trended credit report webinar slides

TRANSCRIPT

TRENDED

CREDIT REPORT

DATA

AGENDADefinition of trended data

Fannie Mae’s announcement

What we know now

Key benefits

View a sample

FAQ’s

Conclusion

Question/Answer

Definition of trended data:

An enhanced credit report with new,

valuable data fields, including Actual

Payment Amount, and up to 30 months of

detailed account history for each tradeline.

Fannie Mae’s Announcement

Fannie Mae’s announcement to utilize

trended consumer credit data in the assessment of mortgage applicants is a

major shift for the industry

Trended credit data can benefit mortgage borrowers by providing

Fannie Mae and mortgage lenders a more comprehensive view of borrowers’

historical credit performance

Fannie Mae’s estimated date of acceptance is

the weekend of

June 25th 2016.

The Federal Housing Finance Agency (FHFA) has recently escalated

emphasis and pressures to increase home ownership and mortgage

access, particularly among:

*Younger consumers *First-time home buyers

WHAT WE KNOW NOW

DISCLAIMER!

This information is subject to change as the bureaus and/or Fannie Mae move forward with the project.

WHAT WE KNOW

Equifax will be offering Trended Data in a product called Acrofile

TransUnion will be offering a Trended Data product called

CreditVision(Experian is not offering a trended data product at this time.)

WHAT WE KNOW

During the testing period (March-June)

this information

Must not be used in underwriting loan

decisions

WHAT WE KNOW

Fannie states that, although bureaus will report trended data on ALL tradelines,

Fannie will ONLY use it on revolving accounts

#1: A borrower summary (one for each borrower on joint reports) that totals Balance, High Credit, Minimum monthly payment, and Actual monthly payment per month across all accounts for 24 months.

#2: A tradeline summary broken out by month that totals Balance, High Credit, Minimum monthly payment, and Actual monthly payment for 24 months.

#3: An individual trade summary.

KEY ENHANCEMENTS

WHAT WE KNOW

Key Benefits

Increase volume, while maintaining credit standards

Identify low-risk consumers who would have previously shown up as non-prime

Open up mortgage access to many new consumers

Assist in portfolio management

KEY BENEFITS OF TRENDED DATA

*source: TransUnion

Separates credit “transactors” from credit “revolvers”

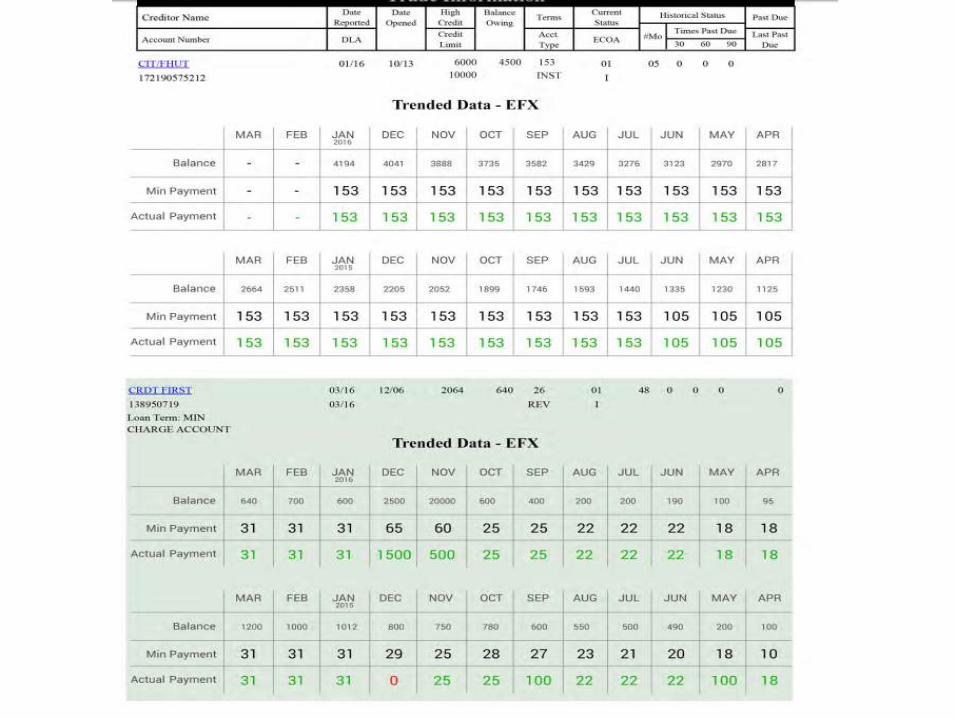

VIEW A SAMPLEThe following examples are from TransUnion.

FAQ’s

“Will loans for borrowers that make only the minimum payment on their credit card each month be able to receive an

Approve recommendation from DU?”

Yes. The use of the actual payment information will impact the analysis of the borrower’s credit. However, the

actual payment information is used in just one of the credit

risk factors analyzed by DU (see Appendix A of the DU Version 10.0 Release Notes).

DU will continue to perform a comprehensive evaluation of all of the credit and non-credit risk factors on

the loan to determine the recommendation.

Source: Fannie Mae FAQ’s

“How does the amount a borrower pays on their credit card account demonstrate how they will pay their mortgage?”

The trended credit data will be used by the DU risk assessment to evaluate howthe borrower manages his/her revolving credit card accounts. A borrower who

uses revolving accounts conservatively (low revolving credit utilization and/or

regular payoff of revolving balance) will be considered a lower risk.

A borrower whose revolving credit utilization is high and/or who makes only the

minimum monthly payment each month will be considered higher risk.

To put in perspective, holding all else equal on a loan…

Research has shown thatborrowers who

are Than borrowers who

Never exceed their limit 75% less likely to become delinquent

Exceeded their credit care limit in the last 12 months

Pay off their credit cards every month

60% less likely to become delinquent

Only make the minimum payment each month

“Do any of the changes made in DU Version 10.0 apply to FHA or VA loan casefiles underwritten through DU?”

No. The DU Version 10.0 updates only impact conventional loans, not FHA or VA loans underwritten through DU for Government Loans.

Lenders will not see the updated guidelines or messages on their FHA or VA loan casefiles.

Source: Fannie Mae FAQ’s

CONCLUSION• Trended data was introduced on the credit report starting in March, 2016, accessible via a link

•Fannie Mae will begin accepting Trended Data June 25, 2016

•Equifax has indicated that trended data is not to be used in underwriting decisions during the trial period (Mar-June)

• You will continue ordering your credit reports as you always have, through your LOS, DO/DU, or online

• Trended data offers an opportunity to expand your customer base without increasing overall levels of delinquency

Q&A??

THANK YOU

For Attending!We will keep you updated on this industry change as more information comes available!

Subscribe to our blog: www.datafacts.com

Connect on Linkedin: Data Facts, Inc

Follow us on Twitter: @dflending

Like us on Facebook: “Data Facts Lending Solutions”

REFERENCES• Fannie Mae:

http://www.fanniemae.com/portal/about-us/media/corporate-news/2015/6305.htmland

https://www.fanniemae.com/content/faq/do-du-release-06252016-faqs.pdf• Transunion:

http://newsroom.transunion.com/fannie-mae• Equifax:

http://investor.equifax.com/releasedetail.cfm?ReleaseID=937216