tri-m technologies (s) ltdrhpetrogas.listedcompany.com/newsroom/20090916_120047_t13_5fc4d... · ......

TRANSCRIPT

Tri-M Technologies (S) Ltd

Agenda

o The Acquisition o Rimbunan Hijau Group o The Oil Field o Production o Economic Evaluation o Technical Team o Future Outlook o Q & A

o On 12 Nov 2007, Kingworld Resources Limited (“KRL”) signed a Production Sharing Contract (“PSC”) with China National Petroleum Corporation (“CNPC”) relating to the joint production of Fuyu 1 Block, Songliao Basin, Jilin, China (“Fuyu 1 Block”).

o On 14 Mar 2008, the Company announced that it had signed a Memorandum of Understanding relating to the acquisition of KRL.

o On 18 Aug 2008, the Company announced that it had signed a Sale and Purchase Agreement (“SPA”) relating to the acquisition of KRL.

o On 27 Apr 2009, the Company announced that it had signed a Supplemental Agreement to amend certain terms in the SPA.

o On 29 Jun 2009, the Company announced that it had received the Approval-in-Principal in relation to the acquisition from SGX.

o On 30 Jul 2009, the Company obtained the Independent Shareholders’ Approval of the acquisition.

o On 17 Aug 2009, the Company announced the completion of the transaction.

The Acquisition - Background

Tiong Family

The Acquisition - Structure (Before)

The Company

Electronic Business

Acquisition Terms ◦ Debt Conversion into equity ◦ Consideration is S$110 million, of

which S$20 million to be paid by cash and S$90 million to be settled by 112.5 million shares at the price of S$0.8 per share

KRL (BVI)

Fuyu 1 Block

CNPC

PSC

KRL China Branch (PRC)

The Acquisition - Structure (After)

Tiong Family

The Company

Electronic Business

100% 100%

Before Completion After Completion

Number of Shares % Number of Shares %

Total shares 273,821,443 100% 401,321,443 100%

Surreyville 187,889,486 68.62% 202,889,486 50.56%

Vendors 0 0% 112,500,000 28.03%

Public 85,931,957 31.38% 85,931,957 21.41%

The Acquisition - Shareholding

After issuing consideration shares and converting the proposed shareholders’ loan (S$12m) into equity at the price of S$0.80 per share, the capital structure of the Company shall be as follows: -

Rimbunan Hijau Group (“RH Group”) is a multinational diversified conglomerate with headquarters in Sibu, Malaysia and controlled by the family of Tan Sri Datuk Sir Tiong Hiew King.

o Forestry, Timber Operations, and Reforestation RH Group is a market leader in the industry of forestry, timber and reforestation with operations in Malaysia, Papua New Guinea, New Zealand, Russia, Gabon, Equatorial Guinea, Congo, etc. It is the controlling shareholder of two main board listed companies in Kuala Lumpur, namely, Jaya Tiasa Holdings Bhd and Subur Tiasa Holdings Bhd.

o Oil Palm Plantations RH Group owns over 100,000 hectares of planted palm oil plantation together with four palm oil mills in Sarawak. It has a further land bank of approximately 400,000 hectares. It is the controlling shareholder of Rimbunan Sawit Bhd, a main board listed company in Kuala Lumpur.

RH Group

o Media Chinese International Ltd Media Chinese, a main board listed company in both Hong Kong and Kuala Lumpur, is one of the largest global media groups in Chinese language. It has 5 daily newspapers in 15 editions with over 1 million copies a day, 1 free daily newspaper, over 30 magazines and various online operations across cities in Southeast Asia, China and North America. It is also the controlling shareholder of One Media Group Ltd, a main board listed company in Hong Kong.

o Information Technology RH Group is also in the production of optical fibers, optical cables and associated devices and accessories. It also has the licenses of Network Facility Provider, Network Service Provider, and Application Service Provider in Malaysia.

o Others RH Group also has extensive investments in a number of industries, including mining, hospitality, biotech, toll road operation, tourism, etc.

RH Group

The Oil Field

Technical Professionals

o Beijing Petroleum University - conducted a feasibility study for evaluation purpose.

o Gaffney, Cline & Associates (“GCA”) - issued a technical report and an economic evaluation report.

Songliao Basin, Fuyu Reservior

General Information: o About 135 km from Changchun,

150 km south of Daqing, and 950 km northeast of Beijing.

o South of CNPC Xinmin and Xinmiao oilfield.

o Consists of 12 to 20 sand groups at a depth of around 1200 to 2000 mSS.

o The crude oil is generally around 28-32 API.

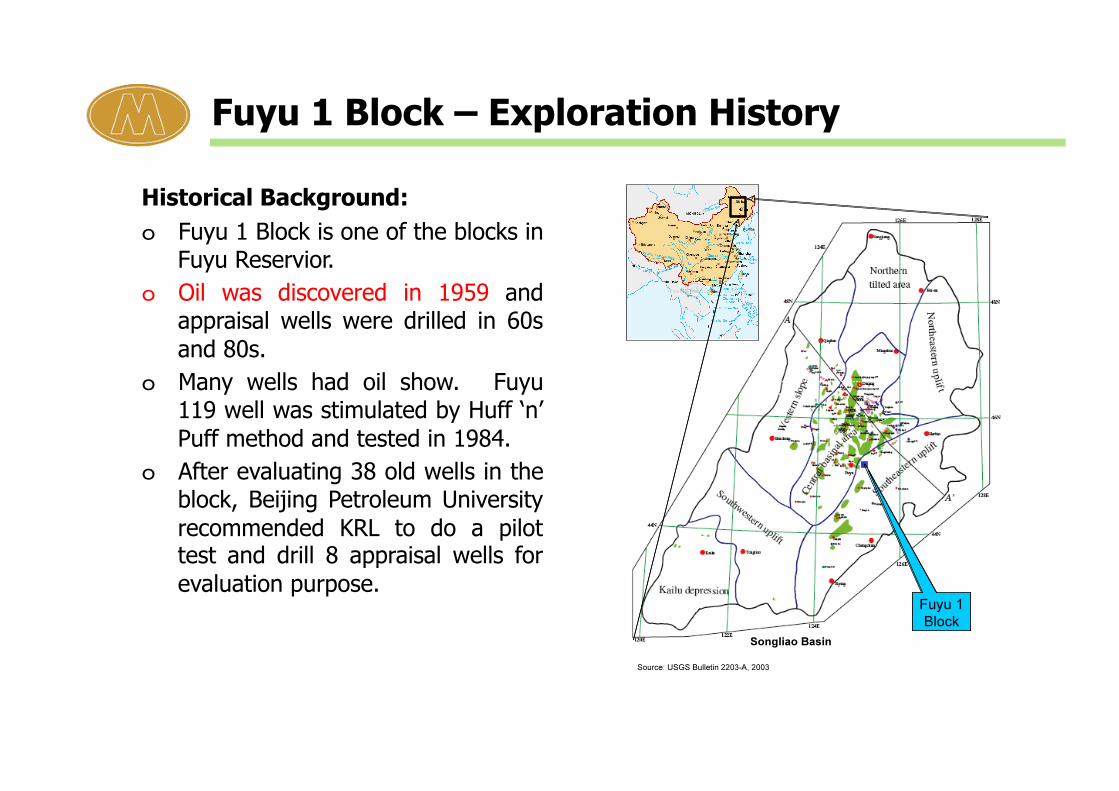

Fuyu 1 Block – Exploration History

Historical Background: o Fuyu 1 Block is one of the blocks in

Fuyu Reservior. o Oil was discovered in 1959 and

appraisal wells were drilled in 60s and 80s.

o Many wells had oil show. Fuyu 119 well was stimulated by Huff ‘n’ Puff method and tested in 1984.

o After evaluating 38 old wells in the block, Beijing Petroleum University recommended KRL to do a pilot test and drill 8 appraisal wells for evaluation purpose.

Fuyu 1 Block – PSC Terms

Major Contract Terms: o Around 254.9 sq km. o Contract Period :

• Evaluation period of 3 years; • Production period of 20 years;

and • Total duration of the PSC

cannot exceed 30 years. o KRL commits evaluation and

development costs. o After “investment recovery”, the

“share oil” is distributed 49% to KRL and 51% to CNPC.

o Crude oil price is paid in USD and sold at world market prices.

Sand Group 1 Sand Group 2

Sand Group 3 Sand Group 4

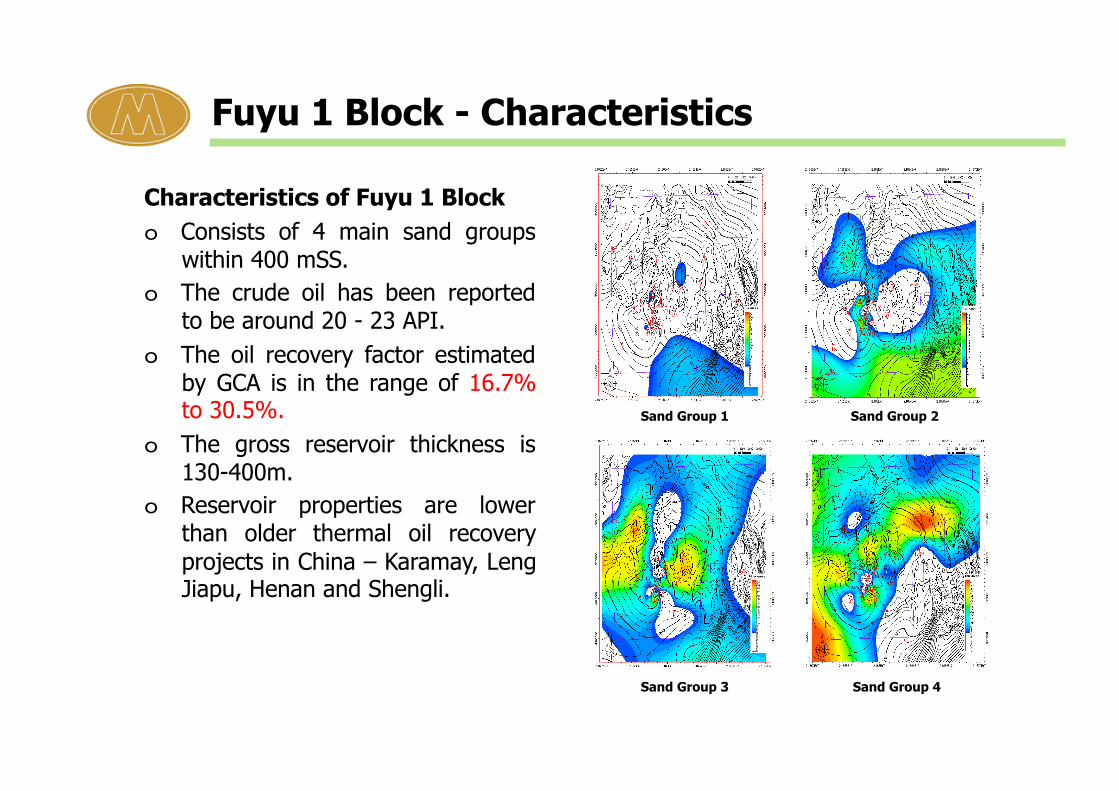

Characteristics of Fuyu 1 Block o Consists of 4 main sand groups

within 400 mSS. o The crude oil has been reported

to be around 20 - 23 API. o The oil recovery factor estimated

by GCA is in the range of 16.7% to 30.5%.

o The gross reservoir thickness is 130-400m.

o Reservoir properties are lower than older thermal oil recovery projects in China – Karamay, Leng Jiapu, Henan and Shengli.

Fuyu 1 Block - Characteristics

Fuyu 1 Block – Oil Estimates

Low Best High

STOIIP (million tons) 11.42 41.12 97.05

STOIIP (million stb) 75.63 272.19 642.50

Stock Tank Oil Initially In Place (31 Dec 2008)

1C 2C 3C

Gross Contingent Resources (million tons)

1.859 10.509 29.599

Net Entitlement Attributable to Kingworld (million tons)

0.906 5.144 14.435

Gross and Net Entitlement Contingent Resources (31 Dec 2008)

Notes: 1. Gross Contingent Resources are 100% of the Contingent Resources attributable to the licence. 2. Contingent Resources are estimated on the basis of GCA’s forecasts of production, costs and price profiles for the

development and operation of the Fuyu 1 Block. 3. Net Entitlement Contingent Resources reflect net economic entitlement attributable to KRL converted to equivalent

tons, and reflect the costs associated with the development concept. 4. Evaluation based on GCA’s 1Q 2009 SPE Forecast Price Scenario.

Fuyu 1 Block - Site Views

Production

Production Methods

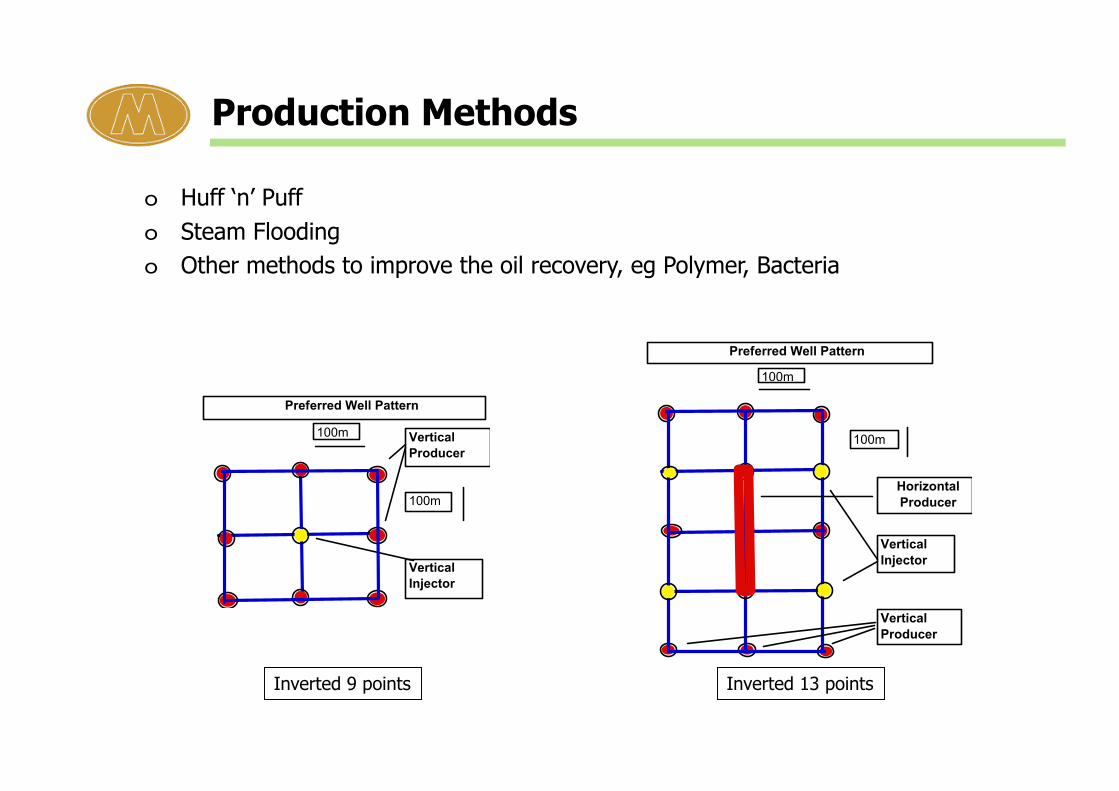

o Huff ‘n’ Puff o Steam Flooding o Other methods to improve the oil recovery, eg Polymer, Bacteria

Inverted 9 points Inverted 13 points

Production Diagram

Production Profile

Economic Evaluation

Crude Price Scenario

Year Brent Crude Fuyu 1 Crude Cost Inflation

2009 55.55 38.75 Nil

2010 65.30 48.50 2.0%

2011 70.33 53.53 2.0%

2012 73.37 56.57 2.0%

2013 75.77 58.97 2.0%

2014 77.29 60.49 2.0%

2015 Onward +2.0% p.a. +2.0% p.a. Notes: 1. From 2014 onwards, Fuyu crude price is escalated in line with the Brent “marker crude”, maintaining the U.S.$16.80/bbl discount. 2. The conversion factor is 6.62 bbls for 1 tonne of Fuyu crude.

Crude Price Scenario estimated by GCA on 31 Dec 2008 (US$/bbl)

Classification

Project Maturity

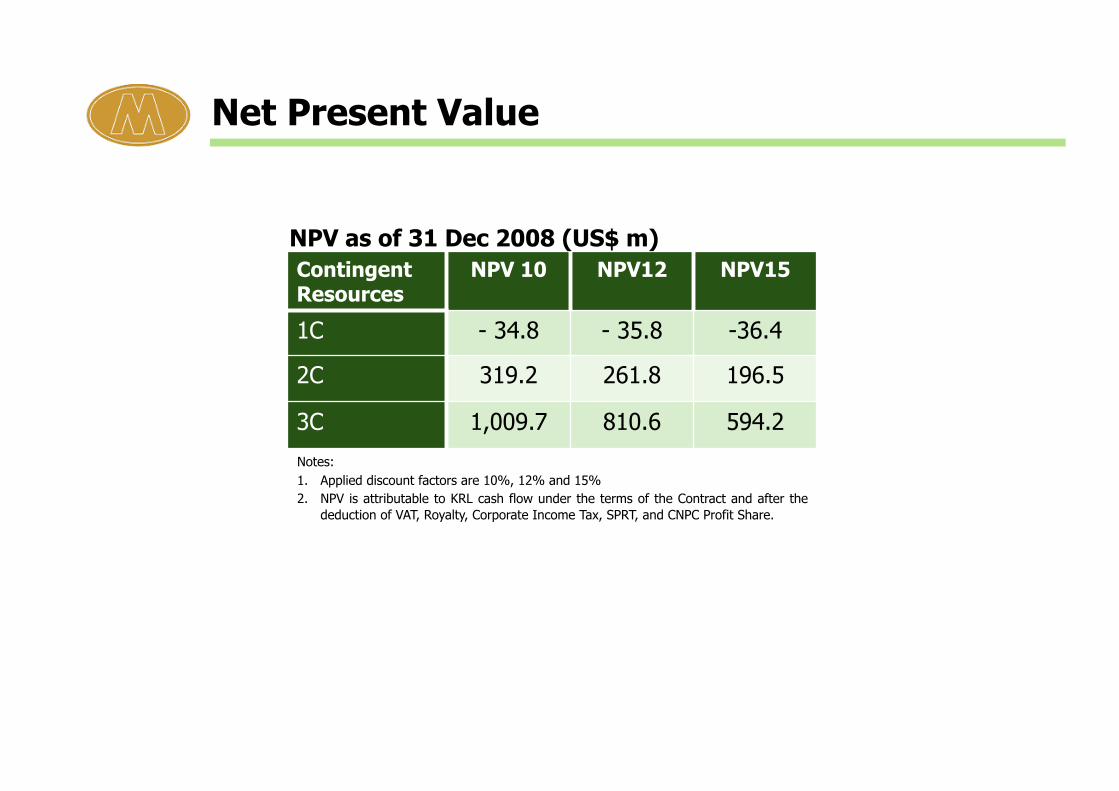

Net Present Value

Contingent Resources

NPV 10 NPV12 NPV15

1C - 34.8 - 35.8 -36.4

2C 319.2 261.8 196.5

3C 1,009.7 810.6 594.2

NPV as of 31 Dec 2008 (US$ m)

Notes: 1. Applied discount factors are 10%, 12% and 15% 2. NPV is attributable to KRL cash flow under the terms of the Contract and after the

deduction of VAT, Royalty, Corporate Income Tax, SPRT, and CNPC Profit Share.

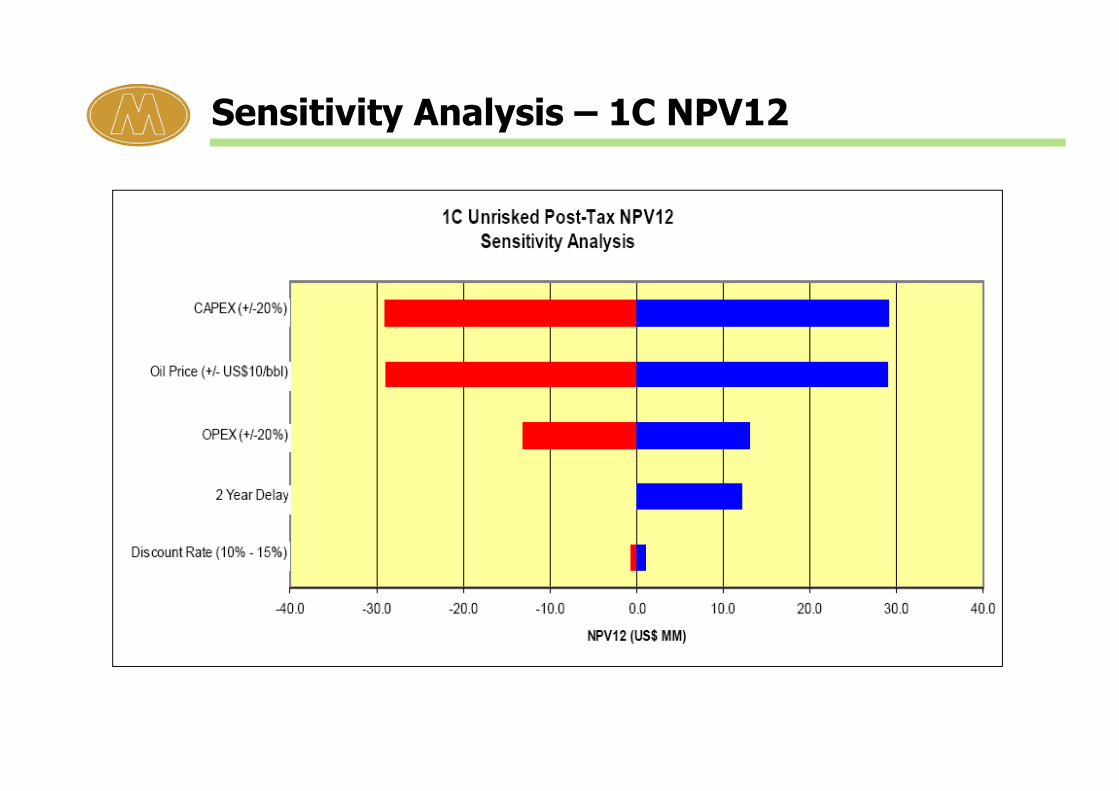

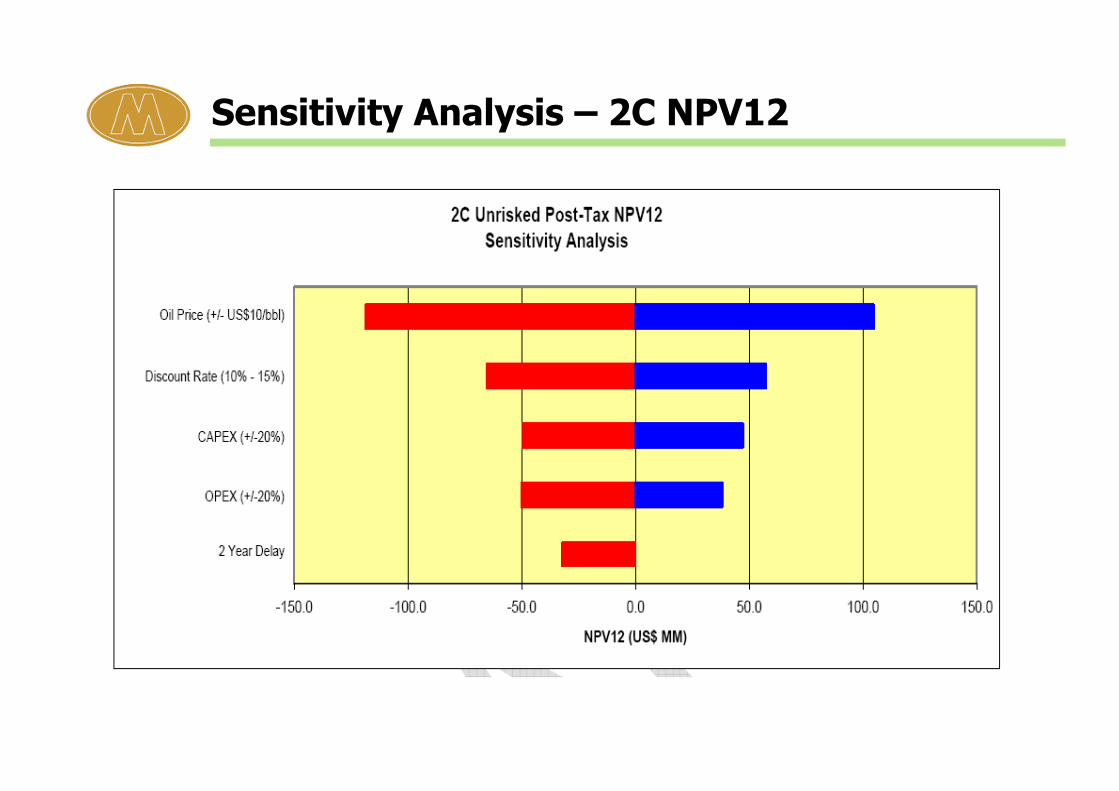

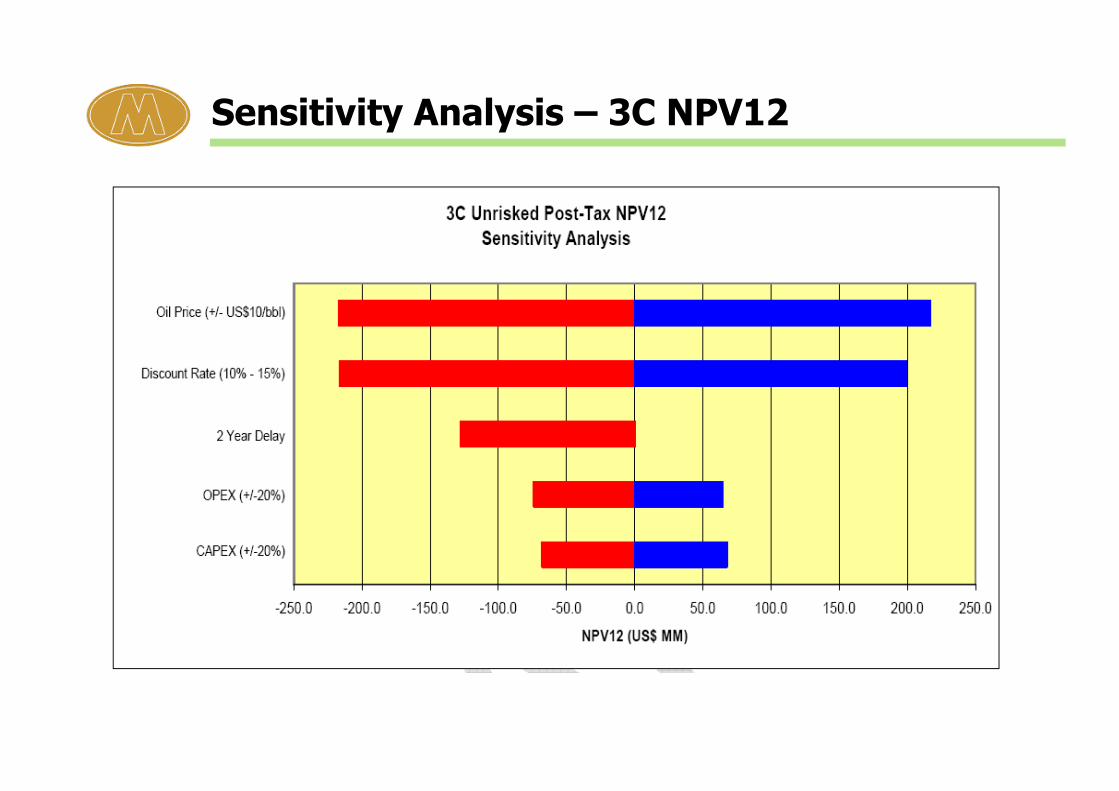

Sensitivity Analysis

Three Cases for the following scenarios o Oil price: +/- US$ 10 per bbl o Capital Expenditure: +/- 20% o Operating Expenditure: +/- 20% o Discount rate: 10%, 12%, 15% o Project development delay of 2 years.

Sensitivity Analysis – 1C NPV12

Sensitivity Analysis – 2C NPV12

Sensitivity Analysis – 3C NPV12

EMV – 3 Scenarios

o Scenario 1 • Contingent Resources as at 31 Dec 2008 per GCA’s Technical Report; • Crude price scenario estimated by GCA on 31 Dec 2008.

o Scenario 2 • Contingent Resources as at 31 Dec 2008 per GCA’s Technical Report

with field development delayed by 2 years; • Crude price scenario estimated by GCA on 31 Dec 2008.

o Scenario 3 • Contingent Resources as at 31 Dec 2008 per GCA’s Technical Report; • Crude price scenario based on latest Brent Strip available at 26 Feb

2009.

Year Brent Crude Fuyu 1 Crude Cost Inflation

2009 55.55 38.75 Nil

2010 65.30 48.50 2.0%

2011 70.33 53.53 2.0%

2012 73.37 56.57 2.0%

2013 75.77 58.97 2.0%

2014 77.29 60.49 2.0%

2015 Onward +2.0% p.a. +2.0% p.a.

Year Brent Crude Fuyu 1 Crude Cost Inflation

2009 50.01 33.21 Nil

2010 56.12 39.32 2.0%

2011 61.07 44.27 2.0%

2012 64.65 47.85 2.0%

2013 67.43 50.63 2.0%

2014 69.97 53.17 2.0%

2015 Onward +2.0% p.a. +2.0% p.a.

Scenario 1 & 2:

Scenario 3:

EMV – Crude Price Scenario

EMV – ECoS

EMV – Formula

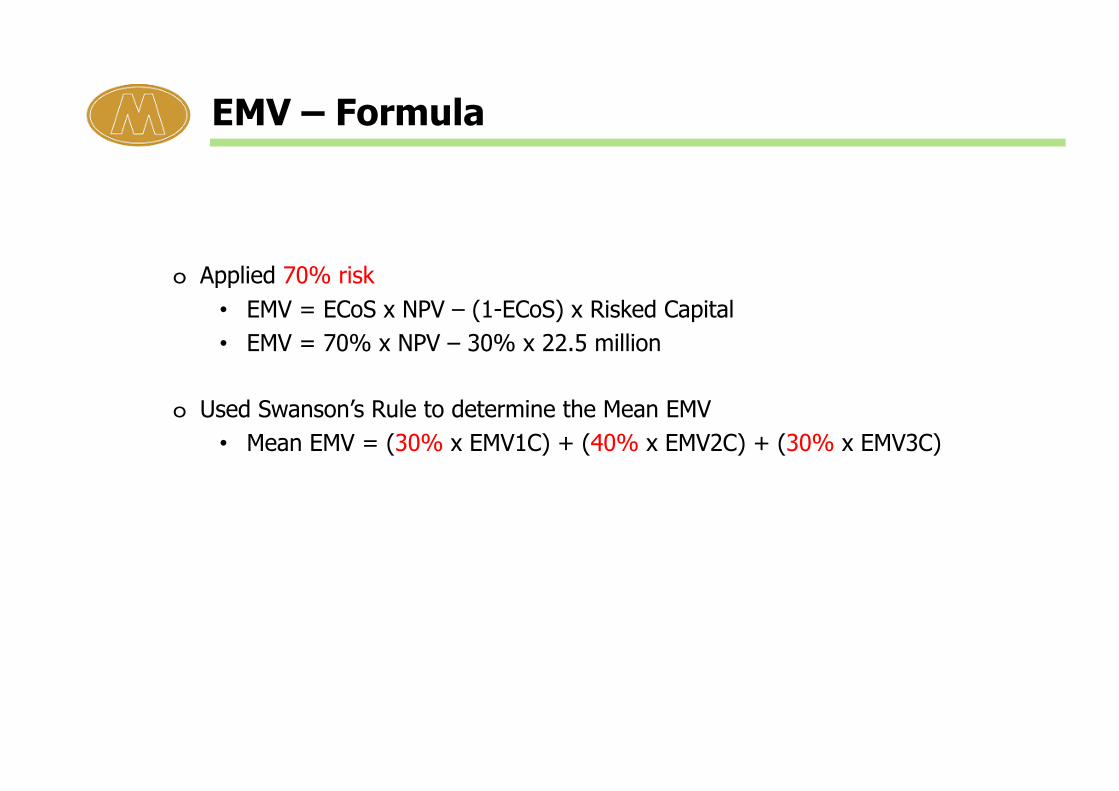

o Applied 70% risk • EMV = ECoS x NPV – (1-ECoS) x Risked Capital • EMV = 70% x NPV – 30% x 22.5 million

o Used Swanson’s Rule to determine the Mean EMV • Mean EMV = (30% x EMV1C) + (40% x EMV2C) + (30% x EMV3C)

GCA suggests that, for a transaction effective 31 Dec 2008, the EMV range of US$160m to US$230m at 12% discount rate could be considered reasonable based on the stated assumptions.

EMV10 EMV12 EMV15

Scenario 1 287.3 229.3 165.4

Scenario 2 252.8 196.0 135.4

Scenario 3 202.6 158.2 109.6

EMV – 3 Scenarios

EMV of 3 Scenarios (US$ m)

Technical Team

Technical Team

Mr Xie Shen, aged 69, is the Chief Engineer and Advisor to General Manager of Kingworld. He is a professor grade Senior Engineer in China and is one of the most experienced all round specialists in the petroleum industry in China. Prior to joining Kingworld, he was the Chairman of Songyuan Yongda Oilfield Development and Technology Company Ltd. Before that, he was the Deputy Director of Jilin Oilfield. Mr. Xie has over 46 years of experience in the petroleum industry in China and has been granted a number of awards, including National Advanced Science and Technology Award. He has obtained a bachelor degree in Petroleum Geology from Beijing Petroleum Institute in China in 1961.

Ms GAO Yinghua, aged 61, is the Technical Director of Kingworld. She is a Senior Engineer in China and is one of the most experienced heavy oil specialists in the petroleum industry in China, especially in the area production and exploitation. Prior to joining Kingworld, she was the Chief Engineer of Beijing BFC Petroleum Technology Ltd. Ms GAO has over 37 years of experience in petroleum industry in China and has been granted a number of awards, including Oilfield Advanced Science and Technology Award. She has obtained a bachelor degree in Oil Production and Exploitation from Southwest China Petroleum Institute in China in 1970.

Future Outlook

o Be the oil and gas exploration and production business flagship of RH Group.

o Apply new production technologies to enhance the oil recovery factor.

o Explore actively acquisition opportunities in oil and gas exploration and production business in various countries.

o Position to be an independent global oil and gas exploration and production group in the world.

Future Outlook

This presentation includes certain forward-looking statements. All statements, other than statements of historical facts, that address activities, events or developments that Tri-M Technologies (S) Ltd expects or anticipates will or may occur in the future are forward-looking statements. Tri-M Technologies (S) Ltd’s actual results or developments may differ materially from those indicated by these forward-looking statements as a result of various factors and uncertainties, including but not limited to price fluctuations, actual demand, exchange rate fluctuations, market shares, competition, environmental risks, changes in legal, financial and regulatory frameworks, international economic and financial market conditions, political risks, project delay, project approval, cost estimates and other risks and factors beyond the control of Tri-M Technologies (S) Ltd . In addition, Tri-M Technologies (S) Ltd makes the forward-looking statements referred to in this presentation as of today and undertakes no obligation to update these statements.

Forward Looking Statements

Q & A

Thank you