volume ii number 6 august 2012 -...

TRANSCRIPT

Africa and Middle East

2% CAGR in 2012-19

NEW home-refuelling technology

Volume II Number 6 August 2012

1st NGVA Europe International LNG WorkshopLNG - Dual Fuel - LBG for transport

19 – 21 September 2012Hotel CASA400, Amsterdam, The Netherlands

An event of Host / Sponsor Diamond

LIQUIFIED BIOGAS

Sponsor Silver Organized by

August 20122

SummarySummaryNGV Africa is a publication of NGVCommunications Group, a publishing houseand fairs-conferences organizer, which website is www.ngvjournal.com. Since 1988 promoting natural gas vehicles.Offices in CH’UNCH’ON (Korea), MARMIROLO(Italy), LIMA (Peru) and BUENOS AIRES(Argentina). Six magazines that reach thewhole world: GNV Latinoamerica, PrensaVehicular Peru, Asian NGV Communications(Greater Asia), The Gas Vehicles Report(Europe, United States and Canada,etc), PrensaVehicular (Argentina) and NGV Africa. We speak about NGV in 16 languages and toover 100 countries.The signed articles are exclusive responsibility ofthe authors, as well as advertising companies andagencies are responsible for the published ads.

Vicolo Gonzaga 13 ■ 46045 Marmirolo (Mn)Tel.: +39 0376 [email protected] ■ www.thegvr.com

Uspallata 711 ■ CP 1268Ciudad Autónoma de Buenos AiresTel./Fax: +54 11 43074559 /5201/ 43006137 [email protected]

The hard copy of NGVAfrica is sent to 324 postal addresses from 21African countries addressedto governmental relatedoffices, OEM and Oil & Gas companies,associations, related NGV industries, refuelling stations,workshops and sup-pliers, according the follow-ing list (some figures rounded):AlgeriaBenin

CameroonComoros

EgyptGhana

Guinea-Bissau Guinea KenyaLiberia

Mozambique NamibiaNigeriaRwandaSenegal

Sierra Leone South Africa,

TanzaniaTunisia, Uganda,

Zimbabwe

In addition, the magazine issent to over more than17,000 in 94 countries by e-mail (.pdf) and is alsoonline inwww.ngvjournal.comEnter this new market!To publish and advertisewith us, [email protected]

300-5, Changchon-Ri ■ Namsan-MyunChuncheon-Si ■ Kangwon-Do ■ 200-911 Tel. +82 33 260 3419Fax. +82 33 260 [email protected] ■ www.asiangv.com

KOREA

ITALY

PERU

Av. Brasil 3222 oficina 403 ■

A Magdalena del Mar ■

CP: Lima 17 ■ Perú[email protected]

NGVJOURNAL

www.ngvjournal.com / www.ngvjournal.us

Summary4

13

14

15

15

16

17

18

20

21

22

27

28ARGENTINA

Distribution Coverage

Study comparisons of natural gas/biogas versus diesel HDVs

Around 25.4 million NGVs sales projected for 2019

Egypt opened eight NG fueling stations during the first half of 2012

Egypt plans to add 24,000 NGVs in 2012

South Africa new vehicle prospect 2016

Mozambique to add two more stations soon

Gas finds in Mozambique and Tanzania

NGC underlined its commitment to promote Compressed natural gas

A new IGU report on NGVs is released

Cheaper and more convenience CNG home refuelling appliance ...

Company and product

NGV statistics

Worldwide NGV statistics

13th NGV Global Biennial conference and exhibition

26

The fuel alternative for all transports

L-CNG. Bio & natural gas.

GothenburgSweden

11-13JUNE2013

Organized by

®

Sponsor Gold

®

Hosted by

®GothenburgSweden

11-13JUNE2013

4th NGVA Europe International Show & WorkshopsNatural Gas – Biomethane - CNG – LNG – Hydrogen Blends Vehicles

The fuel alternative for all transports

L-CNG. Bio & natural gas.

An event of

®

The Swedish Exhibition & Congress Centre

/Svenska Mässan

4th NGVA Europe International Show & WorkshopsNatural Gas – Biomethane - CNG – LNG – Hydrogen Blends Vehicles

The Swedish Exhibition & Congress Centre

/Svenska Mä[email protected]

August 20124

Natural gas or methane is an excellentenergy vector, with the lowest Carbonto Hydrogen ratio of all the hydrocarbons, according to NGVAEurope’s general manager ManuelLage’s presentation. It is an alternativefuel coming from natural wells, whichmainly consists of methane (CH4).

The renewable form of this gas, so-called biogas, is also methanerich, produced by the fermentation ofthe biomass.

Methane has less carbon moleculescompared to traditional fuels. • Methane contents 25 percent H and75 percent Carbon (C), in weight• Petrol contents 13.5 percent Hand 86.5 percent C• Diesel oil contents 13.5 percent Hand 86.5 percent C• LPG contents 17.4 percent H and82.6 percent CBiogas can be further purified intobiomethane which has 80 to 98 percent methane content. Biogas thatis upgraded to pipeline quality-stan-dard can be used interchangeablywith fossil natural gas.

Natural Gas Vehicles (NGVs) aretoday the best and most economicalternative to oil derived fuels. Usingnatural gas in transportation reducesgaseous and acoustic emissions ofthe vehicles.Thanks to a well known and maturecar and commercial vehicle technology, natural gas can be usedin existing internal combustionengines with minor additional investments. Dual Fuel diesel/LNG ordiesel/CNG technology offers thepossibility of conversion for existingengines.Natural gas has been used so far asCNG mainly for urban applications,but also for private cars. Meanwhile,the availability of LNG will spread itsuse for medium and long distancesroad transport, mainly for Heavy-DutyCommercial Vehicles such as trucks,trailers, etc.In terms of Medium and Heavy-Dutytransports, both CNG and LNG are Noise emitted by the truck

CNG.Other emissions comparisionCNG waste-collection trucks in Canada

CNG.Other emissions comparisionCNG waste-collection trucks in Canada

Study comparisons of naturalgas/biogas versus diesel HDVs

August 2012 5

commonly used in America, Asia,and Europe but also in Egypt. InAfrica, leading NGV nation Egypt islaying its hopes on natural gas tohelp reducing energy subsidies thatare eating up 20 percent of its statebudget and are likely to continuegrowing.

Natural gas in Heavy-DutyVehicles

In Heavy-Duty Transport segment,CNG is mainly used in buses, whileLNG and dual fuel system mostlyfound in Heavy-Duty trucks withexceptions in Russia and China thathave public LNG buses.In Africa, with Egypt as exception-interests in CNG is mainly focusedon public bus segment. Using thisfuel in such public transportationcould give a more significant economic and ecological savings asbuses needs a larger volume of fuelsthan cars to operate. Apart from that,the regular operation of the busesrequires a stable and bigger amountof fuel to be purchased. As CNG ischeaper than petrol and diesel, themore fuel used, the bigger the savings. Algeria, Tunisia, Tanzania, and

Mozambique have done the trials onCNG buses. Although NigerianNGV market is mainly in car/taxisegment, various companies arekeen to see CNG in buses or eventrucks. In fact, Nigerian Coca ColaCompany has converted some of itsdelivery trucks powered by diesel todual fuel diesel/CNG system.

Gas-powered trucks

Just to give a few examples of theNG-HDVs use around the world, notonly in Nigeria, Coca-Cola also recognized the advantage of usingCNG in its delivery trucks all overthe world. For example, this year inthe United Kingdom, the firm bought14 Iveco Stralis natural gas lorriesafter 12-month trial finds biomethanecan help cut air and noise pollution.As mentioned above, biomethanehas similar characteristics as naturalgas. Therefore, no adjustment isrequired to allow biomethane insteadof CNG to be used in any CNGvehicles.As per trial result, the gas-poweredvehicles achieved an estimated 50.3percent saving in well-to-wheel greenhouse gas emissions, compared

to an Iveco diesel fuelled vehicle. As Coca Cola plans to install a natural gas filling station at theEnfield depot to facilitate this fleet, itis predicted that the company couldcut greenhouse gas emissions by60.7 percent.

The firm has also trialled a forklifttruck converted to operate onbiomethane at the Enfield site, whichachieved a 71 percent well-to-wheelCO2 saving.The Stralis biomethane trucks alsoproduced 85.6 percent less nitrogenoxides and 97.1 percent less PMemissions compared to the diesel-fuelled truck, and reducednoise levels by up to 10.5 decibels,making it more suitable for late nightand early morning deliveries.Although gas-powered trucks areslightly more expensive than thediesel versions, this can be offset byCNG or biomethane fuel savings. Allover the world, the gas costs muchcheaper than diesel and petrol.The total cost of gas-trucks ownershipof Coca Cola would increase by15.3 percent. However, biogas is

Continue to page 6

August 20126

12.8 percent cheaper than diesel inthe UK (North London).Apart from various countries inEurope (Spain, UK, Sweden, TheNetherlands, France, and many others), North America is known asthe leading user of Heavy-DutyNGVs with many private fleets usingCNG, LNG, or the biomethane version of this fuel to power publicand school buses, waste collectiontrucks as well as long-haul commercial trucks.

Apart from CNG trucks, the NGVindustry also offers dual fueldiesel/methane (CNG or LNG) solution. For the methane part CNGor LNG can be used in the vehicle,or Liquefied Biomethane Gas (LBG)or Compressed Biomethane (CBG). In May 2011, Volvo Trucks introduced Volvo FM MethaneDiesel, a gas-powered truckdesigned for long-haul deliveries. The new technology in this Volvotruck allows a combination of up to75 percent liquefied methane gasand 25 diesel, with the diesel serving as spark plug (assist the combustion process). With biogas inthe fuel tank, CO2 emissions dropby up to 70 percent compared witha conventional diesel engine; withfossil-based gas, emissions drop by10 percent. The dual fuelmethane/diesel system is 30 to 40percent more energy-efficient than atruck fitted with conventional-poweredspark plugs engine.

Gas-powered buses

In 2004, US Department of Energy’sNational Renewable EnergyLaboratory (NREL) conducted an evaluation of the emissions of transitbuses operated by the WashingtonMetropolitan Area Transit Authority(WMATA). The project was carriedout to evaluate the emissions of natural gas transit buses and theimproving baseline emissions of comparable diesel buses withadvanced emission control technologies.

The buses included in the study consist of followings:• CNG buses with model year (MY)2004 John Deere 6081H engines,with oxidation catalysts • CNG buses with MY 2001

Cummins Westport, Inc. (CWI) CGas Plus engines, with oxidation catalysts • Diesel buses with MY 2004Detroit Diesel Corporation (DDC)Series 50 engines, with catalyzedparticulate filters and EGR • Diesel buses with MY 2000 DDCSeries 50 engines, with catalyzedparticulate filters.

The John Deere CNG buses produced 49 percent lower NOxemissions and 84 percent lower PMemissions compared with the MY2004 DDC diesel buses, and 63percent lower NOx emissions and60 percent lower PM emissions compared with the MY 2000 DDCdiesel buses. The CWI buses produced 6.1 percent higher NOxemissions and 60 percent lower PMemissions compared with the MY2004 DDC diesel buses, and 23percent lower NOx emissions andequal PM emissions compared withthe MY 2000 DDC diesel buses.

In terms of fuel economy, the JohnDeere CNG buses showed a 9 percent improvement compared withthe MY 2004 DDC diesel buses anda 2.9 percent improvement compared with the MY 2000 DDCdiesel buses. The CWI CNG busesexhibited a fuel economy 4.2 percent higher than the MY 2004DDC diesel buses and 1.6 percentlower than the MY 2000 DDC dieselbuses. Both CNG engines use leanburn technology.

The emission reductions of CNGbuses will increase when:1. These are compared with dieselbuses without particulate filters,and/or;2. Biomethane is used in the CNGbuses instead of natural gas.3. Diesel buses without particulate filters are used as comparisons.

On the other hand, in the Netherlands,diesel particulate filters are no longersubsidized. Diesel particulate filterswere filled with PM in a “reasonably’short period. When this happened,and the filters were no longer deliveran optimal result, especially whenthese are not regularly cleaned. It wasconcluded that the diesel particulate filters are quite expensive consideringthe filter price versus advantages andproduct life cycle.

NGV deployment map: The Canadian example

In 2010, related stakeholders inCanada launched The Natural GasUse in the Canadian TransportationSector Deployment Roadmap initiative. As a result, a report withsimilar title is released. The report describes a technicalguideline created to help fleets transition to Natural Gas Vehicle useThe report can be obtained athttp://oee.nrcan.gc.ca/sites/oee.nrcan.gc.ca/files/pdf/transportation/alternative-fuels/resources/pdf/roadmap.pdf

Continued from page 5

LNG truck in North America

August 2012 7

Le gaz naturel ou le méthane est unexcellent vecteur énergétique ayant lerapport carbone sur hydrogène leplus bas de tous les hydrocarbonésselon le rapport de Manuel Lagedirecteur général de NGVA Europe.C’est un carburant alternatif provenantde réservoirs naturels contenant principalement du méthane (CH4).

La forme renouvelable de ce gaz,dénommé biogaz, est aussi riche enméthane, produit par la fermentationde la biomassse.

Le méthane a moins de molécules decarbone que les carburants traditionnels.• Le méthane contient 25% d’hydrogène (h) et 75% de Carbone(C) en poids• Le pétrole contient 13,5% de H et86,5 % de C• Le diesel contient 13,5 de H et86,5 % de C• Le LPG contient 17,4% de H et82,6 de C Le biogaz peut être purifié ensuiteen biométhane qui contient 80 à88 % de méthane Le biogaz qui estamélioré au standard de la qualitéréseau peut être inter-changé avec legaz naturel fossile.

Les véhicules au gaz naturel(NGVs)sont aujourd’hui la meilleurealternative et la plus économique parrapport aux carburants dérivés dupétrole. En utilisant le gaz natureldans le transport, on réduit les émissions de gaz nocifs et on réduitle bruit des véhicules.

Grâce à une technologie bienconnue, éprouvée et appliquée auxvoitures et aux véhicules commerciauxle gaz naturel peut être utilisé dansles moteurs à combustion internegrâce à un investissement minimeadditionnel. Le système dual-fuel diesel/LNG ou diesel/CNG offre la possibilité de convertir les moteursexistants

Le gaz naturel a été principalementutilisé sous la forme CNG pour desapplications urbaines, mais

également dans des voitures privées. Entre-temps, la mise à disposition deLNG étendra son utilisation pour desmoyennes et longues distances ,essentiellement pour des véhiculescommerciaux tels que camions, semi-remorques, etc.

En termes de transport moyen etlourd, tant le CNG que le LNG sontutilisés communément en Amérique,Asie et Europe mais aussi en Egypte,en Afrique. L’Egypte, nation piloteNGV, met ses espoirs dans le gaznaturel pour l’aider à réduire les subsides énergétiques qui consument20% du budget de l’état et qui continuent à grandir

Le gaz naturel dans lesvéhicules lourds

Dans le segment du transport parvéhicules lourds, le CNG est principalement utilisé dans les bus,tandis que le LNG et le Dual-Fuelsont utilisés dans les camions. EnRussie et en Chine cependant, ilspossèdent des bus publics au LNG.

En Afrique, à l’exception de l’Egypte,les intérêts sont plutôt dirigés vers leCNG utilisé dans les bus publics. Enutilisant ce carburant pour le transport

public des économies plus importantes peuvent être réaliséestant dans le domaine économiqueque le domaine écologique. En effet,les bus ont besoin d’une quantité plusimportante de carburant que les voitures. Mis à part cela, opérerrégulièrement des bus, exige unequantité de carburant stable et importante à approvisionner. Commele CNG est moins chère que le diesel,au plus on utilise du carburant auplus les économies sont importantes.

L’Algérie, la Tunisie, la Tanzanie et leMozambique ont réalisé des essaisde bus au CNG. Quoique le marchénigérien NGV se situe dans le segment voiture/taxi, diverses compagnies préfèrent voir le CNGdans les bus et même dans lescamioms.La compagnie NigérienneCoca-Cola a converti quelquescamions de livraison fonctionnant audiesel vers le système diesel/CNG.

Gaz-chariots

Juste pour donner quelques exemplesde l’utilisation des NG-HDVs dans lemonde et pas seulement au Nigeria,Coca-Cola a reconnu aussi l’avantagede l’utilisation du CNG dans ses

CNG.Other emissions comparisionBus GNV MAN en Allemagne

Comparaison entre le gaz naturel/biogazet le diesel pour véhicules lourds

Continue to page 8

August 20128

camions de livraison partout dans lemonde. Par exemple, cette année auRoyaume-Uni, la firme a acheté 14Iveco Stralis au gaz naturel, après unessai de 12 mois prouvant que lebiomethane peut réduire la pollutionde l’air et le bruit. Comme renseignéplus haut, le biométhane a lesmêmes caractéristiques que le gaznaturel. C’est pourquoi, aucun ajustement n’est à faire en passantdu CNG au biomethane dans n’importe quel véhicule CNG.

A la suite d’essais, les véhicules augaz atteignent une valeur estimée de50,3 % de bénéfice des émissionsde gaz à effet de serre well-to-wheel,comparé à un Iveco au diesel.Comme Coca-Cola envisage d’installer une station de remplissagede gaz naturel dans son dépôt deEnfield au bénéfice de sa flotte il estprévu que la compagnie pourraitréduire les émissions de gaz à effetde serre de 60,7 % .

La firme a aussi essayé un élévateurà fourche converti au biométhanedans son site de Enfield, lequel aatteint 71% de CO2 en moins well-to-weel.

Les Stralis au biométhane ont produit85.6 % en moins d’oxydes d’azoteet 97.1 % de moins de PM, comparés au camion au diesel et lebruit est réduit de 10.5 db les rendant plus agréable pour les livraisons tard le soir ou tôt le matin. Quoique les camions au gaz soientlégèrement plus coûteux que les versions au diesel, ceci peut êtreeffacé par les avantages du CNGou du biométhane. Partout dans lemonde, le prix du gaz est moinsélevé que le prix du diesel et du pétrol.

Le coût total des camions au gaz,propriété de Coca-Cola, pourraitaugmenté de 15.3%. Cependant lebiogaz est de 12.8% moins cher quele diesel au RU (Nord de Londres).

Mis à part diverses contréesd’Europe ( Espagne, Royaume-Uni,Suède, Pays-Bas, France et beaucoup d’autres ) les USA sontreconnus comme leader dans desHeavy-Duty NGVs avec beaucoupde flottes privées utilisant du CNG,du LNG ou du biométhane pour des

bus publiques ou d’écoles, desbennes à ordures ménagères ainsique des camions semi-remorquescommerciaux.

Mis à part les camions au CNG,l’industrie du NGV offre également lasolution dual-fuel diesel/méthane(CNG ou LNG). Pour la part duméthane, CNG ou LNG peuvent êtreutilisés dans le véhicule , ou encoredu biométhane liquéfié (LBG) ou dubiométhne comprimé (CBG).

En mai 2011, Volvo Trucks a introduit le Volvo FM Méthane Diesel, un camion roulant au gaz du type semi-remorque. La nouvelle technologie de ce camion permetune combinaison de 75% de méthane liquéfié et 25% de diesel, le diesel servant comme bougie d’allumage (assiste au processus decombustion) . Avec du biogaz dansle réservoir, les émissions de CO2sont de plus de 70% comparé aumoteur diesel conventionnel ; avec du gaz tel que le gaz naturel(gaz fossile) les émissions sontréduites de 10%.

Le système dual-fuel méthane/dieselest 30% à 40% plus efficient en énergie que le camion au gaz équipé de bougies classiques

Bus au gaz

En 2004, le Laboratoire Nationaldes Energies Renouvelables duDépartement US de l’Energie menait

une évaluation des émissions des‘’Transit buses’’ exploités par laWashington Metropolitan AreaTransit Authority (WMATA). Le projeta été mis en place dans le but d’évaluer les émissions des bus augaz naturel et les moyens d’augmenter les directives de basecomparées aux bus diesel par destechnologies possédant un contrôleprécis des émissions.

Les bus incorporés dans l’étudeétaient les suivants :• Bus CNG avec MY2004(annéedu modèle) moteurs John Deere6081Havec catalyseur d’oxydation• Bus CNG avec MY2001Cummins Westport ,Inc. (CWI) CMoteurs Gas Plus avec ca talyseurd’oxydation• Bus diesel avec MY2004 DetroitDiesel Corporation (DDC) Série de50 moteurs avec filtres à particulescatalysés et EGR• Bus diesel avec MY2000 DDCSérie de 50 moteurs avec filtres àparticules catalysés

Les bus CNG John Deere ont produit49% de moins de NOx et 84% demoins de PM comparés aux MY2004 DDC bus diesel et 63% demoins de Nox et 60% de moins dePM comparés aux MY 2000 DDCbus diesel.

Les moteurs CWI ont produit 6.1%de plus de Nox et 60% de moinsde PM comparés aux MY2004 DDCbus diesel et 23% de moins de Nox

Continued from page 7

August 2012 9

et l’équivalent en PM comparés auxMY 2000 DDC bus diesel.

En termes d’économie d’énergie, lesbus John Deere CNG ont montré ungain de 9% comparé aux bus équipés de MY 2004 DDC diesel et2.9% comparé aux bus équipés deMY 2000 DDC diesel. Les bus équipés de moteurs CWICNG ont montré une économie de4.2% plus élevée que les bus avecmoteurs MY 2004 DDC diesel et1.6% plus basse que les bus avecmoteurs MY 2000 DDC diesel. Lesbus au CNG utilisent la technologie‘’lean burn’’.

Les réductions d’émissions des bus au CNG diminueront encore quand:1. ils sont comparés aux bus dieselnon équipés de filtres à particules,et/où ;2. le biométhane est utilisé à laplace du gaz naturel ;3. Bus diesel sans filtres à particulessont utilisés comme des compara-isons.

Aux Pays-Bas , les filtres à particulespour moteur diesel ne sont plus subsidiés. Les filtres sont obstrués par

des PM en un temps record . Lorsquecela arrive, les filtres n’ont plus d’effet et plus spécialement quand ilsne sont pas régulièrement nettoyés.

Il a été conclu que les filtres diesel àparticules sont onéreux eu égard auprix du filtre et à sa faible durée devie comparés à ses avantages.

Plan de développement :l’exemple canadien

En 2010, plusieurs partenaires au

Canada ont lancé l’initiative NaturalGas Use in the CanadianTransportation Sector DeployementRoadmap. Comme résultat, un rapport portant le même nom a étépublié. Ce rapport décrit une méthode technique créée pour aiderles flottes à passer à l’utilisation dugaz naturel comme carburant.

Le rapport peut être obtenu :http://oee.nrcan.gc.ca/sites/oee.nrcan.gc.ca/files/pdf/transportation/alternative-fuels/resources/pdf/roadmap.pdf

Rail gets the world moving while helping the environment.

IG5 NOUME

RIZIG3 HORIZON

EA

IG1 APAACHPPAPA HE

August 201210

“Aardgas is een uitstekende energiedrager, met de laagste carbon/waterstofverhouding van allekoolwaterstoffen”, aldus de presentatie van NGVA Europa’sgeneral manager Manuel Lage. Het is een alternatieve brandstof uitnatuurlijke bronnen, die voornamelijkbestaat uit methaan (CH4).

De hernieuwbare vorm van dit gas,zogenaamd biogas, is methaan rijkdoor de fermentatie van de biomassa.

Methaan heeft minder koolstof moleculen in vergelijking met traditionele brandstoffen per gewicht.• Methaan: Koolstof (C) gehalte van75 procent• Benzine: Koolstof (C) gehalte van86.5 procent• Diesel: Koolstof (C) gehalte van86.5 procent• LPG: Koolstof (C) gehalte van82.6 procent

Door biogas verder te zuiveren verkrijgt men bio methaan wat eenmethaangehalte heeft van 80 tot 98procent (gewicht). De kwaliteit vanBiogas kan worden opgewerkt tot destandaard waarden voor pijplijn gasen is dan uitwisselbaar met aardgas.

Natural Gas Vehicles (NGVs) zijnvandaag het beste en het meest economische alternatief voor op oliegebaseerde brandstoffen. Met behulp van aardgas in het transport kunnen daarenboven deakoestische emissies van de voertuigen vermindert worden.

Dankzij een bekende en goed ontwikkelde technologie die al langer word toegepast bij auto`s enbedrijfsauto`s, kan aardgas, met eengeringe extra investering, wordengebruikt in bestaande verbrandingsmotoren. Dual Fuel, diesel / LNG of diesel /CNG-technologie, biedt die mogelijkheid tot omzetting van debestaande motoren.Aardgas is tot nu toe voornamelijkgebruikt als CNG voor stedelijke toe-

passingen en daar naast ook voorprive-auto’s. Tegelijkertijd is ook deverspreiding en beschikbaarheid vanLNG toe genomen waardoor de toepasbaarheid voor middellange enlange afstanden, vooral voor deHeavy-Duty Commercial Vehicles,zoals vrachtauto’s, trailers, enz,steeds verder verbeterd.In Amerika, Azië en Europa, maarook in Egypte worden zowel CNGen LNG veel gebruikt in het Medium-en Heavy-Duty transport segment. In Egypte, het grootsteNGV land van Afrika, hoopt mendoor het aardgas gebruik te bevorde-ren de kosten van energiesubsidiesop benzine/diesel te verlagen. De subsidie neemt nu 20 % van destaats uitgaven in beslag en dit zalwrs. nog verder toenemen bij uitblijven van oplossingen.

Aardgas in zware voertuigen

In het zware transport segment(HDV), wordt CNG voornamelijkgebruikt in bussen, terwijl de LNG-endual fuel systeem vooral zijn te vinden in zware trucks. Met uitzondering van Rusland en Chinawaar LNG-bussen in gebruik zijnvoor het openbaar vervoer.

In Afrika, met Egypte als uitzondering, zijn de belangen inCNG is vooral gericht op het openbaar vervoer-segment. Door toepassing van CNG in hetopenbaar vervoer, kan een belangrijke economische en ecologische besparingen gerealiseerd worden. Bussen hebben enerzijds grotere hoeveelheid brandstof nodig en rijden tevens een meer reguliere route(wat de implementatie vereenvoudigd).

Omdat CNG goedkoper is dan benzine en diesel, neemt de het economisch voordeel toe naar mateer meer brandstof wordt gebruikt.

Algerije, Tunesië, Tanzania enMozambique hebben proevengedaan met aardgasbussen. Hoewelde NGV markt in Nigeriaanse nunog vooral actief is in het auto /taxi segment, zien diverse partijengraag een toename van gebruik vanCNG in stads bussen of zelfs vrachtwagens. De NigeriaanseCoca Cola Company, is hier al opvooruit gelopen door een aantal vanhaar diesel vrachtwagens om te zetten naar dual fuel diesel / CNG-systeem.

Vergelijkende studie van aardgas /biogas ten opzichte van diesel HDVs

August 2012 11

Gas-aangedreven trucks

Om een voorbeeld te geven vanNG-HDVs gebruik in de wereld: Niet allen in Nigeria zag CocaCola de mogelijkheden van NG-HDV`s, Coca-Cola ziet ook eenvoordeel in het gebruik van CNG bijvrachtwagens in de rest van de wereld. Bijvoorbeeld, dit jaar in het VerenigdKoninkrijk, de firma kocht 14 IvecoStralis aardgas vrachtwagens envond, na 12 maanden onderzoek,dat bio methaan kan bijdragen aanvermindering van luchtvervuiling engeluidsoverlast. Zoals hierboven vermeld, heeft bio methaan dezelfdeeigenschappen als aardgasgas.Daarom is geen aanpassing nodig isom het gebruik van bio methaan inplaats van CNG in alle CNG-voertuigen mogelijk te maken.

In deze proef is een besparing (van“well-to-wheel”) in de uitstoot vanboeikasgassen, door gas aangedre-ven voertuigen, bereikt van naarschatting 50,3 procent in vergelijkingmet die van een Iveco diesel aangedreven voertuig. Als CocaCola een aardgas tankstation aanhet Enfield depot neer zet is te

verwachten dat het bedrijf de uitstootvan broeikasgassen nog verder kanverlagen tot 60,7 procent verminderde uitstoot.

Het bedrijf heeft bij de Enfield siteook een test gedaan met een vorkheftruck met bio methaan, dieeen CO-2 uitstoot vermindering van71 procent (well-to-wheel) liet zien.De Stralis bio methaan trucks lietenook een vermindering van de uitstootvan stikstofoxiden zien van maarliefst 85,6 procent gekoppeld aaneen vermindering van 97,1 procent vande uitstoot van fijn stof, in vergelijkingmet de diesel aangedreven truck. Ook was de lawaai productie met10,5 decibel verminderd, waardoorzij meer geschikt worden voor latenacht en vroege ochtend leveringen.Hoewel de gas-aangedreven trucksiets duurder zijn dan de diesel versies, kan dit ruimschoots wordengecompenseerd door de besparingenop de brandstof door het gebruikvan CNG of bio methaan. Over dehele wereld is de kostprijs van dezebrandstoffen nu eenmaal lager danvan diesel en benzine.

De totale kosten van gas-trucks

eigendom voor Coca-Cola zoudenmet 15,3 procent toenemen. Maarbiogas is 12,8 procent goedkoperdan diesel in het Verenigd Koninkrijk(Noord-Londen) en levert dus directebesparingen per kilometer op.

Naast diverse landen in Europa(Spanje, Verenigd Koninkrijk,Zweden, Nederland, Frankrijk envele andere), is ook Noord-Amerikabekend als de toonaangevendegebruiker van Heavy-Duty NGVs enprive-vloten met CNG, LNG en ookbio methaan veel toegepast in hetopenbaar vervoer, schoolbussen, vuilniswagens en lange afstandbedrijfswagens .

Afgezien van CNG trucks, bied deNGV-industrie ook dual fuel diesel /methaan (CNG of LNG) oplossingen. Voor het methaan deelkan CNG of LNG worden gebruiktof vloeibaar Bio methaan Gas (LBG)of Gecomprimeerd Bio methaan(CBG).In mei 2011 introduceerde VolvoTrucks, Volvo FM Methaan Diesel,een met gas aangedreven truck

Continue to page 12

THIRD EDITION

www.ngvjournal.us

Be part of a very special issueThe latest and most important facts

of the US & Canada NGV market.

Extraordinary distribution at:

HHP SUMMIT 2012

"Natural Gas for High Horsepower

Applications" September 26 - 28

Houston, TX.

1st NGVA Europe International

LNG Workshop

13th Biennial NGV Global

Conference and Exhibition

You cannot miss it!

Reserve your space:[email protected]+39-335-189-3249

Deadline: September 7th

» www.weh.com

» WEH® CNG FUELLING SOLUTIONSTop quality for maximum RELIABILITY

WEH® offers a wide range of NGV1 compatible products for safe and easy CNG vehicle refuelling:

» Fuelling Nozzles» Receptacles» Breakaways

» Check Valves» Filters» Hoses

Banamex Center Pavilion AMexico CityNovember 06-10, 2012 Booth #F17

Visit us at:

August 201212

ontworpen voor langeafstanden. De nieuwe technologie in dezeVolvo-truck kan een combinatie vanmaximaal 75 procent vloeibaarmethaangas en 25 diesel, aan.Waar bij de diesel als ontsteker/bougie fungeert (helpt bij een goedverbrandingsproces). Met biogas inde brandstoftank, kan de CO2-uitstoot dalen met 70 procentin vergelijking met een conventioneledieselmotor; en met 10% in vergelijkingmet het gebruik van aardgas.

Het dual fuel methaan / diesel systeem is 30 tot 40 procent meerenergie-efficiënt dan een conventioneel gas aangedreven truckuitgerust met bougies.

Gas-aangedreven bussen

In 2004 heeft de “US Departmentof National Renewable EnergyEnergy Laboratory” (NREL), een evaluatie van de emissies van stadsbussen van de “WashingtonMetropolitan Area Transit Authority“(WMATA) uitgevoerd.

Het project werd uitgevoerd om deuitstoot van aardgas stads bussen ende verbetering van de baseline-uitstoot van vergelijkbaredieselbussen met geavanceerde emissie technologieën, te evalueren.

De bussen in het onderzoek bestaan uit volgende:

• CNG bussen met modeljaar (MY)2004 John Deere 6081H motoren,met een oxidatiekatalysator• CNG bussen met MY 2001Cummins Westport, Inc (CWI) CGas Plus motoren, met een oxidatiekatalysator• Diesel bussen met MY 2004Detroit Diesel Corporation (DDC)Series 50 motoren, met gekatalyseerde roetfilters en EGR• Diesel bussen met MY 2000 DDCSeries 50 motoren, met gekatalyseerde roetfilters.

De John Deere aardgasbussen produceerde 49 procent minderNOx-uitstoot en 84 procent lagerefijn stof emissies in vergelijking metde MY 2004 DDC dieselbussen eneen 63 procent lagere uitstoot vanNOx en 60 procent lagere emissies

van fijn stof in vergelijking met deMY 2000 DDC dieselbussen.

De CWI bussen produceerden 6,1procent hogere NOx-uitstoot en 60procent lagere emissies van fijn stofin vergelijking met de MY 2004DDC dieselbussen en 23 procentlagere uitstoot van NOx en gelijkePM-emissies in vergelijking met deMY 2000 DDC dieselbussen.

In termen van brandstofverbruik: de John Deere aardgasbussen toonde een 9 procent verbetering tenopzichte van de MY 2004 DDC dieselbussen en een 2,9 procent verbetering ten opzichte van de MY2000 DDC dieselbussen.

Het CWI CNG bussen vertoondeneen lager brandstofverbruik 4,2 procent hoger dan de MY 2004DDC dieselbussen en 1,6 procentlager dan het MY 2000 DDC dieselbussen. Beide CNG motorenmaken gebruik van lean burn technologie.

De emissiereducties van CNG voertuigen zal toenemen wanneer:

1. Deze worden vergeleken met dieselbussen zonder roetfilters en / of 2. Bio methaan wordt gebruikt inplaats van aardgas.3. Diesel bussen zonder roetfilter

worden gebruikt als vergelijking.Anderzijds wordt in Nederland hetgebruik van roetfilter niet langergesubsidieerd.

De diesel roetfilters in een redelijkkorte tijd worden gevuld met PMwaarna de werkzaamheid van de filters niet meer optimaal is, het geennog sterker het geval was als de filters niet regelmatig worden gereinigd.

De conclusie was dat de roetfiltersvrij duur zijn t.o.v. de te behalenvoordelen (verminderde roet uitstoot) ende te verwachten levensduur product.

NGV inzet kaart: DeCanadese voorbeeld

In 2010, hebben belanghebbendenuit het Canadese bedrijfsleven het initiatief “The Natural Gas Use in theCanadian Transport Sector” (aDeployment Roadmap) genomen.

Hier bij werd een rapport met dezelfde titel vrijgegeven. Het rapport beschrijft een technische richtlijn die gemaakt is om de overgang van vloten naar NaturalGas Vehicle te vergemakkelijken.Het rapport kan worden verkregen bijhttp://oee.nrcan.gc.ca/sites/oee.nrcan.gc.ca/files/pdf/transportation/alternative-fuels/resources/pdf/roadmap.pdf

Continued from page 11

August 2012 13

Globally, around 25.4 million Light-Duty Natural Gas Vehicles (LD-NGVs) would run across theworld, according to Pike Research’sforecasts. This global-market-researchcompany has projected that sales ofLD-NGVs, including passenger cars,light-duty trucks and commercial vehicles will reach 3.2 million vehicles in 2019. This represents acompound average annual growthrate (CAGR) of 6.2 percent between2012 and 2019. By July 2012, justover 15 million LD-NGVs around theworld were recorded by the GVRstatistics (see also the statistics pageof NGVAfrica).

The Light-Duty segment in the totalNGV sales of 2012 is projected tomake up about 97 percent, or 2.08million out of 2.15 million vehicles.Four main growth drivers were identified, which include economicbenefits, environmental benefits,availability of fuel and vehicles, andenergy security.

Strongest NGV region, Asia-Pacific,is expected to continue leading, withThailand (24 percent CAGR), India(23 percent) and China (20 percent)being in the front rows, whilePakistan experiencing a volatility. North America is reported to experience 10 percent CAGR. The market largely consists of fleetpurchases, not individual consumers.A two percent CAGR between 2012and 2019 is anticipated for theMiddle East and Africa regions.Egypt is well-known as a relativelystrong light-duty vehicle market due toits taxi fleets.

The Latin American market will continue to grow. The two biggestnations in the region, Argentina andBrazil hold 25 percent share of theworld’s total NGVs population. The other markets in this region areforecasted to have combines sales ofless than 100,000 vehicles in2012. The company forecasts about10 percent CAGR each inColombia, Bolivia, Peru, andVenezuela over the next severalyears. Other report by Infinity

Research projected a total of 6.8 million NGVs (sales and conversionof all types vehicles) by 2015. Seemore notes about this below.Leading market in Europe, Italy, isexpected to witness 159,046 NGVsin 2012 sales. The sales in Ukraineare expected to reach 151,487units. Both countries will see slowedgrowth over the next few years,while Germany and Sweden will seea steady growth.To get this Pike Research report,please check http://www.pikere-search.com/research/light-duty-natu-ral-gas-vehicles

Meanwhile, TechNavio, anotherresearch firm, forecasted 19.8 million NGVs will ply around theglobe by 2015. This figure wouldrepresent the total NGV population-not only sales of LD-HDVs.It means, around 3.4 million wouldbe added to the current NGV population (16.4 million by July2012). Economic benefits/savingsaccumulated from using compressednatural gas is recognized as one of

the main drivers of the industrygrowth, while inadequate refuellingnetwork seen as the biggest challenge. To read more aboutTechNavio report on “GlobalCompressed Natural Gas VehicleMarket 2011-2015”, visithttp://www.theautochannel.com/link.html?http://www.researchandmar-kets.com/research/trcqq3/global_compressed.

Infiniti Research recently published areport entitled “The CompressedNatural Vehicle market in LatinAmerica”. According to the report,the region is expected to have 6.8million units of NGVs by 2015.

One of the key factors contributing tothis market growth is the cost advantage of using compressed natural gas. The NGV market in LatinAmerica has also been witnessing anincreasing number of bi-fuel vehicles.To get this report, visit http://www.reportstack.com/product/86136/cng-vehicle-market-in-latin-america-2011-2015.html

Around 25.4 million LD-NGVs sales projected for 2019

August 201214

In light of the large-scale plans toexpand the service to wider areasacross the nation, that number of filling points have been inauguratedso far this year. Six of them are located in the public transport depots affiliated to Cairo & AlexandriaTransport Authorities, serving bothpublic buses –the facilities are well-equipped to fuel 600 buses perday at the first phase- and the privatevehicles.

A new fueling station was alsoopened in Minya Governorate (southof Egypt). The distribution networkwas extended a couple of years agoto Upper Egypt, which made it easier to establish several natural gas projects including the installation ofCNG dispensing points.

"Setting up new CNG stations isshowing so far the success and theon-going development of NGV activities in Egypt, which started in1996. Besides, further plans andcampaigns will be potentiallydevised to encourage convertingvehicles and buses to CNG," theEgyptian Minister of Petroleum Eng.

Abdullah Ghorab said. By the end ofJune 2012, the number of naturalgas fueling stations hence reached159 and the CNG-converted vehicles amounted to over 173,000.

To ensure a wider spread of NGVuse in the country, the gasoline stations are incorporating CNG fueling within their premises. On the other hand, cooperation withthe vehicles assembling and manufacturing companies in Egypt isunderway in order to convert vehiclesto run on CNG on the productionlines, in the context of the nationalproject of replacing the old taxi cabswith new ones powered by CNG.Hyundai, BYD and Chevrolet are thefrequent models used in this segment.

The Egyptian NGV authorities havealready strengthened the main safety

measures to ensure a safer operationof NGVs. They include testing theCNG cylinders installed in the converted vehicles, which is quite an important procedure to achievethe standard safety objectives. As a result, over 72,000 cylinderswere tested till end of year 2011.

Other serious measures are beingtaken nowadays to cut the huge subsidies directed mainly to gasolineand diesel fuels, and that is why theCNG is seen as the best option dueto its cheap price and availability.

Source: Hamdy Kamal, Gastec

Egypt opened eight NG fueling stations during the first half of 2012

Newly opened CNG station in Basateen area in Cairo City

Egyptian Minister of Petroleum & Cairo governor while opening new CNG station

August 2012 15

AutomotiveWorld.com has recently published a brand new vehicle sales forecast entitled 'South Africa’s newvehicle market - prospects to 2016'.A member of the BRICS group ofnations since Brazil, Russia, Indiaand China invited it to join them in2010, South Africa’s economy isgrowing at a much slower rate thanthose other emerging markets; it alsohas a much smaller population.

In 2011, the South African vehicle market rose by over 19 percent to587,500 cars, trucks and buses.The report presents information of:- Socio-political and macro-economicdata, as well as historic overview of thecountry and a summary of the country'svehicle market;- Examination of the passenger and commercial vehicle markets in 2011,with insight into the prospects forthese markets;- Historical data from 2007, with a forecast to 2016.

To obtain a copy of this forecastplease visithttp://www.automotiveworld.com/forecasts/sales-forecast-south-africa-s-new-vehicle-market-prospects-to-2016

SouthAfricavehicleprospect2016

African’s leading NGV country,Egypt, continues actively expandingNGV services to wider areas.Hence, the Egyptian NGV authoritiesset ambitious plans for the enlargement of CNG filling stationnetwork including the construction of30 new stations across the countrywithin this year.

Three new CNG stations werealready opened in early May 2012.Two of those are located in a publictransport garage in Basateeen areain Cairo City. The stations serve bothpublic buses and private vehicles.The third filling facility will be built inSuez City.

Also, around 24,000 NGVs isplanned to be added. The Egyptianstakeholders seek to have more than187,000 NGVs to ply on the roadsby the end of 2012.

Given the significant (long) queues ofvehicles waiting to be refueled inpetrol stations, motorists are lookingat CNG as the best possible alternative to petrol and diesel.Serious studies are being preparedand submitted to the authorities tospeed up the wide scale improved-NGV- adoption, with extrafocus given to the public transport. Every year, the government offershuge funding to subsidized users ofliquid fuels (petrol and diesel), resulting in a significant budgetdeficit. Thus, energy experts advisethe government and public to switchto CNG. Egypt has a successfulexperience in the NGV segment. Italso has the potentials to be one ofmajor NGV countries in the future.

By: Hamdy Kamal, Board AffairsDepartment, Egyptian InternationalGas Technology (Gas Tec)

Egypt plans to add24,000 NGVs in 2012

Newly opened CNG station in Basateen area in Cairo City

August 201216

A MULTIMEDIA PORTAL IN THE SERVICE OF THE INDUSTRY

Subscribe now !

NGV JOURNAL, THE FIRST WORLDWIDENGV NEWSPAPER

SUBSCRIBEONLINE

FOR FREE

www.ngvjournal.com

.com

HAVE UNLIMITED ACCESS TO OUR MAGAZINES

ngvjournal.com

CNG filling station investors inMozambique plan to build two morestations, hoping to increase the NGVadoption rate in the country.Currently, there are two CNG stations in Maputo and Matola.Maputo is the capital and largest cityof Mozambique, while Matola city insouthern Mozambique lies 12 kilometersto the west of the capital city.In July 2011, there were 433Natural Gas Vehicles (NGVs) in thecountry.By July 2012, 500 bifuel Light-DutyVehicles/cars and 150 CNG busesrun across these two cities.The CNG buses are made byOriginal Equipment Manufacturers(OEMs)/bus producers, while theLight-Duty ones are after-market conversion vehicles.In average, 0.24 million NM3CNG are used by those NGVs in2012.Petrol is sold at 47.62 MZN/liter,

diesel at 36.81 MZN/liter, andCNG at 17.75 MZN/kg, accordingto Stephan de Vos from Gigajoule.The lower heating value of each fuelsis 8.80kWh, 10,00kWh, and10.40 kWh respectively. It means,

the cost of petrol is 0.16MZN/kWh and 0.11 MZN/kWhfor diesel. For CNG, the cost perkWh is only 0.05 MZN, making itthe cheapest fuel for transport sectorin this regards.

Mozambique to add two morestations soon

Sales and subscriptions300-5, Changchon-Ri Namsan-MyunChuncheon-Si Kangwon-Do200-911 Tel. and fax.: +82 33 260 3456

The pioneer and no. 1 specialized NGV magazine for Asianregion including theMiddle East

Expand and intensify your sales in Asia, the world’s biggest NGV market,home to 54% NGVs & 51% NG stations. Advertise in Asian NGVCommunications.

Volume V Number 55 September 2011

LNG standards

The available

standards and those

in the making

LNG and LCNG

Consumer experiences

in the fueling and

vehicle segments

LNG and LCNGtechnology andchallenges

August 2012 17

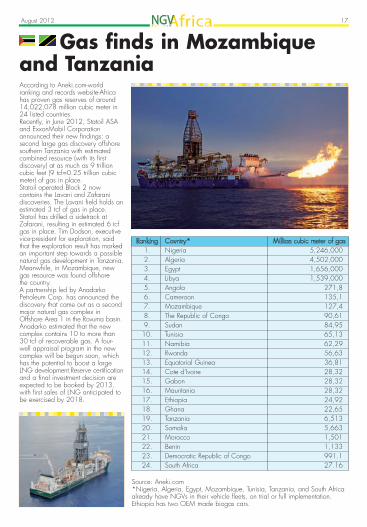

Gas finds in Mozambique and TanzaniaAccording to Aneki.com-world ranking and records website-Africahas proven gas reserves of around14,022,078 million cubic meter in24 listed countries.Recently, in June 2012, Statoil ASAand ExxonMobil Corporationannounced their new findings: a second large gas discovery offshoresouthern Tanzania with estimatedcombined resource (with its first discovery) at as much as 9 trillioncubic feet (9 tcf=0.25 trillion cubicmeter) of gas in place.Statoil operated Block 2 now contains the Lavani and Zafarani discoveries. The Lavani field holds anestimated 3 tcf of gas in place.Statoil has drilled a sidetrack atZafarani, resulting in estimated 6 tcfgas in place. Tim Dodson, executivevice-president for exploration, saidthat the exploration result has markedan important step towards a possiblenatural gas development in Tanzania.Meanwhile, in Mozambique, newgas resource was found offshore the country. A partnership led by AnadarkoPetroleum Corp. has announced thediscovery that came out as a secondmajor natural gas complex inOffshore Area 1 in the Rovuma basin.Anadarko estimated that the newcomplex contains 10 to more than30 tcf of recoverable gas. A four-well appraisal program in the newcomplex will be begun soon, whichhas the potential to boost a largeLNG development.Reserve certificationand a final investment decision areexpected to be booked by 2013,with first sales of LNG anticipated tobe exercised by 2018.

Ranking Country* Million cubic meter of gas1. Nigeria 5,246,0002. Algeria 4,502,0003. Egypt 1,656,0004. Libya 1,539,0005. Angola 271,86. Cameroon 135,17. Mozambique 127,48. The Republic of Congo 90,619. Sudan 84,9510. Tunisia 65,1311. Namibia 62,2912. Rwanda 56,6313. Equatorial Guinea 36,8114. Cote d’Ivoire 28,3215. Gabon 28,3216. Mauritania 28,3217. Ethiopia 24,9218. Ghana 22,6519. Tanzania 6,51320. Somalia 5,66321. Morocco 1,50122. Benin 1,13323. Democratic Republic of Congo 991.124. South Africa 27.16

Source: Aneki.com*Nigeria, Algeria, Egypt, Mozambique, Tunisia, Tanzania, and South Africaalready have NGVs in their vehicle fleets, on trial or full implementation.Ethiopia has two OEM made biogas cars.

August 201218

A subsidiary of state-owned NigerianNational Petroleum Corporation,Nigerian Gas Company Limited(NGC), in July 2012 re-instated itscommitment to develop CNG-for-vehicles market in Nigeria.NGC managing director SaiduMohammed confirmed the company’stotal commitment to the promotion ofalternative vehicular fuel to increasegas consumption in Nigeria.The commitment is largely accountedfor a Joint Venture (JV) betweenGreen Gas Limited with the NigerianIndependent Petrol (NIPCO). TheseJV acts as a platform for building gasinfrastructure that could help developing the CNG market in linewith the gas master plan.During his visit to NIPCO’s CNG station in Apapa-the major port ofLagos City-Mohammed said that thecompany had provided reliableinfrastructure that could help CNGadoption in transport sector acrossthe country.Mohammed, who is also the chairman of Green Gas, feels gladthat the on-going expansion in thecompany led to construction of moreCNG filling stations in Nigeria.He found that the more platformswere created for gas utilisation, thebetter for the country as Nigeria hasan abundant gas resources. He indicated NGC’s willingness tosupport willing partners like NIPCOto develop NGV businesses whilestimulating economic growth at thesame time.Mohammed also underlined thatthanks to good management of theterminal/station-described as the bestever seen during his serve as depotmanager in the Nigeria NationalPetroleum Company (NNPC)-NIPCOdepot ranks the greenest.The Apapa station has a seamlessoperation, also thanks to its highlevel of automation.NIPCO Plc’s managing directorVenkatapathy Venkataraman said thatthe firm was very passionate aboutthe Oil & Gas industry in which thefirm has invested hugely in this regard.Venkataraman said that governmentinitiative in promoting CNG as transport fuel would improve domestic

consumption of gas and reduce fuelsubsidy on petrol.Earlier in November 2011, NIPCOannounced a plan to provide CNGin 5,000 tank stations with its part-ners and over 100 NIPCO dealerstations across Nigeria.Using CNG in cars would allow 50percent savings in fuel costs whileenhancing the air quality.The NGC-NIPCO JV had completedsix CNG stations in Benin, Edo

NGC underlined its commitment topromote Compressed natural gas

State, serving more than 250 CNGtaxis.

Ibrahim Njiddah, senior special assistant to the President on EnergyPartnership, Applauded NIPCO during his past visit, “Your efforts inchampioning the use of CNG andLPG as auto fuel is promising andyour expansion programmes in theindustry should be made realisableand reality in no distant future”.

Nigerian government ended oil subsidy early this year. Hence, prices ofpetroleum fuels increased significantly. This move could encourage motoriststo switch to bifuel CNG should sufficient refuelling network be available

August 2012 19

About NGC

The Nigerian Gas CompanyLimited (NGC) was establishedin 1988 as one of the 11 subsidiaries of the NigerianNational Petroleum Corporation(NNPC). It is charged with theresponsibility of developing anefficient gas industry to fullyserve Nigeria’s energy andindustrial feedstock needsthrough an integrated gaspipeline network and also toexport natural gas and itsderivatives to the West AfricanSub-region. NGC is committedto adding value to natural gasand making it an energyresource of first choice for thebenefit of all stakeholders. The company was initially established to efficiently gather,treat, transmit and marketNigeria’s natural gas and its by-products to major industrialand utility gas distribution companies in Nigeria andneighbouring countries.In other to deliver efficient services to the numerous customers the business philosophy has been reviewedto focus on Transmission,Distribution and Marketing ofNatural Gas.

About NNPC

The NigerianNationalPetroleumCorporation(NNPC) is the

state oil corpora-tion through which the federalgovernment of Nigeria regulatesand participates in the country'spetroleum industry.

[email protected] // www.ngvjournal.com

Bet on NGV trucksSpecial report on the main variants

Obama: $1 billion fundfor clean fuels

More firms joinNational Clean

Fleets Partnership

OEM-madenatural gas

cars andpick-ups

hit the USmarket

MARKETS & MORE

::: WM opens Illinios’ largestcommercial station

::: Trillium CNG teams up with Golden Eagle

::: Frito-Lay will deploy 67 CNG trucks

Second Edition – May 2012

2012 NGV HighlightsPLEASE KEEP THESE IMPORTANT DATES IN MIND FOR YOUR BUSINESS:

Extraordinary distribution at:

HHP SUMMIT 2012 "Natural Gas for High Horsepower

Applications" September 26 - 28 Houston, TX.

1st NGVA Europe International LNG Workshop

Deadline: September 7th

1st NGVA Europe International LNG WorkshopLNG - Dual Fuel - LBG for transport

19 – 21 September 2012Hotel CASA400, Amsterdam, The Netherlands

An event of Host / Sponsor Diamond Sponsor Silver Organized by

1st NGVA Europe International LNG Workshop

LNG – Dual Fuel – LBG for vehiclesHotel CASA400, Amsterdam,

The Netherlands

September 19-21, 2012

13th Biennial NGV Global Conference and Exhibition

NGVs, fuelling global transportation encouraging saving and ecology

Centro Banamex, Pavilion A, Mexico City

November 6-10, 2012

GothenburgSweden

11-13JUNE2013

Organized by

®

Sponsor Gold

®

Hosted by

®

The Swedish Exhibition & Congress Centre/Svenska Mä[email protected]

GothenburgSweden

11-13JUNE2013

4th NGVA Europe International Show & WorkshopsNatural Gas Vehicles – Biomethane - CNG – LNG – Hydrogen Blends

The fuel alternative for all transports

L-CNG. Bio & natural gas.

An event of

®

4th NGVA Europe International Show & Workshops

Natural Gas Vehicles – Biomethane –CNG – LNG – Hydrogen Blends

The Swedish Exhibition & CongressCentre/Svenska Mässan

June 11-13, 2013

NNPC tower, the mother company of NGC Limited

August 201220

A new IGU report on NGVs is releasedThe International Gas Union’s (IGU’s) Study Group 5.3(SG5.3), which operates under Working Committee 5 –‘Utilisation’ (WOC 5) recently presented a report onNGV market with 2012-2015 agenda.

Together with the United Nations Economic Commissionfor Europe (UN ECE) Working Party on Gas, the SG5.3,released a joint 2009-12 report.

According to NGV Global article, a big chunk of thereport discussed about NGV market profile of variouscontinents and countries, but also the respective regulations, government support, important technologicaltrends, cylinder, refuelling and other equipment, etc.Collectively, growth of natural gas vehicles (NGVs) worldwide is more than 12 times that recorded for 2000.

The report cites three examples of rapid change:• Iran has joined Pakistan at the top of the country list forNGV population• India has listed 201 cities where CNG and LPG facilities will be installed in coming years and hasattained 5th place by NGV population• China, a relative newcomer to the NGV market, hasincreased domestic and imported supply of natural gasand has more than 60 original equipment manufacturers(OEMs) producing NGVs.

This report also presents the stories and facts on LNG-for-marine segment that include bunkering, etc.

SG5.3 will commence a new three-year period under theleadership of Mr Olivier Bordelanne (GDF Suez). The group will endeavour to fulfil its declared objectivefor 2012-2015: “To advocate expansion of the use ofnatural gas by on- and off-road, marine/inland waters,airborne, railroad, farming vehicles thus making worldmobility cleaner, safer and cheaper”.

All NGV related stakeholders around the world are invited to participate in SG 5.3. To join this unit, contactthe Study Group Chairman, Mr Olivier Bordelanne –[email protected] — or the Vice ChairmanMr David Graebe – [email protected]— for details of how to participate.

The IGU Working Committee 5 – Utilisation Of Gas:Study Group 5.3 – Natural Gas Vehicles (NGV) and UNECE Working Party On Gas – Joint Report is available athttp://www.ngvglobal.com/docs/IGU_Final_NGV_Report_2012.pdf

General information about IGU’s activities over the pastthree years is available by downloading the IGU’sTriennial Work Programme 2009-2012 – Gas:Sustaining Future Global Growth, available athttp://www.wgc2012.com/assets/pdf/TWP_2009-2012.pdf

IGU International Gas Union

UN ECE United Nations Economic Commission fEurope

NATURAL GAS FOR VEHICLES (NGV)

June 2012

IGU WORKING COMMITTEE 5 UTILISATION of GAS

STUDY GROUP 5.3 NATURAL GAS VEHICLES (NGV)

and

UN ECE WORKING PARTY ON GAS

JOINT REPORT

national Gas UnionInter

national Gas Union

national Gas UnionInter

Global Gr“Gas: Sustaining Futur2009 - 2012WORK PROGRAMMETRIENNIAL

national Gas Union

owth”Global Gr“Gas: Sustaining Futur2009 - 2012WORK PROGRAMMETRIENNIAL

e urre

WORK PROGRAMME

Global Gr

owth”Global Gr

Kuala Lumpurorld Gas Confer25th W

YSIAMALAAYenceorld Gas Confer

4 - 8 June 2012Kuala Lumpur

4 - 8 June 2012YSIA, MALAAYurr,

NATURAL GAS FOR VEHICLES IGU & UN ECE JOINT REPORT

Methane (NG/biomethane) vehicles already meet the next EU goals today

As part of its strategy to cut CO2 emissions from light-duty vehicles, in May 2011 the EUadopted legislation to reduce emissions from vans (light commercial vehicles), passed in 2009 for passenger cars. The Van Regulation will cut emissions from vaverage of 175g CO2/km per kilometre by 2017 with the reduction phased in from 2014 and to 147g CO2/km by 2020. These cuts represent reductions of 14% and 28% respeccompared with the 2007 average of 203 g/km. Only the fleet average is regulatemanufacturers will still be able to make vehicles with emissions above the limprovided these are balanced by vehicles below the curve. The EU fleet average owill be phased in between 2014 and 2017. In 2014 an average of 70% of each manufacturer's newly registered vans must comply with the limit value curve setlegislation. This proportion will rise to 75% in 2015, 80% in 2016, and 100% fronwards. In the case of heavy duty vehicles, it is much more complicated for the EuropeCommission to legislate on CO2 emissions, as manufacturers still try to avoid releasiemission data, also due to the fact that CO2 emissions in a heavy duty vehicle are much related to the type of use, load factor and road profile, all very variable elof-the-art heavy duty trucks with dedicated engines running on natural gas and bioa tank-to-wheel basis, give a CO2 saving of about 3% versus diesel vehicles, but next generation of NG heavy engines with in Multiair type technologies) will improve the saving up to 8%. Dual fuel heavy engines also aimportant CO2 emission reductions. The whole picture changes completely when considering the entire life cycle on ll-to-wheel basis, which is not yet applicable for Europe, as European legislation itailpipe emission only. This is also the main reason why retrofitting in Europesense, because the CO2 benefit, with respect to the engine setting, is much betterfactory produced NGVs instead of converting OEM petrol versions to gas. The application of Euro VI in 2014 reinforces the relevance of environmental anbenefits via CNG and LNG, especially in HD trucks and buses. Euro VI will mark important step as the pollutant emission reductions required by this standard

The energy industry has witnessed rapid and dramatic changes in recent years, following huge swings in the global economic cycles. With the recent global economic and financial crisis weighing heavily on businesses, industries and the populace as a whole, the demand for energy has been in sharp decline, resulting in long-term impact on future investment growth, not only for the gas industry but also other key sectors of the economy.

Reflecting the global nature of the gas industry, the Presidency of the IGU shifts to Asia for the second time in its history. With more than half the world’s human population, relatively low energy intensity and areas of potentially very high economic growth, there is a challenge for Asia which is of interest to the whole world. The Malaysian Presidency will continue to maintain the high standards of excellence of the predecessors to support the mission of IGU and in striving to achieve the vision of being “the most influential, effective and independent non-profit organisation, while serving as the spokesman for the gas industry world-wide”. In this respect, IGU needs to continually reinvent itself to remain relevant to the industry and its members. Efforts to change the organisation and strategies have been initiated and some of these changes will be made during the Malaysian triennium.

Natural gas will continue to play a vital role in meeting the world’s expanding energy needs while helping to cut greenhouse gas emissions, a persistent threat to global growth, life and environmental sustainability. Despite intense interests to accelerate the development of ‘green energy’ for the creation of low carbon economy, natural gas is expected to continue its dominance as the fuel of choice in the coming decades.

This is primarily driven by its premium as an abundant and clean source of energy that is

forewordfrom the IGU President

Datuk (Dr) Abdul Rahim HashimPresident, IGU

being delivered to consumers via advanced technology and infrastructure fully supported by global expertise. Furthermore, constant innovation and technology breakthroughs have continued to enhance natural gas future sustainability from the economic, social, technical and environmental aspects that will significantly contribute towards the global economic growth.

Against this backdrop, the Malaysian IGU Presidency has set the theme “Gas: Sustaining Future Global Growth” as the foundation for the work during the 2009-2012 Triennium. The theme inherently portrays gas as the engine for global growth which has to be sustained in its availability through innovation, technology and competent human capital.

Despite the challenges brought about by the crises, we are confident that the IGU will be able to ride out the storm and turn them into opportunities and upsides for the benefit of the global community. Issues such as global warming and climate change, technology and innovation, geopolitics as well as talent sourcing and management for the gas industry will remain at the forefront. We are committed to promote a constructive intellectual discourse in addressing these issues, provide reference tools for decision makers, strengthen networking and relationship building and add value to all our members.

I am confident that with the full and continuous support from members of the IGU and its fraternity, the Malaysian Triennium will be able to steer the IGU towards greater heights and a promising future for the world.

FOR VL GASARTUAN

IHE FOR V SELC &UIG EC ENU

TROPET RIN JO

These strategic guidelines are briefly explained below: 4.1 Enhancing the role of gasGas is in an increasingly complex and competitive global market in which there are regional differences in the fuel mix and the sectors that prefer the use of natural gas. Globally and locally there is a strong interplay with the cost/price, availability/ reliability and environmental impact of other primary fuels. In recent years, the industry has come under tremendous pressure as the perception of natural gas has shifted in the light of growing environmental concerns and the evolution of energy companies. In fact, the industry is at a cross road and there is a strong need for a coherent voice and a consistent message on natural gas as the industry establishes its role in the future in a carbon constrained world. IGU is in a strong position to be the advocate to enhance the role that natural gas plays to achieve widely sought objectives of enhanced security of energy supply, improved economic performance and in particular to mitigate the environmental impact of climate change. Although some answers may well have a different emphasis throughout the world, these regional issues need to be investigated and communicated clearly. But climate change is a

the strategic guidelines

4

ROLE OF GASSustainability

IntegrityGas Advocacy

GAS:SUSTAINING

FUTURE GLOBALGROWTH

SUPPLYImprove availabilityAccess to markets

DEMANDMaximise efficiency

Expand usage

Geo-politics

ClimateChange

HUMAN RESOURCECapacityCapability

Future generations

The above diagram illustrates the Strategic Framework of the Malaysian triennium. It summarises the Theme and Strategic Guidelines which forms the basis for the development of the Triennial Work Programme.

The four Strategic Guidelines are as follows:

1) Enhance the role of gas for sustainable development and balancing the needs of all stakeholders

2) Improve availability of gas and access to markets 3) Maximise efficiency throughout the expanding gas value chain

4) Ensure adequate human capability to enable growth and integrity of the industry

Promoting understanding and awareness of the problems and solutions in these four areas will provide decision makers, both inside and outside the industry, with a powerful foundation to take the actions that will help build and sustain regional and global growth.

NATURAL GAS FOR VEHICLES IGU & UN ECE JOINT REPORT

CNG stations in 2020 located at the highways and motorways

CNG stations in 2020 in relation to European transport corridors

However the situation may improve if new filling stations will be located in tlocations, the network of Polish CNG refueling stations will not be still totainvestments will be needed, especially along express roads and in Northern andPoland.

Committee Chairs during the 1st CC meetingin Kuala Lumpur on 10 - 11 February 2009

1

2

3

4

5

6

7

8

9

10

11

12

1314

15

1. Ungku Ainon, Secretary CC

2. Datuk Rahim, President

3. Ieda Gomes, TF 1

4. Ho Sook Wah, Chairman CC

5. Tengku Nasariah, TF 2

6. Helene Giouse, WOC 2

7. Tatsuo Kume, WOC 5

8. Eric Dam, WOC 3

9. Joao Toledo, PGC C

10. Dr Colin Lyle, PGC B

11. Kamel Chikhi, WOC 1

12. Juan Puertas, PGC A

13. Alessandro Soresina, WOC 4

14. Marc Hall, PGC E

15. Dirk van Slooten, PGC D

Not in picture

Alaa Abu Jbara, PGC D

Mel Ydreos, TF 3

August 2012 21

Cheaper and more convenienceCNG home refuelling appliancein development

CNG home refueling is not a newtechnology. US-based BRCFuelMaker, Japan and Czech manufacturers, etc have been offering this product for many years.The presently existing appliance (alsoso-called Vehicles RefuelingAppliance or VRA) is sold at aroundUSD5,000 per unit and requireslong filling times that normally doneovernight. Mind you that today’sCNG station have a fast-fill refuelling time (around 3-5 minutes to refuel a car), while the home-refuelling with low input-gaspressure and limited compressioncapacity has a slow-fill mode, andthus, takes around 5 to 8 hours torefuel a vehicle.However, GE is developing a uniquefueling approach that would replacemore expensive and complex compressor technologies used today.The initial target market includes fleetvehicles owners, with an eye to owners of passenger vehicles (private individual) in the future.

New York based multinational conglomerate corporation General Electric (GE) is developinga quick fueling system for Natural Gas Vehicles (NGVs) as part of an Advanced ProjectsResearch Agency-Energy (ARPA-E) to improve CNG refuelling experiences. The new CNG-home-fueling system is expected to attract average consumers, speed up andwidespread NGV adoptions in the US and around the world. The new system would allow an affordable and more convenient refuelling option.

by ARPA-E and GE. GE will be partnering with Chart Industries andscientists at the University of Missourito complete the program.GE researchers will focus on overallsystem design integration. ChartIndustries and University of Missouriwill take care the detailed engineering, cost and manufacturability of the key systemcomponents. On the other hand, GE recently introduced the CNG In A Box™technology which takes natural gasfrom a pipeline and compresses iton-site at an industrial location or ata traditional automotive refilling station to then turn it into CNG, making it faster, easier and lessexpensive for users to fuel up naturalgas vehicles.

About GE Global Research

GE Global Research is the hub oftechnology development for all ofGE's businesses. Our scientists andengineers redefine what’s possible,drive growth for our businesses andfind answers to some of the world’stoughest problems. We innovate 24 hours a day, withsites in Niskayuna, New York;Bangalore, India; Shanghai, China;Munich, Germany; and fifth global

research facility to open in Riode Janeiro, Brazil. Visit GE

Global Research on theweb atwww.ge.com/research.Connect with our technologists at http://edisonsdesk.comand http://twitter.com/edisonsdesk.

The newly developed system of GEis expected to reduce refuelling system cost by 10 times. The product is expected to cost asmuch as USD500 per unit only,according to ARPA-E’s target. Also,the fuelling time is anticipated to bekept under one hour. This unit can be installed in the driveway or garage at home. This aspect alone would reduce landcosts required to install commonCNG station.The system is designed to chill, densify and transfers CNG more efficiently. It will be a much simplerdesign with fewer moving parts, andthat will operate quietly and be virtually maintenance-free. Once mass marketed, the new system would be able to reduce thebarriers to NGVs adoption: refuelinginconvenience and low availability ofrefueling stations. CNG home refuelling appliance is mainly suitablefor areas with gas pipeline connection. Otherwise, a separategas storage tanks are required tosupply the fuel to the appliance.The 28-month project that requires

USD2.3 million will be funded

August 201222

Company and productBook your table-tops and seats at the LNG4Trucks&Ships

Register your workshop participationbefore 15 July and meet the “crèmede la crème” stakeholders.

The Dutch and EU initiatives

The European Commission is about tosign contracts to finance the demonstrationof the use of LNG in trucks within thisyear or early 2013. The commissionis also foresees a global finance of€80 euro since 2014, in whichNatural Gas Vehicles including thosewith LNG and dual fuel system willplay an essential role.Dutch Ministry of Infrastructure andEnvironment has been offering €10million subsidies for inland waterwayssector while the importance of “safe

The European Commission andDutch government are offeringfinancing for the adoption of LNG intransport sector. The role of this fuelis increasingly important and popularsince last year. To help speeding upthe development of LNG-for-transport,NGVA Europe is going to hold “LNG 4Trucks & Ships Workshop” in Amsterdamon 19-21 September 2012.During the workshop, table top exhibition and outside vehicle display will also be held.

Book your table and jointhe other exhibitors!

Ballast Nedam IPM, Cryostar,Emerson Process Management FlowB.V./Micro Motion, VanzettiEngineering, Iveco Schouten (vehicledisplay), Rolande LNG, etc.Highlight your company and productpresence, and meet the marine androad vehicles, fuelling stakeholders,and government representative.Contact:[email protected] the workshop programmes atwww.LNG4TrucksAndShips.comThe event will also incorporate atechnical tour*, CNG boat canalcruise, networking session, andexclusive workshop presentationsand discussion panel members from:Dutch Ministry of Economic Affairs,Agriculture and Innovation/Agentschap, Dutch Commission forLNG regulations, Ballast Nedam ,Gas LNG Europe/Gas InfrastructureEurope, Peter Shipyard, Pro Danube,Emerson Process Management FlowBV/Micro Motion, Rolande LNG,MAN Diesel & Turbo, KIWANetherlands, TUV Saarland, NGVAEurope, Cryostar SAS, Gasrec,Wesport, Vanzetti Engineering,Ecofys, and many others. Book yourseat at the technical tour’s bus.

An event of Host / Sponsor Diamond

LIQUIFIED BIOGAS

Sponsor Silver Organized by

and sustainable” inland waterways isgaining more and more attentionaccordingly. In line with this, recently, the DutchMinistry of Economic Affairs, Agricultureand Innovation through its exclusiveorganisation AgentschapNL and privatesectors signed an agreement on“Green Deal” to adopt hundreds ofLNG or dual fuel barges, ships, andHeavy-Duty trucks by 2015.Additionally, Ballast Nedam is targeting to build 60 LNG filling stations to serve 10,000 HDVs by2017-2022 while other LNGproviders also adding new stations.

*See the technical tour invitation athttp://www.youtube.com/watch?v=PcIOKzq84q8

August 2012 23

Company and productNow available: the new WEH® catalogue for CNG refuelling

The new, hot off the press WEH®product catalogue for CNG refuellingis even better and more detailed than

ever before. It is available in German and English, andshowcases in 140 pages our large variety of high-performance WEH® components for natural gasvehicles and fuelling stations.Newly designed and clearly structured, the cataloguefeatures many product innovations for refuelling of NGVs(natural gas vehicles). Detailed illustrations of the widerange of products and accessories are provided.The well-proven WEH® fuelling nozzles, receptacles andbreak-away couplings are still the highlight of the catalogue. Complete refuelling assemblies, consistingof the fuelling nozzle, hose and break-away couplinghave been included as well.The catalogue is available from now on and can be easily downloaded as a PDF file at www.weh.com/ngv-catalogue. For questions or if youwould prefer a printed version of the catalogue, pleasefeel free to contact us. You may reach us by email [email protected] or by phone at +49 (0) 7303 95190-0.

For further questions or pictures please contact: Dennis Kropf - WEH Public Relations - eMail: [email protected] -Phone: +49 7303 95190-551 - WEH GmbH: Josef-Henle-Str. 1- 89257 Illertissen - Germany - www.weh.com

Compac DCAThe CompacDCA (DrivewayCard Acceptor)

is a stand alone terminal designed tomake refuelling and site managementeasy. It that works seamlessly withyour dispensers to offer secure unattended refuelling, 24 hours aday, 7 days a week.

The DCA allows you the flexibility tomanage your site as you need.Accepting a variety of devices, theDCA authorises fuel delivery forapproved users.

The devices include third party cards,white cards, HID keys, CWID keysand/or pin numbers, with the optionof using some of these devices in combination. User identification at the DCA canbe configured to match with the driver or with the vehicle or with both.

In addition odometer readings canbe recorded at the time of refuelling

with a PinPad prompt.For downloading fuel delivery datafrom the DCA there are two options:CompacOnline or USB data transfer.

CompacOnline requires that theDCA has a connection to the internet, with access to data available by simply logging into theCompacOnline website. USB datatransfer is a simple method wheredata is transferred from DCA to computer and back again using aUSB stick.

Reading and writing of data is doneusing an Excel Spreadsheet.

The DCA is a stand-alone unit madefrom stainless steel. Mounted free-standing on its post the DCArequires no additional shelter.

In addition a receipt printer can beadded to the unit.

This is highly reliable, using a

waterproof chamber that preventswater damage and paper jams.For more information on Compac’sDCA, CompacOnline or USB FuelManagement visit our websitewww.compacngv.com or email us at [email protected]

August 201224

The 4th NGVA EuropeInternational Show &Workshops on natural gas,biomethane, CNG, LNG,and hydrogen blends vehicles will be held inGothenburg City inSweden.

The event will be carriedout at Svenska

Mässan-the Swedish Exhibition &Congress Centre- from 11 to 13 June 2013. The Svenska Mässan is a world-class meeting placelocated in the heart of Gothenburg City.Its very modern exhibition and conference complex contains various exhibition halls, conference rooms, seven restaurants and the largest hotel in Scandinavia-allat one place.The expo venue is situated within easy walking distanceof restaurants, entertainment, shopping, sport, culture andservices it provides the ideal opportunities for all sorts ofancillary arrangements. The event venue is located nextto Gothenburg concert hall, museum, art exhibition building, Museum of World Culture, etc. During the last decade, Sweden has shown a significantdevelopment in the NGV market with 110 percentgrowth in 2002-2011. The country has merely 204NGVs and 8 CNG filling stations in 1996. In 2002,

there were 3,309 NGVs and 30 stations that grew to40,029 vehicles and 183 methane filling facilities (179CNG and 4 LCNG stations). The methane dispensingfacilities are supplied by biomethane as well as natural gas.When ones speak about biomethane, most people thinkimmediately about Sweden, one of the leading producersof this renewable gas. Holding an NGV exhibition andworkshop in this capital nation of biomethane is in linewith the EU’s policy to promote the renewable gas industry. The EU has been financing “Biomaster” project toincrease production, distribution and utilization ofbiomethane in transportation. Through this initiative, EU stakeholders will construct 12 biomethane productionplants in Italy, Sweden, Great Britain and Poland. The project was started in 2011 and will be concludedby 2014.With “L-CNG, bio & natural gas-The Fuel alternative forall transport” as a theme, this NGVA Europe main eventis supported by Energigas Sverige-Swedish GasAssociation, sponsored by Volvo Trucks, and organizedby The GVR/NGV Communications Group.This event will attract people from all over Europe and therest of the world.

The Swedish Exhibition & Congress CentreSvenska Mässan

Organized by

®

Sponsor Gold

®

Hosted by

®

An event of

®

Company and productNGV2013 Gothenburg international exhibition and workshop

August 2012 25

Company and productFHT VERSUSGAS – short presentation and future prioritiesFHT VERSUSGAS is a producer of core components ofVERSUS Sequential Gas Injection systems.

“We are preparing our organization to start two innovative R&D projects in which main targets are:- The project of Electronic Control Unit already downsized, with our best “know-how” included.- New project of CNG pressure regulator oriented on the most recent expectations of the installers as well asstill improving car manufacturers technology that requiresdown-sizing matched with perfect performance also incase of mechanical components production. Last stage of the projects is going to be the investment innew machinery to follow with the market demand.

With the beginning of 2012 the company started severalinvestment projects oriented for next 3 years. Some stageof this plan has already been completed. New and biggerR&D center with over 1000 m2 space has been purchased.

We deeply believe that all of these steps would be thebeginning of “FHT VERSUSGAS way”, that finally wouldplace our organization among top players in NGV sectorwithin few incoming years” said Korczynski.

All management processes in FHT VERSUSGAS are performed according to ISO 9001;2008 QualityManagement System. Since April 2011 FHT VERSUS-GAS obtained ISO 15500-9:2001 certificate for theCNG pressure regulator Type VR-C. “This is the first certified this type of production line existing in Poland. This only underline to our customer that we wish to payour special attention to quality oriented approach in thefuture as well” said Wojciech Korczynski – GeneralManager of FHT VERSUSGAS.