buy Akelius 2020s in EURAttractive pricing considering our expectation of a bond upgrade (published 15 September)

Buy NOKIA 2019 USD, trading at wide margin to Nokia 2019 EUR

Published on 23 May 2016

Key arguments for the trade

• In coming quarters, we expect Akelius’s interest costs to continue to fall, as the company refinances maturing debt with new cheaper financing. This, together with a forthcoming asset sale, suggests potential for some further improvement in credit metrics (end Q2 reported LTV: 47%; with S&P’s adjustments 53%).

• We also expect Akelius’s secured LTV to decline gradually towards its 25% target for 2018 (end-Q2 33%). In our view, this means that at some stage S&P should remove its notching from Akelius’s bonds.

• Considering the high likelihood of a ratings upgrade, we consider Akelius 3.375% 2020s (currently rated BB+) in EUR to offer an attractive pick-up relative to other European real estate names.

• Akelius has a strategy to focus on growth through investing in low-risk residential properties that generate stable cash flow over time. The company invests most of the free cash flow that it generates in renovating and refurbishing the existing properties or reinvests it in new properties.

• Looking at historical property prices, it appears residential property prices normally decline much less than commercial property prices during an economic downturn. At end June, Akelius’s unencumbered assets to outstanding bonds and CPs was a high 5.0x.

• See Property Sector Update: Sweden and Finland: focus on residentials,12 September

• See Trade idea - Buy Akelius 2020s in EUR - Buy Victoria Park 2020s in SEK , 15 September

0

20

40

60

80

100

120

140

160

0

50

100

150

200

250

300

350

XS1295537077[ASW 3M]

IBOXX EURO NON FINANCIALS BBB 3 5[ASSETSWAPSPREAD] RHS

SDAVFH (NR/NR) 3,375% '18

SDAVFH (NR/NR) 2,375% '20

SATOYH (NR/NR) 3,375% '19

SATOYH (Baa3/NR) 2,375% '21SATOYH (Baa3/NR)

2,25% '20

COFBBB (NR/NR) 1,929% '22

CITCON (Baa1/BBB) 3,75% '20

CITCON (Baa1/BBB) 2,5% '24

CITCON (Baa1/BBB) 2,375% '22

CITCON (Baa1/BBB) 1,25% '26

ATRSAV (NR/BBB-) 4% '20

ATRSAV (NR/BBB-) 3,625% '22

AKFAST (NR/BB+) 3,375% '20

0

50

100

150

200

250

1 2 3 4 5 6 7 8 9 10 11 12

Ask Spread (EUR)*

YTW**

* Z-spreads. Discount margin for floaters. Swapped to indicated currency. ** Years-to-worst

77

Chart 1. Relative value, indicative mid spreads Chart 2. Last two months trading in VICPAS ‘18 and ‘20 (price)

Source: Bloomberg, Danske Bank Markets Source: Bloomberg, Danske Bank Markets

Medium credit risk – Buy Victoria Park 2020s in SEKBuilding scale through organic growth and acquisitions (published 15 September)

Buy NOKIA 2019 USD, trading at wide margin to Nokia 2019 EUR

Published on 23 May 2016

Key arguments for the trade

• We regard the outlook for the residential property market in Sweden as positive, considering the recent population growth, a large shortage of apartments and a strong urbanisation trend. Swedish residential companies on average have a lower leverage than peers in the commercial property segment.

• Considering Victoria Park’s focus on the more stable residential market and its long average debt maturity profile, we consider its bonds to be attractively priced compared with sector peers such as D. Carnegie, Heimstaden and Hemfosa.

• As of end-June, Victoria Park reported a gross LTV (excluding preference shares in debt) of 64% (net LTV 52%). Following recent transactions we estimate a gross LTV of around 65%.

• Victoria Park is a Swedish real estate company, which specialises in acquiring, developing and managing housing properties in growth areas in Sweden. At the end of June 2016, the market value of Victoria Park’s property portfolio amounted to SEK8.5bn.

• In mid-July, Victoria Park announced its largest acquisition to date, totalling 1,900 apartments in Malmö and Karlskrona for a total price of SEK1.8bn. Earlier this week the company made an equity issue, raising SEK344m in new equity, which to us demonstrates its commitment to its stipulated financial policy (Max LTV: 65%).

• See Property Sector Update: Sweden and Finland: focus on residentials, 12 September

• See Trade idea - Buy Akelius 2020s in EUR - Buy Victoria Park 2020s in SEK , 15 September

VICPAS FRN '20 (SEK)

VICPAS FRN '18 (SEK)

SAGAX FRN '21 (SEK)

SAGAX FRN '21 (EUR)

SAGAX FRN '20 (SEK)

SAGAX FRN '20 (EUR)

SAGAX FRN '19 (SEK)

SAGAX FRN '19 (EUR)

SAGAX FRN '18 (SEK)

KLOVSS FRN '20 (SEK)

KLOVSS FRN '19 (SEK)

KLOVSS FRN '18 (SEK)KLOVSS FRN '18

(SEK)

HEIMST FRN '19 (SEK)

FPARSS FRN '20 (SEK)FPARSS FRN '19

(SEK)

FPARSS FRN '19 (SEK)

FPARSS FRN '18 (SEK)

FPARSS FRN '16 (SEK)

CORESS FRN '19 (SEK)CORESS FRN '19

(SEK)

CORESS FRN '18 (SEK)

CORESS FRN '17 (SEK)

0

50

100

150

200

250

300

350

400

450

500

0 1 2 3 4 5 6

Mid Spread (SEK)*

YTW**

* Asset swap spread Swapped to indicated currency. ** Years-to-worst

102.5

103

103.5

104

104.5

105

99.8

100

100.2

100.4

100.6

100.8

101

101.2

9009255335 FRN 17JUN2020 9009255335 FRN 03DEC2018

88

Recent trade ideas (high yield and unrated)

Source: Danske Bank Markets

See the end of this document for a list of our coverage including recommendations.

Type Trade Idea

Opened 15 Sep 2016

Opened 15 Sep 2016

Opened 08 Sep 2016

Opened 17 Aug 2016

Opened 23 May 2016

Opened 23 May 2016

Opened 02 May 2016

Opened 29 Mar 2016

Switch Switch to Volvo hybrids (call 20s

or 23s) from the EUR Volvo

senior curve

VLVY EUR senior curve prices in an upgrade, the hybrids do not.

Buy Victoria Park 2020s in SEK Building scale through organic growth and acquisitions

Switch Buy Kemira 2022s, fund by

selling Kemira 2019s

The spread differential between the Kemira 2019s and 2022s has widened significantly since the end of 2015. A flattening of the Kemira curve indicates potential for at least 20bp tightening, in our view.

Outright Buy Akelius 2020s in EUR Attractive pricing considering our expectation of a bond upgrade

Outright

Outright Buy Nokia USD 5.375% 2019 The USD denominated NOKIA 2019’s trade with a good pickup relative to both the EUR denominated NOKIA 2019’s as well as the ‘BBB-’ industrials curve

Outright Buy DSV DKK 2020 and 2022s The 2022s and the 2020 bonds are trading with 120bp and 108bp spreads to the ‘BBB’ industrial curve, respectively. Even taking into account the unrated status of the bonds and a relatively low liquidity, we believe this is very attractive.

Switch Buy Nokia USD 5.375% 2019

outright and fund by selling Nokia

EUR 6.75% 2019

The USD denominated NOKIA 2019’s trade with a good pickup relative to both the EUR denominated NOKIA 2019’s as well as the ‘BBB-’ industrials curve

Outright Buy Kemira 2019s and 2022s

(EUR)

The Kemira 2019s and 2022s trade with a wide differential to rated peers. Despite Kemira’s unrated status, we believe this differential is too large.

99

Best and worst performers (Nordic coverage universe)High yield/unrated

Source: Bloomberg, Danske Bank Markets (both charts)

1 month in local currencies YTD in local currencies

22,531

16,847

9,032

4,986

3,448

3,425

3,341

2,915

2,777

2,686

-165

-167

-172

-181

-192

-201

-205

-235

-258

-333

-50000500010000150002000025000

Prosafe SE NOK 2017

Farstad Shipping ASA NOK 2017

Olympic Ship AS NOK 2017

Seadrill Ltd NOK 2018

Fred Olsen Energy ASA NOK 2019

Farstad Shipping ASA NOK 2018

North Atlantic Drilling Ltd NOK 2018

Olympic Ship AS NOK 2019

Prosafe SE NOK 2018

Seadrill Ltd SEK 2019

Meda AB SEK 2018

Meda AB SEK 2019

SSAB AB SEK 2019

Odfjell SE NOK 2018

Hoegh LNG Holdings Ltd NOK 2017

Hoist Kredit AB EUR 2017

SSAB AB EUR 2019

Outokumpu OYJ EUR 2019

Teekay Offshore Partners LP/Teekay…

Odfjell SE NOK 2017

Change in local currencies (bp)

4,325

3,009

2,514

1,039

796

579

479

464

193

100

-85

-88

-88

-91

-94

-162

-188

-210

-292

-387

-1000010002000300040005000

Farstad Shipping ASA NOK 2017

Fred Olsen Energy ASA NOK 2019

Olympic Ship AS NOK 2017

Seadrill Ltd USD 2017

North Atlantic Drilling Ltd NOK 2018

Olympic Ship AS NOK 2019

Farstad Shipping ASA NOK 2018

Seadrill Ltd NOK 2018

Seadrill Ltd SEK 2019

Teekay Offshore Partners LP NOK 2019

Odfjell SE NOK 2018

Golar LNG Partners LP NOK 2017

Ocean Yield ASA NOK 2019

Hoegh LNG Holdings Ltd NOK 2017

Ship Finance International Ltd NOK 2019

Golar LNG Partners LP USD 2020

BW Offshore Ltd NOK 2020

BW Offshore Ltd NOK 2022

BW Offshore Ltd NOK 2021

BW Offshore Ltd NOK 2020

Change in local currencies (bp)

1010

Recent Nordic high yield/unrated issuance*

*Excluding increases in existing bond issues (taps)

Source: Bloomberg, Danske Bank Markets

Selected new issues (High yield/unrated)

Date Issuer Coupon CCY Volume Maturity S&P / Mdy / Fitch ASW/DM

16/09/2016 Vastra Malardalen STIB3M +110bps SEK 325 m Sep/20 / / 110

16/09/2016 Entra Asa NIBOR3M +94bps NOK 1 000 m Sep/23 / / 94

14/09/2016 Steen & Strom Asa NIBOR3M +110bps NOK 400 m Mar/23 / / 110

14/09/2016 Sunnhordland Kraftlag As NIBOR3M +114bps NOK 300 m Sep/21 / / 114

13/09/2016 Fastator Ab STIB3M +850bps SEK 250 m Sep/19 / / 850

12/09/2016 Ocean Yield Asa NIBOR3M +450bps NOK 750 m Sep/21 / / 450

09/09/2016 Orkla Asa NIBOR3M +85bps NOK 400 m Mar/23 / / 85

09/09/2016 Orkla Asa 2.35% NOK 200 m Sep/26 / / est. 81

08/09/2016 Atrium Ljungberg Ab STIB3M +88bps SEK 400 m Sep/18 / / 88

08/09/2016 Lillestrom Sparebank NIBOR3M +81bps NOK 200 m Nov/19 / / 81

08/09/2016 Tele2 Ab STIB3M +155bps SEK 1 000 m Mar/22 / / 155

08/09/2016 Odfjell Se NIBOR3M +600bps NOK 500 m Sep/19 / / 600

07/09/2016 Jyske Bank A/S (AT1) STIB3M +580bps SEK 1 250 m PERP / / 580

07/09/2016 Jyske Bank A/S (AT1) CIBO03M +530bps DKK 500 m PERP / / 530

07/09/2016 Bank Norwegian As (AT1) NIBOR3M +525bps NOK 210 m PERP / / 525

07/09/2016 Swedavia Ab 0.435% SEK 250 m Sep/20 / / est. 56

06/09/2016 Totens Sparebank NIBOR3M +87bps NOK 200 m Sep/21 / / 87

06/09/2016 Sparebanken Telemark NIBOR3M +85bps NOK 200 m Sep/21 / / 85

01/09/2016 Jaren Sparebank NIBOR3M +102bps NOK 250 m Sep/21 / / 102

01/09/2016 Tronderenergi As 2.68% NOK 200 m Sep/26 / / est. 128

30/08/2016 Fastpartner Ab STIB3M +450bps SEK 600 m Sep/20 / / 450

30/08/2016 Modum Sparebank NIBOR3M +79bps NOK 200 m Mar/20 / / 79

24/08/2016 Resurs Bank STIB3M +175bps SEK 400 m Aug/19 / / 175

24/08/2016 Nya Svensk Fastighets Fi STIB3M +85bps SEK 460 m Sep/18 / / 85

23/08/2016 Sparebank 1 Bv NIBOR3M +85bps NOK 225 m Aug/21 / / 85

1111

Company news from the past week (high yield/unrated)

Source: Danske Bank Markets

Name News Implication

St1 Nordic

St1 Nordic saw a decent first half of 2016. The acquisition of Smart Fuel in Norway caused both reported revenues and earnings to rise significantly y/y. Importantly, margins improved, which is a key variable in monitoring St1 Nordic’s retail-like business. Net debt increased following the acquisition of Smart Fuel and high capex in the TuuliWatti joint venture. Metrics are still at decent levels, though. We see the illiquid STNORD trading at very generous levels compared with the ‘BB’ curve despite its illiquidity. Subsequently, we assign an Overweight recommendation to St1 Nordic’s bonds.

Credit neutral

Hoist Finance

Hoist Finance (Ba1 bond rating) hosted its first CMD where previous guidance of c. EUR3.6bn in annual portfolio purchases for 16-18 was confirmed. Market to continue growing in coming years by 7%/year to 2020. SME and secured to grow as % of Hoist's business. CEO as usual reinforcing the importance of its status as a regulated entity (bank) when it approaches portfolio sellers (international banks). Interestingly, in the recent Bank of Greece deal, where Hoist is appointed one of few partners to manage the Greek bad bank (all asset classes) for the liquidated banks, the ECB told the BoG to involve an international collection partner and Hoist was the one chosen. No changes to guidance overall. We like Hoist and its strategy of cautious growth but so does the market - EUR '19 bond trading at fair value.

Credit neutral

Kemira

Kemira held its capital markets day in London. In connection with this the group updated its EBITDA margin target to 14%-16% versus 15% previously. The integration of AkzoNobel paper chemicals is progressing better than expected and synergies have been raised from EUR15m to EUR20m. Furthermore, Kemira has launched a new efficiency programme aiming to cut cost by EUR20-30m in 2-3 years. Company stated that it is comfortable with a leverage of 2.5x (we have Kemira at 2.2x reported currently), i.e. Kemira leaves some scope to raise leverage in case a smaller M&A opportunity comes up. The news presented in connection with the CMD is unlikely to move spreads significantly, in our view.

Credit neutral

Neste

Neste (MW) announced that it will revise its dividend policy slightly. The payout ratio should now be at least 40% of comparable net profit versus at least 33% before. This reflects Neste's strong performance in recent sessions and its strong FoCF. Slightly credit negative that shareholder focus continues to be on the rise but this is mitigated by Neste having credit metrics that are in the strong end of its target range.

Credit negative

Nordax Bank

Nordax Bank's main shareholder, Vision Capital Partners, said on Wednesday that it had sold 15,000,000 shares in Nordax Group taking its holding down to 25,058,347 shares corresponding to 22.6% of the total number of shares and votes. This was an expected move by Vision Capital as it normally has an investment horizon of three to six years albeit the fund behind the investment in Nordax has an investment horizon stretching beyond 2018/21 (extension options to 2021). We expect further sales the coming years and generally view this as credit neutral.

Credit neutral

1212

Company news from the past week (high yield/unrated)

Source: Danske Bank Markets

Name News Implication

Victoria Park

Victoria Park (DBM: Overweight) announced the intention of a placement of 14.5m B-shares. The reason is to allow for a higher speed of investments, both related to property upgrades and potential further acquisitions. We obviously see this announcement as credit positive. At end June Victoria Park had a gross LTV of 64% (net: 52%). In July the company announced the largest acquisition so far, with properties in Malmö and Karlskrona for SEK1.8bn following which the total market value of its entire property portfolio will amount to SEK10.3bn. We see the announced equity issuance as a logic step to preserve healthy credit metrics. Generally we expect LTV to remain at maximum 65%. Considering the company’s focus on the more stable residential market and its long average debt maturity profile, we consider its bonds to be attractively priced compared with sector peers such as D. Carnegie and Hemfosa and maintain an Overweight recommendation.

Credit positive

Husqvarna

During its CMD on 8 September Husqvarna emphasised a shift towards a more growth-oriented strategy. To reflect this, Husqvarna set a new topline growth target of 3-5% (currency adjusted and excluding the Consumer Brands division) – equal to outpacing the market by 1-2%. The previous ambition of reaching an EBIT margin of at least 10% remains firm and management expects to be there by 2017-18. Further, the net debt / EBITDA target of <2.5x (was at 1.7x LTM by end of Q2) was scrapped and a new target for capital efficiency was set as Net Working Capital < 25% (around 27% end of Q2). In terms of operational performance the company gave a confident impression regarding its three profitable divisions; Husqvarna, Gardena and Construction. The strategy going forward includes, among others, steering the mix further towards attractive segments such as Battery and Robotics as well as geographic expansion in Europe for Gardena. For the lagging division Consumer Brands profitability is still the focus rather than topline growth (aiming for 5% EBIT margin by 2018). From a credit perspective we see the dismissed net debt/EBITDA target as somewhat negative. Although management said it is open for acquisitions, it did not state any explicit M&A ambition in the near term (the topline growth target refers to organic growth). On the other side, we see the increased focus on capital efficiency as well as the continued commitment to its margin target as offsetting. All in all we regard the CMD as credit neutral for Husqvarna. We see the company's bond spreads as fair relative to relevant peers and the SEK 'BBB' index.

Credit neutral

Outokumpu

US authorities announced preliminary determination that stainless steel sheet and strip imports from China are being dumped to the market at less than fair value. US customs are instructed to begin requiring Chinese importers to deposit estimated antidumping rates earlier decided at a range of 64-77%. Positive for Outokumpu as it should help to further reduce import volumes to US market giving more room for local producers.

Credit positive

1313

Company news from the past week (high yield/unrated)

Source: Danske Bank Markets

Name News Implication

Ahlstrom

Raised outlook on profitability for the third time this year and narrowed the sales forecast range to EUR1.060m-EUR1.100m. Adj. operating profit is now expected to come in at 6.5%-7.5% of sales vs 5.4%-6.4% previously. The improved outlook comes on the back of a continued improvement from cost cutting efforts as well as lower variable costs. Overall credit positive.

Credit positive

Heimstaden

Heimstaden announced that it had closed the merger of the Swedish part of its property portfolio with that of its associated company Nordhalla in order to attract operating synergies and build a platform for further growth. The new property-owning parent company will be Heimstaden Bostäder AB (HBAB, formerly Nordhalla Fastigheter) with Heimstaden AB as majority owner and property manager. Alecta, together with Sandvik's and Ericsson's pension funds, has taken a 35% stake in the enlarged HBAB. In return for this, Heimstaden received a cash payment, with a total cash position of SEK3.2bn post the transaction. Due to this payment and as Heimstaden has communicated that its financial policy remains unchanged, we regard the transaction as credit neutral. We assign a Marketweightrecommendation to Heimstaden’s 2019 bond, which we consider fairly priced.

Credit neutral

Stockman

Stockmann (NR) has appointed Lauri Veijalainen as its new CEO as of 12 September 2016. Lauri Veijalainen (born 1968), B.Sc., MBA, has served as Stockmann’s interim CEO since April 2016. Before that he was the company’s CFO from August 2015. He joined Stockmann in 2010 as Development Director for the Group’s International Operations. This was largely an expected outcome and should be neutral for the credit in our view.

Credit neutral

Stockman

August comparable sales flat y/y, largely in line with DBM estimates of +1% and clearly better than July’s -10%. Lindex at +4% was not quite as strong as expectations (DBMe +9% on the back of very weak y/y comps) but importantly, Retail clearly better at -5% vs DBMe -9%. From a credit perspective August sales figures should be neutral for spreads, in our view.

Credit neutral

14

Scandi investment grade

1515

Chart 1. Relative value (EUR), indicative mid spreads Chart 2. Credit spread development

Source: Bloomberg, Danske Bank Markets Source: Bloomberg, Danske Bank Markets

Trade idea – Carlsberg revisitedPublished 30 August

Buy NOKIA 2019 USD, trading at wide margin to Nokia 2019 EUR

Published on 23 May 2016

Key arguments for the trade

• On 27 May we launched a trade idea in which we recommended to buy the Carlsberg EUR2024 outright or fund it by selling the Carlsberg EUR2019 against. We revisit this trade idea as we believe the fundamental case has improved further following the H1 16 report from Carlsberg.

• Carlsberg reported net debt to EBITDA of 2.2x in H1 16 – the lowest leverage level since Q3 10.

• Carlsberg now has lower reported net debt to EBITDA than ‘BBB+’ rated Heineken.

• Carlsberg’s leverage of 2.2x is still above the company target of <2.0x. We continue to believe it is a key priority for the relatively new management team to continue to strengthen the balance sheet and deliver on the leverage target.

• We believe that Carlsberg will reach the <2.0x leverage target as of end-2016. If so, we believe that Moody’s will remove the Negative Outlook on the Baa2 rating. We expect this to support spread levels - especially in the longer end of the curve.

• We continue to see attractive value in the EUR2024.

• See Trade recommendation - Carlsberg EUR 2024 revisited –

BUY, 30 August

1616

Recent trade ideas (investment grade)

Source: Danske Bank Markets

See the end of this document for a list of our coverage including recommendations

Recent ideasType Trade Idea

Opened 30 Aug 2016

Opened 30 Aug 2016

Opened 09 Aug 2016

Opened 27 Jun 2016

Opened 03 Jun 2016

Opened 03 Jun 2016

Opened 18 Apr 2016

Opened 29 Feb 2016Outright Buy INVSA EUR 4.875% 2021 Spread on the INVSA 2021 has widened recently and is too wide compared with average spreads for industrials with high (AA) ratings.

Outright Buy Danfoss 1.375% 2022

(EUR)

The spread on the DNFSDC 22s trades wider than the ‘BBB’ fair value curve and is rated ‘BBB’ with stable outlook by S&P.

Outright Buy SEB AT1 USD 5.75% call

2020

SEB's AT1 USD 5.75% call 2020 has underperformed closest peers recently resulting in about 50bp pick up to Swedbank's'20 or SHB's '21 and about 30bp to Nordea's '21

Outright Buy Maersk EUR 2021 Maersk EUR 2021 is trading wider than the BBB- industrial curve vs. Maersks BBB+/NO rating.

Switch Buy Maersk EUR 2021 and fund

by selling Maersk EUR 2019

Pick-up is c. 40bp for around 1.5 years of maturity extension.

Buy Carlsberg EUR 2024 and

fund it by selling Carlsberg EUR

2019 (revisited)

We recommended to buy the Carlsberg EUR2024 and fund it by selling the Carlsberg EUR2019. The fundamental case has improved further following the H1 16 report from Carlsberg.

Switch Buy DONGAS 3% call 2020 and

fund by selling DONGAS 4.875%

call 2018

The DONGAS 3% call 2020 have clearly underperformed the DONGAS 4.875% call 2018 in the past 6 months. This is unjustified biven the benign newsflow in DONG Energy

Outright Buy Carlsberg EUR 2024

(revisited)

We recommended to buy the Carlsberg EUR2024. The fundamental case has improved further following the H1 16 report from Carlsberg.

Switch

1717

Best and worst performers (Nordic coverage universe)- Investment grade

Source: Bloomberg, Danske Bank Markets (both charts)

1 week in local currencies 1 month in local currencies

11

11

8

8

6

6

5

5

5

5

-4

-4

-5

-6

-7

-8

-10

-13

-17

-21

-25-20-15-10-5051015

Fortum Varme Holding samagt med…

Swedish Match AB SEK 2020

Telia Co AB EUR 2035

Vattenfall AB EUR 2024

Statkraft AS EUR 2030

DNB Bank ASA EUR 2022

DNB Bank ASA EUR 2020

DNB Bank ASA EUR 2021

Svenska Cellulosa AB SCA EUR 2023

Nordea Bank AB EUR 2025

Statkraft AS EUR 2017

Fortum Varme Holding samagt med…

Swedbank AB SEK 2018

SBAB Bank AB SEK 2018

Swedbank AB SEK 2020

Statkraft AS NOK 2020

Volvo Treasury AB SEK 2017

Sampo Oyj SEK 2020

Fortum OYJ EUR 2021

Statkraft AS NOK 2025

Change in local currencies (bp)

19

17

6

6

6

5

5

5

5

4

0

0

0

0

-1

-1

-1

-1

-2

-4

-505101520

Fortum Varme Holding samagt med…

Swedish Match AB SEK 2020

Telia Co AB EUR 2027

Svenska Cellulosa AB SCA SEK 2019

Telia Co AB EUR 2025

Statkraft AS NOK 2025

Telia Co AB EUR 2035

Telia Co AB EUR 2031

Danske Bank A/S SEK 2019

Telia Co AB EUR 2027

Swedbank AB SEK 2018

SpareBank 1 SR-Bank ASA EUR 2021

Sampo Oyj EUR 2021

Swedish Match AB EUR 2017

TDC A/S EUR 2027

Statkraft AS EUR 2017

Statkraft AS EUR 2023

Fortum Varme Holding samagt med…

Skandinaviska Enskilda Banken AB EUR…

Volvo Treasury AB SEK 2017

Change in local currencies (bp)

1818

Selected new investment-grade issues**

Source: Bloomberg, Danske Bank Markets

*Estimated

**Excluding increases in existing bond issues (taps)

Date Issuer Coupon CCY Volume Maturity S&P / Mdy / Fitch ASW/DM

15/09/2016 Deutsche Bahn Finance Bv 0.625% EUR 500 m Sep/28 / Aa1e / 20

14/09/2016 Swedish Match Ab 0.875% EUR 300 m Sep/24 BBB / Baa2e / 78

14/09/2016 Cie De Saint-Gobain 0% EUR 1 000 m Mar/20 BBB / Baa2e / BBB 30

14/09/2016 Bp Capital Markets Plc 0.83% EUR 850 m Sep/24 A- / A2 / 65

14/09/2016 National Grid Gas Fin 0.625% EUR 750 m Sep/24 A- / A3e / Ae 55

13/09/2016 Novomatic Ag 1.625% EUR 500 m Sep/23 BBB / / 170

13/09/2016 Eni Spa 1.125% EUR 600 m Sep/28 BBB+ / Baa1 / A- 70

13/09/2016 Eni Spa 0.625% EUR 900 m Sep/24 BBB+ / Baa1 / A- 55

13/09/2016 Vf Corp 0.625% EUR 850 m Sep/23 A / A3 / 57

13/09/2016 Eaton Capital Unlimited 0.75% EUR 550 m Sep/24 / Baa1 / BBB+ 65

13/09/2016 Novartis Finance Sa 0.625% EUR 500 m Sep/28 AA- / Aa3 / 27*

13/09/2016 Novartis Finance Sa 0.125% EUR 1 250 m Sep/23 AA- / Aa3 / 21*

1919

Company news from the past week (investment grade)

Source: Danske Bank Markets

Name News Implication

ISS and G4S

ISS (OW), G4S (MW): UK facility management company Mitie plunges 25% on a profit warning. Mitie says it is experiencing significant earnings pressure pre- and post-Brexit due to a combination of further public sector budget constraints in the UK (Mitie is UK-based and focused and gets 50% of group revenue from UK public contracts), overall higher minimum wages and lower margins on contract rebids. ISS generates 15% of group revenue in the UK and G4S generates around 23% of group revenue in the UK – hence an important market. However, these two companies are larger and more diverse regarding sectors and industries so the potential negative impact should not be as high as for Mitie. Both ISS and G4S have stated that they have not seen any material impact on their businesses post the UK referendum. That said, a significant profit warning from a competitor is a warning signal even though the competitor is smaller and more focused on troubled segments.

Credit neutral

Telia

Telia (OW) has commented on a proposed settlement from US and Dutch authorities. Fine amount USD1.4bn (c. SEK12bn) is higher than we and most likely the market had anticipated, given that Vimpelcom received a fine of USD800m for a similar charge in Uzbekistan. Leverage should increase by c. 0.4-0.5x as a result. We note that most of the Telia curve is trading at BBB+ equivalent levels, i.e. downside should be limited in case S&P decides that its current A- rating is too high. We also note that S&P expects leverage as high as 3x in 2016 and most of the agency's current scenario analysis is built on 2017 numbers (post Eurasia divestments). The fine will result in leverage increasing to 2.9x on LTM figures, i.e. it is not certain that the higher-than-expected settlement will result in a downgrade from S&P. We expect the Moody's rating of BBB+ to remain firm as it has already downgraded Teliathis year. Overall the news was negative but at least some uncertainty has been taken off the table for now.

Credit negative

DONG

The Danish National Audit office has been assigned to investigate the partial sale of DONG Energy (MW). This is irrelevant from a credit perspective, as the audit is meant to find out if parts of DONG Energy was sold too cheaply to Goldman Sachs. So a potential bad story for the politicians behind the sale but not something that will impact DONG Energy.

Credit neutral

2020

Company news from the past week (investment grade)

Source: Danske Bank Markets

Name News Implication

Dong

DONG Energy (MW) appeals the decision from the Copenhagen maritime and commercial high court that Elsam (which later became a part of DONG) had abused its dominant position in western Denmark charging too high prices in some periods. DONG stated that it has read the verdict closely and strongly disagrees with the findings. At the time of the verdict, DONG also clearly indicated that an appeal was likely. Now the case will be tried at the next level court and it will likely be at least a couple of years before a new verdict is passed. The potential downside for DONG Energy, if it is also found guilty in the next court, is mentioned to be as high as DKK6-10bn. DONG has only provisioned DKK298m plus interest and costs. Overall the decision to appeal is slightly positive, as any cash outflows relating to this case have been postponed at least a couple of years.

Credit positive

Banks

Danish FSA advised that banks do not use synthetic securitisations, like Nordea's recent deal, to remove risk from their balance sheets in order to decrease capital requirements. In Jesper Berg's view it sends the wrong signal to global regulators amid the region's fight to keep the current internal models. This confirms our view that other Nordic banks are not likely to pursue similar deals.

Credit neutral

Swedish Match

Swedish Match (OW): Moody's affirmed Swedish Match's Baa2/Stable rating after the partial sale of the stake in STG. Moody's stated that ‘today's affirmation reflects Moody's view that Swedish Match will remain well positioned in the rating category with fairly strong credit metrics compensating for the company's aggressive shareholders' return policy both in the form of dividends and share buybacks, and the modest geographical diversification’. We believe this is in line with market expectations and we believe this is credit neutral.

Credit neutral

Telenor

Telenor (MW) has started its selloff of its 33% stake in Vimpelcom as flagged previously. The company wishes to exit Eurasia to focus more on its expansion in South East Asia, such as Vietnam or Indonesia. The entire stake will be too large for the market to digest so Telenor will start by selling some 8.1% in the market and the rest through convertible bonds. Overall this news is neutral for the credit as the sale of the stake has already been flagged.

Credit neutral

Fortum Värme

The H1 16 results were robust. Clean earnings fell marginally due to one-off costs. Underlying operations were strong and heat volumes were up. The capex run rate is now lower, yielding a higher FCF. This caused net debt to decline. Subsequently, group credit metrics improved to solid levels for the current ‘BBB+’ rating from S&P. Overall, it was a credit neutral report. We assign a Marketweightrecommendation to Fortum Värme as we find the bonds to be fairly priced when considering illiquidity.

Credit neutral

2121

Company news from the past week (investment grade)

Source: Danske Bank Markets

Name News Implication

Vattenfall

Vattenfall (MW) has just won a 350MW near-coast offshore wind turbine concession with a feed-in-tariff price of DKK0.475/KWh (EUR63.8/MWh). However, the Danish government is currently doing an overhaul of its wind subsidy policy and it is currently the plan to scrap new concessions of near-coast offshore projects including the ones just won by Vattenfall. Therefore this project is unlikely to goahead as things are now. That said, the Danish political situation is currently very volatile and it cannot be ruled out that a general election is on its way, as the coalition parties disagree about the new long term economic plan for Denmark. If a general election comes and the current right wing government is replaced with a left-wing government, we see it as very likely that the 350MW offshore project will get the green light. This would be mildly positive for Vattenfall, although we flag that the price of only EUR63.8/MWh is very low and leaves little room for error in construction and operations of the wind farm. Overall credit neutral for now.

Credit neutral

22Credit Indicators

Credit indicators

2323

Chart pack: euro spreads and returns

Source: Macrobond Financial, Danske Bank Markets [all charts]

Euro IG ASW, iBoxx indices

Euro HY ASW, Merrill Lynch indices

IG total return, iBoxx indices, 2014-01=100

HY total return, Merrill Lynch indices, 2014-01=100

2424

Chart pack: relative value

Source: Macrobond Financial, Danske Bank Markets [all charts]

iTraxx vs iBoxx

Euro vs US CDS indices - IG (Markit) Euro vs US HY bond indices (Merrill Lynch)

2525

Chart pack: general market development

Source: Macrobond Financial, Danske Bank Markets [all charts]

European swap and government yields

Euro swap curve spread

3M Libor, US and euro area

EUR/USD basis swaps

2626

Chart pack: funds flow

Source: Macrobond Financial, Danske Bank Markets [all charts]

Europe, net sales

Sweden, net sales

US, net sales

Norway, net sales

2727

Chart pack: macro

Source: Macrobond Financial, Danske Bank Markets [all charts]

GDP y/y growth, calendar adjusted

Euro area y/y change in bank lending

Purchasing Manager Indices

Euro area lending standards

28

Coverage universe, credit ratings

and recommendations

2929

Our coverage 1 of 6

Source: Standard & Poor's, Moody's, Fitch, Danske Bank Markets

Ratings from S&P/Moody's/Fitch

Analyst(s)

Company Rating Outlook Rating Outlook Rating OutlookAhlstrom Oyj M. Rosendal / J. MagnussenAkelius Residential Property Ab BBB- Stable L. Landeman / G. Bergin OVERWEIGHTAktia Bank Plc A- Neg A3 Pos L. Holm / K. JensenAlandsbanken Abp BBB Neg L. Holm / K. JensenAmbu A/S J. Magnussen / M. RosendalAp Moeller - Maersk A/S BBB Baa1 Stable B. Børsting/J. Magnussen MARKETWEIGHTArla Foods Amba G. Bergin / L. LandemanAtlas Copco Ab A Stable A2 Stable A Stable B. Børsting / M. Rosendal UNDERWEIGHTAvinor As AA- Stable A1 Stable G. Bergin / L. Landeman MARKETWEIGHTBalder L. Landeman / G. Bergin OVERWEIGHTBank 1 Oslo Akershus As L. Holm / K. JensenBank Norwegian As L. Holm / K. JensenBeerenberg Holdco Ii As Ø. MossigeBillerudkorsnas Ab M. Rosendal / L. LandemanBonum Pankki Oyj BBB Stable L. Holm / K. JensenBrage Finans As L. Holm / K. JensenBw Offshore Ø. MossigeCaruna Networks Oy BBB+ Stable J.Magnussen / L.Landeman OVERWEIGHTCarlsberg Breweries A/S Baa2 Neg BBB Stable B. Børsting / M. Rosendal MARKETWEIGHTCastellum Ab L. Landeman / G. Bergin MARKETWEIGHTCitycon Oyj BBB Stable Baa1 Stable L. Landeman / G. Bergin MARKETWEIGHTColor Group As B. Børsting / N. Ripa MARKETWEIGHTCom Hem Holding Ab BB Stable M. Rosendal / J. Magnussen OVERWEIGHTCorem Property Group Ab L. Landeman / G. Bergin MARKETWEIGHTDanfoss A/S BBB Stable J. Magnussen / B. Børsting MARKETWEIGHTDanske Bank A/S A Stable A2 Stable A StableDeep Sea Supply Plc Ø. MossigeDestia Group Oy L. Landeman / G. BerginDfds A/S B. Børsting / N. RipaDlg Finance As M. Rosendal / B. BørstingDna Ltd M. Rosendal / J. MagnussenDnb Bank Asa A+ Neg Aa2 Neg L. Holm / K. Jensen UNDERWEIGHT

Recomm.S&P Moody's Fitch

3030

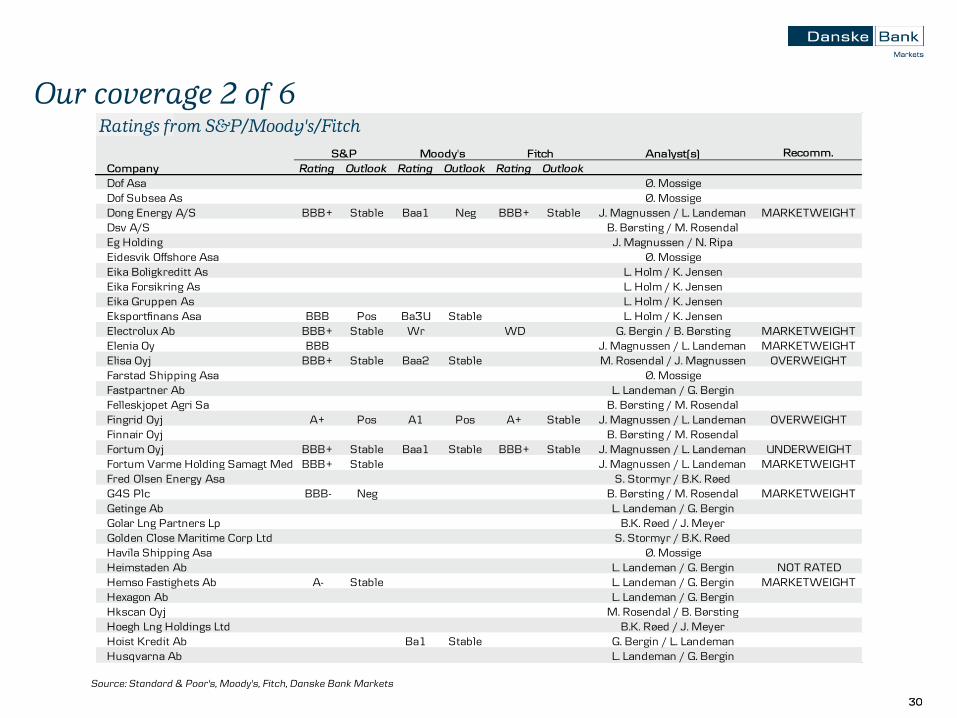

Our coverage 2 of 6

Source: Standard & Poor's, Moody's, Fitch, Danske Bank Markets

Ratings from S&P/Moody's/Fitch

Analyst(s)

Company Rating Outlook Rating Outlook Rating OutlookDof Asa Ø. MossigeDof Subsea As Ø. MossigeDong Energy A/S BBB+ Stable Baa1 Neg BBB+ Stable J. Magnussen / L. Landeman MARKETWEIGHTDsv A/S B. Børsting / M. RosendalEg Holding J. Magnussen / N. RipaEidesvik Offshore Asa Ø. MossigeEika Boligkreditt As L. Holm / K. JensenEika Forsikring As L. Holm / K. JensenEika Gruppen As L. Holm / K. JensenEksportfinans Asa BBB Pos Ba3U Stable L. Holm / K. JensenElectrolux Ab BBB+ Stable Wr WD G. Bergin / B. Børsting MARKETWEIGHTElenia Oy BBB J. Magnussen / L. Landeman MARKETWEIGHTElisa Oyj BBB+ Stable Baa2 Stable M. Rosendal / J. Magnussen OVERWEIGHTFarstad Shipping Asa Ø. MossigeFastpartner Ab L. Landeman / G. BerginFelleskjopet Agri Sa B. Børsting / M. RosendalFingrid Oyj A+ Pos A1 Pos A+ Stable J. Magnussen / L. Landeman OVERWEIGHTFinnair Oyj B. Børsting / M. RosendalFortum Oyj BBB+ Stable Baa1 Stable BBB+ Stable J. Magnussen / L. Landeman UNDERWEIGHTFortum Varme Holding Samagt Med Stockholms Stad AbBBB+ Stable J. Magnussen / L. Landeman MARKETWEIGHTFred Olsen Energy Asa S. Stormyr / B.K. RøedG4S Plc BBB- Neg B. Børsting / M. Rosendal MARKETWEIGHTGetinge Ab L. Landeman / G. BerginGolar Lng Partners Lp B.K. Røed / J. MeyerGolden Close Maritime Corp Ltd S. Stormyr / B.K. RøedHavila Shipping Asa Ø. MossigeHeimstaden Ab L. Landeman / G. Bergin NOT RATEDHemso Fastighets Ab A- Stable L. Landeman / G. Bergin MARKETWEIGHTHexagon Ab L. Landeman / G. BerginHkscan Oyj M. Rosendal / B. BørstingHoegh Lng Holdings Ltd B.K. Røed / J. MeyerHoist Kredit Ab Ba1 Stable G. Bergin / L. LandemanHusqvarna Ab L. Landeman / G. Bergin

Recomm.S&P Moody's Fitch

3131

Our coverage 3 of 6

Source: Standard & Poor's, Moody's, Fitch, Danske Bank Markets

Ratings from S&P/Moody's/Fitch

Analyst(s)

Company Rating Outlook Rating Outlook Rating OutlookIca Gruppen Ab G. Bergin / L. LandemanIkano Bank Ab L. Holm / K. JensenInvestor Ab AA- Stable Aa3 Stable G. Bergin / B. Børsting OVERWEIGHTIss A/S BBB Stable B. Børsting / M. Rosendal OVERWEIGHTJ Lauritzen A/S B.K. Røed / J. MeyerJefast Holding Ab L. Landeman / G. Bergin OVERWEIGHTJernhusen Ab G. Bergin / L. Landeman UNDERWEIGHTJyske Bank A/S A- Stable Baa1U Stable L. Holm / K. Jensen OVERWEIGHTKemira Oyj Wr M. Rosendal / L. LandemanKesko Oyj G. Bergin / L. LandemanKlaveness Ship Holding As B.K. Røed / J. MeyerKlovern Ab L. Landeman / G. Bergin OVERWEIGHTKongsberg Gruppen Ø. MossigeLantmannen Ek For G. Bergin / L. LandemanLoomis Ab B. Børsting / M. RosendalLuossavaara-Kiirunavaara Ab L. Landeman / G. BerginMeda Ab L. Landeman / G. BerginMetsa Board Oyj BB+ Pos Ba2 Stable M. Rosendal / L. Landeman OVERWEIGHTMetso Oyj BBB Stable Baa2 Stable B. Børsting / M. Rosendal MARKETWEIGHTNcc Ab L. Landeman / G. BerginNeste Oyj J. Magnussen / L. Landeman MARKETWEIGHTNibe Industrier Ab G. Bergin / L. LandemanNokia Oyj BB+ Pos Ba1 Stable BB+ Pos M. Rosendal / J. Magnussen OVERWEIGHTNordax Bank Ab L. Holm / K. JensenNordea Bank Ab AA- Neg Aa3 Stable AA- Stable L. Holm / K. Jensen UNDERWEIGHTNorth Atlantic Drilling Ltd S. Stormyr / B.K. RøedNorwegian Air Shuttle Asa B. Børsting / M. RosendalNorwegian Property Asa H. Syed/ B. EngebretsenNykredit Bank A/S A Stable Baa3U Stable A Stable L. Holm / K. Jensen MARKETWEIGHTNynas Group J. Magnussen / L. Landeman OVERWEIGHTObos Bbl H. Syed/ B. Engebretsen MARKETWEIGHTOcean Rig Udw Inc CCC- Neg Ca Neg S. Stormyr / B.K. Røed

Recomm.S&P Moody's Fitch

3232

Our coverage 4 of 6

Source: Standard & Poor's, Moody's, Fitch, Danske Bank Markets

Ratings from S&P/Moody's/Fitch

Analyst(s)

Company Rating Outlook Rating Outlook Rating OutlookOcean Yield Asa Ø. MossigeOdfjell Se B.K. Røed / J. MeyerOlympic Ship As Ø. MossigeOp Corporate Bank Plc AA- Neg Aa3 Stable WD L. Holm / K. Jensen OVERWEIGHTOrava Residential Reit Plc L. Landeman / G. BerginOrkla Asa H. Syed/ B. EngebretsenOutokumpu Oyj B3 Pos M. Rosendal / L. LandemanPacific Drilling Sa CCC+ Neg Caa2 Neg S. Stormyr / B.K. RøedPetroleum Geo-Services Asa CCC+ Neg Caa1 Neg S. StormyrPostnord Ab G. Bergin / L. LandemanProsafe Se S. Stormyr / B.K. RøedRamirent Oyj B. Børsting / M. RosendalRem Offshore Asa Ø. MossigeSaab Ab Wr G. Bergin / L. LandemanSandnes Sparebank L. Holm / K. JensenSandvik Ab BBB Neg B. Børsting / M. Rosendal MARKETWEIGHTSas Ab B Stable Wr Stable B. Børsting / M. Rosendal OVERWEIGHTSbab Bank Ab A Neg A2 Stable L. Holm / K. Jensen MARKETWEIGHTScania Ab BBB+ Neg M. Rosendal / B. Børsting MARKETWEIGHTSeadrill Ltd S. Stormyr / B.K. RøedSecuritas Ab BBB Stable Wr B. Børsting / M. Rosendal MARKETWEIGHTShip Finance International Ltd Wr B.K. Røed / J. MeyerSiem Offshore Inc Ø. MossigeSkandinaviska Enskilda Banken Ab A+ Stable Aa3 Stable AA- Stable L. Holm / K. Jensen OVERWEIGHTSkanska Ab L. Landeman / G. BerginSkf Ab BBB Neg Baa2 Stable M. Rosendal / G. Bergin MARKETWEIGHTSognekraft As J. Magnussen / L. LandemanSolstad Offshore Asa Ø. MossigeSpar Nord Bank A/S L. Holm / K. JensenSparbanken Skane Ab BBB+ Pos L. Holm / K. JensenSparebank 1 Boligkreditt As L. Holm / K. JensenSparebank 1 Nord Norge A1 Stable A Stable L. Holm / K. Jensen MARKETWEIGHT

Recomm.S&P Moody's Fitch

3333

Our coverage 5 of 6

Source: Standard & Poor's, Moody's, Fitch, Danske Bank Markets

Ratings from S&P/Moody's/Fitch

Analyst(s)

Company Rating Outlook Rating Outlook Rating OutlookSparebank 1 Smn A1 Stable A- Stable L. Holm / K. Jensen UNDERWEIGHTSparebank 1 Sr-Bank Asa A1 Neg A- Stable L. Holm / K. Jensen UNDERWEIGHTSparekassen Kronjylland L. Holm / K. JensenSponda Oyj L. Landeman / G. Bergin OVERWEIGHTSrv Group Oyj Louis LandemanSsab Ab B+ Stable M. Rosendal / L. Landeman MARKETWEIGHTSt1 Nordic Oy J. Magnussen / L. Landeman OVERWEIGHTStatkraft Sf A- Neg Aaa Stable J. Magnussen / L. Landeman MARKETWEIGHTStatnett Sf A+ Stable Wr Stable J. Magnussen / L. Landeman MARKETWEIGHTStatoil Asa A+ Stable Aa3 Stable J. Magnussen / L. Landeman UNDERWEIGHTStena Ab BB- Neg B3 Stable B. Børsting / N. Ripa UNDERWEIGHTStockmann Oyj Abp M. Rosendal / G. BerginStolt-Nielsen Ltd B.K. Røed / J. MeyerStora Enso Oyj BB Pos Ba2 Pos WD M. Rosendal / L. Landeman UNDERWEIGHTStorebrand Bank Asa BBB+ Stable Nr Stable L. Holm / K. JensenStorebrand Livsforsikring Group BBB+ Stable Baa1 Stable L. Holm / K. JensenSunnfjord Energi As J. Magnussen / L. LandemanSuomen Hypoteekkiyhdistys BBB Neg L. Holm / K. JensenSvensk Fastighetsfinansiering Ab Louis LandemanSvenska Cellulosa Ab Sca A- Stable Baa1 Neg M. Rosendal / B. Børsting UNDERWEIGHTSvenska Handelsbanken Ab AA- Neg Aa2 Stable AA Stable L. Holm / K. Jensen MARKETWEIGHTSwedavia Ab G. Bergin / L. LandemanSwedbank Ab AA- Neg Aa3 Stable AA- Stable L. Holm / K. Jensen MARKETWEIGHTSwedish Match Ab BBB Stable Baa2 Stable B. Børsting / M. Rosendal OVERWEIGHTSydbank A/S Baa1 Stable L. Holm / K. Jensen OVERWEIGHTTallink Grupp As B. Børsting / J. MagnussenTdc A/S BBB- Stable Baa3 Stable BBB- Stable M. Rosendal / J. Magnussen MARKETWEIGHTTechnopolis Oyj L. Landeman / G. Bergin MARKETWEIGHTTeekay Lng Partners Lp Ø. MossigeTeekay Offshore Partners Lp Ø. MossigeTele2 Ab M. Rosendal / J. MagnussenTelefonaktiebolaget Lm Ericsson BBB+ Neg Baa1 Stable BBB+ Stable M. Rosendal / J. Magnussen MARKETWEIGHT

Recomm.S&P Moody's Fitch

3434

Our coverage 6 of 6

Source: Standard & Poor's, Moody's, Fitch, Danske Bank Markets

Ratings from S&P/Moody's/Fitch

Analyst(s)

Company Rating Outlook Rating Outlook Rating OutlookTelenor Asa A Stable A3 Stable M. Rosendal / J. Magnussen MARKETWEIGHTTelia Co Ab A- Stable Baa1 Stable A- Stable M. Rosendal / J. Magnussen OVERWEIGHTTeollisuuden Voima Oyj BB+ Stable Wr BBB Neg J. Magnussen / L. Landeman OVERWEIGHTTopdanmark A/S L. Holm / K. JensenTryg Forsikring A/S L. Holm / K. JensenUpm-Kymmene Oyj BB+ Pos Ba1 Pos WD M. Rosendal / L. Landeman MARKETWEIGHTVasakronan Ab L. Landeman / G. Bergin MARKETWEIGHTVattenfall Ab BBB+ Neg A3 Neg BBB+ Stable J. Magnussen / L. Landeman MARKETWEIGHTVestas Wind Systems A/S J. Magnussen / N. Ripa OVERWEIGHTVictoria Park Ab L. Landeman / G. Bergin OVERWEIGHTVolvo Ab BBB Stable Baa2 Stable BBB Stable M. Rosendal / B. Børsting MARKETWEIGHTWelltec A/S B Neg B2 Neg S. StormyrWihlborgs Fastigheter Ab L. Landeman / G. Bergin UNDERWEIGHTWilh Wilhelmsen Asa B.K. Røed / J. MeyerYit Oyj L. Landeman / G. Bergin

Recomm.S&P Moody's Fitch

3535

Fixed Income Credit Research team

Find the latest Credit Research: :

Danske Bank Markets: http://www.danskebank.com/danskemarketsresearch Bloomberg: DNSK<GO>

Thomas Hovard

Head of Credit Research

+45 45 12 85 05

Gabriel Bergin

Strategy, Industrials

+46 8 568 80602

Øyvind Mossige

Oil services

+47 85 40 54 91

Sondre Dale Stormyr

Offshore rigs

+47 85 40 70 70

Katrine Jensen

Financials

+45 45 12 80 56

Jakob Magnussen

Utilities, Energy

+45 45 12 85 03

Bjørn Kristian Røed

Shipping

+47 85 40 70 72

Henrik René Andresen

Credit Portfolios

+45 45 13 33 27

Bendik Engebretsen

Industrials

+47 85 40 69 14

Brian Børsting

Industrials

+45 45 12 85 19

Niklas Ripa

High Yield, Industrials

+45 45 12 80 47

Louis Landeman

Industrials, Real Estate

+46 8 568 80524

Lars Holm

Financials

+45 45 12 80 41

Knut-Ivar Bakken

Fish farming

+47 85 40 70 74

Mads Rosendal

Industrials, TMT

+45 45 14 88 79

August Moberg

Industrials & Construction

+46 8 568 80593

Haseeb Syed

Industrials

+47 85 40 54 19

Jonas Meyer

Shipping

+47 85 40 70 79

3636

Disclosures

This research report has been prepared by Danske Bank Markets, a division of Danske Bank A/S ('Danske Bank'). The authors of this research report are stated on the front page of this report.

Analyst certification

Each research analyst responsible for the content of this research report certifies that the views expressed in the research report accurately reflect the research analyst’s personal view about the financial instruments and issuers covered by the research report. Each responsible research analyst further certifies that no part of the compensation of the research analyst was, is or will be, directly or indirectly, related to the specific recommendations expressed in the research report.

Regulation

Danske Bank is authorised and subject to regulation by the Danish Financial Supervisory Authority and is subject to the rules and regulation of the relevant regulators in all other jurisdictions where it conducts business. Danske Bank is subject to limited regulation by the Financial Conduct Authority and the Prudential Regulation Authority (UK). Details on the extent of the regulation by the Financial Conduct Authority and the Prudential Regulation Authority are available from Danske Bank on request.

The research reports of Danske Bank are prepared in accordance with the Danish Finance Society’s rules of ethics and the recommendations of the Danish Securities Dealers Association.

Danske Bank is not registered as a Credit Rating Agency pursuant to the CRA Regulation (Regulation (EC) no. 1060/2009); hence, Danske Bank does not comply with or seek to comply with the requirements applicable to credit rating agencies.

Any ratings are provided as part of an investment research product and do not equate with ratings produced by Credit Rating Agencies.

Conflicts of interest

Danske Bank has established procedures to prevent conflicts of interest and to ensure the provision of high-quality research based on research objectivity and independence. These procedures are documented in Danske Bank’s research policies. Employees within Danske Bank’s Research Departments have been instructed that any request that might impair the objectivity and independence of research shall be referred to Research Management and the Compliance Department. Danske Bank’s Research Departments are organised independently from and do not report to other business areas within Danske Bank.

Research analysts are remunerated in part based on the overall profitability of Danske Bank, which includes investment banking revenues, but do not receive bonuses or other remuneration linked to specific corporate finance or debt capital transactions.

Danske Bank, its affiliates and subsidiaries are engaged in commercial banking, securities underwriting, dealing, trading, brokerage, investment management, investment banking, custody and other financial services activities, may be a lender to the companies mentioned in this publication and have whatever rights are available to a creditor under applicable law and the applicable loan and credit agreements. At any time, Danske Bank, its affiliates and subsidiaries may have credit or other information regarding the companies mentioned in this publication that is not available to or may not be used by the personnel responsible for the preparation of this report, which might affect the analysis and opinions expressed in this research report

See http://www-2.danskebank.com/Link/researchdisclaimer for further disclosures and information..

3737

General disclaimer

This research has been prepared by Danske Bank Markets (a division of Danske Bank A/S). It is provided for informational purposes only. It does not constitute or form part of, and shall under no circumstances be considered as, an offer to sell or a solicitation of an offer to purchase or sell any relevant financial instruments (i.e. financial instruments mentioned herein or other financial instruments of any issuer mentioned herein and/or options, warrants, rights or other interests with respect to any such financial instruments) ('Relevant Financial Instruments').

The research report has been prepared independently and solely on the basis of publicly available information that Danske Bank considers to be reliable. While reasonable care has been taken to ensure that its contents are not untrue or misleading, no representation is made as to its accuracy or completeness and Danske Bank, its affiliates and subsidiaries accept no liability whatsoever for any direct or consequential loss, including without limitation any loss of profits, arising from reliance on this research report.

The opinions expressed herein are the opinions of the research analysts responsible for the research report and reflect their judgement as of the date hereof. These opinions are subject to change, and Danske Bank does not undertake to notify any recipient of this research report of any such change nor of any other changes related to the information provided in this research report.

This research report is not intended for, and may not be redistributed to, retail customers in the United Kingdom or the United States.

This research report is protected by copyright and is intended solely for the designated addressee. It may not be reproduced or distributed, in whole or in part, by any recipient for any purpose without Danske Bank's prior written consent.

Disclaimer related to distribution in the United States

This research report was created by Danske Bank A/S and is distributed in the United States by Danske Markets Inc., a U.S. registered broker-dealer and subsidiary of Danske Bank A/S, pursuant to SEC Rule 15a-6 and related interpretations issued by the U.S. Securities and Exchange Commission. The research report is intended for distribution in the United States solely to 'U.S. institutional investors' as defined in SEC Rule 15a-6. Danske Markets Inc. accepts responsibility for this research report in connection with distribution in the United States solely to 'U.S. institutional investors'.

Danske Bank is not subject to U.S. rules with regard to the preparation of research reports and the independence of research analysts. In addition, the research analysts of Danske Bank who have prepared this research report are not registered or qualified as research analysts with the NYSE or FINRA but satisfy the applicable requirements of a non-U.S. jurisdiction.

Any U.S. investor recipient of this research report who wishes to purchase or sell any Relevant Financial Instrument may do so only by contacting Danske Markets Inc. directly and should be aware that investing in non-U.S. financial instruments may entail certain risks. Financial instruments of non-U.S. issuers may not be registered with the U.S. Securities and Exchange Commission and may not be subject to the reporting and auditing standards of the U.S. Securities and Exchange Commission.