us pe middle market report - madison capital funding · 2017-12-18 · us pe middle market report....

TRANSCRIPT

2016 Annual Sponsored by

Co-sponsored by

US PE Middle Market

ReportIn partnership with

Take everyone’s game to the next level

Deloitte serves private equity investors extensively, applying our business and sector experience to help their portfolio companies enhance financial reporting, improve operations, and solve challenges. Visit www2.deloitte.com/us/pe.

Audit | Tax | Consulting | Advisory

Copyright © 2017 Deloitte Development LLC. All rights reserved.

Credits & ContactPitchBook Data, Inc.

JOHN GABBERT Founder, CEO

ADLEY BOWDEN Vice President,

Market Development & Analysis

Content

DYLAN E. COX Analyst

NIZAR TARHUNI Senior Analyst

GARRETT JAMES BLACK Publisher

BRYAN HANSON Data Analyst

JENNIFER SAM Senior Graphic Designer

Contact PitchBook pitchbook.com

RESEARCH

EDITORIAL

SALES

ACG GlobalGARY LABRANCHE President & CEO

KRISTIN GOMEZ Vice President,

Communications & Marketing

DEBORAH COHEN Editor-in-Chief

COPYRIGHT © 2017 by PitchBook Data, Inc. All rights reserved. No part of this publication may be reproduced in any form or by any means—graphic, electronic, or mechanical, including photocopying, recording, taping, and information storage and retrieval systems—without the express written permission of PitchBook Data, Inc. Contents are based on information from sources believed to be reliable, but accuracy and completeness cannot be guaranteed. Nothing herein should be construed as any past, current or future recommendation to buy or sell any security or an offer to sell, or a solicitation of an offer to buy any security. This material does not purport to contain all of the information that a prospective investor may wish to consider and is not to be relied upon as such or used in substitution for the exercise of independent judgment.

Methodology 4

Introduction 5

Note from ACG 6

Overview 8-9

Deloitte Q&A: How Can PE Succeed

in 2017?10

Lower Middle Market 11

Core Middle Market 12

Upper Middle Market 13

Company Inventory 15

Exits 16

Fundraising 17

League Tables 18

CONTENTS

IN PARTNERSHIP WITH

CO-SPONSOR

SPONSORED BY

3 PITCHBOOK 2016 ANNUAL US PE MIDDLE MARKET REPORT

METHODOLOGY

At Deloitte, we believe the audit is more than an obligation—it’s an opportunity to see further and deeper into the business. That is the approach we take with private equity investors’ (PEI) portfolios. It helps that Deloitte is able to bring the full power of one of the largest professional services organizations in the world to each engagement—not

to mention a deep understanding of the unique characteristics of the PEI market and business model. We know that portfolio companies look for a high level of commitment and resources, and we can access a network of seasoned individuals with M&A and IPO experience to help address their issues.

Deloitte’s Private Equity Portfolio Company Program provides a single point of contact for PEI clients and their portfolio companies—an experienced leader able to marshal the full resources of the organization to respond to individual opportunities and challenges.

Our Private Equity Portfolio Company Program fosters an innovative culture—our people are continuously reinventing the tools, technologies and processes they use to serve the needs of PEI clients. Visit www2.deloitte.com/us/PE. As used in this document, “Deloitte” means Deloitte & Touche LLP, a subsidiary of Deloitte LLP. Please see www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte USA LLP, Deloitte LLP and their respective subsidiaries. Certain services may not be available to attest clients under the rules and regulations of public accounting.

IN PARTNERSHIP WITH

CO-SPONSOR

SPONSORED BY

4 PITCHBOOK 2016 ANNUAL US PE MIDDLE MARKET REPORT

MIDDLE MARKET DEFINITIONFor this report, the middle market (MM) is defined as US-based companies acquired through buyout transactions between $25 million and $1 billion. Note that minority deals are not included. The middle market is further broken down into the lower middle market (LMM; $25 million to $100 million), the core middle market (CMM; $100 million to $500 million) and the upper middle market (UMM; $500 million to $1 billion). This report covers only US-based

middle-market companies that have received some type of private equity investment.

TOTAL CAPITAL INVESTED/DEAL VALUETotal amount of equity and debt used in the private equity investment

Ex. $10 million of equity and $20 million of debt = $30 million of total capital investment

PitchBook’s total capital invested figures include deal amounts that were not collected by PitchBook but have been estimated using a multidimensional estimation matrix, which takes into account year of investment, deal type, platform v. add-on, industry and sector. Some datasets will include these extrapolated numbers while others will be compiled using only data collected directly by PitchBook; this explains any potential discrepancies that may be noticed.

EXITSThe report includes both full and partial exits of middle-market companies via corporate acquisition, secondary private equity buyout and initial public offering (IPO). PitchBook has utilized its multidimensional substitution and estimation matrix to estimate transaction sizes where the deal amount is unknown. For the MM company inventory,

we included companies that are expected to exit between $25 million and $1 billion.

FUNDRAISINGPitchBook defines middle-market funds as PE investment vehicles with between $100 million and $5 billion in capital commitments. The report only includes PE funds that have held their final close. Funds-of-funds and LP secondary

funds are not included.

LEAGUE TABLESAll league tables are compiled using deal counts for middle-market leveraged buyouts only to better reflect the other datasets within the report, with only the Lenders table also including all PitchBook debt round types in order to capture all debt provided to facilitate buyouts. For example, the Most Active Advisors league table shows the number of US-based middle-market buyouts that a firm advised on during the fourth quarter of 2016. Deals on which a firm advised multiple parties will only be counted once for that firm.

INTRODUCTION

Look up a company.

And its cap table.

And its investors.

And its EBITDA

multiples.

And its board

members.

In seconds.

The PitchBook Platform

has the data you need

to close your next deal.

Learn more at

pitchbook.com

Key takeaways

» Competition from strategic acquirers in 2016 forced PE investors to look for

value in smaller portfolio companies.

» As managers increasingly flocked to the lower middle market, deal value

in that space increased by 21.3% last year, across approximately the same

number of transactions as in 2015.

» Median transaction size for the entire middle market decreased to $134.0

million, the lowest in three years.

Much of the concern around PE dealmaking last year had to do with political

uncertainty and anticipated macroeconomic headwinds. And while those

certainly affected dealmaking, smaller middle-market activity showed resilience

due to less exposure to those very factors.

Shrewd investors shifted focus and deployed capital at smaller enterprise

values, making selective bets and finding relative bargains. In this more crowded

environment, deal sourcing will remain difficult, and operational prowess will be

put to the test. Yet, even with the aforementioned challenges, demand for the

asset class remains relatively strong and investor confidence is high.

We hope this report is useful in your practice. As always, feel free to send any

questions or comments to [email protected].

DYLAN E. COX

Analyst

The PitchBook PlatformThe data in this report comes from the PitchBook Platform–our data

software for VC, PE and M&A. Contact [email protected] to request

a free trial.

IN PARTNERSHIP WITH

CO-SPONSOR

SPONSORED BY

5 PITCHBOOK 2016 ANNUAL US PE MIDDLE MARKET REPORT

The new administration is moving fast. Less than a month after the inauguration, President Trump and Congressional Republicans

have begun to make good on campaign promises and Republican Party priorities. Moves to curb illegal immigration, build a Mexican

border wall, repeal the Affordable Care Act, select a Supreme Court nominee, withdraw from the Trans-Pacific Partnership and

tackle major tax reform signal swift policy changes that will create opportunities and challenges for middle-market PE.

On the regulatory side, important personnel hires and changes will drive policy in the new Republican-controlled Securities and

Exchange Commission. Trump has appointed attorney Jay Clayton, a partner at Sullivan & Cromwell LLP and an adviser to Goldman

Sachs, as new SEC chairman. Once Clayton is confirmed by the Senate and takes office, creating a new regulatory and enforcement

environment will be a top priority, but change will not happen overnight. ACG will take advantage of the interim period to establish

a relationship with new SEC staff before they begin their work of reviewing regulations in earnest. Steve Mnuchin, Trump’s pick

for treasury secretary, indicated that he may loosen some financial regulations under Dodd-Frank. While Mnuchin said in January

that he supports the Volcker Rule—restricting banks from making certain speculative investments—he suggested a desire to

make some changes to Dodd-Frank’s regulatory framework. The financial services industry is watching closely to see if the Trump

Administration halts the Labor Department fiduciary rule, which expands the “investment advice fiduciary” definition under the

Employee Retirement Income Security Act, slated to take effect in April.

Trump has generated significant momentum for comprehensive tax reform, voicing support for the so-called “Better Way Forward

on Tax Reform” unveiled by the House Ways and Means Committee in June. With a current corporate tax rate of 35%, House Speaker

Paul Ryan has called for cutting the corporate tax rate to 20%. Trump is pushing for an even lower rate. ACG agrees that a lower tax

rate would have a beneficial impact on private capital investors—but there will be tradeoffs for investors.

The new policy landscape is expected to directly impact private capital providers serving the middle market. Consider the

administration’s support for eliminating the ability to deduct interest on corporate debt. Since the early twentieth century, interest

deductibility has been a key driver of growth for capital providers and many small and midsize businesses. The House GOP Blueprint

limits interest deductibility in favor of 100% expensing. This would make borrowing more expensive for the majority of businesses.

Businesses of all sizes rely on credit to fund new investments and meet operating costs; without the ability to deduct interest

the incentive to invest and grow is diminished. The treatment of carried interest from capital gains to ordinary income is another

important issue for middle-market PE. In January, the Americans for Tax Reform recently stated that higher rates on capital gains

would have a disproportionate effect on investment partnerships and hurt investors such as pension funds, colleges and charities.

ATR suggested a model contained in the House GOP blueprint that would reduce the top rate on capital gains to 16.5%.

While the new administration is moving rapidly to implement campaign promises, President Trump will ultimately face fiscal realities

that will influence policy outcomes. With a slim Republican majority in the Senate, there will continue to be challenges in clearing the

necessary 60-vote threshold to move White House policy priorities forward. As the minority party, Senate Democrats will continue

to exert significant influence in that chamber and push back on many of Trump’s campaign promises, and some fiscally conservative

House Republicans will also push back on aggressive spending.

GARY LABRANCHE, FASAE, CAE

President & CEO

ACG Global

TRUMP’S FIRST 100 DAYS AND THEIR IMPACT ON PE by Gary LaBranche

IN PARTNERSHIP WITH

CO-SPONSOR

SPONSORED BY

6 PITCHBOOK 2016 ANNUAL US PE MIDDLE MARKET REPORT

Built solid.Communicate. Commit. Deliver.®

Since 2001, our record speaks for itself...

billion of net commitments new transactions private equity sponsors

of transactions closed as Administrative Agent, Sole Lender or Co-Agent since 2012

MANUFACTURING | DISTRIBUTION | SERVICES | CONSUMER PRODUCTS | HEALTHCARE | INSURANCE/FINANCIAL SERVICES | AEROSPACE & DEFENSE | TECHNOLOGY SERVICES

Madison Capital Funding is a subsidiary of New York Life Insurance Company. MCF-1722966

170-year commitment

exceptional success for ourselves and our partners.

THE BUYOUT CYCLE SLOWEDOverview

Deal flow stifled by corporate

competition

Middle-market PE deal value totaled

$366.8 billion across 1,908 deals in

2016, representing 8.1% and 11.6% year-

over-year decreases. The slowdown

was less pronounced than that of the

overall US PE marketplace, which

saw value and volume fall by 12.0%

and 14.4% respectively last year. PE

dealmaking, no matter the size, was

hindered by competition from large

corporate acquirers. These companies,

with inflated stock prices and record

amounts of cash on their balance

sheets, are able to move quickly and

justify higher multiples than many

financial sponsors are willing to pay.

US PE middle-market activity

After back-to-back robust years, activity finally subsided

US PE middle-market activity

$281

$352

$194

$94

$237

$272

$318

$301

$441

$399

$367

1,469

1,861

1,284

719

1,299 1,460

1,876 1,704

2,155 2,159 1,908

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Deal Value ($B) # of Deals Closed

Source: PitchBook

0

100

200

300

400

500

600

700

$0

$20

$40

$60

$80

$100

$120

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

2010 2011 2012 2013 2014 2015 2016

Deal Value # of Deals Closed

Source: PitchBook

IN PARTNERSHIP WITH

CO-SPONSOR

SPONSORED BY

8 PITCHBOOK 2016 ANNUAL US PE MIDDLE MARKET REPORT

US PE MM deals ($B) by segmentUS PE MM deals (#) by segment

Source: PitchBook Source: PitchBook

Fishing for value in the lower middle

market

The relative resilience of the middle

market can be attributed to its

insulation from strategic competitors.

That is, the smaller the PE fund, the

less likely it is to face competition from

large corporates for the most sought-

after acquisition targets. The same also

holds true within the middle market.

Competition is pushing financial

sponsors to search for relative value in

smaller portfolio companies. The lower

middle market (LMM)—enterprise

values between $25 million and $100

million—saw deal value increase by

21.3% this year, across approximately

the same number of transactions.

Meanwhile, 28.5% fewer deals were

completed in the upper middle market

(UMM)—deals between $500 million

and $1 billion—accounting for a 20.3%

decrease in value. With the move

to lower enterprise values, median

transactions size decreased to $134.0

million in 2016, the lowest in three

years.

Pricing cools, debt usage slides

As a result of the increased activity in

the LMM last year, median EV/EBITDA

multiples decreased by more than

a turn to 8.1x, with a caveat that the

population of eligible EBITDA multiples

is admittedly small. Smaller companies,

which tend to trade at lower multiples,

are also an integral part of the add-

on strategy that has become more

popular in private dealmaking lately.

Similarly to what we saw in the overall

PE and M&A markets in the US last

year, median debt usage fell to just

50% of enterprise value. For an

asset class that traditionally relies on

substantial leverage, the decreased

debt usage could lead to difficulty in

meeting LP expectations for future

distributions. However, the easing

of pricing pressures could lead to

a healthy re-balancing of leverage

and purchase prices, if not for larger

transactions, then at least in the middle

market.

Median US PE middle-market transaction size ($M)

$138.0

$134.0

$0

$20

$40

$60

$80

$100

$120

$140

$160

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Source: PitchBook

0

100

200

300

400

500

600

700

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

2013 2014 2015 2016

LMM CMM UMM

IN PARTNERSHIP WITH

CO-SPONSOR

SPONSORED BY

9 PITCHBOOK 2016 ANNUAL US PE MIDDLE MARKET REPORT

$0

$20

$40

$60

$80

$100

$120

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

2013 2014 2015 2016

LMM CMM UMM

FRANK FUMAI

Audit Partner

Deloitte & Touche, LLP

Frank is the National Audit

Leader for Deloitte’s Private

Equity practice. For over

20 years, he has served a

diverse range of clients, including private equity

firms, publicly-traded companies, registered

investment advisors, registered broker dealer

entities, and other investment funds. Frank has

an extensive understanding of the financial

services industry, SEC registrants, and the

rules impacting the investment management

industry. He is a contributor to Deloitte’s

Investment Management Industry Outlook and

Private Equity Fair Value Survey.

TIM MUNDY National Managing

Partner, PE Program

& West Coast Asset

Management Leader

Deloitte & Touche, LLP

With more than 27 years of

public and private investment management

audit and accounting experience, Tim

specializes in providing such services to asset

management companies. Tim is the national

managing partner for the private equity

portfolio company practice, providing services

committed to supporting private equity

enterprises and portfolios with distinction. As

Deloitte’s West Coast Regional Leader of the

Investment Management Services Group, Tim is

responsible for the coordination and oversight

of the regional practice serving asset managers

and their products, including mutual funds, and

alternative investments, such as hedge funds,

private equity/venture funds.

can help attract new investments with

their track record of success.

Particularly for the US lower middle

market, what do you deem are the

most important factors in value

creation for PE buyers looking to

increase their rate of adding on to

extant platforms?

Tim: The ability to address these three

threads will prove to be important for

value creation in my opinion:

• Are there operational improvements

to achieve?

• Can the companies commit

to controls, and thus quality

enhancement?

• Where is the overall industry

heading?

Frank: A big part of investment

success at a PE firm relies on

upfront due diligence and continued

monitoring of portfolio company

investments, which help lower overall

operational risk across portfolios

while achieving value creation and

increasing chance of success. For

example:

• Performing more operations

diligence in key functional areas of

a target company, and using data

and analytics to assess and improve

performance

• Looking for best practices or

functional areas at the top-performing

portfolio companies and sharing these

ideas across the entire portfolio

Many lower-middle-market firms

can improve functional business

processes that become more critical

as these portfolio companies grow and

mature. PE firms that recognize this

opportunity and support it through

programs can play an important role

in assisting management through

development stages that often carry

growing pains.

As used in this document, “Deloitte” means Deloitte & Touche LLP, a subsidiary of Deloitte LLP. Please see http://www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte USA LLP, Deloitte LLP and their respective subsidiaries. Certain services may not be available to attest clients under the rules and regulations of public accounting.

One of the evolving narratives in US

PE has been increased interest in even

lower reaches of the middle market.

How do you expect the level of

competition for quality middle-market

targets to fare in 2017, given the PE

industry’s dry powder overhang?

Tim: PE has grown dramatically over

the past decade but it has been

slowing over the past few years.

There has been a huge increase in the

number of PE firms over the last 20

years, now with approximately 5,000

PE firms globally. In response to this

competitive pressure, PE firms have

become more specialized and shifted

some of their focus to value creation

in the underlying portfolio companies.

Clearly competition will force PE firms

into new emerging markets, as well

as some niche strategies. We may

also see more joint deals amongst

competitors, as PE firms seek to put

their dry powder to work.

Frank: The competition, along with

higher values, has only intensified

the search for the perfect deal. This

search has extended across the

spectrum of firm sizes, including the

lower end of the middle market. PE

firms are seeking high-quality deals,

and in many of the best deals the PE

firms invest capital and their expertise

to drive value creation and future

investment returns. The dry powder

leads to competition, which ultimately

may lead to better match-making

between portfolio companies and PE

firms. Dry powder may also provide

some stability to the current valuations

of portfolio companies.

In this competitive dealmaking

environment, how can PE investors

further distinguish worthwhile targets

and, in turn, amend their strategies

to appeal to the management of

prospective businesses?

Tim: Specialize, specialize, and

specialize. You have to show that

you are focused on helping portfolio

companies achieve operational

change and growth, and bring value

proposition through evidence. PE

firms that have programs in place

to share leading practices across

portfolio companies may be favorably

positioned, in the eyes of potential

portfolio companies, compared to

competitors that do not. The ability to

share data analytics capabilities is an

example of an area where PE firms can

leverage scale and experience for the

benefit of portfolio companies. This

sharing of leading practices fosters

value creation, and tends to lower

overall operational risk. In this sense

the capabilities of portfolio companies

SPONSORED BY

10 PITCHBOOK 2016 ANNUAL US PE MIDDLE MARKET REPORT

US PE LMM deal flow

US PE LMM deals (#) by sector in 2016

Source: PitchBook. Transactions sized between $25 million and

$100 million comprise the lower middle market.

SURGE IN DEAL VALUELower-middle-market activity

Heavy investment in LMM. Deal value jumped 21.3% YoY.

$31

$37

$37

$17

$23

$27

$35

$29

$30

$30

$36

628

784

697

411

516 571

817

677

721 745 748

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Deal Value ($B) # of Deals Closed

36%

30%

8%

2%

8%

14%2%

B2B B2C Energy

Financial Services Healthcare IT

Materials & Resources Source: PitchBook

Select US LMM PE deals in 2016

Company Investor(s)Deal Size ($M)

West Star AviationNorwest Equity Partners

$99.3

Perforce Software Summit Partners $97.4

TRANZACTClayton, Dubilier & Rice

$85

Northstar Travel Group

Wasserstein Partners, Alberta Teachers’ Retirement Fund Board

$76

D&S Community Services

Comvest Partners $70

Source: PitchBook

IN PARTNERSHIP WITH

CO-SPONSOR

SPONSORED BY

11 PITCHBOOK 2016 ANNUAL US PE MIDDLE MARKET REPORT

US PE CMM deal flow

US PE CMM deals (#) by sector in 2016

CONTINUED DOWNTURNCore-middle-market activity

Activity in CMM remains fairly steady in 2016.

Source: PitchBook. Transactions sized between $100 million and

$500 million comprise the core middle market.

$139

$169

$104

$46

$100

$139

$159

$151

$213

$171

$173

675

832

502

251

574

702 821 813

1,106 1,020

879

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Deal Value ($B) # of Deals Closed

28%

24%11%

7%

15%

12%3%

B2B B2C Energy

Financial Services Healthcare IT

Materials & ResourcesSource: PitchBook

Select US CMM PE deals in 2016

Company Investor(s)Deal Size ($M)

Power Products Genstar Capital $496

Accuride Crestview Partners $460.9

Electro Rent Platinum Equity $382.2

TransMontaigne GPArcLight Capital Partners

$350

Bomgar Thoma Bravo $282

Source: PitchBook

IN PARTNERSHIP WITH

CO-SPONSOR

SPONSORED BY

12 PITCHBOOK 2016 ANNUAL US PE MIDDLE MARKET REPORT

US PE UMM deal flow

US PE UMM deals (#) by sector in 2016

A SHARP DECLINEUpper-middle-market activity

PE moves away from UMM. Deal value fell 20.3% YoY.

Source: PitchBook. Transactions sized between $500 million

and $1 billion comprise the upper middle market.

$111

$147

$54

$31

$113

$107

$123

$121

$197

$198

$158

167

244

86 57

209 187

238 214

328

393

281

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Deal Value ($B) # of Deals Closed

19%

17%

14%3%

19%

28%

B2B B2C Energy

Financial Services Healthcare IT

Materials & ResourcesSource: PitchBook

Select US UMM PE deals in 2016

Company Investor(s)Deal Size ($M)

Masergy Berkshire Partners $900

Vivid Seats Vista Equity Partners $825

American Bath Group Lone Star Funds $750

Great Expressions Dental Centers

Roark Capital Group $675

Xura Siris Capital $649

Source: PitchBook

IN PARTNERSHIP WITH

CO-SPONSOR

SPONSORED BY

13 PITCHBOOK 2016 ANNUAL US PE MIDDLE MARKET REPORT

T H E P R E M I E R N E T W O R K I N G & D E A L F L O W E V E N T F O R

M I D D L E - M A R K E T D E A L - M A K E R S F E A T U R I N G K E Y N O T E

S P E A K E R E A R V I N “ M A G I C ” J O H N S O N .

W W W . I N T E R G R O W T H . O R G

IT’S YOUR DEAL.

© 2017 Association for Corporate Growth. All Rights Reserved.

A GROWING INVENTORYUS PE middle-market company inventory

Inventory is increasingly concentrated in relatively younger companies

US PE middle-market company inventory by count and year

US PE MM median hold period (years) by exit type

Middle-market companies make up 74.1% of all PE-backed company inventory in the US.

1,9432,254

2,670

3,1163,490 3,647 3,891

4,1264,388 4,594

4,8485,120 5,310

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

2011-2016 2006-2010

2000-2005 Pre-2000

Year of Investment

6.4

4.8

5.5 5.4

4.8

5.1

0.5

1.5

2.5

3.5

4.5

5.5

6.5

7.5

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

IPOs Corporate Secondary Buyout

Source: PitchBook

Source: PitchBook

IN PARTNERSHIP WITH

CO-SPONSOR

SPONSORED BY

15 PITCHBOOK 2016 ANNUAL US PE MIDDLE MARKET REPORT

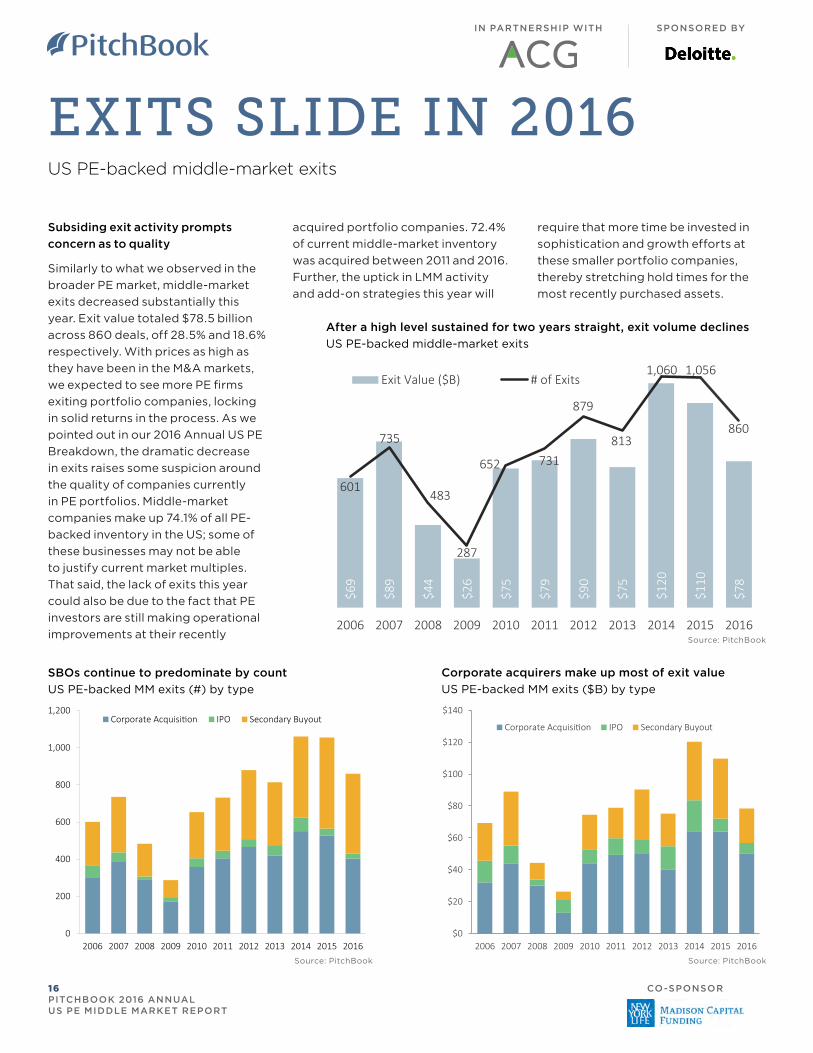

EXITS SLIDE IN 2016US PE-backed middle-market exits

Subsiding exit activity prompts

concern as to quality

Similarly to what we observed in the

broader PE market, middle-market

exits decreased substantially this

year. Exit value totaled $78.5 billion

across 860 deals, off 28.5% and 18.6%

respectively. With prices as high as

they have been in the M&A markets,

we expected to see more PE firms

exiting portfolio companies, locking

in solid returns in the process. As we

pointed out in our 2016 Annual US PE

Breakdown, the dramatic decrease

in exits raises some suspicion around

the quality of companies currently

in PE portfolios. Middle-market

companies make up 74.1% of all PE-

backed inventory in the US; some of

these businesses may not be able

to justify current market multiples.

That said, the lack of exits this year

could also be due to the fact that PE

investors are still making operational

improvements at their recently

SBOs continue to predominate by count

US PE-backed MM exits (#) by type

After a high level sustained for two years straight, exit volume declines

US PE-backed middle-market exits$6

9

$89

$44

$26

$75

$79

$90

$75

$120

$110

$78

601

735

483

287

652 731

879

813

1,060 1,056

860

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Exit Value ($B) # of Exits

0

200

400

600

800

1,000

1,200

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Corporate Acquisition IPO Secondary Buyout

Source: PitchBook

Source: PitchBook

Corporate acquirers make up most of exit value

US PE-backed MM exits ($B) by type

$0

$20

$40

$60

$80

$100

$120

$140

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Corporate Acquisition IPO Secondary Buyout

Source: PitchBook

acquired portfolio companies. 72.4%

of current middle-market inventory

was acquired between 2011 and 2016.

Further, the uptick in LMM activity

and add-on strategies this year will

require that more time be invested in

sophistication and growth efforts at

these smaller portfolio companies,

thereby stretching hold times for the

most recently purchased assets.

IN PARTNERSHIP WITH

CO-SPONSOR

SPONSORED BY

16 PITCHBOOK 2016 ANNUAL US PE MIDDLE MARKET REPORT

FUNDRAISING

Fundraising flattens by count

US PE middle-market fundraising by year

Fundraising count plateaus

Though they garnered about $15 billion

less in capital commitments, virtually

the same number of middle-market

A decrease of 19.4% YoY

Average US PE middle-market buyout fund size

Steady LMM-focused fund volume

US LMM PE funds

$118

$121

$113

$77

$52

$86

$90

$108

$133

$125

$110

168

193172

99 94

117 119

169 177165 164

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Capital Raised ($B) # of Funds Closed

Source: PitchBook

Source: PitchBook

0

20

40

60

80

100

120

2010 2011 2012 2013 2014 2015 201650%

52%

54%

56%

58%

60%

62%

64%

66%

68%Fund Count % in LMM ($100M-$500M)

Source: PitchBook

funds closed last year as did in 2015.

In our Annual US PE Breakdown, we

observed that larger funds have had

more success and accounted for a

higher proportion of total capital

commitments to PE. This trend,

however, is markedly different in the

middle market. Average buyout fund

size decreased by 19.4% last year to

$687.9 million. As firms target more

LMM companies, the average check

size for equity contributions will come

down, which could be contributing to

the decrease in fund size. The PE market

is showing signs of splitting itself into

two distinct segments: larger, more

institutionalized firms and smaller,

possibly nimbler specialty buyout

shops, such as LMM-focused PE shops.

The latter of which are certainly still in

high demand. In a sign of confidence,

the number of first-time funds to

close hit a five-year high last year, as

experienced associates are branching

out on their own in order to capitalize on

the quite palpable demand from LPs.

$853.0

$687.9

$500

$600

$700

$800

$900

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Average Buyout Fund Size ($M)

IN PARTNERSHIP WITH

CO-SPONSOR

SPONSORED BY

17 PITCHBOOK 2016 ANNUAL US PE MIDDLE MARKET REPORT

MIDDLE MARKET LEAGUE TABLES

4Q 2016

HarbourVest Partners 19

Audax Group 18

ABRY Partners 11

AlpInvest Partners 11

Genstar Capital 11

Hellman & Friedman 9

GTCR 8

Maranon Capital 8

H.I.G. Capital 6

Huron Capital Partners 6

The Riverside Company 6

Advent International 5

AEA Investors 5

Aquiline Capital Partners 5

Charlesbank Capital Partnesr 5

GoldPoint Partners 5

Kelso & Company 5

The Carlyle Group 5

Kirkland & Ellis 40

Jones Day 17

Paul Hastings 13

Latham & Watkins 12

Ropes & Gray 12

Weil, Gotshal & Manges 12

Morgan, Lewis & Bockius 9

Paul, Weiss, Rifkind, Wharton & Garrison

9

DLA Piper 7

Finn Dixon & Herling 7

Greenberg Traurig 7

Choate Hall & Stewart 6

McDermott Will & Emery 6

Morrison & Foerster 6

Shearman & Sterling 6

Covington & Burling 5

Honigman Miller Schwartz and Cohn

5

Most active investors by deal count

Most active law firms by deal count

Antares Capital 23

Madison Capital Funding 16

Twin Brook Capital Partners 11

Houlihan Lokey 15

Harris Williams & Co. 8

Lincoln International 8

Robert W. Baird & Co. 8

William Blair & Company 8

Piper Jaffray 6

Stifel 6

BB&T Capital Markets 5

Most active advisors by deal count

Source: PitchBook

Source: PitchBook

Source: PitchBook

Source: PitchBook

Note: The lenders’ table was updated as of 3/2/2017

given errors in deal attribution.

BMO Harris Bank 10

Monroe Capital 9

NewStar Financial 7

NXT Capital 7

RBC Capital Markets 5

Citizens Bank 5

Golub Capital 4

Fifth Street 4

KeyBanc Capital Markets 4

ORIX 4

PNC Bank 4

Webster Financial 4

Most active lenders by deal count

Most active lenders by deal count, ctd.

CHILDS Advisory Partners 5

Moelis & Company 5

RBC Capital Markets 5

The Jordan Edmiston Group 5

Most active advisors by deal count, ctd.

IN PARTNERSHIP WITH

CO-SPONSOR

SPONSORED BY

18 PITCHBOOK 2016 ANNUAL US PE MIDDLE MARKET REPORT

Madison Capital, founded in 2001, and headquartered in Chicago, Illinois, is a premier finance company focused exclusively on the corporate financing needs of middle market private equity firms. Madison Capital has closed transactions with over 255 different private equity firms and provides enterprise-value

leveraged financing for leveraged buyouts, management buyouts, add-on acquisitions and recapitalizations. Madison Capital Funding LLC is a subsidiary of New York Life Insurance Company. Additional information may be found at: www.mcfllc.com

See how the PitchBook Platform can

help your private equity firm close your

next deal.

We do EBITDA multiples,private comps,valuations,market trends,growth metrics.

You build a better portfolio.