pemex presentation non-deal roadshow 100623 ri

TRANSCRIPT

Investor Presentation

June 2010June 2010

Forward-Looking StatementsThis presentation contains forward-looking statements. We may also make written or oral forward-lookingThis presentation contains forward looking statements. We may also make written or oral forward lookingstatements in our periodic reports to the Comisión Nacional Bancaria y de Valores (Mexican National Bankingand Securities Commission, or CNBV), and the U.S. Securities and Exchange Commission (SEC), in our annualreport, in our offering circulars and prospectuses, in press releases, in other written materials, and in oralstatements made by our officers, directors or employees to third parties.

We may include forward-looking statements that address, among other things, our:• drilling and other exploration activities;• import and export activities;• projected and targeted capital expenditures and other costs and;• commitments revenues and liquidity etccommitments, revenues and liquidity, etc.

Actual results could differ materially from those projected in such forward-looking statements as a result ofvarious factors that may be beyond our control. These factors include, but are not limited to:

• changes in international crude oil and natural gas prices;• effects on us from competition;• effects on us from competition;• limitations on our access to sources of financing on competitive terms;• significant economic or political developments in Mexico;• developments affecting the energy sector; and• changes in our regulatory environment.

Accordingly, you should not place undue reliance on these forward-looking statements. In any event, thesestatements speak only as of their dates, and we undertake no obligation to update or revise any of them,whether as a result of new information, future events or otherwise. These risks and uncertainties are morefully detailed in PEMEX’s most recent Form 20-F filing with the SEC (www.sec.gov), and the prospectus filedwith the CNBV available through the Mexican Stock Exchange (www bmv com mx) These factors could cause

2

with the CNBV, available through the Mexican Stock Exchange (www.bmv.com.mx). These factors could causeactual results to differ materially from those contained in any forward-looking statement.

Cautionary NoteProved reserves estimates as of December 31, 2009 are consistent with the conclusions of theindependent engineering firms that audit Mexico’s reserves However pursuant to the Regulatoryindependent engineering firms that audit Mexico’s reserves. However, pursuant to the RegulatoryLaw to Article 27 of the Constitution of the United Mexican States Concerning Petroleum Affairs, theNational Hydrocarbons Commission is currently reviewing the hydrocarbon reserves evaluationreports. The Energy Ministry will disclose the hydrocarbon reserves of the country once this review iscomplete. It is possible that differences may arise, particularly with respect to the probable andp p y , p y p ppossible reserves associated with Chicontepec.

As of January 1, 2010, the SEC changed its rules to permit oil and gas companies, in their filings withthe SEC, to disclose not only proved reserves, but also probable reserves and possible reserves. Inaddition, we do not necessarily mean that the probable or possible reserves described herein meety p pthe recoverability thresholds established by the SEC in its new definitions. Investors are urged toconsider closely the disclosure in our Form 20-F “File No. 0-99” and our annual report to CNBV,available at www.pemex.com.

EBITDA is a non-GAAP measure.

Convenience translations into U.S. dollars of amounts in Mexican pesos from 2002 to 2007 have been made at the following exchange rates for the corresponding years in pesos per US$: 2003, 11.23; 2004, 11.26; 2005, 10.77; 2006, 10.88; and 2007, 10.86. In addition, convenience translation into U.S. dollars of amounts in pesos for the income statement have been made at the following average exchange rates in Pesos per U.S.$: 2008, 11.18; 2009, 13.52; and 1Q10, 12.79, unless otherwise noted. Finally, convenience translation into U.S. dollars of amounts in pesos from the balance sheet have been made at the established exchange rate at March 31, 2010 in Pesos per U.S.$ of 12.33. Such translations should not be construed as a representation that the peso amounts have been of could be converted into U S dollars at the foregoing or any other rate

3

could be converted into U.S. dollars at the foregoing or any other rate.

Cumulative or annual variations are computed as compared to the same period of the previous year, unless otherwise specified.

Content

Energy Reform

Upstream

Downstream

PEMEX Sustainability

Investment Program and Debt Strategy

4

Energy Reform

PEMEX Value Creation

Corporate Governance Special Contracting Regime Financial Flexibility

• Board with the participation of professional

• Flexible procurement and contracting.

• Independent financial program (without affecting our free

members.

• Incorporation of best corporate practices.

• Contracts with performance incentives.

cash flows).

• Financing from external sources.corporate practices.

• Schemes to develop and support suppliers and contractors in

d t i

external sources.

• Citizen bonds.

Diff ti t d fi l

5

order to increase participation of Mexican providers.

• Differentiated fiscal regime.

Content

Energy Reform

Upstream

Downstream

PEMEX Sustainabilityy

Investment Program and Debt Strategy

6

Total Reserves by Area

Proved Reserves and Prospective Resources

Oil and Gas

Basin Production

as of December 31, 2009MMMboe

Basin 3P 2P 1P

Burgos and Sabinas 0.9 0.6 0.4

Gas

B

Deep-waters 0.6 0.2 0.1

Southeastern 23.4 17.5 12.6Tampico–Misantla (ATG) 18.5 9.7 0.8Veracruz 0.2 0.2 0.2

Tampico-Misantla

Sabinas

19

Tampico-Misantla

BurgosSabinas

Gulf of Mexico

Deep sea exploration

P ti R

Total(1) 43.1 28.2 14.0Equivalent to(years of production)(1) 31.3 20.5 10.2

dd

tla19.20.3

ddVeracruz

Prospective Resources

Basin MMMboe

Burgos 3.1Deep waters in the Gulf of Mexico 29.5

Southeastern

Sabinas 0.3Sureste (Southeastern) 16.7Tampico-Misantla (ATG) 1.7Veracruz 0.7Y tá Pl tf 0 3

7

(“Sureste”)Yucatán Platform 0.3

Total(1) 52.3

(1) Numbers may not total due to rounding.

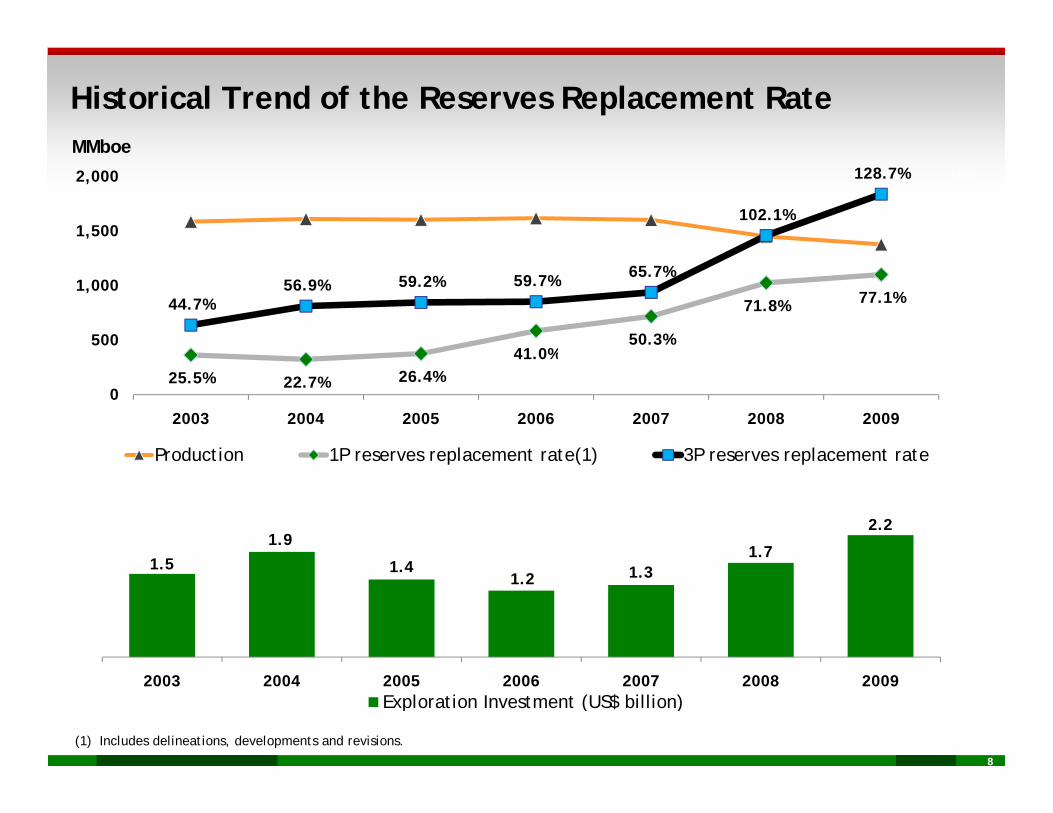

Historical Trend of the Reserves Replacement RateMMboe

102.1%

128.7%

100%

120%

140%

1,500

2,000

MMboe

41 0%50.3%

71.8% 77.1%44.7%56.9% 59.2% 59.7% 65.7%

40%

60%

80%

500

1,000

25.5% 22.7% 26.4%41.0%

0%

20%

02003 2004 2005 2006 2007 2008 2009

Production 1P reserves replacement rate(1) 3P reserves replacement rateProduction 1P reserves replacement rate(1) 3P reserves replacement rate

1 51.9

1.7

2.22

2.5

1.5 1.41.2 1.3

0

0.5

1

1.5

8

2003 2004 2005 2006 2007 2008 2009Exploration Investment (US$ billion)

(1) Includes delineations, developments and revisions.

Upstream Exploration Strategy: Deepwater

Area RiskWater depth

(m)

Prospective resources

(MMboe)1

Perdido

( ) (MMboe)

1. Perdido folded belt Low-Moderate >2000 100-600

2. Oreos Moderate-High 800-2000 40-130

3 Nancan High 500 2500 35 290

2

3Gulf of

Southern Gulf of Mexico

3. Nancan High 500-2500 35-290

4. Jaca-Patini Moderate-High 1000-1500 90-260

5. Lipax Moderate 950-2000 50-200

Low-moderate (Western) 1500-2000 100-480

8

976

5

4Gulf of

Mexico “B”

6. Holok(Western) Moderate-High(Eastern)

600-1100 65-300

7. Temoa High 850-1950 20-270

8 H Hi h

Heavy oil Gas / Light oilLight oil

8. Han High 450-2250 80-350

9. Nox-Hux Moderate 650-1850 90-250

• Nine areas were defined as the most important in Mexican deep waters, considering

9

economic value, prospective size, hydrocarbon type, geological risk, closeness toproduction facilities and environmental restrictions as the most relevant criteria.

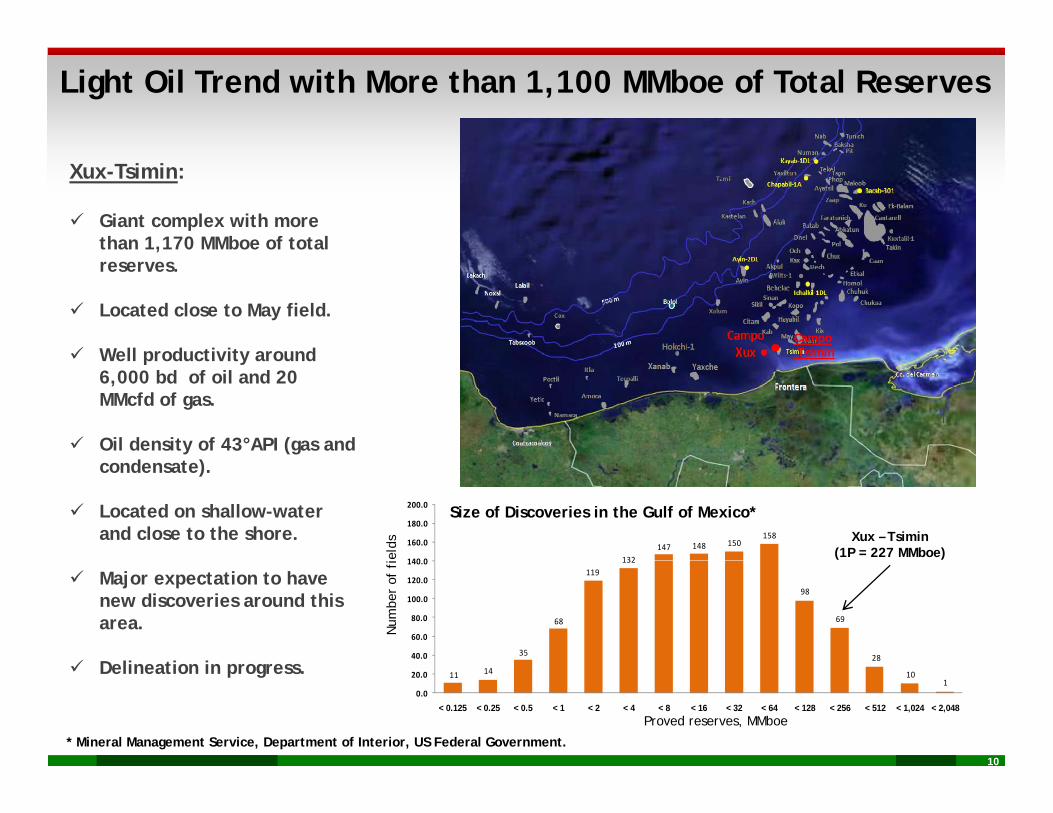

Light Oil Trend with More than 1,100 MMboe of Total Reserves

Xux-Tsimin:

Giant complex with more than 1,170 MMboe of total

CampoTsimin

reserves.

Located close to May field.

Well productivity around Tsimin Well productivity around 6,000 bd of oil and 20 MMcfd of gas.

Oil density of 43°API (gas and

132147 148 150

158

140 0

160.0

180.0

200.0

condensate).

Located on shallow-water and close to the shore. Xux – Tsimin

(1P = 227 MMboe)ield

s

Size of Discoveries in the Gulf of Mexico*

35

68

119132

98

69

2840.0

60.0

80.0

100.0

120.0

140.0

Major expectation to have new discoveries around this area.

D li ti i

Num

ber

of f

i

10

11 14 101

0.0

20.0

< 0.125 < 0.25 < 0.5 < 1 < 2 < 4 < 8 < 16 < 32 < 64 < 128 < 256 < 512 < 1,024 < 2,048

Delineation in progress.

Proved reserves, MMboe

* Mineral Management Service, Department of Interior, US Federal Government.

Heavy Oil Trend with more than 1,200 MMboe of Total Reserves

Producer well

Ayatsil-Tekel:

Giant complex with more than 725 MMboe of total reserves. Pit

Baksha

TunichNab

Numan

Kayab

Kanche

Bok

LemDrilling well

Non-productive well

Delineation well

100

500

Platform

Pipe line

Located close to Maloob field.

Well productivity around 5,000 bd using electric submersible pumps (ESP).

n

Maloob

TsonDL 1

DL 1

Yaxiltun Tekel

PP-M-BPP-M-A

Ayatsil

DL 1

PohpDL 1

Oil density of 12°API.

Development plan in progress.Zaap

DL3

Bacab

PP M A

PP-Zaap-C

E-Ku-A2 PP-Ku-S

PP-Bacab-ALum-A

PB-Ku-H

PP-Zaap-D

PP-Zaap-A

E-Ku-A2

1

2

3

147 148 150158

160.0

180.0

200.0

Pit- Baksha:

Giant complex with more than 510 MMboe of total reserves. Ayatsil-Tekel-Pit-Baksha

(1P = 387 MMboe)

Discoveries sizes in the Gulf of Mexico*

Ku

35

68

119132

98

69

40 0

60.0

80.0

100.0

120.0

140.0 Development based on connection with Ayatsil-Tekel.

Well productivity around 4,500 bd using ESP.

umbe

r of

fie

lds

( )

11

11 14

35 28

101

0.0

20.0

40.0

< 0.125 < 0.25 < 0.5 < 1 < 2 < 4 < 8 < 16 < 32 < 64 < 128 < 256 < 512 < 1,024 < 2,048

Oil density of 12°API.

Development plan in progress.

N

Proved reserves, MMboe* Mineral Management Service, Department of Interior, US Federal Government.

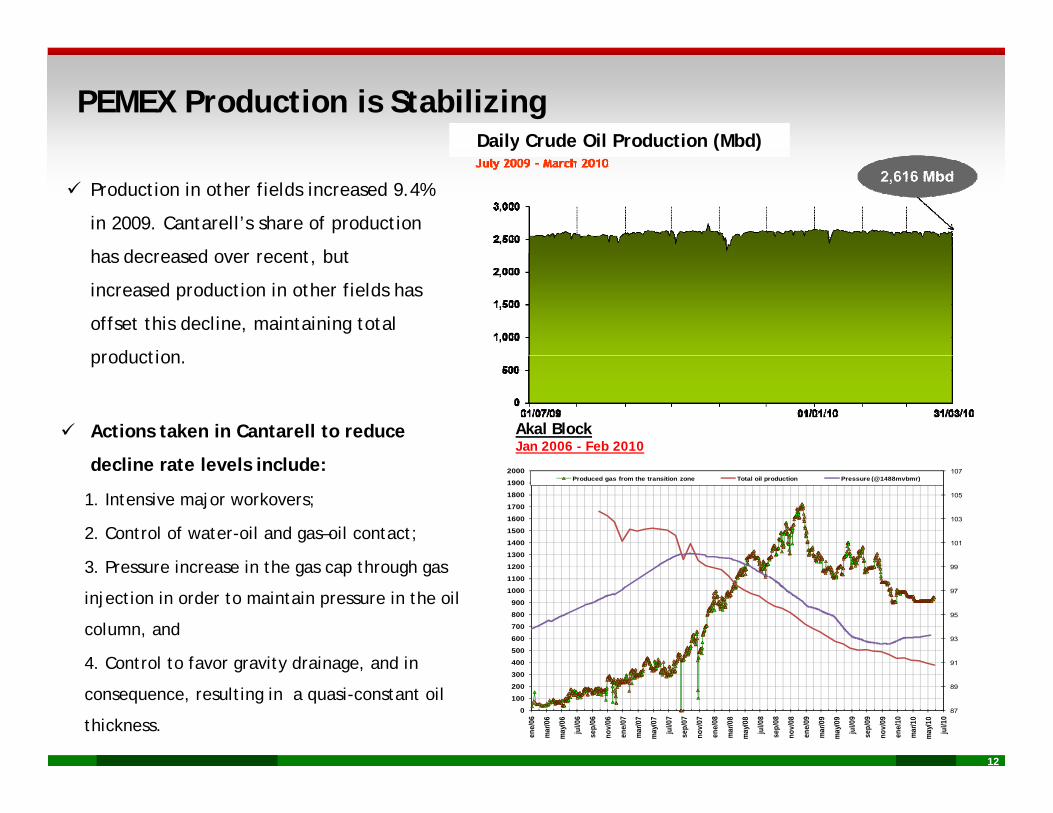

PEMEX Production is StabilizingDaily Crude Oil Production (Mbd)

Production in other fields increased 9.4%

in 2009. Cantarell’s share of production

has decreased o er recent b t

y ( )

has decreased over recent, but

increased production in other fields has

offset this decline, maintaining total

production

Actions taken in Cantarell to reduce

d li l l i l d

production.

Akal BlockJan 2006 - Feb 2010

decline rate levels include:

1. Intensive major workovers;

2. Control of water-oil and gas–oil contact;

3 P i i h h h

101

103

105

107

1300

1400

1500

1600

1700

1800

1900

2000Produced gas from the transition zone Total oil production Pressure (@1488mvbmr)

3. Pressure increase in the gas cap through gas

injection in order to maintain pressure in the oil

column, and

4 Control to favor gravity drainage and in 91

93

95

97

99

400

500

600

700

800

900

1000

1100

1200

12

4. Control to favor gravity drainage, and in

consequence, resulting in a quasi-constant oil

thickness.87

89

91

0

100

200

300

400

ene/

06

mar

/06

may

/06

jul/0

6

sep/

06

nov/

06

ene/

07

mar

/07

may

/07

jul/0

7

sep/

07

nov/

07

ene/

08

mar

/08

may

/08

jul/0

8

sep/

08

nov/

08

ene/

09

mar

/09

may

/09

jul/0

9

sep/

09

nov/

09

ene/

10

mar

/10

may

/10

jul/1

0

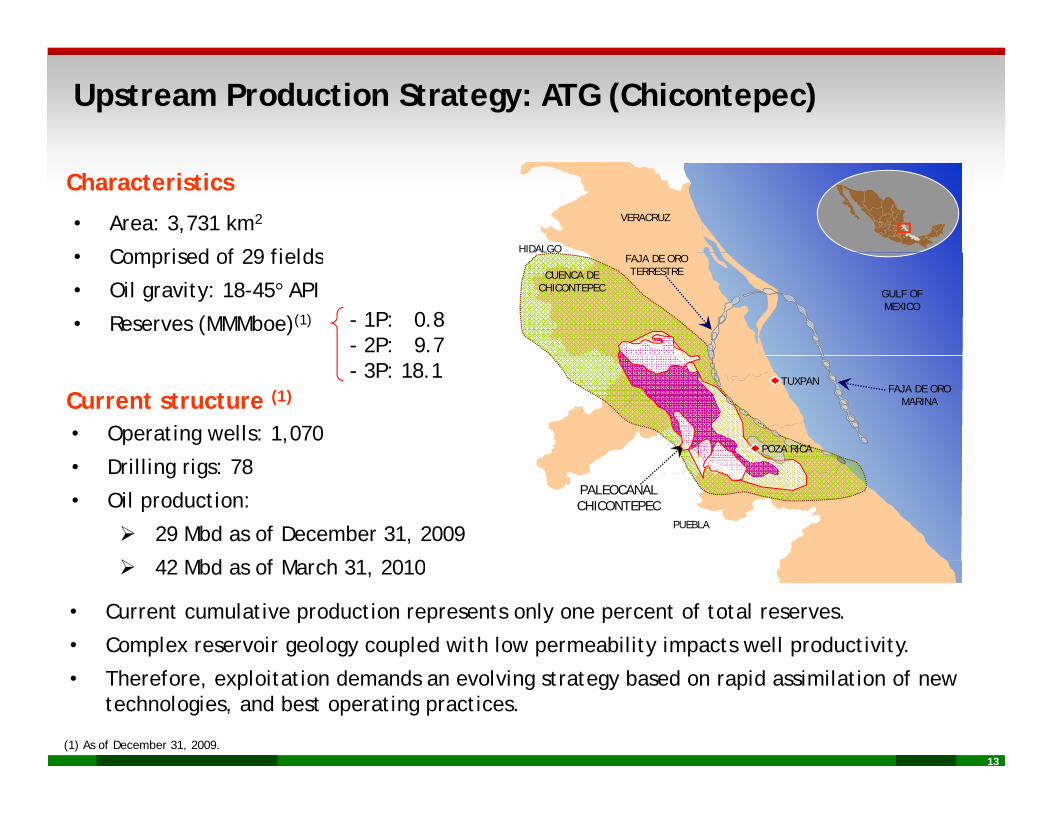

Upstream Production Strategy: ATG (Chicontepec)

VERACRUZ

HIDALGO

• Area: 3,731 km2

Comprised of 29 fields

Characteristics

CUENCA DECHICONTEPEC

FAJA DE OROTERRESTRE

GULF OFMEXICO

• Comprised of 29 fields

• Oil gravity: 18-45° API

• Reserves (MMMboe)(1) - 1P: 0.8- 2P: 9.7

FAJA DE OROMARINA

TUXPAN

POZA RICA• Operating wells: 1,070Current structure (1)

- 3P: 18.1

PALEOCANALCHICONTEPEC

PUEBLA

• Drilling rigs: 78

• Oil production:

29 Mbd as of December 31, 2009

42 Mbd f M h 31 2010 42 Mbd as of March 31, 2010

• Current cumulative production represents only one percent of total reserves.

• Complex reservoir geology coupled with low permeability impacts well productivity.

13(1) As of December 31, 2009.

• Therefore, exploitation demands an evolving strategy based on rapid assimilation of new technologies, and best operating practices.

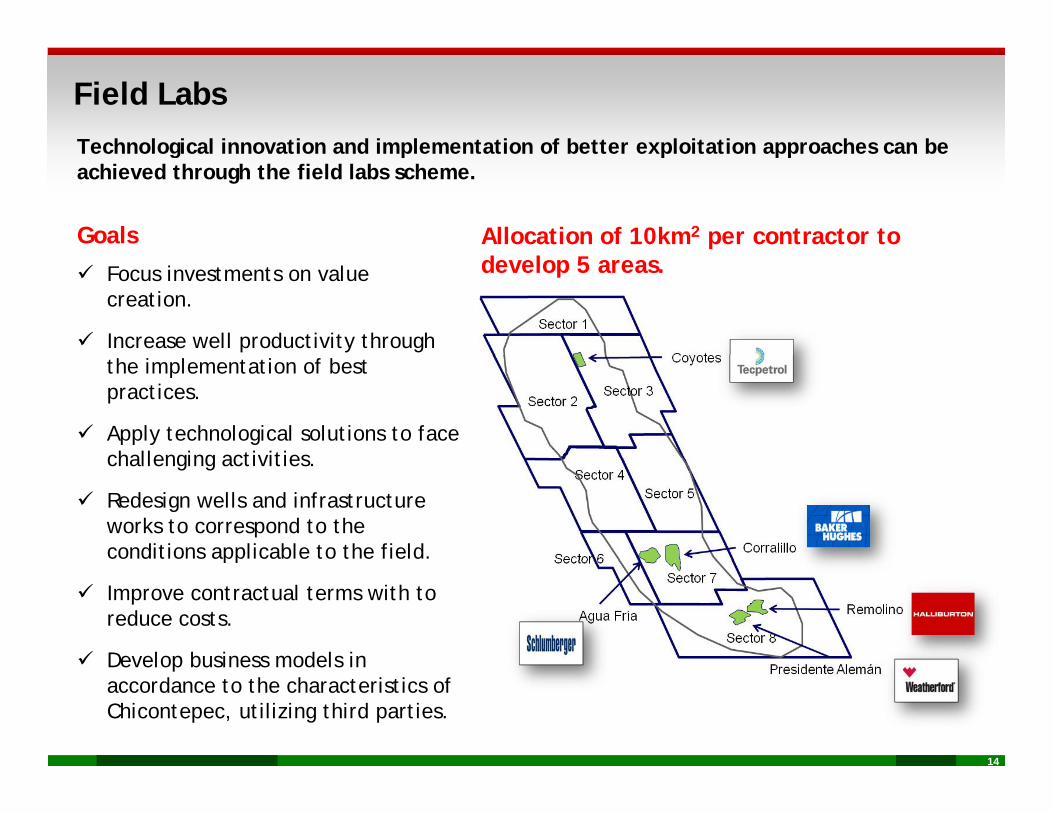

Technological innovation and implementation of better exploitation approaches can be

Field Labs

Goals Allocation of 10km2 per contractor to

Technological innovation and implementation of better exploitation approaches can be achieved through the field labs scheme.

Focus investments on value creation.

Increase well productivity through

develop 5 areas.

the implementation of best practices.

Apply technological solutions to face challenging activities challenging activities.

Redesign wells and infrastructure works to correspond to the conditions applicable to the field. pp

Improve contractual terms with to reduce costs.

Develop business models in

14

Develop business models in accordance to the characteristics of Chicontepec, utilizing third parties.

Mature Fields Represent an Opportunity to Generate Value

202 marginal fields

▪ 202 marginal fields have been identified, with proved reserves representing 29 percent of total reserves. This implies a great

Remaining Reserves and Production to be Recovered (MMboe)

139590

228

519786

opportunity for reclassification.

▪ Furthermore, 57 percent of total 228 451

1P 2P 3P Producción

Reservas Documentada AdicionalReserves Documented Additional

Production

, preserves are documented for production. Our goal is to document an additional 139 MMboe.Benefits

▪ Average production to be recovered in the 2011-2025 period is estimated at 94 Mbd of oil and 162 MMcfd of gas.

▪ The objective is to produce 75 percent of total remaining reserves.j p p g

▪ With support from third parties, we should be able to recover these additional hydrocarbons, through technological improvements and operational efficiency.

▪ Increased execution capacity requires drilling wells in addition to those already

15

c eased e ecut o capac ty equ es d ll g wells add t o to t ose al eady included in our current project portfolio (an average of 500 wells between 2011-2025) in areas such as Cinco Presidentes, Muspac, Poza Rica and Burgos.

Contracting Alternatives: Capability and Execution In the short term, PEMEX must leverage the use of Performance Contracts and alternative contracts

to develop internal capabilities in core businessesto develop internal capabilities in core businesses.

Each project’s execution strategy is defined as a function of its complexity and PEMEX’s internalcapability. The proposed contracting schemes are: Performance Contracts (PC), Field Labs (FL) andTransactional Service Contracts (TSC).

Low Medium High

Internal Capability

InternalCapability:

High PC PCFL

FLTSC

exit

y

Capability:• Human

Resources• Technology• Cost Efficiency

Medium PC FL

FLTSC TSC

Com

ple

Complexity:•Scale

• Cost Efficiency

Low FLTSC TSC TSC

•Scale•Technological

Challenge•Service Market

16

Deep waters Chicontepec Mature Field (Reactivation)

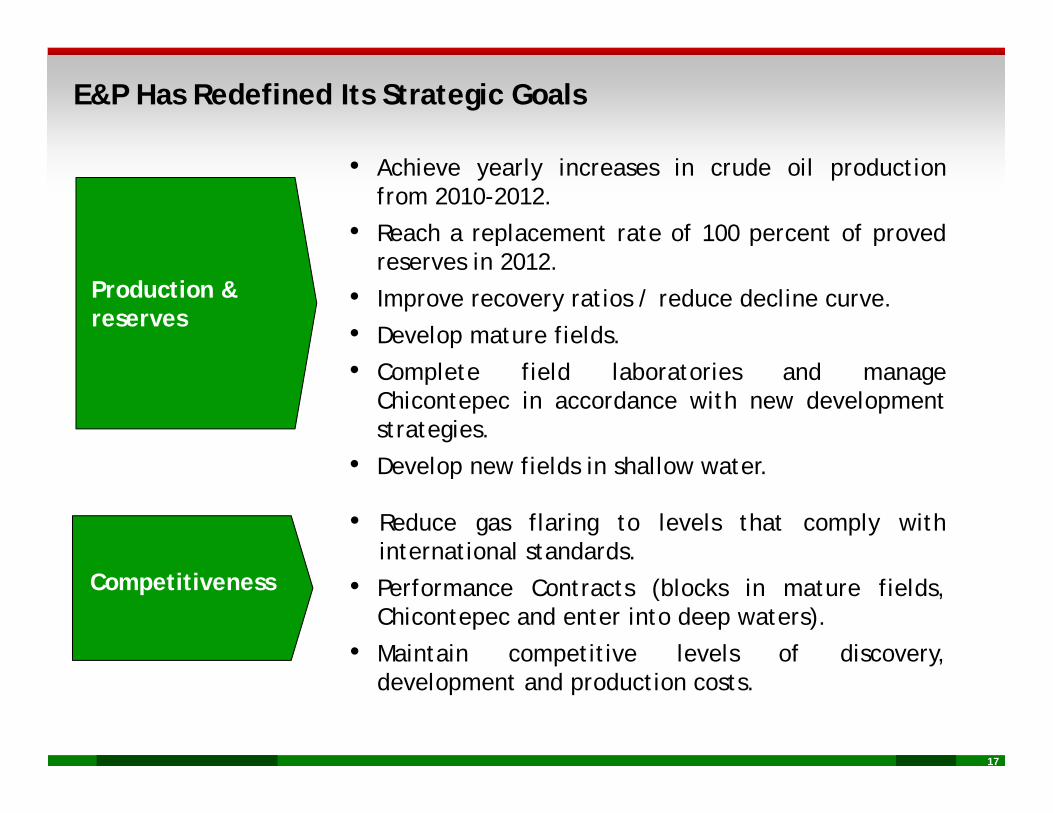

E&P Has Redefined Its Strategic Goals

• Achieve yearly increases in crude oil productionfrom 2010-2012.

• Reach a replacement rate of 100 percent of provedi 2012

Production & reserves

reserves in 2012.

• Improve recovery ratios / reduce decline curve.

• Develop mature fields.

• Complete field laboratories and manageChicontepec in accordance with new developmentstrategies.

D l fi ld i h ll

• Reduce gas flaring to levels that comply withinternational standards.

• Develop new fields in shallow water.

Competitiveness • Performance Contracts (blocks in mature fields,Chicontepec and enter into deep waters).

• Maintain competitive levels of discovery,

17

p y,development and production costs.

Content

Energy Reform

Upstream

Downstream

PEMEX Sustainabilityy

Investment Program and Debt Strategy

18

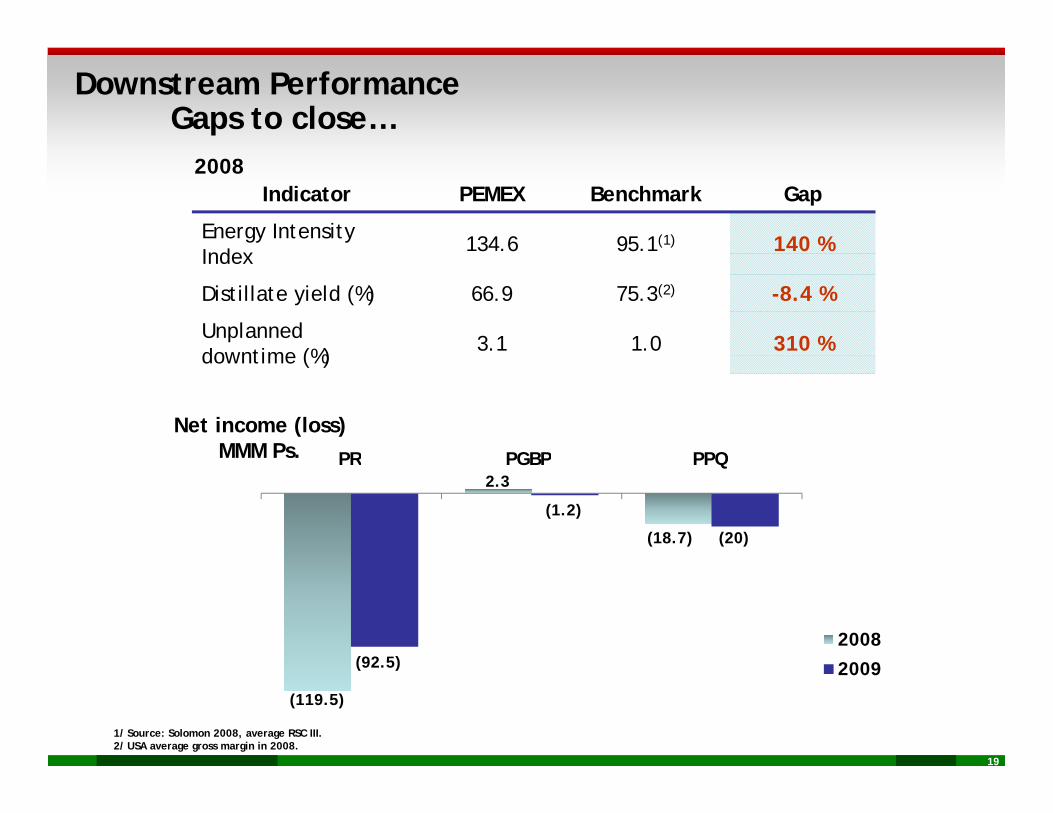

Downstream PerformanceGaps to close…

Indicator PEMEX Benchmark Gap

Energy Intensity Index 134.6 95.1(1) 140 %

2008

Index

Distillate yield (%) 66.9 75.3(2) -8.4 %

Unplanned downtime (%) 3.1 1.0 310 %downtime (%)

Net income (loss)MMM Ps. PR PGBP PPQ

(20)

. PR PGBP PPQ2.3

(1.2)

(18.7)

2008

2009(92 5)

19

1/ Source: Solomon 2008, average RSC III.2/ USA average gross margin in 2008.

2009

(119.5)

(92.5)

Refining Strategies• Maintenance and reliability improvements.

Increase reliability and profitability

y p• Yield improvements in gasoline and middle distillates.• Integrated optimization of the SNR (National Refining

System).

Deep conversionProjects atMinatitlán, Salamanca and Tula

• Minatitlán to start in 4Q-2010.• Salamanca to start in 2014.• Tula project to be merged with new capacity project.• Salina Cruz scope and startup date to be determined.

New refined products supply • New supply projects under study.

C li i h d d h h i d l l

Fuels qualityNOM-086

• Compliance with standard through imports and localproduction.

• Third and final public bid for gasoline: Dec. 2009.• First public bid for diesel: Jan 2010 (Cadereyta).

R i i bid b i d i 2011

• New pipeline (Tuxpan-México) scheduled to start operationsin 2010.

l f l

Increase importcapacity and

• Remaining bids to be assigned in 2011.

20

• Relocation of terminals.• Redefinition of inventory requirements.• Turnaround maintenance in marine terminals.

strengthen storage and distribution

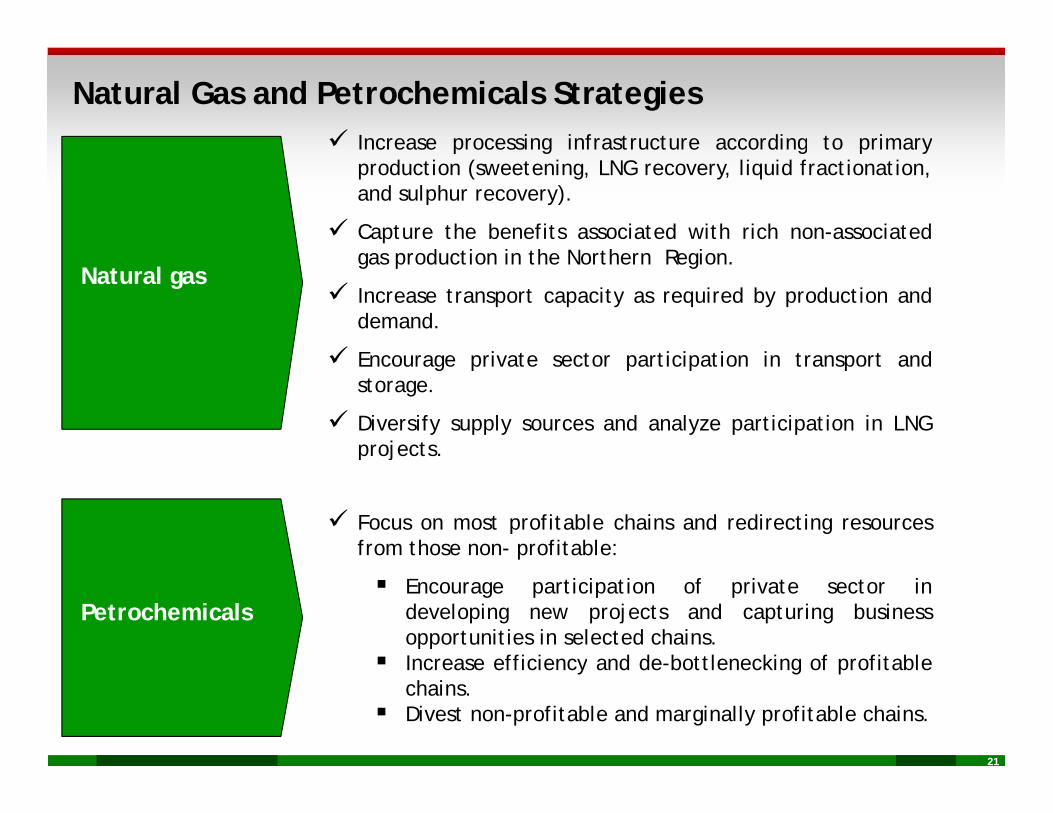

Natural Gas and Petrochemicals Strategies Increase processing infrastructure according to primaryp g g p y

production (sweetening, LNG recovery, liquid fractionation,and sulphur recovery).

Capture the benefits associated with rich non-associatedg d ti i th N th R gigas production in the Northern Region.

Increase transport capacity as required by production anddemand.

Encourage private sector participation in transport and

Natural gas

Encourage private sector participation in transport andstorage.

Diversify supply sources and analyze participation in LNGprojects.p j

Focus on most profitable chains and redirecting resourcesfrom those non- profitable:

Petrochemicals Encourage participation of private sector in

developing new projects and capturing businessopportunities in selected chains.

Increase efficiency and de-bottlenecking of profitable

21

Increase efficiency and de-bottlenecking of profitablechains.

Divest non-profitable and marginally profitable chains.

Content

Energy Reform

Upstream

Downstream

PEMEX Sustainabilityy

Investment Program and Debt Strategy

22

Public Finance Public Policies

Pemex Sustainability

•Explicit role and objectives of the Federal Government.T t b idi

•Adequate fiscal regime.•Alternative tax sources.

Public Finance Public Policies

•Transparent subsidies.

•Corporate Governance

GovernanceEnergy Security

Equilibrium •Exploration investments.•New market design.•Investment in refining and distribution

•Corporate Governance.•Business decisions autonomy.

•Financial, budgetary and operational flexibility.

•Value creation and growth. •Environmental protection and social responsibility.

distribution.operational flexibility.

PEMEX Long-Term SustainabilityValue c eat o a d g owt .

•Strategic focus and process orientation.•Operational excellence.•Superior project execution.•Infrastructure modernization

v o e tal p otect o a d soc al espo s b l ty.•Industrial Safety.•Flexible labor relationships.•Development of human resources and research and development capabilities

23

•Infrastructure modernization.•Procurement flexibility.•Financial sustainability.

development capabilities.•Alignment of Union and PEMEX objectives.

Content

Energy Reform

U tUpstream

Downstream

PEMEX Sustainability

Investment Program and Debt Strategy

24

Investments (1)(2)(3)

Billion pesosTOTAL 263.4

32.0

251.9

2.0%Pemex-Petroquímica

Pemex- Gas y

113.7 122.9 127.0150.4

170.1201.7

251.9220.0

12%Pemex-Refinación

2.0%Pemex Gas y PetroquímicaBásica

3.

2003 2004 2005 2006 2007 2008 2009 2010 E(7)

Pemex-Exploración y Producción

84%

US$ billion10.7 10.9 10.8 13.8 15.6 18.1(4) 18.6(5) 20.4E(6)(7)

( )

25

(1) Figures may not total due to rounding(2) Includes upstream maintenance expenditures(3) Nominal figures

(4) Pesos per US$: 11.15 (7) “E” means Estimated(5) Pesos per US$: 13.52(6) Pesos per US$: 12.94

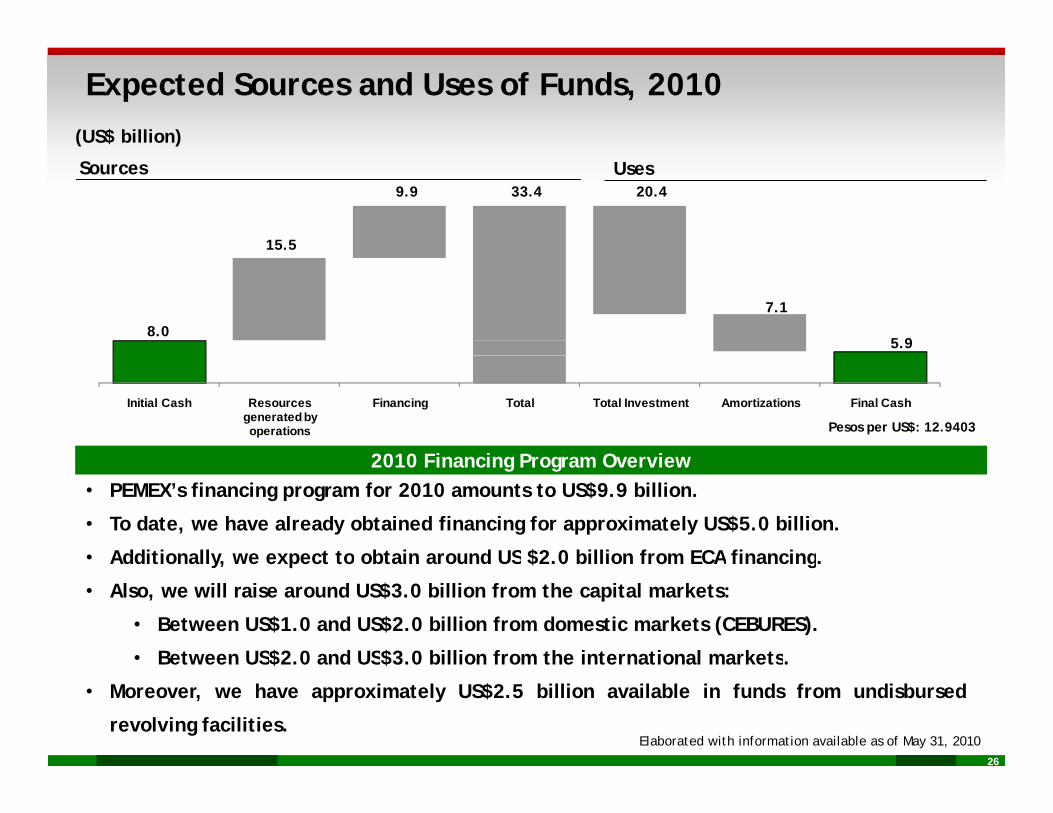

Expected Sources and Uses of Funds, 2010(US$ billion)

15.5

9.9 33.4 20.4Sources Uses

8.0

7.1

5.9

2010 Financing Program Overview

Initial Cash Resources generated by operations

Financing Total Total Investment Amortizations Final Cash

Pesos per US$: 12.9403

• PEMEX’s financing program for 2010 amounts to US$9.9 billion.

• To date, we have already obtained financing for approximately US$5.0 billion.

• Additionally we expect to obtain around US $2 0 billion from ECA financing

2010 Financing Program Overview

Additionally, we expect to obtain around US $2.0 billion from ECA financing.

• Also, we will raise around US$3.0 billion from the capital markets:

• Between US$1.0 and US$2.0 billion from domestic markets (CEBURES).

• Between US$2.0 and US$3.0 billion from the international markets.

26

Between US$2.0 and US$3.0 billion from the international markets.

• Moreover, we have approximately US$2.5 billion available in funds from undisbursed

revolving facilities.Elaborated with information available as of May 31, 2010

Debt Portfolio7 3

Maturity Profile – Consolidated DebtUS$ billion

6.2 5.7

5.2 5.3 4.9

4.3

7.3 US$ billion

Outstanding amount as of March 2010: 50 U.S.$ billion

4.3

2.5 2.2

3.0 3.4

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Debt by InstrumentPercentage

Debt by Currency ExposurePercentage

Pesos20%4%

Other

Cebures

49%15%

15%

BankLoans

InternationalBonds

27

Dollars80%

17%ECAs