two italian leaders in the food industry: ferrero & barilla & risetti case... · two...

TRANSCRIPT

1

Two Italian leaders in the food industry:

Ferrero & Barilla

Jasmine Bentivegna

Simone Risetti

2

OutlineFerrero The internationalization history Organizational structure The East-Europe strategy The OLI framework Value chain and subsidiary role dynamics

Barilla The internationalization steps Multinationality criteria Activity undertaken Behaviour The OLI framework Value chain and subsidiary role dynamics

3

Ferrero is an Italian manufacturer of chocolate and other

confectionery products, founded in 1946 in Alba (Piedmont); it is

a multinational private company owned by the eponymous family

since its birth.

With a 7,8 billion revenue (close to the 8,3bln of Nestlé's

confectionery department) and 22400 employees, it is one of the

biggest players in the industry.

Reputation Institute's survey in 2009 ranked Ferrero as the most

reputable company in the world.

4

Transnationality

20%

59%

21%

Geographic distribution of revenues

Italy

Europe

ROW36%

64%

National employees vs Foreign employees

National

Foreign

Even with the assets information missing, we have

reasons to estimate that the TNI of Ferrero is around

60-65%.

5

6

Ferrero in the world

7

The internationalization history 1942 = first workshop opened in Alba (Piedmont, Italy)

1956 = first foreign plant in Europe: Stadtallendorf (Germany)

1960 = birth of the French and Belgian subsidiaries

1969 = expansion in the US market with an office in NY

1973 = the Ferrero International holding is created

1974 = expansion in Australia and New Zealand

1994 = the official distributor in China is chosen

2007 = constitution of the Ferrero Trading (Shanghai) Co. Ltd

8

Organizational structure

The company adopts – as of 2006 – a functional structure:

InstitutionalChairman

InstitutionalChairman

R&DProducts &Systems Manag.

Co-CEO Co-CEO

DevelopmentChairman

Commercialarea Marketing

DevelopmentChairman

9

Non-core activitiesFerrero performs some non-core activities through inner

specialized companies:

Soremartec = it is the company devoted to R&D and

business intelligence; it is located in Alba and provides

innovations to all the branches worldwide, focusing especially

on product innovations and the study of new, original

products ( long-term orientation). Typical innovations →concern packaging reduction, improvement of nutritional

aspects, portioning and food security (in collaboration with

local universities), but the centre also covers other tasks such

as business analysis and data mining.

10

Pubbliregia = focused on advertising and promotional

communications, in which Michele Ferrero has been a pioneer

in understanding its power since the early '70s. Nowadays

the company still puts lots of efforts in strengthening brand

loyalty and also engaging younger customers, even through a

massive use of new media.

Energhe = the mission of this company is the improvement

of energetic efficiency within production facilities and offices

and the construction of high efficiency electrical plants. The

aim is not only cost reduction, but it falls within the broader

Ferrero environmental sustainability policy (e.g. water and

CO2 reduction, energetic self-sufficiency, renewable sources).

11

The East-Europe strategy The productive internationalization strategy emerging from the multiple

growth actions taken is characterized – from a strategic perspective - by

differentiation and complementarity of FDI goals.

The market entry in Centre-East Europe is double-sided:

1. establishment of a production plant in Poland for specific products

(mid '90s) greenfield investment→

2. constitution of a network of commercial offices, run by managers

from within the company but completely autonomous, in order to

directly oversee the national markets

→ multidimensional approach

12

Why this kind of FDI?

Part of a broader plan of international rationalization of

production

Cover the expansion of local demand, also due to welfare

increase in the years after the USSR fall

Preservation of the quality and freshness standards of the

products, as well as reduction of logistics costs (local

production is cheaper than supplying from a distance).

However, there is no qualitative nor quantitative

adjustment of the goods in the various markets.

13

These operations show:

an efficiency-seeking attitude, as concerning the overall

rationalization of production; the food industry in which it

operates is tipically defined as a scale-intensive industry

a market-seeking behaviour, regarding the emphasis put on

the positioning in nascent markets and the reduction of

logistics costs

All the actions taken manifest a proactive mindset by the firm,

acting as an innovative market leader aggressive activities→

14

Production

The productive structure is highly integrated: most of the value

chain activities are directly performed by the firm itself, from

the selection of the raw materials to the final packaging.

The only partnerships of external supply are those related to

the provision of raw and packaging materials.

This is also confirmed by the kind of FDIs undertaken, which

take the form of horizontal FDI (expansion of a similar

business) rather than a vertical one (outsourcing).

15

The OLI Framework Ownership advantages = Trademark and brand awareness

are really high (e.g. people want Nutella, not a hazelnut

cream), as well as trust from customers. The industry is

scale-intensive, too.

Location advantages = Not very relevant, aside from a

purely geographical perspective (i.e.to better serve some

markets)

Internalization advantages = High degree of freedom, tight

control over production, pursue of family values like

physiological and “healthy” growth; the company never

engaged in partnerships or joint ventures

16

Value chain Innovation: all the subsidiaries are implementers or even

blank rows (Soremartec acts as the strategic leader)

Production: since production is centralized and supplies

several countries, the subsidiaries where production plants

are located are all contributors or strategic leaders, while

the others are implementers (logistics excluded, which is

autonomous for every branch)

Sales: some of them are strategic leaders, other

contributors (depending on the strategic importance of each

market)

Administrative functions: centralized; internal competences

are low (e.g. Ferrero self-finances) implementers→

17

Subsidiary role dynamicsWe refer to a typical Ferrero subsidiary, i.e. we do not consider

the relatively few with production facilities. Basing on the

available information (and given that Ferrero is considered

one of the most secretive companies in the world), we can

only try to understand the pattern it has undertaken

throughout the years.

We find that:

innovation has worsened and it is now a blank row

(absorption of the activities by Soremartec)

there is an improvement of sales competences (each

subsidiary has a large degree of freedom and self-governing)

18

production weakened too: they only retain the logistics

operations

administrative functions have always been developed at a

centralized level and are thus at a status quo level

Therefore we find the Pattern 5 (single activity specialization)

the most suitable one to describe the dynamics of the

majority of subsidiaries in the company.

19

Barilla is one of the leading Italian groups in the food

industry, the first in pasta sales all over the world,

ready sauces in continental Europe, baked products in

Italy and crunchy bread in Scandinavian countries.

20

21

The internationalization stepsIn 1877 Pietro Barilla opened a shop where he produced bread and

pasta.

After some oven improvements, his son went to the USA in 1950 to

keep up-to-date about packaging, advertisement and large-scale

retail trade.

The first step towards internationalization is in 1991, when they buy

Misko, the Greek leader of pasta production, and the consequent

birth of “Barilla Deutschland”.

In 1999 they open the plants of Foggia and Ames (USA).

In 2004 Academia Barilla was born with the aim to protect, develop

and promote the Italian gastronomic culture in the world.

22

The Barilla Centers for Food & Nutrition are designed to do

research about local tastes, in order to offer products

better tailored to each market preferences, by collecting

mondial knowledge, analysing it and proposing solutions to

deal with future food industry challenges.

23

Multinationality Criteria• Number and size of foreign affiliates:

The company from Parma operates mostly in Italy, USA,

France, Germany; it controls 43 subsidiaries (30 abroad) and

commercializes 2,5 million tons of products every year with

its brands: Barilla, Mulino Bianco, Voiello, Pavesi, Academia

Barilla, Wasa, Harrys (France and Russia), Lieken Urkorn and

Golden Toast (Germany).

• Number of countries the MNE is active in:

14 countries in Europe, 3 in America, 2 in Asia and Oceania

24

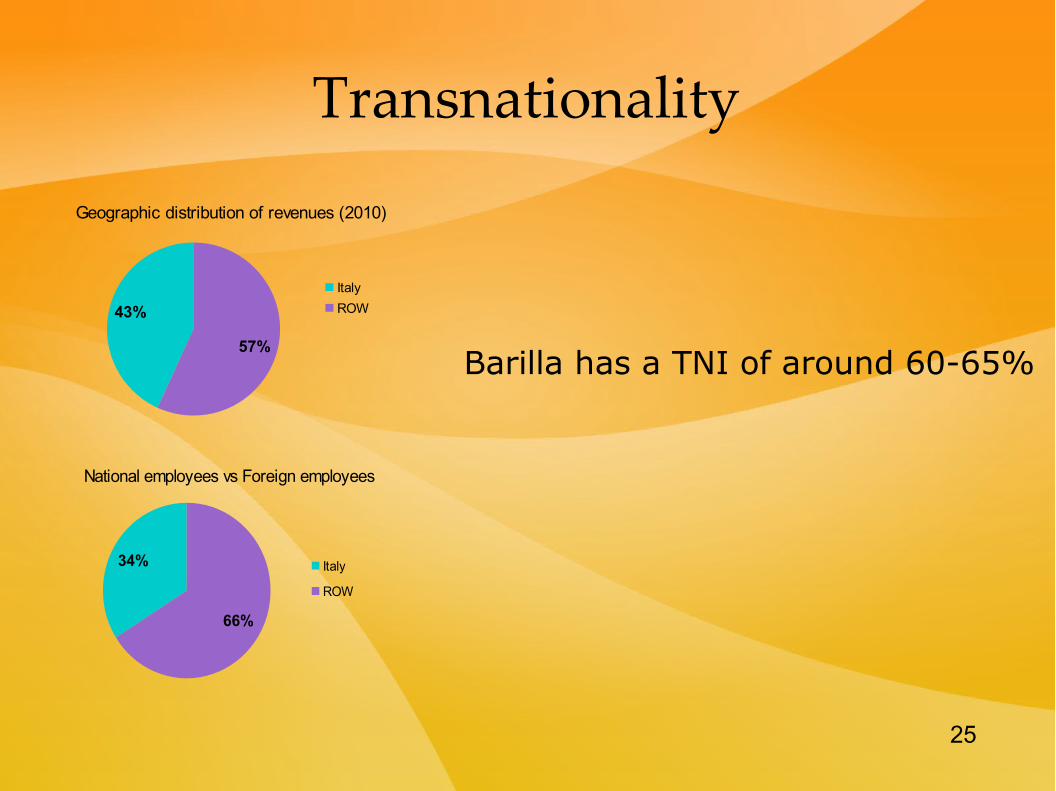

25

43%

57%

Geographic distribution of revenues (2010)

Italy

ROW

Transnationality

34%

66%

National employees vs Foreign employees

Italy

ROW

Barilla has a TNI of around 60-65%

26

Aggressive activityThe goal is maintaining the market share in Europe and North

America while pursuing an “aggressive growth” in

developing countries, where now the company makes the 4%

of the total revenue (and planned to double).

This year revenues are growing by 3-4% in monetary value,

and volumes by 4%. The boost for the latters will come from

America (+10%) and Asia (+10%), while Europe will

increase by 2%, but Italy is still decreasing (-2%): “The duty

for a brand leader is to boost the whole category, get people

to consume more pasta as once. We want to stop this

decline”.

27

They also point to Brazil to increase volumes and revenues.

There the company already started exporting some types

of pasta and sauces, but it will obtain more control when

some local firms will produce for the Group near São Paulo,

following the preferences of the local population. It focuses

on soft wheat and egg pasta, obtaining at the same time

lower prices than the imported products. From 18 millions

euros gained in Brazil in 2012, they now aim at 100

millions by 2016. As the CEO Guido Barilla says, it is one of

the most promising markets for pasta in the world.

→ The company is seeking to take proactive action to pursue

its strategic objectives

28

EXPORT

LICENSING

GREENFIELDINVESTMENT?

29

BehaviourThey can be classified as market seekers: market-seeking

investment is undertaken, in this case, to exploit the

possibilities offered by a new market.

The products need to be adapted to local tastes or needs,

not only for the goods intrinsic characteristics (e.g. Brazil),

but also in the way they are commercialized (e.g. e-

commerce in China)

Of course, it is also easier to control the business overseas

instead of having a centralized headquarter. For this

reason, they have set up foreign-producing facilities.

30

The OLI FrameworkOwnership advantages:

strong trademark

long tradition

good reputation

The Locational advantages are negligible

Internalization advantages:

strong span of control

freedom (since they are a family, they do not have to ask or

decide with someone else)

mills as a form of backward integration (more efficient than

outsourcing)

31

Value chain

Innovation: most of the subsidiaries are black holes, given

the importance of local preferences; however, the general

R&D activities are centralized in Italy and USA

Production: strengthening of production facilities with a role

of contributors

Sales: large autonomy of subsidiaries as contributors

Administrative functions: they are performed at a

centralized level blank rows for most subsidiaries→

32

Subsidiary role dynamics

If we take into account the subsidiary in Rubbiano (Italy), we

can see how there is a strengthening of the productive part

of the value chain, while the other activities can be

considered as status quo; we are then talking about an

added, single-activity regional charter (Pattern 6).

33