uk tax environment assignment help

TRANSCRIPT

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

INTRODUCTION

My name is Vivien; recently I am a tax practitioner of L & T consultancy firm which provides taxation

advices for private clients. I am going to meet a new client who named Julia Gillard, she is an UK

resident, and she was born on 16th December, 1970. She has received correspondence from HMRC

department to proclaim her income earned from employment (Marketing Director) ans self-

employment (Graphic Designer). After reading, she does not understand clearly about the authority

requirements, so now as a tax practioner I will prepare various documents and explain to her what she

does not clear.

In this presentation, I will help Julia to identify, also caculate her relevant income, expenses,

allowances, her tax payable, advice her on payment dates and finally I will help her to complete

relevant documentation and tax return. In addition, I will explain UK Tax Environment for her.

1

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

LO1 - UNDERSTAND THE DUTIES AND RESPONSIBILITIES OF THE TAX PRACTITIONER IN

THE UK TAX ENVIRONMENT

OUTLINE TASK 1.1- THE UK TAX ENVIRONMENT:

UK TAX ENVIRONMENT

DIAGRAM OF UK TAX FRAMEWORK

UK TAX FRAMEWORK

UK TAX LEGISLATION

TAX YEAR DIRECT TAX INDIRECT TAX

VAT CUSTOMS & EXCISE duty

CAPITAL GAIN TAX INCOME TAX CORPORATION TAX

SAVING INCOME NON-SAVING INCOME DIVIDEND

PAYE TAX RATE

PARTIES INVOLVED

HMRC TAX PAYER TAX PRACTITIONER

1.1 THE UK TAX ENVIRONMENT:

For any country in the world, tax is the main source of the state revenue, and it is the most important

thing of a country, and UK is not an exception. In UK, every citizen has a responsibility in paying tax 2

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

for the gorvernment if they have income. In order to help my client to understand clearly, in this section

I will explain some basic information about UK Tax System.

UK Tax Environment:

In UK, everyone who has income must pay tax for the gorvernment through tax department, and the tax

authority of UK called HMRC, which stand for Her Majesty’s Revenue & Customs. The main

responsibilities of HMRC is making sure that the money is available to fund the UK’s public services

and for helping families and individuals with targeted financial support, for safeguarding the flow of

money to the Exchequer through our collection, compliance and enforcement activities1. In order to do

that, HMRC will collect the tax from both of individual (includes UK residence and non UK residence)

and corporation, which do the business in UK through direct and indirect tax. HMRC works with help

from the UK Treasury so The Tax System of UK can run smoothly. Treasury has responsibility in

imposing and collecting the tax.

UK Tax Framework:

1 HMRC Websites,n.d : https://www.gov.uk/government/organisations/hm-revenue-customs/about

3

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

Figure 1: UK tax framework

In the UK Tax Framework, the top one is Treasure, they are responsible for the public finance in UK

imposes and collect taxation, and they appoint the Board of Inland Revenue (HMRC). On April 2005,

Inland Revenue is a department of the British Government responsible for the collection of direct

taxation, including income tax, national insurance contributions, capital gains tax, inheritance tax,

corporation tax, petroleum revenue tax and stamp duty. Recently, they administered the Tax Credits

schemes, annd Child Tax Credit, the Inland Revenue was also responsible for the payment of child

benefit. Therefore, Broad of Inland Revenue must collect income tax of individual and companies

based on decentralization system in UK that is they will divide the country into 4 regions and each

4

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

regions subdivided into districts and each district has a district inspector and the official title of

inspector is HM inspector of Taxes.2

UK tax legislation:

Tax Year:

In UK, the tax year or year assessment runs from 6th April of this year to 5th April of the next year.

For example, from the scenario, in this assignment, the tax year last from 6th April 2011 to 5th April

2012.

According to the UK Tax framework, in tax legislation people have to pay tax follwed two types, which

are direct tax and indirect tax:

1. Direct Tax:

Direct taxes are caculated based on income, profits or gains and are either deducted at source or paid

directly to the tax authorities3. All of those taxes are administered by HM Revenue and Customs

(HMRC). The main direct taxes which are payable are include income tax, capital gains tax and

corporation tax

2 Source: Taxation Lecture Slide Number 12, 13

3 Source: Taxation lecture session 1 – slide number 10

5

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

Tax Suffered by Source

Income tax

individual Partnerships Income & Corporation Taxes Act 1988,

Capital Allowance Act 2001, Income

Tax Act 2003

Corporation Tax Companies ICTA 1988, CAA 2001 as above

CGT

Individual, Partnerships,

Companies (which pay

tex on CG in the form of

corporation tax)

Taxation of Chargebale Gains Act 1992

(TCGA 1992) and subsequent Finance

Acts

Figure 2: The Main Taxes4

Income Tax:

“Income Tax is a tax on income. Not all income is taxable and you're only taxed on 'taxable

income' above a certain level. Even then, there are other reliefs and allowances that can reduce

your Income

Tax bill - and in some cases mean you've no tax to pay”5.

Types of Income:Income tax charged on income, which is amount of money you earn from employment, self-

employment, rental income, pension income, interest on savings, or money from shares.6 Each

tax payer will have a different amount of income money, so they will have different taxable

amount and tax payable amount. However, in order to caculate the income tax of tax payers,

4 Source: Taxation Lecture session 1 – slide numbert 9

5 HMRC Websites,n.d: http://www.hmrc.gov.uk/incometax/basics.htm

6 HMRC Websites,n.d: http://www.hmrc.gov.uk/complaints-appeals/how-to-appeal/direct-tax.htm

6

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

HMRC will caculate through 3 types of income which are saving income, non-saving income

and dividend, and it is applied for everyone who pays income tax.- Savings income : savings income is all the income from the investment. It can be the interest

on loan and bank or building society accounts.- Non-savings income: Non savings income includes three types of income that employment

income (the income from employment), trading income (the income from trades and

profession) and the property income (the income from renting out property)- Dividend income : dividend income is the income which related in the investment on

dividend. Tax rate 2011/2012 by tax band:

Each tax payer will have a different amount of income money, so they will have different

taxable amount and tax payable amount, the more money tax payer can earn, the more tax they

will pay. However, the way to caculate income tax of individual will base on the tax rates and

taxable bands which are fixed by HMRC:

Rate 2011-12 2012-13 2013-14

Starting rate for savings: 10%*

£0 - £2,560 £0-£2,710 £0- £2,790

Basic rate: 20% £0 - £35,000 £0-£34,370 £0-£32,010

Higher rate: 40% £35,001 - £150,000 £34,371-£150,000 £32,011- £150,000

Additional rate: 50% Over £150,000 Over £150,000 N/A

45% from 6 April 2013

Over £150,000 Over £150,000 Over £150,000

Figure 2: Income Tax rates and taxable bands

The 10 per cent starting rate applies to savings income only. If, after deducting your Personal

Allowance from your total income liable to Income Tax, your non-savings income is above this limit

7

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

then the 10 per cent starting rate for savings will not apply. Non-savings income includes income from

employment, profits from self-employment, pensions, income from property and taxable benefits.7

From this figure above, in the year 2011-2012, we can see that if the income of an

individual from £0 to £2,560, they need to pay 10% of their income for taxation and it is

only apply for the savings income. The income from £0 to £35,000 incur the basic rate

of taxation with 20% and from £35,001 to £150,000, individual must pay 40% in their

income for the taxation. The addition rate with 50% will impose in person which earn

over £150,000, and as a rule of HMRC that when we caculate the non-saving income,

we will apply the rate from the basic rate 20%.

Dividend income in relation to the basic rate or higher rate tax bands

Dividend Taxrate applied2011/2012

Dividend Taxrate applied2012/2013

Dividend Taxrate applied2013/2014

Dividend Income received below higher rate income tax threshold (£ 37, 400)

10% 10% 10%

Dividend Income recieved within higher rate income tax threshold (£ 37, 400 - £ 150, 000)

32.5% 32.5% 32.5%

Dividend income above the higher 42.5% 42.5% 37.5

7Source: Taxation Lecture Session 1 – Slide number 17

8

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

rate income tax threshold (£ 150, 000)

Figure 3: Dividend tax rates8

PAYE (Pay As You Earn):

“The Pay as You Earn (PAYE) system is a method of paying income tax and national insurance

contributions. Your employer deducts tax and national insurance contributions from your wages

or occupational pension before paying you your wages or pension.”9.

Using the PAYE system, the money that you will receive is your net profit, before paying for

taxation and other expenses as national insurance contribution and so on.

Capital Gain Tax:

Capital gain is the profits that an investor receive when they sells their asset or shares for a

price that is higher than the purchase price. Capital gains tax is caculated on the gain or profit

when they sell, give away or otherwise dispose of something.

For example: Mr. Alex is an investor, in 2000 he bought some shares in company A with the

price at £5,000, in 2012 he sell those shares with the price at £25,000. Caculating we can see

that he just made a gain around £20,000, so as a rule of HMRC Alex has to pay on his gain

which is £20,000.

The rates for capital gain tax as follows 2011-2012, 2012-2013 and 2013-2014:

8PCG Advice Websites: https://www.pcg.org.uk/advice/dividend-tax-rates

9 Advice Guide Websites, n.d: http://www.adviceguide.org.uk/england/tax_e/tax_how_to_pay_income_tax_e/the_pay_as_you_earn_paye_system.htm

9

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

18% and 28% tax rates for individuals (the tax rate you use depends on the total amount of

your taxable income, so you need to work this out first)

28% for trustees or for personal representatives of someone who has died

10% for gains qualifying for Entrepreneurs' Relief10

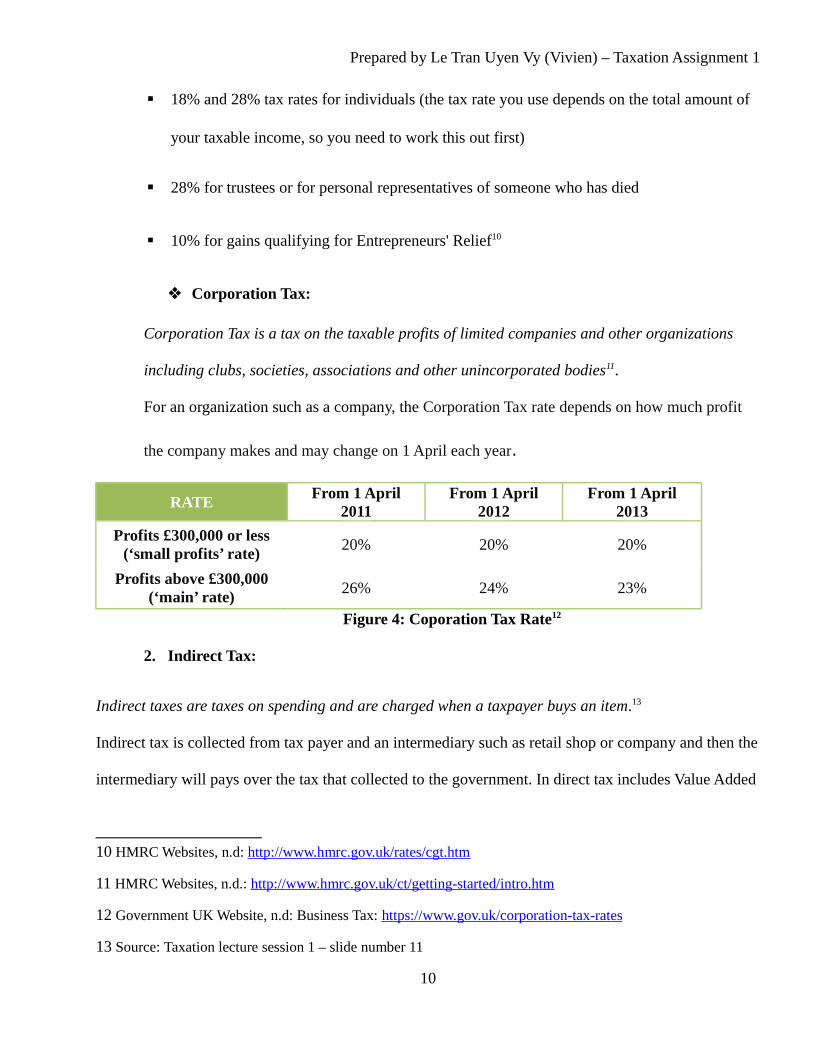

Corporation Tax:

Corporation Tax is a tax on the taxable profits of limited companies and other organizations

including clubs, societies, associations and other unincorporated bodies11.

For an organization such as a company, the Corporation Tax rate depends on how much profit

the company makes and may change on 1 April each year.

RATEFrom 1 April

2011From 1 April

2012From 1 April

2013

Profits £300,000 or less(‘small profits’ rate)

20% 20% 20%

Profits above £300,000(‘main’ rate)

26% 24% 23%

Figure 4: Coporation Tax Rate12

2. Indirect Tax:

Indirect taxes are taxes on spending and are charged when a taxpayer buys an item.13

Indirect tax is collected from tax payer and an intermediary such as retail shop or company and then the

intermediary will pays over the tax that collected to the government. In direct tax includes Value Added

10 HMRC Websites, n.d: http://www.hmrc.gov.uk/rates/cgt.htm

11 HMRC Websites, n.d.: http://www.hmrc.gov.uk/ct/getting-started/intro.htm

12 Government UK Website, n.d: Business Tax: https://www.gov.uk/corporation-tax-rates

13 Source: Taxation lecture session 1 – slide number 11

10

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

Tax (VAT), Customs Duties and The Excise Duties. These taxes also administered by HM Revenue and

Customs.

Value Add Tax (VAT):

VAT is a tax that's charged on most goods and services that VAT-registered businesses provide in

the UK. It's also charged on goods and some services that are imported from countries outside

the European Union (EU), and brought into the UK from other EU countries. There are three

rates of VAT, depending on the goods or services the business provides. The rates are:

Standard - 20 per cent Reduced - 5 per cents Zero - 0 per cent

In addition, in UK there are some goods and services will be reduced rated such as domestic

fuel and power, installing energy-saving materials, sanitary hygiene products, children's car

seats and some goods and services that consumer will not pay VAT for these product such as:

food - but not meals in restaurants or hot takeaways, books and newspapers, children's clothes

and shoes, public transport14.

Customs Duties and Excise Duties:

If you're bringing goods for personal use into the UK, or sending or ordering them from abroad,

including over the internet, you may need to pay UK Customs Duty, Excise Duty and/or import

VAT, and the tax rate that they must to pay depends on the type of goods and where come from.

Custom Duty: Customs Duty is a tax charged on importation of goods produced

outside the European Union (EU). You won't have to pay Customs Duty if you're

14 HMRC Websites, n.d: http://www.hmrc.gov.uk/vat/start/introduction.htm

11

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

travelling from the EU, or buying, ordering or sending goods to the UK from the EU

for your own use.

Excise Duty: Excide duty is a tax on certain goods such as alcohol and tobacco.

When you buy excise goods in the UK the price you pay includes this tax15.

The figure below is a presentation about the data on direct and indirect taxes collected from 2006 to

2010:

Unit: £ billion

YEAR

2006-20072007-2008

2008-2009

2009-2010

DIRECTTAX

Income Tax 143.3 147.3 147.9 134.4

Cappital Gain Tax 3.8 5.3 7.9 2.5

Corporation Tax 44.3 46.4 43.1 33.3

TOTAL 191.4 199 198.0 170.2

INDIRECT TAX

VAT 77.4 80.6 78.4 67.2

Fuel Duties 23.6 24.9 24.6 26.4

Tobacco Duties 8.1 8.1 8.2 8.8

Spirit Duty 2.3 2.4 2.4 2.6

Beer Duties 3.1 3.1 3.1 3.2

Wine Duties 2.4 2.6 2.7 2.9

Cider & Perry Duties 0.2 0.2 0.2 0.3

Stamp Duties 13.4 14.1 8.0 7.5

Betting & Gaming Duties 1.4 1.5 1.5 1.4

Customs duties & Levies 2.3 2.5 2.7 2.6

Air Passenger Duty 1.0 2.0 1.9 1.9

TOTAL 135.2 142 133.7 124.8

15 HMRC Websites, n.d: http://www.hmrc.gov.uk/customs/tax-and-duty.htm

12

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

Figure 5: Collected Tax from 2006 to 201016

From the figure number 5, we can see that is a huge amount of money of gorvernment’s budget is come

from income tax, which is caculated into saving income, non-saving income, and dividend. In the last

year 2009-2010, the total of income tax is around £134.4 billion, it made up around 79% of direct tax.

About indirect tax, apart from VAT, HMRC can collect tax from many duties such as fuel duties,

tobacco duties, spirit duties, beer duties, etc. However, VAT still made up a large of percentation of

indirect tax, in 2009-2010, HMRC collected £67.2 billion from VAT, it made up more than 53% of

indirect tax.

Parties Involved:

As the above outline, there are three parties involved which are HMRC (Administration), Tax Payer

(Individual/Organization) and Tax Practitioner:

16 Source: From the Appendix 1

13

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

1. HMRC:

In the tax environment of UK, HMRC is considered as the the administration. In 2005, HMRC

was established by Act of Parliament as a new department replacing the Inland Revenue and

Customs and Excise. Generally, HMRC have responsibility in collecting tax from people and

organizations that do business in UK, and they also manage the tax system of UK17.

2. Tax Payer:

Tax payer is the one who pays an amount of money as a tax for HMRC. Tax payer could be

individual or organization such as company. For organization such as a company, all the

company does the business in UK has to pay tax for the HMRC, the company will pay tax based

on their profit. For individual, HMRC divide into types of individual which is UK residence,

and non UK residence.

UK Residence: - Who is UK Residence?

People who come from another country, and they are in the UK for 183 days or more in

a tax year, they will be resident in the UK for that tax year (from 6th April of this year to

5th April of the next year), or people who visit to the UK averaging at least 91 days per

tax year.

People who born in UK are UK residence, in case they have UK citizenship, but they

leave UK to work full time abroad, they also have to pay tax as nomally.

- How UK Resident paying Tax to HMRC?

17 HMRC Websites,n.d: https://www.gov.uk/government/organisations/hm-revenue-customs/about

14

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

For the UK residents, they have to pay tax which called income tax based on their

income, those income includes both of the income arising in the UK and income arising

overseas.

For example, there is a man named Tom, and he is a UK residence. He has doing

business in UK and he also has worked in Vinamilk which is company located in

Vietnam, so once a year he has to pay income tax for HMRC in UK based on the the

income he collects in UK and also the income he has from the job in Vinamilk located in

Vietnam.

Non UK Residence:

- Who is non UK Residence?

Excepting for some cases that I mention in the UK residents section, it is non UK

residents, so non UK Residence is a person who present in the UK for less than 183 days

during the tax year or they visit to the UK averaging less than 91 days per tax year non

UK residents.

- How non UK Residence paying Tax to HMRC?

The non UK residentces only have to pay the income tax to HMRN based on their

income which generate in UK.

For example, Van is a business woman; and she is Vietnamese. She has a business trip to

UK in 2 months which is about 60 days so she is non UK residence because her stay is

less than 183 days. In those 2 months, Van earned 1000 pounds from doing business in

UK, and 10 million VND from her business in Vietnam, so she has to pay income tax for

HMRC in UK just bases on 1000 pounds that she collected in UK, she does not have to

15

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

pay tax on 10 million VND from her business in Vietnam because she is non UK

Residence.

3. Tax practitioner:

Tax practitioner is the tax agent, lawyer or accountant who helps the tax payer to file the tax

return. On the behalf of the tax payers, tax practitioner was hired for doing what related to the

taxation of the taxpayer. In working with the HMRC, tax practitioners represent for the tax

payer in dealing the matter. The main role and responsibilities of tax practitioner are give the

advice to tax payer in their tax obligations, collect information of taxpayer and file in the tax

return. They also need to calculate the tax liabilities of tax payer based on their gross income.

1.2 THE ROLE AND RESPONSIBILITY OF TAX PRACTITIONER:

Individuals and companies or organization take responsibility to pay tax for government. However, tax

payers need to understand and have basic knowledge about payment tax and tax practitioner is the one

who will help taxpayers.

Tax practitioner:

16

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

Tax practitioner is an accountant, lawyer or tax agent which helps the tax payer to file the tax return

accordance to HMRC. In paying the tax, it has a lot of information to cover and the tax payer cannot

have enough time or knowledge to do it, so they need a tax practitioner to help them to paying the tax

and claim back the tax if it’s necessary.

The role of tax practitioner:

Taxpayer arrange for their accountants to prepare and submit their tax returns .Tax practitioners who

help taxpayer deal with the HMRC on behalf of client. Besides that, tax practitioners play important

roles to taxpayer because they will make effectiveness on tax and ensure requirement of HMRC.

Moreover, Tax Practitioner likewise play important roles between taxpayer and tax collectors because

of having to explain and advise tax law for taxpayer and submit information tax of taxpayer to tax

collectors as HMRC on their behalf (Course book Taxation, page 146).

- The tax practitioners have to have legal responsibilities to obey with the common-law rules,

meet the qualifications and experience like rules and regulation of HMRC. That means the tax

practitioners have roles to help taxpayer deal with HR Revenue and Customs to report initially

tax payments namely income tax, corporation tax, capital gains tax and so on.

- Tax practitioners are able to effect to the tax reporting process in lots of ways. Practitioners can

reduce tax liabilities for taxpayer by technical knowledge of tax law and regulations. To give

advices for client to perform their obligation in tax, Tax practitioners need to have the

knowledge of tax law. In addition, they are able to propose and improve policies to reach perfect

reporting tax.

- Tax practitioners play important role between HMRC and taxpayers, they like intermediaries.

Because complicated content of law, advise and ‘educate’ taxpayers in tax law matters, and hand

in information to HMRC for their clients.

17

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

- The tax practitioners like tax advisor on business transactions, they are able to help to provide

and explain clients with the clear understandings of risks and opportunities. In addition, the tax

practitioners need to have any the suitable choices to consult for their clients.

The responsibilities of tax practitioner:

Besides the roles bring for customers in taxation, tax practitioners also take responsibilities about

ethical such as:

- Complying with the taxation laws in the conduct of their personal affairs.

- Tax practitioners will advise client to prepare the good tax return by preparing the tax returns

competently and honestly so as to it will be true and exactly. Besides that, Tax practitioners are

able to comply and advise the issue related to the audit law for companies.

- Do not leak out information, which related to client’s issues to third party without client‘s

permission.

- Certainly, the tax practitioner has an obligation to both the client and the system, but that

obligation is to assist the client to comply with the tax laws, paying no more than the law

requires.

- Keeping up-to-date with changes in taxation laws and practice. The tax practitioners play

important because they are intermediaries between taxpayer and HMRC. Therefore, they have

to be responsibility to update to explain for taxpayer and send information for HMRC.

1.3 THE TAX OBLIGATIONS OF TAX PAYER OR THEIR AGENTS AND THE

IMPLICATIONS OF NON-COMPLIANCE:

The tax obligations of tax payer:

18

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

When an individual or organization operates in UK, they have to implement their tax obligation to the

UK’s government. And here is the tax obligation of the tax payers:

Honesty: when file the tax return, the tax payer need to honesty in listing the income. They

must to fill full and right income that they have. It createS the fair between people in UK in pay

the tax. With the right number of income, the HMRC can collect the right taxation of each

others because the tax liabilities of them base on their income. Besides, tax payer should be

truth in communicate with HMRC for paying their tax.

Cooperation: The tax payer need to coordinate closely to the tax agency, specific is the HMRC

Department to give them information if they need to reduce the cost of tax collection.

Submit the documents and pay the tax on time: That means if the HMRC require, tax payer

need to submit the document which related to the taxation to them. Besides, they also should

pay the tax on time. Pay tax on time can help people avoid the penalties from HMRC and the

HMRC department can be easy in collect the tax.

Deadlines for paying Tax18:

31st January:

You must pay any tax you owe by 31 January following the end of the tax year. The payment

deadline is the same for both of paper and online returns and there are very few exceptions.

For example, for the tax year 2011-12 (ending on 5 April 2012) you must pay any tax you owe

by 31st January 2012.

18 HMRC Websites, n.d: http://www.hmrc.gov.uk/sa/deadlines-penalties.htm

19

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

31st July:

This is your deadline for making any further payments on account.

For example on 31st July 2012, you'd make your second payment on account for the tax year

2011-12.

The implications of non-compliance:

Tax payer need to comply with the HMRC regulatory, if they do not comply, they will face up with

some penalties from HMRC.

Penalties of paying tax late:19

If the tax payers do not implement their tax obligation on time, they will pay more for the

penalty after 30 days and the longer they delay. It also increases the money for taxation of them.

So pay the tax on time is necessary to save their money. The table below will show the penalties

of paying late.

Length of delay Penalty you will have to pay

30 days late 5% of the tax you owe at that date

6 months late5% of the tax you owe at that date. This is

as well as the 5% above.

12 months late5% of the tax unpaid at that date. This as

well as the two 5% penalties above

Penalties if you miss the tax return deadline20

19 HMRC Websites, n.d: http://www.hmrc.gov.uk/sa/deadlines-penalties.htm

20 HMRC Websites, n.d: http://www.hmrc.gov.uk/sa/deadlines-penalties.htm

20

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

The taxpayer need to submit the tax return to HMRC on time. If they do not comply, they must

pay more time depending on the day that they are late. The table below will show their paying is

their tax return is late:

Length of delay Penalty you will have to pay

1 day late A penalty of £100. This applies even if you haveno tax to pay or have paid the tax you owe.

3 months late £10 for each following day - up to a 90 day maximum of £900. This is as well as the fixed penalty above.

6 months late £300 or 5% of the tax due, whichever is the higher. This is as well as the penalties above.

12 months late £300 or 5% of the tax due, whichever is the higher.In serious cases you may be asked to pay up to 100% of the tax due instead. In some cases the penalties can be even higher than this.These are as well as the penalties above.

21

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

LO2 – BE ABLE TO CACULATE PERSONAL TAX LIABILITIES FOR UNDIVIDUAL AND

PARTNERSHIPS

2.1 CACULATE RELEVANT INCOME, EXPENSES ANS ALLOWANCES:

As a we know that, currently I’m a tax practitioner of L&T consultancy, and at present my client is Mrs

Julia, so my role and responsibility here is giving and advicing her some information which related to

her tax resposibility. In the previous task, I already have explained all the basic information of UK Tax

Environment such as the UK Tax Framework, parties involved, UK Tax legislation, the tax rate of the

year 2011-2012, type of tax, how to caculate the tax, the penalty, so now my job in this section is

finding down how much Julia’s the relevant income, expenses and allowances for the year 2011-2012.

Julia’s Relevant Income:

Income is an amount of money that a person can earn from their employment or their investment or

both of that. In the UK tax system, the income is devided into three types of income which is non-

saving income, saving income, and dividend income. Non-saving income is came from employment

income, trading income, property income, saving income is all the money that can be earned from the

interest such as interest on loan, bank, or building society accounts, and finally dividend income is the

money come from inverstment on share.

22

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

1. Trading Income

According to scenario, Julia’s trading profits for the final two periods of trading were as follow21:

£

Year ended 30 April 2011 98,200

Two-month period ended 30 June 2011 16,600

Overview Capital Allow22

On 1 May 2010, the tax written down value of the capital allowances main pool (general pool) was

£13,200, based on the figure above that Julia will receive 20% of tax written down value which is

£2,64023. Therefore, the trading profit of Julia in year ended 30 April 2011 is £95,56024.

21 Source: Scenario Page 4, paragraph 5

22 Source: Taxation Lecture Session 6 – Slide Number 19.

23 Caculation: £13,200 x 20% (belong to main pool) = £2,640

24 Trading profit year ended 30 April 2011: £98,200 – £2640 = £95,560

23

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

From 20% the capital allowance which belong to main pool, we have the year balance after the capital

allowance is £10,56025.

However, because on 21 May 2011, Julia pruchased computer equipment for £3,600, and all the items

included in the main pool were sold for £7,700 on 30 June 2011, so the capital allowance of two-month

period ended 30 June 2011 will be reduce at £6,46026, so we have the trading profit of Julia in two-

month period ended 30 June 2011 is £10,14027.

After minusing the capital allowances we have the total trading profit of Julia is 105,70028. In addition,

according to the scenario, Julia has unused overlap profits brought forward of 41,700, this amount of

money will reliefs Julia’s Trading Profit, so trading profit of Julia after reliefing is £64,00029

Suming up Julia’s Trading Profit:

Capital Allowance Caculation:

Written down Asset of C.A main pool £13,200

Receive 20% of tax written down value £2,640

Balance £10,560

Purchase/Addition £3,600

Selling/Disposals £7,700

Capital Allow £6,460

Julia’s Trading Profit Caculation:

Year ended 30 April 2011 £98,200

Capital Allowance (20% of main pool) £2,640

£95,560

Two-month period ended 30 June 2011 £16,600

25 Caculation: £13,200 – £2, 6450 = £10,560

26 Caculation: £10,560 + £3,600 (Computer Addition) – £7,700 (Items Disposal) = £6,460

27 Caculation: £16,600 – £6,460 = £10,140

28 Caculation: £95,560 + £10,140 = £105,700

29 Caculation: £105,700 – £41,700 = £64,000

24

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

Capital Allowance £6,460

£10,140

Total trading profit of Julia £95,560 + £10,140 = £105,700

Unused overlap profits £41,700

Final Trading Income of Julia £64,000

2. Salary Income30:

According to scenario that Julia was paid a Salary of 15,100 per month by Unicorn plc, and she worked

for Unicorn pls as a marketing director from 1 August, 2011. According to HMRC of the tax year

which begin from 6 April and ending 5 April next year, and because the salary is paid on the last day of

each calendar month, so the salary of Julia of the tax year 2011-2012 will be caculated from 1 August,

2011 to 31 March, 2012 which is about 8 months. Therefore, the total salary of Julia in the tax year

2011 – 2012 is £120,80031

3. Property Income32:

According to the scenario, Julia owns 2 properties. The income and the allowable expenditure for

her two properties for the tax year 2011 – 2012 are as follows:

Property 1 Property 2

Income £6,600 £7,200

Allowable expenditure £9,700 £2,100

“Expenditure on buying, creating or improving a business asset that you keep to earn the profits of

your business is capital expenditure”33. In other words, allowable expenditure is an amount of money

30 Source: Scenario Page 4, paragraph 8

31 Caculation: £15,100 (each month) x 8 months = £120,800

32 SourceL Scenario Page 5, paragraph 5

33 HMRC Websites, n.d: Capital expenditure: http://www.hmrc.gov.uk/incometax/relief-self-emp.htm

25

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

which is used to maintain your properties, without the allowable expenditure your property maybe

cannot run the business to earn profit, so the government allows the property owner some money to

maintain the property and it called allowable expenditure. The owner of property will pay tax for the

gorvernment after minusing the allowablw expeenditure.

The Allowable expenses may include34:

rents, rates, insurance, ground rents etc

property repairs and maintenance

renewals - although you cannot claim these and capital allowances or the 10% wear and tear

allowance

interest and other finance charges

legal, management and other professional fees

costs of services provided, including wages

other property expenses

For the property 1, we see that the amount of money from income is lower than the allowable

expenditure by £3,10035, which is also considered as loss for Julia in the property 1, according to

HMRC that any rental business loss is automatically carried forward and set off against rental business

profits of the following year36, so the loss at £3,100 of the property 1 will be carried forward to the next

year to caculate the income of this property.

34 HMRC Websites, n.d: https://online.hmrc.gov.uk/information/help?helpcategory=selfAssessmentFiling1112&affinitygroup=individual&helpid=PropertyExpenses

35 £9,700 – £6,600 = £3,100

36 PIM4210 - Losses: set against future profits: http://www.hmrc.gov.uk/manuals/pimmanual/pim4210.htm

26

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

For the property 2, the income was £7,200 and the allowable expenditure was £2,100 so the income of

Julia from this property is £5,10037

In general, from the properties that Julia owns, in the tax year 2011 – 2012, she just has income from

the second property which is £5,100.

4. Interest from buliding Society38:

During the tax year 2011 – 2012 Julia receive building society interest of £8,96039, but this amount of

money is the net income40 so tralating to gross income by 20%, the gross income of Julia from building

society is £11,20041

5. Dividend42:

According to the scenario, in 2011-2012 Julia also received an amount of money from dividend at

£6,480, but this amount of money is also after tax so tranlating to before tax by 10%, the amount of

money Julia can received from her dividend is £7,20043

6. On 2 Octorber 2011, Julia received a premium bond prize of £10044

The Total relevant income of Julia is £208,40045

Julia’s Allowance:

37 Caculation: £7,200 – £2,100 = £5,100

38 Source: Source: Scenario Page 5, “Other information” Section

39 Source: Scenario Page 5, “Other information” Section

40 Source: Taxation Lecture – Session 1: Income Tax at Source Slide 16

41 Caculation: £8,960 x 100/80 = £11,200

42 Source: Scenario Page 5, “Other information” Section

43 Caculation: £6,480 x 100/90 = £7,200

44 Souces: Scenario page number 5

45 Caculation: 64,000 + 120,800 + 5,100 + 11,200 + 7,200 + 100 = 208,400

27

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

Nearly everyone who lives in the UK is entitled to an Income Tax Personal Allowance. This is the

amount of income you can receive each year without having to pay tax on it. Depending on your

circumstances, you may also be able to claim certain other allowances.46

Personal Allowance 2011-2012:

Allowance 2011 to 2012 tax year

Personal Allowance £7,475

Age 65 to 74 - Personal Allowance £9,940

Age 75 and over - Personal Allowance £10,090

Figure: Personal Allowance 2011-201247

If you’re over 65- If your income(less deductions) is between £25,400 and £100,000 in the

2012 to 2013 tax year, your Personal Allowance goes down by £1 for every £2 of income above

£25,400, to a minimum Personal Allowance of £8,105.

If your income is over £100,000- For every £2 your income is above £100,000, your Personal

Allowance goes down by £1. If your income is high enough, this can reduce your Personal

Allowance to zero.

As the income of Julia which I already mention above, the figure of income is £208,400. From the

infomation of “If your income is over £100,000” section above that if your income is over £100,000,

your Personal Allowance will be reduced by half of the amount - £1 for every £2. Caculating to 2012,

Julia is 42 years old so her personal allowance is £7,475, and her income is more than £100,000 so her

Personal Allowance is reduced by half of the amount - £1 for every £2, we have the caculation:

46 HMRC Websites,n.d.: Personal Allowance: http://www.hmrc.gov.uk/incometax/personal-allow.htm

47 Source: Taxation Lecture – Session 2 – Slide number 22 - Allowance for personal

28

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

£7,475 – (£208,400 – £100,000)/2 = £ 7,475 – (£108,400/2) = - £46,725.

As the caculation above that the personal allowance of Julia is negative, it means the Personal

Allowance of Julia is zero.

Julia’s Expenses:

Expenses are the costs that you pay out in the course of earning business profits and which you can

claim for. You can't claim for non-business or personal items. Buying or improving capital items, such

as machinery, which last for several years, is not a business expense for tax purposes but you may still

be able to claim for them as long as they are related to your business.48

As the scenario that there is no mention about the expenses that Julia had to pay out so we can consider

that the expense of Julia is zero.

Summary, we have the table of income, allowance and expenses of Julia below:

Income Expenses Allowance

Trading Income £64,000 N/A N/ASalary Income £120,800 N/A N/A

Property Income £5,100 N/A N/ABuilding Society Interest £11,200 N/A N/A

Dividend £7,200 N/A N/APremium Bond Prize £100 N/A N/A

Expenses N/A 0 N/AAllowance N/A N/A 0

TOTAL £208,400 0 0

2.2 CACULATE TAXABLE AMOUNTS AND TAX PAYABLE FOR EMPLOYED

INDIVIDUALS, AND ADVICSE ON PAYMENT DATES:

1. Premium Bond Prize

48 HMRC Websites, n.d: What are 'allowable expenses'?: http://www.hmrc.gov.uk/incometax/relief-self-emp.htm

29

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

As the information from the scenario that on 2 Octorber 2011, Julia received a premium bond prize of

£100, and according to HMRC that a premium bond prize is not taken into accounts for inheritance tax

purposes49, so Julia does not have to pay any tax for this £100

2. Tax Benefit:

Removal Expenses:

As the scenario that during August 2011, Unicorn plc paid £11,600 towards Julia’s removal expenses,

and according to HmRC that there is £8,000 of removal expenses and benefits will be exempted50 so for

the removal expenses Julia just have to pay tax on £3,60051.

Beneficial Loan:

From 1 September, 2011 to 5 April, 2012, which is around 7 months Unicorn plc provided Julia a loan

with free interest of £33,000. It means Julia borrows £33,000 from the company and she does not have

to pay any interest. However, at the same with that period time if Julia borrows that amount of money

outside, it would charge Julia 4% of interest52, so because Julia borrowed that from the company so she

can save 4% of interest each month, so after 7 months, the amount of money that she can save was

£77053

Free Meals:

49 HMRC Websites, n.d: IHTM10082 - Premium Bonds: http://www.hmrc.gov.uk/manuals/ihtmanual/ihtm10082.htm

50 HMRC Websites, n.d: EIM03104 - Removal or transfer costs: http://www.hmrc.gov.uk/manuals/eimanual/EIM03104.htm

51 Caculation: £11,600 – £8,000 = £3,600

52 HMRC Websites, n.d: EIM26104 - The benefits code: http://www.hmrc.gov.uk/manuals/eimanual/eim26104.htm

53 Caculation: £33,000 x 4% x 7/12 = £770

30

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

During the period from 1 August 2011 to 5 April 2012, Julia was provided free meal from Unicorn plc’s

canteen, and the total cost of these meals was £1,34054. It’s a benefit of the company for Julia, and she

does not have to pay any tax for this benefit, because according to HMRC that there is no tax charge on

the provision of meals for directors or employees if the meal is provided in a canteen55

Vehicle Benefit:

From the scenario that during the period from 1 Octorber 2011 to the end of tax year 2011-2012,

Unicorn plc provided Julia a diesel-powered motocar which has a list price of £14,400 with an official

CO2 emission rate of 149 grams per kilimeter. The taxable benefit of Julia about vehicle benefit will be

caculated based on the list price of her vehicle and the rate at which the car emits carbon dioxide.

From Mrsalvage Website56, we have the table below:

CO2 emissions(g/km)

Appropriate percentage

Petrol % Diesel %

Up to 75 5 8

76-120 10 13

121-129 15 18

130-134 16 19

135-139 17 20

140-144 18 21

145-149 19 22

150-154 20 23

155-159 21 24

160-164 22 25

165-169 23 26

170-174 24 27

54 Source: Scenario page 5, the second paragraph

55 HMRC Websites, n.d: EIM21671 - Particular benefits: http://www.hmrc.gov.uk/manuals/eimanual/eim21671.htm

56 Mrsalvage Website: Vehicle Benefits: http://www.mrsalvage.co.uk/Tax-2011/vehicle.html

31

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

175-179 25 28

180-184 26 29

185-189 27 30

190-194 28 31

195-199 29 32

200-204 30 33

205-209 31 34

210-214 32 35

215-219 33 35

220-224 34 35

225 and above 35 35

Based on the table and the information below, the appropriate percentage of Julia’s vehicle will be 22%

because Julia’s vehicle is a diesel-powered motocar. In addition, Julia used this motocar from 1

Octorber 2011 to 5 April 2012 which is about 6 months, so after caculating the vehicle benefit of Julia

is £1,58457.

2. Taxable Amount:

As the information I have mentioned above that the relevant income of Julia includes trading income,

salary income, property income, interest from building society, dividend and premium bond prize

which is about £208,400. However, as I have explained above that Julia does not have to pay any tax

for her premium bond prize, so in the taxable income I will minus £100 from premium bond prize, so

after minusing the prize, Julia’s income is £208,30058.

57 Caculation: £14,400 x 22% x 6/12 = £1,584

58 Caculation: £208,400 – £100 = £208,300

32

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

In addition, I have caculated the taxable benefit of Julia which includes removal exepenses, benefical

loan, and vehicle benefit. Therefore the total taxable benefit of Julia will be £5,95459, and all the taxable

benefit will belong with the non-saving income of Julia.

Summary, we have the table of Julia’s tax amount below:

Non-SavingIncome

SavingIncome

DividendIncome

Total

Trading Income £64,000Salary £120,800

Property Income £5,100

Interest from Building Society

£11,200

Dividend £7,200

Total £208,300

Taxable Benefit

Removal Expenses £3,600

Benefit loan £770

Car benefit £1,584

Total Taxable Benefit £5,954

Taxable income £195,854 £11,200 £7,200 £214,254

3. Tax Liability:

According to the scenario that during the tax year 2011 – 2012, Julia made gift aid donation totalling

£4,400 which is considered as net to national charities, so after tranlating to gross by 20%60, the gross

of girt aid donation will be £5,50061. According to HMRC that Gift Aid is a way for charities to increase

the value of monetary gifts from UK taxpayers by claiming back the basic rate tax paid by the donor on

59 Caculation: £3,600 + £770 + £1,584 = £5,954

60 HMRC Websites, n.d: Tax relief for charities: http://www.hmrc.gov.uk/charities/gift_aid/basics.htm

61 Caculation: £4,400 x 100/80 = £5,500

33

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

the donation62, the Gift Aid Donation will not deducted in the tax structure, it is only used to expand tax

rate band:

Rate 2011-12

Starting rate for savings: 10%* £0 - £2,560

Basic rate: 20% £0 - £40,500

Higher rate: 40% £40,501 - £155,500

Additional rate: 50% Over £155,500

Additional rate: 45% from 6 April 2013 N/A

Figure: New Tax Rate by the Gift Aid Donation of Julia

Based on the new tax rate above, I will calculate the tax liability for Julia:

Non-Saving Income:

In order to caculating taxable of non-saving income, I have to minus personal allowance from non-

saving income. However, the personal allowance of Julia is zero63, so the taxable of non-saving income

is £195,584. Therefore, we have the tax liability of non-saving income as follows:

NSI Rate Tax Liability

£40,500 x 20% = £8,100

£114,999 x 40% = £45999, 6

£40,355 x 50% = £20177, 5

Total NSI £195,854

Total Tax Liability of NSI £74277, 1

Saving Income:

62 HMRC Websites, n.d: Gift Aid: the basics: http://www.hmrc.gov.uk/charities/gift_aid/basics.htm

63 Source: Task 2.1 – page 27

34

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

Because the non-saving income of Julia is over 10% limit which is the starting rate, so saving income

of Julia will be caculated as non-saving income. Saving income of Julia is £11,200 is belong with the

basic rate which is 20%, so the tax liability of saving income is £2,24064.

Dividend Income:

According to tax fix website65 that the amount of money that Julia must pay as tax for her dividends

depends on the total taxable income. For the tax year 2011 -2012, if the total taxable income is below to

£150,000 then the tax rate for dividend will be 32.5%. If the total taxable income is more than £150,000

then the tax rate for dividend will be 42.5%. In addition, HMRC also applies 10% tax rate for dividend

if the total income is belong with the basic rate. For Julia, her total taxable income is more than

£150,000, so HMRC will apply 42.5% tax rate for her dividend, after caclating her dividend tax

liability is £3,06066.

Tax Liability

Tax Liability of Julia from Non-saving Income £74277, 1

Tax Liability of Julia from Saving Income £2,240

Tax Liability of Julia from Dividend Income £3,060

Total Tax Liability £79577, 1

4. Tax Payable:

64 Caculation: £11,200 x 20% = £2,240

65 Tax Fix Website: Paying Tax On UK Dividends: http://taxfix.co.uk/articles/paying-tax-on-uk-dividends/

66 Caculation: £7,200 x 42.5% = £3,060

35

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

Tax payable is an amount of money that exactly Julia has to pay for HMRC, the total income tax

liability minuses tax deducted at source will be the tax payable of Julia.

Tax deducted at source:

From the income of Julia, the tax deducted at source will include:

- PAYE from non-saving income is £43,77767

- 20% of interest from building society (saving income) which is £2,24068

According to HMRC that interest on most savings include building society interest has 20 % tax deducted

before Julia receives it69

- 10% from Dividend (from dividend income) which is about £72070

According to HMRC that the dividend Julia is paid represents 90% of 'dividend income'. The

remaining 10% of the dividend income is made up of the tax credit. Put another way, the tax credit

represents 10% of the dividend income71.

Total Tax deduction at source is: £46,73772

Tax Payable of Julia is about £32,840

Summary Table:

Non Saving Income Tax Liability £74277, 1Saving Income Tax Liability £2,240Dividend Income Tax Liability £3,060Total Tax Liability £79577, 1PAYE from non-saving income £43,77720% of interest from building £2,240

67 Source: Scenario page 4, paragraph 8

68 Caculation: £11,200 x 20% = £2,240

69 HMRC Websites, n.d: Income Tax deducted at source from savings income: http://www.hmrc.gov.uk/incometax/ways-to-pay.htm

70 Caculation: £7,200 x 10% = £720

71 HMRC Websites, n.d: Tax on UK dividends: http://www.hmrc.gov.uk/taxon/uk.htm

72 Caculation: £43,777 + £2,420 + £720 = £46,737

36

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

society10% from Dividend £720Total Tax deducted at source £46,737Tax Payable of Julia £32,840

5. Payment dates 73 :

In order to avoid the penalty from HRMC, Julia needs to know exactly the date to submit tax return and

the due day Julia pay tax.

There are two ways for Julia to submit tax return:

- 31 January for online returns

If Julia sends the tax return online to HMRC, the deadline will be 31 January or in other words that

if Julia sends the tax return online, then HMRC must receive her online tax return before the

midnight on 31 January.

- 31 October for paper returns

If Julia sends the tax return offline to HMRC by paper, the the deadline will be 31 Octorber. Or in

another words that HMRC must receive tax return paper of Julia before midnight on 31 October.

Deadlines for paying Julia tax that is 31 January, Julia must pay any Tax she owes by 31 January

following the tax year. The payment deadline is the same for both paper and online returns and there

are very few exceptions

73 Gov Website: Self Assessment Dealine: https://www.gov.uk/self-assessment-tax-return-deadlines

37

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

Julia needs to pay tax before the deadline for HMRC, if she pays tax late, she will face up with some

penalties from HMRC. The specific information about the penalty of paying tax late is presented

above74

2.3 COMPLETE RELEVENT DOCUMENTATION AND TAX RETURN:

After calculating the tax liability for Julia, as a tax practitioner of L&T Company, I also have

responsibility in preparing and filling the tax return form and the relevent document for my client and

submit it to the HMRC.

According to scenario that Julia Gillard is a UK resident, she was born on 16th December 1970, she live

at B15 2TT Edgbaston, west Midlands Birminglam, and her tax code (NINO) is DA671892Z75. All

those information will be used to fill in some document to submit to HMRC.

There are a few forms that I need to prepare for her payment tax:

1. Form 64-8 - Authorizing tax practitioner76

This form is an important form, which is about the deal between tax payer and tax practitioner. The

authorises use it to communicate with an accountant, tax agent or adviser acting on your behalf. The

form covers authorisation for individual tax affairs (partnerships, trusts, tax credits and individuals

under PAYE) and business taxes (VAT, PAYE for employers and Corporation Tax).

74 Question 1.3 – Page 19

75 Source: Scenario Page 4 – the third paragraph

76 HMRC Websites, n.d : 68-4: http://search2.hmrc.gov.uk/kb5/hmrc/forms/view.page?record=cZuAgB_KEpk&formid=14

38

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

2. Form SA103S77

This is the full version form of the SA103; this form is used for self-employment, business detail, VAT,

business income, allowable and disallowable expenses, capital allowances for vehicles and equipment,

calculating taxable profit or loss, CIS deductions, balance sheet, Class 4 National Insurance

contributions.

3. Form SA102 78

This is an employment form, if you are employed, whether it is part-time, full-time or casual employment, you

will usually have to complete Form SA102 Employment pages of the tax returns

4. SA105 UK Property Form79

Using the SA105 supplementary pages when filing a tax return if you are an individual or a rental

business declaring income generated from land and property in the UK, or chargeable premiums arising

from leases of land in the UK, or furnished holiday lettings in the UK, or a reverse premium.

5. Form P6080:

If you are an employer, you must provide a form P60 to each employee at the end of the tax year and

for whom you have completed P11. The P60 confirms an employee's final tax code and shows their

77 HMRC Websites, n.d : SA103S: http://www.theaccountancy.co.uk/articles/how-to-use-form-sa102-907.html

78HMRC Website: SA102: http://search2.hmrc.gov.uk/kb5/hmrc/forms/view.page?record=8MlslNCX1mI&formId=7287

79 .HMRC Website: SA105 http://search2.hmrc.gov.uk/kb5/hmrc/forms/view.page?record=OSWvtKIMh2c&formid=3187

80 HMRC Websites, n.d: P60 https://www.gov.uk/paye-forms-p45-p60-p11d/p60

39

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

total pension and/or earnings for the year, as well as the year's total tax deductions and National

Insurance contributions. If you're an employee, keep form P60 as a record for self-assessment purposes

6. Form SA100:

SA100 is the main tax return for individuals. People use this form to file your tax return for income and

capital gains, student loan repayments, interest, pensions, annuities, charitable giving and to claim tax

reliefs and allowances.

7. Form P11D:

Your employer uses a P11D to tell HMRC about the value of any benefits in kind they've given you

during the tax year. Your employer will only declare them if you've earned at least £8,500 in the year,

including the value of the benefits. They will work out how much each benefit is worth, record it on the

form and send it to HMRC81

8. Form P8782:

This form is used to claim back work related expenses. The form is only used for employed tax payers

and not for the self employed.

9. Guidance HS25283:

This is a guidance which could help you fill in the capital allowances boxes in the Self-employment,

UK property, Employment and Foreign pages of your personal tax return. It also applies to the

Partnership Tax Return, the Trust and Estate Tax Return and the Tax Return for a non-resident

Company liable to Income Tax.

81 HMRC Website: P11D: http://www.hmrc.gov.uk/payerti/exb/forms.htm

82 UK intheblacksolutions Website: http://www.intheblacksolutions.co.uk/getting-tax-relief-expenses/

83 HMRC Website: HS252: http://search2.hmrc.gov.uk/kb5/hmrc/forms/view.page?record=yDSaRxbn_CQ&formId=3871

40

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

10. Form R8584:

Use form R85 to tell your bank or building society that you qualify for tax free interest on your account

CONCLUSION

As a tax practitioner of L&T Company, my role and responsibility is helping my client who named

Julia in carrying out her tax responsibility with UK government. In this presentation, I already have

explained about UK tax environment, the role and responsibility of tax practitioner and the obligations

of tax payer as well as the implications of non-compliance. Besides, I have calculated the relevant

income, allowance and expenses, taxable amount and tax payable of Julia, and lastly is preparing and

filling the tax returns form and relevant documents which related in the taxation obligations.

84 HMRC Website: R85: http://search2.hmrc.gov.uk/kb5/hmrc/forms/view.page?record=nCRoVNw8-lk&formid=835

41

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

References:

Advice Guide, n.d. PAYE System. [Online]

Available at:

http://www.adviceguide.org.uk/england/tax_e/tax_how_to_pay_income_tax_e/the_pay_as_you_earn_p

aye_system.htm

[Accessed 20th August 2014].

Anon., n.d. EIM26104 - The benefits code. [Online]

Available at: www.hmrc.gov.uk/manuals/eimanual/eim26104.htm

[Accessed 20th August 2014].

HMRC, n.d. About HMRC. [Online]

Available at: https://www.gov.uk/government/organisations/hm-revenue-customs/about

[Accessed 20th August 2014].

HMRC, n.d. Capital Gain Tax. [Online]

Available at: http://www.hmrc.gov.uk/rates/cgt.htm

[Accessed 20th August 2014].

42

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

HMRC, n.d. Corporation Tax Rate. [Online]

Available at: : https://www.gov.uk/corporation-tax-rates

[Accessed 20th August 2014].

HMRC, n.d. Direct Tax. [Online]

Available at: http://www.hmrc.gov.uk/complaints-appeals/how-to-appeal/direct-tax.htm

[Accessed 20th August 2014].

HMRC, n.d. Dividend Tax Rate. [Online]

Available at: : https://www.pcg.org.uk/advice/dividend-tax-rates

[Accessed 20th August 2014].

HMRC, n.d. EIM03104 - Removal or transfer costs. [Online]

Available at: www.hmrc.gov.uk/manuals/eimanual/EIM03104.htm

[Accessed 20th August 2014].

HMRC, n.d. EIM03104 - Removal or transfer costs. [Online]

Available at: www.hmrc.gov.uk/manuals/eimanual/EIM03104.htm

[Accessed 20th August 2014].

HMRC, n.d. EIM21671 - Particular benefits. [Online]

Available at: www.hmrc.gov.uk/manuals/eimanual/eim21671.htm

[Accessed 20th August 2014].

HMRC, n.d. EIM26104 - The benefits code. [Online]

Available at: www.hmrc.gov.uk/manuals/eimanual/eim26104.htm

[Accessed 20th August 2014].

HMRC, n.d. Form 64-8. [Online]

Available at: http://search2.hmrc.gov.uk/kb5/hmrc/forms/view.page?

record=cZuAgB_KEpk&formid=14

[Accessed 20 August 2014].

HMRC, n.d. Gift Aid: the basics. [Online]

Available at: www.hmrc.gov.uk/charities/gift_aid/basics.htm

[Accessed 20th August 2014].

HMRC, n.d. IHTM10082 - Premium Bonds. [Online]

Available at: www.hmrc.gov.uk/manuals/ihtmanual/ihtm10082.htm

[Accessed 20th August 2014].

43

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

HMRC, n.d. Income Tax - The Basic. [Online]

Available at: http://www.hmrc.gov.uk/incometax/basics.htm

[Accessed 20th August 2014].

HMRC, n.d. Introduce Corporation Tax. [Online]

Available at: http://www.hmrc.gov.uk/ct/getting-started/intro.htm

[Accessed 20th August 2014].

HMRC, n.d. Personal Allowance. [Online]

Available at: http://www.hmrc.gov.uk/incometax/personal-allow.htm

[Accessed 20th August 2014].

HMRC, n.d. PIM4210 - Losses: set against future profits. [Online]

Available at: www.hmrc.gov.uk/manuals/pimmanual/pim4210.htm

[Accessed 20th August 2014].

HMRC, n.d. Property Expenses. [Online]

Available at: https://online.hmrc.gov.uk/information/help?

helpcategory=selfAssessmentFiling1112&affinitygroup=individual&helpid=PropertyExpenses

[Accessed 20th August 2014].

HMRC, n.d. Self Assessment Deadline. [Online]

Available at: http://www.hmrc.gov.uk/sa/deadlines-penalties.htm

[Accessed 20th August 2014].

HMRC, n.d. Tax Allowance. [Online]

Available at: http://www.hmrc.gov.uk/incometax/relief-self-emp.htm

[Accessed 20th August 2014].

HMRC, n.d. Tax Allowance. [Online]

Available at: http://www.hmrc.gov.uk/incometax/relief-self-emp.htm

[Accessed 20th August 2014].

HMRC, n.d. Ways you pay Income Tax. [Online]

Available at: www.hmrc.gov.uk/incometax/ways-to-pay.htm

mrsalvage, n.d. Vehicle Benefit. [Online]

Available at: http://www.mrsalvage.co.uk/Tax-2011/vehicle.html

[Accessed 20th August 2014].

44

Prepared by Le Tran Uyen Vy (Vivien) – Taxation Assignment 1

Taxfix22, n.d. Paying Tax On UK Dividends. [Online]

Available at: taxfix.co.uk/articles/paying-tax-on-uk-dividends/

[Accessed 20th August 2014].

45