ubs roadshow - mpm groupmpmgroup.co.id/.../06/2014.05.08-mpmx-ubs_presentation_.pdfubs roadshow 15...

TRANSCRIPT

UBS Roadshow 15 -16 May 2014

www.mpmgroup.co.id

PT Mitra Pinasthika Mustika Tbk

Mission

To provide high quality and friendly transportation products and services that make our customers happy

MPM CREDO

Vision

Become a friendly household name through resourceful and passionate people led by respectable and humble leaders

MPM Core Values

1. Passion for Excellence

2. Customer Focus

3. Continuous Improvement

4. Respect & Humble

5. Gratefulness

6. Integrity

7. Adaptability

8. Teamwork

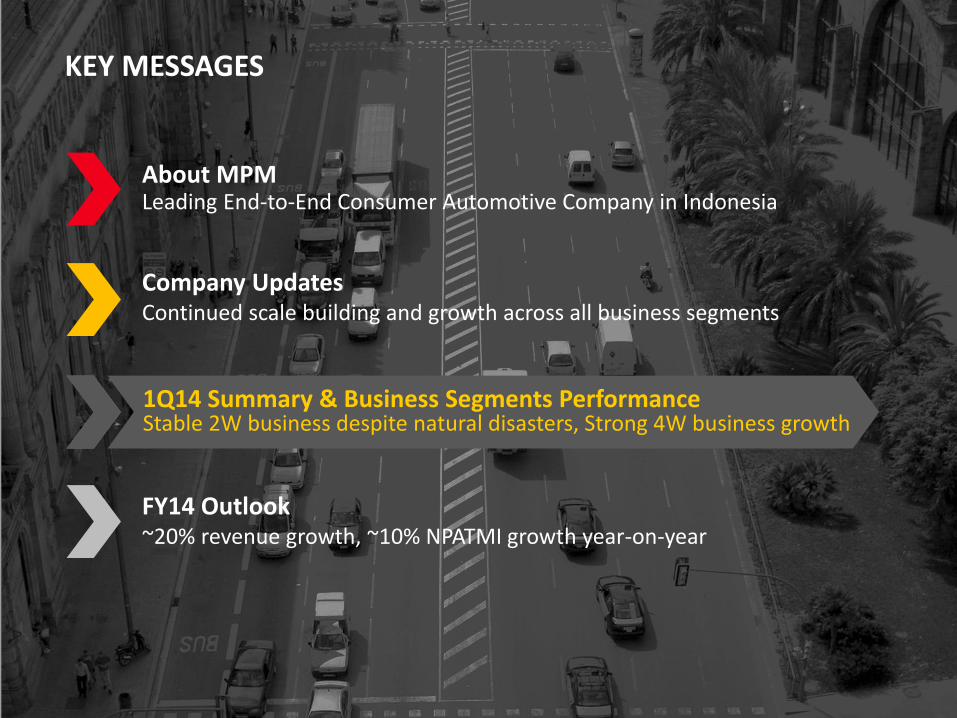

KEY MESSAGES

3

About MPM Leading End-to-End Consumer Automotive Company in Indonesia

Company Updates Continued scale building and growth across all business segments

1Q14 Summary & Business Segments Performance Stable 2W business despite natural disasters, Strong 4W business growth

FY14 Outlook ~20% revenue growth, ~10% NPATMI growth year-on-year

26 YEAR SUCCESSFUL LEGACY AND EXPERTISE IN AUTOMOTIVE...

4

1987

Founded by William Soeryadjaya as 2W

distribution business

1988

FKT was established

1992

MPMMotor 1st retail outlet was

opened

Establishment – Pre 2012

1994

Acquired initial shareholding in SAF, originally established

in 1982

2010 - 2011

Mulia was established; distribution business was transferred from

MPM to Mulia

Jan ‘12

Acquired MPMRent and MPMFinance

May ‘12

MPMInsurance was established

Dec ‘12

JACCS acquired significant

minority shares in SAF + options

May ‘13

Listed in Indonesian Stock Exchange, Ticker: MPMX

Aug ‘13

MPMAuto was established, signed Dealer and Service

Agreement with Nissan Motor Indonesia

2012 - Present

Apr ‘14

Signed merger deed of

MPMFinance and SAF

5

...CREATING AN END-TO-END NATIONWIDE ECOSYSTEM SERVING VAST CONSUMERS IN AUTOMOTIVE SECTOR...

2,4M+ active 2W customers,

~500 new 4W customers since

inception

3200+ Federal Oil Centers, 10,000+ 3rd

party retailers, 10M+ 2W customers

1,400+ corporate clients

220K+ finance & lease customers, 33K+ insurance

clients

DISTRIBUTION & RETAIL AUTO CONSUMER PARTS AUTO SERVICES FINANCIAL SERVICES

2W Honda distribution in E. Java + E. Nusa

Tenggara with 288 dealer relationships

2W Honda retail dealers with 40 outlets

nationwide

2W engine lubricant brand principal with

13,000+ outlets nationwide

4W engine lubricants (currently in bulk)

Independent 4W rental/lease company

with 34 outlets nationwide

Independent 4W financing business with 162 outlets nationwide

Independent 2W financing business with 44 outlets nationwide

Non-life insurance including 2W, 4W, cargo,

& property with 10 offices nationwide

N/A

4W Nissan & Datsun dealership, opened 1st

outlet in Mar ‘14

Data as of 1Q14

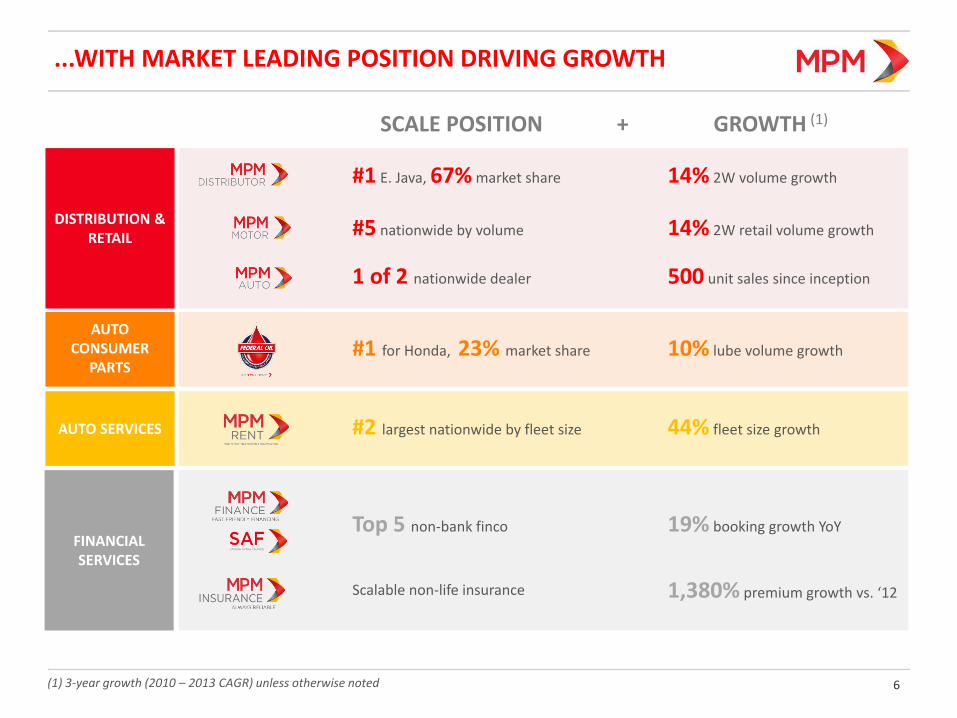

...WITH MARKET LEADING POSITION DRIVING GROWTH

6

14% 2W volume growth

GROWTH (1) SCALE POSITION +

#1 E. Java, 67% market share

14% 2W retail volume growth #5 nationwide by volume

500 unit sales since inception 1 of 2 nationwide dealer

10% lube volume growth #1 for Honda, 23% market share

44% fleet size growth #2 largest nationwide by fleet size

19% booking growth YoY Top 5 non-bank finco

1,380% premium growth vs. ‘12 Scalable non-life insurance

DISTRIBUTION & RETAIL

AUTO CONSUMER

PARTS

AUTO SERVICES

FINANCIAL SERVICES

(1) 3-year growth (2010 – 2013 CAGR) unless otherwise noted

7

15%

10%

32%

43%

Revenues FY13

IDR 13.9T

BALANCED SEGMENT PROFIT CONTRIBUTION IN THE ECOSYSTEM

Revenues 1Q14

IDR 3.6T

NPATMI FY13

IDR 526B NPATMI 1Q14

IDR 152B

Distribution & Retail Auto Consumer Parts Auto Services Financial Services

7% 7%

10%

76%

+29% YoY

+32% YoY

20%

9%

28%

43% +41% YoY

8% 7%

11%

74%

+13% YoY

8

STRONG GOVERNANCE AND MANAGEMENT IN PLACE WITH ACTIVE MAJOR SHAREHOLDERS

BOARD OF COMMISSIONERS BOARD OF DIRECTORS

Shareholder Composition

BoC brings strong mix of operational, strategy, M&A, and governance expertise

BoD members bring over 79 years of combined professional experience

47.2%

15.3%

37.5%

PT Saratoga Investama Sedaya Tbk and Affiliates

Morninglight Investments S.a.r.l

Public & Others

KEY MESSAGES

About MPM Leading End-to-End Consumer Automotive Company in Indonesia

Company Updates Continued scale building and growth across all business segments

1Q14 Summary & Business Segments Performance Stable 2W business despite natural disasters, Strong 4W business growth

FY14 Outlook ~20% revenue growth, ~10% NPATMI growth year-on-year

Company Updates Continued scale building and growth across all business segments

9

Company Updates Continued scale building and growth across all business segments

4Q13 – 1Q14 KEY EVENTS: BUILDING FOUNDATION FOR FUTURE GROWTH

10

2 Feb ‘14 26 Nov ‘13 Oct ’13 – Mar ‘14

1st MPM Dealership for Nissan opened in Enggano, JKT

MPMRent driving school opened in Bogor, W. Java

MPMFinance and SAF merger announced

FKT received Top Brand Award for 2W lube category

MPMX added into MSCI Small Cap Indices

HR talent development and GCG continuous improvements, CPM

finalized Mar ‘14

28 Mar ‘14 24 Mar ‘14 17 Mar ‘14

More details to be discussed in subsequent slides

1 2

3

Start of Sales (SOS)

11

MPMAUTO: THE FIRST OF ITS KIND BUSINESS MODEL IN BUILDING NISSAN-DATSUN DEALERSHIPS

Nissan Tj. Priok Opened Mar ‘14

Alam Sutera Coming soon

Sep ‘14

Local Partnership Scheme • Increase brand presence • Reduce CAPEX • 100% MPMAuto management

control • Fast pace expansion

Finco Partnership Scheme • Max 4 other fincos • Pre-approved customer names • 1-day loan disbursement post

document completion

Product Differentiation • Body Shop • Spare part whosaler center • Nissan U-Cars • MPMA customer loyalty card • Virtual community, website &

social media

5 mio

10 mio

70 mio

20 mio

Population

FINANCE COMPANY NETWORK CUSTOMER

BCA Finance & KKB 1,062 3,000,000

ADIRA Finance 669 1,600,000

BFI Finance 185 500,000

OTO Multiartha Finance 177 200,000

MPM Finance 62 30,000

Finance Company Alliance

1

12

Loan Portfolio, IDR B

95.9%

MPMF AND SAF MERGER WILL CREATE LEADING INDEPENDENT AUTOMOTIVE FINANCING COMPANY IN INDONESIA

FY14E

4,209

29.7%

4.2%

48.6%

17.4%

1Q14

3,435

28.3%

3.6%

48.3%

19.9%

FY13

3,278

28.2%

3.5%

47.5%

20.8%

Finance lease

Used 2W financing

Used car financing

New car financing

FY14E

1,836

90.0%

9.0% 1.0%

1Q14

1,369

90.0%

9.0% 1.0%

FY13

1,279

90.0%

9.0%

1.0%

New 2W financing

Used 2W financing

Electronic goods

FY14E

6,045

1Q14

20.7%

5.7%

27.3%

33.9%

12.1% 4,804

0.3% 20.2%

5.1%

25.6%

34.5%

14.2%

FY13

4,557

0.3% 20.3%

5.0%

25.3%

34.2%

15.0%

Electronic goods

Used 2W financing

Finance lease Used car financing

New 2W financing

New car financing

• Focus on new and used car purchases as well as used car and motorcycle refinancing

• Strong relationship with funding providers as well as numerous retail car dealers and showrooms

• Focus on new Honda motorcycle and used motorcycle financing

• Strong relationship with dealers especially in East Java

• Strengthen foothold in financing business

• Become more efficient and competitive through a stronger capital base and network expansion in Indonesia

• Lead to positive business synergy with other MPMX business entities

+

+28% YoY +44% YoY

0.3%

+33% YoY

+

2

13

MPMF AND SAF MERGER PROFORMA (ILLUSTRATION) 2

FOR ILLUSTRATION ONLY

Merger Impact to MPM IDR Billion Assumptions

[+] New Capital Injection 27 IDR 510 B at 20% yield

[+] CoF Savings 12 100 bps savings on bank borrowings

[+] Cost Synergies 1 50 bps savings on combined opex

[-] Dilution Impact (39) MPM ownership from 84.86% to 60%

Full Benefit FY14E 1 Year 1 impact

ROE before Full Benefit 12%

ROE with Full Benefit 12%

Leverage pre-capital injection 3.6x

Leverage post-capital injection 2.5x

Based on post tax (25%), annualized FY14E figures

14

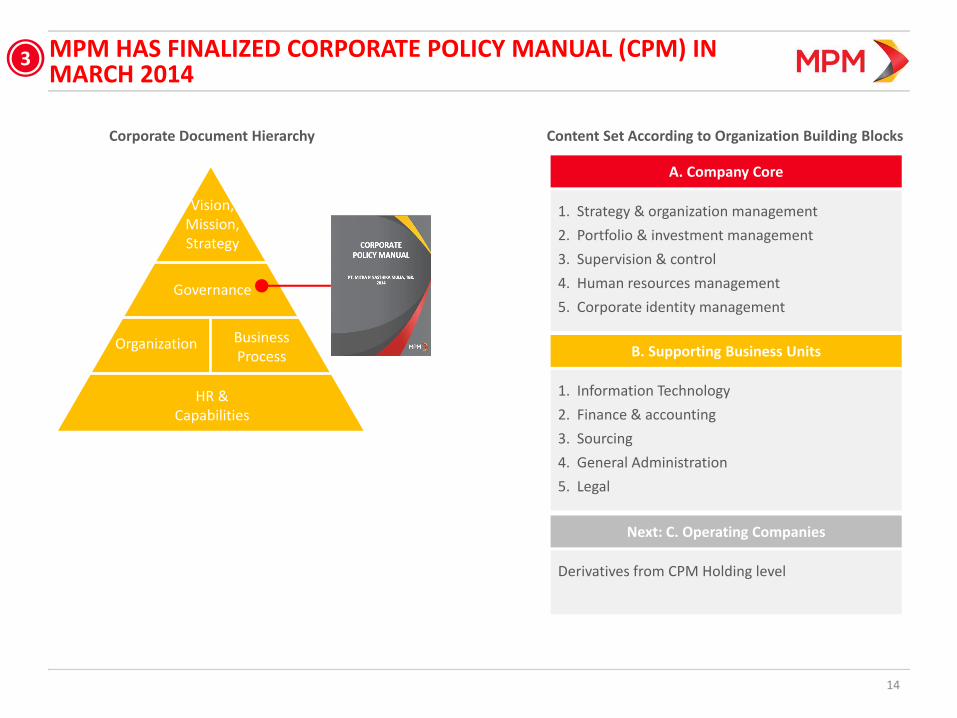

MPM HAS FINALIZED CORPORATE POLICY MANUAL (CPM) IN MARCH 2014

Vision, Mission, Strategy

Governance

Organization Business Process

HR & Capabilities

Corporate Document Hierarchy Content Set According to Organization Building Blocks

A. Company Core

B. Supporting Business Units

1. Strategy & organization management

2. Portfolio & investment management

3. Supervision & control

4. Human resources management

5. Corporate identity management

1. Information Technology

2. Finance & accounting

3. Sourcing

4. General Administration

5. Legal

Next: C. Operating Companies

Derivatives from CPM Holding level

3

15

In IDR B (%) denotes percentage of net IPO proceeds.

MPM HAS USED UP 77% OF THE PROCEEDS RAISED IN THE IPO

20%

3% 8%

13%

16%

17%

23% 970,000,000 shares

(21.7% of enlarged TSO) were offered to public market

at IDR1,500 per share

The 2013 P/E valuation is about 10.7X, with MPMX

price at IDR 1,300

Has been executed

To be executed

220 MPMRent acquisition

of SAK (1,280 cars)

225 MPMRent purchase

new cars

115 Loan repayment

175 MPMAuto build dealers

300 FKT 17% stake acquisition

45 MPMRent organic & inorganic opportunities

275 FKT factory

1,355 Net IPO proceeds

KEY MESSAGES

About MPM Leading End-to-End Consumer Automotive Company in Indonesia

Company Updates Continued scale building and growth across all business segments

1Q14 Summary & Business Segments Performance Stable 2W business despite natural disasters, Strong 4W business growth

FY14 Outlook ~20% revenue growth, ~10% NPATMI growth year-on-year

1Q14 Summary & Business Segments Performance Stable 2W business despite natural disasters, Strong 4W business growth

16

1Q14 Summary & Business Segments Performance Stable 2W business despite natural disasters, Strong 4W business growth

17

1Q14 & FY13 CONSOLIDATED REVENUE RESULTS

IDR B

10,777

FY12

2,480

159 377 205

13,879

FY13

(119)

% Growth from LY

+9% +7% +45% +26%

% Growth from LY

+27% +12% +67% +25%

Distribution & Retail

245 28 88 59

3,642

1Q14

(11)

3,233

1Q13

Auto Consumer Parts

Auto Services Financial Services

Elimination

+13%

+29% Stable revenue growth in all business units

18

1Q14 & FY13 CONSOLIDATED NET PROFIT AFTER TAX RESULTS

IDR B

% Growth from LY +5% +7% +20% +20%

Distribution & Retail

3 4 4 6

152

1Q14

17

115

1Q13

Auto Consumer

Parts

Auto Services

Financial Services

+32%

Positive growth in all business units while maintaining strong profitability

8 (5)

-29% -57%

% Growth from LY +27% +9% +159% +54%

57

19 95 51

526

FY13

(9)

374

FY12

+41%

(56)

+4% +16%

(5)

Elimination Head Office

Minority Interest

19

2W DISTRIBUTION & RETAIL: OUTPERFORM MARKET IN FY13, MANAGING IMPACT JAN-FEB ’14

736 905 968

FY12 FY13 FY14E

+7% +23%

216 216

1Q13 1Q14

0%

Sales Volume (000 units, YoY%)

211 266 288

FY12 FY13 FY14E

+8% +26%

Revenue (IDR B, YoY%)

NPAT (IDR B, YoY%)

FY13 / 1Q14 Highlights

FY14 Initiatives

• FY13: 23% sales volume growth vs. 10% industry

• 1Q14: volume impacted by flooding in Jan ‘14 and Kelud volcano eruption in Feb ’14, by Mar ‘14 volume back to normal

• Manage more efficient distribution by adding 1 warehouse to cater Southern area of E. Java

• Plan inventory level especially for Festive season preparation in July ‘14

• Increase retail sales volume by adding sales points and review financing sales portion

• Focus on operational improvement and CRM activities

Mulia

99 110 126

FY12 FY13 FY14E

+5% +12% 25

24

1Q13 1Q14

-3% MSO

9,112

FY12 FY13 FY14E

11,602 12,807

+10% +27%

1Q13 1Q14

2,897 2,695

+7%

70 74

1Q13 1Q14

+5%

20

4W DEALERSHIP: READY TO LAUNCH

Sales Volume (Car Units, YoY%)

0 -0.3

(14)

FY12 FY13 FY14E

NPAT (IDR B, YoY%)

FY13 / 1Q14 Highlights

FY14 Initiatives

• Signed agreement with Nissan Motor Distributor Indonesia in Aug ‘13

• MPMX 1st dealer was opened in Enggano, North Jakarta ... For Nissan & upcoming Datsun brand

• Sold 365 units since its inception in Nov ‘13

• Nissan launched New Teana in Mar ‘14

• Open at least 7 dealerships nationwide focusing on “3S”: showroom, services, and spare parts

• Tap into e-community channels + loyalty programs

• Partners with major financing companies & local partners

• Upcoming new lineups’ launching by Nissan:

- (0)

1Q13 1Q14

16,670

FY12 FY13 FY14E1Q13 1Q14

235

- 130

4,203

-

Revenue (IDR B, YoY%)

0

FY12 FY13 FY14E

1,444 627

1Q13 1Q14

43

387 - - 23

- (0)

FY12 FY13

21

CONSUMER PARTS: CONTINUING BRAND BUILDING & DISTRIBUTION ACTIVITIES IN FKT(1) TO INCREASE GROWTH

FY12 FY13 FY14E

+19% +8%

1Q13 1Q14

+0%

Sales Volume (KL, YoY%)

202 218 247

FY12 FY13 FY14E

+13% +8%

Revenue (IDR B, YoY%)

NPAT (IDR B, YoY%)

FY13 / 1Q14 Highlights

FY14 Initiatives

• Revenue and NPAT steady growth at +7%

• Slower volume growth due to lower repacking volume (FY13) and FO price increase (Feb 14) ... Competitors allowing “last bite” price

• Introduce new Y-MATIC product in 4Q13 to tap new market segment ... Branding “Spesialis Dingin”

• Ongoing ATL and BTL marketing and promotion activities to strenghten brand equity

• Focus on higher growth MATIC segment ... Product/SKU refinement and new product formulation introduction

• Implement key marketing and branding initiatives: Festive Season, World Cup, Racing events

• Strengthen sales and distribution organization

• Enter 4W lubricant business

• Continue feasibility study on blending plant expansion + operational efficiencies

1,286

FY12 FY13 FY14E

1,444

1,858

+29% +12%

1Q13 1Q14

415 387

+7%

62 67

1Q13 1Q14

+7%

16,670 16,678 56,393 60,632

72,033

(1) FKT = PT Federal Karyatama through its lubricant brand

22

AUTO SERVICES: STRONG PIPELINE, FOCUS ON OPERATIONAL IMPROVEMENTS

FY12 FY13 FY14E

+37% +69%

1Q13 1Q14

+41%

Fleet Size (Units, YoY%)

60 83

108

FY12 FY13 FY14E

+30% +38%

Revenue (IDR B, YoY%)

NPAT (IDR B, YoY%)

FY13 / 1Q14 Highlights

FY14 Initiatives

• FY13 fleet growth supported by 2 acquisitions, organic growth at 25% YoY

• Launched drivers training school in Mar ‘14 ... Key differentiator for corporate customers

• Average length of contract: 2.5 years

• Key Customers:

• Focus on operational improvements while growing customer base especially in MNCs

• Increase B2B brand awareness on MPMRent

• Strengthen MIS and CRM / CS capabilities

562

FY12 FY13 FY14E

938 1,256

+34% +67%

1Q13 1Q14

281

193

+45%

21 25

1Q13 1Q14

+20%

10,302

14,573

7,991

13,502

18,514

• Top New Customers:

23

MPMFINANCE: MERGER TO STRENGTHEN FRONT-END AND BACK END CAPABILITIES

2,286 2,361

4,349

FY12 FY13 FY14E

+84% +3%

506 709

1Q13 1Q14

+40%

New Booking (IDR B, YoY%)

578 674

1,280

FY12 FY13 FY14E

+90% +17%

161 183

1Q13 1Q14

+14%

100 95

196

FY12 FY13 FY14E

+105% -4%

24 23

1Q13 1Q14

-5%

Revenue (IDR B, YoY%)

NPAT (IDR B, YoY%)

FY13 / 1Q14 Highlights

FY14 Initiatives

• Strong growth in new booking ... Contributed equally between financial lease, 2W + 4W financing

• Increased revenue due to network expansion and higher lending rate

• Offset in opex and additional provisionings due to commodity business situation outside Java

• NPL performance:

• Execute merger with SAF with JACCS as 40% partner

• Diversify new product offerings, especially to support the growth of MPMAuto (Nissan & Datsun dealership)

• Strengthen risk management ... Centralized Desk Collection and recovery of write-offs

• Implementation of life insurance for car financing

• Increase collection efforts to reduce NPL to become <2.0%

2.2%

2.5% 2.4%

2.6%

Jun '13 Sep '13 Dec '13 Mar '14

Note: Assume combined MPMFinance and SAF financials for FY14E

24

SAF: TURNAROUND PERFORMANCE IN 2013

551

FY12 FY13

+86%

182 293

1Q13 1Q14

+61%

New Booking (IDR B, YoY%)

233 305

FY12 FY13

+31%

63

94

1Q13 1Q14

+49%

45

FY12 FY13

(6)

N/A

1Q13 1Q14

+83%

Revenue (IDR B, YoY%)

NPAT (IDR B, YoY%)

FY13 / 1Q14 Highlights

FY14 Initiatives

• Strong turn-around performance in new booking and

profitability

• Offset in additional provisionings / write-offs due to

commodity business situation outside Java

• NPL performance:

• Execute merger with SAF with JACCS as 40% partner

• Strengthen risk management and collection capabilities

• Maintain NPL <2%

6

12

1.7% 2.0%

1.5% 1.5%

Jun ’13 Sep ‘13 Dec ‘13 Mar ‘14

Note: Please refer to MPMFinance FY14E outlook for post-merger estimation

1.027

25

MPMINSURANCE: STRONG GROWTH THROUGH GROUP AND NON-GROUP BUSINESSES

Gross Premium (IDR B, YoY%)

5

13

FY12 FY13 FY14E

1

+146% +517%

1Q13 1Q14

+287%

NPAT (IDR B, YoY%)

FY13 / 1Q14 Highlights

FY14 Initiatives

• Additional businesses from new channels

• 10 nationwide representative offices are registered (Jakarta, Surabaya, Medan, Bandung, Denpasar, Bogor, Pekanbaru, Makasar, Malang and Semarang)

• Increase new partnerships with banks, financing companies and brokers

• Open 5 additional locations for representative offices

1

3

76

FY12 FY13 FY14E

+72% +1,411%

10

24

1Q13 1Q14

+132%

5

KEY MESSAGES

About MPM Leading End-to-End Consumer Automotive Company in Indonesia

Company Updates Continued scale building and growth across all business segments

FY14 Outlook [20 - 25%] revenue growth, [8 - 15%] NPATMI growth year-on-year

1Q14 Summary & Business Segments Performance Stable 2W business despite natural disasters, Strong 4W business growth

FY14 Outlook [20 - 25%] revenue growth, [8 - 15%] NPATMI growth year-on-year

26

FY14 Outlook ~20% revenue growth, ~10% NPATMI growth year-on-year

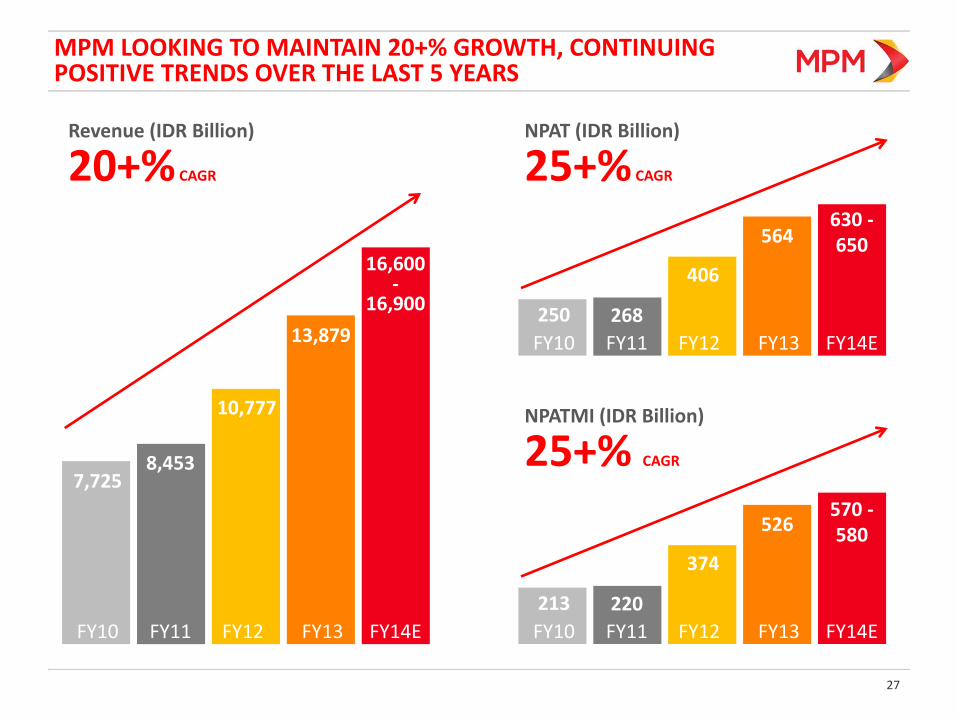

MPM LOOKING TO MAINTAIN 20+% GROWTH, CONTINUING POSITIVE TRENDS OVER THE LAST 5 YEARS

27

Revenue (IDR Billion)

20+% CAGR

16,600 -

16,900

13,879

10,777

8,453 7,725

FY10 FY11 FY12 FY13 FY14E

NPAT (IDR Billion)

25+% CAGR

570 - 580 526

374

220 213

FY10 FY11 FY12 FY13 FY14E

NPATMI (IDR Billion)

25+% CAGR

630 - 650 564

406

268 250

FY10 FY11 FY12 FY13 FY14E

1Q14 SUMMARY AND FY2014 OUTLOOK

28

Key Metrics FY12 FY13 % FY14E % 1Q13 1Q14 %

Profit & Loss (IDR Billion)

Net Revenue 10,777 13,879 29% 16,600 - 16,900

20 - 22% 3,233 3,642 13%

Gross Profit 1,618 2,024 25% 480 551 15%

GP Margins 15.0% 14.6% 14.8% 15.1%

Operating Profit 746 901 21% 217 244 12%

OP Margins 6.9% 6.5% 6.7% 6.7%

Net Profit from Cont. Operations 405 564 39% 128 157 23%

NP Margins 3.8% 4.1% 4.0% 4.3%

NPAT 406 564 39% 630 - 650 13 - 15% 128 157 23%

NPAT Margins 3.8% 4.1% 3.8 – 3.9% 4.0% 4.3%

NPATMI 374 526 41% 570 – 580 9 - 10% 115 152 32%

NPATMI Margins 3.5% 3.8% 3.4 – 3.5% 3.6% 4.2%

EBITDA 958 1,254 31% 287 338 18%

EBITDA % of Revenue 8.9% 9.0% 8.9% 9.3%

1Q14 SUMMARY AND FY2014 OUTLOOK (CONTINUED)

29

Key Metrics FY12 FY13 % FY14E % 1Q14 %

Balance Sheet (IDR Billion)

Cash 1,192 1,103 (7%) 771 (30%) 1,052 (5%)

ST & LT Loans 1,911 1,987 4% 3,107 56% 2,102 6%

MCNs 1,010 - (100%) - - 0%

Bank Funding for fincos (1) 3,216 3,551 10% 4,071 15% 3,770 6%

Book Value of Equity 1,837 4,395 139% 5,794 32% 4,564 4%

Ratios

Net Debt / Equity 2.69x 1.01x 1.11x 1.06 x

Net Debt / Equity excl. Fincos (1) 0.39x 0.20x 0.40x 0.23x

ROA 4.51% 5.05% 4.19% 5.16%

Debt / EBITDA 5.35x 4.42x 4.81x 4.34x

Debt / EBITDA excl. Fincos (1) 1.99x 1.58x 2.08x 1.55x

(1) MPMFinance and SAF

Disclaimer

30

• These materials have been prepared by PT Mitra Pinasthika Mustika Tbk (the “Company”, “MPM”) and have not been

independently verified. No representation or warranty, expressed or implied, is made and no reliance should be placed on the

accuracy, fairness or completeness of the information presented or contained in these materials. The Company or any of its

affiliates, advisers or representatives accepts no liability whatsoever for any loss howsoever arising from any information

presented or contained in these materials. The information presented or contained in these materials is subject to change

without notice and its accuracy is not guaranteed.

• These materials may contain statements that constitute forward-looking statements. These statements include descriptions

regarding the intent, belief or current expectations of the Company or its officers with respect to the consolidated results of

operations and financial condition of the Company. These statements can be recognized by the use of words such as “expects,”

“plan,” “will,” “estimates,” “projects,” “intends,” or words of similar meaning. Such forward-looking statements are not

guarantees of future performance and involve risks and uncertainties, and actual results may differ from those in the forward-

looking statements as a result of various factors and assumptions. The Company has no obligation and does not undertake to

revise forward-looking statements to reflect future events or circumstances.

• These materials are for information purposes only and do not constitute or form part of an offer, solicitation or invitation of any

offer to buy or subscribe for any securities of the Company, in any jurisdiction, nor should it or any part of it form the basis of, or

be relied upon in any connection with, any contract, commitment or investment decision whatsoever. Any decision to purchase

or subscribe for any securities of the Company should be made after seeking appropriate professional advice.