valuation methodology

TRANSCRIPT

VALUATION

METHODOLOGY

An overview

“If I am not worth the wooing, I am

surely not worth the winning.” - Henry

Wadsworth Longfellow

Methodologies2

So what multiple do we use?

P/E multiple

Market to Book multiple

Price to Revenue multiple

Enterprise value to EBIT multiple

How about Discounted Cash Flows (DCF)

NPV, IRR, or EVA based MethodsWACC method

APV method

CF to Equity method

Valuation: P/E multiple3

IPO or a takeover target? This is how we get value;

Value of firm = Average Transaction P/E multiple EPS of firm

Average Transaction multiple is the average multiple of recent transactions (IPO or takeover as the case may be)

If valuation is being done to estimate the firm’s value

Value of firm = Average P/E multiple in industry EPS of firm

This method can be used when

firms in the industry are making a profit (have positive earnings)

firms in the industry have similar growth rates (more likely for “mature” industries)

firms in the industry have analogous capital structure

Valuation: Price to book multiple4

The application of this method is similar to that of the P/E multiple method.

Since the book value of equity is essentially the amount of equity capital injected in the firm, this method measures the market value of each dollar of equity injected.

This method can be used for

companies in the manufacturing sector which have huge capital requirements.

companies which are not in technical default (negative book value of equity)

Valuation: Value to EBITDA

multiple5

This gives us the enterprise value, the

value of the business operations (versus the

value of the equity).

In figuring out the enterprise value, just the

operational value of the business is included.

Value from investment activities, such as

investment in T-bills or bonds, or investment in

stocks of other companies, is not factored in.

The following economic value balance sheet

brings to light the concept of enterprise value.

Enterprise Value6

Economic Value Balance Sheet

PV of future cash from business

operations$1500

Cash $200 Debt $650

Marketable securities $150 Equity $1200

$1850 $1850

Enterprise Value

Value to EBITDA multiple:

Example7

Let’s value a Target using the following data

points:

Enterprise Value to EBITDA (business operations

only) multiple of 5 recent transactions in this industry:

10.1, 9.8, 9.2, 10.5, 10.3.

Recent EBITDA of target company = $20 million

Cash in hand of target company = $5 million

Marketable securities held by target company = $45

million

Interest rate received on marketable securities = 6%.

Sum of long-term and short-term debt held by target =

$75 million

Value to EBITDA multiple:

Example8

Take the mean (Value/ EBITDA) of recent transactions

(10.1+9.8+9.2+10.5+10.3)/5 = 9.98

Interest income from marketable securities

0.06 45 = $2.7 million

EBITDA – Interest income from marketable securities

20 – 2.7 = $17.3 million

Estimated enterprise value of the target

9.98 17.3 = $172.65 million

Add cash plus marketable securities

172.65 + 5 + 45 = $222.65 million

Subtract debt to find equity value: 222.65 – 75 = $147.65 million.

Valuation: Value to EBITDA

multiple9

Since this method measures enterprise value it accounts for different capital structures

cash and security holdings

By evaluating cash flows prior to discretionary capital investments, this method provides a better estimate of value.

Appropriate for valuing companies with heavy debt burdens: while earnings might be negative, EBIT is likely to be positive.

It provides a measure of cash flows that can be used to support debt payments in levered companies.

Heuristic methods: drawbacks10

While heuristic methods are simple, all of them

share several common disadvantages:

they do not accurately reflect the synergies that

may be produced in a takeover.

they assume that the market valuations are

accurate. For example, in an overvalued

market, we might overvalue the firm.

They assume that the firm being valued is similar

to the median or average firm in the industry.

They require that firms use uniform accounting

practices.

Valuation: DCF method11

Here we follow the discounted cash flow

(DCF) technique we used in capital budgeting:

Estimate expected cash flows considering the

synergy in a takeover

“PV it,” Discount it at the appropriate cost of

capital

DCF methods: Starting data12

Free Cash Flow (FCF) of the firm

Cost of debt of firm

Cost of equity of firm

Target debt ratio (debt to total value) of the

firm.

Template for Free Cash Flow13

“Inco

me

Sta

tem

en

t”

Working capital

Year 0 1 2

Revenue

Costs

Depreciation of equipment Noncash item

Profit/Loss from asset sales Noncash item

Taxable income

Tax

Net oper proft after tax (NOPAT)

Depreciation Adjustment for

Profit/Loss from asset sales for non-cash

Operating cash flow

Change in working capital

Capital Expenditure Capital items

Salvage of assets

Free cash flow

Template for Free Cash Flow14

The goal of the template is to estimate cash flows, not profits.

Template is made up of three parts.

An “Income Statement”

Adjustments for non-cash items included in the “Income statement” to calculate taxes

Adjustments for Capital items, such as capital expenditures, working capital, salvage, etc.

The “Income Statement” portion differs from the usual income statement because it ignores interest. This is because, interest, the cost of debt, is included in the cost of capital and including it in the cash flow would be double counting.

Sign convention: Inflows are positive, outflows are negative. Items are entered with the appropriate sign to avoid confusion.

Template for Free Cash Flow15

There are four categories of items in our “Income Statement”. While

the first three items occur most of the time, the last one is likely to

be less frequent.

Revenue items

Cost items

Depreciation items

Profit from asset sales

Adjustments for non-cash items is to simply add all non-cash items

subtracted earlier (e.g. depreciation) and subtract all non-cash

items added earlier (e.g. gain from salvage).

There are two type of capital items

Fixed capital (also called Capital Expenditure (Cap-Ex), or Property,

Plant, and Equipment (PP&E))

Working capital

Template for Free Cash Flow16

It is important to recover both at the end of a finite-lived project.

Salvage the market value property plant and equipment

Recover the working capital left in the project (assume full recovery)

Template for Free Cash Flow17

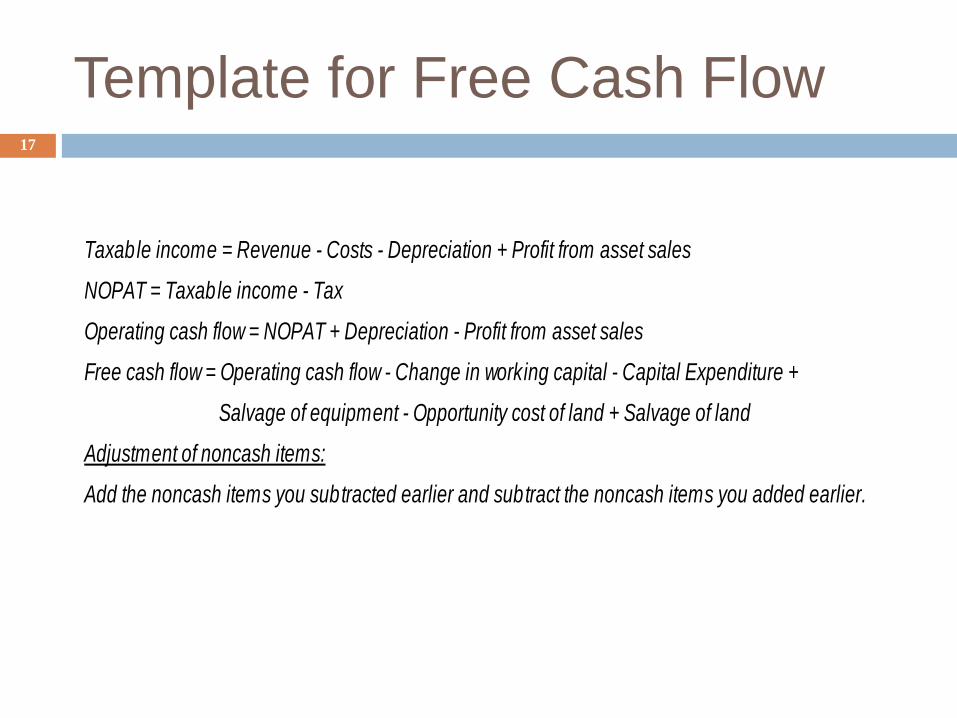

Taxable income = Revenue - Costs - Depreciation + Profit from asset sales

NOPAT = Taxable income - Tax

Operating cash flow = NOPAT + Depreciation - Profit from asset sales

Free cash flow = Operating cash flow - Change in working capital - Capital Expenditure +

Salvage of equipment - Opportunity cost of land + Salvage of land

Adjustment of noncash items:

Add the noncash items you subtracted earlier and subtract the noncash items you added earlier.

Estimating Horizon18

For a finite stream, it is usually either the life of the product or the life of the equipment used to manufacture it.

Since a company is assumed to have infinite life:

Estimate FCF on a yearly basis for about 5 10 years.

After that, calculate a “Terminal Value”, which is the ongoing value of the firm.

Terminal value is calculated one of two ways:

Estimate a long-term growth and use the constant growth perpetuity model.

Use a Enterprise value to EBIT multiple, or some such multiple

Costs of debt and equity19

Cost of debt can be approximated by the yield to

maturity (YTM) of the debt.

If it is not directly available, check the bond rating

of the company and find the YTM of similar rated

bonds.

Cost of equity

Capital Asset Pricing Model (CAPM)

Find e and calculate required re.

Use Gordon-growth model and find expected re.

Under the assumption that market is efficient, this is

the required re.

Model of a Firm20

Value from

Operations

FIRM

DEBT and

other

liabilities

EQUITY

Value generated

Value to Equity

Equal if debt

is fairly priced

Value from

investments

Enterprise value

Value of equity21

Value of equity

= Enterprise value

+ Value of cash and investments

- Value of debt and other liabilities