upuuppup scaling non-deal roadshow …/media/mlt/newsroom...scaling non-deal roadshow -presentation...

TRANSCRIPT

Non-deal Roadshow -Presentation

September-October 2007

SCALING

UP

UP

UP

UP

1

1

�MapletreeLog -Overview

�Snapshot

�Our portfolio

�Scaling up

�Capital management

�Total returns

�Outlook

Agen

daAg

enda

Agen

daAg

enda

22

2

�First Asia-focused logistics REIT in Singapore

�Sponsor’s historical links with Port Authority of Singapore

�Focus: Logistics-related real estate assets in Asia

�S$2.4billion portfolio of 74 properties : Singapore (44), Malaysia (11),

Hong Kong (8), Japan (7) and China (4)

�Strategy: yield + growth

�Strategic Relationships: Itochu, CIMB and Embassy

�Sponsor’s Support: 5-year right of first refusal until 2010 from the Sponsor for

logistics assets

Ove

rvie

w o

f Map

letre

eLog

Ove

rvie

w o

f Map

letre

eLog

Ove

rvie

w o

f Map

letre

eLog

Ove

rvie

w o

f Map

letre

eLog

3

3

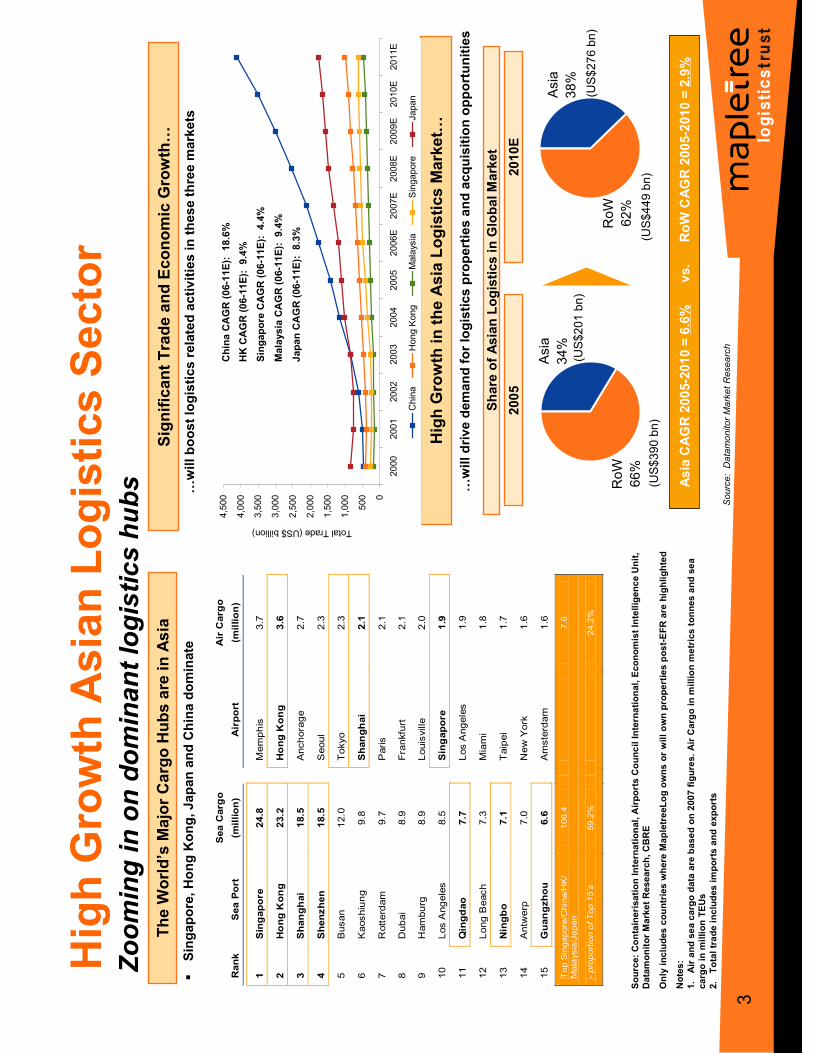

Asia

34%

RoW

66%

Asia

38%

RoW

62%

Zooming in on dominant logistics hubs

Significant Trade and Economic Growth…

…will boost logistics related activities in these three markets

High Growth in the Asia Logistics Market…

…will drive demand for logistics properties and acquisition opportunities

The W

orld’s Major Cargo Hubs are in Asia

Source: Datamonitor Market Research

High Growth Asian Logistics Sector

Source: Containerisation International, Airports Council International, Economist Intelligence Unit,

Datamonitor Market Research, CBRE

Only includes countries where MapletreeLog owns or will own properties post-EFR are highlighted

Notes:

1. Air and sea cargo data are based on 2007 figures. Air Cargoin million metrics tonnes and sea

cargo in million TEUs

2. Total trade includes imports and exports

Rank

Sea Port

Sea Cargo

(million)

Airport

Air Cargo

(million)

1

Singapore

24.8

Memphis

3.7

2

Hong Kong

23.2

Hong Kong

3.6

3

Shanghai

18.5

Anchorage

2.7

4

Shenzhen

18.5

Seoul

2.3

5

Busan

12.0

Tokyo

2.3

6

Kaoshiung

9.8

Shanghai

2.1

7

Rotterdam

9.7

Paris

2.1

8

Dubai

8.9

Frankfurt

2.1

9

Hamburg

8.9

Louisville

2.0

10

Los Angeles

8.5

Singapore

1.9

11

Qingdao

7.7

Los Angeles

1.9

12

Long Beach

7.3

Miami

1.8

13

Ningbo

7.1

Taipei

1.7

14

Antwerp

7.0

New York

1.6

15

Guangzhou

6.6

Amsterdam

1.6

Top Singapore/China/HK/

Malaysia/Japan

106.4

7.6

- proportion of Top 15’s

59.2%

24.2%

�Singapore, Hong Kong, Japan and China dominate

2005

2010E

(US$201 bn)

(US$276 bn)

(US$390 bn)

(US$449 bn)

Asia CAGR 2005-2010 = 6.6%

vs. RoW CAGR 2005-2010 = 2.9%

Share of Asian Logistics in Global Market

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2000

2001

2002

2003

2004

2005

2006E

2007E

2008E

2009E

2010E

2011E

Total Trade (US$ billion)

China

Hong Kong

Malaysia

Singapore

Japan

China CAGR (06-11E): 18.6%

HK CAGR (06-11E): 9.4%

Malaysia CAGR (06-11E): 9.4%

Singapore CAGR (06-11E): 4.4%

Japan CAGR (06-11E): 8.3%

4

4

�100% owned by Temasek Holdings

�Form

ed in 2000 to hold PSA’s non-port property

assets

�S$4.5billion asset base –

office, logistics, industrial

and retail/lifestyle properties

�S$2.1billion AUM in S’pore and Asia

�Extensive regional presence –

offices in Ho Chi

Minh city, Hong Kong, Kuala Lumpur, Beijing,

Shanghai and Tokyo

Our

Spo

nsor

O

ur S

pons

or

Our

Spo

nsor

O

ur S

pons

or - ---

MIP

LM

IPL

MIP

LM

IPL

55

5

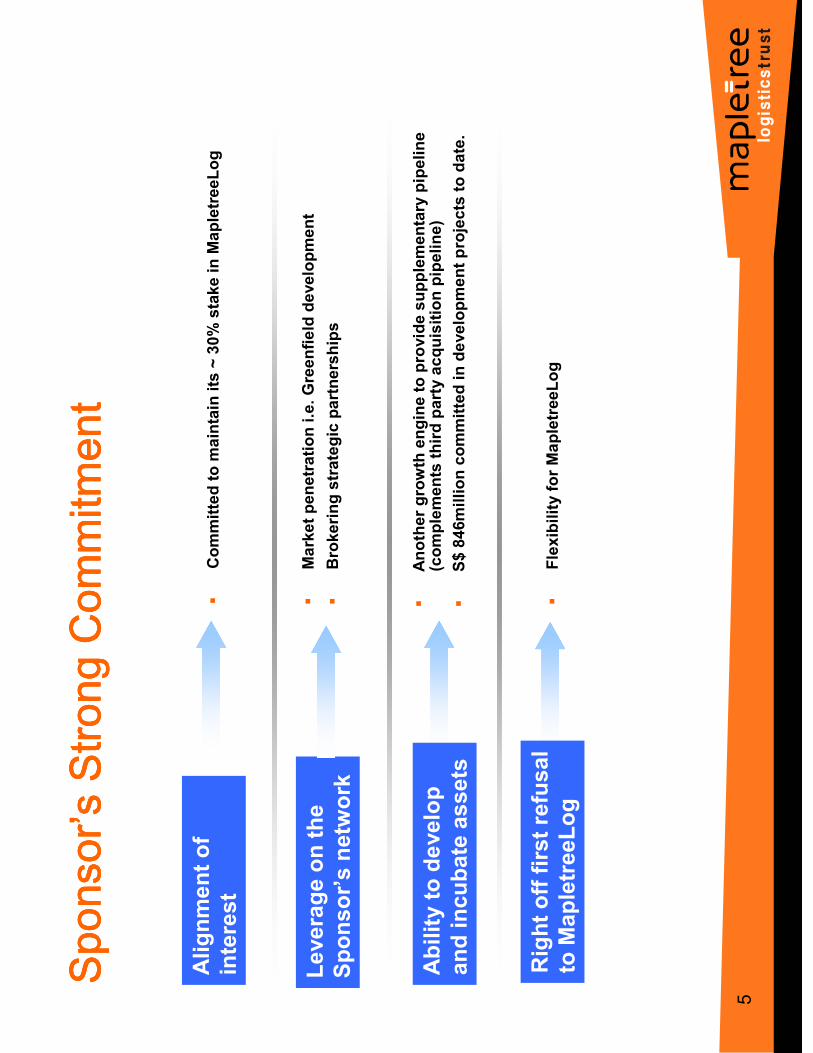

�Committed to maintain its ~ 30% stake in MapletreeLog

Spon

sor’s

Stro

ng C

omm

itmen

tSp

onso

r’s S

trong

Com

mitm

ent

Spon

sor’s

Stro

ng C

omm

itmen

tSp

onso

r’s S

trong

Com

mitm

ent

Alignment of

interest

Ability to develop

and incubate assets

�Another growth engine to provide supplementary pipeline

(complements third party acquisition pipeline)

�Market penetration i.e. Greenfield development

�Brokering strategic partnerships

Leverage on the

Sponsor’s network

�Flexibility for MapletreeLog

Right off first refusal

to MapletreeLog

�S$ 846million committed in development projects to date.

6

6

�MapletreeLog -Overview

�Snapshot

�Our portfolio

�Scaling up

�Capital Management

�Total Returns

�Outlook

Agenda

7

7

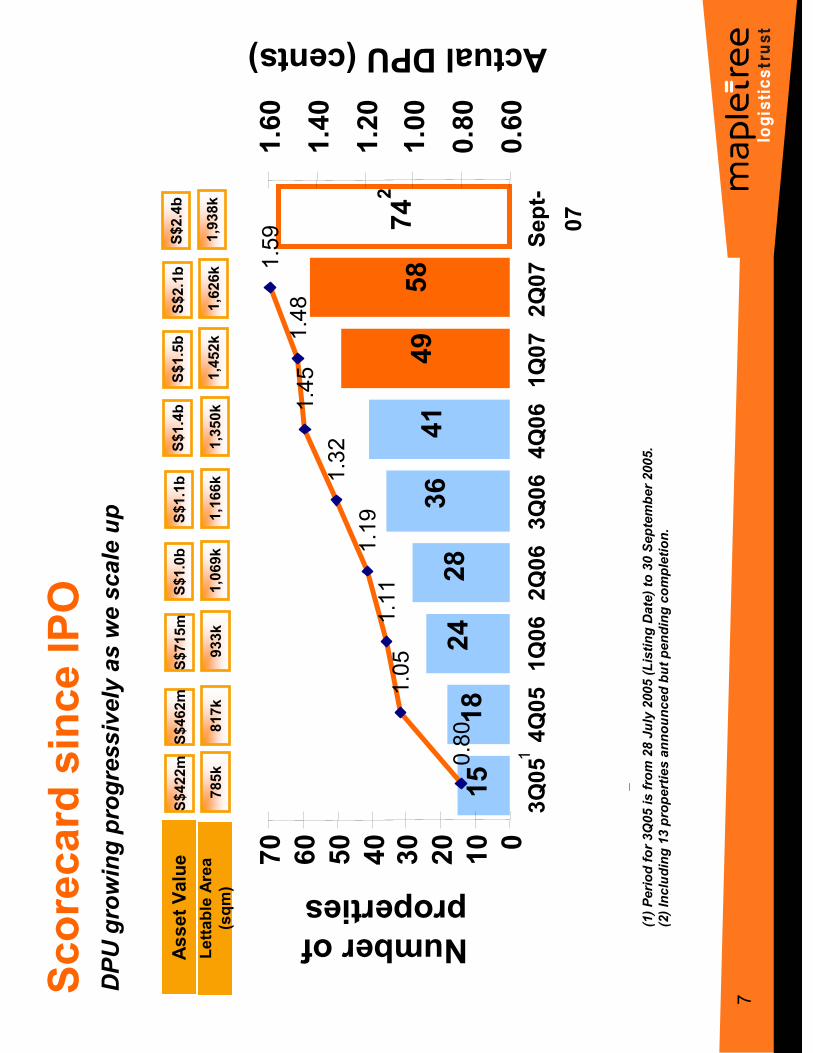

Scorecard since IPO

(1) Period for 3Q05 is from 28 July 2005 (Listing Date) to 30 September 2005.

(2) Including 13 properties announced but pending completion.

DPU growing progressively as we scale up

*

Asset Value

S$422m

S$1.0b

S$1.1b

S$1.4b

S$1.5b

2Q07 forecast DPU1(1.42 cts)

S$2.1b

S$715m

S$462m

2

S$2.4b

742

58

49

41

15

18

24

28

36

0.80

1.05

1.11

1.19

1.32

1.45

1.48

1.59

0

10

20

3040

50

60

70

3Q05

4Q05

1Q06

2Q06

3Q06

4Q06

1Q07

2Q07Sept-

07

Number of properties

0.60

0.80

1.00

1.20

1.40

1.60

Actual DPU (cents)

1

Lettable Area

(sqm)

785k

1,069k

1,166k

1,350k

1,452k

1,626k

933k

817k

1,938k

8

8

Geographical Diversification

Japa

nJa

pan

Japa

nJa

pan

1% 1%1%1%C

hina

Chi

naC

hina

Chi

na1% 1%1%1%

Mal

aysi

aM

alay

sia

Mal

aysi

aM

alay

sia

4% 4%4%4%

Hon

g H

ong

Hon

g H

ong

Kon

gK

ong

Kon

gK

ong

28%

28%

28%

28%

Sin

gapo

reS

inga

pore

Sin

gapo

reS

inga

pore

66%

66%

66%

66%

Japa

nJa

pan

Japa

nJa

pan

1% 1%1%1%C

hina

Chi

naC

hina

Chi

na1% 1%1%1%

Mal

aysi

aM

alay

sia

Mal

aysi

aM

alay

sia

4% 4%4%4%

Hon

g H

ong

Hon

g H

ong

Kon

gK

ong

Kon

gK

ong

28%

28%

28%

28%

Sin

gapo

reS

inga

pore

Sin

gapo

reS

inga

pore

66%

66%

66%

66%

Japa

nJa

pan

Japa

nJa

pan

11%

11%

11%

11%

Chi

naC

hina

Chi

naC

hina

2% 2%2%2%

Mal

aysi

aM

alay

sia

Mal

aysi

aM

alay

sia

3% 3%3%3%

Hon

g H

ong

Hon

g H

ong

Kon

gK

ong

Kon

gK

ong

26%

26%

26%

26%

Sin

gapo

reS

inga

pore

Sin

gapo

reS

inga

pore

58%

58%

58%

58%

Japa

nJa

pan

Japa

nJa

pan

11%

11%

11%

11%

Chi

naC

hina

Chi

naC

hina

2% 2%2%2%

Mal

aysi

aM

alay

sia

Mal

aysi

aM

alay

sia

3% 3%3%3%

Hon

g H

ong

Hon

g H

ong

Kon

gK

ong

Kon

gK

ong

26%

26%

26%

26%

Sin

gapo

reS

inga

pore

Sin

gapo

reS

inga

pore

58%

58%

58%

58%

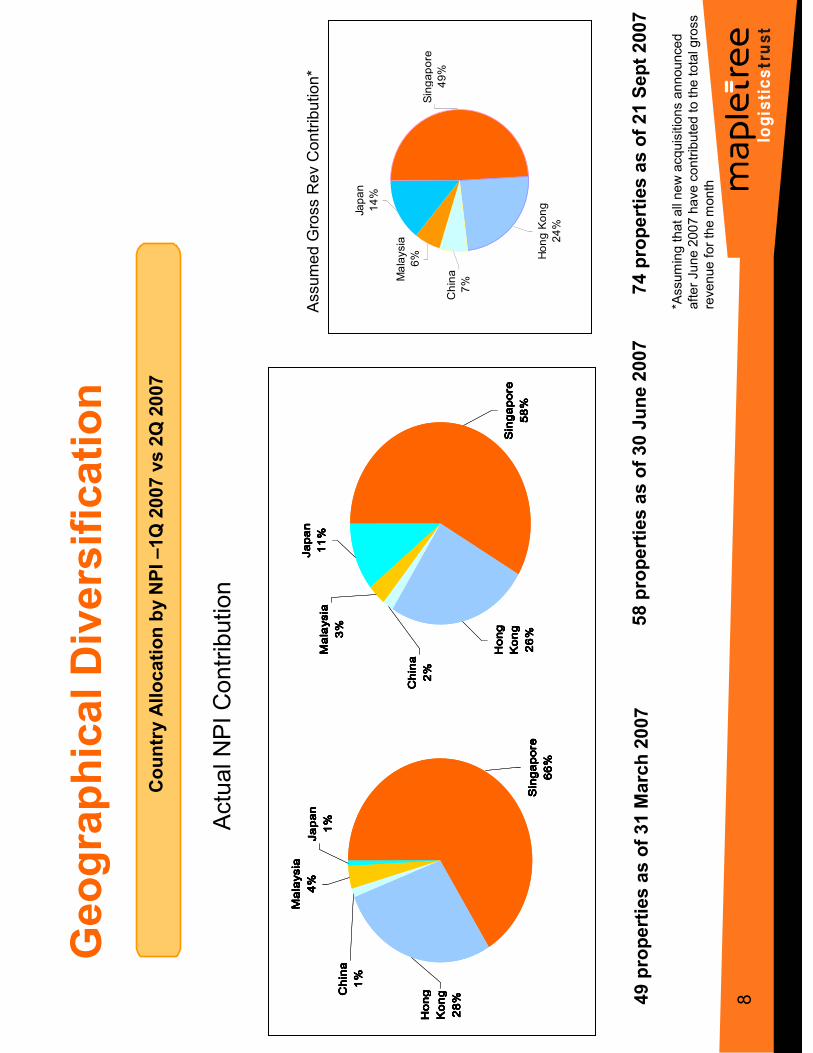

Country Allocation by NPI –1Q 2007 vs 2Q 2007

49 properties as of 31 March 2007

58 properties as of 30 June 2007

74 properties as of 21 Sept 2007

Singapore

49%

China

7%

Hong Kong

24%

Malaysia

6%

Japan

14%

Actual NPI Contribution

Assumed Gross Rev Contribution*

*Assuming that all new acquisitions announced

after June 2007 have contributed to the total gross

revenue for the m

onth

9

9

Snapshot @ 30 June 2007

Footnotes:

1.

Include derivative financial instruments, at fair value, liability of S$14.9 m

illion.

2.

Include net derivative financial instruments, at fair value, liability of S$3.6 m

illion.

3.

Include net derivative financial instruments, at fair value, liability of S$14.3 m

illion. Excluding this, the

NAV per unit would be S$0.86.

4.

Include net derivative financial instruments, at fair value, liability of S$3.0 m

illion. Excluding this, the NAV

per unit would be S$0.87.

5.

Ratio of EBITDA over interest expense for period up to balance sheet date.

Balance Sheet

31 Mar 2007

S$’000

30 Jun 2007

S$’000

Total assets

1,637,450

2,201,186

Total liabilities

700,334 1

1,243,440 2

Net assets attributable to unitholders

937,116

957,746

NAV per Unit

S$0.85 3

S$0.86 4

Financial Ratio

Aggregate Leverage Ratio

39.0%

54.0%

Total Debt

S$630million

S$1182million

Weighted Average Annualised Interest Rate

4.1%

3.3%

Interest Service Ratio 5

3.4 times

3.3 times

10

10

�MapletreeLog -Overview

�Snapshot

�Our portfolio

�Scaling up

�Capital management

�Total returns

�Outlook

Agen

daAg

enda

Agen

daAg

enda

11

11

6.0%

0.0%

4.9%

0.0%

3.6%

3.0%

2.2%

2.1%

2.1%

0.0%

4.8%

4.3%

3.8%

3.7%

2.8%

2.4%

1.7%

1.7%

1.6%

1.6%

0%

1%

2%

3%

4%

5%

6%

7%

49 properties as at 31 Mar 2007

58 properties as at 30 Jun 2007

Better Tenant Diversification

Reduction in top ten tenants concentration from 29.5% to 28.5% @

30 Jun 2007

…increasing the number of quality tenants from 133 to 189

1

Ever Gain

Group

Teckwah

Industrial

Taiun

NEC

Logistics

Nichirei

Corporation

Fu Yu

corporation

Crescendas

Distribution

DG

Logistik

Senko Co

Vopak

Term

inals

Multinational logistics operators

Singapore listed groups

Private groups

Top ten tenants by gross revenue

12

12

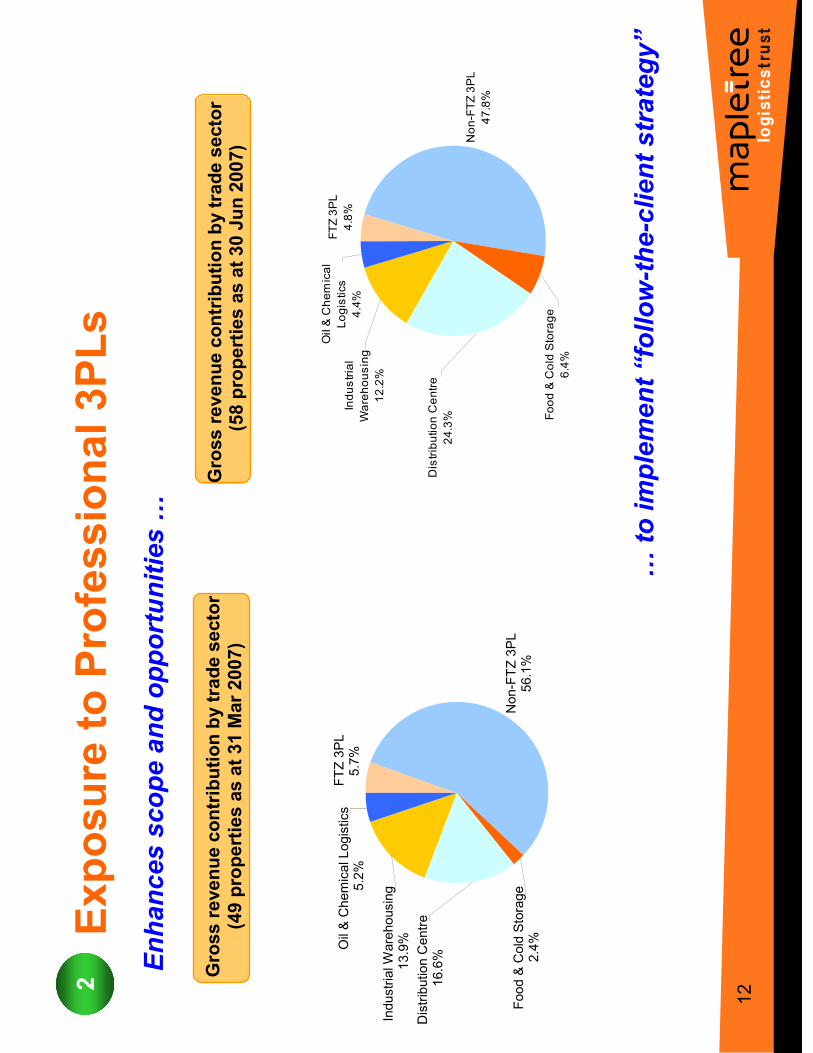

Exposure to Professional 3PLs

Enhances scope and opportunities …

2

…to implement “follow-the-client strategy”

Gross revenue contribution by trade sector

(58 properties as at 30 Jun 2007)

Gross revenue contribution by trade sector

(49 properties as at 31 Mar 2007)

FTZ 3PL

4.8%

Non-FTZ 3PL

47.8%

Oil & Chemical

Logistics

4.4%

Distribution Centre

24.3% Food & Cold Storage

6.4%

Industrial

Warehousing

12.2%

FTZ 3PL

5.7%

Non-FTZ 3PL

56.1%

Industrial W

arehousing

13.9%

Food & Cold Storage

2.4%

Distribution Centre

16.6%

Oil & Chemical Logistics

5.2%

13

13

Shorter Leases to Tap Growing Markets

Lease Expiry Profile by Gross Revenue

5.4 years

6.4 years

Weighted average lease term

to expiry

58 properties

as at 30 Jun 2007

49 properties

as at 31 Mar 2007

3

10.2%

19.5%

10.7%

5.6%

32.0%

5.9%

15.8%

38.6%

18.3%

13.7%

8.3%

5.8%

6.4%

8.5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Expiring in

2007

Expiring in

2008

Expiring in

2009

Expiring in

2010

Expiring in

2011

Expiring in

2012

Expiring after

2012

49 properties as at 31 Mar 2007

58 properties as at 30 Jun 2007

Shorter Leases to tap

growing markets (47%)

Longer leases form

the

stable core (53%)

14

14

Leas

e Pr

ofile

Leas

e Pr

ofile

Leas

e Pr

ofile

Leas

e Pr

ofile

S$13.1 m

S$7.2 m (55%)

S$5.9 m (45%)

Gross revenue per mth(%)

1.6

1.2 (75%)

0.4 (25%)

Lettable area (million sqm)

Total

Long Leases (>3 yrs)

Short Leases (=<3 yrs)

55%

55%

55%

55%

45%

45%

45%

45%

Shor

t Lea

ses

(<3

yrs)

Shor

t Lea

ses

(<3

yrs)

Shor

t Lea

ses

(<3

yrs)

Shor

t Lea

ses

(<3

yrs)

Long

Lea

ses

(>3

yrs)

Long

Lea

ses

(>3

yrs)

Long

Lea

ses

(>3

yrs)

Long

Lea

ses

(>3

yrs)

15

15

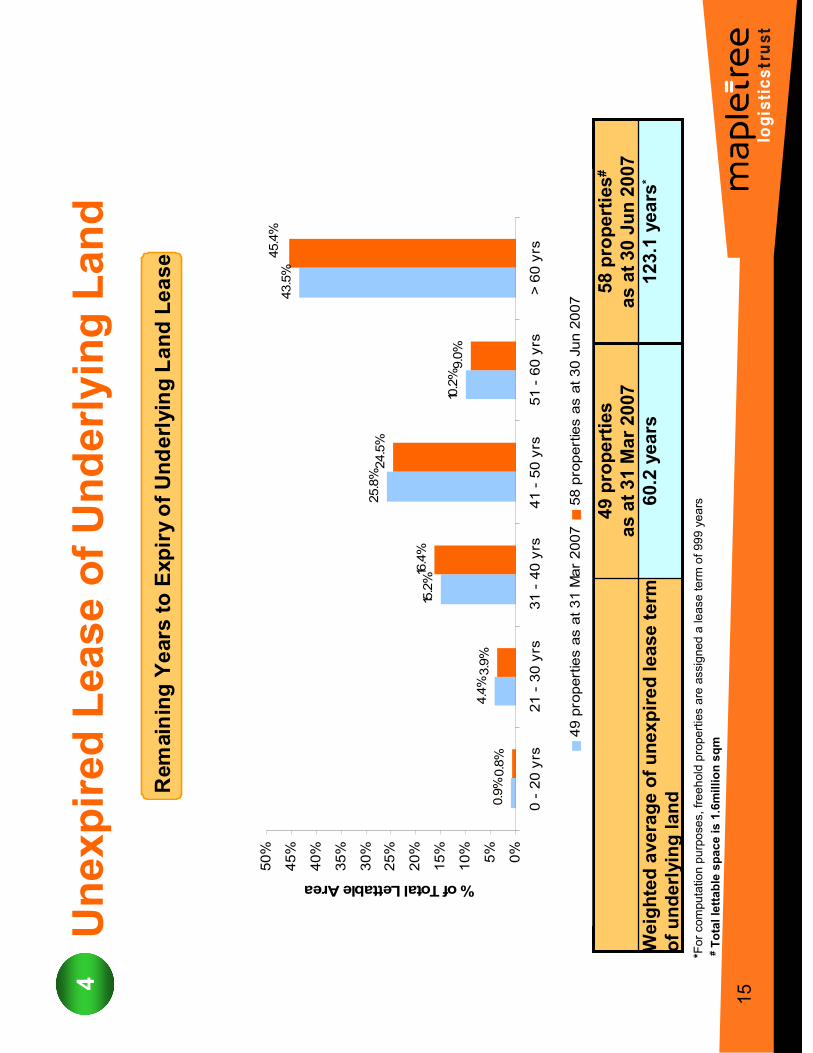

Unexpired Lease of Underlying Land

123.1 years

*60.2 years

Weighted average of unexpired lease term

of underlying land

58 properties#

as at 30 Jun 2007

49 properties

as at 31 Mar 2007

Remaining Years to Expiry of Underlying Land Lease

4

*For computation purposes, freehold properties are assigned a lease term

of 999 years

0.9%

4.4%

15.2%

25.8%

10.2%

43.5%

0.8%

3.9%

16.4%

9.0%

24.5%

45.4%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0 - 20 yrs

21 - 30 yrs

31 - 40 yrs

41 - 50 yrs

51 - 60 yrs

> 60 yrs

% of Total Lettable Area

49 properties as at 31 Mar 2007

58 properties as at 30 Jun 2007

#Total lettable space is 1.6million sqm

16

16

�MapletreeLog -Overview

�Snapshot

�Our portfolio

�Scaling up

�Capital management

�Total Returns

�Outlook

Agen

daAg

enda

Agen

daAg

enda

17

17

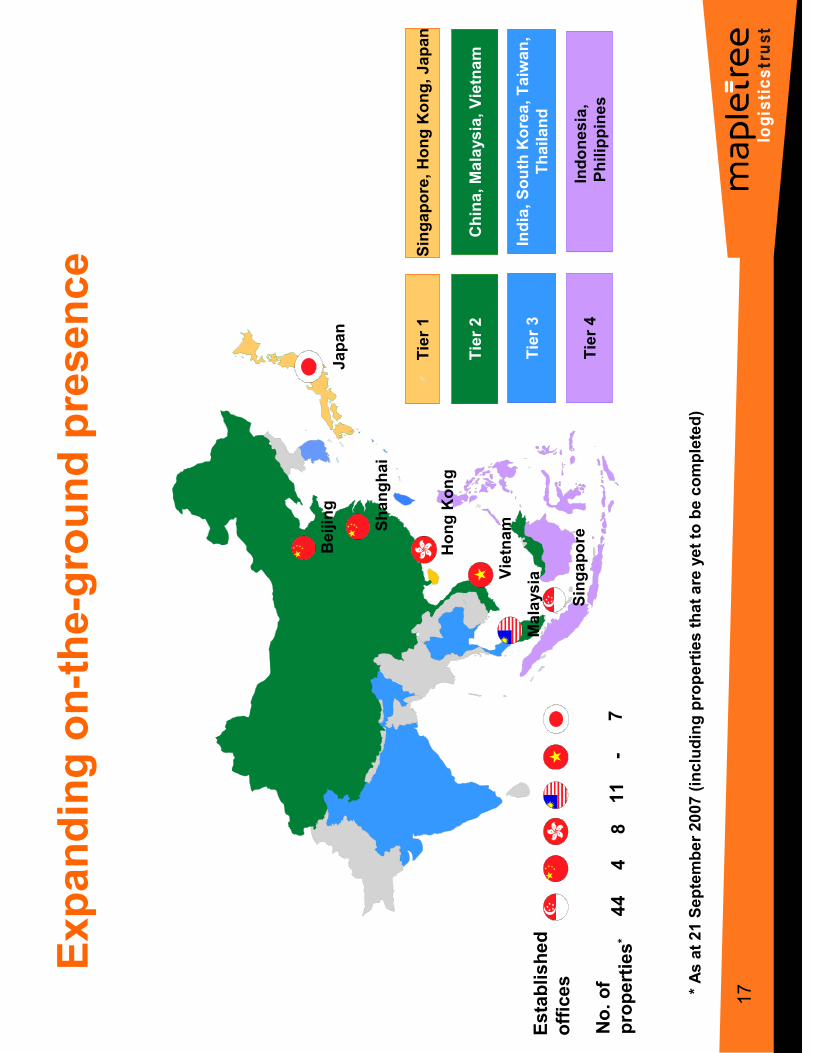

Tier 4

Tier 1

Tier 2

Tier 3

Singapore, Hong Kong, Japan

China, Malaysia, Vietnam

India, South Korea, Taiwan,

Thailand

Indonesia,

Philippines

Established

offices

Singapore

Shanghai

Hong Kong

Malaysia

Japan

Vietnam

Beijing

Expanding on-the-ground presence

No. of

properties*

* As at 21 September 2007 (including properties that are yet to be completed)

44

11

-7

48

18

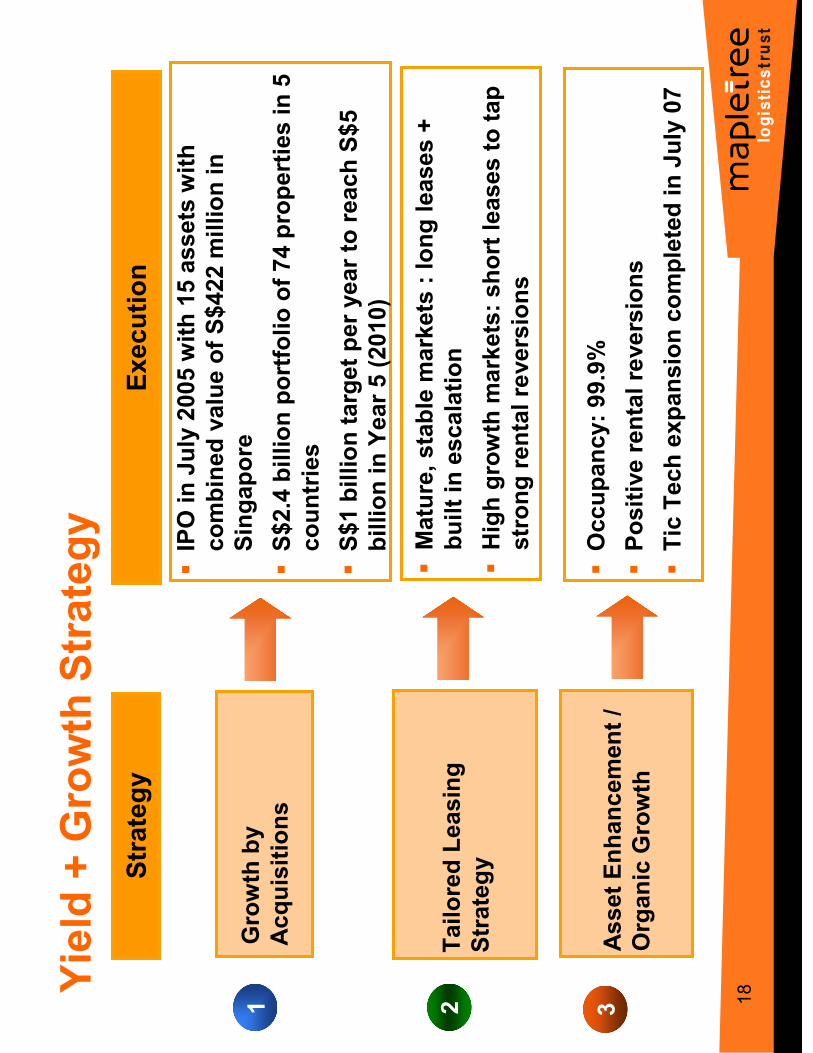

18Yield + Growth Strategy

Execution

�IPO in July 2005 with 15 assets with

combined value of S$422 million in

Singapore

�S$2.4 billion portfolio of 74 properties in 5

countries

�S$1 billion target per year to reach S$5

billion in Year 5 (2010)

�Mature, stable markets : long leases +

built in escalation

�High growth markets: short leases to tap

strong rental reversions

Strategy

Growth by

Acquisitions

Tailored Leasing

Strategy

Asset Enhancement /

Organic Growth

�Occupancy: 99.9%

�Positive rental reversions

�Tic Tech expansion completed in July 07

1 2 3

1919

19

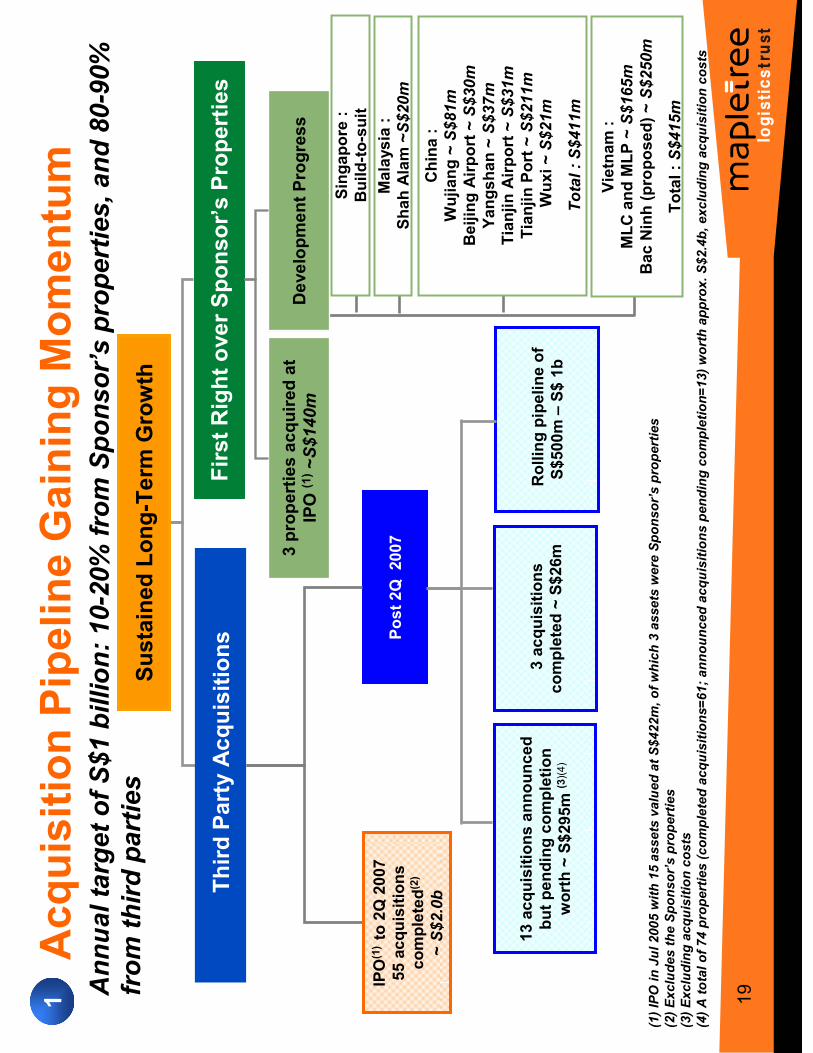

(1) IPO in Jul 2005 with 15 assets valued at S$422m, of which 3 assets were Sponsor’s properties

(2) Excludes the Sponsor’s properties

(3) Excluding acquisition costs

(4) A total of 74 properties (completed acquisitions=61; announced acquisitions pending completion=13) worth approx. S$2.4b, excluding acquisition costs

Post 2Q 2007

IPO(1) to 2Q 2007

55 acquisitions

completed(2)

~ S$2.0b

Annual target of S$1 billion: 10-20% from Sponsor’s properties, and 80-90%

from third parties

Acquisition Pipeline Gaining Momentum

Third Party Acquisitions

Sustained Long-Term

Growth

First Right over Sponsor’s Properties

3 properties acquired at

IPO (1)~S$140m

Development Progress

Singapore :

Build-to-suit

Malaysia :

Shah Alam ~S$20m

China :

Wujiang ~ S$81m

Beijing Airport ~ S$30m

Yangshan ~ S$37m

Tianjin Airport ~ S$31m

Tianjin Port~ S$211m

Wuxi ~ S$21m

Total : S$411m

Vietnam :

MLC and MLP ~ S$165m

Bac Ninh (proposed)~ S$250m

Total :S$415m

1

13 acquisitions announced

but pending completion

worth ~ S$295m (3)(4)

Rolling pipeline of

S$500m –S$ 1b

3 acquisitions

completed ~ S$26m

20

20

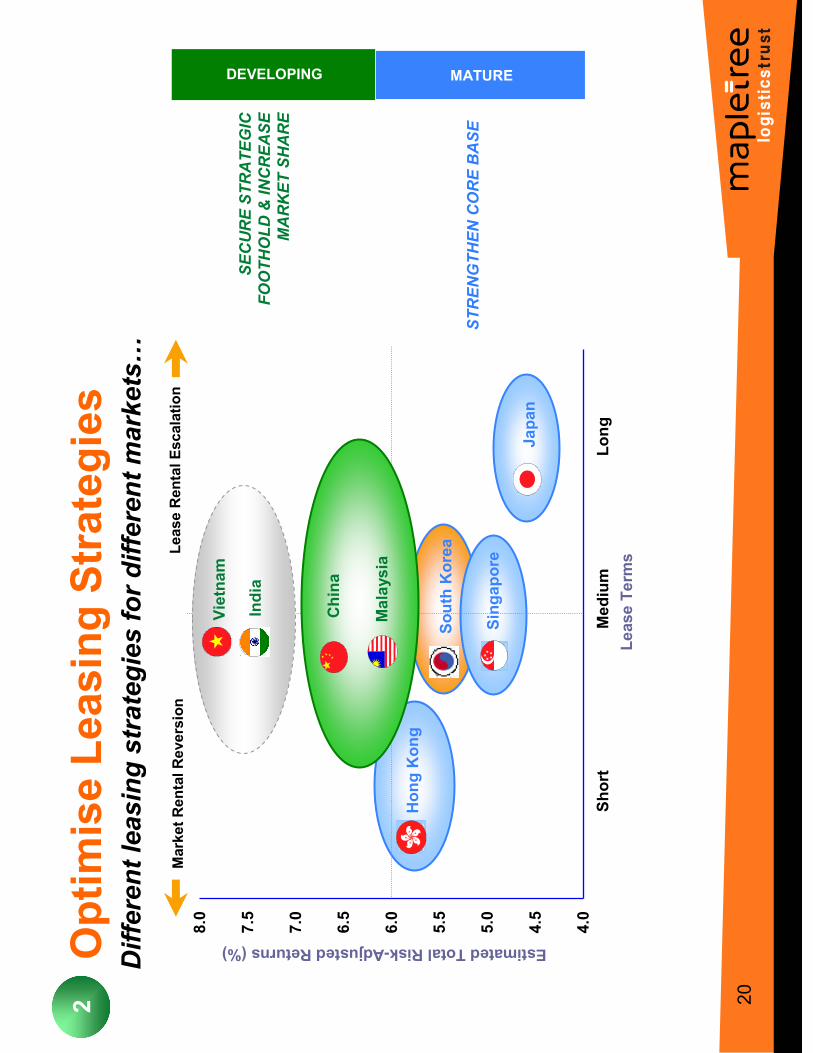

Singapore

Japan

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

Short

Medium

Long

Lease Term

s

Estimated Total Risk-Adjusted Returns (%)

STRENGTHEN CORE BASE

Hong Kong

SECURE STRATEGIC

FOOTHOLD & INCREASE

MARKET SHARE

DEVELOPING MATURE

Market Rental Reversion

Lease Rental Escalation

Vietnam

China

Malaysia

India

Different leasing strategies for different markets…

2Optimise Leasing Strategies

South Korea

21

21

Asset enhancement

3

�Portfolio occupancy as at 30 June 2007: 99.9%

�TIC Tech Centre extension

-Additional 3-storeys, 5,700 sqm

-TOP obtained on 20 July 2007

-Yielding additionalrental income ofS$92,000 per month (17%) from Oct 07

�Summary of renewals for 1H 2007

-80,000 sqm ~ 5% of portfolio

space renewed at positive reversion rates averaging 12%. The

average rental reversion in each country was :

-7%

-Malaysia

-39%

-China

-15%

-Hong Kong

-8%

-S'pore

�Space due for renewal in 2008

-171,000 sqm ~ 9% of portfolio space, due for renewal in 2008, with expected reversion rate of ~

13%.

22

22

Spon

sor’s

com

mitm

ent i

n D

evel

opm

ent P

roje

cts

by

Spon

sor’s

com

mitm

ent i

n D

evel

opm

ent P

roje

cts

by

Spon

sor’s

com

mitm

ent i

n D

evel

opm

ent P

roje

cts

by

Spon

sor’s

com

mitm

ent i

n D

evel

opm

ent P

roje

cts

by

Cou

ntrie

sC

ount

ries

Cou

ntrie

sC

ount

ries

SGD 30

41,100

Mapletree Beijing Airport Logistics Park

China

4

SGD 31

63,400

Tianjin Airport

China

5

SGD 37

46,000

Yangshan Bonded Logistics Park

China

1

SGD 846

1,656,150

Total

SGD 415

745,600

Vietnam

Subtotal

SGD 250

366,000

Proposed Mapletree Logistics Park -Bac Ninh

Vietnam,

Bach Ninh Province

10

SGD 155

356,000

Mapletree Logistics Park (MLP)

Vietnam,

Binh Duong Province

9

SGD 10

23,600

Mapletree Logistics Centre (MLC)

Vietnam,

Binh Duong Province

8

SGD 20

60,000

Malaysia

Subtotal

SGD 20

60,000

Mapletree Taian W

arehouse Development

Malaysia

7

SGD 411

850,550

China

Subtotal

SGD 211

484,000

Tianjin Dongjiang Port

China

6

SGD 81

170,750

Wujiang Logistics Centre

China

3

SGD 21

45,300

Wuxi Logistics Park

China

2

Total Commitment

(SG Dollars)

Total GFA (m

2)

Project Name

Country

S/No.

All figures in Millions

23

23

Spon

sor’s

Dev

elop

men

t Pro

ject

s in

Chi

na

Shanghai

Mapletree Yangshan Bonded

Logistics Park

1

Jiangsu Province

Mapletree W

uxi Logistics Park

1

Beijing

Beijing Airport Logistics Park

2

Tianjin

Tianjin Airport Logistics Park

1

Tianjin Donjiang Port1

Mapletree W

ujiang Logistics

Centre2

1= Existing Site

2= Proposed Site

24

24

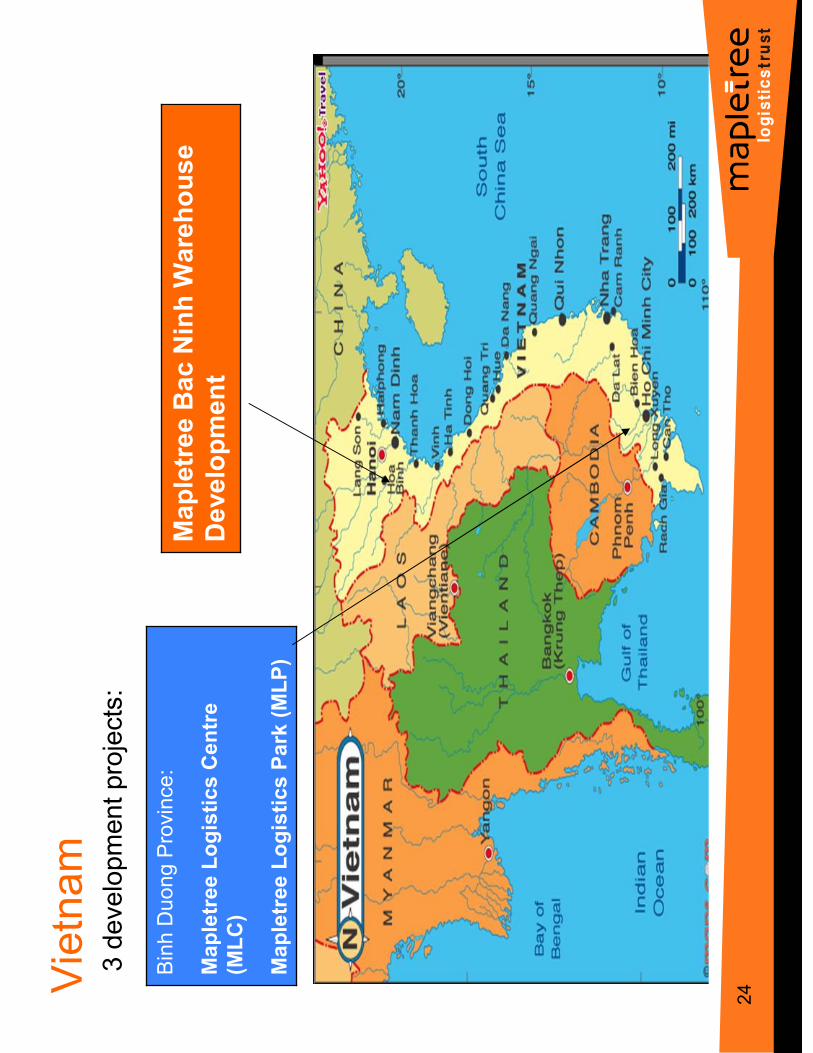

Mapletree Bac Ninh Warehouse

Development

Binh Duong Province:

Mapletree Logistics Centre

(MLC)

Mapletree Logistics Park (MLP)

Viet

nam

3 development projects:

25

25

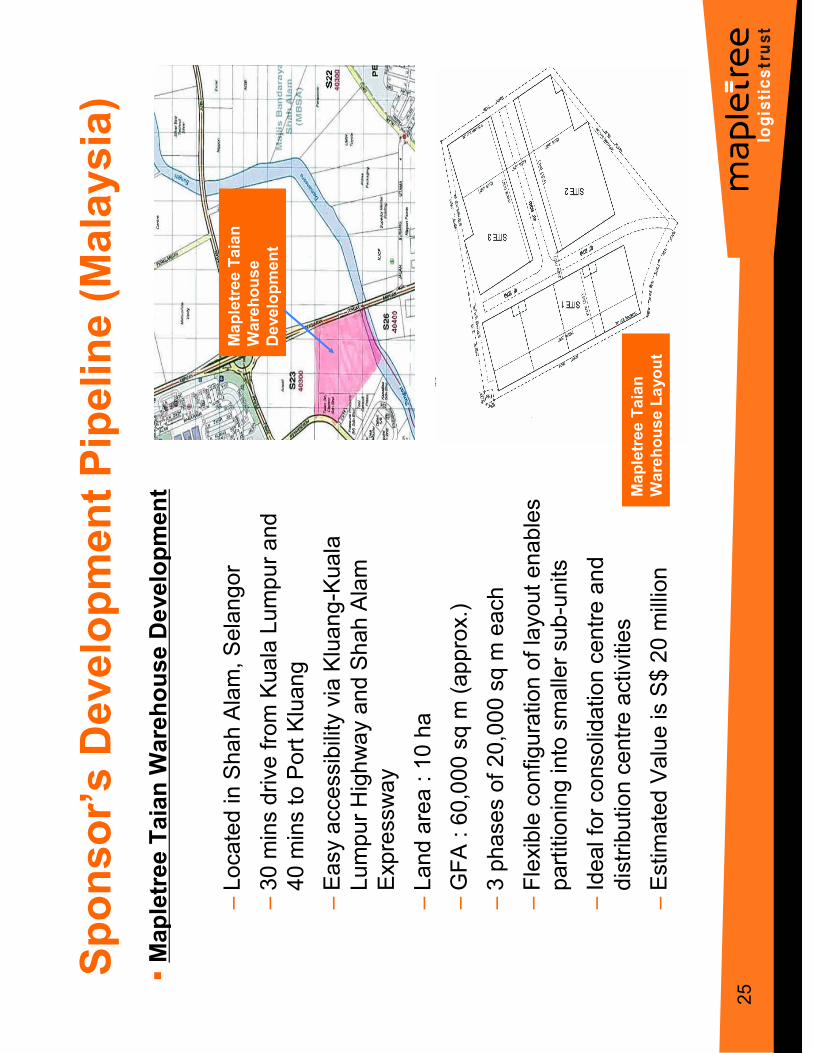

�Mapletree Taian W

arehouse Development

–Located in Shah Alam, Selangor

–30 mins drive from Kuala Lumpur and

40 mins to Port Kluang

–Easy accessibility via Kluang-Kuala

Lumpur Highway and Shah Alam

Expressway

–Land area : 10 ha

–GFA : 60,000 sq m (approx.)

–3 phases of 20,000 sq m each

–Flexible configuration of layout enables

partitioning into smaller sub-units

–Ideal for consolidation centre and

distribution centre activities

–Estimated Value is S$ 20 million

Sponsor’s Development Pipeline (Malaysia)

Mapletree Taian

Warehouse

Development

Mapletree Taian

Warehouse Layout

26

26

�MapletreeLog -Overview

�Snapshot

�Our portfolio

�Scaling up

�Capital Management

�Total Returns

�Outlook

Agen

daAg

enda

Agen

daAg

enda

27

27♦

Strong balance sheet with optimum leverage levels

♦Secure diversified funding sources

♦Competitive cost of debt financing

♦Interest rate management

–~55% of total current borrowings as at 30 June 2007 has been hedged

♦Foreign currency management

–Borrowing in foreign currencies, maintain currency hedges over residual earnings

after interest generated by overseas assetswhere possible and cost perm

itting

Optimise capital management initiatives to deliver…

…competitive risk-adjusted returns and sustainable growth for

Unitholders

Capital Management Strategy

28

28

4%

7%

14%

10%

3%

22%

2%

30%

4%2%

2%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

55%

Maturing

in 2007

Maturing

in 2008

Maturing

in 2009

Maturing

in 2010

Maturing

in 2011

Maturing

in 2012

SGD

HKD

JPY

MYR

CNY

8%

10%

25%

42%

4%

7%

4%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Maturing

in 2007

Maturing

in 2008

Maturing

in 2009

Maturing

in 2010

Maturing

in 2011

Maturing

in 2012

SGD

HKD

JPY

MYR

CNY

(1)

Actual Debt as at 31 Mar 2007; excludes deferred consideration of S$ 8.0 million

(2)

Actual Debt as at 31 Jun 2007; excludes deferred consideration of S$ 7.6 million

(3)

This figure reflects the Average Duration of the Actual Debt as at 31 Mar 2007, recalibrated and profiled as at 30 Jun 2007. Before the recalibration, the Average Duration

of the Actual D

ebt as at 31 Mar 2007 was at 3.25 years.

Debt Amount

Debt Maturity Profile

Actual Debt as at 30 Jun 2007(2)

Average Duration (3)

= 3.00 years

S$630 million

Actual Debt as at 31 Mar 2007(1)

42%

4%

36%

10%

8%

S$1,182 million

14%

2%

16%

52%

Average Duration

= 3.13 years

16%

29

29

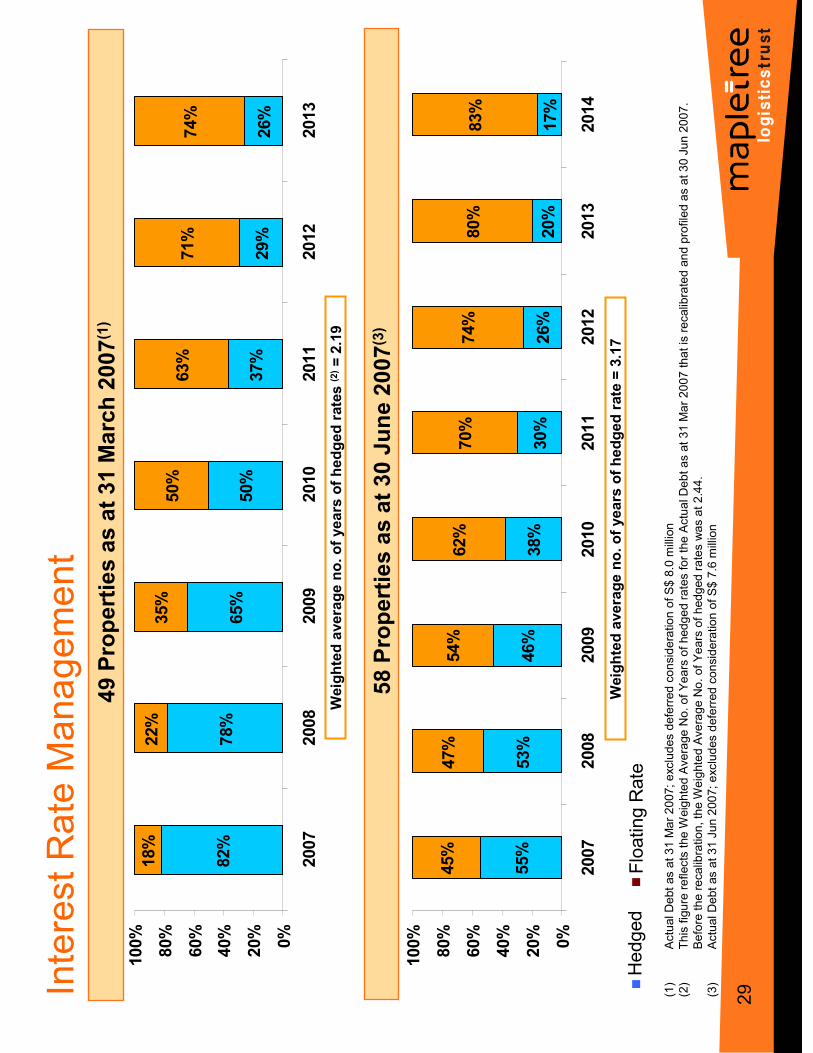

Hedged

Floating Rate

Interest Rate Management

49 Properties as at 31 March 2007(1)

Weighted average no. of years of hedged rates (2

)= 2.19

58 Properties as at 30 June 2007(3)

(1)

Actual Debt as at 31 Mar 2007; excludes deferred consideration of S$ 8.0 million

(2)

This figure reflects the W

eighted Average No. of Years of hedgedrates for the Actual D

ebt as at 31 Mar 2007 that is recalibrated and profiled as at 30 Jun 2007.

Before the recalibration, the W

eighted Average No. of Years of hedged rates was at 2.44.

(3)

Actual Debt as at 31 Jun 2007; excludes deferred consideration of S$ 7.6 million

Weighted average no. of years of hedged rate = 3.17

82%

78%

65%

50%

37%

29%

26%

18%

22%

35%

50%

63%

71%

74%

0%

20%

40%

60%

80%

100%

2007

2008

2009

2010

2011

2012

2013

55%

53%

46%

38%

30%

26%

20%

17%

45%

47%

54%

62%

70%

74%

80%

83%

0%

20%

40%

60%

80%

100%

2007

2008

2009

2010

2011

2012

2013

2014

30

30

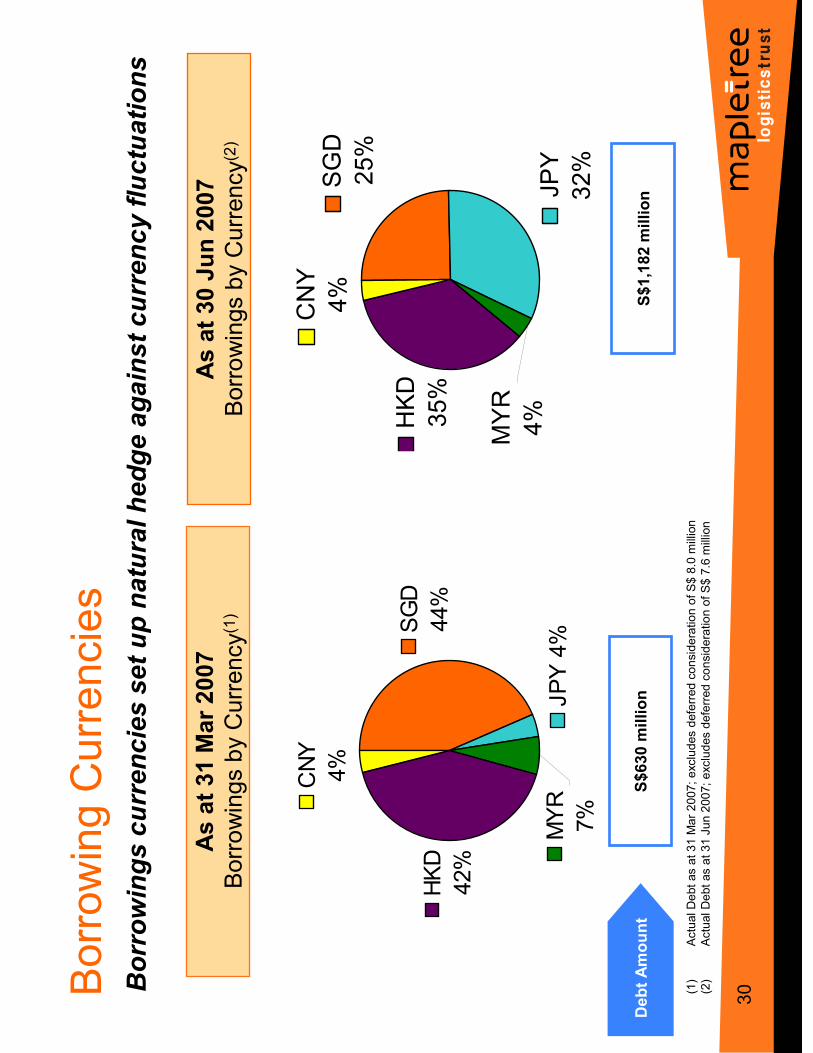

SGD

25%

JPY

32%

HKD

35%

CNY

4%

MYR

4%

SGD

44%

JPY 4%

HKD

42%

CNY

4%

MYR

7%

Borrowings currencies set up natural hedge against currency fluctuations

As at 31 Mar 2007

Borrowings by Currency(1)

S$1,182 million

As at 30 Jun 2007

Borrowings by Currency(2)

S$630 million

Borrowing Currencies

Debt Amount

(1)

Actual Debt as at 31 Mar 2007; excludes deferred consideration of S$ 8.0 million

(2)

Actual Debt as at 31 Jun 2007; excludes deferred consideration of S$ 7.6 million

31

31

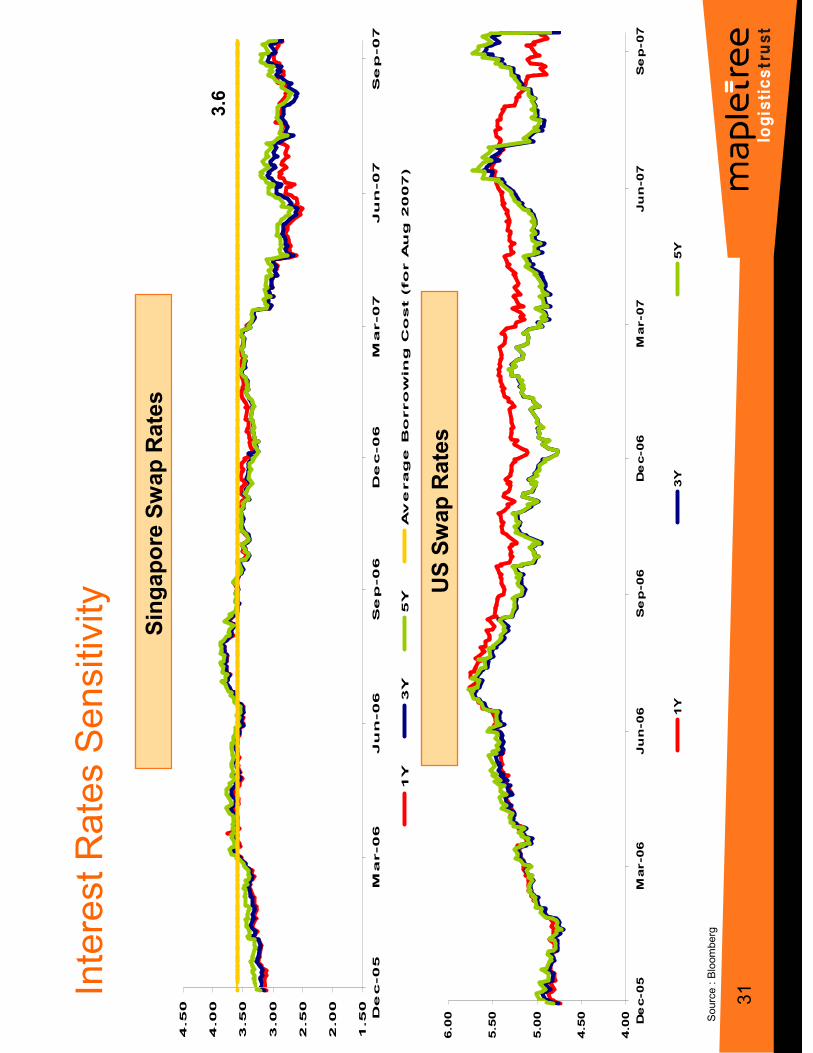

Singapore Swap Rates

Interest Rates Sensitivity

Source : Bloomberg

3.65

1.50

2.00

2.50

3.00

3.50

4.00

4.50

Dec-05

Mar-06

Jun-06

Sep-06

Dec-06

Mar-07

Jun-07

Sep-07

1Y

3Y

5Y

Average Borrowing Cost (for Aug 2007)

3.6

4.00

4.50

5.00

5.50

6.00

Dec-05

Mar-06

Jun-06

Sep-06

Dec-06

Mar-07

Jun-07

Sep-07

1Y

3Y

5Y

US Swap Rates

32

32

-2.00

-1.00

0.00

1.00

2.00

3.00

4.00

5.00 Aug-05

Nov-05

Feb-06

May-06

Aug-06

Nov-06

Feb-07

May-07

Aug-07

1Y3Y

5YAverage Borrowing Cost (for A

ug 2007)

3.60

3.80

4.00

4.20

4.40

4.60

4.80

5.00

5.20

5.40 Aug-05

Jan-06

Jun-06

Nov-06

Apr-07

30-Aug-07

1Y3Y

5YAverage Borrowing Cost (for Aug 2007)

2.40

2.80

3.20

3.60

4.00

4.40

4.80

5.20

5.60 Aug-05

Nov-05

Feb-06

May-06

Aug-06

Nov-06

Feb-07

May-07

Aug-07

1Y

3Y

5YAverage Borrowing Cost (for Aug 2007)

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00 Feb-06

May-06

Aug-06

Nov-06

Feb-07

May-07

Aug-07

1Y

3Y

5Y

Average Borrowing Cost (for Aug 2007)

Hong Kong Swap Rates

China Swap Rates

Malaysia Swap Rates

Japan Swap Rates

Interest Rates Sensitivity

Source : Bloomberg

5.0

2.8

4.2

1.5

33

33

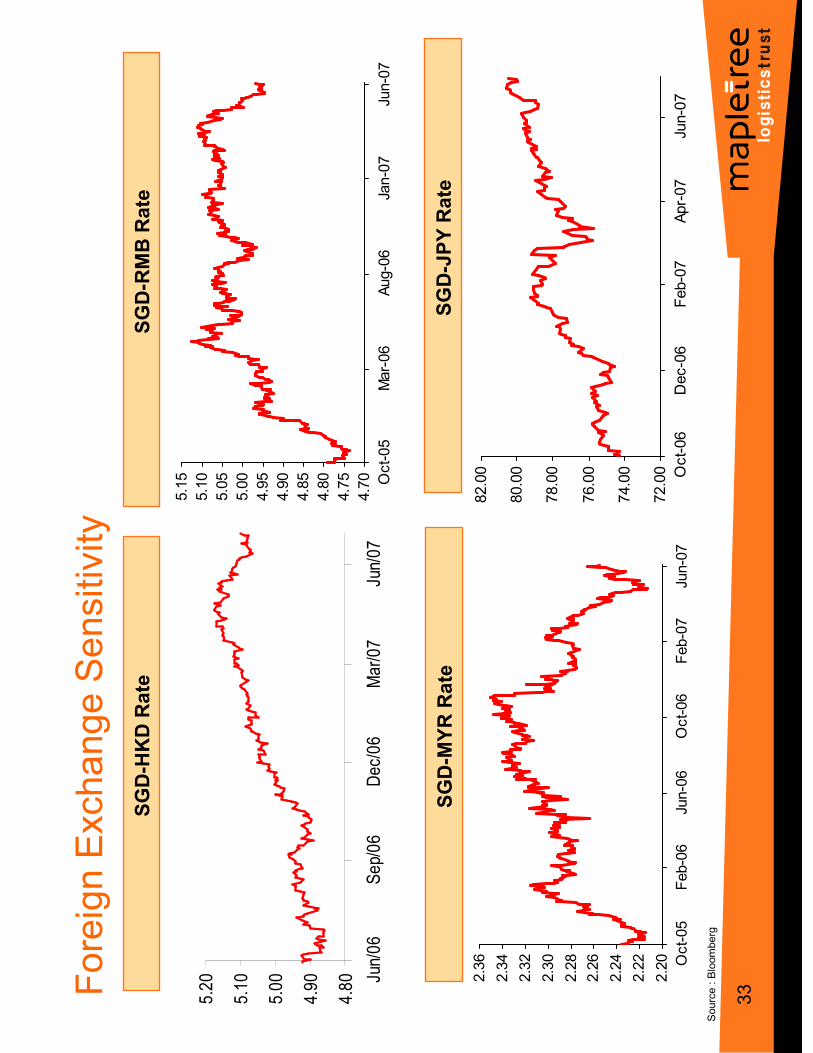

SGD-HKD Rate

SGD-RMB Rate

SGD-MYR Rate

72.00

74.00

76.00

78.00

80.00

82.00 Oct-06

Dec-06

Feb-07

Apr-07

Jun-07

Foreign Exchange Sensitivity

SGD-JPY Rate

4.70

4.75

4.80

4.85

4.90

4.95

5.00

5.05

5.10

5.15 Oct-05

Mar-06

Aug-06

Jan-07

Jun-07

2.20

2.22

2.24

2.26

2.28

2.30

2.32

2.34

2.36 Oct-05

Feb-06

Jun-06

Oct-06

Feb-07

Jun-07

Source : Bloomberg

4.80

4.90

5.00

5.10

5.20 Ju

n/06

Sep/06

Dec/06

Mar/07

Jun/07

34

34

�MapletreeLog -Overview

�Snapshot

�Our portfolio

�Scaling Up

�Capital Management

�Total Returns

�Outlook

Agen

daAg

enda

Agen

daAg

enda

35

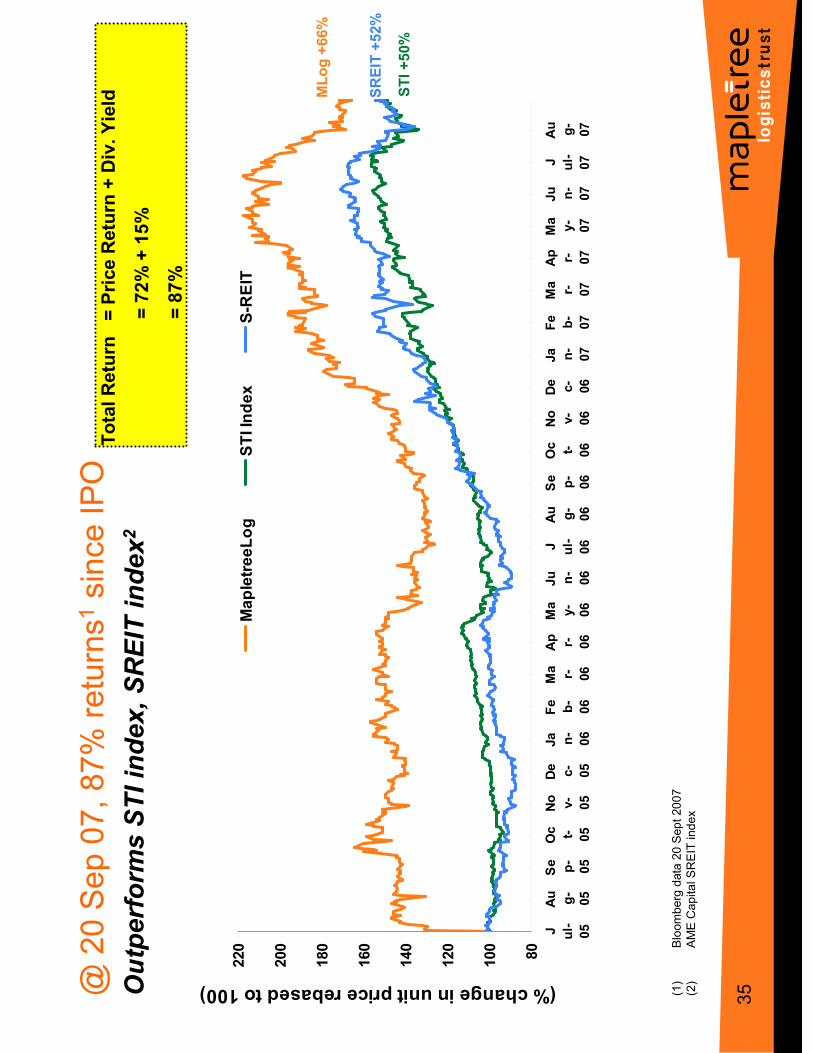

35Outperform

s STI index, SREIT index2

(1)

Bloomberg data 20 Sept 2007

(2)

AME Capital SREIT index

@ 20 Sep 07, 87% returns1since IPO

Total Return = Price Return + Div. Yield

= 72% + 15%

= 87%

80

100

120

140

160

180

200

220

J ul-

05

Au g-

05

Se p-

05

Oc t- 05

No v-

05

De c-

05

Ja n-

06

Fe b-

06

Ma r- 06

Ap r- 06

Ma

y-

06

Ju n-

06

J ul-

06

Au g-

06

Se p-

06

Oc t- 06

No v-

06

De c-

06

Ja n-

07

Fe b-

07

Ma r- 07

Ap r- 07

Ma

y-

07

Ju n-

07

J ul-

07

Au g-

07

(% change in unit price rebased to 100)

MapletreeLog

STI Index

S-REIT

MLog +66%

SREIT +52%

STI +50%

36

36

�MapletreeLog -Overview

�Snapshot

�Our portfolio

�Scaling Up

�Capital Management

�Total Returns

�Outlook

Agen

daAg

enda

Agen

daAg

enda

3737

37

�Successful track record since IPO

�Sound strategy for future growth and scaling up

�Asset size of 61 properties valued ~ S$2.1 billion as at 21 Sept

07 (announced –74 properties –approx. S$2.4 billion)

Why

Map

letre

eLog

?W

hy M

aple

treeL

og?

Why

Map

letre

eLog

?W

hy M

aple

treeL

og?

Experienced

management

team

Focused on Asia

logistics

�Asia logistics industry –high growth

�Pan-Asian platform

–“follow the client strategy

�Geographically diversified

�Anchored in strong mature (Singapore, Hong Kong, Japan)

�Expanding presence in new, developing markets (China, Malaysia, Vietnam)

�Sponsor’s development pipeline

�Organic growth and asset enhancement

Yield plus growth

strategy

�Diversified cashflows from different markets

�Stable core combined with exposure to high growth markets

�Optimal capital structure

Robust Income

stream

3838

38

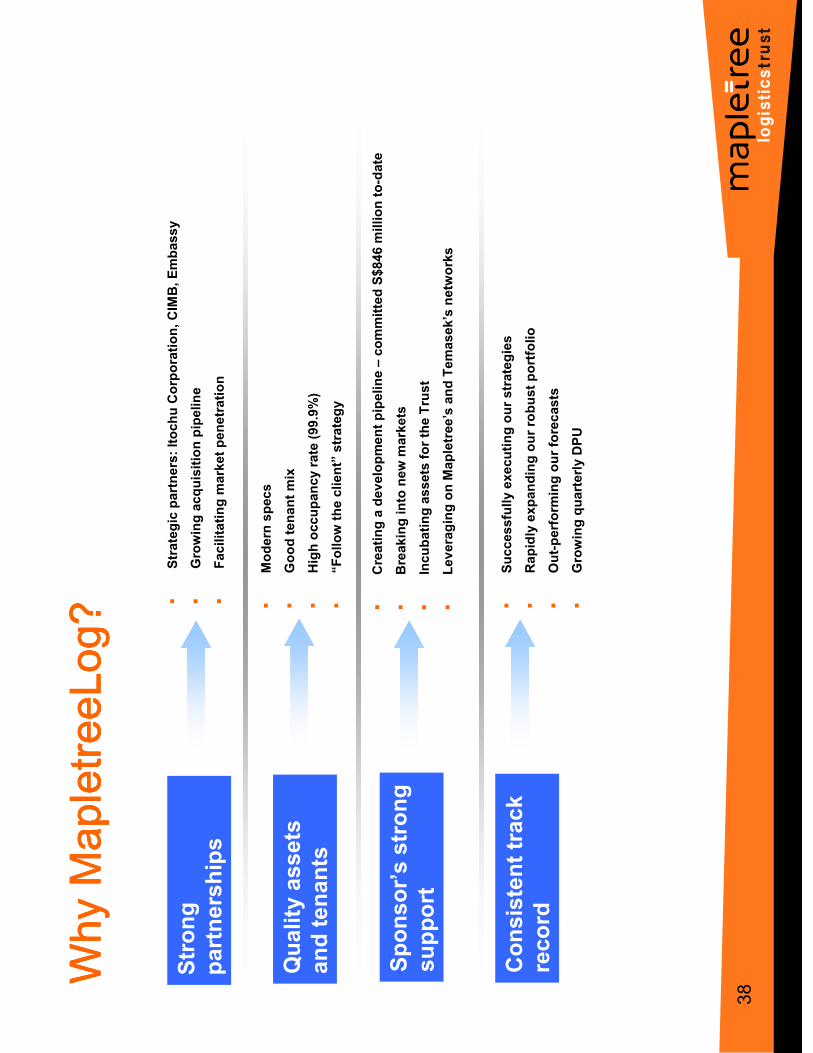

�Strategic partners: Itochu Corporation, CIMB, Embassy

�Growing acquisition pipeline

�Facilitating market penetration

Why

Map

letre

eLog

?W

hy M

aple

treeL

og?

Why

Map

letre

eLog

?W

hy M

aple

treeL

og?

Strong

partnerships

Quality assets

and tenants

Consistent track

record

�Modern specs

�Good tenant mix

�High occupancy rate (99.9%)

�“Follow the client”strategy

�Creating a development pipeline –committed S$846 million to-date

�Breaking into new markets

�Incubating assets for the Trust

�Leveraging on Mapletree’s and Temasek’s networks

�Successfully executing our strategies

�Rapidly expanding our robust portfolio

�Out-perform

ing our forecasts

�Growing quarterly DPU

Sponsor’s strong

support

39

39Analyst Recommendations

Firm name

Analyst

Recomm.

Price Target

(S$)

Date

DPU 07F

(cents)

DPU 08F

(cents)

Christopher Gee

Overweight

1.34

23 Aug 07

6.47

6.76

Alastair Gillespie

Buy 2

1.63

20 Sep 07

6.5

6.8

David Lum

Buy 2

1.65

20 Aug 07

6.68

7.66

Gregory Lui

Buy

1.41

26 Jul 07

6.4

6.7

Leslie Yee

Neutral

1.43

20 Sep 07

6.55

7.1

Elaine Cheong

Outperform

1.45

26 Jul 07

6.2

7.2

Ho Zy Sew

Buy

1.59

19 Sep 07

6.5

6.7

Wong Yew Kiang

Outperform

1.72

26 Jul 07

6.56

8.58

Average

6.48

7.19

40

40

Important Notice

The inform

ation contained in this presentation is for inform

ation purposes only and does not constitute an offer to sell or any solicitation of an offer or invitation to purchase or subscribe for

units in Mapletree Logistics Trust (“MapletreeLog”, and units inMapletreeLog, “Units”) in Singapore or any other jurisdiction, nor should it or any part of it form

the basis of, or be relied upon

in any connection with, any contract or commitm

ent whatsoever.

The past perform

ance of the U

nits and M

apletree Logistics Trust Management Ltd. (the “Manager”) is not indicative of the future perform

ance of MapletreeLog and the Manager.

Predictions, projections or forecasts of the economy or economictrends of the m

arkets are not necessarily indicative of the future or likely perform

ance of MapletreeLog.

The value of the Units and the income derived from them m

ay fallas well as rise. Units are not obligations of, deposits in, or guaranteed by, the M

anager. An investm

ent in Units is subject

to investm

ent risks, including the possible loss of the principal amount invested. Investors have no right to request that the M

anager redeem their U

nits while the U

nits are listed. It is

intended that Unitholders m

ay only deal in their Units through trading on Singapore Exchange Securities Trading Limited (the “SGX-ST”). Listing of the Units on the SGX-ST does not

guarantee a liquid m

arket for the Units.

This presentation m

ay contain forward-looking statements that involve risks and uncertainties. Actual future perform

ance, outcomes and results m

ay differ materially from those expressed

in forward-looking statements as a result of a number of risks, uncertainties and assumptions. Representatives examples of these factors include (without lim

itation) general industry and

economic conditions, interest rate trends, cost of capital and capital availability, competition from similar developments, shifts in expected levels of property rental income, changes in

operating expenses, including employee wages, benefits and training, property expenses and governmental and public policy changes and the continued availability of financing in the

amounts and the term

s necessary to support future business. You are cautioned not to place undue reliance on these forward-looking statements, which are based on the M

anager's

current view of future events. The forecast financial perform

ance of MapletreeLog is not guaranteed and there is no certainty that it can be achieved.

This presentation has been prepared by the M

anager. The inform

ation in this presentation has not been independently verified. Norepresentation, warranty, express or implied, is m

ade as

to, and no reliance should be placed on, the fairness, accuracy,completeness or correctness of the inform

ation and opinions in this presentation. None of the M

anager or any of its agents

or advisers, or any of their respective affiliates, advisers or representatives, shall have any liability (in negligence or otherwise) for any loss howsoever arising from any use of this

presentation or its contents or otherwise arising in connection with this presentation.

Neither this presentation, nor any copy or portion of it, may besent, taken, transm

itted or distributed, directly or indirectly, in or into the United States, Japan or Canada, or to any U.S.

person (as such term

is defined in Regulation S under the Securities Act of 1933, as amended (the “Securities Act”)). It is not an offer of securities for sale into the United States. The Units

may not be offered or sold into the United States, Canada or Japan or to, or for the account or benefit of, U.S. persons unless they are registered or exempt from registration. The Units

have not been and will not be registered under the Securities Act or the securities laws of any state of the United States. There will be no public offer of securities in the United States.

This presentation m

ay not be forwarded or distributed to any other person and m

ay not be reproduced in any manner whatsoever. Any forwarding, distribution or reproduction of this

inform

ation in whole or in part is unauthorised. Failure to comply with this directive m

ay result in a violation of the Securities Act or the applicable laws of other jurisdictions.

The inform

ation in this presentation m

ust not be published outside the Republic of Singapore and in particular, but without lim

itation, must not be published in any United States edition of

any publication.

This document is not intended to be distributed or passed on, directly or indirectly, to any person in the United Kingdom or anyother jurisdiction in which such action could not be lawfully

made. Persons in the United Kingdom or any other jurisdiction inwhich such action would not be lawfully m

ade should not take any action upon this document. These m

aterials do not

constitute an offer, solicitation or other recommendation to invest in MapletreeLog.

41

41

Than

k Yo

uTh

ank

You

Than

k Yo

uTh

ank

You