unit 2 seminar ac 410 auditing unit 2 seminar chapters 1, 2, and 3

TRANSCRIPT

UNIT 2 SEMINAR

AC 410 AUDITING

UNIT 2 SEMINAR

CHAPTERS 1, 2, AND 3

Audit Opinion Formulation Process

The Audit Function

• Perform tests on an organization’s records to determine that they are accurate.

• Interpret FASB, IASB, GASB, and other authoritative pronouncements to ensure that financial statements are fairly presented.

• Make judgments about the fairness of complex accounting processes and then test, the organization’s system of internal control over financial reporting.

• Do all this in a totally objective, unbiased, and professionally skeptical manner.

LO 1: Auditing

“A systematic process of objectively obtaining and evaluating evidence regarding assertions about economic actions and events to ascertain the degree of correspondence between those assertions and established criteria and communicating the results to interested users.”

What is Attestation?

• Attestation involves gathering evidence about assertions, evaluating the evidence against objective criteria, and communicating the conclusion reached.

• Auditing is specific attestation service where the auditor gathers evidence to determine whether the financial statements are fairly presented in accordance with Generally Accepted Accounting Principles and issues an opinion to be used by third-party users, management, and the Board of Directors.

Auditing Process

• Gathering evidence to attest to assertions.

• Evaluating those assertions against objective criteria.

• Communicating the audit conclusion to interested parties.

LO 2: Auditing: A Special Function

• Auditing is both more and less than public accounting.– More because it includes internal and operational

auditing, governmental auditing, and other services that evaluate and report on managerial performance.

– Less because public accounting firms provide a variety of other assurance and non-audit services.

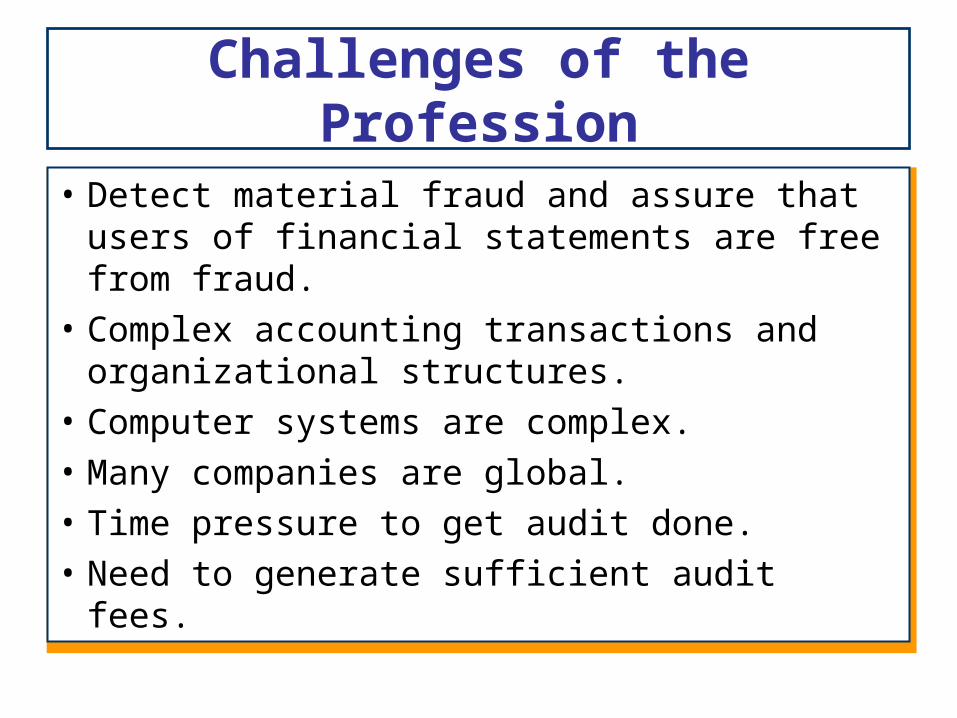

Challenges of the Profession

• Detect material fraud and assure that users of financial statements are free from fraud.

• Complex accounting transactions and organizational structures.

• Computer systems are complex.

• Many companies are global.

• Time pressure to get audit done.

• Need to generate sufficient audit fees.

Users of Audited Financial Statements

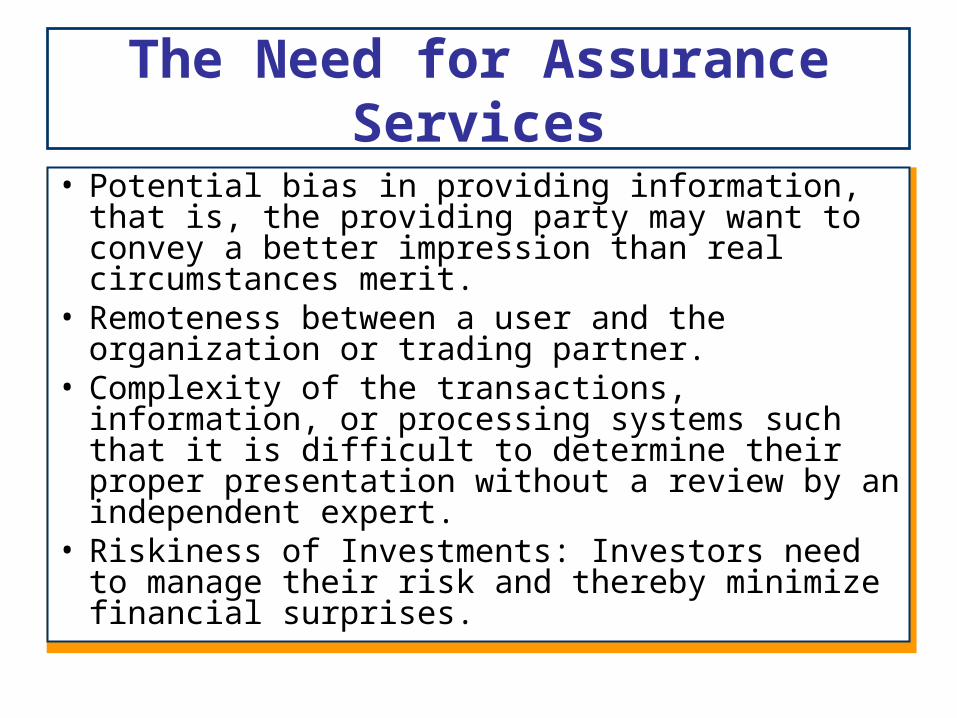

The Need for Assurance Services

• Potential bias in providing information, that is, the providing party may want to convey a better impression than real circumstances merit.

• Remoteness between a user and the organization or trading partner.

• Complexity of the transactions, information, or processing systems such that it is difficult to determine their proper presentation without a review by an independent expert.

• Riskiness of Investments: Investors need to manage their risk and thereby minimize financial surprises.

LO 3: The Accounting Profession’s Decade of Unprecedented Turmoil and Change

• The failure of one of the largest public accounting firms (Andersen).

• Four of the largest bankruptcies ever - each in companies where financial statement misrepresentation had taken place.

• Billions of investment and retirement dollars lost.

• Perception that auditors were not independent from their clients.

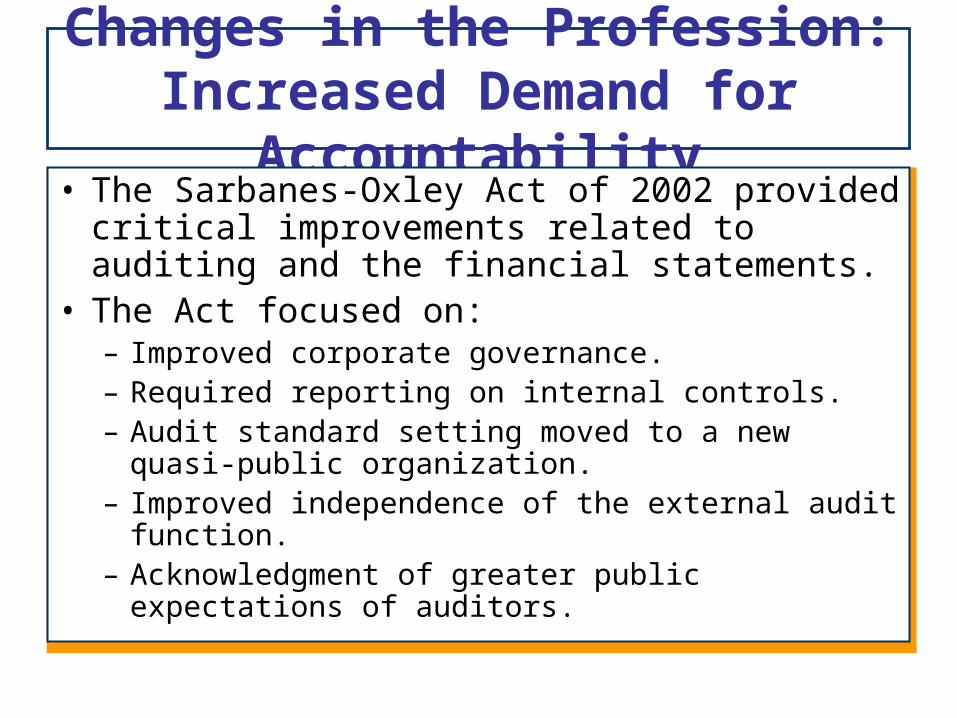

Changes in the Profession: Increased Demand for Accountability

• The Sarbanes-Oxley Act of 2002 provided critical improvements related to auditing and the financial statements.

• The Act focused on:– Improved corporate governance.– Required reporting on internal controls.– Audit standard setting moved to a new quasi-public

organization.– Improved independence of the external audit function.– Acknowledgment of greater public expectations of

auditors.

Improved Corporate Governance

• The lack of corporate governance was a major factor in business failures; most notably, a failure of Boards of Directors to oversee management, and effectively utilize the audit function.

• Sarbanes requires Boards of Directors be independent of the organization and exercise oversight over management and the audit function.

• Further, the Board of Directors, through its audit committee, is the "client" of the public accounting firm.

LO 4: Required Reporting on Internal Controls

• In most cases of major fraud, companies had poor internal

controls over financial reporting.• Effective internal control system that produces reliable

information should be established.• Report deficiencies in public reports so that its impact can be

assessed.• Treadway Commission’s report on Fraudulent Financial

Reporting in 1987 advanced the need for public reporting on internal control.

• Sarbanes requires the CEO and CFO of SEC registered

companies to assess and publicly report on the quality of its

internal controls over financial reporting.

Audit Standard Setting and Auditor Independence

• The audit function must be independent and objective if assurances are to be trusted by third parties.

• Auditor independence has been strengthened by requiring:1. The audit committee has the authority to hire and fire the

external auditors.2. Mandatory rotation of the audit engagement partner every five

years.3. Consulting work cannot be performed for audit clients.4. Increased oversight of potential independence conflicts by the

audit committee.

• Non-public companies and smaller audit firms are not required to follow all these guidelines.

Audit Standard Setting Moved

• The public lost confidence in the ability of the profession to serve the public interest.

• Sarbanes created the Public Company Accounting Oversight Board (PCAOB). – The PCAOB has authority to develop audit standards for

audits of publicly traded companies.– The PCAOB is also charged with performing peer review

of all public accounting firms that perform audits of public companies.

– The PCAOB is comprised of five public members appointed by the SEC.

• No more than two members can be CPAs.

LO 5: The AICPA’s Definition of Assurance Services

• The AICPA's Special Committee on Assurance Services defines assurance as: “Independent professional services that improve the quality of information, or its context, for decision makers."

• Assurance services involve three components:– Information or a process on which the assurance is provided.

– A user or group of users who derive value from the assurance provided.

– An assurance service provider.

What are the Attributes Needed to Perform Assurance Services?

1. Subject matter knowledge

2. Independence from parties requesting assurance

3. Agreed upon criteria to evaluate quality of presentation

4. Expertise in the process of gathering and evaluating evidence

What are the Levels of Assurance Provided?

1. Positive assurance (such as an audit opinion)

2. Limited or negative assurance (such as a review of financial statements)

3. No assurance (such as a compilation of financial statements)

The AICPA's Special Committee on Assurance Services has identified six areas of potential service:

1. Risk Assessment: Quality of processes implemented by an organization to identify, assess, and manage risks.

2. Business Performance Measurement: Processes to identify, measure, and communicate alternative measures of performance.

3. Information System Reliability: Quality of controls to ensure system security, reliability, timeliness, and accuracy.

4. Healthcare Performance Measurement: Provide information about the quality of services provided by healthcare providers.

5. Electronic Commerce: Provide assurance that systems and tools are designed and functioning with integrity and security.

6. Elder Care Plus: Provide assurance whether the needs of the elderly are being met by various caregivers.

What are Attest Services?

• Attest services are a subset of assurance

services.

• Attest services always involve evaluation of an

assertion made by one party to a third party.

• Attest services always involve a report sent to

a third party.

LO 6: Requirements to Enter the Public Accounting Profession

• Accounting and Auditing Expertise: In addition to technical knowledge, auditor must have sound conceptual understanding of financial reporting and auditing.

• Internal Auditing Expertise: Auditor must be able to analyze the organization’s internal controls to determine if there are weaknesses.

• Knowledge of Business and its Risks: Auditor must understand the basic structure of a business in order to identify significant risks affecting the client.

• Understanding Accounting System Complexity: Auditor must understand the challenges posed in a system in which traditional source documents do not exist.

Who Are the Providers of Assurance Services?

• The Public Accounting Profession

• The Internal Audit Profession

• The Governmental Audit Profession

The Public Accounting Profession

• More than 45,000 CPA firms in the United States, ranging sole-practitioners to large multinationals such as the Big 4.

• These firms provide a variety of services in the areas of assurance and financial statement services, tax planning and compliance, and consulting.

• The SEC has prohibited accounting firms from providing most consulting services to public companies that they audit.

• Such restriction on services has not been specified by the AICPA or regulatory authorities for public accounting firms that do not audit SEC registered clients.

Organization of CPA Firms

• The organizational hierarchy of CPA firms has been described as a pyramidal structure.– Partners (or owners) are at the top and are responsible for

the overall conduct of each audit.– Next, managers review the detailed audit work performed

by staff auditors.– Seniors are responsible for overseeing much of the day-to-

day activities on a specific audit.– Staff auditors perform the basic, detailed audit work.– Partners and managers may be involved in a number of

audit engagements being conducted simultaneously; seniors and staff are usually assigned to only one audit at a time.

The Internal Audit Profession

• Internal auditing is defined as: “An independent, objective assurance and consulting activity designed to add value and improve an organization's operations. It helps an organization accomplish its objectives by bringing a systematic, disciplined approach to evaluate and improve the effectiveness of risk management, control, and governance processes."

Internal Auditors Add Value to an Organization

• Internal auditors evaluate processes to identify and management risk, develop and implement effective internal controls.

• Internal auditors assure management and the Board of Directors on the company's compliance with policies or regulatory requirements, or the effectiveness of processes and operations.

• Internal auditors provide consulting services such as analyzing problems and identifying potential solutions.

• Internal auditors perform operational audits designed to evaluate the effectiveness, economy, and efficiency with which resources are employed.

Governmental Auditing Profession

• Employed by various Federal, state, and local

agencies.

• Governmental auditors perform all the types of

audits that internal auditors perform including

compliance, operational, and performance

audits.

LO 8: Professional and Regulatory Organizations

• The PCAOB established as part of the Sarbanes-Oxley Act of 2002 has authority to set auditing standards for audits of public companies and to perform quality reviews of all registered CPA firms.

• The SEC oversees the PCAOB and all companies publicly traded on the U.S. capital markets. It has the authority to establish GAAP for publicly traded companies, and to prosecute companies who violate SEC laws.

• The AICPA has long served as the primary governing organization of the public accounting profession. It provides a variety of continuing education programs and administers the Uniform CPA Examination. Membership in the AICPA is voluntary.

The Securities and Exchange Commission (SEC)

• Established by Congress in 1934 to regulate the capital market system.

• Over site of PCAOB and all public companies required to register with it to gain access to the U.S. capital market.

• Has the authority to establish GAAP for publicly traded companies.

• Has prosecutorial authority.

The American Institute of Certified Public Accountants (AICPA)

• Primary governing body of the public

accounting profession

• Continues to develop standards for audits of

non-public companies

• Administers the Uniform CPA Examination

Professional and Regulatory Organizations

• The State Boards of Accountancy are responsible for certifying and licensing CPAs in their state. While all state boards require passage of the Uniform CPA Examination, education and experience requirements vary by state.

• The Institute of Internal Auditors issued internal auditing standards and administers the Certified Internal Auditor program.

• The U. S. General Accounting Office is the nonpartisan audit agency for Congress. The GAO develops auditing standards for governmental audits.

LO1: Corporate Governance

“A process by which the owners and creditors of an organization exert control and require accountability for the resources entrusted to the organization. The owners (stockholders) elect a board of directors to provide oversight of the organization's activities and accountability to stakeholders"

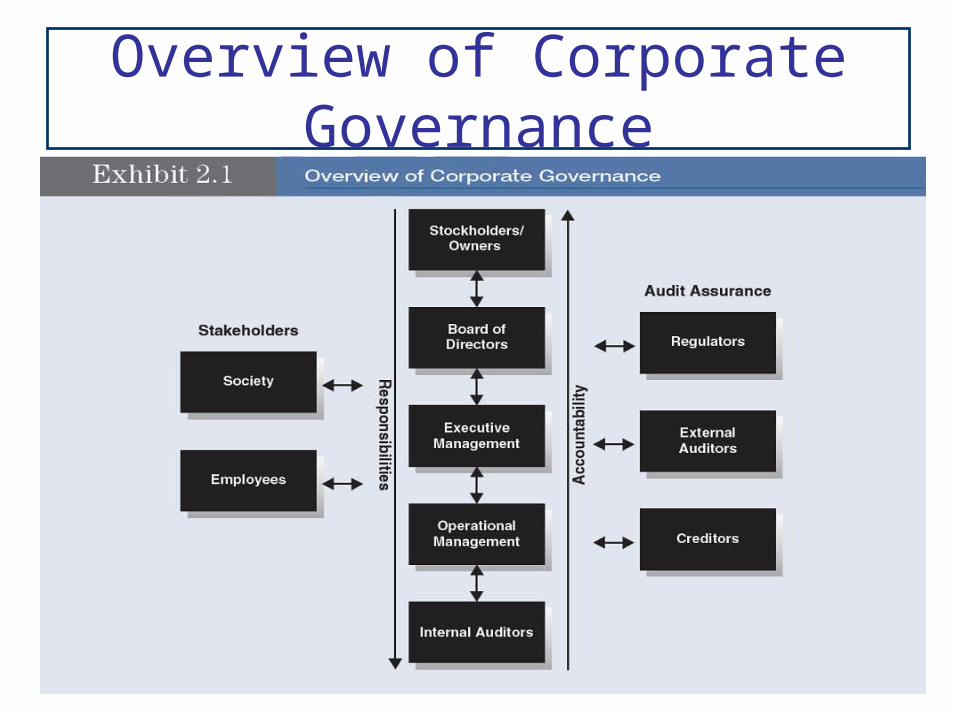

Primary parties involved in corporate governance

• Stockholders• Boards of Directors• Audit Committee as a subcommittee of the Board• Management• Internal Auditors• Self-Regulatory Accounting Organizations (e.g. AICPA,

FASB)• Other Self-Regulatory Organizations (e.g. NYSE, NASD)• Regulatory Agencies (e.g. SEC, FDIC, Environmental

Protection Agency)• External Auditors

Overview of Corporate Governance

LO2: Corporate Governance Responsibilities and Failures

• What are SEC concerns regarding the auditing profession?– Auditors were no longer willing to confront clients

over questionable accounting practices– Consulting fees were impairing auditor

independence– Accountants were using technical interpretations

of GAAP to push the limits of accounting

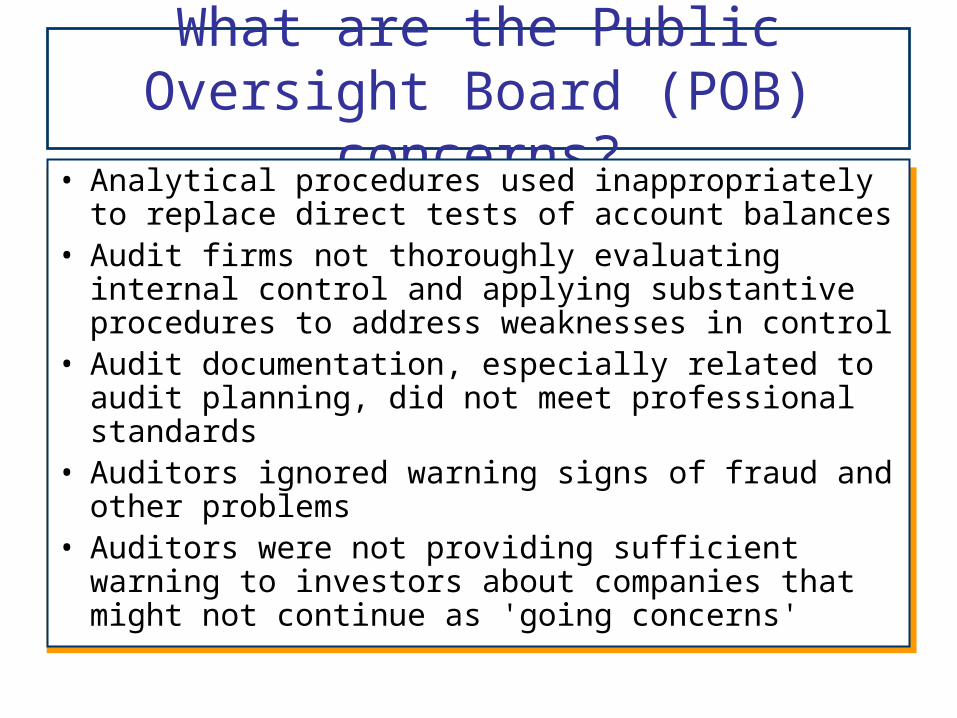

What are the Public Oversight Board (POB) concerns?

• Analytical procedures used inappropriately to replace direct tests of account balances

• Audit firms not thoroughly evaluating internal control and applying substantive procedures to address weaknesses in control

• Audit documentation, especially related to audit planning, did not meet professional standards

• Auditors ignored warning signs of fraud and other problems

• Auditors were not providing sufficient warning to investors about companies that might not continue as 'going concerns'

LO3: The Sarbanes/Oxley Act of 2002

Was passed by Congress in response to massiveaccounting scandals

Significant provisions include:• Establishes the Public Companies Accounting

Oversight Board (PCAOB) with broad powers, including the power to set auditing standards for audits of public companies

• Requires the CEO and CFO certify the financial statements

• Requires companies to provide a comprehensive report on internal controls over financial reporting

• Requires companies to certify correctness of financial statements quality of its internal controls

• Audit Committees given expanded powers as the 'audit client' and must pre-approve any non-audit services by its external auditors

• Audit Committees must report their activities to the public

• Audit Committees must have at least one person who is a financial expert. Other members must be knowledgeable in financial accounting and control

The Sarbanes/Oxley Act of 2002 (continued)

The Sarbanes/Oxley Act of 2002 (continued)

• Audit engagement partners, as well as other partners and managers with significant roles in the audit, must be rotated off the engagement every five years

• A "cooling off" period before an audit partner or manager can take a high-level position with an audit client without jeopardizing the independence of the public accounting firm

• Increased disclosure of "off-balance sheet" transactions or agreements that may have a material effect Requires the GAO to study a number of issues including the effect of consolidation on competition with the accounting profession, and an analysis of mandatory audit firm rotation

The PCAOB

• Sarbanes/Oxley granted the PCAOB broad authority including the powers to– Set auditing standards - the PCAOB has chosen to

set auditing standards– Set financial accounting standards - the PCAOB

has chosen to let the FASB continue to set accounting standards

– Set standards for the reports on internal control and risk management

– Perform quality reviews of public accounting firms and recommend penalties if the firms fail to perform

The PCAOB (continued)

– Establish quality control standards for the audits of public companies

– Require all public accounting firms that audit public companies to register with the PCAOB and become licensed to perform such audits

What are auditor independence provisions?

• Prohibits audit firms from performing consulting work for their audit clients (in most cases)

• Makes the Audit Committee the auditor's client• Requires the Audit Committee to pre-approve all

non-audit services by the audit firm• Requiring the audit committee to pre-approve any

nonaudit services provided by the public accounting firm

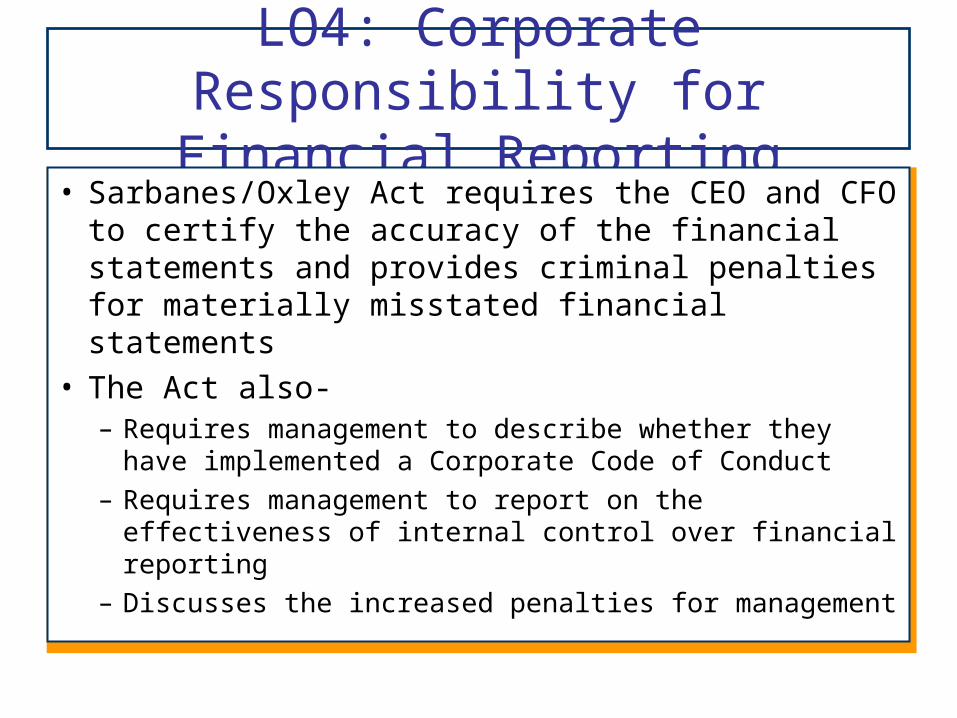

LO4: Corporate Responsibility for Financial Reporting

• Sarbanes/Oxley Act requires the CEO and CFO to certify the accuracy of the financial statements and provides criminal penalties for materially misstated financial statements

• The Act also-– Requires management to describe whether they have

implemented a Corporate Code of Conduct

– Requires management to report on the effectiveness of internal control over financial reporting

– Discusses the increased penalties for management

LO5: Enhanced role of audit committees

• As per Sarbanes-Oxley Act audit committees– Is designated as the audit client

– Has oversight responsibilities over the internal audit and financial reporting processes

– Must be comprised of "outside" directors, i.e. not members of management or have other relationships with the organization

– Must report on its activities, including the results of significant discussions with the external auditor

Audit committee responsibilities include

• Be apprised of all significant accounting decisions made by management

• Be apprised of all significant changes in accounting systems and system controls

• Have authority to hire and fire the external auditor. Review the audit plan and discuss audit results with the auditor

• Have authority to hire and fire the head of the internal audit function and set the budget for the internal audit function. Review the audit plan and discuss all significant results

• Receive all regulatory audit reports and meet with regulatory auditors to discuss findings

LO10: Generally Accepted Auditing Standards (GAAS) and IAASB Principles

• General Standards provide guidance in hiring and training of auditors

• Fieldwork Standards help auditors plan and perform the audit

• Reporting Standards help ensure clear communication between auditor and statement users

LO11: Fundamental Principles of IAASB Auditing Standards

• Objective of an audit of financial statements• Comply with relevant ethical requirements relating to

the audit engagement• Audit should be conducted in accordance with

International Standards on Auditing• Auditor should plan and perform an audit with an

attitude of professional skepticism• Reasonable assurance provided• Audit risk and materiality• Acceptability of the Financial Reporting Framework

Assurance Standards

• Reasonable assurance engagements– “Engagements in which a practitioner expresses a

conclusion designed to enhance the degree of confidence of the intended users other than the responsible party about the outcome of the evaluation or measurement of a subject matter against criteria"

• Limited assurance engagements– This is one in which the objective is to provide more

limited assurance by doing less work that may be appropriately understood by all three parties. Limited assurance engagements normally result in “negative assurance” and check to see if anything comes to their attention indicating a problem.

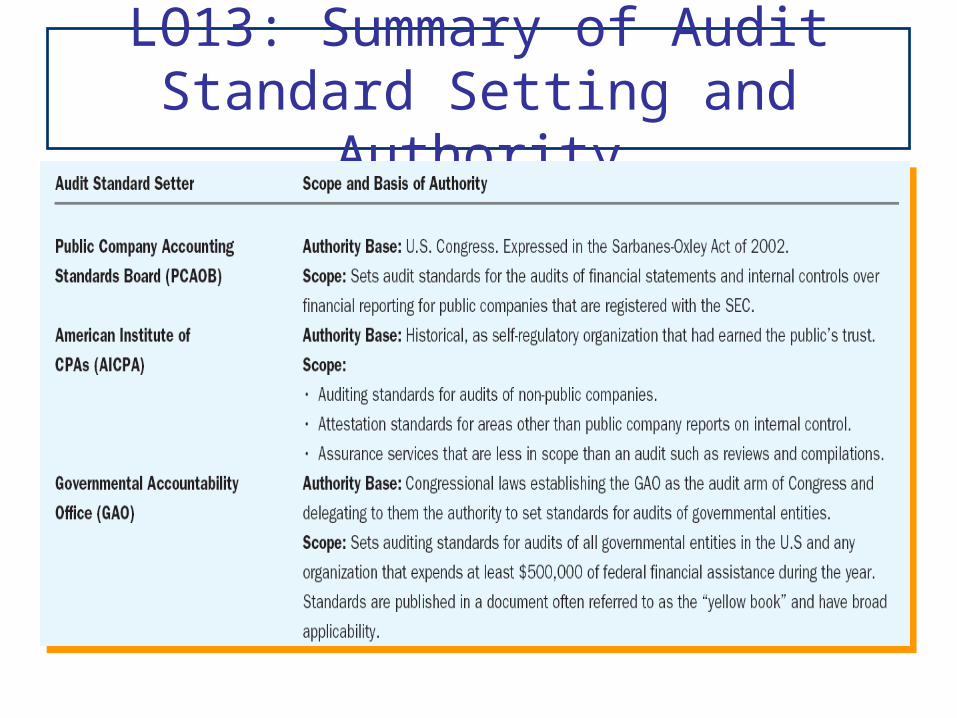

LO13: Summary of Audit Standard Setting and Authority

Summary of Audit Standard Setting and Authority (continued)

LO 1 Framework for Professional Decision-Making

LO 2 Accepting a Public Trust

• To maintain the public's trust, public accountants must act with professional integrity

• Ethical problem occurs when an individual is morally or ethically required to take an action that may conflict with his or her immediate self-interest

• Ethical dilemma occurs when there are conflicting moral duties or obligations

LO 3 Ethical Theories

• Utilitarian theory - an action is ethical if it achieves the greatest good for the greatest number of people. Utilitarianism requires:– Identify potential problem and courses of action– Identify potential impact of actions on each affected party– Assess the desirability of each action– Perform overall assessment of the greatest good for the

greatest number• Problems with utilitarianism include:

– Disagreement about the likely impact of actions– Problems measuring the "greatest good"– Assumption that the ends achieved justify the means

Rights Theory

• Rights theory - evaluates actions based on the fundamental rights of the parties involved. Uses a hierarchy of rights where higher-order rights take precedence over lower-order rights.

• Rights theory requires the rights of affected parties be examined as a constraint on ethical decision making.

• It is most effective in identifying outcomes that should be eliminated or identifying situations in which the utilitarian answer would be at odds with most societal values.

LO 4 An Ethical Framework (Using the Utilitarian & Rights Theories)

• Identify the ethical issue(s)• Determine the affected parties and identify their rights• Determine the most important rights• Develop alternative courses of action• Determine the likely consequences of each proposed course of

action• Assess possible consequences including estimation of the

greatest good for the greatest number• Determine whether rights framework would cause any action

to be eliminated• Decide on appropriate course of action

International Ethics Standards Board for Accountants

The IESBA Code of Ethics require accountants to adhere to five fundamental principles:

• Integrity

• Objectivity

• Professional Competence and Due Care

• Confidentiality

• Professional Behavior

LO 6 The AICPA Code of Professional Conduct

• The AICPA Code of Professional Conduct provide guidance and rules to all members

• Provide the basis for the rules of conduct

• Rules of Conduct are specific guidelines that reflect the broad principles of the profession

• RULINGS are issued in response to member questions about specific situations

The AICPA Principles of Professional Conduct (continued)

• Responsibilities - members should exercise sensitive professional and moral judgment in all their activities

• Public interest - members should act in a way that serves the public interest, maintains public trust, and shows commitment to professionalism

• Objectivity and independence - members should be objective and free of conflicts when performing professional responsibilities. Members in public practice must be independent in fact and appearance when providing attestation services.

The AICPA Principles of Professional Conduct (continued)

• Integrity - members should perform all professional responsibilities with the highest sense of integrity

• Due care - members shall observe the profession's ethical and technical standards, strive to improve competence and quality of services provided, and discharge professional responsibilities to the best of their ability.

• Scope and nature of services - members in public practice shall observe the principles of the Code of Professional Conduct in determining the scope and nature of services to be provided.

Enforcement of the Code

• Members who violate the AICPA code may have their membership terminated

• Members who violate a State Board of Accountancy's code are subject to disciplinary action including suspension or revocation of the member's certificate and license to practice.

• If the State Board suspends the member's certificate, it can mandate conditions, such as additional continuing education, that must be satisfied before the member's certificate is reinstated.

LO 7 Independence Rules of the SEC and the PCAOB

• SEC and PCAOB have established independence guidance and rules that apply to auditors of publicly held companies

• The SEC has taken a principles-based approach in dealing with independence issues

Independence Rules of the SEC and the PCAOB

• Auditor independence is impaired when– mutual or conflicting interest between the

accountant and the audit client is created– accountant is placed in the position of auditing his

or her own work– accountant is acting as management or an

employee of the audit client– An accountant is placed as an advocate for the

audit client

Prohibited non audit services

• Bookkeeping or other services related to the accounting records of audit client

• Financial information systems design and implementation

• Appraisal and valuation services, fairness opinions, or contribution-in-kind reports

• Actuarial services,• Internal audit outsourcing services,• Management functions, etc

LO 8 Further Considerations Regarding Auditor Independence

• Independence is the cornerstone of auditing profession

• Auditors must be independent – in fact – objective and unbiased in their actions

and– in appearance – perceived by knowledgeable users

of financial statements as independent

LO 9 Major Threats to Independence

• Compensation schemes

• Who is the client?

• Familiarity with the client

• Time pressures

• Rationalizing behavior

• Providing nonaudit services

Managing Threats to Independence

• Establishing and monitoring corporate codes of conduct

• Developing appropriate compensation schemes• Implementing high-level reviews of decisions to

accept or retain clients• Separating consulting activities from audit activities• Performing within-firm reviews of audit work and

audit documentation• Performing reviews and inspections within the

profession

Important Role of Audit Committees

• Oversight of engagement of company’s external auditor

• Overseeing auditors independence

• Preapprove permitted services provided by auditor

• Require firms to communicate certain information related to the firm’s independence

UNIT 2 SEMINAR

THE END