trust holding limited consolidated financial statements … consolidated... · trust holding...

TRANSCRIPT

TRUST HOLDING LIMITED

CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER, 2009

Trust Holding Limited – Consolidated Financial Statements 2009

C o n t e n t s

Page

Directors' report 1

Auditors' report 2 - 3

Consolidated statement of comprehensive income 4

Consolidated revenue account 5

Consolidated statement of financial position 6

Statement of changes in equity 7 - 8

Consolidated statement of changes in cash flows 9

Notes to the consolidated financial statements 10 – 24

Trust Holding Limited – Consolidated Financial Statements 2009

1

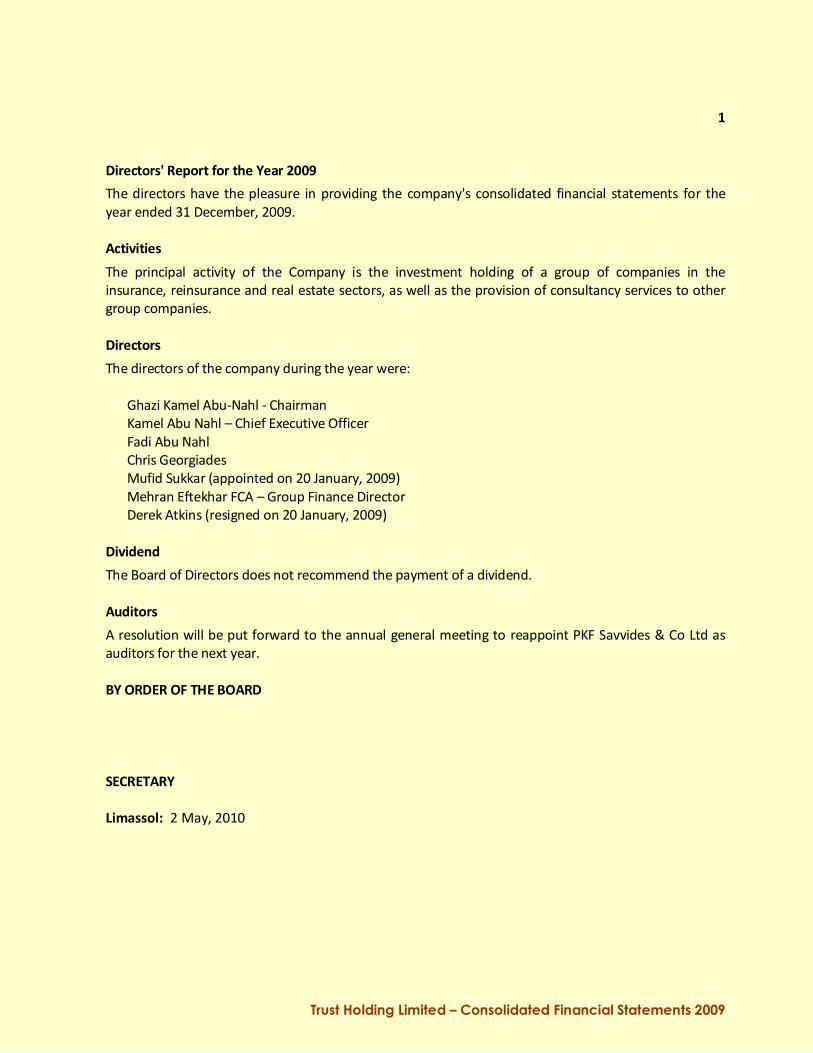

Directors' Report for the Year 2009 The directors have the pleasure in providing the company's consolidated financial statements for the

year ended 31 December, 2009.

Activities The principal activity of the Company is the investment holding of a group of companies in the

insurance, reinsurance and real estate sectors, as well as the provision of consultancy services to other

group companies.

Directors The directors of the company during the year were:

Ghazi Kamel Abu-Nahl - Chairman

Kamel Abu Nahl – Chief Executive Officer

Fadi Abu Nahl

Chris Georgiades

Mufid Sukkar (appointed on 20 January, 2009)

Mehran Eftekhar FCA – Group Finance Director

Derek Atkins (resigned on 20 January, 2009)

Dividend The Board of Directors does not recommend the payment of a dividend.

Auditors A resolution will be put forward to the annual general meeting to reappoint PKF Savvides & Co Ltd as

auditors for the next year.

BY ORDER OF THE BOARD

SECRETARY

Limassol: 2 May, 2010

PKF Savvides & Co Limited

Accountants & business advisers

Limassol office

PKF Savvides & Co Limited 229 Arch. Makarios Ave., Meliza Court 3105 Limassol Cyprus

Tel + 0357 25 868000 Fax + 357 25 587871 Email [email protected] www.pkf.com.cy Nicosia Office PKF / ATCO Limited 2 Limassol Avenue, Aluminium Tower, Floors 2

nd,3

rd & 4

th 2003 Nicosia Cyprus

Tel + 0357 22 462727 Fax + 357 22 339866 Email [email protected] www.atconet.net

The list of directors’ names of each firm is open for inspection at their principal place of business.

Pannell Kerr Forster associated offices covering Africa, Australia, Canada, Caribbean, Central and South America, Europe, Middle and Far East, New Zealand, United States of America.

Trust Holding Limited – Consolidated Financial Statements 2009

2

AUDITORS' REPORT TO THE MEMBERS OF TRUST HOLDING LIMITED

Report on the consolidated financial statements We have audited the consolidated financial statements of Trust Holding Limited (the “Company”) on pages 4 to 25, which comprise the consolidated statement of financial position as at 31 December 2009, and the consolidated statement of comprehensive income, consolidated statement of changes in equity and consolidated statement of changes in cash flows for the year then ended, and a summary of significant accounting policies and other explanatory notes.

Board of Directors’ Responsibility for the Consolidated Financial Statements

The Company’s Board of Directors is responsible for the preparation and fair presentation of these financial statements in accordance with International Financial Reporting Standards as adopted by the European Union (EU) and International Financial Reporting Standards as issued by the International Accounting Standards Board (IASB). This responsibility includes: designing, implementing and maintaining internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error; selecting and applying appropriate accounting policies; and making accounting estimates that are reasonable in the circumstances.

Auditor’s Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. This report is made solely to the Company’s members, as a body. Our audit work has been undertaken so that we might state to the Company’s members those matters we are required to state to them in an auditor’s report and for no other purpose. To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other than the Company and the Company’s members as a body, for our audit work, for this report, or for the opinions we have formed. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by the Board of Directors, as well as evaluating the overall presentation of the financial statements.

Trust Holding Limited – Consolidated Financial Statements 2009

3

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the consolidated financial statements give a true and fair view of the financial position of Trust Holding Limited as of 31 December 2009, and of its financial performance and its cash flows for the year then ended in accordance with International Financial Reporting Standards as adopted by the EU and International Financial Reporting Standards as issued by the IASB and the requirements of the Cyprus Companies Law, Cap 113.

Report on Other Legal Requirements

Pursuant to the requirements of the Companies Law, Cap. 113 we report the following:

• We have obtained all the information and explanations we considered necessary for the purposes of our audit.

• In our opinion, proper books of account have been kept by the Company.

• The Company’s financial statements are in agreement with the books of account.

• In our opinion and to the best of our information and according to the explanations given to us, the financial statements give the information required by the Companies Law, Cap. 113, in the manner so required.

• In our opinion, the information given in the report of the Board of Directors on page 1 is consistent with the financial statements.

Other Matter

This report, including the opinion, has been prepared for and only for the Company’s members as a body in accordance with Section 156 of the Companies Law, Cap.113 and for no other purpose. We do not, in giving this opinion, accept or assume responsibility for any other purpose or to any other person to whose knowledge this report may come to.

Certified Public Accountants Limassol: 2 May 2010

Trust Holding Limited – Consolidated Financial Statements 2009

4

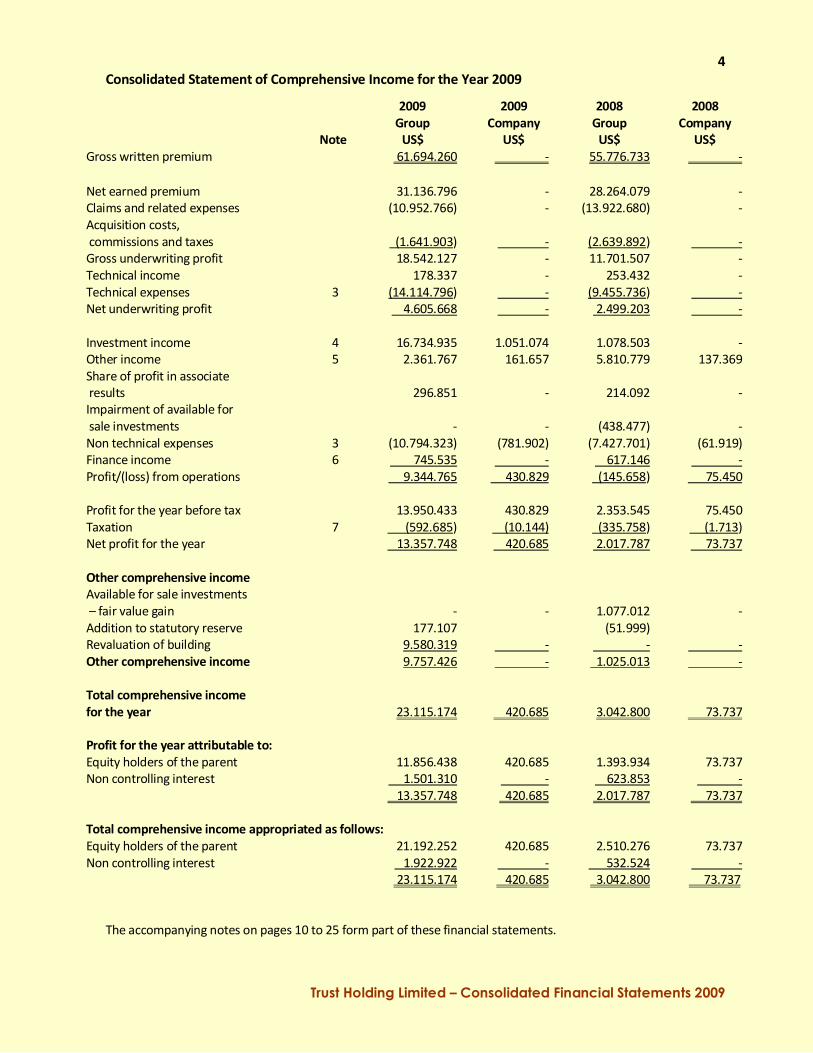

Consolidated Statement of Comprehensive Income for the Year 2009

Note

2009

Group

US$

2009

Company

US$

2008

Group

US$

2008

Company

US$

Gross written premium 61.694.260 - 55.776.733 -

Net earned premium 31.136.796 - 28.264.079 -

Claims and related expenses (10.952.766) - (13.922.680) -

Acquisition costs,

commissions and taxes (1.641.903) - (2.639.892) -

Gross underwriting profit 18.542.127 - 11.701.507 -

Technical income 178.337 - 253.432 -

Technical expenses 3 (14.114.796) - (9.455.736) -

Net underwriting profit 4.605.668 - 2.499.203 -

Investment income 4 16.734.935 1.051.074 1.078.503 -

Other income 5 2.361.767 161.657 5.810.779 137.369

Share of profit in associate

results 296.851 - 214.092 -

Impairment of available for

sale investments - - (438.477) -

Non technical expenses 3 (10.794.323) (781.902) (7.427.701) (61.919)

Finance income 6 745.535 - 617.146 -

Profit/(loss) from operations 9.344.765 430.829 (145.658) 75.450

Profit for the year before tax 13.950.433 430.829 2.353.545 75.450

Taxation 7 (592.685) (10.144) (335.758) (1.713)

Net profit for the year 13.357.748 420.685 2.017.787 73.737

Other comprehensive income

Available for sale investments

– fair value gain

- - 1.077.012 -

Addition to statutory reserve 177.107 (51.999)

Revaluation of building 9.580.319 - - -

Other comprehensive income 9.757.426 - 1.025.013 -

Total comprehensive income

for the year

23.115.174 420.685 3.042.800 73.737

Profit for the year attributable to:

Equity holders of the parent 11.856.438 420.685 1.393.934 73.737

Non controlling interest 1.501.310 - 623.853 -

13.357.748 420.685 2.017.787 73.737

Total comprehensive income appropriated as follows:

Equity holders of the parent 21.192.252 420.685 2.510.276 73.737

Non controlling interest 1.922.922 - 532.524 -

23.115.174 420.685 3.042.800 73.737

The accompanying notes on pages 10 to 25 form part of these financial statements.

Trust Holding Limited – Consolidated Financial Statements 2009

5

Consolidated Revenue Account for the Year 2009

2009 2009 2008 2008

Group Company Group Company

US$ US$ US$ US$

Insurance revenue Gross written premium 61.694.260 - 55.776.733 -

Outward reinsurance premium (29.903.516) - (27.002.451) -

Retained premium 31.790.744 - 28.774.282 -

Change in unearned premium (653.948) - (510.203) -

Net earned premium 31.136.796 - 28.264.079 -

Cost and expenses Gross claims paid (16.854.443) - (22.391.200) -

Claims recovered from reinsurers 5.539.439 - 8.631.211 -

Change in provision for outstanding

claims - Gross (2.072.622) - (645.724) -

Change in provision for outstanding

claims - Reinsurance 2.434.860 - 483.033 -

Claims and related expenses (10.952.766) - (13.922.680) -

Commissions and taxes paid (5.728.114) - (5.486.659) -

Commissions and taxes received

from reinsurers 3.700.312 - 2.989.052 -

Interest on premium reserve (1.700) - (1.380) -

Change in deferred acquisition cost 294.273 - 32.132 -

Change in unexpired risk reserve 77.389 - (163.531) -

Change in IBNR 15.937 - (9.506) -

Deferred acquisition costs, (1.641.903)

commissions and taxes - (2.639.892) -

Gross underwriting profit 18.542.127 - 11.701.507 -

Technical income 178.337 - 253.432 -

Technical expenses (14.114.796) - (9.455.736) -

Net underwriting profit 4.605.668 - 2.499.203 -

The accompanying notes on pages 10 to 25 form part of these financial statements.

Trust Holding Limited – Consolidated Financial Statements 2009

6

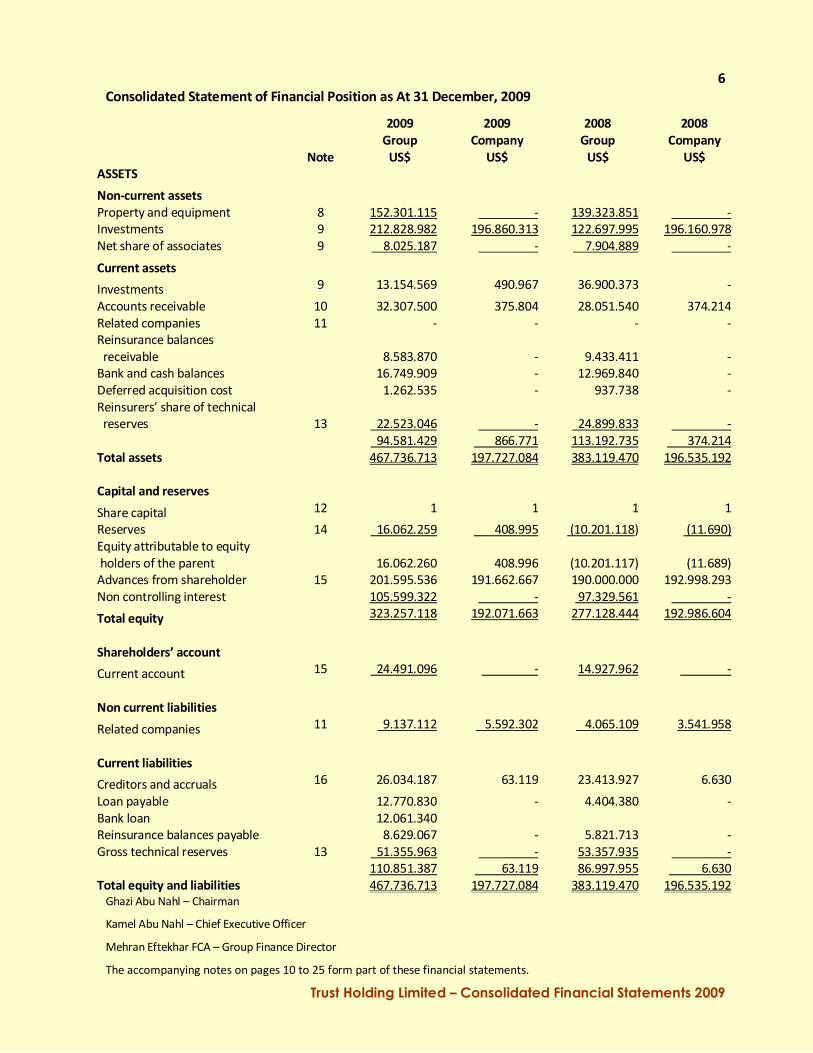

Consolidated Statement of Financial Position as At 31 December, 2009

2009 2009 2008 2008

Group Company Group Company

Note US$ US$ US$ US$

ASSETS Non-current assets

Property and equipment 8 152.301.115 - 139.323.851 -

Investments 9 212.828.982 196.860.313 122.697.995 196.160.978

Net share of associates 9 8.025.187 - 7.904.889 - Current assets Investments 9 13.154.569 490.967 36.900.373 -

Accounts receivable 10 32.307.500 375.804 28.051.540 374.214

Related companies 11 - - - -

Reinsurance balances

receivable 8.583.870 - 9.433.411 -

Bank and cash balances 16.749.909 - 12.969.840 -

Deferred acquisition cost 1.262.535 - 937.738 -

Reinsurers’ share of technical

reserves 13 22.523.046 - 24.899.833 -

94.581.429 866.771 113.192.735 374.214

Total assets 467.736.713 197.727.084 383.119.470 196.535.192

Capital and reserves Share capital 12 1 1 1 1

Reserves 14 16.062.259 408.995 (10.201.118) (11.690)

Equity attributable to equity

holders of the parent 16.062.260 408.996 (10.201.117) (11.689)

Advances from shareholder 15 201.595.536 191.662.667 190.000.000 192.998.293

Non controlling interest 105.599.322 - 97.329.561 - Total equity 323.257.118 192.071.663 277.128.444 192.986.604

Shareholders’ account Current account 15 24.491.096 - 14.927.962 -

Non current liabilities Related companies 11 9.137.112 5.592.302 4.065.109 3.541.958

Current liabilities Creditors and accruals 16 26.034.187 63.119 23.413.927 6.630

Loan payable 12.770.830 - 4.404.380 -

Bank loan 12.061.340

Reinsurance balances payable 8.629.067 - 5.821.713 -

Gross technical reserves 13 51.355.963 - 53.357.935 -

110.851.387 63.119 86.997.955 6.630

Total equity and liabilities 467.736.713 197.727.084 383.119.470 196.535.192 Ghazi Abu Nahl – Chairman

Kamel Abu Nahl – Chief Executive Officer

Mehran Eftekhar FCA – Group Finance Director

The accompanying notes on pages 10 to 25 form part of these financial statements.

Trust Holding Limited – Consolidated Financial Statements 2009

7

Statement of Changes in Equity as at 31 December, 2009

Share Retained

Capital Earnings Total

US$ US$ US$

a. Company

Balance 1 January, 2008 1 (85.427) (85.426)

Net profit for the year 73.737 73.737

Balance 1 January, 2009 1 (11.690) (11.689)

Total comprehensive income 420.685 420.685

Balance 31 December, 2009 1 408.995 408.996

The accompanying notes on pages 10 to 25 form part of these financial statements.

Trust Holding Limited – Consolidated Financial Statements 2009

8 Statement of Changes in Equity as at 31 December, 2009

Statutory Investment Property Exchange

Share General and other Revaluation Revaluation Merger Difference Non Controlling

Capital Reserve Reserves Reserve Reserve Reserve Reserve Interest Total

US$ US$ US$ US$ US$ US$ US$ US$ US$

b. Group

Balance 1 January, 2008 1 (85.427) - - - - - - (85.426)

Total comprehensive income - 1.393.934 75.852 1.040.490 - - - 532.524 3.042.800

Transfer to capital reserves - (159.956) 159.956 - - - - - -

Merger reserve due to

acquisition of subsidiaries - - - - - (3.341.839) - (3.341.839)

Minority interest on

acquisition of subsidiaries - - - - - - - 97.387.333 97.387.333

Exchange of differences - (2.219.402) (83.934) 4.452 - (6.985.243) - (590.296) (9.874.423)

Balance 1 January, 2009 1 (1.070.851) 151.874 1.044.942 - (10.327.082) - 97.329.561 87.128.445

Total comprehensive income - 11.856.438 119.547 - 9.216.267 - - 1.922.922 23.115.174

Dividend payable - (483.175) - - - - - 483.175 -

Transfer to capital reserves - (195.108) 195.108 - - - - (167.659) (167.659)

Exchange of differences - 1.411.483 104.107 (905.229) 2.949.189 113.402 1.881.347 6.031.323 11.585.622

At 31 December, 2009 1 11.518.787 570.636 139.713 12.165.456 (10.213.680) 1.881.347 105.599.322 121.661.582

The accompanying notes on pages 10 to 25 form part of these financial statements.

Trust Holding Limited – Consolidated Financial Statements 2009

9 Consolidated Statement of Changes in Cash Flows for the Year 2009

2009 2009 2008 2008

Group Company Group Company

US$ US$ US$ US$

Cash flows from operating activities:

Net profit before taxation 13.950.433 430.829 2.353.545 75.450

Adjustments for:

Exchange differences 2.699.384 - 6.666.457 -

Profit on fixed assets sold (131.367) - (1.042) -

Depreciation 1.801.594 - 1.152.100 -

Net share in associates results (120.298) - (7.533.038) -

Impairment in value of investment - 438.477 -

Profit on sale of investments (6.466.589) - (898.502) -

Interest expense 584.330

Decrease in provision for outstanding

claims and IBNR (net) (575.834) - (632.097) -

Increase in reserve for unearned premium (net) 625.852 - 744.962 -

Operating profit before working capital

changes 11.783.175 1.015.159 2.290.862 75.450

Accounts receivable and prepayments (4.334.981) 165.384 (5.881.755) (3.930.026)

Creditors and accruals (341.434) 1.940.563 1.401.980 6.657.314

Reinsurance balances 3.656.895 - (575.017) -

Related companies 5.072.003 - 40.150.700 -

Cash from operations 15.835.658 3.121.106 37.386.770 2.802.738

Income tax and exchange difference 2.448.030 (10.848) (90.952) -

Cash flows (used in)/from operating activities 18.283.688 3.110.258 37.295.818 2.802.738

Cash flows from investing activities

Acquisition of subsidiaries outflow on

acquisition - - (32.089.589) -

Purchase of fixed assets (3.693.534) - (8.952.431) -

Proceeds from sale of fixed assets 4.264.988 - 316.959 -

Acquisition of investments (net) (56.661.528) (1.190.302) (45.559.649) (196.160.978)

Net cash used in investing activities (56.090.074) (1.190.302) (86.284.710) (196.160.978)

Cash flows from financing activities

Issuance of share capital - 1 -

Loan payable 20.427.790 - 4.404.380 -

Dividend paid - -

Income received in advance - -

Shareholder’s accounts 21.158.665 (1.919.956) 46.316.242 190.000.000

Net cash from/(used in) financing activities 41.586.455 (1.919.956) 50.720.623 190.000.000

Net (decrease)/increase in cash and cash

equivalents 3.780.069 - 1.731.731 (3.358.240)

Cash and cash equivalents at beginning

of year 12.969.840 - 11.238.109 3.358.240

Cash and cash equivalents at end of year 16.749.909 - 12.969.840 -

The accompanying notes on pages 10 to 25 form part of these financial statements.

Trust Holding Limited – Consolidated Financial Statements 2009

10

Notes to the Consolidated Financial Statements 31 December, 2009

1. Introduction The company was incorporated in Cyprus on 20 March, 2007 as a private international limited liability

company in compliance with the provision of the Cyprus Companies Law Cap. 113. The main activity of

the company is the holding of investments and the provision of consultancy services to other group

companies.

2. Summary of principal accounting policies The most important principal accounting policies that are followed by the company are shown below: a. Basis of preparation of the Financial Statements The consolidated financial statements have been prepared in accordance with International Financial

Reporting Standards (IFRSs) as adopted by the European Union (EU). The consolidated financial

statements have been prepared under the historical cost convention.

The preparation of financial statements in conformity with IFRSs requires the use of certain critical

accounting estimates and requires management to exercise its judgement in the process of applying

the Group’s accounting policies. It also requires the use of assumptions that affect the reported

amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the

financial statements and the reported amounts of revenues and expenses during the reporting

period. Although these estimates are based on management’s best knowledge of current events and

actions, actual results may ultimately differ from those estimates. Basis of consolidation The Group consolidated financial statements comprise the financial statements of the parent

company Trust Holding Ltd and the financial statements of the subsidiary companies: Compass

Insurance S.A.L. registered in Lebanon, Trust Algeria Investment Company registered in Algeria and

its subsidiary companies Trust Real Estate registered in Algeria and Trust Industries, Trust Algeria

Insurance and Reinsurance registered in Algeria, Trust International Insurance Company (Palestine)

registered in Palestine, Trust Yemen Insurance & Reinsurance Co. (Y.S.C.) registered in Yemen, and

the activities of the associated companies Trust Libya Insurance Co. registered in Libya and Trust Syria

Insurance Co. (SASC) registered in Syria.

The consolidated financial statements have been prepared under IFRS but do not fall under the scope

of IFRS 3 in relation to the combination of the company and its subsidiaries. The acquisition of the

shares in subsidiaries is considered to be a combination of entities under common control.

In the absence of an IFRS that specifically applies to this transaction, the company has relied on the

hierarchy in IAS 8, paragraphs 10 -12 to decide on the appropriate accounting treatment. Specifically,

the following relevant hierarchy has been checked whether it applies to the transaction:

Trust Holding Limited – Consolidated Financial Statements 2009

11

Notes to the Consolidated Financial Statements 31 December, 2009

• IFRS and interpretations

• Definitions, recognition and measurement principles in the framework

• Recent pronouncements for other standard setting bodies with similar framework

• Other accounting literature

• Accepted industry practice The income and expenses of the subsidiaries are included in the consolidated financial statements

from the date of the combination. The underlying carrying amount of the assets and liabilities of the

subsidiaries have been recorded on the combination date. When the cost of acquiring of the shares

in the subsidiary companies is less that the respective underlying net assets value of this subsidiary,

the difference is credited to a merger reserve in the shareholder’s equity.

b. Reinsurance The reinsurance programme consists of proportional and non-proportional treaties. The accounting

for premiums due and claim recoveries is carried out periodically for proportional treaties. The

premium due for non-proportional cover is booked on the due date while claims recovery is

accounted as and when the priority is exceeded, taking outstanding claims reserve, if any, into

account.

Reinsurance premiums ceded and reinsurance recoveries on claims incurred are deducted from the

gross premiums written and claims costs respectively.

The company enters into contracts with other reinsurers for minimizing its financial exposure from

large claims. This arrangement results in reinsurance assets and liabilities which include amounts

recoverable from reinsurance companies for paid and unpaid losses, ceded unearned premiums and

reinsurance balances payable.

Amounts due to reinsurers are calculated in a manner consistent to the relative reinsurance contract.

Amounts recoverable from reinsurers are calculated with reference to the claims liabilities associated

with the reinsured risk.

Ceded premiums are recognised in the revenue account over the period that coverage is provided.

c. Revenue recognition Revenues earned by the company are recognised on the following basis: Premiums Premium income is recognised when Technical Reinsurance accounts or policy debit notes are issued

for contracts incepting in the financial year, as well as adjustments arising in the current financial

year for premiums receivable relating to business written in previous financial years.

Trust Holding Limited – Consolidated Financial Statements 2009

12

Notes to the Consolidated Financial Statements 31 December, 2009

Net commission earned This represents net commission earned on accepted and ceded reinsurance and profit commission

received from reinsurers on previous underwriting years in accordance with treaty conditions.

Commissions earned and paid are recognised when the Treaty Reinsurance accounts or policy debit

notes are issued.

Interest income Interest income is recognised on a time proportion basis using the effective interest method.

Dividend income Dividend income is recognised when the right to receive payment is established.

d. Claims paid Claims paid represent amounts settled during the year arising either from events during the year or

prior years and are charged to revenue account as incurred net of any recoveries.

e. Liability adequacy test At each balance sheet date, a liability adequacy test is performed, to ensure the adequacy of

unearned premiums net of related deferred acquisition costs, outstanding claims reserve and

Incurred But Not Reported reserves. Any inadequacy is immediately charged to the income

statement by establishing a provision.

f. Salvage, subrogation and other recoveries from third parties When the salvage amount is known at the time of claims settlement, the same is deducted from the

claim amount and the net amount is credited to the reinsured. If salvage recovery is done later, the

amount is credited to the claims paid account by debiting the reinsured account. As subrogation and

other recoveries will take place after claims settlement, they will be treated as above.

The corresponding refund to the reinsurers is recorded simultaneously with the accounting of

recoveries for salvage, subrogation and other recoveries from third parties.

g. Deferred acquisition costs Policy acquisition costs which relate to periods of risk that extend beyond the end of the financial year

are reported as deferred acquisition costs.

Trust Holding Limited – Consolidated Financial Statements 2009

13

Notes to the Consolidated Financial Statements 31 December, 2009

h. Technical reserves Outstanding claims Full provision is made in outstanding claims for the estimated cost of all claims notified but not settled at

the date of the balance sheet, using the best information available at the time. A provision is calculated

for claims incurred but not reported (IBNR) using statistical methods that incorporate historical data

analysis, quantitative and qualitative information and underwriters’, management and actuary’s

valuation of reserves. Any differences between the estimated cost and subsequent settlement of claims

are included in the revenue account in the year of settlement. Subsequent re-estimations are dealt with

in the same manner.

Unearned premium Unearned premiums are those proportions of the premiums accounted for in the financial year, but

relate to periods of risks that extend beyond the end of the financial year. These premiums are

calculated using the 1/24th

method. For facultative business the company used the 1/365th

method.

One subsidiary takes 25% on marine policies and uses the 1/24th

method for the other classes except for

life where a mathematical provision is prepared by management and approved by an actuary. Another

subsidiary takes 25% on cargo business and uses the 1/365th method for other classes. The other two

subsidiaries take 40% of the net premiums.

The provision is maintained in order to take account of any element of unearned premium in relation to

such policies. Acquisition costs are written off in the year in which they are incurred.

i. Foreign currencies The Financial Statements are expressed in United States dollars.

Current assets and liabilities of the company other than in United States dollars are converted at the rate

of exchange ruling at the balance sheet date. Transactions during the year other than in United States

dollars are converted at the rates of exchange ruling on the dates when they occur.

Differences on exchange are included in the income statement.

Trust Holding Limited – Consolidated Financial Statements 2009

14

Notes to the Consolidated Financial Statements 31 December, 2009

j. Property and equipment Items of own-use property and equipment are stated at cost less accumulated depreciation, except

for land and building, which as from the current year are stated at fair value based on professional

valuation by independent external Valuers.

On revaluation, any increase in the carrying amount of the asset is carried in the Statement of

changes in equity, under Property Revaluation Reserve and any decrease is recognised as an expense,

except to the extent that it reverses a previous increase recognised in equity. The balance in the

property revaluation reserve is transferred to the general reserve upon sale of property and

realization of profit.

Depreciation on revalued buildings is charged to the income statement. The directors have decided

to revalue the building and land annually towards the end of each year; therefore no depreciation

will be charged.

Investment properties are accounted for as long term investments and as from the current year are

stated at fair value in accordance with IAS 40 “Investment property”. Fair value is determined by

independent external Valuers. The change in fair value of investment property is transferred to the

income statement.

Fixtures and equipment are stated at cost less accumulated depreciation and any accumulated

impairment losses.

Depreciation is charged so as to write off the cost, other than land and properties, over the estimated

useful lives, using the straight line method. The principal annual rates used for this purpose are:

%

Buildings for own use 2 - 4

Leasehold improvements 10

Furniture, fittings and office equipment 6 - 20

Computer hardware and software 15 - 33⅓

Motor vehicles 15 – 20

Land is not depreciated The gain or loss arising on the disposal or retirement of an item of property, plant and equipment is

determined as the difference between the sales proceeds and the carrying amount of the assets and

is recognised in the income statement. k. Impairment of tangible assets At each balance sheet date, the company reviews the carrying amounts of its tangible assets to

determine whether there is any indication that those assets have suffered an impairment loss. If any

such indication exists, the recoverable amount of the asset is estimated in order to determine the extent

of the impairment loss (if any). Where it is not possible to estimate the recoverable amount of an

individual asset, the company estimates the recoverable amount of the cash-generating unit to which

the asset belongs.

Trust Holding Limited – Consolidated Financial Statements 2009

15

Notes to the Consolidated Financial Statements 31 December, 2009

k. Impairment of tangible assets – cont. Recoverable amount is the higher of fair value less costs to sell and value in use. If the recoverable

amount of an asset is estimated to be less than its carrying amount the carrying amount of asset is

reduced to its recoverable amount.

An impairment loss is recognised immediately in the income statement unless the relevant asset is

carried at a revalued amount, in which case the impairment loss is treated as a revaluation decrease.

Where an impairment loss subsequently reverses, the carrying amount of the asset is increased to the

revised estimate of its recoverable amount, but so that the increased carrying amount does not exceed

the carrying amount that would have been determined had no impairment loss been recognised for the

asset in prior years. A reversal of an impairment loss is recognised immediately in the income statement,

unless the relevant asset is carried at a revalued amount, in which case the reversal of the impairment

loss is treated as a revaluation increase.

l. Investments Investment in subsidiaries and associates are stated at cost unless there is impairment in value. Any

such impairment is recognised directly in the income statement.

Investments are recognised and de-recognised on a trade date where the purchase or sale of an

investment is under a contract whose terms require delivery of the investment within the timeframe

established by the market concerned and are initially measured at fair value plus directly attributable

transaction costs.

Investments are classified as either investments held for trading or as available-for-sale, and are

measured at subsequent reporting dates at fair value. Where securities are held for trading purposes,

gains and losses arising from changes in fair value are included in the income statement for the period.

For available-for-sale investments, gains and losses arising from changes in fair value are recognised

directly in equity, until the security is disposed of or is determined to be impaired, at which time the

cumulative gain or loss previously recognised in equity is included in the income statement for the

period. Impairment losses recognised in the income statement for equity investments, classified as

available-for-sale, are not subsequently reversed through the income statement.

For publicly traded investments, their fair value is based on quoted market prices as at the Balance Sheet

date. Fair values of other investments are estimated realisable values. Where the fair value can not be

estimated, the investment is carried at initial recognition cost.

Trust Holding Limited – Consolidated Financial Statements 2009

16

Notes to the Consolidated Financial Statements 31 December, 2009

m. Investment properties Investment properties which are properties held to earn rentals and/or for capital appreciation, are

accounted for as long term investments and are measured initially at their cost. Subsequent to initial

recognition, investment properties are measured at fair value (based on independent professional

valuation). Gains and losses arising from charges in the fair value of investment properties are included

in the income statement of the period in which they arise.

n. Investments Fair Value Reserve Investments fair value reserve represents the unrealised gains or losses on the year-end valuation of AFS

investments. In the event of sale or impairment, the cumulative gains or losses recognised under

investments fair value reserve are included in the income statement for the year.

o. Financial Instruments Financial instruments comprise cash and cash equivalents, due to banks, investments, receivable,

outstanding claims, payables and certain other assets and liabilities. Fair values of financial instruments

are based on quoted prices for marketable instruments, or estimated fair values calculated by using

methods such as net present values of future cash flows.

p. Cash and cash equivalents Bank and cash balances comprise of cash balances and bank deposits with maturity not more than one

month which are convertible to known accounts and are subject to insignificant risk of changes in value.

q. Accounts receivables/reinsurance, balances These receivables are measured at initial recognition at fair value. Appropriate allowances for estimated

irrecoverable amounts are recognised in the income statement when there is objective evidence that

the asset is impaired.

r. Trade account payables Trade account payables are measured at fair value.

s. Contingent liabilities Contingent liabilities are disclosed if their confirmation or loss is considered possible from future events.

t. Provisions Provisions are recognised when the company has a present obligation as a result of a past event, and it is

probable that the company will be required to settle that obligation. Provisions are measured at the

directors’ best estimate of the expenditure required to settle the obligation at the balance sheet date,

and are discounted to present value where the effect is material.

u. Dividend and Directors’ fees Dividends and Directors’ fees are recognised as a liability in the year in relation to which they are

approved.

Trust Holding Limited – Consolidated Financial Statements 2009

17

Notes to the Consolidated Financial Statements 31 December, 2009

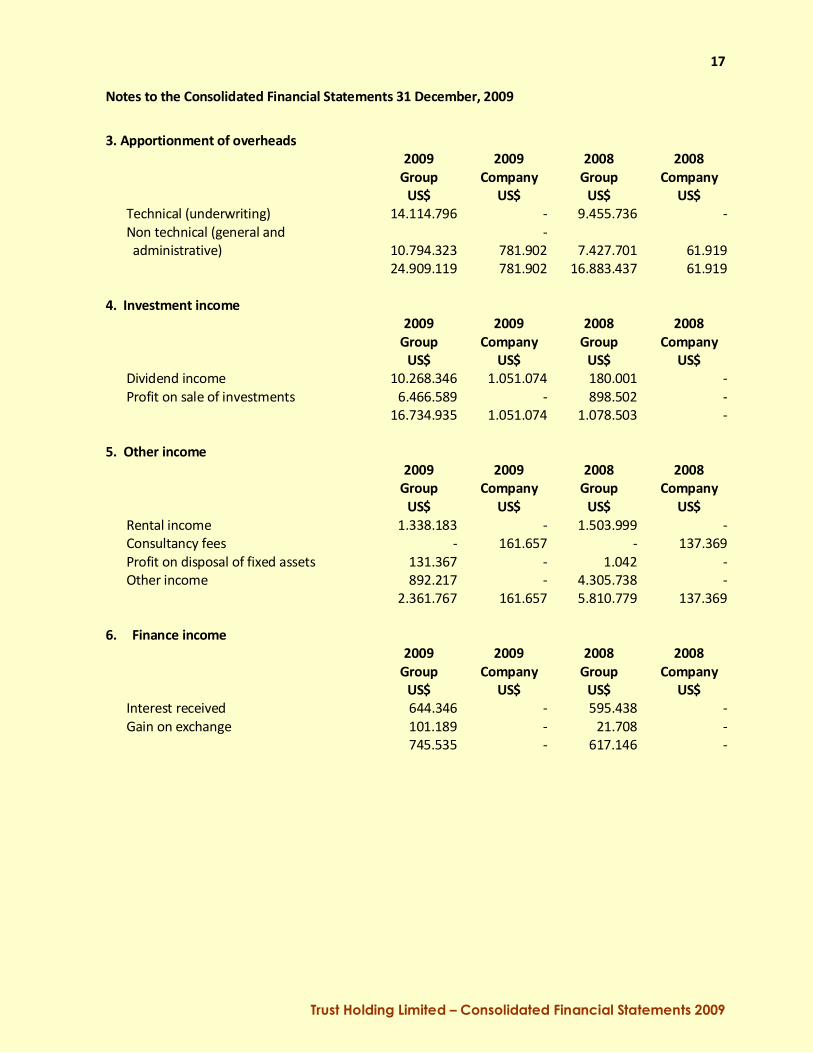

3. Apportionment of overheads

2009 2009 2008 2008

Group Company Group Company

US$ US$ US$ US$

Technical (underwriting) 14.114.796 - 9.455.736 -

Non technical (general and -

administrative) 10.794.323 781.902 7.427.701 61.919

24.909.119 781.902 16.883.437 61.919

4. Investment income

2009 2009 2008 2008

Group Company Group Company

US$ US$ US$ US$

Dividend income 10.268.346 1.051.074 180.001 -

Profit on sale of investments 6.466.589 - 898.502 -

16.734.935 1.051.074 1.078.503 -

5. Other income

2009 2009 2008 2008

Group Company Group Company

US$ US$ US$ US$

Rental income 1.338.183 - 1.503.999 -

Consultancy fees - 161.657 - 137.369

Profit on disposal of fixed assets 131.367 - 1.042 -

Other income 892.217 - 4.305.738 -

2.361.767 161.657 5.810.779 137.369

6. Finance income

2009 2009 2008 2008

Group Company Group Company

US$ US$ US$ US$

Interest received 644.346 - 595.438 -

Gain on exchange 101.189 - 21.708 -

745.535 - 617.146 -

Trust Holding Limited – Consolidated Financial Statements 2009

18

Notes to the Consolidated Financial Statements 31 December, 2009

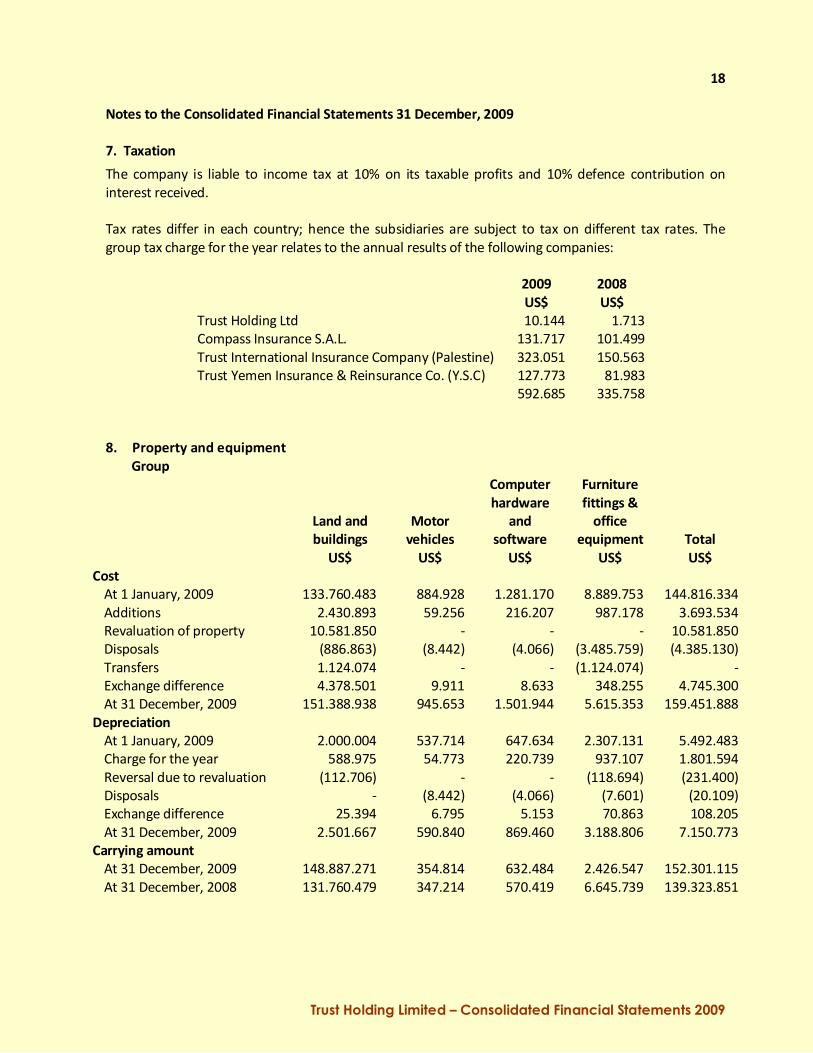

7. Taxation The company is liable to income tax at 10% on its taxable profits and 10% defence contribution on

interest received.

Tax rates differ in each country; hence the subsidiaries are subject to tax on different tax rates. The

group tax charge for the year relates to the annual results of the following companies:

2009 2008

US$ US$

Trust Holding Ltd 10.144 1.713

Compass Insurance S.A.L. 131.717 101.499

Trust International Insurance Company (Palestine) 323.051 150.563

Trust Yemen Insurance & Reinsurance Co. (Y.S.C) 127.773 81.983

592.685 335.758

8. Property and equipment

Group

Computer Furniture

hardware fittings &

Land and Motor and office

buildings vehicles software equipment Total

US$ US$ US$ US$ US$

Cost

At 1 January, 2009 133.760.483 884.928 1.281.170 8.889.753 144.816.334

Additions 2.430.893 59.256 216.207 987.178 3.693.534

Revaluation of property 10.581.850 - - - 10.581.850

Disposals (886.863) (8.442) (4.066) (3.485.759) (4.385.130)

Transfers 1.124.074 - - (1.124.074) -

Exchange difference 4.378.501 9.911 8.633 348.255 4.745.300

At 31 December, 2009 151.388.938 945.653 1.501.944 5.615.353 159.451.888

Depreciation

At 1 January, 2009 2.000.004 537.714 647.634 2.307.131 5.492.483

Charge for the year 588.975 54.773 220.739 937.107 1.801.594

Reversal due to revaluation (112.706) - - (118.694) (231.400)

Disposals - (8.442) (4.066) (7.601) (20.109)

Exchange difference 25.394 6.795 5.153 70.863 108.205

At 31 December, 2009 2.501.667 590.840 869.460 3.188.806 7.150.773

Carrying amount

At 31 December, 2009 148.887.271 354.814 632.484 2.426.547 152.301.115

At 31 December, 2008 131.760.479 347.214 570.419 6.645.739 139.323.851

Trust Holding Limited – Consolidated Financial Statements 2009

19

Notes to the Consolidated Financial Statements 31 December, 2009

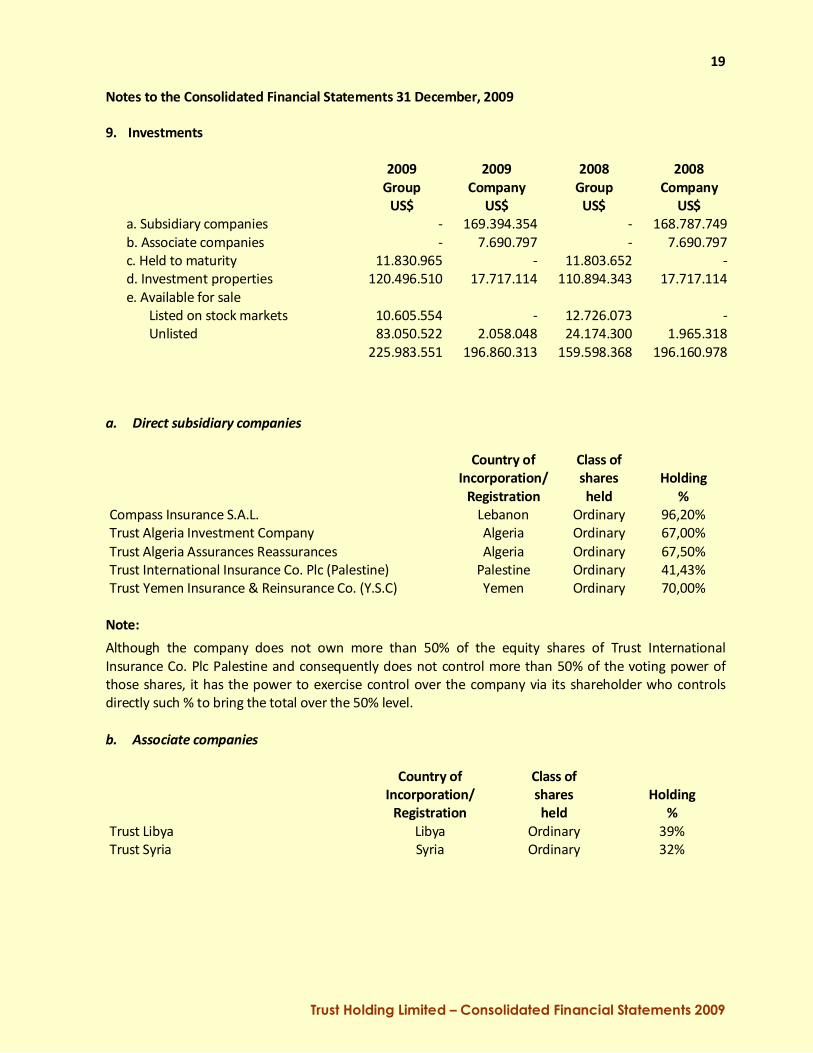

9. Investments

2009 2009 2008 2008

Group Company Group Company

US$ US$ US$ US$

a. Subsidiary companies - 169.394.354 - 168.787.749

b. Associate companies - 7.690.797 - 7.690.797

c. Held to maturity 11.830.965 - 11.803.652 -

d. Investment properties 120.496.510 17.717.114 110.894.343 17.717.114

e. Available for sale

Listed on stock markets 10.605.554 - 12.726.073 -

Unlisted 83.050.522 2.058.048 24.174.300 1.965.318

225.983.551 196.860.313 159.598.368 196.160.978

a. Direct subsidiary companies

Country of Class of

Incorporation/ shares Holding

Registration held %

Compass Insurance S.A.L. Lebanon Ordinary 96,20%

Trust Algeria Investment Company Algeria Ordinary 67,00%

Trust Algeria Assurances Reassurances Algeria Ordinary 67,50%

Trust International Insurance Co. Plc (Palestine) Palestine Ordinary 41,43%

Trust Yemen Insurance & Reinsurance Co. (Y.S.C) Yemen Ordinary 70,00%

Note: Although the company does not own more than 50% of the equity shares of Trust International

Insurance Co. Plc Palestine and consequently does not control more than 50% of the voting power of

those shares, it has the power to exercise control over the company via its shareholder who controls

directly such % to bring the total over the 50% level.

b. Associate companies

Country of Class of

Incorporation/ shares Holding

Registration held %

Trust Libya Libya Ordinary 39%

Trust Syria Syria Ordinary 32%

Trust Holding Limited – Consolidated Financial Statements 2009

20

Notes to the Consolidated Financial Statements 31 December, 2009

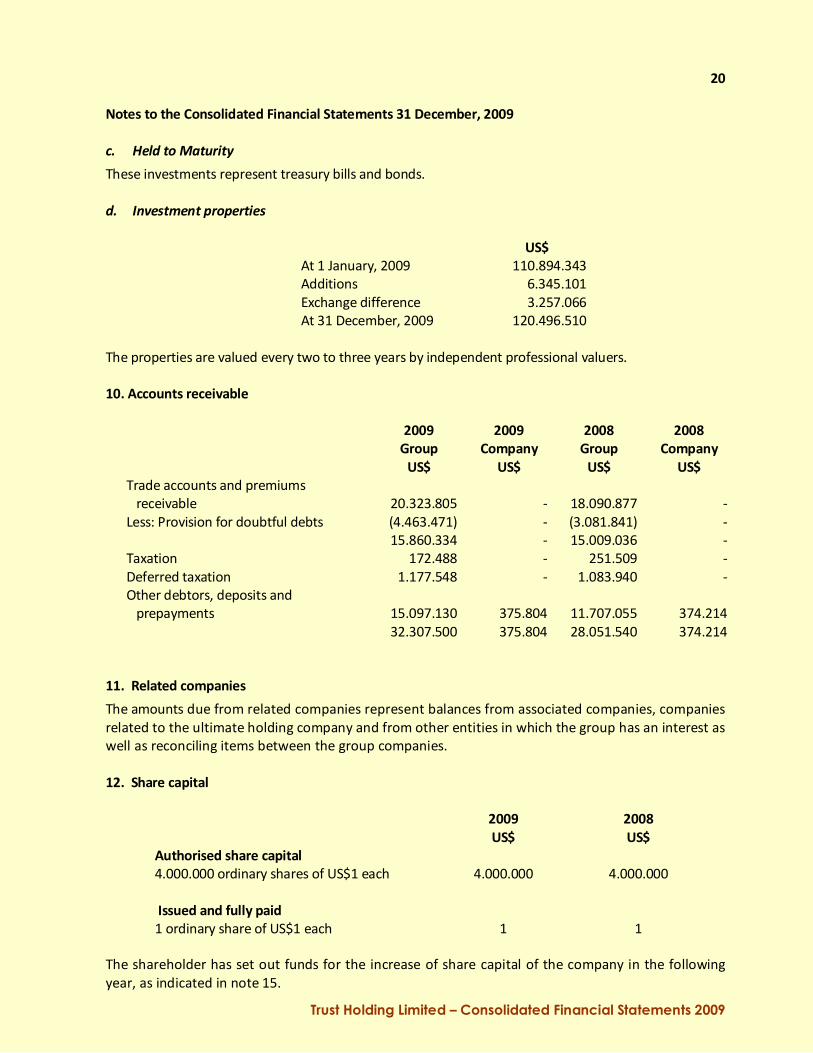

c. Held to Maturity These investments represent treasury bills and bonds.

d. Investment properties

US$

At 1 January, 2009 110.894.343

Additions 6.345.101

Exchange difference 3.257.066

At 31 December, 2009 120.496.510

The properties are valued every two to three years by independent professional valuers.

10. Accounts receivable

2009 2009 2008 2008

Group Company Group Company

US$ US$ US$ US$

Trade accounts and premiums

receivable 20.323.805 - 18.090.877 -

Less: Provision for doubtful debts (4.463.471) - (3.081.841) -

15.860.334 - 15.009.036 -

Taxation 172.488 - 251.509 -

Deferred taxation 1.177.548 - 1.083.940 -

Other debtors, deposits and

prepayments 15.097.130 375.804 11.707.055 374.214

32.307.500 375.804 28.051.540 374.214

11. Related companies The amounts due from related companies represent balances from associated companies, companies

related to the ultimate holding company and from other entities in which the group has an interest as

well as reconciling items between the group companies.

12. Share capital

2009 2008

US$ US$

Authorised share capital

4.000.000 ordinary shares of US$1 each 4.000.000 4.000.000

Issued and fully paid

1 ordinary share of US$1 each 1 1

The shareholder has set out funds for the increase of share capital of the company in the following

year, as indicated in note 15.

Trust Holding Limited – Consolidated Financial Statements 2009

21

Notes to the Consolidated Financial Statements 31 December, 2009

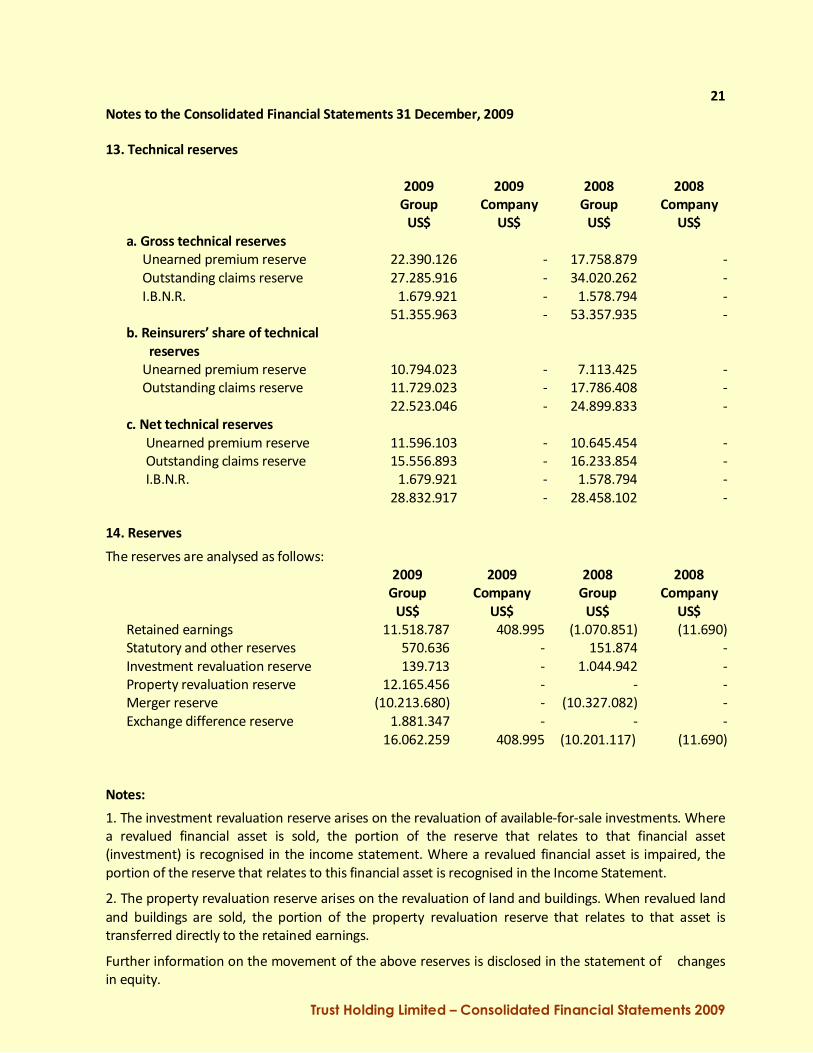

13. Technical reserves

2009 2009 2008 2008

Group Company Group Company

US$ US$ US$ US$

a. Gross technical reserves

Unearned premium reserve 22.390.126 - 17.758.879 -

Outstanding claims reserve 27.285.916 - 34.020.262 -

I.B.N.R. 1.679.921 - 1.578.794 -

51.355.963 - 53.357.935 -

b. Reinsurers’ share of technical

reserves

Unearned premium reserve 10.794.023 - 7.113.425 -

Outstanding claims reserve 11.729.023 - 17.786.408 -

22.523.046 - 24.899.833 -

c. Net technical reserves

Unearned premium reserve 11.596.103 - 10.645.454 -

Outstanding claims reserve 15.556.893 - 16.233.854 -

I.B.N.R. 1.679.921 - 1.578.794 -

28.832.917 - 28.458.102 -

14. Reserves The reserves are analysed as follows:

2009 2009 2008 2008

Group Company Group Company

US$ US$ US$ US$

Retained earnings 11.518.787 408.995 (1.070.851) (11.690)

Statutory and other reserves 570.636 - 151.874 -

Investment revaluation reserve 139.713 - 1.044.942 -

Property revaluation reserve 12.165.456 - - -

Merger reserve (10.213.680) - (10.327.082) -

Exchange difference reserve 1.881.347 - - -

16.062.259 408.995 (10.201.117) (11.690)

Notes: 1. The investment revaluation reserve arises on the revaluation of available-for-sale investments. Where

a revalued financial asset is sold, the portion of the reserve that relates to that financial asset

(investment) is recognised in the income statement. Where a revalued financial asset is impaired, the

portion of the reserve that relates to this financial asset is recognised in the Income Statement.

2. The property revaluation reserve arises on the revaluation of land and buildings. When revalued land

and buildings are sold, the portion of the property revaluation reserve that relates to that asset is

transferred directly to the retained earnings.

Further information on the movement of the above reserves is disclosed in the statement of changes

in equity.

Trust Holding Limited – Consolidated Financial Statements 2009

22

Notes to the Consolidated Financial Statements 31 December, 2009

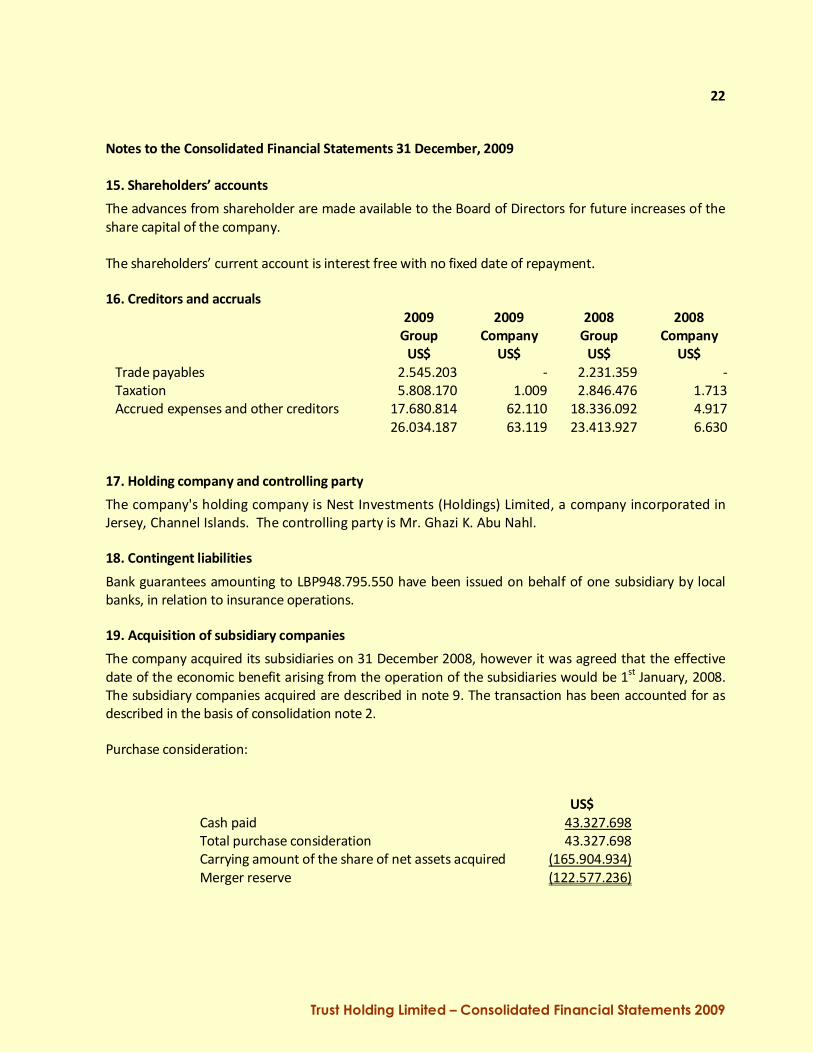

15. Shareholders’ accounts The advances from shareholder are made available to the Board of Directors for future increases of the

share capital of the company.

The shareholders’ current account is interest free with no fixed date of repayment.

16. Creditors and accruals

2009 2009 2008 2008

Group Company Group Company

US$ US$ US$ US$

Trade payables 2.545.203 - 2.231.359 -

Taxation 5.808.170 1.009 2.846.476 1.713

Accrued expenses and other creditors 17.680.814 62.110 18.336.092 4.917

26.034.187 63.119 23.413.927 6.630

17. Holding company and controlling party The company's holding company is Nest Investments (Holdings) Limited, a company incorporated in

Jersey, Channel Islands. The controlling party is Mr. Ghazi K. Abu Nahl.

18. Contingent liabilities Bank guarantees amounting to LBP948.795.550 have been issued on behalf of one subsidiary by local

banks, in relation to insurance operations.

19. Acquisition of subsidiary companies The company acquired its subsidiaries on 31 December 2008, however it was agreed that the effective

date of the economic benefit arising from the operation of the subsidiaries would be 1st January, 2008.

The subsidiary companies acquired are described in note 9. The transaction has been accounted for as

described in the basis of consolidation note 2.

Purchase consideration:

US$ Cash paid 43.327.698 Total purchase consideration 43.327.698 Carrying amount of the share of net assets acquired (165.904.934) Merger reserve (122.577.236)

Trust Holding Limited – Consolidated Financial Statements 2009

23

Notes to the Consolidated Financial Statements 31 December, 2009

19. Acquisition of subsidiary companies (cont’d)

Acquiree’s carrying amount before combination

US$

Property, plant and equipment 138.981.321 Investments 134.421.670

Trade and other receivables 27.470.536

Deferred acquisition costs 905.474

Related Companies 3.764.796

Bank and cash balances 11.238.109

Creditors and accruals (21.766.101)

Reinsurance balances – net (2.265.108)

Technical reserves – net (28.312.972)

264.437.725

Carrying amount of the share of net assets acquired 165.904.934

Cash consideration paid (43.327.698)

Cash and cash equivalents acquired 11.238.109

Cash outflow on acquisition (32.089.589)

20. Capital commitments As at the balance sheet date there were no capital commitments.

21. Financial instruments and risk management Financial instruments consist of financial assets and financial liabilities. Financial assets and financial

liabilities are recognised on the company’s balance sheet when the group becomes a party to the

contractual provisions of the instrument.

Financial assets of the group include cash and cash equivalents, deposits, investments and receivables.

Financial liabilities of the group include payables to insurance and reinsurance companies and other

creditors and accrued liabilities.

The risks management policies used by the group to manage various risks factors are explained below:

Reinsurance risk In order to control financial exposure arising from large claims, each company in its normal course of

business enters into agreements with other parties for reinsurance purposes. This is a common practice

in reinsurance industry.

Trust Holding Limited – Consolidated Financial Statements 2009

24

Notes to the Consolidated Financial Statements 31 December, 2009 21. Financial instruments and risk management (cont’d) Reinsurance ceded contracts do not relieve the group’s companies from their obligations to ceding

companies or clients and consequently each company remains liable for the portion of outstanding

claims reinsured to the extent that the reinsurer fails to meet the obligations under the reinsurance

agreements. In order to limit its exposure to significant losses that might arise from large claims from

insolvent reinsurers, each company continuously evaluates its reinsurers’ financial condition and follows

up developments in their areas of operations. Currency risk Currency risk is the risk that the value of a financial instrument will fluctuate due to changes in foreign

exchange rates. The group’s reporting currency is the United States Dollars. The company does not have

significant exposure in other currencies, other than those recognised and disclosed in the Financial

Statements. Market risk Market risk is the risk that the value of a financial instrument will fluctuate as a result of changes in

market prices. The group is exposed to market risk with respect to its investments in quoted securities

and investment properties.

The Group limits its market risk by maintaining a conservative investment portfolio and continuously

monitoring the related stock markets and the factors which affect their performance. Interest rate risk Interest rate risk is the risk that the value of a financial instrument will fluctuate due to changes in

market interest rates.

The Group has time deposits that are subject to interest rate risk. Interest rate risk to the company is the

risk of changes in market interest rates reducing the overall return on its interest bearing time deposits.

The group limits interest rate risk by following up changes in interest rates in the currencies in which its

time deposits are denominated. Credit risk Credit risk is the risk that one party to a financial instrument will fail to discharge an obligation and cause

the other party to incur a financial loss. The group employs certain policies and procedures in order to

maintain credit risk exposures within reasonable limits.

The credit risk on liquid funds is limited, as the counter parties are well known banks, with high credit

rating by international credit rating agencies. The maximum exposure to credit risk for the Group is

represented by the carrying amount of each financial asset as disclosed in the Financial Statements. Liquidity risk Liquidity risk is the risk that an enterprise will encounter difficulty in raising funds to meet commitments

associated with financial liabilities. Liquidity requirements are monitored on a regular basis and the

management is confident that sufficient funds are available to meet any commitments as they may

arise.