tsx eqb eqb.pr · · 2018-03-011 fourth quarter report tsx eqb eqb.pr.c 2017. q4. canada’s...

TRANSCRIPT

1

FourthQuarterReport

T S X E Q BE Q B . P R . C

2017Q4

Canada’s Challenger Bank. Money Well Banked.For the three and twelve months ended December 31, 2017

2

Forward-Looking Statements

Certain forward-looking statements may be made in this presentation, including statements regarding possible future business, financing and growth objectives. Forward-looking statements include, but are not limited to, statements relating to our financial performance objectives, vision and strategic goals, the economic and market review and outlook, the regulatory environment in which we operate, the outlook and priorities for each of our business lines, the risk environment including our liquidity and funding risk, and statements by our Chief Executive Officer and Chief Financial Officer. The forward-looking information contained herein is presented for the purpose of assisting the holders of our securities and financial analysts in understanding our financial position and results of operations as at and for the periods ended on the dates presented, as well as our financial performance objectives, vision and strategic goals, and may not be appropriate for other purposes. Forward-looking statements are typically identified by words such as “believe”, “expect”, “foresee”, “forecast”, “anticipate”, “intend”, “estimate”, “goal”, “plan” and “project” and similar expressions of future or conditional verbs such as “will”, “may”, “should”, “could” or “would”. Investors are cautioned that such forward-looking statements involve risks and uncertainties detailed from time to time in the Company’s periodic reports filed with Canadian regulatory authorities. Many factors could cause actual results, performance or achievements to be materially different from any future results, performance or achievements that may be expressed or implied by such forward-looking statements. Equitable Group Inc. does not undertake to update any forward-looking statements, oral or written, made by itself or on its behalf except in accordance with applicable securities laws.

3

Demonstrating Success As Canada’s Challenger Bank™

Major 2017 Milestones

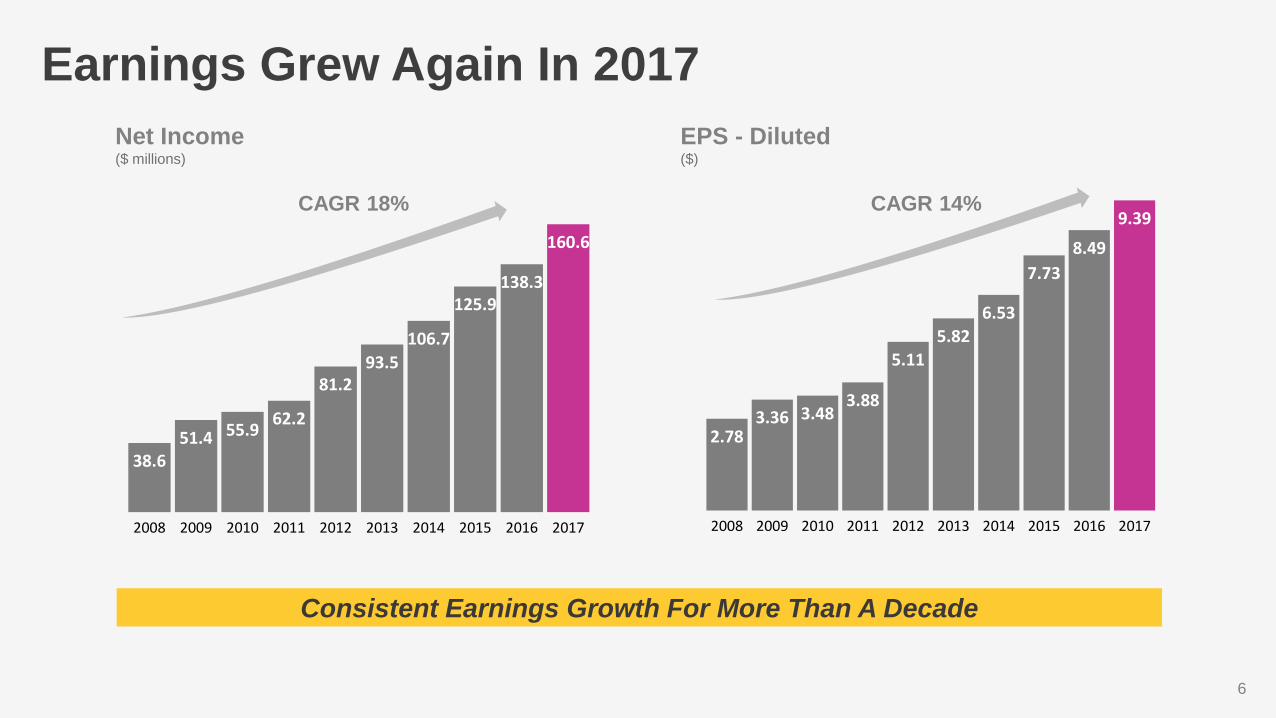

Record Annual Earnings of $160.6M

Record Assets Under Management of $24.6B

Record Deposit Principal of $11.0B

4

8.7 9.0 9.29.7 9.9 10.0

10.511.0

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q42016 2017

Maintaining the Confidence of Our DepositorsDeposit Principal Balances($ billions)

14% Growth Over 2016 With EQ Bank Ahead 53%

5

High Quality And Measured Asset GrowthTotal Originations($ billions)

Mortgages Under Management($ billions)

0.9

1.31.4

1.31.2

1.1

1.5

1.20.7

0.70.7 0.9

0.4 0.5

0.5

0.5

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Securitization FinancingCore Lending

17.718.7

19.921.0 21.7 22.0 22.8 23.2

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q42016 20172016 2017

Originations Down Primarily In Lower Margin Securitization

Financing Business

6

Earnings Grew Again In 2017

Consistent Earnings Growth For More Than A Decade

2.783.36 3.48

3.88

5.115.82

6.53

7.738.49

9.39

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

38.651.4 55.9 62.2

81.293.5

106.7

125.9138.3

160.6

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

EPS - Diluted ($)

Net Income($ millions)

CAGR 18% CAGR 14%

7

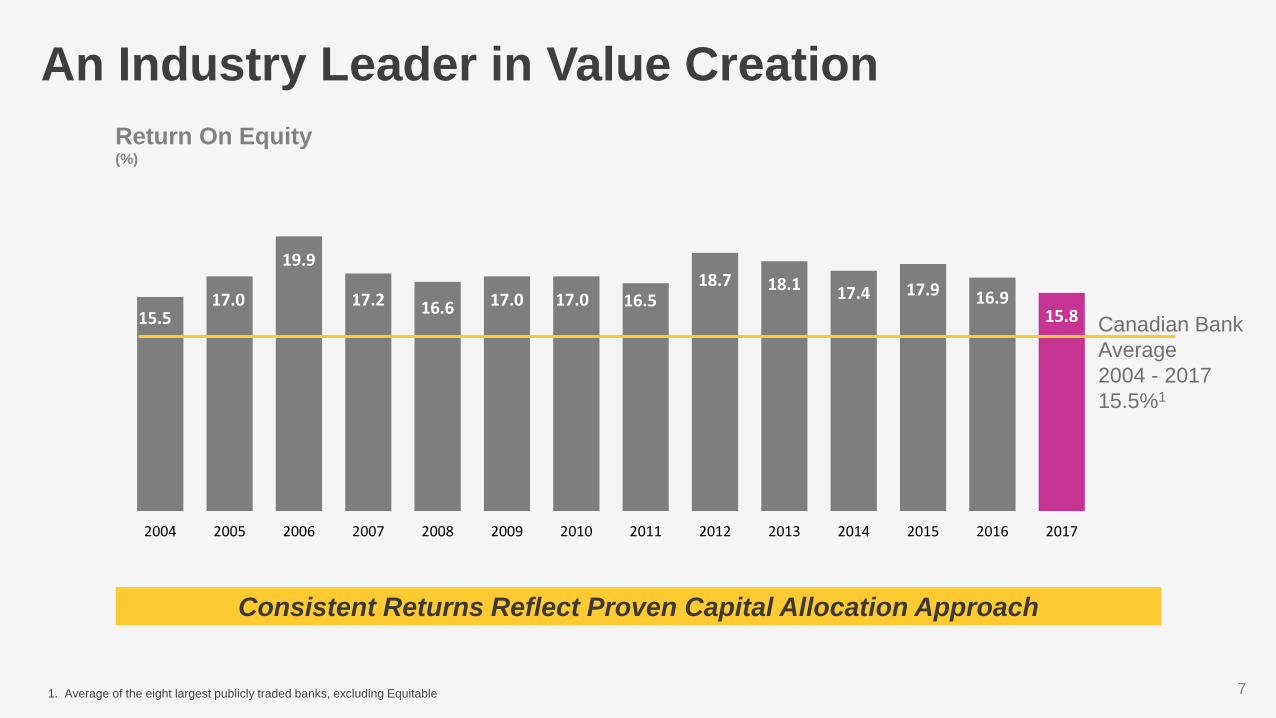

An Industry Leader in Value Creation

Consistent Returns Reflect Proven Capital Allocation Approach

15.517.0

19.9

17.2 16.6 17.0 17.0 16.518.7 18.1 17.4 17.9 16.9

15.8

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Canadian Bank Average 2004 - 201715.5%1

Return On Equity(%)

1. Average of the eight largest publicly traded banks, excluding Equitable

8

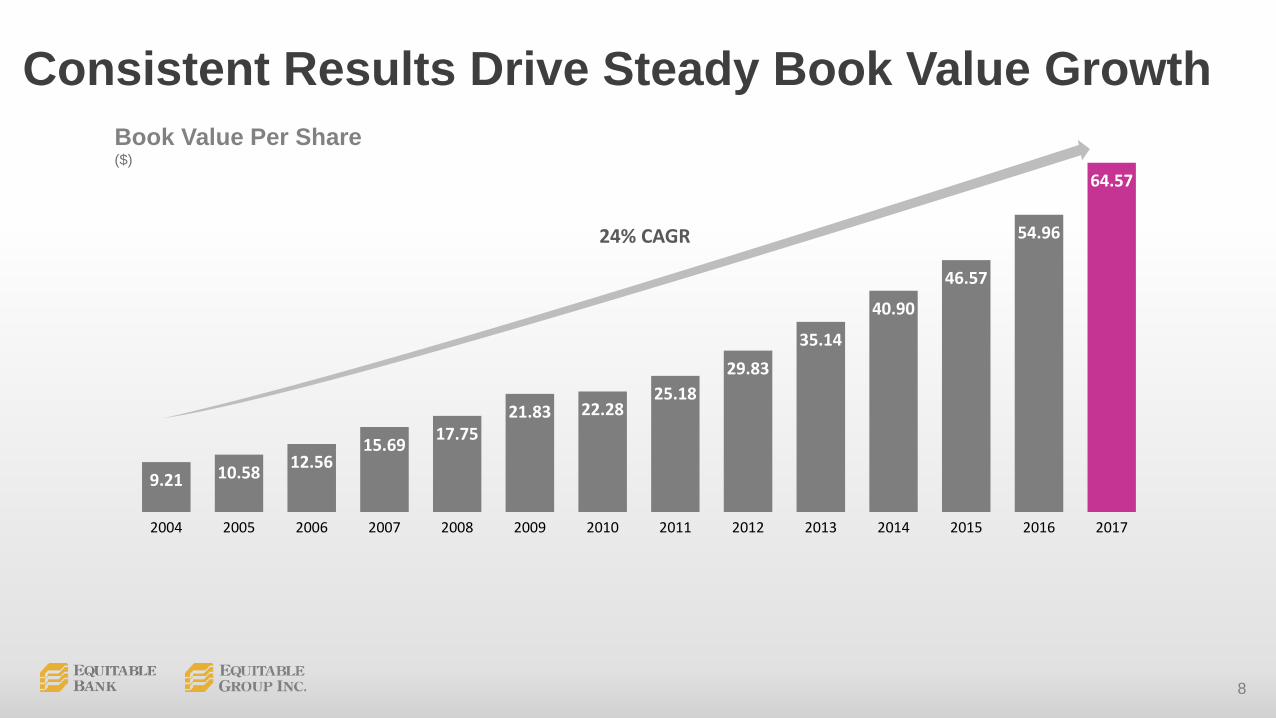

9.21 10.58 12.5615.69 17.75

21.83 22.2825.18

29.8335.14

40.90

46.57

54.96

64.57

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

24% CAGR

Book Value Per Share ($)

Consistent Results Drive Steady Book Value Growth

9

0.260.25

0.240.23

0.220.21

0.200.19

0.180.17

0.160.15

0.14

0.12

Dividend Grows For The 15th Time In 10 Years

2011 2012 2013 2014 2015 2016 2017 2018

Dividend Per Common Share$

Common Share Dividend Increased 4% Effective With Payment In April 2018

10

35.2

41.7 43.438.9 37.9

40.4

Q3 Q4 Q1 Q2 Q3 Q4

Q4 EPS Includes $0.32 Of Costs Related To Liquidity Protection

Re-Establishing Upward Quarterly Earnings Trend

2.16

2.56 2.542.28 2.21

2.36

Q3 Q4 Q1 Q2 Q3 Q4

Earnings Per Share Diluted($)

Net Income($ millions)

2016 20172016 2017

7% 7%

11

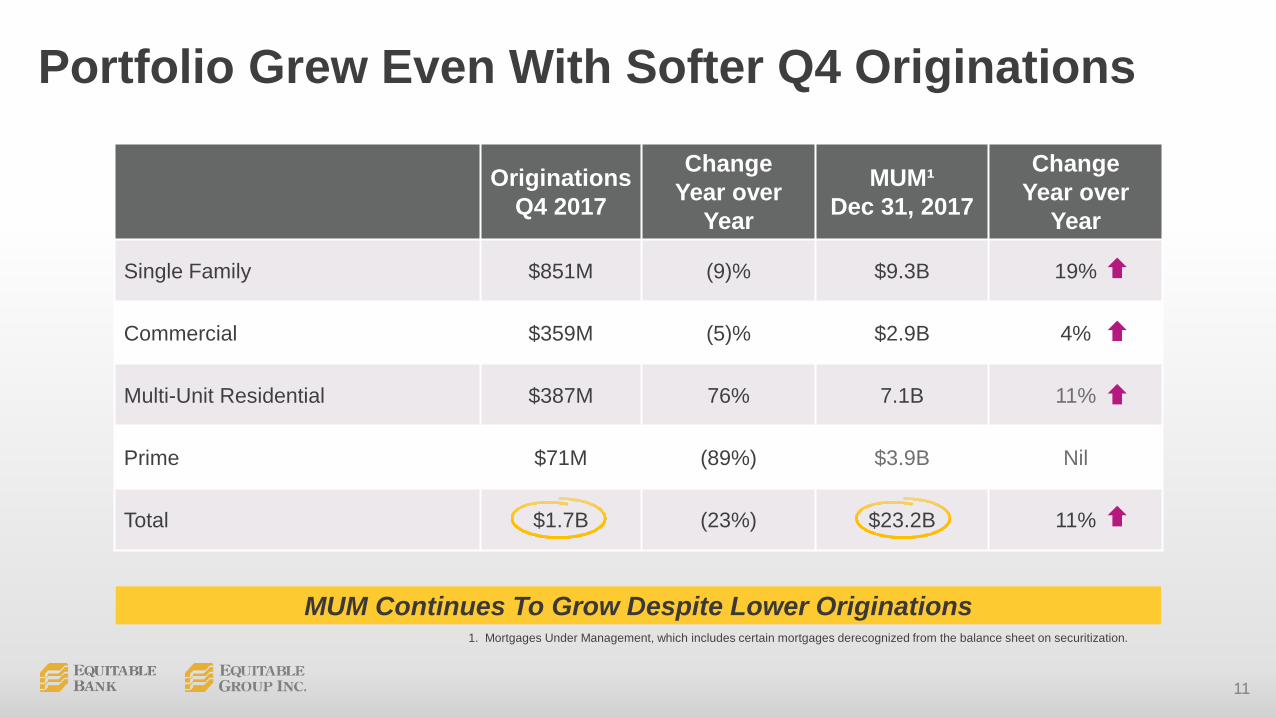

Portfolio Grew Even With Softer Q4 Originations

OriginationsQ4 2017

ChangeYear over

Year

MUM¹Dec 31, 2017

ChangeYear over

Year

Single Family $851M (9)% $9.3B 19%

Commercial $359M (5)% $2.9B 4%

Multi-Unit Residential $387M 76% 7.1B 11%

Prime $71M (89%) $3.9B Nil

Total $1.7B (23%) $23.2B 11%

MUM Continues To Grow Despite Lower Originations1. Mortgages Under Management, which includes certain mortgages derecognized from the balance sheet on securitization.

12

0.8 0.91.1

0.9

3.6 3.7

Q1 Q2 Q3 Q4 2016 2017

Alternative Single Family Lending

4.3 4.6 4.95.4 5.7 5.9 6.2 6.4

6.87.2 7.5

7.9 8.2 8.59.1 9.3

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q42014 2015 2016 2017

Mortgage Principal($ billions)

Mortgage Originations($ billions)

Annual Originations An All-Time Record $3.7B

2017

13

0.4

0.2

0.4 0.4

1.3 1.3

Q1 Q2 Q3 Q4 2016 2017

Commercial Lending

4.3 2.3 2.3 2.3 2.3 2.3 2.2 2.2 2.3 2.42.7 2.8

3.02.8 2.9 2.9

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Mortgage Principal($ billions)

Mortgage Originations($ billions)

Strong and Growing Customer Relationships Creating Opportunity

2014 2015 2016 2017 2017

14

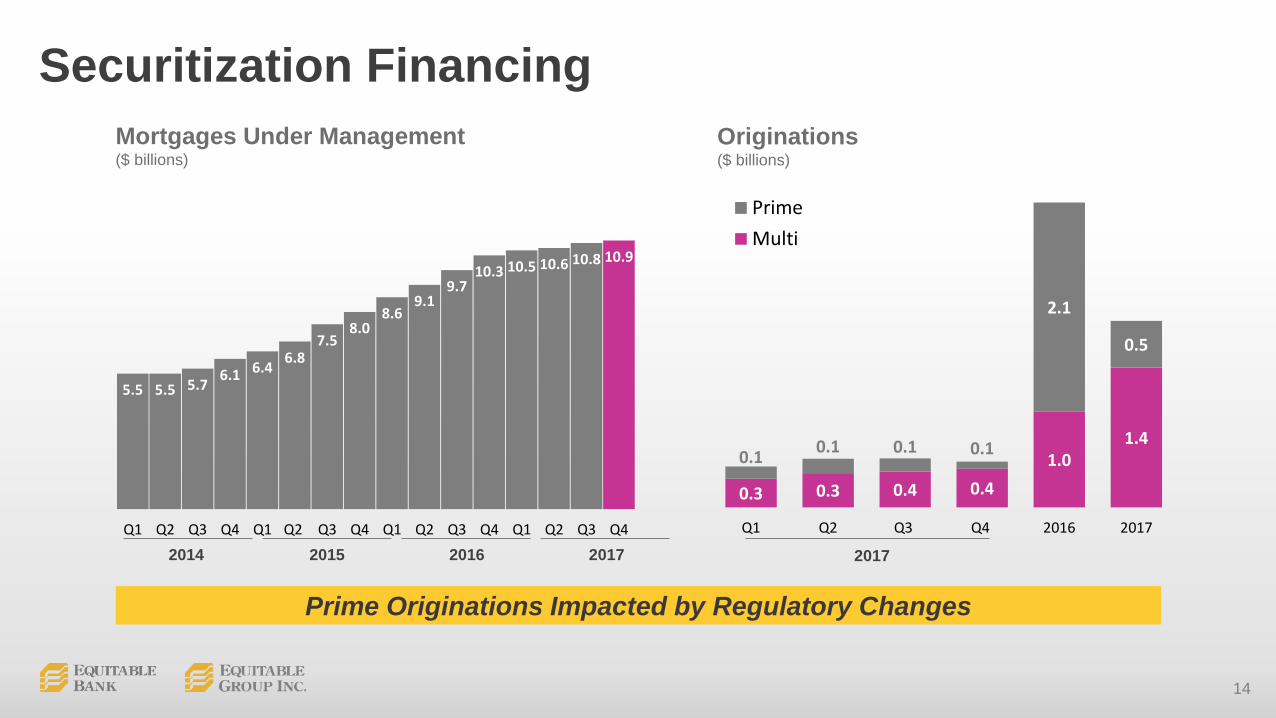

0.3 0.3 0.4 0.41.0

1.40.1 0.1 0.1 0.1

2.1

0.5

Q1 Q2 Q3 Q4 2016 2017

PrimeMulti

Securitization Financing

5.5 5.5 5.7 6.1 6.4 6.87.5

8.08.6

9.19.7

10.3 10.5 10.6 10.8 10.9

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Mortgages Under Management($ billions)

Originations($ billions)

Prime Originations Impacted by Regulatory Changes

2014 2015 2016 2017 2017

15

0.0%

0.1%

0.2%

0.3%

0.4%

0.5%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Best in Class Credit Performance Continues

Well Protected By Allowance for Credit Losses

EQB

Comparator Group1

1. Represents eight largest publicly traded banks

Net Realized Credit Losses as a % of Total Loans

Net impaired mortgage assets $22.5M (down from Q3 2017 and Q4 2016) and now only 0.12% of total mortgage book

Allowance for credit losses to total mortgage assets ratio of 0.17% much higher than Bank’s average loss rate of 0.04% over past decade

PCL of $1.5M (1 basis point of average loan balances) reflects quality of book

16

5.4

14.816.3

Growing While Maintaining Solid Capital Ratios

December 31, 2017 (%)

Basel III minimumTotal Capital level of 10.5%Basel III

minimum CET1 target of 7.0%

Full compliance with new standard

Leverage Ratio CET1 Total Capital

17

The Cost of Adding Downside Protection

Q2 EPS Impact

Q3 EPS Impact

Q4 EPS Impact

Backstop Funding Facility $0.06 $0.24 $0.24

Insurance premium amortization, net of associated funding benefits $0.20 $0.18 $0.08

EQ Bank marketing campaign $0.12 nil nil

Total $0.38 $0.42 $0.32

Impact Expected to Dissipate To ~$5M Per Quarter in 2018

18

2.55 2.62 2.56 2.64 2.50 2.55 2.60 2.64 2.55 2.412.17 2.33

0.29 0.31 0.34 0.22 0.31 0.22 0.19 0.24 0.22 0.30 0.25 0.24

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Core Lending Securitization Financing

Margin Trends

Net Interest Margin – TEB

2015 2016 2017

Expect NII To Grow 8-10% in 2018 Due To Asset Growth

TotalNIM 1.74 1.79 1.73 1.69 1.62 1.61 1.64 1.70 1.66 1.63 1.47 1.59

Total NIM 12 basis higher sequentially mainly due to higher Core Lending NIM

Core Lending NIM up due to lower liquidity event costs and mid-2017 pricing changes

Expect slightly lower Total and Core NIMs in 2018

19

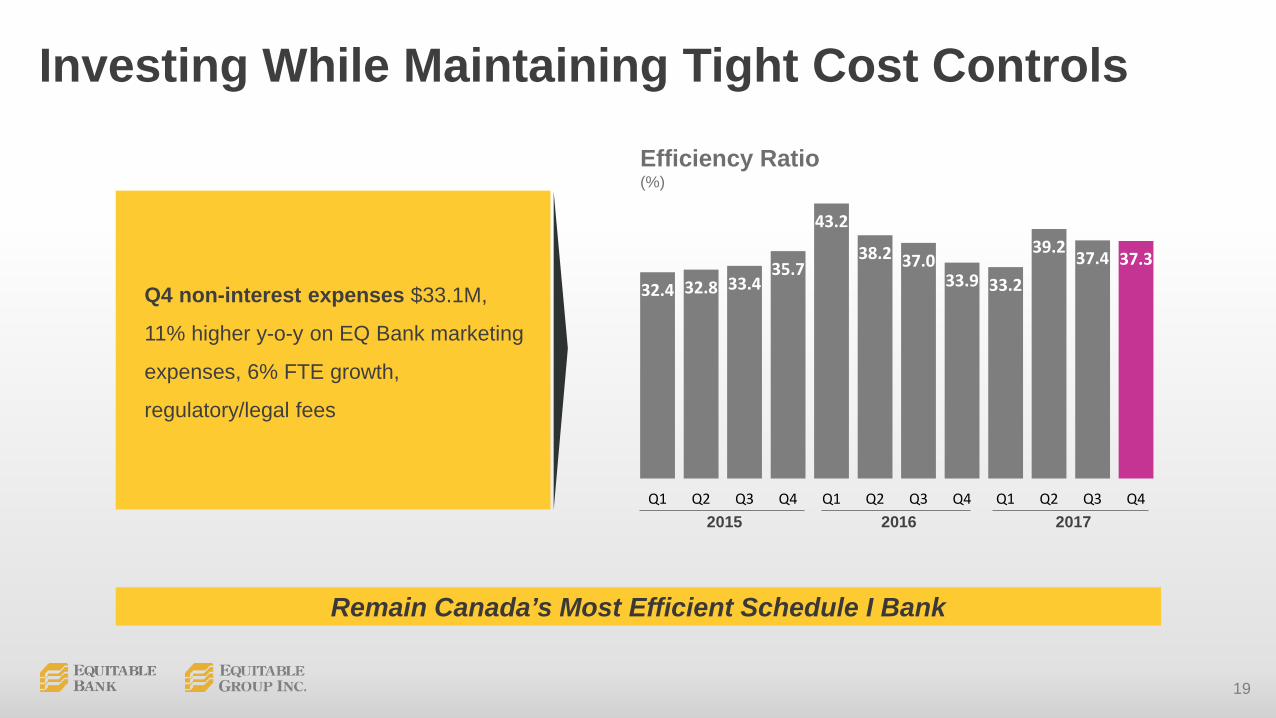

2015 2016 2017

Investing While Maintaining Tight Cost Controls

32.4 32.8 33.435.7

43.2

38.2 37.033.9 33.2

39.2 37.4 37.3

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Remain Canada’s Most Efficient Schedule I Bank

Efficiency Ratio(%)

Q4 non-interest expenses $33.1M,

11% higher y-o-y on EQ Bank marketing

expenses, 6% FTE growth,

regulatory/legal fees

20

Strong Challenger Bank Fundamentals

Disciplined Capital Deployment

National Distribution Presence

Responsive Service

EQ BankCanada's Leading Digital Bank

21

Enhancing Single Family Service

New 24/7 Self-Service Technology

Platform

22

Leverage Experience to Safely Grow

Commercial Assets

Capital Deployment in Other Lending Opportunities

23

Equity Release Product Overview

Target Market

Distribution

Brand

Loan Parameters

• Homeowners 55 years and older• Residents of larger urban centers, such as Toronto or Calgary

• Through Canada’s vibrant mortgage broker community

• Maximum LTV at origination of 40%• Term of up to 5 years• Floating interest rate (based off prime)

• PATH Home Plan branding• Delivers message of equity release being a natural part of an overall financial plan

24

Why and Why Now?Attractive Market

Favorable Competitive Landscape

Diversification Platform

Synergies with Existing Business

• Targets the growing demographic of aging Canadians

• Addresses increasing gap between retirement savings and needs

• Provides an option for borrowers if recent regulatory changes reduce availability of traditional mortgage credit

• New asset class but adjacent to existing businesses

• Broader range of products enhances our value proposition to the broker community

• Leverages existing capabilities and financial strength

• Cash flow from current operations can finance reverse mortgage investments

• Systems, corporate centre, and funding channels

• Relationships with brokers

• Robust risk management framework

• Only one incumbent regulated player

• Market size will likely make it appealing to only mid-sized FIs; niche market not addressed by big-6

25

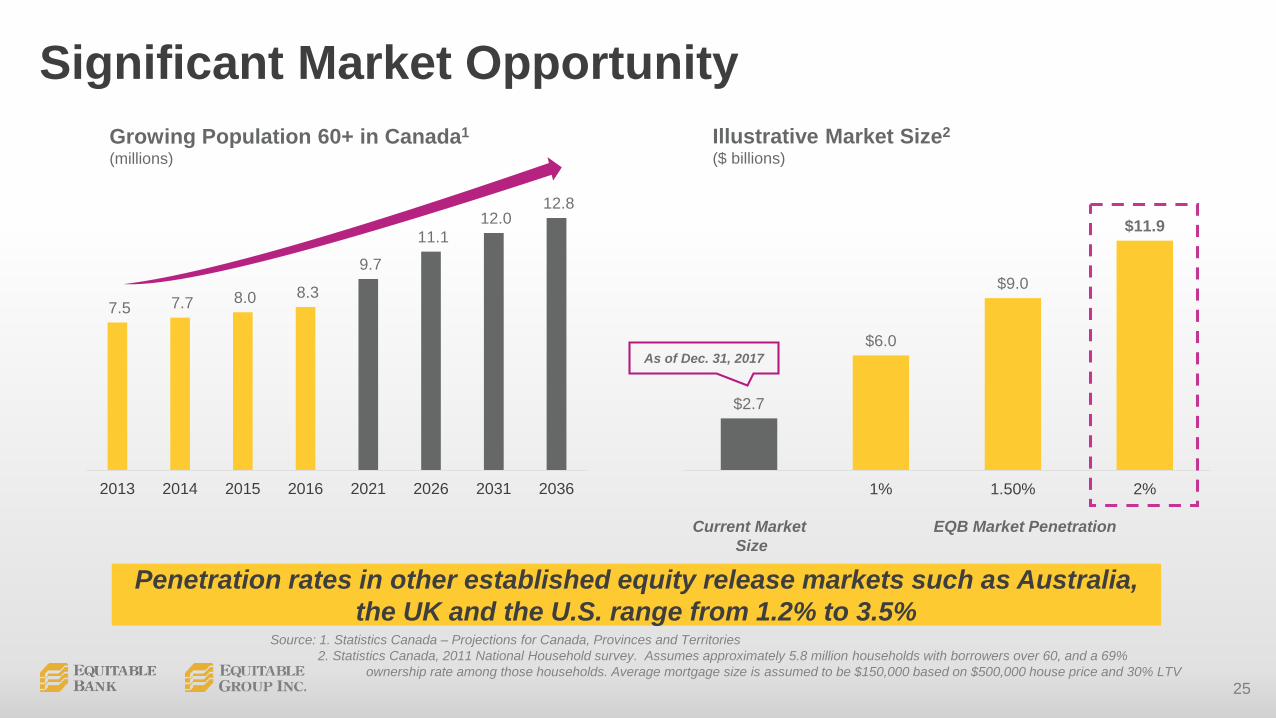

Significant Market Opportunity

Source: 1. Statistics Canada – Projections for Canada, Provinces and Territories2. Statistics Canada, 2011 National Household survey. Assumes approximately 5.8 million households with borrowers over 60, and a 69%

ownership rate among those households. Average mortgage size is assumed to be $150,000 based on $500,000 house price and 30% LTV

Growing Population 60+ in Canada1

(millions)Illustrative Market Size2

($ billions)

Penetration rates in other established equity release markets such as Australia, the UK and the U.S. range from 1.2% to 3.5%

$2.7

$6.0

$9.0

$11.9

1% 1.50% 2%

EQB Market Penetration

7.5 7.7 8.0 8.3

9.7

11.1 12.0

12.8

2013 2014 2015 2016 2021 2026 2031 2036

Current MarketSize

As of Dec. 31, 2017

26

Expanding Our Challenger Bank Vision