v1 21/02/06 sepa impacts and opportunities ifb seminar lisbon, 23 february 2006

Post on 19-Dec-2015

217 views

TRANSCRIPT

V1 21/02/06

SEPA Impacts and Opportunities

IFB SeminarLisbon, 23 February 2006

IFB Seminar Lisbon Feb 20062V1 21/02/06

“Politics is the art of looking for trouble,

finding it whether it exists or not,

diagnosing it incorrectly and applying

the wrong remedy”

Sir Ernest Bevin, 1930

IFB Seminar Lisbon Feb 20063V1 21/02/06

Agenda

• Review of SEPA/NLF Features

• Banks – Perspective and Impacts

• Consumers – New Propositions

• Corporates – New Propositions

• Merchants – Impacts/Benefits

• Card / ACH Schemes – Impacts / Opportunities

• Interbank / Commercial Processors – Impacts / Opportunities

• Sector Suppliers – Impacts / Opportunities

IFB Seminar Lisbon Feb 20064V1 21/02/06

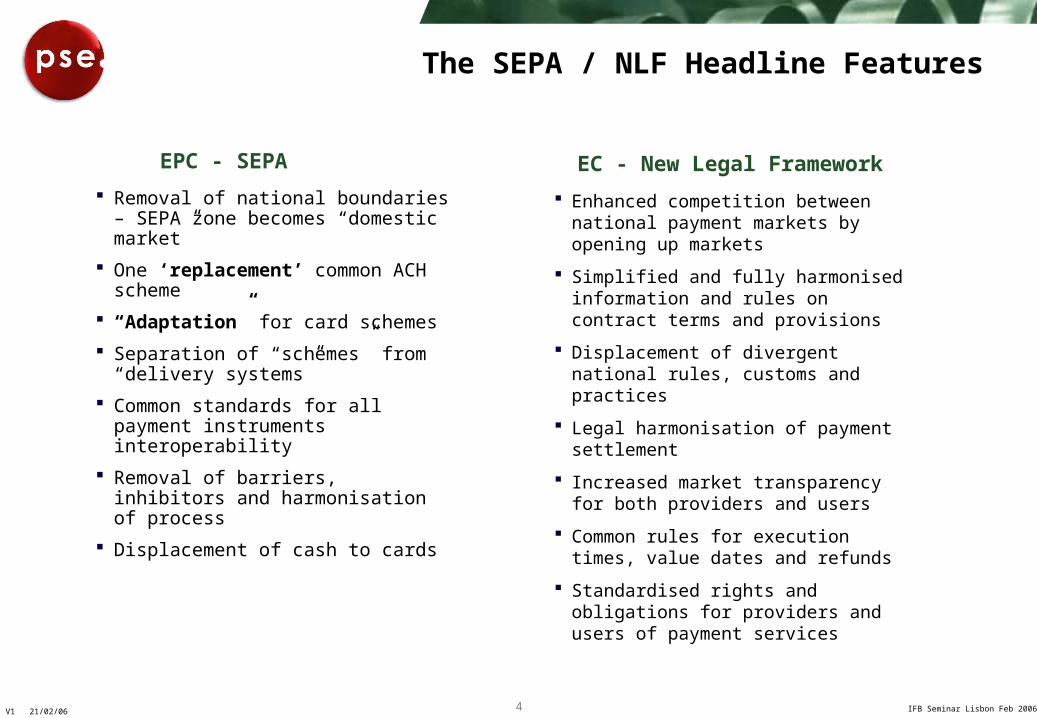

The SEPA / NLF Headline Features

Removal of national boundaries – SEPA zone becomes “domestic market”

One ‘replacement’ common ACH scheme

“Adaptation” for card schemes

Separation of “schemes” from “delivery systems”

Common standards for all payment instruments interoperability

Removal of barriers, inhibitors and harmonisation of process

Displacement of cash to cards

Enhanced competition between national payment markets by opening up markets

Simplified and fully harmonised information and rules on contract terms and provisions

Displacement of divergent national rules, customs and practices

Legal harmonisation of payment settlement

Increased market transparency for both providers and users

Common rules for execution times, value dates and refunds

Standardised rights and obligations for providers and users of payment services

EPC - SEPA EC - New Legal Framework

IFB Seminar Lisbon Feb 20065V1 21/02/06

SEPA - European Banks Perspective

Large are supportive - perceive substantial benefit

Banking Associations and Savings/ Co-op banks cautious but supportive

New ACH scheme and governance well advanced

SCF to be issued – detail/standards – end 2006

Worried over competitive disadvantages unless participate

Unsure how and when all SEPA can be delivered

IFB Seminar Lisbon Feb 20066V1 21/02/06

SEPA – European Banks Perspective – cont’d

Increased competition – any bank can sell in “SEPA domestic markets”

Price transparency, lower cost products encourages switching

Increased regulatory burden and new mandated rules add to operational costs

Lower revenue streams from many forms of payment and potentially much lower card revenues

Substantial costs – business case not clear

Some major concerns and issues to be resolvedSome major concerns and issues to be resolved

IFB Seminar Lisbon Feb 20067V1 21/02/06

SEPA – Macro Bank Positive Impacts

New open market – develop new propositions/products

New SEPA products have a potential market of 400m+ customers

Single payments platform can serve the whole of Europe

Easier cross-border M&A and lower costs of market entry

Open market for ACH and cards issuing/acquiring and processing

Simplified and common scheme rules

Open membership of all schemes (ACH/Cards) in all countries

Greater competition lower costs in supplier and processor markets

SEPA delivers many benefits – but new strategies neededSEPA delivers many benefits – but new strategies needed

IFB Seminar Lisbon Feb 20068V1 21/02/06

SEPA – Typical Bank Strategies - PSE Feedback

New competitive offers to retain existing customers – defend new competitors

Reposition card account with ICS brands

Leverage SEPA – development of new “SEPA” propositions:

new account products

multi country workers products

high net worth – cross border home owners/tourists

new large corporate products

cross border trading – small corporate products

online/e-banking

Develop white label payment processing services for smaller banks

Build new processing platforms – replace old

Become acquirers and offer services across SEPA

Plus implementation of SEPA infrastructure changesPlus implementation of SEPA infrastructure changes

IFB Seminar Lisbon Feb 20069V1 21/02/06

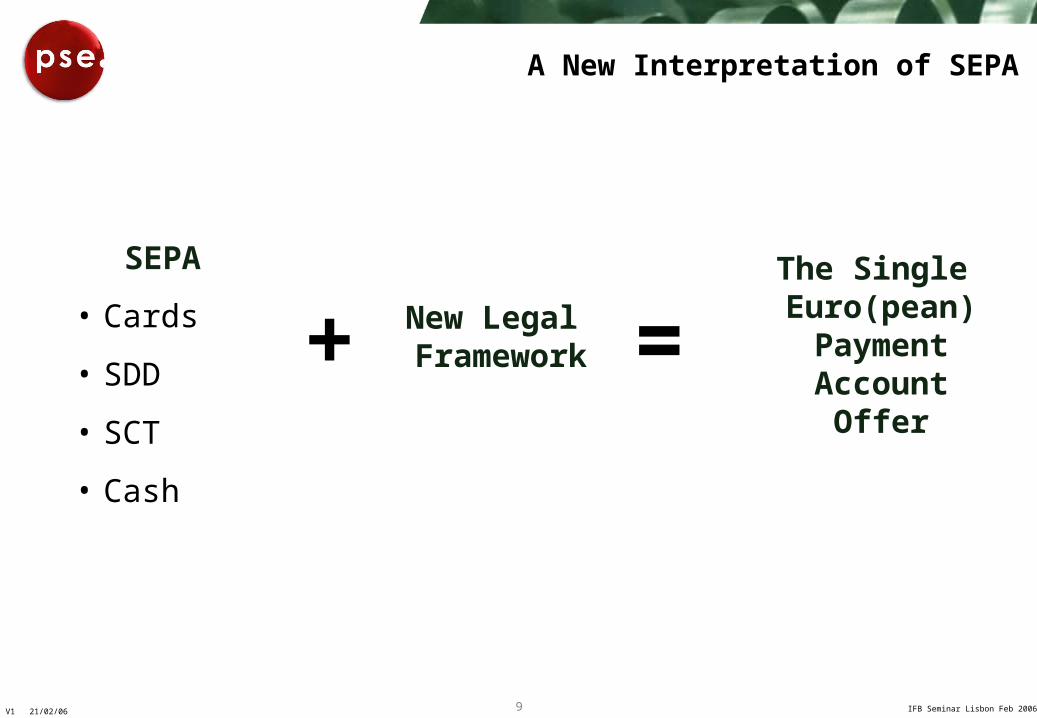

A New Interpretation of SEPA

SEPA

• Cards

• SDD

• SCT

• Cash

New Legal Framework+

The Single Euro(pean) Payment Account

Offer

=

IFB Seminar Lisbon Feb 200610V1 21/02/06

A Lesson in Mathematics

1Account

= 29Nations

IFB Seminar Lisbon Feb 200611V1 21/02/06

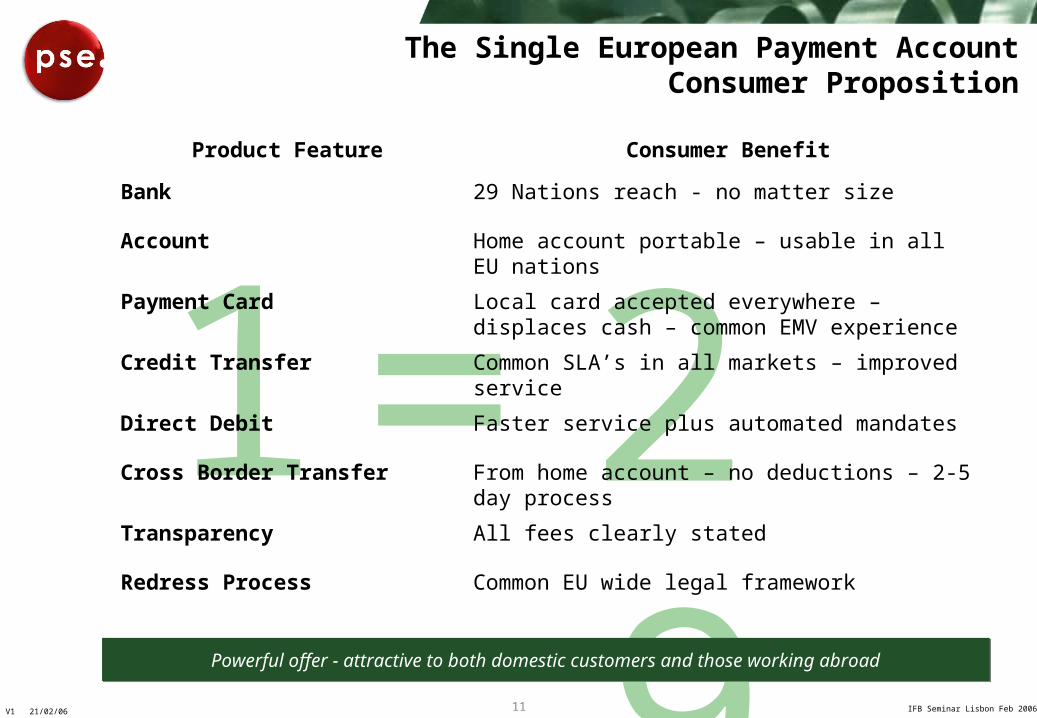

1 29=Product Feature Consumer Benefit

Bank 29 Nations reach - no matter size

Account Home account portable – usable in all EU nations

Payment Card Local card accepted everywhere – displaces cash – common EMV experience

Credit Transfer Common SLA’s in all markets – improved service

Direct Debit Faster service plus automated mandates

Cross Border Transfer From home account – no deductions – 2-5 day process

Transparency All fees clearly stated

Redress Process Common EU wide legal framework

The Single European Payment AccountConsumer Proposition

Powerful offer - attractive to both domestic customers and those working abroadPowerful offer - attractive to both domestic customers and those working abroad

IFB Seminar Lisbon Feb 200612V1 21/02/06

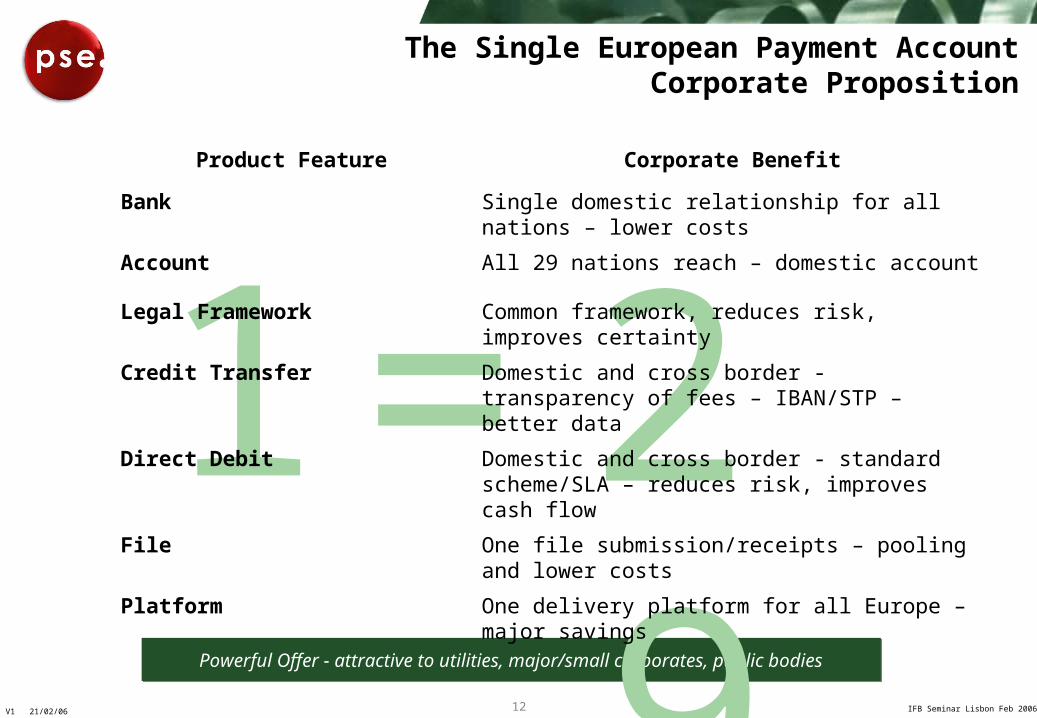

The Single European Payment AccountCorporate Proposition

Powerful Offer - attractive to utilities, major/small corporates, public bodiesPowerful Offer - attractive to utilities, major/small corporates, public bodies

1 29=Product Feature Corporate Benefit

Bank Single domestic relationship for all nations – lower costs

Account All 29 nations reach – domestic account

Legal Framework Common framework, reduces risk, improves certainty

Credit Transfer Domestic and cross border - transparency of fees – IBAN/STP – better data

Direct Debit Domestic and cross border - standard scheme/SLA – reduces risk, improves cash flow

File One file submission/receipts – pooling and lower costs

Platform One delivery platform for all Europe – major savings

IFB Seminar Lisbon Feb 200613V1 21/02/06

SEPA – Merchant Impacts and Benefits

Migration from cash to payment cards – lower costs

Acceptance of all national debit cards

Consistent acceptance process – removal of multiple terminals, lower costs, mandated EMV

Lower cost terminals, switches and technology – common applications/standards

For large single delivery platform serves all EU

Common process for redress/exception items

M&A and consolidation in processor/vendor sector – lower prices

Growth of pan-EU acquirers increased choice, lower prices

Powerful Offer - largest merchants benefit mostPowerful Offer - largest merchants benefit most

IFB Seminar Lisbon Feb 200614V1 21/02/06

SEPA - International Card Schemes

Impacts

Separation of scheme from processing (see recent EC Incentives Paper)

Growth of debit market share

Loss of mandated use of networks (VisaNet /MCI Net)

Potential for reduced scheme revenues

New governance structures

Potential to undermine global frameworks

Opportunities

Creation of two new businesses, new revenue streams

Potential for new and value added processing products – multi brand

Potential for increased processing revenues

Move to full commercialisation

Greater focus on member service, standards, processes

Major Impacts – potential to radically change EU structure – overall positiveMajor Impacts – potential to radically change EU structure – overall positive

IFB Seminar Lisbon Feb 200615V1 21/02/06

SEPA - Domestic ACH Debit Card ATM Schemes

Impacts

Loss of national ACH schemes

Open membership – any bank/player

New SEPA scheme rule books/frameworks

Separation of schemes from processor

Migration of members to ICS/other debit

Reduced revenues / resources

Increased transparency and regulation

Survival in the new competitive SEPA domestic market

Migration to four party card model (Germany)

Opportunities

Potential to become pan-EU schemes

More efficient, lower cost operations, new products/services

Many threats and challenges – only strongest will surviveMany threats and challenges – only strongest will survive

IFB Seminar Lisbon Feb 200616V1 21/02/06

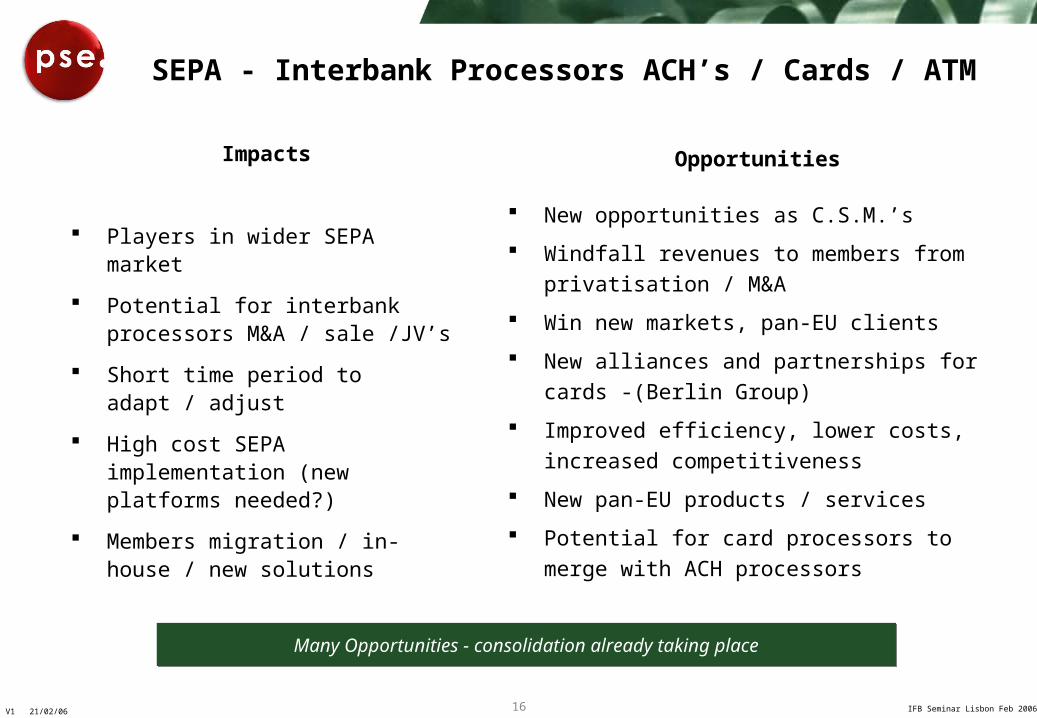

SEPA - Interbank Processors ACH’s / Cards / ATM

Impacts

Players in wider SEPA market

Potential for interbank processors M&A / sale /JV’s

Short time period to adapt / adjust

High cost SEPA implementation (new platforms needed?)

Members migration / in-house / new solutions

Opportunities

New opportunities as C.S.M.’s

Windfall revenues to members from privatisation / M&A

Win new markets, pan-EU clients

New alliances and partnerships for cards -(Berlin Group)

Improved efficiency, lower costs, increased competitiveness

New pan-EU products / services

Potential for card processors to merge with ACH processors

Many Opportunities - consolidation already taking placeMany Opportunities - consolidation already taking place

IFB Seminar Lisbon Feb 200617V1 21/02/06

SEPA – Commercial Processors Impacts and Benefits

Market consolidation through M&A already occurring

New customers and revenues as barriers removed

Single common platform results in lower processing cost

Growth of ISO/on-risk acquiring displacing banks

Major investments required to build/modify platforms to SEPA

New pan-EU products and services

Major consolidation already taking placeMajor consolidation already taking place

IFB Seminar Lisbon Feb 200618V1 21/02/06

SEPA - Impacts and BenefitsSupplier Sector

Few have SEPA strategies – many “vapourware” products

No business / technical specifications or standards yet - what has to be done?

Major opportunity for new software products and systems integration contracts

Lower cost common products – old multi country solutions become obsolete

Potential surge in demand for new switches, back office clearing / settlement platforms

Potential for interim interface adaptors / boxes

Increased M&A in supplier sector

Of €10bn cost – significant share to supplier sectorOf €10bn cost – significant share to supplier sector

IFB Seminar Lisbon Feb 200619V1 21/02/06

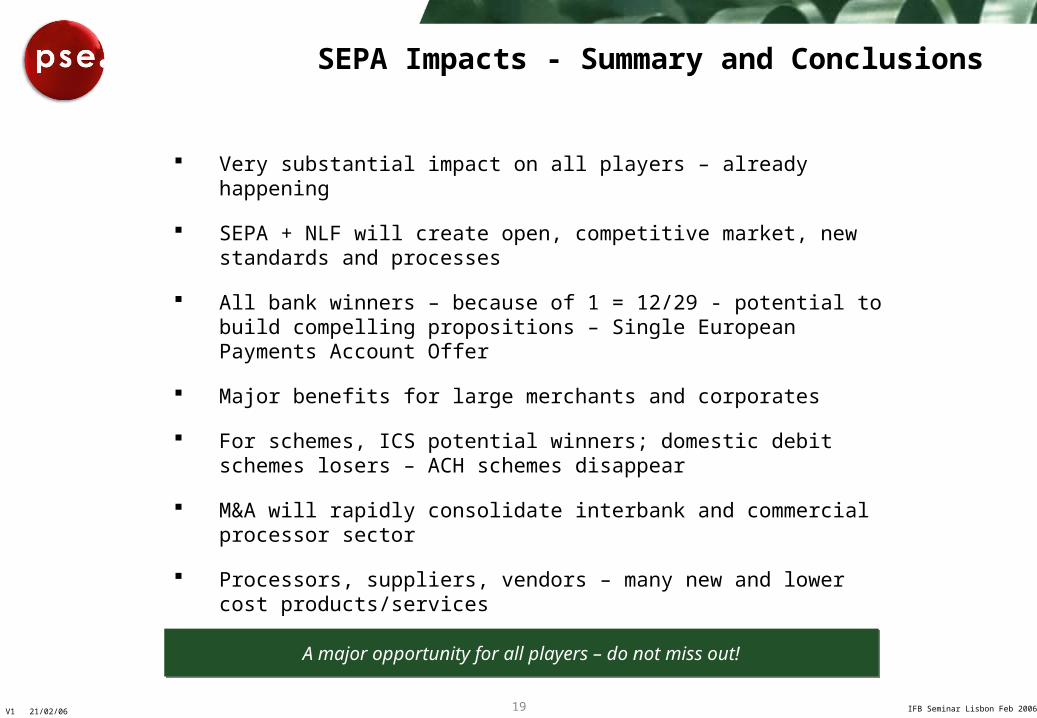

Very substantial impact on all players – already happening

SEPA + NLF will create open, competitive market, new standards and processes

All bank winners – because of 1 = 12/29 - potential to build compelling propositions – Single European Payments Account Offer

Major benefits for large merchants and corporates

For schemes, ICS potential winners; domestic debit schemes losers – ACH schemes disappear

M&A will rapidly consolidate interbank and commercial processor sector

Processors, suppliers, vendors – many new and lower cost products/services

SEPA Impacts - Summary and Conclusions

A major opportunity for all players – do not miss out!A major opportunity for all players – do not miss out!

IFB Seminar Lisbon Feb 200620V1 21/02/06

“Politics is not the art of the possible.

It consists of choosing between the

disastrous and the unpalatable”

J K Galbraith, 1969

IFB Seminar Lisbon Feb 200621V1 21/02/06

Peter Jones Managing Director

+44 (0) 20 8891 6244