unicredit - globalcapital · unicredit’s ratings reflect its good geographical and business...

TRANSCRIPT

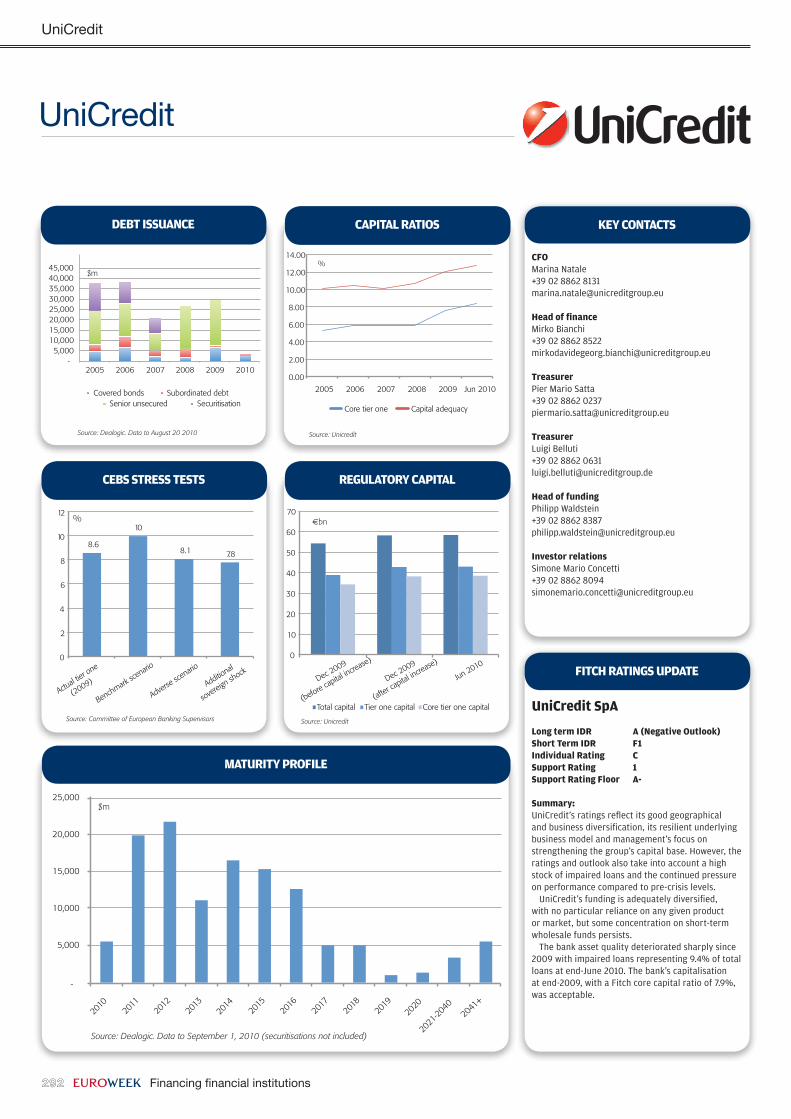

UniCredit

292 EuroWeek Financing financial institutions

UniCredit

- 2005 2006 2007 2008 2009 2010

Covered bonds Subordinated debt Senior unsecured Securitisation

5,000 10,000 15,000 20,000 25,000 30,000 35,000

40,000 45,000

Debt issuance

$m

Source: Dealogic. Data to August 20 2010

Debt issuance

-

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

-204

0

2041

+

5,000

10,000

15,000

20,000

25,000

Source: Dealogic. Data to September 1, 2010 (securitisations not included)

$m

Maturity Profile

Source: Unicredit

%

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

2005 2006 2007 2008 2009 Jun 2010

Core tier one Capital adequacy

caPital ratios

Actual t

ier one

(2009)

Benchmark sc

enario

Adverse

scenario

Additional

sovereig

n shock

Source: Committee of European Banking Supervisors

%

8.6

10

8.1 7.8

0

2

4

6

8

10

12

cebs stress tests

cfoMarina Natale+39 02 8862 [email protected]

Head of financeMirko Bianchi+39 02 8862 [email protected]

treasurerPier Mario Satta+39 02 8862 [email protected]

treasurerLuigi Belluti+39 02 8862 [email protected]

Head of fundingPhilipp Waldstein+39 02 8862 [email protected]

investor relationsSimone Mario Concetti+39 02 8862 [email protected]

Key contacts

Source: Unicredit

�bn

0

10

20

30

40

50

60

70

Dec 2009

(before capital

increase

)

Dec 2009

(after ca

pital incre

ase)

Jun 2010

Total capital Tier one capital Core tier one capital

regulatory caPital

unicredit spa

long term iDr a (negative outlook)short term iDr f1individual rating csupport rating 1support rating floor a-

summary:UniCredit’s ratings reflect its good geographical and business diversification, its resilient underlying business model and management’s focus on strengthening the group’s capital base. However, the ratings and outlook also take into account a high stock of impaired loans and the continued pressure on performance compared to pre-crisis levels.

UniCredit’s funding is adequately diversified, with no particular reliance on any given product or market, but some concentration on short-term wholesale funds persists.

The bank asset quality deteriorated sharply since 2009 with impaired loans representing 9.4% of total loans at end-June 2010. The bank’s capitalisation at end-2009, with a Fitch core capital ratio of 7.9%, was acceptable.

fitcH ratings uPDate

UniCredit

Financing financial institutions EuroWeek 293

unicredit spa

issue type: TierI

Pricing date: July14,2010

Value: €500m

Maturity date: Perpetualnon-call10

coupon: 9.375%

bookrunners: CreditSuisse,JPMorgan,Hypovereinsbank

unicredit bank austria ag

issue type: Coveredbond

Pricing date: June8,2010

Value: €750m

Maturity date: June15,2015

coupon: 2.375%

bookrunners: BayernLB,DZBank,ErsteGroupBank,LBBW,UniCreditGroup

unicredit bank ag

issue type: Coveredbond

Pricing date: May20,2010

Value: €500m

Maturity date: May31,2017

coupon: 2.625%

bookrunners: BayernLB,GudmeRaaschouBank,NordLB,UniCreditGroup,WestLB

Source: Dealogic

rank lead Manager amount $m no of issues

% share

1 UniCredit Group 5,488 33 42.59

2 SG Corporate & Investment Banking

1,108 3 8.6

3 LBBW 671 6 5.2

4 HSBC 588 3 4.56

5 Natixis 552 4 4.28

6 BNP Paribas 494 4 3.83

7 Deutsche Bank 471 2 3.65

8 DZ Bank 467 3 3.63

9 ING 393 2 3.05

10 BayernLB 300 2 2.33

subtotal 10,530 42 81.73

total 12,884 48 100

Source: Dealogic (Sep 20, 2009 to Sep 19, 2010)

recent Deals

toP booKrunners

bp

Five year senior CDS prices. Source: Markit

24-Au

g-2009

24-Se

p-2009

24-O

ct-20

09

24-N

ov-20

09

24-D

ec-20

09

24-Ja

n-201

0

24-Fe

b-201

0

24-M

ar-20

10

24-Ap

r-201

0

24-M

ay-20

10

24-Ju

n-201

0

24-Ju

l-201

0

24-Au

g-201

0 0

50

100

150

200

250

UniCreditUBS

Intesa SanpaoloDeutsche Bank

Commerzbank

cDs Pricing

Source: Unicredit

%

50.0

52.0

54.0

56.0

58.0

60.0

62.0

64.0

2005 2006 2007 2008 2009 1H10

cost/incoMe ratio

Source: Unicredit

%

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

2005 2006 2007 2008 2009 1H10

return on equity

Source: Unicredit

�m

0

500

1000

1500

2000

2500

3000

3500

4000

4500

1Q09 2Q09 3Q09 4Q09 1Q10 2Q10

Operating profit Net profit attributable to the group

incoMe stateMent

Source: Unicredit

�bn

0

200

400

600

800

1000

1200

2005 2006 2007 2008 2009 Jun 2010

total assets