v207 1 canadian association of university business officers effective governance of investment funds...

TRANSCRIPT

1V207

Canadian Association of University Business OfficersCanadian Association of University Business Officers

Effective Governance of Investment Funds and Fund Performance: Are they linked?

Russell Investments Canada / University of Western Ontario

Effective Governance of Investment Funds and Fund Performance: Are they linked?

Russell Investments Canada / University of Western Ontario

Bruce B. Curwood MBA, CFA, CIMA, Director, Research and Strategy Russell

Stu Finlayson, CFA, Treasurer UWO

Bruce B. Curwood MBA, CFA, CIMA, Director, Research and Strategy Russell

Stu Finlayson, CFA, Treasurer UWO

2V207

Agenda – Effective Governance Matters!

1. Governance Research

2. Governance Changes at UWO

3. Appendix

3V207

Governance ResearchGovernance Research

Bruce B Curwood, MBA, CFA, CIMADirector, Investment StrategyRussell Investments Canada(416) [email protected]

4V207

Requirements for a successful investment program

Insight

Research…expertise and experience

Capital Markets and investment manager

Governance structures

Policy development

Diversified vs. concentrated portfolios (by mix & manager)

Stock selection vs. market timing

Align return expectations and risk tolerance

Align investment structure and strategy

Ongoing research is essential to identify the best ways to earn consistent returns and to minimize sources of slippage.

Governing

Operating

Managing

5V207

Requirements for a successful investment program

Long-term Investment Strategy

Implementation...efficient and cost effective execution

Asset mix

Asset class structure

Rebalancing (asset mix & managers) to control risk

Stay fully invested to minimize cash drag

Ensure best execution to minimize trading & transition costs (commission recapture, foreign exchange, etc.)

Utilize implementation techniques to reduce costs

Governing

Operating

Managing

6V207

Requirements for a successful investment program

Timely Decisions

Governance...delegation to skilled resources

Build (internal staff) or buy (outsource) the skilled resources consistent with your investment business model

Major policy decision to the Board based on a firm understanding of investment principles & research

Delegating decisions to investment and implementation professionals (internal/external)

Governing

Operating

Managing

7V207

What is Governance?

Important distinctions:

Management is about running a business

Governance is about seeing that the business is run properly

Governance is not about completing a one size fits all checklist but requires a well designed, tailored approach!

8V207

The investment industry is in the midst of the biggest change environment in a generation

Changing regulatory/accounting/societal environment

Demographics

Rapid growth in less developed markets

Increased technology and the use of derivatives

Globalization

Lower return environment

Significant expected changes to asset mix

Result:

Funds are exploring innovative new strategies to add value

9V207

A host of additional products are available to meet fund needs Beyond Traditional Products

Core Plus Fixed Income (adding foreign bonds opportunistically)

Global fixed income

High yield

Emerging market debt & equity

Alternatives (Cdn & global) Private equity

Hedge funds

Real estate

Infrastructure

Active currency management

Global tactical asset allocation

Long/Short (120/20 or 130/30)

Derivatives

Commodities

Leverage

Governance, risk management and effective implementation become more important to understand, vet and utilize these new investment products!

10V207

Source: Venture Economics and Russell Investment Group.Universes are unmanaged and cannot be invested in directly.

Manager Universes1996 – 2005

Private Equity1996 Vintage

US Large Cap US Small Cap

Inter-Quartile RangeUS Large Cap: 190 bpsUS Small Cap: 370 bpsUS Private Equity: 3780 bps

Fund selection is critical

25%

0%

50%

And selecting good managers is even more critical

11V207

Implications

The rate of change in the investment industry has been dramatic in the last 5 years

The typical 60/40 herd strategy is vanishing

Asset holding periods increase (as less liquid investments used)

Modelling behaviour is more subjective Inputs often based on specific products

Highly specialized management expertise required

Usually higher fees and/or transaction costs incurred

Complexity of strategies increases

Management and oversight is more onerous Fund staffing requirements increase

Manager selection and implementation skills are more important

Fiduciary risk may be greater!

The disparity between 1st and 4th quartile will be greater in the future

Poor governance practices combined with new products, which increase risk & implementation costs, is a recipe for disaster!

12V207

Applying the Knowing-Doing Gap to Investments

Over the last 15 years there have been a number of research studies that have been conducted on The Barriers to Investment Excellence or Implementation Slippage

Despite the fact that

These research papers are common knowledge

Many solutions have been offered up by the pundits/consultants

In many cases fiduciaries know what should be done

1. Poor processes persist in the institutional investment industry

2. The average institutional fund pays active management fees for passive performance

3. The costs of implementation slippage are significant (estimated between 50 bps to 150 bps per annum)

13V207

Sources of slippage

PolicyRisk / Return

PortfolioStructure /ManagerSelectionValue AddedValue Added

STRATEGYSTRATEGY

Actual Risk / Return

Value LostValue Lost

IMPLEMENTATIONIMPLEMENTATION

Manager Research Risk Budgeting Asset Class Structure

“Unintended” Exposures Asset Allocation Drift Frictional Cash Other

(e.g., structural bets) Diverted Attention Implementation Delay

Source: Russell Investments

14V207

GovernanceThe UK Pensions Regulator 2006 Report

Size Matters

“The largest DB schemes, in particular stand out from other schemes. They are more confident in their self assessment and have frequently produced above average results across a wide range of objective measures.”

15V207

Governance The UK Pensions Regulator 2006 Report

Areas where large funds demonstrated better governance include:

Professional trustees were more commonly found in larger schemes, with above-average results

Schemes with professional trustees were more likely to be confident they have ensured that appropriate internal controls are in place to monitor and mitigate risks

Formal processes to identify risks are only common among the largest schemes

The degree of appropriate knowledge and learning ascribed to trustees generally increases with size of scheme

Training levels were higher where, arguably, the responsibilities of trustees are greatest, namely at large schemes

Confidence was greater among larger DB schemes and those with in-house administration

16V207

What drives institutional fund performance?Insights from CEM Benchmarking Inc.

Higher net value-added results (1991-2005) were positively associated with fund size, internal management and asset mix (including use of alternative strategies)

Three key themes

1. Scale matters/bigger is better“Large scale reduces unit costs and makes the acquisition of good fund oversight and good fund management more affordable.”

2. “Effective risk management is central to good pension fund management.”

3. Good governance matters in a material way“It improves long term returns” and “requires both expertise and a willingness to differentiate from the pack.”

17V207

2005 NACUBO Endowment StudyMajor Findings

10-year compounded rates of return Ending fiscal year 2005

Less thanor equal to

$25 M10-year compounded rates of return

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

Greaterthan $1 B

>$500 Mto $1 B

>$100 Mto $500 M

>$50 Mto $100 M

>$25 M to $50 M

12.0%

10.3%9.3% 8.7% 8.3% 7.9%

18V207

2005 NACUBO Endowment StudyMajor Findings

“As customary, large endowments outperformed small endowments on average”

CIO at larger funds tended to make the decision in the area of hiring and firing managers

Larger endowments had greater allocations to alternatives

Returns within alternative asset classes varied considerably, with large funds generally outperforming smaller

19V207

CAUBO Endowment Study 2006

5 Years 10 Years

Large (>$100mm) 8.5% 8.8%

$30mm to $100mm 8.3% 8.6%

$10mm to $30mm 7.6% 7.8%

Small (<$10mm) 6.4% 7.5%

Median 7.7% 8.1%

20V207

Comparison of asset mix changes 98–06

NACUBO

1998*

NACUBO

2006*

CAUBO

1998*

CAUBO

2006*

PIAC

1998**

PIAC

2006**

Fixed 30% 23% 50% 41% 40% 31%

Equity 64% 58% 50% 55% 54% 52%

Alts 6% 19% 0% 4% 6% 17%

RE 2% 3% ? ? 4% 7%

PE 1% 3% ? ? ? ?

hedge 3% 10% ? ? ? ?

other 0% 3% ? ? ? ?

*equal weighted **asset weighted

21V207

Investment staffing/consultant use

Large US universities averaged 5.0 FTE staff devoted to investment management

At Canadian & USA Universities the staffing assigned to Investment Management is about .8 FTE on average

However for funds below $100 mm the staffing assigned to Investment Management is about .3 FTE (Cda & USA)

In US universities 74% employ a consultant

Only 36% of Cdn Universities employ a consultant on average (for funds over $100mm it is higher at 48%)

Conclusion and Opportunity

Most smaller foundations & endowments are under- resourced!

Source: NACUBO, CAUBO and Commonfund Benchmark Study Foundation Report

22V207

Pension Fund Trustee competenceUniversity of Oxford 2005

Major Findings

Many trustees have limited problem-solving skills relevant to investment issues

Most trustees are unable to deal with probabilities and are inefficient information processors

Shortcuts (heuristics) dominate trustee decision-making procedures

Diversity of trustee competence suggests the possibility of considerable disagreement or resistance

Leadership and structured decision-making are crucial; otherwise there will be low levels of innovation and slow adaptation to changing

circumstances

23V207

What the research has shown!

Underperformance is a symptom of ineffective decision-making (poor governance)

Who makes which decisions (delegation)

Why they are made (other agendas)

How they are made (behavioural roadblocks)

When they are made (timeliness)

24V207

Governance arrangements

The toughest issue

What to decide

What to delegate

There’s only one solution

Keep control over decisions you are competent to make

Delegate all other decisions

Prudently

Profitably

25V207

A Templatefor Thinking About the Issues

Issues/ Objectives

Required Skills & Availability

Have/Acquire/ Outsource

Decision

26V207

The first key decision! What is our investment business model?(Internal/Outsourced/Hybrid solution)

Is investments a core function in our organization?

What is our comparative advantage in investments?

Should we be making the investment decision ourselves or should we delegate to investment professionals?

Do we have and can we retain sufficient internal investment expertise and resources?

Should we staff up internally, partner or outsource?

Size is usually the determining factor!

27V207

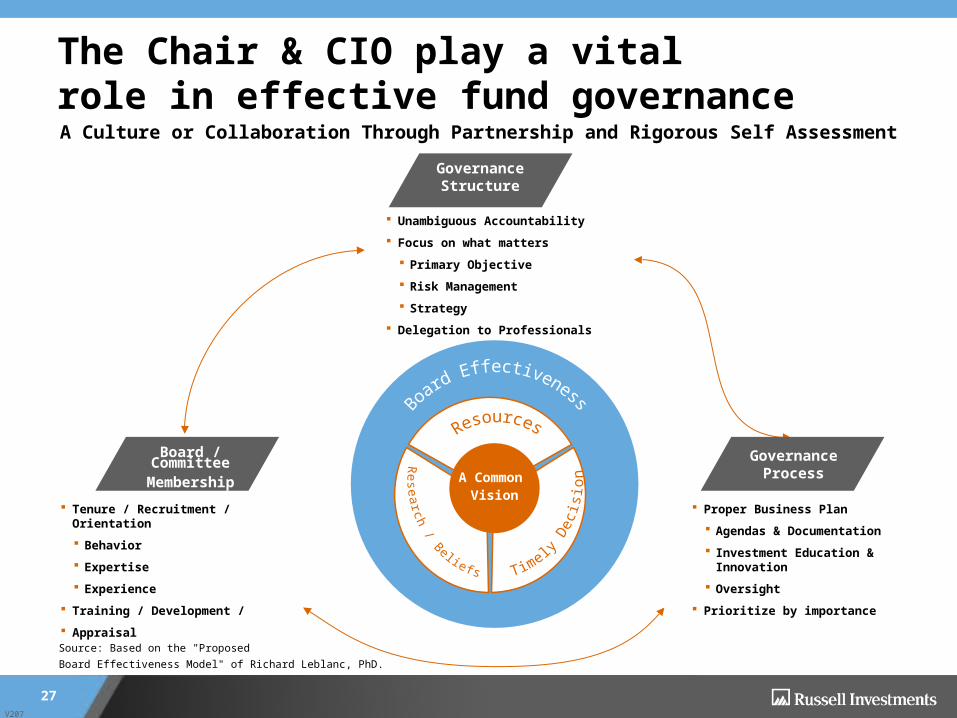

A Common Vision

Board / CommitteeMembership

Tenure / Recruitment / Orientation

Behavior

Expertise

Experience

Training / Development /

Appraisal

Proper Business Plan

Agendas & Documentation

Investment Education & Innovation

Oversight

Prioritize by importance

Unambiguous Accountability

Focus on what matters

Primary Objective

Risk Management

Strategy

Delegation to Professionals

Source: Based on the "Proposed

Board Effectiveness Model" of Richard Leblanc, PhD.

Governance Structure

Governance Process

The Chair & CIO play a vital role in effective fund governance

A Culture or Collaboration Through Partnership and Rigorous Self Assessment

28V207

A purpose-driven agenda

Risk Definition & Management

Implementation& Performance

Education & Innovation

29V207

Conclusions for better governance

Governance matters!

Determine your business model

Foster a culture of collaboration, openness and trust

Trustees focus on high-level important issues and the primary objective

Delegate to skilled investment professionals (internal staff/outsource), retaining oversight

Risk management via strategy, structure and process, rather than performance takes center stage

Education and innovation key to long-term success

Document the strategies based on sound research and beliefs

Maintain discipline, vigilance and oversight of process

A self-evaluation process of continuous refinement

In this era of accelerating change and a plethora of new investment solutions, good governance matters more than ever!

30V207

Governance Changes at UWOGovernance Changes at UWO

Stu Finlayson, CFATreasurerUniversity of Western Ontario(519) 661-2111 [email protected]

31V207

Investment Governance - What it was like before

Investment setting

Traditional 60/40 asset mix policy

5% allocation to alternative approved in 2003 (Hedge funds)

Avoided maverick risk

Long serving volunteers, mostly from local community

Focus on Managers and economic reviews

Members had extensive business experience

New investment opportunities studied but slow to put into policy

32V207

Investment Governance - What it was like before

Sometimes meetings did not go well

Agenda not always followed

Run out of time

Sometimes one member dominated discussions

Poor inconsistent attendance at meetings

A great deal of time devoted to Managers’ presentations

33V207

Investment Governance - What it is like now

Committee membership

Membership 5 year terms with renewal possible

Stressed professional qualifications and hands on investment experience of new members

Referrals for membership from Development office

Attendance policy established and enforced

Pay travel to more easily recruit Committee members from outside of London

34V207

Investment Governance - What it is like now

Committee meetings

Provide Member education on new issues

Focus on new opportunities and investment policy issues

Meeting rules - Working as a team

Share your knowledge

Respect the opinions of others

Give constructive feedback not criticism

Accept feedback with an open mind

Don’t interrupt others

Be brief and to the point

Avoid side conversations

Avoid personal agendas

Place side issues in a parking lot for future discussion

Decide by consensus whenever possible

Come prepared

Have fun

35V207

Investment Governance - What it is like now

More items delegated to Treasury Staff

Manager reviews done by Staff no longer conducted at Committee meetings

Manager searches and hiring Staff do research and recommend a manager to Committee

Recommended manager may present to Committee

Manager terminations recommended by Staff approved by Committee

Business plan to implement new investment strategies developed by Staff approved by Investment Committee

36V207

Why we needed to make changes to the Portfolio

We came to realize that our 60/40 mix likely not going to provide a real rate of return objective of 4.5%

(35% invested in bonds yielding about 2% real return)

We needed to improve returns or reduce spending allocations

BUT

Not really sure what the Board of Governors tolerance for risk really was

Regular turnover in members of Board of Governors

We had not focused on investment risks very much with the Board

Impact of large negative returns on reputation of: Western

Board members

Committee members

Staff

37V207

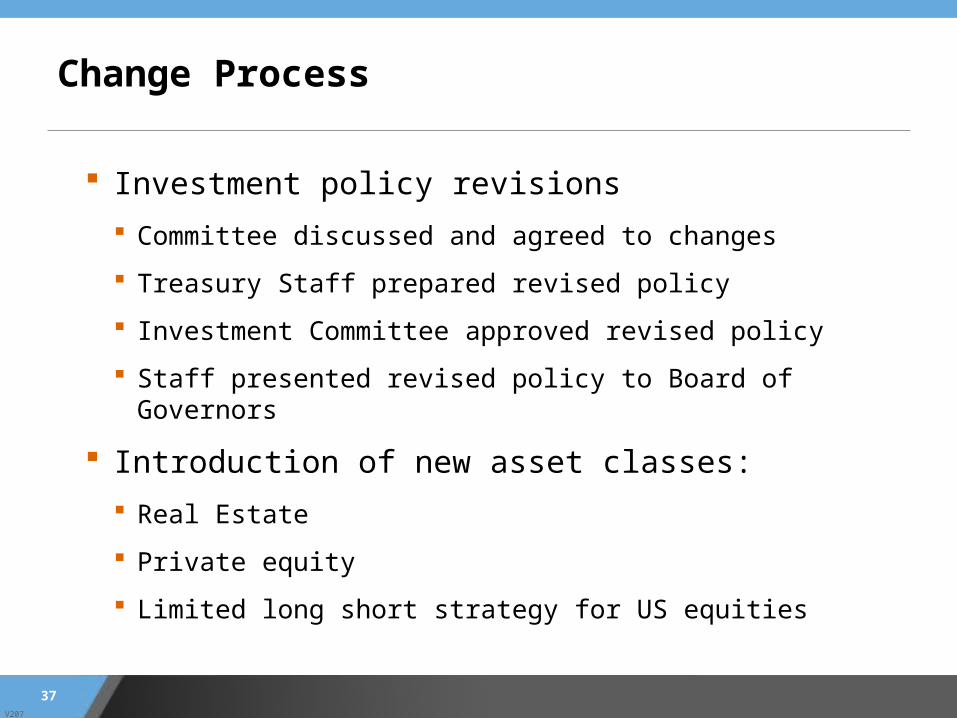

Change Process

Investment policy revisions

Committee discussed and agreed to changes

Treasury Staff prepared revised policy

Investment Committee approved revised policy

Staff presented revised policy to Board of Governors

Introduction of new asset classes:

Real Estate

Private equity

Limited long short strategy for US equities

38V207

Challenge

To obtain the ok from our Board of Governors to make these major changes to investment policy we tried to:

State reasons for changes to portfolio

Keep it simple

Compare to others

Show the expected impact on results and returns

39V207

Reasons for change

Our 60/40 mix is expected to earn a real return about 4 %

The real return on fixed income investments, which currently represent 35% of the total fund, is now about 2%

Likely not going to provide our real rate of return objective of 4.5%

If we want to maintain the real value of the endowment capital for future generations

We need to improve returns

OR

We need to reduce spending allocations to about 4%

40V207

Compared to others

Asset Mix Comparison Current Proposed 2006 2006

Asset class Western Western CAUBO NACUBO Equities 60% 60% 62% 59% Bonds 35% 25% 32% 25% Alternatives 5% 15% 6% 16%

total 100% 100% 100% 100% Alternatives consist of: Hedge funds 5% 5% n.a 9% Real Estate - 5% n.a 3% Private equity - 5% n.a 4%

total alternatives 5% 15% 6% 16%

Changes will move UWO to be more like US endowments

41V207

Showed the expected impact on results and returns

Current policy Proposed policy

Expected annual return 7.3% 7.7%

Expected inflation 3.2 % 3.2%

Expected real return 4.1% 4.5%

Expected standard deviation: RISK 9.8% 10.7%

The new policy mix is expected to provide sufficient returns to:

meet our payout objective for the endowments of 4.5% over time

allow the endowment capital to grow over time to compensate for inflation.

We expect that, about 2/3rd of the time, annual returns should fall in the range of

18.4% to (3.0%) LEVEL OF RISK

42V207

Provided reasons for new approaches

Why add real estate?

provides a long-term hedge against inflation

returns tend to have a low correlation with returns from other asset classes

represents a large category of investment opportunities

provides ongoing income as a large part of the total return

infrastructure investments offer a long duration income flow

income increases with inflation

43V207

Provided reasons for new approaches (cont’d)

Why add private equity?

Returns in excess of public equity markets have been available

Experienced investment managers have been able to find the best opportunities

inefficient market based on negotiated transactions with valuations and price

Successful private equity managers have access to proprietary information not available to all investors.

new investment opportunities that are often based on business relationships

but returns from this strategy tend to be negative in the early years

44V207

Provided reasons for new approaches (cont’d)

Why use a long short strategy?

Fairly new strategy that has been able to add value over index returns

Manager can buy the companies that they anticipate will perform well (long positions)

Manager can “sell short” companies that they anticipate will not perform well.

This portion of the portfolio will perform when the share price of the company decreases.

Strategy gives the manager more opportunity to use their investment skills,

But price increases in the shorted securities can accelerate losses since they exert a relatively larger impact on the portfolio.

45V207

Provided reasons for new approaches (cont’d)

How will the new strategies impact the liquidity of the portfolio?

Real estate and private equities will result in less liquidity for the fund

These investments do not trade on a daily basis on open markets.

Commitment to each strategy for a period of about 10 years.

Majority of overall portfolio will remain fully liquid.

By giving up a small amount of liquidity that we hope to achieve incremental returns over time.

46V207

Provided reasons for new approaches (cont’d)

“Guiding Principles” related to the changes in the portfolio:

Limit disruptions to the portfolio

Do not take on any significant new exposures (currency, market cap)

Stage in significant asset mix changes to limit asset timing decisions

Recognize the limits of current staff resources

Ensure all changes conform to Investment Policy

47V207

Conclusions

Fine tuning of Investment Governance:

Allows Committee to focus on policy and oversight

Allows management to focus on investment activities

Helps in the discovery and implementation of new investment ideas

AND

Hopefully results in sufficient returns to support long term endowment spending needs

48V207

What do I worry about now?

Will we be able to manage more complex investments with limited staff?

How to rebalance when portions of portfolio are not liquid?

Will the changes add value?

What will be our staying power if changes do not pay off within first 2 to 3 years?

V207

AppendixAppendix

50V207

Ten major investment hurdles

1. Not managing investment activities in a business like manner

2. Flawed governance structure

3. Failure to understand risk and the fund’s risk tolerance

4. Inappropriate asset allocation policies

5. Poor investment structures

6. Hiring unsuitable investment managers

7. Limited research and proper due diligence

8. Improper measurement and evaluation processes

9. Poor documentation of decision rationale; and finally

10.Failure to take advantage of economies of scale

51V207

Fiduciary fashion – 2007A look at what makes a good fiduciary

A fresh look at “purpose” driven investing

Annual plan

Agenda-driven meetings

Cultivating a culture of collaboration

Focus on the primary objective

Define and manage risk

Decisions pushed to highest level of expertise

Emphasis on education and application of new ideas

De-emphasis on repetitive, low-value activities

Good oversight & monitoring capability

Constant refinement of the governance process

52V207

“It is not the strongest of the species that survives, nor the most intelligent, but the one that responds to change.”

– Charles Darwin

Image Source: http://www.ped.fas.harvard.edu/images/PG8519.jpg

53V207

Why don’t organizations respond better to change?

“The Knowing-Doing Gap”

by Jeffrey Pfeffer and Robert I. SuttonCopyright 2000 Harvard Business School Press

54V207

“What Is the Knowing-Doing Gap?”

Knowledge of what needs to be done frequently fails to result in action or behaviour consistent with that knowledge

The knowing-doing problem – “the challenge of turning knowledge about how to enhance organizational performance into actions consistent with that knowledge”

“Time after time, people understand the issues, understand what needs to happen to affect performance, but don’t do the things they know they should”

55V207

No simple answers

“Knowledge that is actually implemented is much more likely to be acquired from learning by doing than from learning from reading.”

“Research demonstrates that the success of most interventions designed to improve organizational performance depends largely on implementing what is already known, rather than adopting knew or previously unknown ways of doing things.”

“The best practices were actually well known, with the extra dimension that they were reinforced and carried out reliably in better performing organizations. They are in fact common sense…Yet it is interesting how uncommon common sense is in its implementation.”

“Attempting to copy just what is done –the explicit practices and policies- without holding the underlying philosophy is at once a more difficult task and an approach that is less likely to be successful”

If you and your colleagues learn from your own actions and behaviour there won’t be much of a knowing-doing gap because you will be “knowing” on the basis of your doing and implementing that knowledge will be substantially easier.

56V207

The main barriers to turning knowledge into action

A. When talk substitutes for action

B. When memory is a substitute for thinking

C. When fear prevents acting on knowledge

D. When measurement obstructs good judgement

E. When internal competition turns friends into enemies

57V207

Examples of the Knowing-Doing Gap in investments

A. When Talk Substitutes for Action in Investments There is no end to the amount of talk or meetings in investments but:

The institutional committee meeting agendas are large and time is short;

Committee members are part time and often lack expertise;

The resources to implement effectively are underestimated.

Attending seminars and conferences is common practice but: The speakers often have vested interests (e.g. an emerging market manager talking about the benefits of

emerging markets);

Jargon and acronyms are used extensively to make the speakers appear smart, leading to complicated discussion that is incomprehensible to the fiduciaries.

Consultants and sponsors rarely have implementation experience “At the end of the day what consultants provide is advice –talk- and only rarely to they get involved in the

details of doing something. What they rarely supply is implementation”.

Investment committees critique ideas to death but: This generally postpones or delays implementation;

There is a failure to delegate to investment professionals either internal or external (micromanagement).

“Mission statements and checklists are the most blatant and common means that organizations substitute talk for action” but “The problem is there are too many organizations where having a mission statement written down somewhere

is confused with implementing those values.”

Source: The Knowing-Doing Gap, Jeffrey Pfeffer and Robert I. Sutton/Russell Investments

58V207

Examples of the Knowing-Doing Gap in investments

B. When Memory is a Substitute for Thinking in Investments “When people are unsure about how they or their organization should act,

they automatically imitate what others do” but They may not have the same resources or philosophy (i.e. Yale, Harvard, OTPP)

Their circumstances (Liabilities, etc.) may be different

Commitment to past decisions signals consistency and persistence but these past decisions are often Based on untested and inaccurate models

Not well researched

Not questioned; or

Not well documented

A good example is Investment Committees refusing to discuss investment strategies based on a previous bad experience to a specific event or strategy. Those conditions may not hold in a diversified strategy or today’s very different market environment; Similarly avoiding a specific manager who previously performed poorly but has addressed their process issues is an error in judgment

Source: The Knowing-Doing Gap, Jeffrey Pfeffer and Robert I. Sutton/Russell Investments

59V207

Examples of the Knowing-Doing Gap in investments

C. When Fear Prevents Acting on Knowledge in Investments Investment committees generally hire the best Sponsor/CIO or consultant they can

afford, but often Don’t allow the Sponsor to be an equal member of the Investment Committee

Mistrust the Sponsor or consultant and don’t heed their advice

‘Are penny wise and pound foolish’

Sponsors/Consultants are generally afraid to go against the Investment Committee views for fear of losing their jobs

appearing confrontational by going against the majority

Committees recognize the importance of a well researched, long term investment strategy but Succumb to fear or greed

Fall victim to behavioural biases; or

Follow the herd for fear of taking maverick risk (being different from most other funds)

Source: The Knowing-Doing Gap, Jeffrey Pfeffer and Robert I. Sutton/Russell Investments

60V207

Examples of the Knowing-Doing Gap in investments

D. When Measurement Obstructs Good Judgement in Investments

Too many measures, such as

High absolute returns

Failure to beat a benchmark

Poor relative performance

Failure to focus on a few good measures

Hard measures drive out soft measures

“The time scales of the measurement – how often the organization assesses results- helps to establish the time horizons that tend to govern behaviour”

Quarterly meetings

Failure to recognize the difference in timing between investment (long) and organizational results (annual)

Source: The Knowing-Doing Gap, Jeffrey Pfeffer and Robert I. Sutton/Russell Investments

61V207

Examples of the Knowing-Doing Gap in investments

E. Internal Competition Turns Friends into Enemies in Investments High committee turnover hurts performance as

They don’t learn by doing and experiencing from past mistakes

They don’t remember past market cycles

“Companies spend all their money hiring smart people and then overburden them and do not allow them to share their knowledge” Consultants and staff are seldom treated like experts, but are seen as peers at best and often worse

mistrusted

There are generally few rewards from having a successful fund Most funds do not have incentive bonuses tied to performance objectives

As pensions is not generally a core function of the business, there is little career upside for success but there can be considerable downside for failing to control risk or provide proper oversight

There is very little partnering with outside investment experts. Investment Committee members tend to Judge service providers based on the relative numbers

Try to score points by embarrassing these well paid investment professionals by being Monday morning quarterbacks

Overly focus on costs to their detriment

Source: The Knowing-Doing Gap, Jeffrey Pfeffer and Robert I. Sutton/Russell Investments

62V207

Global research – 1 to 5

1992: O’Barr and Conley

US pension funds organize to manage blame

Community response

No: poor decision process

1994: 50 senior North American pension fund managers

Barriers to excellence

Poor processes

Inadequate resources

Lack of focus

Value of excellence

66 basis point p.a.

1998: Ambachtsheer et al.

80 pension funds

Average RANVA (-50 basis points p.a.)

6 pension funds

Organizational design explains 60% of RANVA differentials

1997: Coopers & Lybrand Australian super funds

Superior parts, inferior whole

1998: William M. MercerAustralian super funds

Poor decision-making and implementation

63V207

Global research – 6

1999: Frank Russell Company 22 leading UK pension fund executives

Barriers to excellence

Trustees’ poor processes and lack of knowledge

Inability of money managers

Value of excellence

50 basis points p.a.

64V207

Global research – 7

2001: Myners Review

Trustees poorly prepared

Concentrate expertise in investment sub-committee and use in-house staff

Delegate to advisers if youcan’t critically evaluatetheir advice

65V207

Global research – 8

Vrije Universiteit/Russell Study

Distinctive focus: ambitions versus resources

Fund Size Ambitions Resources

Large High High

Medium High Low

Small Low Low

Note the one mismatch!

66V207

Average asset mix as of 12/31/2005

*equal weighted **asset weighted

Asset Type NACUBO*CAUBO*

PIAC**

Large Average DB DC

Fixed Income 17% 26% 42% 36% 38%

Canadian Equity

n/a 28% 24% 26%

Global Equity 45% 59% 26% 25% 16%

Other (balanced)

n/a n/a 0% 19%

Alternatives 38% 15% 4% 15% 1%

- Real Estate 4% 3% ? 7% 1%

- PE & VC 9% 2% ? ? 0%

- Hedge 22% 9% ? ? 0%

- Other 3% 1% ? ? 0%

67 For Advisor Use OnlyV207

Important Information - Disclaimer

Nothing in this publication is intended to constitute legal, tax securities or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type. This is a publication of Russell Investments Canada Limited and has been prepared solely for information purposes. It is made available on an “as is” basis. Russell Investments Canada Limited does not make any warranty or representation regarding the information.

Russell Investments and Russell are either trademarks or registered trademarks of Frank Russell Company and used under a license by Russell Investments Canada Limited.

Copyright © 2008. Russell Investments Canada Limited. All rights reserved.

68V207

www.russell.com