turkish ict sector

TRANSCRIPT

Republic of Turkey Prime Ministry

Investment Support and

Promotion Agency of Turkey (ISPAT)

Turkish ICT Sector

Necmettin KAYMAZ

Chief Project Director

“Technology, the Way to Prosperity”

UK Trade and Investment

British Consulate-General Istanbul

February 23, 2015

AGENDA

Turkish ICT Market

Drivers of Turkish ICT Sector

Incentives for ICT Sector

Turkish ICT Market

Summary of Turkish ICT Market..

Sizeable Domestic Market of $32bn

Double-Digit Growth Performance

Young & Dynamic Population

Skilled-Labor Force

e-government

Incentives

Ambitious Targets

Export Opportunities

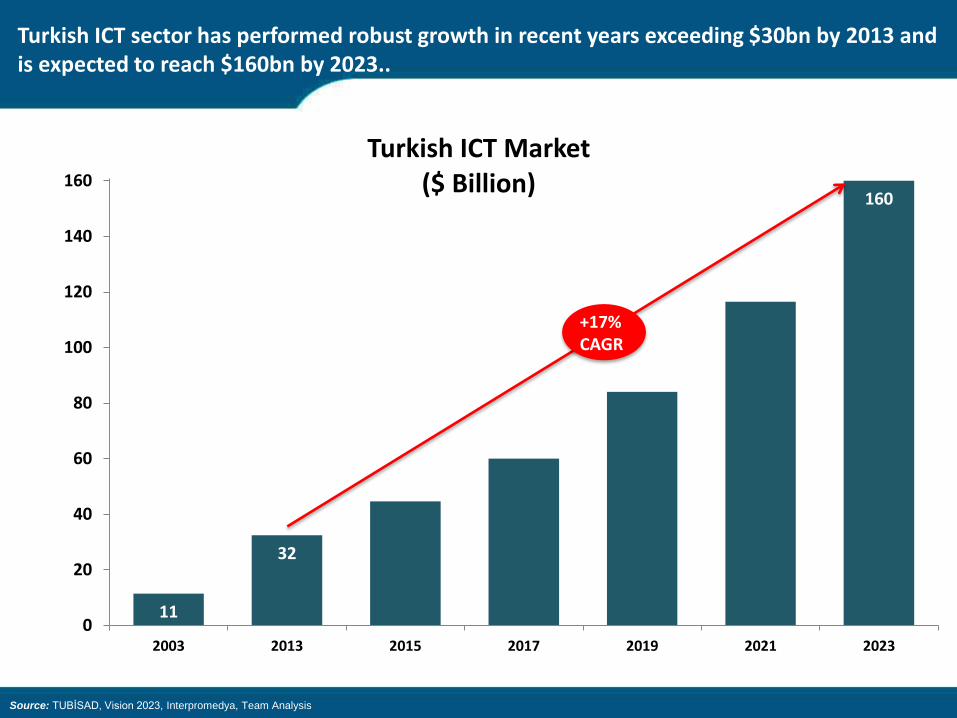

11

32

160

0

20

40

60

80

100

120

140

160

2003 2013 2015 2017 2019 2021 2023

Turkish ICT Market ($ Billion)

Source: TUBİSAD, Vision 2023, Interpromedya, Team Analysis

Turkish ICT sector has performed robust growth in recent years exceeding $30bn by 2013 and is expected to reach $160bn by 2023..

+17% CAGR

Source: Deloitte

Growth performance of Turkish IT companies has been also observed in international rankings..

86

67

45

43

42

36

32

24

22

18

15

93

86

54

48

53

27

23

23

18

7

15

0 20 40 60 80 100

France

UK

Sweden

Norway

Netherlands

Turkey

Germany

Finland

Israel

Belgium

Poland

2014

2011

Number of Companies in EMEA’s 500 Fastest Growing Companies

Source: TUBISAD

Turkish ICT sector is mainly dominated by communication technologies…

IT $9,4bn

Breakdown of Turkish ICT Market 2013

Communication Technologies $23bn

$32,4bn

Hardware $6bn

Communication Technologies Market

Electronic Communication $17bn

$23bn

Hardware $5,3bn

Software $2,6bn

Service $1,6bn

IT Market

$9,4bn

Potential growth areas: • Software • Services • Hardware

Source: TUBISAD

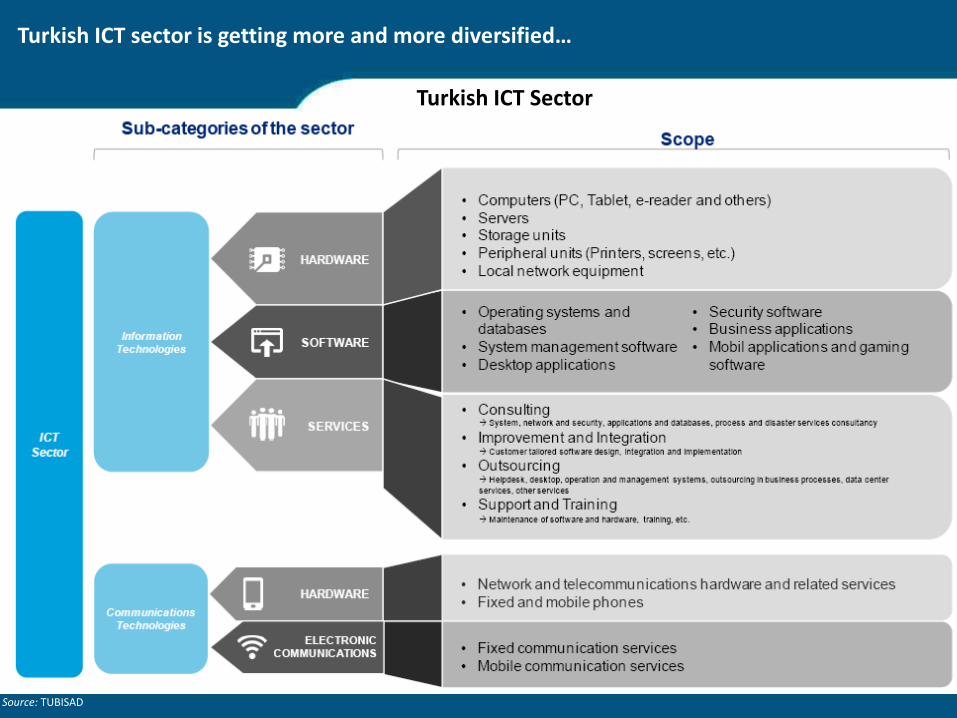

Turkish ICT sector is getting more and more diversified…

Turkish ICT Sector

Source: Information and Communication Technologies Authority *As of Sep 2014

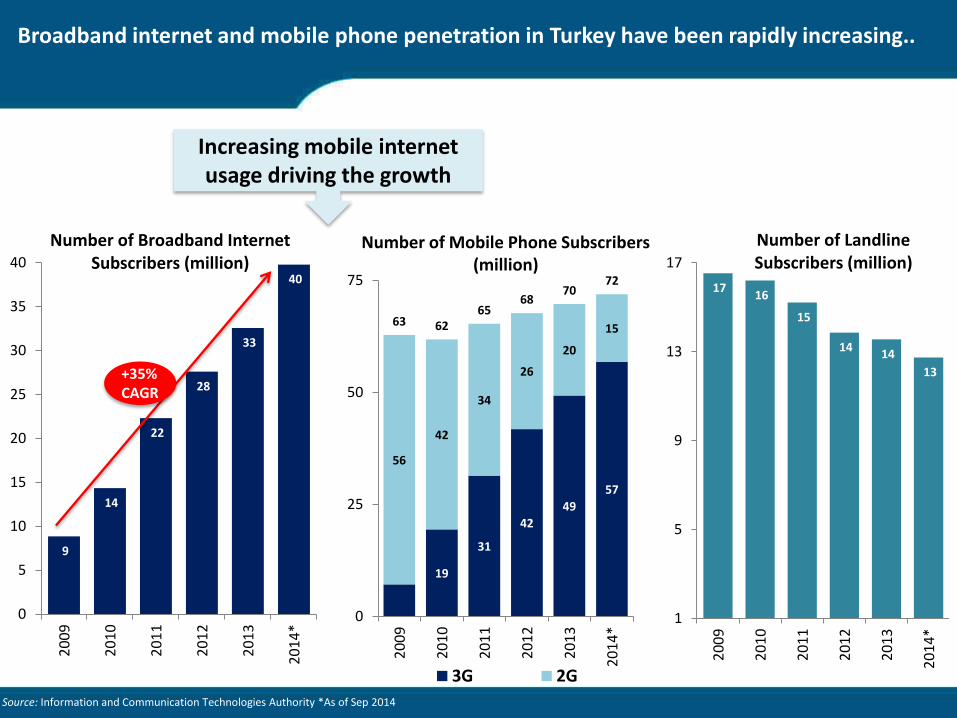

9

14

22

28

33

40

0

5

10

15

20

25

30

35

40

20

09

20

10

20

11

20

12

20

13

20

14

*

Number of Broadband Internet Subscribers (million)

+35% CAGR

19

31

42

49

57

56

42

34

26

20

15 63 62

65 68

70 72

0

25

50

75

20

09

20

10

20

11

20

12

20

13

20

14

*

3G 2G

Number of Mobile Phone Subscribers (million)

Broadband internet and mobile phone penetration in Turkey have been rapidly increasing..

17 16

15

14 14

13

1

5

9

13

17

20

09

20

10

20

11

20

12

20

13

20

14

*

Number of Landline Subscribers (million)

Increasing mobile internet usage driving the growth

Source: TURKSTAT *16-74 age group

ICT statistics show rapidly increasing usage among both Turkish households and enterprises…

Online Transactions

Source: Interbank Card Center (BKM), domestic and international transactions with domestic cards as well as domestic transactions with international cards

61

227

10

45

5

10

15

20

25

30

35

40

45

50

50

70

90

110

130

150

170

190

210

230

2009 2010 2011 2012 2013 2014

Number (Million, LHS) Value (Billion TL, RHS)

36,5% CAGR

30% CAGR

88

80

48

92 91

54

40

50

60

70

80

90

Computerusage

Internetaccess

Firms withinternet

2005

2013

Enterprise ICT Usage (%)

20

33 30

60

54 54

10

20

30

40

50

60

Householdswith Internet

ComputerUsage*

InternetUsage*

2007 2014

Household & Individual ICT Usage (%)

57 million credit cards

(2014)

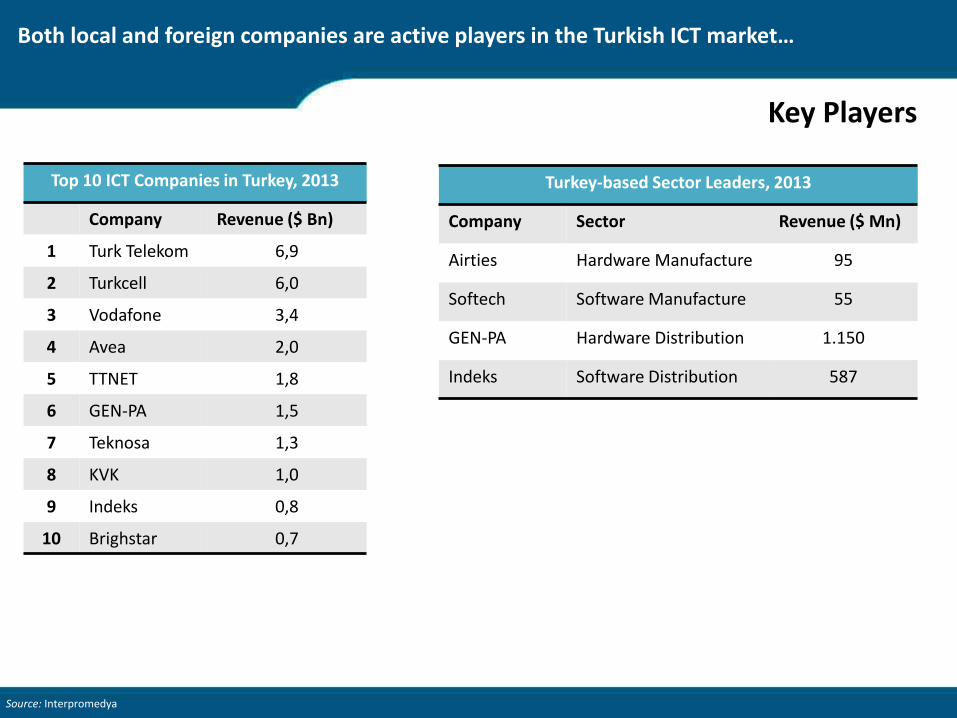

Key Players

Top 10 ICT Companies in Turkey, 2013

Company Revenue ($ Bn)

1 Turk Telekom 6,9

2 Turkcell 6,0

3 Vodafone 3,4

4 Avea 2,0

5 TTNET 1,8

6 GEN-PA 1,5

7 Teknosa 1,3

8 KVK 1,0

9 Indeks 0,8

10 Brighstar 0,7

Source: Interpromedya

Turkey-based Sector Leaders, 2013

Company Sector Revenue ($ Mn)

Airties Hardware Manufacture 95

Softech Software Manufacture 55

GEN-PA Hardware Distribution 1.150

Indeks Software Distribution 587

Both local and foreign companies are active players in the Turkish ICT market…

Source: OECD

Turkish ICT sector is more open to FDI than many countries… 0

,75

0,5

75

0,4

0,3

25

0,1

75

0,2

65

0,2

0,1

0,1

1

0,0

89

0,0

75

0,0

25

0,0

23

0

0,7

5

0,5

75

0,4

0,3

25

0,1

75

0,5

05

0,2

0,1

5

0,0

2

0,0

95

0,0

75

0,0

25

0,0

23

0

0,7

5

0,5

75

0,4

0,3

25

0,1

75

0,0

25

0,2

0,0

5

0,2

0,0

82

0,0

75

0,0

25

0,0

23

0 0

0,1

0,2

0,3

0,4

0,5

0,6

0,7

0,8

Ch

ina

Can

ada

Au

stra

lia

Ko

rea

Ind

ia

Jap

an

Swed

en

Ru

ssia US

OEC

D -

Ave

rage

Po

lan

d

Bra

zil

UK

Turk

ey

Communications Fixed telecoms Mobile telecoms

Index Score:

• 1 = Closed to FDI

• 0 = Open to FDI

FDI Regulatory Restrictiveness Index 2013

The FDI Index gauges the restrictiveness of a country’s FDI rules by looking at the four main types of restrictions on FDI: 1. Foreign equity limitations, 2. Screening or approval mechanisms , 3. Restrictions on the employment of foreigners as key personnel, 4.Operational restrictions, e.g. restrictions on branching and on capital repatriation or on land ownership

Source: CBRT, Ministry of Economy

Turkish ICT sector has been one of the most attractive sectors for foreign direct investment (FDI)..

$11,6bn

$2,9bn

FDI in Turkish ICT Sector, 2004-2014

Information and Communication Services

Manufacture of Computers, Electronic-Electricaland Optical Equipment

Total FDI in ICT

$14,5 Billion

1.239

516

194 15

Number of Foreign Companies in Turkish ICT, 2014

Computer and related activities

Post & telecommunications

Manufacture of radio, TV & communication equipment

Manufacture of office, accounting & computing machinery

1.964 companies

Source: TURKSTAT; ITC, UNCTAD, WTO joint dataset.

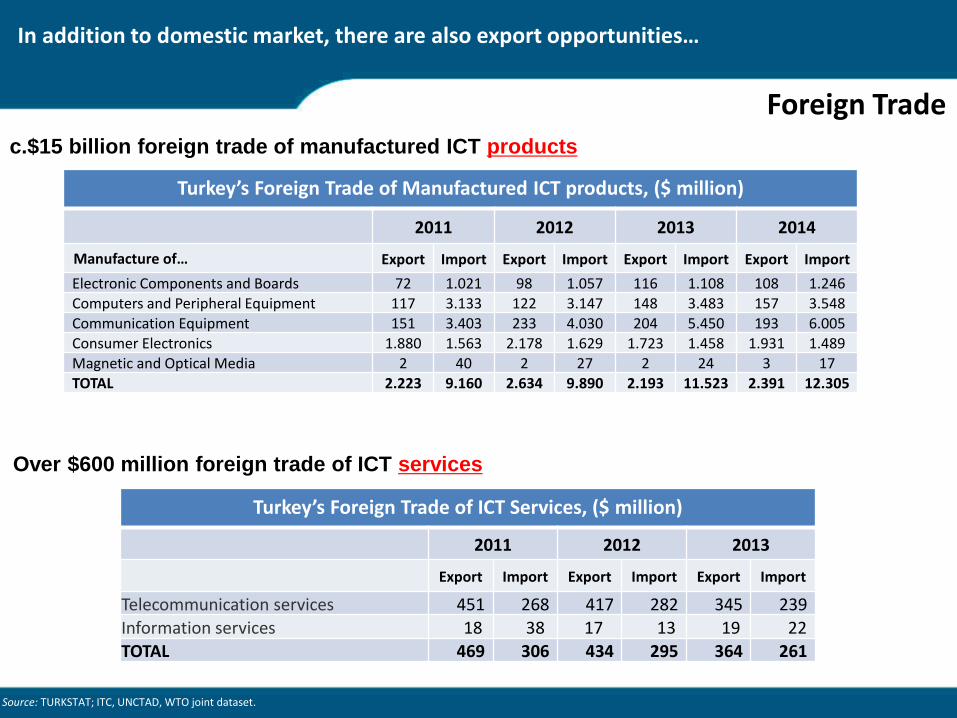

Foreign Trade

Turkey’s Foreign Trade of Manufactured ICT products, ($ million)

2011 2012 2013 2014

Manufacture of… Export Import Export Import Export Import Export Import

Electronic Components and Boards 72 1.021 98 1.057 116 1.108 108 1.246 Computers and Peripheral Equipment 117 3.133 122 3.147 148 3.483 157 3.548

Communication Equipment 151 3.403 233 4.030 204 5.450 193 6.005 Consumer Electronics 1.880 1.563 2.178 1.629 1.723 1.458 1.931 1.489 Magnetic and Optical Media 2 40 2 27 2 24 3 17 TOTAL 2.223 9.160 2.634 9.890 2.193 11.523 2.391 12.305

c.$15 billion foreign trade of manufactured ICT products

Turkey’s Foreign Trade of ICT Services, ($ million)

2011 2012 2013

Export Import Export Import Export Import

Telecommunication services 451 268 417 282 345 239

Information services 18 38 17 13 19 22 TOTAL 469 306 434 295 364 261

Over $600 million foreign trade of ICT services

In addition to domestic market, there are also export opportunities…

Source: International Trade Center, latest data available as of 17.02.2015

EUROPE

ICT Service Import: • Computer & Information Services: $79bn • Telecommunication Services: $43bn

RUSSIA

ICT Service Import: • Computer & Information Services: $3,3bn • Telecommunication Services: $2,8bn

MENA

ICT Service Import: • Computer & Information Services: $2bn • Telecommunication Services: $4,7bn

CENTRAL ASIA & CAUCASUS

ICT Service Import: • Computer & Information Services: $0,2bn • Telecommunication Services: $0,4bn

Over $135 billion

foreign trade of

ICT Services at a

4-hour flight

distance from

Turkey

Turkey has the potential to emerge as an ICT service center in the region as Turkey incentivizes export of services by exempting 50% of the export revenues from tax..

Import of ICT Services, 2013

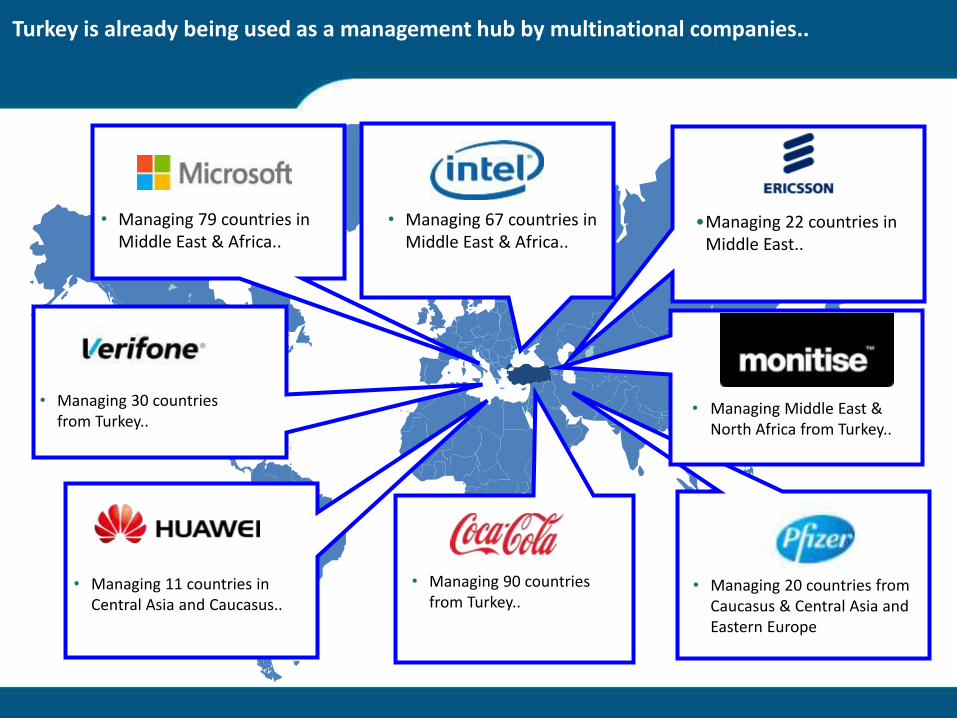

Access to Multiple Markets

• Managing 79 countries in Middle East & Africa..

• Managing 67 countries in

Middle East & Africa..

• Managing 20 countries from

Caucasus & Central Asia and Eastern Europe

• Managing 30 countries from Turkey..

• Managing 11 countries in

Central Asia and Caucasus..

• Managing 90 countries from Turkey..

•Managing 22 countries in Middle East..

• Managing Middle East & North Africa from Turkey..

Turkey is already being used as a management hub by multinational companies..

Drivers of ICT Sector

Population Pyramid (%)

5 4 3 2 1 0 1 2 3 4 5

0-4

5-9

10-14

15-19

20-24

25-29

30-34

35-39

40-44

45-49

50-54

55-59

60-64

65-69

70-74

75-79

80-84

85-89

90+

Female Male

%

Age Group TURKEY

5 4 3 2 1 0 1 2 3 4 5

0-4

5-9

10-14

15-19

20-24

25-29

30-34

35-39

40-44

45-49

50-54

55-59

60-64

65-69

70-74

75-79

80-84

85-89

90+

Female Male

%

Age Group EUROPE

Source: Turkstat, Eurostat, UN, 2014

78 million young & dynamic people

5 4 3 2 1 0 1 2 3 4 5

0-4

5-9

10-14

15-19

20-24

25-29

30-34

35-39

40-44

45-49

50-54

55-59

60-64

65-69

70-74

75-79

80-84

85-89

90+

Female Male

%

Age Group ASIA

Turkey has a young and dynamic population, with half under the age of 30, making Turkey the country with the largest youth population in Europe…

Favorable demographic trend is here to stay for the next two decades with increasing working age population and low dependency ratio..

Source: UN

80

100

120

2014 2017 2020 2023 2026 2029 2032 2035

Working Age Population (15-64) (Index: 2014=100)

Europe

Turkey

40

45

50

55

60

65

70

75

2014 2017 2020 2023 2026 2029 2032 2035

Total Dependency Ratio (%) (Age 0-14 & Age 65+) / Age 15-64

Europe

Turkey

95

100

105

110

115

120

20

14

20

15

20

16

20

17

20

18

20

19

20

20

2021

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

20

35

Turkey

Europe

Population Projections (Index: 2014=100)

Source: IMD World Competitiveness Yearbook 2014,

7,4

7,2

7,0

6,9

6,7

5,3

0 2 4 6 8

Turkey

Bulgaria

Hungary

China

Romania

Brazil

Availability of IT Skills

7,1

6,8

6,7

6,0

4,5

3,9

0 2 4 6 8

Turkey

Hungary

Romania

China

Brazil

Bulgaria

Availability of Qualified Engineers

Turkey offers investors with necessary ICT skills and talents..

Executive Opinion Survey based on an index from 0 to 10 0 = Not available 10 = Readily available

Availability of ICT Skills, 2014

Source: OSYM

3621

3987

4403

3000

3300

3600

3900

4200

4500

2010 2011 2012

Number of Annual Graduates in Electrical-Electronics Engineering

3028

2906

3187

2700

2800

2900

3000

3100

3200

2010 2011 2012

Number of Annual Graduates in Computer Engineering

4881

5161

5605

4500

4700

4900

5100

5300

5500

5700

2010 2011 2012

Number of Annual Graduates in Mathematics

13203

13607

15175

12000

13000

14000

15000

16000

2010 2011 2012

Number of Annual Graduates in Computer Tech & Programming

Turkish higher education does support the ICT industry through training world-class engineers and technicians…

Turkish primary & secondary education also supports the ICT industry through enhanced usage of ICT products…

Hardware & Software infrastructure

Educational e-content and Management of e-content

Effective Usage of the ICT in Teaching Programs

In-service Training of the Teachers

Conscious, Reliable, Manageable and Measurable ICT Usage

To integrate state-of-the-art computer technology into Turkey’s public education system and provide tablets and internet access.

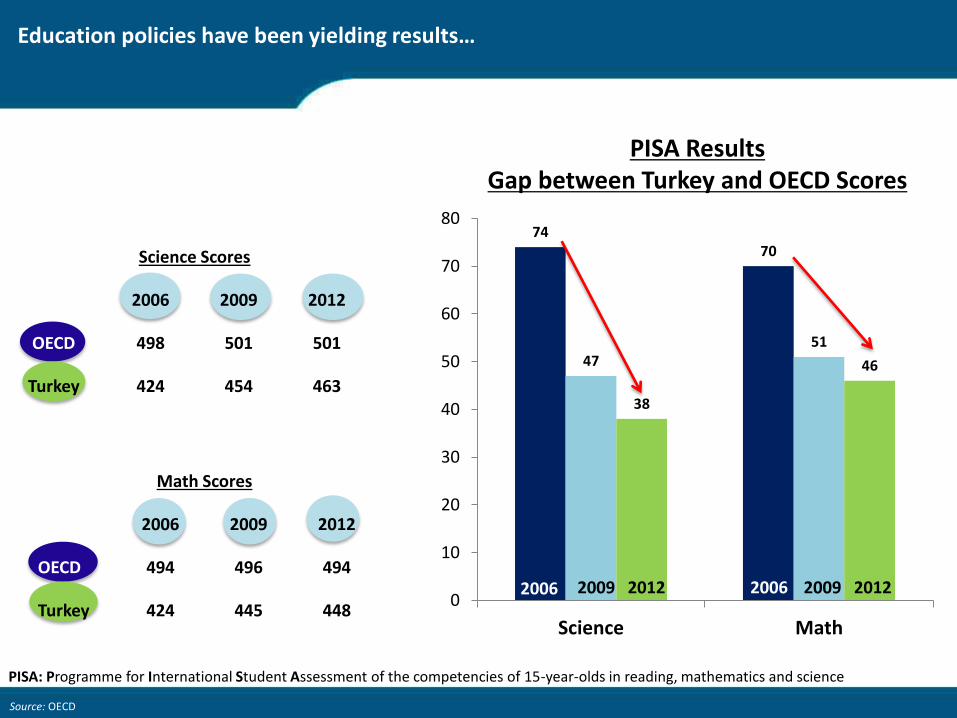

Education policies have been yielding results…

74 70

47 51

38

46

0

10

20

30

40

50

60

70

80

Science Math

2006 2006 2009 2009 2012 2012

Source: OECD

PISA Results Gap between Turkey and OECD Scores

PISA: Programme for International Student Assessment of the competencies of 15-year-olds in reading, mathematics and science

Math Scores

2006 2009 2012

OECD 494 496 494

Turkey 424 445 448

Science Scores

2006 2009 2012

OECD 498 501 501

Turkey 424 454 463

Source: EUROSTAT, 2012

42,4

37,5 37,3

25,0

10,0 8,3 8,0

6,8

0

10

20

30

40

Labor cost per hour (€) in manufacture of computer, electronic and optical products

42,6

39,1 36,8

19,3

10,0 7,4 7,0 6,7

0

10

20

30

40

Labor cost per hour (€) in manufacture of electrical equipment

Labor cost ICT Manufacturing, 2012

Turkey offers a cost-competitive labor force in ICT manufacturing..

Source: EUROSTAT, 2012

44,8 42,7

38,4

31,6

19,2 14,3 13,8 13,4

0

10

20

30

40

50

Labor cost per hour (€) in computer programming, consultancy and

related activities

46,6 41,8 40,2

29,0 23,3

19,4 15,9 14,0

0

10

20

30

40

50

Labor cost per hour (€) in Telecommunications

42,6 40,6

35,7 33,2

18,5

12,1 11,6 10,8

0

10

20

30

40

50

Labor cost per hour (€) in Information service activities

Labor cost ICT Services, 2012

Turkey has also a competitive edge in labor cost for ICT services..

Source: Turkey Vision 2023

Industrial Strategy of the Ministry of Science, Industry & Technology

• Increasing the number of companies that continuously improve their skills within the economy.

• Increasing the number of medium- and high-technology sectors in production & export.

• Transition to products with high added value in low-tech sectors.

• To increase the sector's share in the GDP from 2.9% to 8% in 2023.

Communication Strategy of The Ministry of Transport, Maritime Affairs &

Communications

• Having 120 million mobile subscribers.

• Increasing number of broadband subscribers to 30 million.

• Providing internet connections for 14 million houses at a speed of 1000 Mbps

• Reaching an ICT sector size of $160 billion.

R&D Strategy of the Supreme Council of Science and Technology

• Increasing the number of researchers from 135,000 to 300,000.

• Reaching a number of 180,000 private sector researchers from 39,000.

• Increasing the R&D expenditure to GDP ratio to 3% from 0.85%.

• Increasing private sector R&D expenditure of the GDP ratio to 2%.

2023 ICT

Targets

The government has also set ambitious goals in ICT sector to ensure Turkey becomes an information society with a fully developed ICT sector by 2023

Information Society

Objectives

Citizens Businesses Government

A globally competitive IT sector

Competitive, widespread and affordable telecommunications infrastructure and services

Improvement in R&D and Innovation

Social

transformation

ICT Adoption

by businesses

Citizen focused

service

transformation

Modernization in

public

administration

Information Society

• Government's holistic e-transformation efforts started in 2003

– Department of Information Society has been established under M. of Development for coordination of activities

• Since its inception, Turkey has made

progress in improving its Networked Readiness Index (NRI) from 3.96 to 4.30 (on a scale from 1=worst to 7= best) between 2007 and 2014; moving the country ranking from 55 to 511

• For the coming years, government focus is on transforming Turkey into an ICT hub

Major growth in Turkish ICT market is expected to be driven by public expenditure which has been increasing steadily as a result of information society strategy…

1. Source: WEF, NRI measures the propensity for countries to exploit the opportunities offered by ICT. The NRI has 3 components: the environment for ICT offered by a given country or community(Market, political, regulatory, infrastructure),the readiness of the community’s key stakeholders (individuals, businesses, and governments) to use ICT, and finally the usage of ICT.

Source: Ministry of Development *Adjusted to 2014 prices

Government has been a key driver of ICT development for Turkey’s e-transformation…

0,7 0,8 0,9

1,2 1,3 1,3

1,2 1,2

1,6

2,5

2,8

3,8 3,7

0

1

2

3

4

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

Government Investment in ICT (Billion TL*)

12% CAGR

Education; 43,7%

Other public services; 41,7%

Agriculture; 5,5%

Health; 2,5%

Breakdown of Government Investment in ICT (2014)

Source: Ministry of Development

Government has launched ICT projects to transform Turkey into an information society through e-government…

1415

257

209

167

157

114

114

108

106

104

0 300 600 900 1200 1500

Ministry of National Education

Ministry of Interior

Ministry of Transport

Universities

Ministry of Justice

Turkish National Police

Ministry of Agriculture

Social Security Institutions

Land Registry

Revenue Administration

1400

87

77

63

58

58

55

55

55

54

0 300 600 900 1200 1500

Fatih Project

Various Projects (MoJ)

Modernization of Land Registry

GSM Infrastructure

Improving Communication Infrastructurein Disasters (MoH)

Agricultural Monitoring & Info System

City Security Management System(MOBESE)

IT Project (Turkish National Police)

Emergency Call System (112)

National Identity Card

Top 10 Public Institutions Investing ICT (Million TL, 2014)

Top 10 Public Project in ICT (Million TL, 2014)

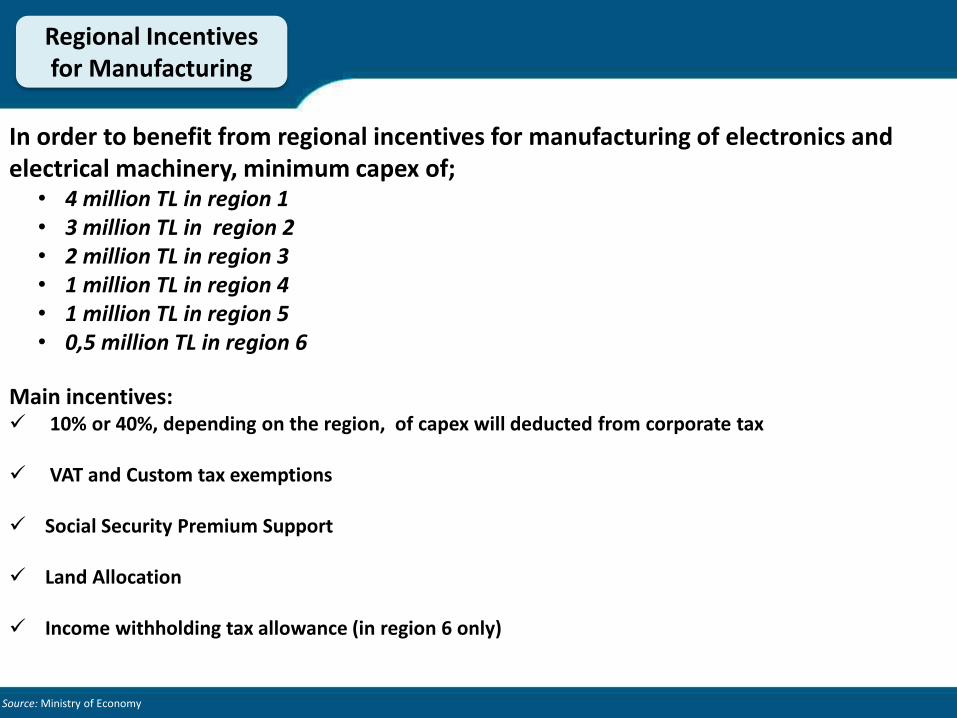

Incentives

Source: Ministry of Economy

In order to benefit from regional incentives for manufacturing of electronics and electrical machinery, minimum capex of;

• 4 million TL in region 1 • 3 million TL in region 2 • 2 million TL in region 3 • 1 million TL in region 4 • 1 million TL in region 5 • 0,5 million TL in region 6

Main incentives: 10% or 40%, depending on the region, of capex will deducted from corporate tax

VAT and Custom tax exemptions

Social Security Premium Support

Land Allocation

Income withholding tax allowance (in region 6 only)

Regional Incentives for Manufacturing

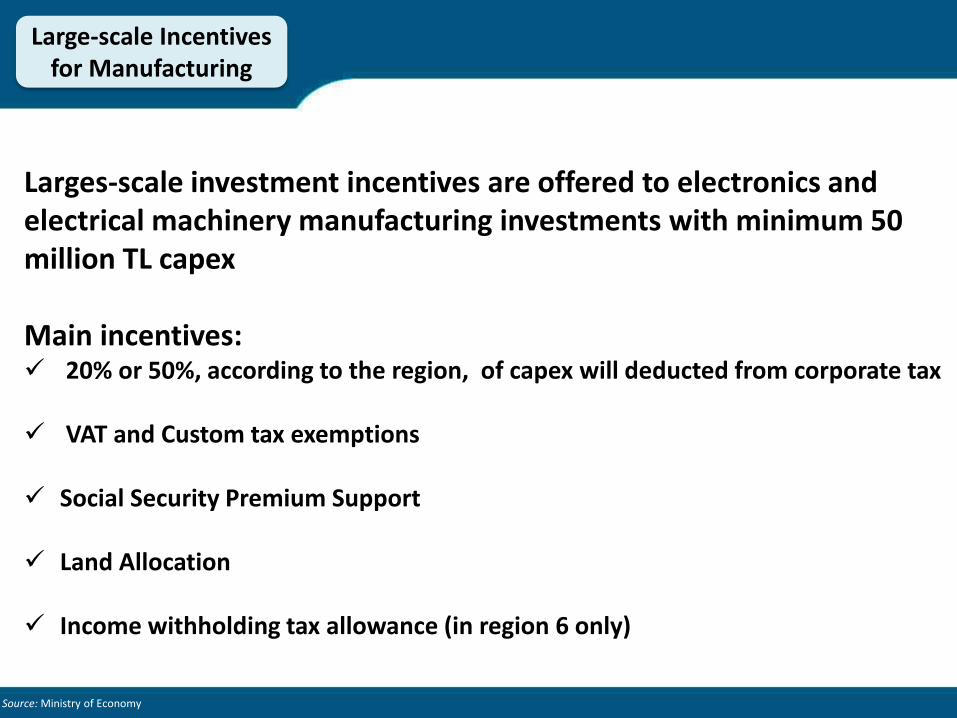

Source: Ministry of Economy

Larges-scale investment incentives are offered to electronics and electrical machinery manufacturing investments with minimum 50 million TL capex Main incentives: 20% or 50%, according to the region, of capex will deducted from corporate tax

VAT and Custom tax exemptions

Social Security Premium Support

Land Allocation

Income withholding tax allowance (in region 6 only)

Large-scale Incentives for Manufacturing

Investments in the manufacturing of products and parts developed

through R&D projects incentivized by the Ministry of Science, Industry

and Technology, TUBİTAK and Small and Medium Enterprises

Development Organization (KOSGEB)

… are deemed as priority investments and incentivized accordingly…

Main incentives: 30% or 40%, according to the region, of capex will deducted from corporate tax

VAT and Custom tax exemptions

Social Security Premium Support

Land Allocation

Income withholding tax allowance (in region 6 only)

Priority Incentives for Manufacturing

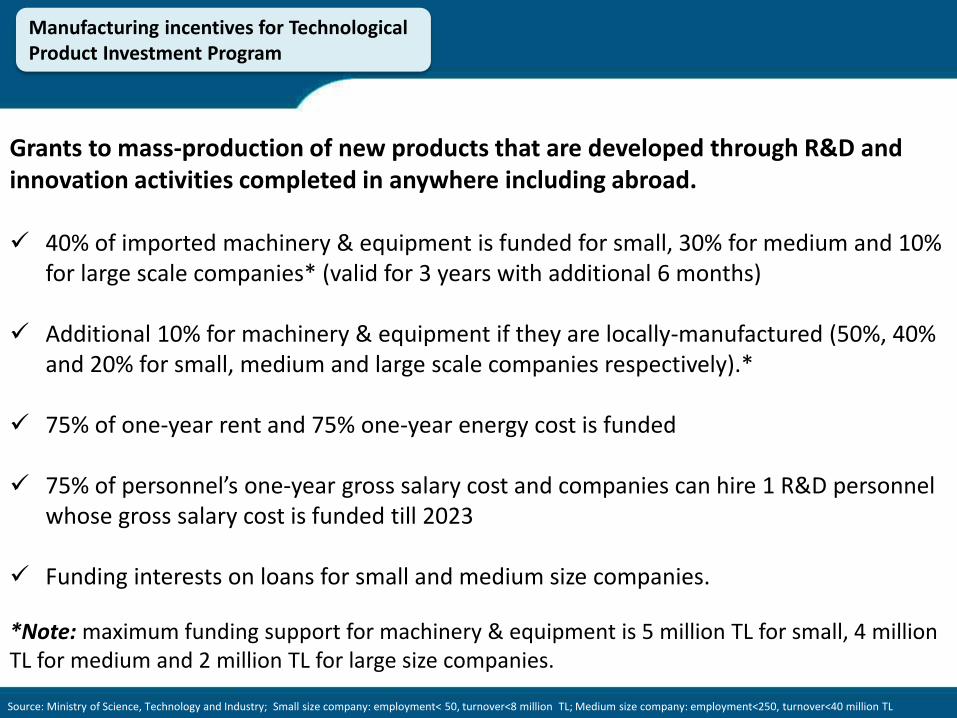

Source: Ministry of Economy

Grants to mass-production of new products that are developed through R&D and innovation activities completed in anywhere including abroad. 40% of imported machinery & equipment is funded for small, 30% for medium and 10%

for large scale companies* (valid for 3 years with additional 6 months)

Additional 10% for machinery & equipment if they are locally-manufactured (50%, 40% and 20% for small, medium and large scale companies respectively).*

75% of one-year rent and 75% one-year energy cost is funded

75% of personnel’s one-year gross salary cost and companies can hire 1 R&D personnel whose gross salary cost is funded till 2023

Funding interests on loans for small and medium size companies.

*Note: maximum funding support for machinery & equipment is 5 million TL for small, 4 million TL for medium and 2 million TL for large size companies.

Source: Ministry of Science, Technology and Industry; Small size company: employment< 50, turnover<8 million TL; Medium size company: employment<250, turnover<40 million TL

Manufacturing incentives for Technological Product Investment Program

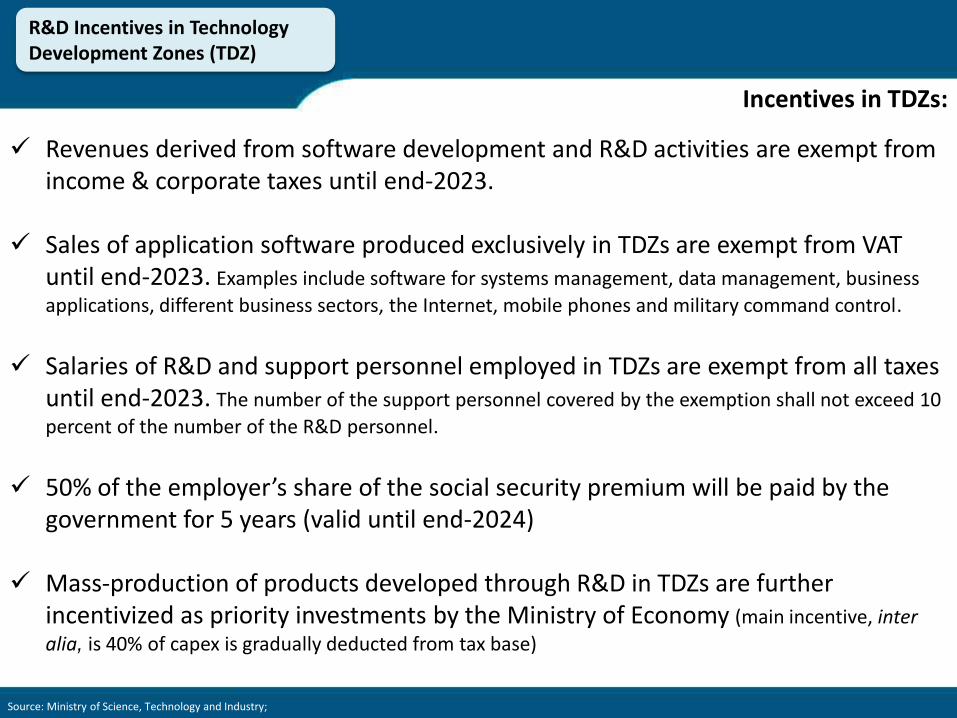

Revenues derived from software development and R&D activities are exempt from income & corporate taxes until end-2023.

Sales of application software produced exclusively in TDZs are exempt from VAT until end-2023. Examples include software for systems management, data management, business

applications, different business sectors, the Internet, mobile phones and military command control.

Salaries of R&D and support personnel employed in TDZs are exempt from all taxes

until end-2023. The number of the support personnel covered by the exemption shall not exceed 10

percent of the number of the R&D personnel.

50% of the employer’s share of the social security premium will be paid by the

government for 5 years (valid until end-2024)

Mass-production of products developed through R&D in TDZs are further incentivized as priority investments by the Ministry of Economy (main incentive, inter

alia, is 40% of capex is gradually deducted from tax base)

Incentives in TDZs:

R&D Incentives in Technology Development Zones (TDZ)

Source: Ministry of Science, Technology and Industry;

R&D Incentives valid until end-2024

Objective: To establish R&D centers in Turkey Condition: Employing minimum 30 R&D personnel 100 % deduction of R&D expenditure from the tax base, if 500 R&D staff employed, then in

addition to the 100% deduction, half of the R&D expenditure increase incurred in the operational year compared to the previous year is also deducted.

Income withholding tax exemption for 80% of staff ‘s salaries are exempted from income withholding tax; for staff with PhD 90% exemption (until end-2023.)

50% social security premium exemption for employers for 5 years

Stamp duty exemption

Mass-production of products developed in R&D centers are further incentivized as priority investments by the Ministry of Economy (main incentive, inter alia, is 40% of capex is gradually deducted from tax base)

If employment is less than 30 R&D staff, still R&D expenditures are deducted from tax base.

R&D Incentives for R&D Centers

Source: Ministry of Science, Technology and Industry;

R&D Incentives for SMEs

Source: KOSGEB

R&D and Innovation Program Upper

Limit (TL) Support Rate (%)

Rental Support 12.000 75

Machinery – Equipment, Hardware, Raw Material, Software and Service Purchase Cost Support 100.000 75

Machinery – Equipment, Hardware, Raw Material, Software and Service Purchase Cost Support (with payback)

200.000 75

Personnel Cost Support 100.000 75

Initial Support 100.000 100

Pro

ject

Dev

elo

pm

ent

Sup

po

rt

Project Consulting Support 25.000

75

Training Support 5.000

Industrial and Intellectual Property Rights Support 25.000

Project Promotion Support 5.000

Foreign Convention/Conference/Exhibition Visit/Technologic Cooperation Visit Support 15.000

Test, Analyses and Certification Support 25.000

Industrial Implementation Program

Rental Support 18.000 75

Staff Costs Support 100.000 75

Machinery – Equipment, Hardware, Consumables, Software and Design Cost Support 150.000 75

Machinery– Equipment, Hardware, Consumables Software and Design Cost Support (with Payback) 200.000 75

Source: TUBİTAK

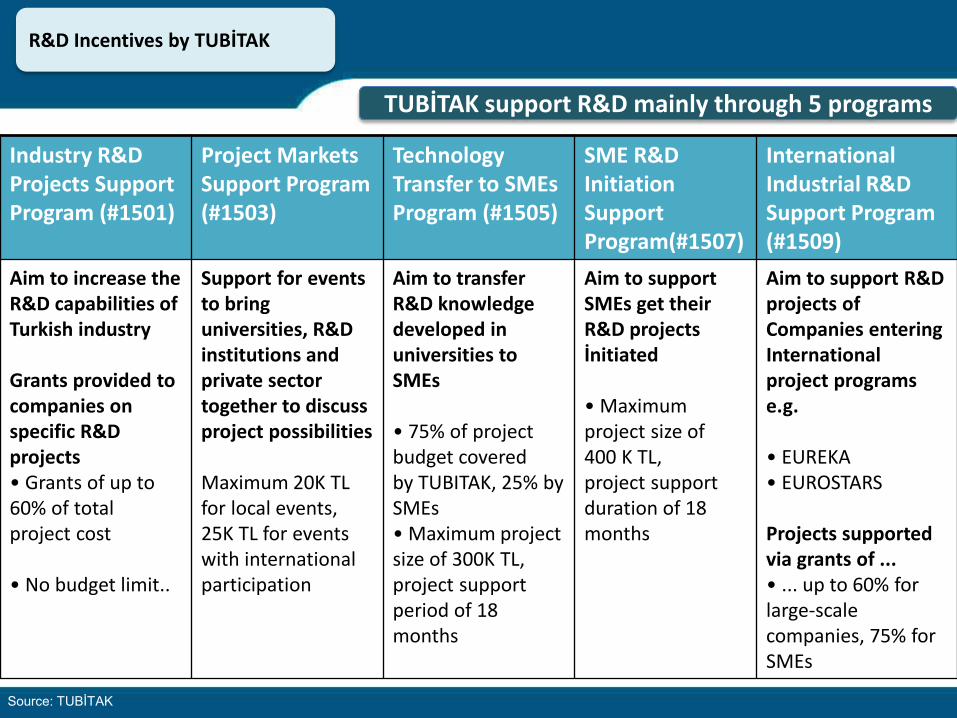

Industry R&D Projects Support Program (#1501)

Project Markets Support Program (#1503)

Technology Transfer to SMEs Program (#1505)

SME R&D Initiation Support Program(#1507)

International Industrial R&D Support Program (#1509)

Aim to increase the R&D capabilities of Turkish industry Grants provided to companies on specific R&D projects • Grants of up to 60% of total project cost • No budget limit..

Support for events to bring universities, R&D institutions and private sector together to discuss project possibilities Maximum 20K TL for local events, 25K TL for events with international participation

Aim to transfer R&D knowledge developed in universities to SMEs • 75% of project budget covered by TUBITAK, 25% by SMEs • Maximum project size of 300K TL, project support period of 18 months

Aim to support SMEs get their R&D projects İnitiated • Maximum project size of 400 K TL, project support duration of 18 months

Aim to support R&D projects of Companies entering International project programs e.g. • EUREKA • EUROSTARS Projects supported via grants of ... • ... up to 60% for large-scale companies, 75% for SMEs

TUBİTAK support R&D mainly through 5 programs

R&D Incentives by TUBİTAK

THANK YOU