190,191 espirito santo - globalcapital...espirito santo financial group espirito santo financial...

TRANSCRIPT

190 EuroWeek Financing financial institutions

Espirito Santo Financial Group

Espirito Santo Financial Group

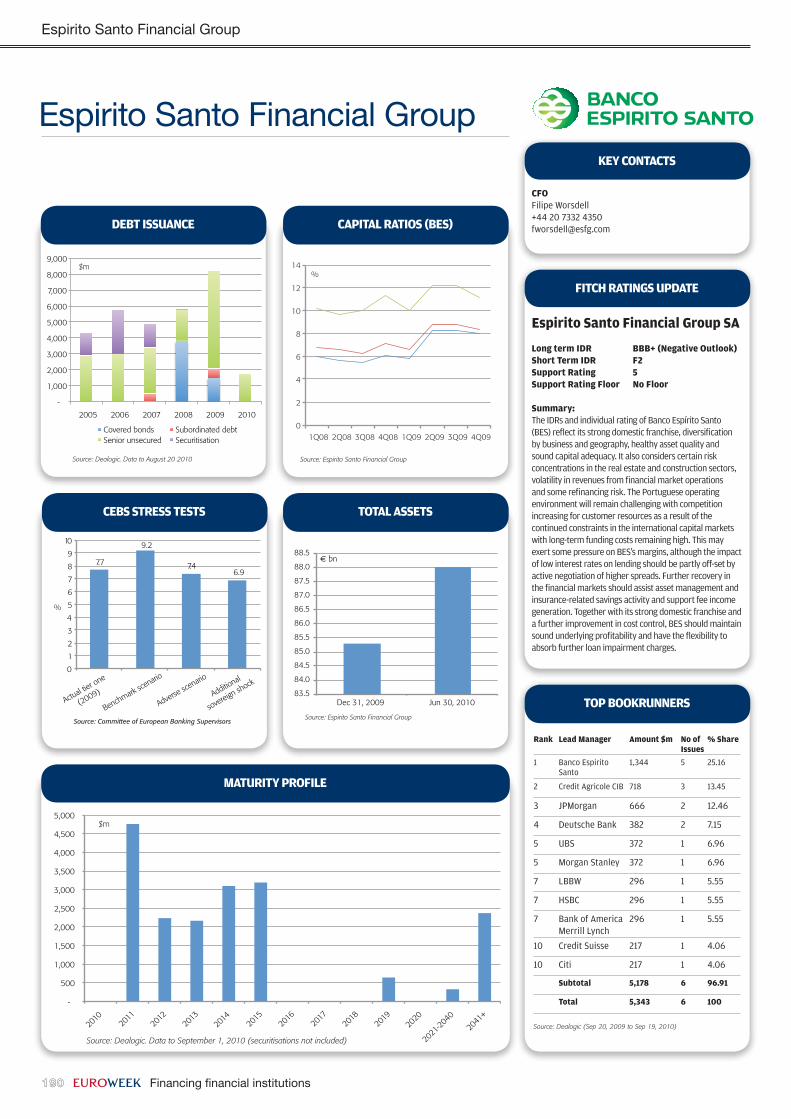

Covered bonds Subordinated debt Senior unsecured Securitisation

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2005 2006 2007 2008 2009 2010

Source: Dealogic. Data to August 20 2010

$m

Debt issuance

Debt issuance

Rank Lead Manager amount $m no of issues

% share

1 Banco Espirito Santo

1,344 5 25.16

2 Credit Agricole CIB 718 3 13.45

3 JPMorgan 666 2 12.46

4 Deutsche Bank 382 2 7.15

5 UBS 372 1 6.96

5 Morgan Stanley 372 1 6.96

7 LBBW 296 1 5.55

7 HSBC 296 1 5.55

7 Bank of America Merrill Lynch

296 1 5.55

10 Credit Suisse 217 1 4.06

10 Citi 217 1 4.06

subtotal 5,178 6 96.91

total 5,343 6 100

Source: Dealogic (Sep 20, 2009 to Sep 19, 2010)

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2010

20

11

2012

2013

2014

20

15

2016

2017

2018

2019

2020

2021

-204

0

2041

+

Source: Dealogic. Data to September 1, 2010 (securitisations not included)

$m

MatuRity PRofiLe

toP bookRunneRs

cfoFilipe Worsdell+44 20 7332 [email protected]

key contacts

Actual t

ier one

(2009)

Benchmark sce

nario

Adverse sce

nario

Additional

sovereign sh

ock

Source: Committee of European Banking Supervisors

%

7.7

9.2

7.4 6.9

0

1

2

3

4

5

6

7

8

9

10

cebs stRess tests

Source: Espirito Santo Financial Group

€ bn

83.5

84.0

84.5

85.0

85.5

86.0

86.5

87.0

87.5

88.0

88.5

Dec 31, 2009 Jun 30, 2010

totaL assets

Source: Espirito Santo Financial Group

%

0

2

4

6

8

10

12

14

1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09

caPitaL Ratios (bes)

espirito santo financial Group sa

Long term iDR bbb+ (negative outlook)short term iDR f2support Rating 5support Rating floor no floor

summary:The IDRs and individual rating of Banco Espírito Santo (BES) reflect its strong domestic franchise, diversification by business and geography, healthy asset quality and sound capital adequacy. It also considers certain risk concentrations in the real estate and construction sectors, volatility in revenues from financial market operations and some refinancing risk. The Portuguese operating environment will remain challenging with competition increasing for customer resources as a result of the continued constraints in the international capital markets with long-term funding costs remaining high. This may exert some pressure on BES’s margins, although the impact of low interest rates on lending should be partly off-set by active negotiation of higher spreads. Further recovery in the financial markets should assist asset management and insurance-related savings activity and support fee income generation. Together with its strong domestic franchise and a further improvement in cost control, BES should maintain sound underlying profitability and have the flexibility to absorb further loan impairment charges.

fitch RatinGs uPDate

Financing financial institutions EuroWeek 191

Espirito Santo Financial Group

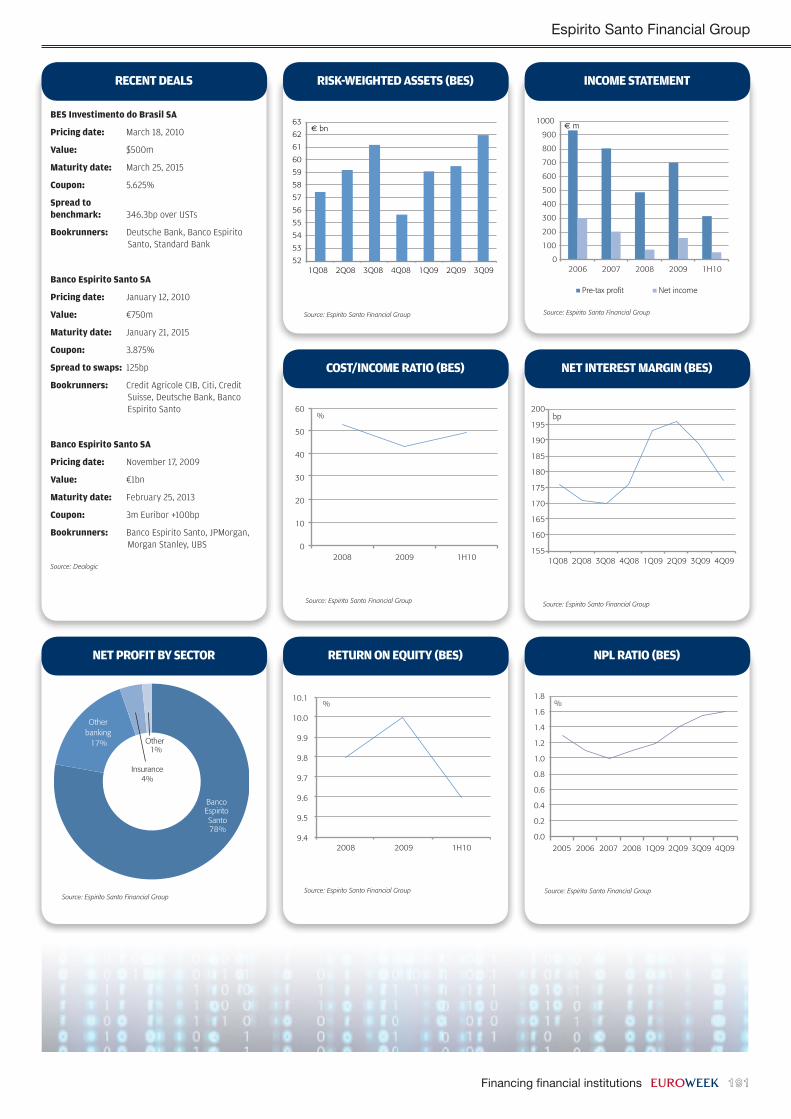

bes investimento do brasil sa

Pricing date: March18,2010

Value: $500m

Maturity date: March25,2015

coupon: 5.625%

spread to benchmark: 346.3bpoverUSTs

bookrunners: DeutscheBank,BancoEspiritoSanto,StandardBank

banco espirito santo sa

Pricing date: January12,2010

Value: €750m

Maturity date: January21,2015

coupon: 3.875%

spread to swaps: 125bp

bookrunners: CreditAgricoleCIB,Citi,CreditSuisse,DeutscheBank,BancoEspiritoSanto

banco espirito santo sa

Pricing date: November17,2009

Value: €1bn

Maturity date: February25,2013

coupon: 3mEuribor+100bp

bookrunners: BancoEspiritoSanto,JPMorgan,MorganStanley,UBS

Source: Dealogic

Recent DeaLs

Source: Espirito Santo Financial Group

%

0

100

200

300

400

500

600

700

800

900

1000

2006 2007 2008 2009 1H10

Pre-tax profit Net income

€ m

incoMe stateMent

Source: Espirito Santo Financial Group

%

0

10

20

30

40

50

60

2008 2009 1H10

cost/incoMe Ratio (bes)

Source: Espirito Santo Financial Group

%

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2005 2006 2007 2008 1Q09 2Q09 3Q09 4Q09

nPL Ratio (bes)

Source: Espirito Santo Financial Group

€ bn

52

53

54

55

56

57

58

59

60

61

62

63

1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09

Risk-weiGhteD assets (bes)

Source: Espirito Santo Financial Group

bp

155

160

165

170

175

180

185

190

195

200

1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09

net inteRest MaRGin (bes)

Source: Espirito Santo Financial Group

%

9.4

9.5

9.6

9.7

9.8

9.9

10.0

10.1

2008 2009 1H10

RetuRn on equity (bes)

Source: Espirito Santo Financial Group

Banco Espirito Santo 78%

Other banking

17%

Insurance 4%

Other 1%

net PRofit by sectoR