triodos vastgoedfonds - · pdf file7 triodos vastgoedfonds offers investors the opportunity to...

TRANSCRIPT

TLIM

Triodos VastgoedfondsAnnual report 2014

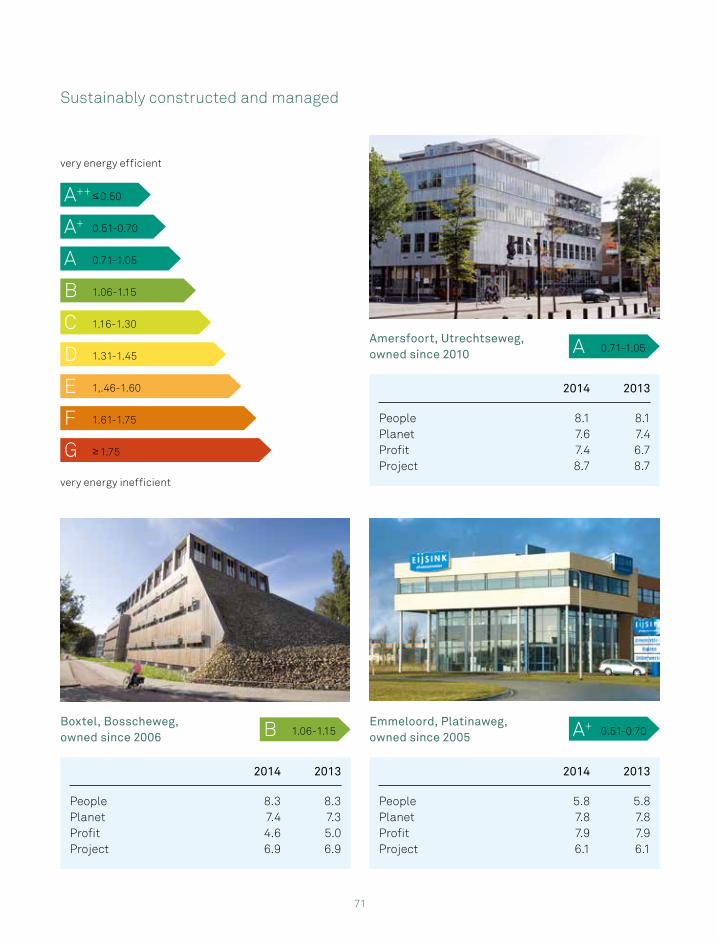

Sustainable real estate takes into account the efficient use of assets and the impact on individuals and the environment during the entire life cycle of a building, from its development and funding to its management and reuse.

Sustainable real estate

Information for shareholders

General Meeting of Shareholders 21 May 2015 Ex-dividend date 27 May 2015Dividend payment date 29 May 2015

Triodos Investment Management is a wholly owned subsidiary of TriodosBank and is the manager of Triodos Vastgoedfonds.

The original Annual Accounts were prepared in Dutch. This document is an English translation of the original annual accounts. Where there are discrepancies between the English and Dutch versions, the latter prevails.

TriodosVastgoedfonds NVAnnual Report2014

4

Key figures

(amounts in EUR x 1,000) 2014 2013 2012 2011 2010

Net asset value at year-end 29,941 30,168 34,646 40,270 49,970Solvency 43% 42% 45% 46% 59%Loan to Value 54% 52% 52% 52% 43%Cost of Debt 5.0% 5.0% 5.0% 4.9% 4.5%Interest coverage 2,7 2,3 1,7 2,5 1,9Average maturity of loans (in years) 5.7 6.7 7.6 7.9 7.8Number of Shares outstanding at other institutions (x1,000) 8,399 8,399 8,449 8,175 9,066Investments at year-end 69,310 71,045 75,911 87,194 77,740Number of properties in portfolio at year-end 17 17 17 17 14Occupancy rate at year-end 97% 98% 96% 98% 99%Average term of leases (in years) 5.0 5.3 6.1 6.7 6.5Income 5,873 5,419 6,128 6,088 6,034Realised changes in the value of investments – – -1,426 -1 -1,345Unrealised changes in the valueof investments -1,771 -5,319 -6,097 -4,965 -301Changes in the value of receivables -20 – – – -75Expenses -2,630 -2,959 -3,279 -3,214 -3,039Result 1,452 -2,859 -4,674 -2,092 1,274Operating result 3,223 2,460 1,423 2,873 1,575Current cost ratio1 5.67% 6.89% 5.07% 4.70% 3.80%Fund cost expense ratio2 3.06% 3.35% 3.10% 2.90% 2.79%Ratio illiquid investments at year-end3 231% 235% 219% 216% 156%

Per share

(amounts in EUR) 2014 2013 2012 2011 2010

Net asset value 3.56 3.59 4.10 4.93 5.51Share price 2.63 2.86 4.10 4.93 5.51Direct result4 0.38 0.29 0.34 0.33 0.35Indirect result4 -0.21 -0.63 -0.90 -0.57 -0.20Total result4 0.17 -0.34 -0.56 -0.24 0.15Dividend (or other distribution to shareholders)) – 5 0.20 0.20 0.29 0.29

5

Return Triodos Vastgoedfonds

2013 2012 2011 2010 2009

Dividend yield6 7.0% 4.5% 5.4% 3.6% 4.2%

1 The current cost ratio (CCR) indicates the total costs during the past 12 months excluding the costs of investment transactions and interest costs relative to the average net asset value during the relevant period. (For further information we refer to page 16.)2 The fund cost expense ratio is represented by the fund costs, including the management fee, auditor’s fees and marketing costs, as a percentage of the average net asset value. The difference with the current cost ratio is that the operating expenses, such as maintenance costs, that are included in that ratio are not included in the fund costs expense ratio.3 The sum of the illiquid investments divided by the net asset value as at the end of the reporting period.4 The result per share is calculated on the basis of the average number of shares outstanding during the financial year.5 No distribution has been paid out yet for the 2014 financial year.6 Dividend divided by the share value as at the end of the financial year to which the dividend relates.

6

Contents Page

Investing in sustainable real estate 7

Report of the Supervisory Board 8

Report of the Board 9

General information 19

Annual Accounts 2014 Triodos Vastgoedfonds 21

Other information 63

Appendix A. Investment portfolio Triodos Vastgoedfonds 70

Appendix B. Triodos Sustainable Real Estate Screen 77

Appendix C. Triodos Vastgoedfonds: first zero emission real estate fund 81

Personal details 88

Glossary 90

Address and colophon 91

7

Triodos Vastgoedfonds offers investors the opportunity to invest in sustainable real estate. The fund invests mainly in office buildings that have been constructed and are managed in a sustainable manner. The sustainability of the real estate is assessed by means of the Triodos Sustainable Real Estate Screen. This assessment model was developed by Triodos Vastgoedfonds. In this model the concepts of people, planet and profit are geared specifically to the real estate sector and project has been added as fourth factor. By means of these four factors, the social (people), environmental (planet), economic (profit) and spatial aspects (project) are taken into account during the assessment of the office buildings.

Triodos Vastgoedfonds was established by Triodos Bank NV and was the first sustainable real estate fund to be recognised as such in the Netherlands. Triodos Bank’s objective is to promote human dignity, caring for the earth and the quality of life in general. Triodos Vastgoedfonds aims to realise this mission within the real estate market. Real estate is one of the elements that determines the quality of our living environment. Sustainably constructed buildings offer a more pleasant and healthier environment to live and work in. Energy consumption is lower and their impact on the environment is less harmful.

Triodos Vastgoedfonds was established in 2004 as the first sustainable real estate fund in the Netherlands and is managed by Triodos Investment Management BV.

Investing in sustainable real estate

8

Report of the Supervisory Board

To the shareholders of Triodos Vastgoedfonds

We are pleased to present the annual report for 2014 of Triodos Vastgoedfonds NV. The annual report comprises the report of the Board, the annual accounts and the other information. The annual accounts for 2014 have been approved by KPMG Accountants NV. The auditor’s report is included in this annual report under the heading of ‘Other Information’.

The Supervisory Board has signed the annual accounts and proposes to discharge the Board and the members of the Supervisory Board for the performance of their duties in the past financial year.

The Board is satisfied with the conduct of management and the collaboration with the Board. Throughout 2014, the fund’s management kept the Supervisory Board informed about the developments in the market and within the fund. In the second half of the year, the interim distribution charged to the direct result for 2013 was discussed in detail. The Board supports the fund’s ambition to find prospective new shareholders interested in investing in Triodos Vastgoedfonds.Meiny Prins intends to retire during the General Meeting of Shareholders scheduled for 21 May 2015.

Zeist, the Netherlands, 9 April 2015

Kees Duijvestein (Chair) Meiny PrinsRené GeskesCarel de Vos tot Nederveen Cappel

9

Triodos Vastgoedfonds manages a portfolio of office buildings with a value of EUR 69.3 million (as at 2014 year-end) and invests in the main urban areas of the Netherlands. In 2014 the fund realised a positive result of EUR 1.5 million. For the first time since 2010 the amount by which the value of real estate was written down was lower than the operational result.The office buildings that the fund invests in are easily accessible by public transport and by car and have long-term leases. During the management phase the sustainability of the real estate is further enhanced. This is done in consultation with the tenants. The constant dialogue with the tenants results in a very active management style. This applies to the day-to-day operational management of properties as well as to the efforts aimed at enhancing the sustainability of specific properties. This is how the fund aims to increase sustainability, the occupancy rate and the cash flow from investments.Triodos Vastgoedfonds offers tenants sustainable and distinctive accommodation that makes a positive contribution to their operating processes and enhances their recognizability. The fund aims to offer institutional and private investors a stable distribution policy.On 7 October 2014, during an Extraordinary General Meeting, the shareholders of Triodos Vastgoedfonds adopted the proposal by the Board of the fund to reduce the nominal value of the shares to EUR 0.50. By lowering the nominal value, the necessary scope was created for pursuing a stable distribution policy. During the Extraordinary General Meeting of Shareholders a large majority of the shareholders present adopted the proposal to lower the nominal value and the related amendment of the Articles of Association. Subsequently, on 18 December 2014 a distribution of EUR 0.20 per share was paid out. This distribution was based on the operational result for 2013. On 6 January 2014 a distribution of EUR 0.20 per share had already been made payable. This distribution was based on the operational result for 2012.

In 2014 a project undertaken by Triodos Vastgoedfonds was nominated for the FGH Real Estate Award, together with only two other projects. The nomination for this award again resulted in a considerable amount of publicity focusing on the sustainabilisation of the office building at Stationsweg in Groningen, which is currently let to gas trading company GasTerra.

European regulations

For Triodos Investment Management, the manager of Triodos Vastgoedfonds, 2014 was dominated by the need to comply with the requirements of new European regulations, covered by the Alternative Investment Fund Managers Directive (AIFMD). For investors in Triodos Vastgoedfonds the prospectus has been supplemented with a document entitled ‘Aanvullende informatie voor beleggers in Triodos Vastgoedfonds als gevolg van nieuwe regels’ (‘additional information for investors in Triodos Vastgoedfonds resulting from new regulations’). This document, which is available on the website, outlines the changes that the AIFMD entails for the fund. Furthermore, a depositary has been appointed for the fund. The duties of this depositary, BNP Paribas Securities Services S.C.A., include monitoring the investments and the cash flows of the fund. In addition, various forms of internal policy, such as risk management, valuation policy and liquidity management, have been modified to comply with the requirements of the AIFMD. As a result, Triodos Vastgoedfonds operates in line with these new rules.

Report of the Board

97%of the portfolio has been let

10

Market developments

The modest recovery of the real estate market is reflected mainly in the investment market. The dynamic development of the offices market remains restricted to a limited number of locations. In 2014 the letting transactions in the four big cities represented over 40% of the national letting transactions. Prospective tenants tend to require larger open floor spaces with attractive communal areas. Properties must be located in areas that are easily accessible by public transport and offer a high level of amenities. Office-accommodated organisations increasingly critically review the office floor space that they need for their organisation to operate. Users are mainly interested in office buildings with large floor spaces that are suitable for flexible work space concepts.

Organisations have shorter horizons and lease terms are becoming shorter. This implies that tenants also return to the market more quickly. Given the ample supply, they have the choice to renegotiate or look for different premises that may be let on more attractive terms.

In view of the tentative economic recovery, it seems likely that demand for real estate for investment purposes will increase. In addition, the

negative value trend appears to be coming to an end. In 2014 the dynamics in the investment market increased. According to international property consultancy firm Savills, the total investment volume in the Netherlands grew to over EUR 8 billion in 2014, which constitutes a significant increase relative to the volume of EUR 4.7 billion in 2013. This increase was mainly accounted for by foreign investors, who were responsible for around two thirds of the investment volume in 2014.

The property markets are expected to start benefiting from the European Central Bank’s government and corporate bond purchase programme. This is expected to result in a modest decline of initial yields and a further increase in investment volumes.

Triodos Vastgoedfonds in the market

Triodos Vastgoedfonds aims to be a pioneer with regard to the sustainabilisation of the Dutch real estate market. These are challenging times, also for the real estate sector, but the fund still actively aims to make a positive contribution to enhancing the sustainability of office property. These efforts by Triodos Vastgoedfonds have again been recognised by the market. For instance, the renovation and sustainabilisation of the vacant property at Stationsweg in Groningen for a new tenant, GasTerra, was nominated for the FGH Real Estate Award. Previously, in 2012, the fund had already received the ‘Golden Frog Award’ for this sustainabilisation project. In 2013 the project received the Energy Efficiency prize during the presentation of the Benelux Aluminium Award for Sustainable Renovation. By renovating and enhancing the sustainability of the building, the energy label was upgraded from G to A+, which results in a 60% energy saving on an annual basis.

As part of the ‘Energy leap’ (Energie-sprong) programme set up by the Foundation for experimental housing (Stichting Experimentele

Total annual return according to IPD Netherlands Property Index for office buildings

1 year 3 years 5 years

Triodos Vastgoedfonds 5.9% 1.7% 2.3%IPD 3.3% -0.9% 0.6%

Performance of the portfolio of Triodos Vastgoedfonds relative to the IPD benchmark 2014

Direct Indirect Total

Triodos Vastgoedfonds 8.6% -2.4% 5.9%IPD 6.8% -3.3% 4.7%

7 Savills World Research: Netherlands Market in Minutes – Interest of buyers and sellers aligned, December 2014.

11

Volkshuisvesting - SEV), this project also received a subsidy because it was considered a prime example of ‘energy neutral’ renovation. Finally, the office building received a ‘green certificate’ (groenverklaring) from the Dutch ministry of Housing, Spatial planning and Environment.

The ‘green lease’ concept pioneered by Triodos Vastgoedfonds was the basis for the extensive sustainabilisation of the property in Groningen. This concept implies that the tenant and the owner join forces to realise a sustainable, pleasant and modern work environment. Triodos Vastgoedfonds believes that this concept could be applied on a much wider scale. The basic objective of a ‘green lease’ contract is to completely renovate an existing building in a sustainable manner without raising the housing expenses. The sustainable renovation results in impressive energy savings, which significantly reduces the energy costs as compared with those for similar non-renovated office buildings. The renovation funded by the landlord pays itself back from the ‘profit’ that the energy saving yields. It is a simple concept that can be applied on a much wider scale. With the ‘green lease’ concept, the fund aims to further promote the market for sustainable real estate.

During the Dutch Green Building Week 2014, Triodos Vastgoedfonds introduced a new project under the name of ‘De Nederlanden van 2020’. This project is aimed at making six properties in the province of Gelderland energy neutral. This real estate will be used to generate and store as much sustainable energy as possible. In addition, the energy systems of these households will be interconnected.

In 2014 Triodos Vastgoedfonds participated in the Global Real Estate Sustainability Benchmark (GRESB) for the second time. Triodos Vastgoedfonds, which has a ‘Green Star’ rating, is once again one of the best performing Dutch property funds participating in GRESB.

InvestmentsBecause the offices market remained under pressure in 2014, Triodos Vastgoedfonds did not acquire or sell any real estate during the year. In 2014 the focus was on managing the existing real estate portfolio. The quality of the portfolio remained intact, in terms of sustainability as well as occupancy rate.Triodos Vastgoedfonds managed to maintain the high occupancy rate. At 2014 year-end the occupancy rate was 97% (2013 year-end: 98%). In this respect, the fund outperforms the market, which has an average occupancy rate of 84% (2014 year-end). Although rents in the market came down, the inflow of rents for the fund rose 0.9% to EUR 6,816,914 (2013: EUR 6,754,923). The rental income ensures a stable cash flow.

The properties in the fund’s portfolio use more than 48.6% less energy than average office property investments in the Netherlands. The energy that is used in the properties is 100% green. This applies to electricity as well as gas. The remaining CO2 emissions are fully offset by means of voluntary emission rights. As a result, Triodos Vastgoedfonds is a zero emission real estate fund. Water consumption is almost 25.3% lower than for an average Dutch offices portfolio.Because of the many uncertainties in the market, tenants currently opt for shorter lease terms. Consequently, new leases have not resulted in a

0%first‘zero emission’ real estate fund

12

longer average lease term. As at 2014 year-end, the average lease term is 5.0 years (2013 year-end: 5.3 years). It appears that both for existing and potential tenants, the sustainable nature of the properties in the fund’s portfolio is an important consideration when deciding whether or not to renew or take out a new lease. Moreover, tenants who are looking for sustainable accommodation are proactively approaching Triodos Vastgoedfonds.

Value development portfolio

The market conditions for commercial real estate improved slightly in 2014 and as a result, the negative revaluation trend is starting to bottom out. In 2014 the total portfolio was written down by 2.4% (from EUR 71.0 to EUR 69.3). In 2013, the write-down still amounted to 7.0%. The figures from the Index Property Database (IPD), which calculates the benchmark for the offices market, show that on average the value of real estate in the Dutch market fell 3.3%. The decrease in value for Triodos Vastgoedfonds was therefore lower than for the market as a whole, which is related to the sustainability of the properties and their high occupancy rate.

In view of the many uncertainties in the offices market, Triodos Vastgoedfonds decided to not acquire or sell any property in 2014 and focus its attention on credit management. This kept the accounts receivable under control. In 2014, an amount of EUR 16,000 in rent receivables was

written off and a provision of EUR 4,000 was established.

Liquidity management

Liquidity projections are prepared based on operating budgets. Frequent checks are carried out to ascertain whether the liquidity position is developing in line with projections. If necessary, corrective measures are taken.

Result

Financial result

The result of Triodos Vastgoedfonds comprises the operating result and the changes in value of the properties caused by the developments in the real estate market. The operating result is made up of the rental income and other income minus the total costs. The operating result for 2014 amounts to EUR 3.2 million (2013: EUR 2.5 million). The direct result per share amounts to EUR 0.38 (2013: EUR 0.29).

Triodos Vastgoedfonds’ equity before profit appropriation fell to EUR 29.9 million as at 2014 year-end (2013: EUR 30.2 million). This decline is due to the dividend distribution of EUR 1.7 million for 2013, which was partly offset by a positive result of EUR 1.5 million for 2014. The number of shares outstanding was 8.4 million. The indirect or revaluation result per share amounts to EUR -0.21 (2013: -0.63). This brings the total result per share to

Returns (%) 2014 2013 2012 2011 2010 2009 2008 2007 2006

Direct* 10.5 7.3 7.5 6.2 6.3 6.0 5.0 5.3 6.3Indirect** -5.8 -15.7 -19.8 -10.7 -3.5 -14.0 -10.7 1.9 -1.9

Total*** 4.7 -8.4 -12.3 -4.5 2.8 -8.0 -5.7 7.2 4.4

*The direct return comprises the operating result divided by the average amount of equity for the period to which it relates.** The indirect return comprises the revaluations divided by the average amount of equity during the period to which it relates.*** The total return comprises the result divided by the average amount of equity during the period to which it relates.

13

EUR 0.17 (2013: EUR -0.34).The net asset value per share as at 2014 year-end amounts to EUR 3.56 (2013: EUR 3.59).

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Dec-2014Sep-2014Jun-2014Mar-2014Dec-2013Sep-2013July-2013

Net asset valueShare price

Net asset value and share price since July 2013

70

80

90

100

110

120

130

Dec-14Dec-12Dec-10Dec-08Dec-06July-04

Indexed stock market price Triodos Vastgoedfonds

Change in value per share since inception

Indexedvalue

14

15

GRONINGEN, STATIONSWEG

Triodos Vastgoedfonds bought this property in 2011. The architectural features of the building were significantly improved, causing its energy label to be upgraded from E to A+. Due to its enhanced sustainability, the useful life of the property was extended by many years. This is a prime example of sustainable redevelopment. Triodos Vastgoedfonds has received several awards for this project.

16

Return and distributions

Triodos Vastgoedfonds aims for a stable distribution policy, based on its direct operational result.

The distribution of EUR 0.20 per share was paid out on 18 December 2014. If the distribution at the time of distribution is divided by the stock market value as at that time, the dividend yield comes to 7.6%.The total return is calculated based on the share price that is determined by supply and demand, including reinvestment of dividends.

Costs

Triodos Vastgoedfonds pays a management fee of 1% of the fund’s invested capital to the manager of the fund, Triodos Investment Management. This management fee is used to cover the fund management costs incurred by Triodos Investment Management as well as the costs of the outsourced asset and property management activities. In addition, the management fee is used to cover the costs of all the activities required to keep the accounts and meet the reporting requirements.

The current cost ratio (CCR) indicates the costs incurred by an investment fund as a percentage of the weighted average equity over the reporting period. These are the costs excluding the costs of investment transactions and interest costs relative to the average net asset value of the fund. In 2014 the CCR for Triodos Vastgoedfonds was 5.67% (2013: 6.89%). For further information about the current cost ratio we refer to page 48.

It should be noted that the CCR for real estate funds cannot be compared with that of, for instance, equity and bond funds. This is due to the running costs for property that real estate funds incur, for instance for maintaining the properties in their portfolio. Not taking into account the property expenses, the fund costs expense ratio comes to 3.06% (2013: 3.35%).

Risks

Triodos Vastgoedfonds invests the funds contributed by investors for their account and at their risk. In order to keep shareholders as fully informed as possible, all relevant risks to which the fund is exposed are described in the fund’s prospectus.

Adequate risk control is part of the day-to-day responsibilities of the fund’s manager and should ensure that all the relevant risks connected with the investment strategy and to which the fund is or could be exposed are sufficiently recognised, measured, managed and monitored. In addition to the management measures already in place, the manager took or prepared a number of measures in 2014 to further improve risk management. For instance, the manager has recorded the risk policy in a policy document and a permanent risk management position was instituted within the organisation.

In order to manage the risks, the manager has comprehensively documented its risk management policy. The aim is to manage the risks involved in operations, in the financial position (on a portfolio level and at the level of each individual investment) and in outsourcing relationships with regard to the objective of the fund by specifying, measuring, managing and monitoring them by means of appropriate stress test procedures.

The manager’s policy is based on the COSO approach (The Committee of Sponsoring Organizations of the Treadway Commission). This approach provides uniform and common terms of reference for internal control that are generally accepted in the market and has the following constituents:

1. The objectives of the fund with regard to risk management;

2. The duties and responsibilities of the risk manager;

3. The arrangement of the risk management model in the Manager’s organisation such that procedures and measures are established that

17

guarantee that a functional and hierarchical separation is made between the tasks involved in risk management and those of the operational departments.;

4. Definitions and control measures for the risks to which the fund and the manager are exposed;

5. Criteria with regard to risk management for the fund, the manager and the operational parties, and

6. Relevant legislation and regulations (paying attention to the specific requirements set by AIFMD) with regard to risk management and internal control.

The Board periodically performs a ‘control risk self assessment’, during which the risks and the extent to which they are under control are determined. Every year the Board provides an explanation of the way in which the risks involved in the investments were dealt with during the year under review in the Notes to the Annual Accounts (see page 21). The main risks in 2014 and the manner in which they were controlled are also briefly described below.

Liquidity risk

Liquidity risk is the risk that Triodos Vastgoedfonds cannot obtain the financial means necessary to meet its obligations. Projections are made at regular intervals in order to predict the development of the liquidity position. In order to absorb fluctuations, the fund has an overdraft facility of EUR 3 million.

Market risk

The value of real estate is influenced by many factors, including the outlook for economic growth, the rate of inflation and rental income at the time of divestment. The more these factors fluctuate, the greater the market risk will be. Triodos Vastgoedfonds cannot defend itself against the macro economic factors that impact the value of its real estate. However, the fund endeavours to ensure the attractiveness of its real estate through appropriate management of its properties and by making its view on sustainability visible in those properties.

Leverage risk

The fund may borrow up to 60% of the fiscal book value of the fund’s real estate or rights attached to that real estate. Triodos Vastgoedfonds aims to limit the leverage to 50% of the invested capital. The risk of investing with borrowed money is that the shareholders may lose the capital that they have invested because upon divestment loans must be repaid first, as the investments serve as collateral for the debt. This risk is limited by the fact that the shareholders are not required to supplement any shortfalls incurred by Triodos Vastgoedfonds in case the losses exceed the capital that they have invested.

Manager’s statement

Triodos Vastgoedfonds is managed by Triodos Investment Management BV. Triodos Investment Management is licensed to act as manager of investment funds by the Netherlands Authority for the Financial Markets and is therefore in possession of a description of operational management procedures that meets the requirements of the Dutch Financial Supervision Act (Wet Financieel toezicht - Wft) and the Dutch Decree on the Supervision of the Conduct of Business (Besluit Gedragstoezicht financiële ondernemingen - Bgfo).

During the past financial year Triodos Investment Management assessed various aspects of its operational management procedures. Based on the outcome of this assessment, Triodos Investment Management states that as manager of Triodos Vastgoedfonds it has a description of the operational management procedures as referred to in Article 115y, paragraph 5 Bgfo that meets the requirements as set out in article 3:17 paragraph 2, sub c and article 4:14, paragraph 1 of the Wft.

During its assessment activities, Triodos Investment Management found no evidence that operational management does not function effectively or not in accordance with the description. For this reason, Triodos Investment Management can report with a

18

reasonable degree of certainty that operational management during the financial year 2014 functioned effectively and in accordance with the description.

Triodos Investment Management is a member of the Dutch Fund & Asset Management Association (DUFAS). DUFAS is the trade organisation for the Dutch asset management sector and represents this sector’s common interests. DUFAS has drawn up the DUFAS Asset Managers’ Code (the Code). You will find this code on our website. This Code contains a number of principles. The members of DUFAS have agreed to act in accordance with these principles. Triodos Investment Management endorses these principles. The principles are not new for Triodos Investment Management and were already incorporated in our way of working:- We act in the interests of you, our clients;- We offer our investment institutions primarily

through distributors inside and outside the Triodos group; they are the first point of contact for clients;

- We act honourably;- We control conflicts of interest; to this end, we

have drawn up a policy that governs how we deal with conflicts of interest within Triodos Investment Management. We also provide information about this in the prospectus and where relevant on the website;

- We act professionally and conscientiously;- We communicate clearly and transparently;- We are open about our remuneration policy. We

provide information about this policy on page 27 of this annual report and on the website;

- We are transparent about costs. We explain the costs on pages 50 and 51 of this annual report and in the prospectus;

- We adhere to this Code and to the Principles of Fund Governance of Triodos Investment Management (see website). Certain elements of the Principles of Fund Governance of Triodos Investment Management are a more detailed version of the general principles of the Code.

Outlook

The market conditions are improving. There are signs that the economy is picking up further and that due to the ECB’s monetary easing, the property markets are enjoying increasing interest from investors.

In 2015 the fund will pro-actively manage the existing portfolio as well as consider possibilities for further enhancing the sustainability of the portfolio, possibly by adjusting the composition of the portfolio. When acquiring new properties, the investment policy continues to centre on sustainable office buildings in the urban areas of the Netherlands. The focus is on the sustainability of buildings and maintaining the CO2 neutrality that has been achieved is an important factor. The selected locations must, moreover, be easily accessible by public transport. Effective collaboration with the tenants and high-quality leases also remain areas of attention. Triodos Vastgoedfonds aims to continue to pursue its stable distribution policy in 2015.Finally, it would be expedient to expand the fund in order to improve its quality, reduce the risks, strengthen the fund’s balance sheet and enhance the marketability of the shares. In 2015 the Board of the fund will explore the possibilities for expanding the portfolio.

Zeist, the Netherlands, 9 April 2015

The fund manager for Triodos Vastgoedfonds Guus Berkhout

The Board of Triodos Investment Management BV Marilou van Golstein BrouwersMichael Jongeneel

19

Triodos Vastgoedfonds is a closed-end investment company with variable capital. Private investors can buy shares in Triodos Vastgoedfonds via Triodos Bank and via the auction market of Euronext Amsterdam. Triodos Vastgoedfonds is managed by Triodos Investment Management BV.

Triodos Investment Management holds a licence under the Wft. The AFM is the licensing supervisor and performs the conduct-of-business supervision. De Nederlandsche Bank NV is charged with the prudential oversight.

The board of directors of Triodos Investment Management consists of Marilou van Golstein Brouwers and Michael Jongeneel. Triodos Investment Management BV is managed by the two-member board of management.

An independent Supervisory Board monitors the investment policy and advises the Board. Members of the Supervisory Board are appointed by the General Meeting of Shareholders on the recommendation of the holder of priority shares. The Supervisory Board comprises Kees Duijvestein (chair), René Geskes, Meiny Prins and Carel de Vos tot Nederveen Cappel. Properties are acquired partly on the basis of the recommendation received from an investment committee consisting of John Mak and Theo Overbeeke. The acquisition of real estate and management of the property portfolio is carried out in close consultation with Bouwfonds Investment Management.

In 2011 Triodos Investment Management BV joined the Financial Services Complaints Tribunal (Stichting Klachteninstituut Financiële Dienstverlening, or Kifid).

Operating procedure

Triodos Vastgoedfonds acquires real estate that meets the criteria defined by the fund. Triodos Vastgoedfonds manages all the properties that it owns in a sustainable manner. Rent and other income received by the fund is distributed to the shareholder net of costs if the amount of equity is sufficient.

Sustainability reporting

Triodos Vastgoedfonds is managed by Triodos Investment Management BV, a wholly owned subsidiary of Triodos Bank NV. The staff of Triodos Investment Management BV who are involved in managing the funds are employed by Triodos Bank NV. The Triodos Bank annual report contains an integral sustainability report that applies to all the companies within the Triodos group.

Triodos Bank has been using the guidelines drawn up by the Global Reporting Initiative (GRI) since 2001. GRI was established in 1997 by the United Nations and the Coalition for Environmentally Responsible Economies. GRI aims to establish a consistent framework for sustainability reporting and thus make performances objective and easier to compare. Triodos Bank is one of GRI’s organisational stakeholders.

In 2013 GRI introduced new guidelines aimed at making reporting more relevant for the sustainability impact of the institution and more useful for its stakeholders. This is affected mainly by focusing attention on the issues that the organisation and its stakeholders find the most important or essential for their activities. This approach, which was first used for the report for 2013, has been developed further. In the report for 2014 the G4 guidelines have been applied comprehensively. Further information about the application of the G4 guidelines can be found on www.annual-report-triodos.com.

General information

20

Our reporting is based on internal and external data. This year’s report was prepared partly on the basis of discussions, including a thinking session with a number of external parties organised specifically for this purpose.

Climate neutral entrepreneurship

In addition to Triodos Vastgoedfonds, Triodos Bank is also CO2 neutral. Triodos Bank’s environmental policy is based on the trias energetica. This means that energy consumption is reduced as much as possible, that sustainable energy or sustainable resources are used whenever possible and that the climate impact of energy that is generated is offset. The bank thus minimises and offsets its environmental impact. Triodos Bank is a climate neutral, CO2-neutral organisation.

Further information about the social and environmental performance of Triodos Bank and its investment funds can be found in the Triodos Bank annual report.

21

Consolidated balance sheet as at 31 December, 2014 22

Consolidated profit and loss account for 2014 23

Consolidated statement of realised and unrealised results for 2014 24

Consolidated cash flow statement for 2014 25

Consolidated statement of changes in the number of shares outstanding 26

Notes to the consolidated balance sheet and profit and loss account 27

Separate balance sheet as at 31 December 2014 54

Separate profit and loss account for 2014 55

Notes to the separate annual accounts 56

Notes to the separate balance sheet 57

Annual accounts 2014Triodos Vastgoedfonds NV Page

22

Consolidated balance sheet as at 31 December 2014

before profit appropriation (amounts in EUR) Note* 2014 2013

Assets

Fixed assetsReal estate 1 69,310,000 71,045,000Work in progress 2 800 12,852Other long-term assets 3 218,445 280,137

Total fixed assets 69,529,245 71,337,989

Current assetsReceivables and prepayments and accrued 4 211,477 174,258Cash and cash equivalents 5 2,177 5,802

Total current assets 213,654 180,060

Totaal assets 69,742,899 71,518,049

Liabilities

EquityIssued capital 6 4,199,496 31,916,166Share premium 7 50,965,991 23,249,321Other reserves 8 -26,676,860 -22,138,471Undistributed result 9 1,452,357 -2,858,823

Total equity 29,940,984 30,168,193

Debt

Long-term debtExternal funding 10 36,325,864 36,364,689

Short-term debtExternal funding 11 1,247,330 888,617Creditors and other liabilities 12 2,228,721 4,096,550

Totaal debt 39,801,915 41,349,856

Totaal liabilities 69,742,899 71,518,049

* The numbers of the items in the financial statements refer to the numbers of the notes to the balance sheet and the profit and loss account. The notes are an integral part of the financial statements.

23

Consolidated profit and loss account for 2014

(amounts in EUR) Note* 2014 2013

Gross rental income 6,816,914 6,715,042Construction period interest – 39,881Other income from investments 13 1,321 –

Total income from investments 6,818,235 6,754,923

Service charges passed on 828,556 868,574Service charges paid -819,221 -981,099

Net service charges 9,335 -112,525Property expenses 14 -954,763 -1,222,875

Total property expenses -945,428 -1,335,400

Net rental income 5,872,807 5,419,523

Unrealised changes in the value of investments in real estate 15 -1,770,805 -5,318,500

Changes in the value of receivables 16 -19,903 –

Management costs 17 -703,418 -881,831

Other operating income 44,772 6,129Other operating costs -83,817 -136,824

Net other operating result 18 -39,045 -130,695

Net operating result 3,339,636 -911,503

Funding charges -1,886,074 -1,948,620Interest income 24 1,300

Net funding results 19 -1,886,050 -1,947,320

Pre-tax result 1,453,586 -2,858,823

Corporation tax 20 -1,229 –

Net result 1,452,357 -2,858,823

* The numbers of the items in the financial statements refer to the numbers of the notes to the balance sheet and the profit and loss account. The notes are an integral part of the financial statements.

24

Consolidated statement of realised and non-realised results

(amounts in EUR) 2014 2013

Net result 1,452,357 -2,858,823

Items which in accordance with the definition in IAS 1 will never be transferred to the resultChange due to positive revaluations – -287,451Total unrealised results – -287,451

Total realised and unrealised results 1,452,357 -3,146,274

The notes are an integral part of the financial statements.

25

Consolidated cash flow statement for 2014

(amounts in EUR) 2014 2013

Cash flow from operational activitiesRental income received 6,703,382 7,097,024Property expenses -1,062,405 -1,228,767Management fees and other operating costs -833,851 -1,187,896Interest paid -1,882,975 -1,957,309Interest received 24 1,300Increase/decrease in other receivables and prepayments and accrued income -21,180 491,247Other income -1,341 7,471

2,901,654 3,223,070

Cash flow from investment activitiesInvestments in real estate including purchase costs -117,546 -854,728Divestments of real estate including selling expenses – 75,000

-117,546 -779,728

Cash flow from funding activitiesIssue minus redemption of shares – 70,672Dividend paid (for 2012 and 2013) -3,107,621 –Repayment of long-term debt -738,825 -738,780Increase/decrease short-term debt 1,058,713 -1,781,111

-2,787,733 -2,449,219

Change in cash and cash equivalents -3,625 -5,877

The notes are an integral part of the financial statements.

26

(amounts in EUR)Issued capital

Share premium

Other reserves

Retained earnings for

the year Total

Balance as at 31 December 31,916,166 23,249,321 -22,138,471 -2,858,823 30,168,193Recapitalisation -27,716,670 27,716,670 – – 0Dividend distribution 2013 – – – -1,679,566 -1,679,566Profit appropriation 2013 – – -4,538,389 4,538,389 0Result 2014 – – – 1,452,357 1,452,357

Balance as at 31 December 2014 4,199,496 50,965,991 -26,676,860 1,452,357 29,940,984

The notes are an integral part of the financial statements.

Consolidated statement of changes in the number of shares outstanding for 2014

27

General

Triodos Vastgoedfonds is a closed-end investment company with variable capital within the meaning of article 2:76a of the Dutch Civil Code and has its registered office in Zeist, the Netherlands. Private investors can buy shares in Triodos Vastgoedfonds via Triodos Bank and via the auction market of Euronext Amsterdam.

The investments owned by Triodos Vastgoedfonds are illiquid. The ratios for illiquid investments relative to the fund’s equity are presented in the key figures included in this report. All special arrangements concerning this category of investments are, if applicable, described in this report.

AIFMD

Triodos Investment Management BV is the manager of Triodos Vastgoedfonds. On 22 July 2014 the Alternative Investment Fund Managers Directive (AIFMD), a European directive, was implemented in the Dutch Financial Supervision Act (Wet op het financieel toezicht - Wft). This European directive is almost exclusively directed at the Manager of Triodos Vastgoedfonds. Because Triodos Investment Management had a license to manage investment institutions under the Dutch Financial Supervision Act on 21 July 2013, this license was converted into an AIFMD licence by operation of law on 22 July 2014. In line with the AIFMD, Triodos Vastgoedfonds has had to appoint a custodian. BNP Paribas Securities Services has been appointed as custodian. The custodian is charged with the safekeeping of the investments. The custodian furthermore has a number of supervisory duties. For instance, the custodian must supervise the manner in which assets are acquired and reported. The custodian also monitors the cash flows. The implementation of the directive was completed in 2014.

Please refer to the prospectus of Triodos Vastgoedfonds for a description of the way in which liability with respect to outsourcing of custody of the investment entity’s assets is regulated.

Remuneration policy

Based on Article 22(2) of the Alternative Investment Fund Managers Directive (“AIFMD”) and section XIII (Guidelines on disclosure) of the ‘ESMA Guidelines on sound remuneration policies under the AIFMD’, managers are required to at least provide information on their remuneration practices for employees whose professional activities have a material impact on its risk profile (so-called “identified staff”).

All of the staff members of Triodos Investment Management are employed by Triodos Bank. Triodos Bank believes adequate and appropriate remuneration for all of its employees is very important. The core elements of Triodos Bank’s international remuneration policy are set out in the Principles of Fund Governance, which can be accessed via www.triodos.nl.

Notes to the consolidated balance sheet and profit and loss account

28

The following table sets out the total remuneration, broken down into fixed and variable remuneration, for all the staff employed by Triodos Investment Management, categorized into senior management and other identified staff.

(amounts in EUR)

All staff of Triodos Investment Ma-

nagement

“Identified staff” in senior manage-

ment positionsAll other

“Identified staff”

Number of staff (average for 2014) 113 6 28

RemunerationTotal fixed remuneration (for 2014) 8,916,911 995,936 2,581,671Total variable remuneration (for 2014) 49,925 12,800 10,825

Statement of compliance

These annual accounts were prepared in accordance with International Financial Reporting Standards as adopted by the European Union (hereinafter: EU-IFRS) and the interpretations that have been issued by the International Accounting Standards Board (IASB) and that ensue from the Wft or the Dutch Civil Code Book 2, Title 9.

Functional currency and presentation currency

The annual accounts are presented in euros, as the euro is the functional currency of Triodos Vastgoedfonds. Unless indicated otherwise, all financial information in euros has been rounded.

Use of estimates and assumption

In order to prepare these consolidated annual accounts, the management of the fund made judgements, estimates and assumptions that affect the application of accounting principles and the reported value of real estate. The actual figures may differ from these estimates. Note 1 of the Notes to the consolidated balance sheet on page 37 shows the change in the value of real estate.Estimates and underlying assumptions are constantly reviewed. Changes in estimates are accounted for prospectively.

Changes in the financial accounting principles

As of 1 January 2013 Triodos Vastgoedfonds has observed the following standards and changes to standards, including any consequent changes to other standards:

29

- In December 2013 the IASB published its annual improvements, which became effective on 1 July 2014. The improvements to IAS 24: Related Parties refer to the situation in which an entity may be identified as ‘key management personnel’. The improvement to IFRS 13: Fair value measurement includes a modification of the scope of the ‘portfolio exception’ for the valuation of a group of financial instruments (assets as well as liabilities) on a net basis. The improvements have no significant impact on the annual accounts of Triodos Vastgoedfonds.

- On 31 October 2012 the IASB published the IASB ‘Investment Entities: amendments to IFRS 10, IFRS 11, IFRS 12, IAS 27 and IAS 28’, which came into effect on 1 January 2014. The EU adopted these changes on 20 November 2013. Subject to certain conditions, the changes provide for exemption from consolidation for investment entities and give a different definition of the term ‘control’. Triodos Vastgoedfonds qualifies as a real estate entity within the meaning of IFRS 10 and is required to prepare consolidated annual accounts. Triodos Vastgoedfonds prepared consolidated annual accounts even before the adoption of the amendments and this change in IFRS therefore has no impact for the fund.

New standards and changes to and interpretations of the existing standards that are of limited relevance for the fund and have not yet come into effect:

- With the publication of IFRS 9 Financial Instruments in July 2014, the International Accounting Standards Board (IASB) completed the last element of a substantial project that was undertaken in reaction to the financial crisis. The total package of improvements as introduced with IFRS 9 includes a logical model for classification and valuation, a prospective ‘expected loss’ impairment model and a modified approach for hedge accounting.

- The effective date for the compulsory adoption of IFRS 9 Financial Instruments is 1 January 2018. The EU has not yet adopted this standard. IFRS 9 is not expected to have a significant impact, because the fund already values and presents all financial instruments based on fair value.

Calculation of the fair value of investments

Investments are recognised in the balance sheet at fair value. EU-IFRS distinguishes three different levels:Level I - Fair value based on published prices realised in an active market Level 2 - Fair value based on available market informationLevel 3 - Fair value not based on available market information

All investments owned by Triodos Vastgoedfonds are level 3 investments. During the reporting period no transfers between the different levels occurred. For an overview of the changes in the level 3 investments we refer to note 1 of the Notes to the consolidated balance sheet.

Real estate

Investments in real estate are level 3 real estate investments that are held in order to realise rental income and/or increases in value. When determining the value of level 3 investments, subjective assumptions apply. The manager uses parties that operate independently from the operational departments to monitor the valuation methods and to make the subjective estimates as prudently as possible. Below we will describe how investments in real estate are recognised and how their fair value is determined.

30

Initial valuation

Real estate investments that are acquired during the financial year are recognised at their acquisition price plus the purchase costs. The purchase costs include all external costs related to the purchase of real estate, including the acquisition costs, comprising property transfer tax, notarial charges, registration charges, estate agent’s commission and the costs of external due diligence. Expenditure incurred after the purchase has been made is added to the book value when it is likely that such expenditure will result in future economic income. All other expenditure, for instance on repairs and maintenance, is charged to the result for the period in which the costs are incurred.

Subsequent valuation

Investments in real estate are stated at their current value, i.e. their fair value. The fair value is based on the market value, being the estimated amount for which a property should reasonably be expected to exchange on the balance sheet date between a willing buyer and a willing seller in an arm’s-length transaction after proper marketing wherein the parties have each acted knowledgeably, prudently, and without compulsion. The market values are determined on a quarterly basis, by means of valuations. Each year, the entire portfolio is valued by an external valuer. After three years a new external valuer is appointed. The external valuer is independent and holds a recognised and relevant professional qualification and has recent experience with regard to the location and class of the real estate investments that are to be valued. Real estate that has not been valued by an external valuer during the relevant quarter is valued in-house.

The value of property is determined by capitalising the gross or net rental value (gross rental value less the charges related to the property). The rental value is determined by means of the so-called comparative method: by comparing the property with a supply of comparable properties or realised transactions in similar properties. The value is determined by dividing the rental value by the required gross or net yield. This yield is determined by assessing factors such as the market conditions (supply and demand), economic conditions (interest rates, inflation, etc), location (surroundings, accessibility, infrastructure, amenities and developments) and the quality of the property (type of construction, quality, state of repair and potential uses). In case of any discrepancy between the rent that is actually paid and the rental value, the present value of any such discrepancy is calculated for the remaining term of the lease. The value that has been determined based on the comparative method is compared with the value that is determined using the discounted cash flow method. The final valuation is determined by weighting both values. The discounted cash flow method involves calculating the present value of all expected future income and expenditure as per the valuation date, taking into account potential vacancies. During this process, the rental value trend, rate of inflation and exit value are also taken into account. The discount rate is estimated based on the long-term government bond yield plus a risk premium that depends on the degree of investment risk of the property itself. If Triodos Vastgoedfonds decides to redevelop an existing investment property for continued future use as a property investment, the property will remain a real estate investment recognised at fair value.

Changes due to (un)realised revaluations of investments are taken through the profit and loss account. That part of the result that concerns unrealised revaluations shall be added to or deducted from the revaluation reserve or other reserves via the profit appropriation, depending on whether the revaluation is positive or negative. The tax laws allow realised revaluations to be added to the reinvestment reserve. Triodos Vastgoedfonds will in principle make use of this option.

31

Work in progress

Work in progress is stated at fair value. If an internal or external valuation is available for the project to which the work in progress is related, the fair value is calculated based on the appraised value minus any future costs. During the valuation process, the current stage of development of the project is taken into account. If no internal or external valuation is available, the cost price is used as the best approximation of the fair value.

Subsidiaries

Subsidiaries are companies over which Triodos Vastgoedfonds may exercise decisive control. The fund can exercise decisive control if it exercises indirect control over the financial and operational policies of the company for the benefit of its own operations. When determining the degree of control, potential voting rights that may currently be exercised are taken into account. The figures of these subsidiaries are included in the consolidated figures from the date on which the control comes into effect until the date on which this ceases to exist.The consolidated annual accounts include the financial figures for the following companies, in addition to those for Triodos Vastgoedfonds:- Triodos Vastgoedfonds Monumenten BV, Zeist, 100% interest- Triodos Vastgoedfonds Duurzame Concepten BV, Zeist, 100% interest- Triodos Immobilien GmbH in Liquidation, Frankfurt am Main, 100% interestTriodos Vastgoedfonds NV has full control over these wholly owned subsidiaries. The value of the subsidiaries is determined by using the equity method.

Other long-term assets (capitalised costs)

Capitalised rent-free periods and other lettings costs are initially stated at cost price and subsequently valued based on amortised costs, which are amortised over the term of the lease.

Receivables and prepayments and accrued income

Other receivables and prepayments and accrued income are carried at their amortised cost price less impairment.

Cash and cash equivalents

Cash and cash equivalents include demand deposits, as well as short-term, highly liquid investments that may be converted into a fixed amount of cash at any time and that entail only a very limited risk of changes in value.

Equity

Equity represents the value of all issued (ordinary and priority) shares in the fund.

Interest-bearing debt

Interest-bearing debt is initially recognised at cost price less the attributable transaction costs. Subsequent to initial recognition, interest-bearing debt is recognised in the balance sheet at its amortisation value, while differences between the cost price and the repayment value are recorded in the result during the term to maturity based on the effective interest method.

32

Other liabilities

Creditors and other liabilities are stated at their amortised cost price.

Rental income

Rental income from real estate investments covered by operational leases is added to the profit and loss account on a linear basis over the term of the lease contracts. Lease incentives in the form of a rent-free period are considered an inherent part of the rental income. Such incentives are amortised over the term of the lease contract. Service, property and management expenses

Service expenses for service contracts with third parties are passed on to tenants one-on-one. The service expenses with regard to vacant properties are charged directly to the result. Service expenses mainly consist of charges for gas, water and light and cleaning and security costs. The property expenses include the expenses that can be attributed directly to the operation of the property investments, excluding the expenses that are passed on to tenants. These mainly include taxes, insurance premiums, maintenance costs and consultancy fees. These expenses are charged to the result when they are incurred. Management expenses are expenses that cannot be attributed directly to the operation of property. These include fees payable to the manager, office expenses, consultancy fees, publicity costs, auditor’s fees, depository fees, charges for the supervision exercised by the Dutch Financial Markets authority and listing charges.

Other operating income and costs

Other operating income includes the surcharges and discounts charged when issuing or redeeming shares, as well as other income from operating activities. Other operating costs include the costs related to the registration of shares, marketing expenses and other operating expenses.

Net funding charges

Net funding charges consist of the interest payable for outstanding debt and are calculated by means of the effective interest rate method.Interest income is attributed to the period that it relates to.

Segment report

A segment constitutes a group of assets and activities with segment-specific risks and outcomes. The following segmented overview presents the investments and results for each country where Triodos Vastgoedfonds operates.

33

The values of the investments in each country as at 31 December 2014 are as follows:

(amounts in EUR) The Netherlands Germany

Investments as at 31 December 2014 69,310,000 –Result 2014 1,421,651 35,706

The positive result in Germany is due to EUR 44,772 in income from a debtor whose debt had already been written off but whose possessions had been seized, and EUR -9,066 in costs.

Triodos Vastgoedfonds uses segmentation into sustainably constructed and managed property, sustainability managed listed buildings and sustainably managed existing real estate. The value of the investments in each segment as at 31 December 2014 is as follows:

(amounts in EUR) Acquisition value Revaluation Fair value

Sustainably constructed and managed 42,348,708 -9,628,708 32,720,000Listed building, sustainably managed 27,005,420 -3,695,420 23,310,000Existing real estate, sustainably 23,791,424 -10,511,424 13,280,000

93,145,552 -23,835,552 69,310,000

Direct and indirect return

The direct investment result comprises the rental income minus the property expenses, management expenses, general expenses and funding costs.The indirect investment result comprises the revaluation of property investments and the net profit on the divestment of investments.

Cash flow statement

The cash flow statement is prepared using the direct method.

Management of the financial risks

The use of (derivative) financial instruments exposes the fund to various financial risks. These risks are caused by the management of the investment portfolio. The policy pursued by Triodos Vastgoedfonds with respect to these risks is described below.

Market risk

Market risk is the risk that the value of an investment will fluctuate as a result of external factors that cause changes in the level of, for instance, the rate of inflation, interest rates, currency rates or the market price of investments. The value of real estate is impacted by a wide range of external factors, including macro-economic conditions, the rate of inflation and rental income. The greater the fluctuation in the development of these factors, the greater the market risk. Triodos Vastgoedfonds cannot influence the macro-economic factors that impact the value of its real estate. However, the fund tries to ensure the

34

attractiveness of its real estate through appropriate management of its properties and by means of marketing efforts.

Interest rate and currency risk

Developments with respect to the rate of inflation and interest rates present an interest rate risk. Via the debt position of the fund, the interest rate trend may have an impact on the fund’s return. The fund’s policy is aimed at keeping the fixed-rate periods of its debt aligned with the lease terms. The structure of the fixed-rate periods of the fund’s debt is set out on pages 40 through 42. The fund does not use derivative financial instruments to hedge interest rate risks.Because all assets, liabilities and results of the fund are denominated in euros, the fund is not exposed to currency risk.

Cash flow risk

Cash flow risk is the risk that future cash flows related to a financial instrument will fluctuate in volume. The fund has no investments that involve variable cash flows and is therefore not exposed to a significant cash flow risk. Future rental income is, however, dependent on contract revisions at the end of the lease term.

As at 2014 year-end the average term of the leases that have been entered into weighted according to annual rental income is 5.0 years (2013: 5.3 years). The lease terms weighted according to annual rental income can be broken down as follows:

31-12-2014 31-12-2013

<1 year 7.1% 0.2%1-3 years 24.5% 14.9%3-5 years 38.1% 39.6%5-10 years 27.4% 42.4%>10 years 2.9% 2.9%

Total 100.0% 100.0%

The development of rental income is also determined by the rate of inflation. Upon the expiration of leases, rents are adjusted based on arm’s length conditions. Rents are in principle indexed on an annual basis.

The occupancy rate for real estate can decline due to the termination of leases or bankruptcy of tenants. In order to control the vacancy rate, the fund aims to enter into leases with a medium to long term whenever possible. As at 2014 year-end, the vacancy rate for the properties in the fund’s portfolio is 2.9%.

Credit risk

Credit risk is the risk that a specific counterparty cannot fulfil its obligations towards the fund. The fund’s policy is aimed at limiting the credit risk by subjecting (potential) tenants to a solvency test and by diversifying tenants across various industries and sectors in order to prevent the fund from becoming dependent on specific economic developments that only have an impact on certain sectors. The segment

35

report on page 31 shows in which segments the credit risk is concentrated.

Breakdown of rental income according to sector of tenants

At 2014 year-end the fund had 38 tenants (2013: 36) spread across the following sectors:

23%NON-PROFIT

21%HEALTHCARE SECTOR

15%ENERGY

14%CONSULTANCY

10%FINANCIAL SERVICES

5%REAL ESTATE

5%ELECTRICAL ENGINEERING

7%OTHER

Concentration risk is a form of credit risk that can occur if Triodos Vastgoedfonds has a significant concentration of investments in a particular region. In order to limit this risk, the investments are spread across various regions of the Netherlands.

0

2

4

6

8

10

12

14

2040203520222021202020192018201720160

2

4

6

8

10

20222021202020192018201720162015

Term to maturity of loans(amounts in EUR x 1,000,000)

Expiration years of fixed-rate periods of loans (amounts in EUR x 1,000)

36

Geographical diversification of rental income

Liquidity risk

Liquidity risk is the risk that Triodos Vastgoedfonds has no possibility of obtaining the financial means it needs to be able to fulfil its financial obligations at a certain point in time. Triodos Investment Management further formalised its liquidity management policy in 2014 and will continue to focus on this policy as part of its risk management efforts in 2015.

The following cash flows have a significant impact on the liquidity risk:

Rental income of EUR 6.7 million in 2014 (2013: EUR 7.1 million).The rental income offers stable and predictable cash flows to which the fund can respond quickly. The quality of these cash flows is monitored on a permanent basis. Please see the notes on credit and cash flow risk for further information.

Distributions to shareholders amounting to EUR -3.1 million in 2014 (2013: EUR 0.0 million) and transactions related to the acquisition and divestment of real estate of EUR -0.1 million (2013: EUR -0.8 million).Because these cash flows are predictable and are scheduled by the manager, they constitute a limited threat in terms of liquidity risk.

Management expenses of EUR -0.8 million in 2014 (2013: EUR -1.2 million) and refinancing transactions of EUR 0.3 million (2013: EUR -2.5 million).

Because these cash flows are predictable, they constitute a limited threat in terms of liquidity risk..

Leverage ratio

Leverage ratios provide insight into the degree to which the fund uses debt as compared with the net asset value. The leverage ratio is calculated by using the so-called “commitment method of calculation”, where 100% means that there is no leverage.

As at 2014 year-end the leverage ratio based on the “commitment method of calculation” is 352.8%.

37

Sensitivity analysis

Below is a summary of some of the variables that may have a significant impact on the fund’s equity or result:

Variables Explanation Situation in 2014

Occupancy rate The occupancy rate indicates which percentage of the real estate is occupied and may fluctuate depending on the expiration of leases. We also refer to the notes on cash flow risk.

97.1%

Rental income per m2

This indicates the rent per m2 and may change following the expiration of leases, depending on market developments. We also refer to the notes on cash flow risk.

EUR 148

GIY In the real estate sector, the GIY (Gross Initial Yield) is a popular instrument for expressing the value and quality of a building. The gross initial yield is expressed as a percentage and is calculated by dividing the rental income in the first year by the total invest-ment. This in effect reflects the degree of risk entailed by the property investment as perceived by the market and may go up or down depending on market developments.

9.84%

Average borrowing rate

This is determined by the funding costs payable to the bank providing the loan and by the risk premiums that this lender believes to be opportune for the portfolio. As the borrowing rate is fixed for a longer period of time, which limits its impact for the reporting period, this variable has not been included in the sensitivity analysis.

4.99%

The sensitivity of the fund to these variables is as follows:

Gevoeligheid op eigen vermogen (indicatief)

Occupancy rate +1% 693,000Occupancy rate -1% -693,000Rental income per m² +1% 693,000Rental income per m² -1% -693,000GIY +1% -698,000GIY -1% 712,000

38

Tax aspects of the fund

Corporation tax

Triodos Vastgoedfonds is a fiscal investment institution within the meaning of Article 28 of the Dutch Corporation Tax Act 1969. This means that the fund is in principle liable to corporation tax at a rate of 0%, provided that all the applicable conditions are met. One condition is that the taxable profit that is available for distribution must be fully distributed within eight months after the end of the relevant financial year. In Dutch law this is referred to as the doorstootverplichting. The taxable result for the 2014 financial year is negative. A distribution is not required in order to comply with the doorstootverplichting.

For the purpose of corporation tax, Triodos Vastgoedfonds is part of a tax entity of which Triodos Vastgoedfonds NV is the parent company and Triodos Vastgoedfonds Monumenten BV is the subsidiary. The corporation tax is settled between Triodos Vastgoedfonds NV and its subsidiary as if the entities are independently liable to pay tax. However, the two companies remain severally liable for the tax liabilities of the companies that are part of the tax entity.

Triodos Vastgoedfonds Duurzame Concepten BV, another subsidiary of Triodos Vastgoedfonds NV, is liable to pay tax under the Corporation Tax Act 1969 due to the nature of its activities and is therefore not part of the tax entity.

Dividend tax

In accordance with the Dutch Dividend Withholding Tax Act 1965, Triodos Vastgoedfonds in principle withholds dividend tax at a rate of 15%. If the shareholder is liable to Dutch income tax or corporation tax, the dividend tax withheld by the fund constitutes advance income tax or advance corporation tax respectively and may therefore in principle be set off against such tax depending on the specific facts and circumstances. Please ask your advisor whether this applies to you. For further information we refer to the prospectus of the fund, which may be obtained free of charge from Triodos Bank and via www.triodos.nl.

VAT

Triodos Vastgoedfonds qualifies as a company based on the Turnover Tax Act 1968. Collective investment management is in principle exempt from VAT. The management fee charged to the fund by Triodos Investment Management BV is therefore exempt from VAT. For the purpose of VAT Triodos Vastgoedfonds is part of a tax entity of which Triodos Vastgoedfonds NV is the parent company and Triodos Vastgoedfonds Monumenten BV is the subsidiary. The corporation tax is settled between Triodos Vastgoedfonds NV and its subsidiary as if the entities are independently liable to pay tax. However, the two companies remain severally liable for the tax liabilities of the companies that are part of the tax entity.

39

Notes to the consolidated balance sheet as at 31 December 2014

1. Real estate

(amounts in EUR) 2014 2013

Book value as at 1 January 71,045,000 75,911,134Investments including acquisition costs 35,805 452,366Revaluation of properties still present in the portfolio -1,770,805 -5,318,500

Book value as at 31 December 69,310,000 71,045,000

Any acquisition costs for properties are an inherent part of the acquisition price. Real estate is stated at fair value. As a rule, the initial valuation will result in a negative revaluation, because the acquisitions costs are not taken into account for the valuation. Valuations are performed in line with the guidelines of the IPD/ROZ property index. Important input variables include rents and gross initial yields.

2. Work in progress

As at 2014 year-end this comprises consultancy fees for a roof terrace for the property at Willemsplein in Arnhem.

3. Other long-term assets

(amounts in EUR) 2014 2013

Capitalised estate agent's commissionBook value as at 1 January 79,235 71,903Capitalised amount 37,155 25,791Depreciation -26,880 -18,459

89,510 79,235Capitalised rent discountBook value as at 1 January 178,158 130,621Capitalised amount 52,966 155,634Charged to the result -119,851 -108,097

111,273 178,158

Capitalised loan commissionsBook value as at 1 January 22,744 27,824Depreciation -5,082 -5,080

17,662 22,744

Book value as at 31 December 218,445 280,137

40

4. Receivables and prepayments and accrued income

(amounts in EUR) 2014 2013

Rent debtors 60,334 41,449Costs to be charged on 18,452 17,227Value added tax 45,315 33,909Corporation tax 1,865 –Sustainabilisation subsidy receivable 75,000 75,000Other prepayments and accrued income 10,511 6,673

Book value as at 31 December 211,477 174,258

The term of other receivables and other prepayments and accrued income is less than 1 year. Specification of rent debtors

(amounts in EUR) 2014 2013

Overview of items outstanding as at 31 December 64,302 41,449Less: provision -3,968 –

Rent debtors as at 31 December 60,334 41,449

5. Cash and cash equivalents

(amounts in EUR) 2014 2013

Triodos Bank, current accounts 319 458KAS BANK, current account 197 20Rabobank, current accounts 15 130GLS Bank, current account 1,646 5,194

Balance as at 31 December 2,177 5,802

Cash and cash equivalents are at the fund’s free disposal.As at 2014 year-end, the interest rate for the current accounts held at Triodos Bank is 0%. As at 2014 year-end, the interest rate for the current account held at KAS BANK is -0.20%.As at 2014 year-end, the interest rate for the current accounts held at Rabobank is 0.60% for one account and 0.0% for the other account.As at 2014 year-end, the interest rate for the current accounts held at GLS Bank is 0%.

41

6. Issued capital

(amounts in EUR) 2014 2013

Issued and paid up as at 1 January 31,916,166 42,244,272Issued minus redeemed – -249,317Lowering of nominal value -27,716,670 -10,078,789

Issued and paid up as at 31 December 4,199,496 31,916,166

As at the balance sheet date, the authorised capital amounts to EUR 10,000,050 (2013 year-end: EUR 76,000,038), consisting of 20,000,000 ordinary shares and 10 priority shares. On 11 December 2014 the nominal value of all shares was lowered from EUR 3,80 to EUR 0.50.

The priority shares are owned by Stichting Triodos Holding and entitle the holder to a dividend of 4% of the capital paid up on these shares. The ordinary shares have been issued via Euronext Amsterdam.

Changes in the number of shares issued, in number of shares:

(number of shares) 2014 2013

Balance as at 1 January 8,398,991 8,448,854Shares issued during the year – 113,147Shares redeemed during the year – -163,010

Shares issued to other parties than the Fund as at 31 December 8,398,991 8,398,991

As at 2014 year-end the total number of shares issued amounts to 8,536,828.

7. Share premium

(amounts in EUR) 2014 2013

Balance as at 1 January 23,249,321 12,860,245Change due to issue and redemption of shares – 310,287Recapitalisation due to lowering of nominal value 27,716,670 10,078,789

Balance as at 31 December 50,965,991 23,249,321

The full share premium amount is recognised by the tax authorities.

42

8. Other reserves

This item includes the negative revaluations of real estate investments, the tax difference reserve and tax adjustments.

These reserves have changed as follows:

(amounts in EUR) 2014 2013

Balance as at 1 January -22,138,471 -16,071,699Transferred from revaluation reserve – 287,451Transferred from the undistributed result -4,538,389 -6,354,223

Balance as at 31 December -26,676,860 -22,138,471

9. Undistributed result

The undistributed result is the result for the financial year that has not yet been distributed.

This item has changed as follows:

(amounts in EUR) 2014 2013

Balance as at 1 January -2,858,823 -4,674,426Distributions to shareholders relating to previous financial year -1,679,566 -1,679,797Withdrawn from the other reserves 4,538,389 6,354,223

– –Undistributed profit for the year 1,452,357 -2,858,823

Balance as at 31 December 1,452,357 -2,858,823

43

10. Long-term debt

(amounts in EUR) 2014 2013

Loans from Triodos Groenfonds 7,437,174 7,437,174Loans from Triodos Bank 16,160,852 16,195,196Loans from Rabobank 12,600,000 13,300,000Short-term segment of loans from Rabobank – -700,000Loan from Stichting Nationaal Restauratiefonds (Dutch National Restauration Fund) 127,838 132,319

Balance as at 31 December 36,325,864 36,364,689

This item has changed as follows:Balance as at 1 January 36,364,689 37,803,469Loan repayments -38,825 -738,780Short-term segment of loans from Rabobank – -700,000

Balance as at 31 December 36,325,864 36,364,689

Triodos Groenfonds NV

The fund has taken out four long-term loans from Triodos Groenfonds NV:

Principal amount in EUR Maturity Interest rate Repayment

393,600 1 January 2016 2.700% until 1 January 2016 in full1,806,600 1 July 2019 3.900% until 1 July 2019 in full

945,174 1 July 2020 4.310% until 1 July 2020 in full4,291,800 1 April 2022 4.800% until 1 April 2022 in full

Triodos Bank NV

The fund has taken out seven long-term loans from Triodos Bank NV:

Principal amount in EUR Maturity Interest rate Repayment

4,500,000 1 January 2018 5.191% until 1 January 2018 In full400,000 1 August 2018 5.407% until 1 August 2018 In full

2,000,000 1 July 2021 5.250% until 1 May 2021 In full5,000,000 1 July 2022 5.300% until 1 May 2022 In full3,193,400 1 December 2022 4.960% until 1 December 2020 In full

712,626 1 July 2035 5.310% until 1 April 2020 EUR 8,586 per quarter354,826 1 July 2035 5.310% until 1 April 2020 In full

44

The collateral for the loans taken out from Triodos Groenfonds and Triodos Bank consists of:A first mortgage of EUR 40,000,000 plus 37.5% for interest and costs on the following properties:

- Kerkenbosch in Nijmegen - J.F. Kennedylaan in Baarn- Platinaweg in Emmeloord - Prins Hendrikstraat in Den Haag- Bosscheweg in Boxtel - Willemsplein in Arnhem- Huis van de Sport in Nieuwegein - Stationsweg in Groningen- Laan van Westenenk in Apeldoorn - Utrechtseweg in Amersfoort- Rostockweg in Groningen - Honingerdijk in Rotterdam

For the loans provided by Triodos Groenfonds and Triodos Bank, Triodos Vastgoedfonds must meet a number of ratios:

2014 2013 Standard

Solvency ratio 42.9% 42.2% > 35%Loan to Value entire portfolio 54.2% 52.4% < 70%Loan to Value for the portfolio funded by Triodos 51.6% 47.4% < 70%

Rabobank

Four long-term loans have been taken out from Rabobank:

Principal amount in EUR Maturity Interest rate Repayment