tone management and earnings management · abstract thesis: master degree project in accounting,...

TRANSCRIPT

Supervisor: Jan Marton, Emmeli Runesson and Niuosha Samani Master Degree Project No. 2015:18 Graduate School

Master Degree Project in Accounting

Tone Management and Earnings Management

A UK evidence of abnormal tone in CEO letters and abnormal accruals

Sara Carlsson and Rania Lamti

Acknowledgements

We would like to take the opportunity to thank all the people who have contributed to the

accomplishment of this thesis and supported us during the past four months. The execution of

this thesis has been both interesting and challenging, and it is with joy that we present the

final product. First of all, we thank our supervisors, Jan Marton, Emmeli Runesson and

Niuosha Samani, for their guidance and valuable insights. Especially, many thanks to Emmeli

Runesson and Niuosha Samani who inspired us to study the subject of tone management. We

would also like to thank all of our seminar opponents, Carin Enocson, Veronica Rodriguez

Labra, Amanda Strandberg and Patricia Sandblom, for their encouragements and useful

advices.

Thank you!

Gothenburg, May 22nd

2015

Sara Carlsson Rania Lamti

Abstract Thesis: Master Degree Project in Accounting, School of Business, Economics and Law at the

University of Gothenburg, Graduate School, Spring 2015

Title: Tone Management and Earnings Management: A UK Evidence of Abnormal Tone in CEO

Letters and Abnormal Accruals

Authors: Sara Carlsson, Rania Lamti

Supervisors: Jan Marton, Emmeli Runesson, Niuosha Samani

Background and Problem Definition: The CEO letter is one significant narrative document through

which senior management have opportunity to express beliefs and values to their shareholders. The

CEO letter is unregulated in its nature and thereby subject to management opportunism through tone

management. Tone management could further be used to manipulate the perception of the firm, which

causes information asymmetry. Similar to the purpose of tone management, accruals could be

opportunistically managed in order to manipulate users’ perceptions of firm fundamentals. Thus,

managers could through CEO letters employ tone management to potentially hide earnings

management, and thereby mislead users about firm fundamentals.

Purpose: The purpose of this thesis is to test the possible association between tone management in

CEO letters and earnings management, using data from 2013 including firms listed on the London

Stock Exchange. Subsequently, the intention is to investigate if earnings management and tone

management are substitutes or complements. The purpose is additionally to test the relation between

tone management in CEO letters and financial performance

Research Design and Methodology: The theoretical framework of this thesis is used to develop

hypotheses, which subsequently guide the research forward. In the execution phase, a customized

dictionary is developed to fit with the purpose of the thesis. The execution phase continues in

correlation and multiple regression analysis. The outcome of the statistical tests contributes to fulfill

the purpose.

Empirical Results and Analysis: In accordance with previous literature, the empirical results reveal a

positive association between tone in CEO letters and financial performance. Strengthening the purpose

and the contribution of this thesis, empirical evidences reveal that abnormal tone in CEO letters and

abnormal accruals are positively associated.

Concluding Remarks: The tone in CEO letters is generally positive regardless of management

discretion. Furthermore the tone in CEO letters can be derived from firm performance, firm size and

annual stock return. Finally, the findings indicate that tone management and earnings management

through the use of abnormal tone and abnormal accruals functions as complements and are thus not

substitutes.

Key Words: Tone Management, Abnormal Tone, CEO letter, Earnings Management, Accruals

Table of Contents

1. Introduction .......................................................................................................................... 1 1.1 Background ....................................................................................................................................... 1 1.2 Problem Definition and Purpose ....................................................................................................... 1 1.3 Contribution....................................................................................................................................... 3 1.4 Delimitations ..................................................................................................................................... 3

2. Frame of Reference and Hypotheses Development ........................................................... 4 2.1 Tone Management ............................................................................................................................. 4

2.1.1 The CEO Letter .......................................................................................................................... 5 2.2 Earnings Management ....................................................................................................................... 6

2.2.1 Accruals-Based Earnings Management ..................................................................................... 7 2.3 Hypotheses Development .................................................................................................................. 8

3. Methodology ....................................................................................................................... 10 3.1 Research Design .............................................................................................................................. 10 3.2 Sample ............................................................................................................................................. 11 3.3 Variables .......................................................................................................................................... 13 3.4 Measuring Tone and Abnormal Accruals ........................................................................................ 15 3.4.1 Tone (TONE) ................................................................................................................................ 15

3.4.2 Abnormal Accruals (ABACC) .................................................................................................. 16 3.5 Statistical Analysis .......................................................................................................................... 17

3.5.1 Initial Data Analysis ................................................................................................................. 17 3.5.2 Correlation Analysis ................................................................................................................ 17 3.5.3 Multiple Regression Analysis .................................................................................................. 18

3.5.3.1 Regression models ........................................................................................................................... 19 3.6 Data Collection ................................................................................................................................ 19 3.7 Reliability and Validity ................................................................................................................... 19 3.8 Limitations....................................................................................................................................... 20

4. Empirical Results and Analysis ........................................................................................ 21 4.1 Descriptive Statistics ....................................................................................................................... 21 4.2 Correlation Analysis ........................................................................................................................ 22 4.3 Multiple Regression Analyses ......................................................................................................... 23

4.3.1 Hypothesis Testing ................................................................................................................... 24 4.3.1.1 Tone and Financial Performance ..................................................................................................... 24 4.3.1.2 Abnormal Positive Tone and Financial Performance ...................................................................... 25 4.3.1.3 Abnormal Tone and Abnormal Accruals ......................................................................................... 26

5. Discussion ............................................................................................................................ 28

6. Concluding Remarks .......................................................................................................... 31

7. Suggestions for Further Research .................................................................................... 32

List of References ................................................................................................................... 33

Appendix 1 .............................................................................................................................. 37

Appendix 2 .............................................................................................................................. 42

Appendix 3 .............................................................................................................................. 46

Appendix 4 .............................................................................................................................. 49

1

1. Introduction

The introducing chapter to this thesis aims to provide the reader with a background of the thesis subject.

Based on this, a discussion regarding the problem is presented and thereafter concluded with the purpose

of the thesis and hypotheses. Thereafter follows a statement of the contribution of this thesis to accounting

theory. Finally, the chapter terminates with a description of the delimitations surrounding the thesis.

1.1 Background

In the context of accounting, people often think about financial reporting as numbers. Interestingly, more

recent studies and analyses focus on accounting language as the medium through which companies

communicate to their externalities (Hales, Kuang & Venkataraman, 2011). Accounting language could be

expressed through narratives, which are becoming increasingly important as they become longer and

more sophisticated. Furthermore, narratives allow preparers of annual reports to disclose further detailed

information and explanations of events (Clatworthy & Jones, 2003; Merkl-Davies & Brennan, 2007). In

turn, the increased importance of accounting narratives helps reducing the information asymmetry that

could occur due to limitations in current accounting standards (Clatworthy & Jones, 2003; Huang, Teoh

& Zhang, 2014). Consequently, accounting numbers complemented with accounting narratives may better

indicate firm fundamentals.

The Chief Executive Officer (CEO) letter is one significant narrative document through which

management have opportunity to express beliefs and values to their shareholders (Amernic, Craig and

Tourish, 2010). The CEO letter is revealed by prior studies to be the most frequently read section in the

annual report (e.g. Courtis, 1998; Clatworthy & Jones, 2003). Thus, as the power of the CEO grows

(Amernic et al., 2010) and importance of accounting language becomes increasingly vital, the rhetorical

tone, i.e. the usage of positive and negative expressions, assessed in CEO letters is proved to be central

for the perception of the firm.

Through increased volume of accounting narratives, corporate leaders may or may not take advantage of

the opportunities to obfuscate perceptions using tone, i.e. tone management. In extension, Schipper

confirms another phenomenon of management manipulation namely, earnings management, in her

commentary paper published in 1989. Prior and recent studies on earnings management confirm, by

empirical evidence, its existence. One context of earnings management is accruals-based earnings

management, which appear to be present as the current accrual system of accounting allows for earnings

management behavior (Teoh, Welch and Wong, 1998).

1.2 Problem Definition and Purpose

Prior literature describe the CEO letter, or equivalent documents such as Management Discussion &

Analysis (MD&A) and chairman's letter, as an important communication part of the annual report, and

argues for its influence on investors and other users of the annual report (e.g. Abrahamson & Amir, 1996;

Amernic & Craig, 2007; Patelli & Pedrini, 2014). Through the CEO letter, management are allowed to

express beliefs, values and attitudes to shareholders and the letter thus provide insight to the motives and

2

intentions of CEOs (Amernic et al., 2010). The CEO letter could therefore provide an overview of firm

activities and performance (Clatworthy & Jones, 2003). The Financial Reporting Council (FRC), an

independent regulator in the UK, provides guidelines for the writing of annual reports that applies to all

parts, including the CEO letter (FRC, 2015). However, these guidelines are not mandatory (FRC, 2015),

and the content of CEO letters is consequently unregulated. Together with the relative freedom in

choosing the informational content and the lack of restrictions surrounding the presentation, the CEO

letter is an interesting document for analysis (Abrahamson & Amir, 1996).

Consequently, accounting narratives, such as the CEO letter, are proved to be subjects to management

manipulation and opportunism (Clatworthy & Jones, 2006). Furthermore, the potential for self-serving

behavior is enhanced by the fact that in the UK, for example, auditors review narratives to ensure that

they are materially consistent with financial statements, but other aspects, such as tone, are not considered

(Clatworthy & Jones, 2006). Clatworthy and Jones (2006) further explain that it might be natural for

individuals to “put our best foot forward”, which could explain opportunistic presentation of accounting

narratives. However, in the context of financial reporting, this thinking conflicts with basic financial

premises, such as true and fair view, if management deliberately misrepresents firm fundamentals

(Clatworthy & Jones, 2006).

According to Huang et al. (2014) tone management could be used as tool to obscure firm fundamentals.

The authors further define tone management as abnormal tone, i.e. a tone level inconsistent with firm

fundamentals. In addition, abnormal tone could further be practiced opportunistically to improve

understanding of the financial reports and as consequence mislead investors by the employment of

positive words to hide poor performance (Huang et al., 2014). This in turn creates a problematic situation

as the users of the annual reports hold less accurate perceptions about the firm. Preparers of annual reports

possess knowledge about the above discussed fact, that the CEO letter is the most frequently read section

(Courtis, 1998), and this awareness by itself reasonably creates incentives for preparers to manage tone in

order to change perceptions, without presenting false data. Thomas (1997) expresses her thoughts about

the problem surrounding managers’ letters by stating that “Managers’ letters suggest and imply, but they

do not lie” (p.63).

Hence, managers with incentives to manipulate users’ perceptions could select to present information in a

positive or negative manner. In connection, Huang et al. (2014) refer to prior studies on accruals-based

earnings management, suggesting that accruals, similar to the purpose of tone management, are managed

in order to manipulate users’ perceptions of firm fundamentals. Teoh et al. (1998) explain that earnings

consist of cash flows from operations and accruals. Accruals are adjusted by management in order reflect

future business transactions, that is, reflecting firm condition more accurately. However, Teoh et al.

(1998) emphasize that this flexibility allowed by the accounting system creates opportunities for earnings

management. Accruals that are managed opportunistically (hereafter abnormal accruals) are thus proxies

for earnings management.

To conclude, when firms engage in tone management, users of the financial reports may be required to

read between the lines. Managers could through CEO letters employ tone management to potentially hide

earnings management behavior, and thereby mislead users about firm fundamentals. Thus, the main

purpose of this thesis is to test if earnings management and tone management are substitutes or

3

complements. The purpose is additionally to test the relation between tone management in CEO letters

and financial performance. The main and the additional purpose are achieved through creating a

customized dictionary in order to measure tone, using data from 2013 including firms listed on the

London Stock exchange. Furthermore, the purposes are fulfilled through testing and analyzing the below

hypotheses1. Thereby, these hypotheses constitute the core of this thesis.

H1 - Tone in CEO letters is positively associated with financial performance

H2 - The probability of observing abnormal positive tone in CEO letters increases as financial

performance decreases

H3 - Abnormal tone in CEO letters is positively associated with abnormal accruals

1.3 Contribution

This thesis provides several contributions to accounting theory. Firstly, it provides empirical evidence and

in-depth analysis of an association between tone management and earnings management. Prior studies

concerning tone management primarily investigate the effect on investors and stock price reactions,

caused by managerial opportunism (e.g. Feldman, Govindaraj, Livnat & Segal, 2010; Tan et al., 2014).

Furthermore, previous scholars include accruals as control variable when studying tone (e.g. Feldman et

al., 2010; Li, 2010; Huang et al., 2014). Although Huang et al. (2014) present a correlation between tone

management and accruals, the main purpose of their study, and previously mentioned studies, is not to

analyze the relation between tone management and earnings management. Furthermore, these studies test

the existence of tone management primarily in MD&As and earnings press releases. Thus, the

combination of tone management in CEO letters and earnings management is, to our knowledge,

unexplored.

In addition, the general focus on previously conducted tone studies has been listed or unlisted firms in the

US. On the contrary, this thesis approaches firms listed on the London Stock Exchange, a large and liquid

stock market characterized with dispersed ownership. Finally, the dictionary created for the purpose of

this thesis is customized to fit CEO letters and could therefore apply to future tone studies.

1.4 Delimitations

With the limited time frame in mind, this master thesis covers a limited scope of the research field.

Firstly, regarding tone management, the document to study is the CEO letter of annual reports. Secondly,

in terms of textual analysis, neither readability in the shape of reading ease, nor graphic presentations, are

considered when measuring tone. In the context of earnings management, only accruals-based

measurements are applied.

1 Hypotheses are developed in section 2.3

4

2. Frame of Reference and Hypotheses Development The following chapter constitutes the theoretical framework used in this thesis and aims at summarizing

relevant arguments provided by existing literature within the chosen fields i.e. tone management and

earnings management. Finally, hypotheses for this thesis are derived from the literature and developed in

section 2.3.

2.1 Tone Management

The linguistic features and textual analysis of accounting have gained attention during recent years. Li

(2008) examines reading complexity in annual reports through measuring annual report readability in

MD&As and in notes to financial statements. The findings indicate that firms with lower and less

persistent earnings report disclosures that are difficult to read, in other words, disclosures with low

readability. Interestingly, the author suggests a clear association between linguistic features in reported

disclosures and firm performance, concluding that firm performance is positively correlated with annual

report readability. Additionally, Li (2008) continues beyond readability by exploring other lexical features

in disclosures, such as the use of positive versus negative words (tone), revealing that loss firms that use

positive words to a larger extent than negative words in their MD&As have less persistent earnings. In

accordance, Rutherford (2005) explains that stylistic choices such as lexical features, words choices,

frequency use and word complexity affect the perception accounting narratives. More so, Rutherford

(2005) concludes that management’s letter to shareholders in general is positively charged, regardless of

financial result.

The notion of tone management has been the subject of several recent papers, both in the context of

accounting and in the context of other research fields. Within accounting and financial reporting, scholars

use the concept mainly in order to establish how tone management would or could influence investors

(e.g. Davis & Tama-Sweet, 2012; Huang et al., 2014; Tan et al., 2014). Huang et al. (2014) further define

tone management as: “... the choice of the tone level in qualitative texts that is incommensurate with

concurrent quantitative information…” (p.1083). According to Huang et al. (2014), the rhetorical use of

narratives is important in order to understand quantitative information. However, when agency motives

are present, the rhetoric could instead mislead the reader and thereby be used strategically rather than

informative (Huang et al., 2014). Thereof, Huang et al. (2014) investigate whether tone management is

used for strategic purposes or for informative purposes, and if the capital market discounts for strategic

motives when reacting to earnings announcements. When firm fundamentals are better than indicated by

quantitative information, due to limitations in accounting standards, tone management could be employed

for informative purposes (Huang et al., 2014). However, tone management may be used for strategic

purposes to change perceptions about firm fundamentals (Huang et al., 2014). Extending the research by

Li (2008), Huang et al. (2014) are of the opinion that tone is jointly affected by firm fundamentals and

managerial incentives to report strategically. They find that despite opportunities for truthful disclosures,

management abuses abnormal positive tone when firm fundamentals are poor. As consequence, the

authors find abnormal positive tone to be negatively correlated with future earnings. Additional findings

reveal that abnormal positive tone is associated with positive immediate market reactions to earnings

5

announcements, followed by negative market reaction in subsequent periods. The authors conclude this

reversal effect to be driven by the overestimated reaction to abnormally positive earnings announcements.

Tan et al. (2014) refer to Huang et al. (2014) explaining that language sentiment effect is associated with

the use of positive versus negative words. By holding the information content constant, Tan et al. (2014)

investigate whether tone management is used to influence investor perceptions. In contrast to remaining

studies on tone management, Tan et al. (2014) explore the co-occurrence of language sentiment and

readability in earnings press releases. In an additional analysis, the authors explain language sentiment to

be an effect of attribute framing, which is the situation when people’s perceptions about identical items

differ depending on the extent to which the items are described in a positive or negative manner. Drawing

on attribute framing, the authors find that positive language (as opposed to neutral language) leads to

positive framing effect as the participants of the study view firm performance to be better than indicated

by financial figures, regardless of investor sophistication. However when taking the co-occurrence of

language sentiment and readability into account, the authors find that when readability is high, the

language used becomes less significant, regardless of sophistication level. In contrast, when readability is

low, language sentiment is proved to affect investor judgment depending on sophistication level (Tan et

al., 2014). Less sophisticated investors are more influenced by positive framing (positive tone) despite the

fact that the information provided in annual reports may be inconsistent with firm fundamentals, leading

investors to make overestimations of earnings (Tan et al., 2014). In contrast, the authors emphasize, when

readability is low, more sophisticated investors regard positive tone as less credible and thereby make

lower earnings judgments than firm fundamentals. Tan et al. (2014) conclude that underestimated

earnings cause the use of positive language to backfire.

The common feature behind the reviewed literature above is that management incentives behind the use

of language appear to determine the tone. According to Courtis (1998), firms subject to media attention

might have motives to influence readers’ perceptions and engage in tone management in order to restrict

outside interference. In accordance, Huang et al. (2014) identify that tone management is used when there

are incentives to mislead investors, for example when management have targets to meet or beat. This

argument is further strengthened by Henry (2008) explaining that firm’s ability to manage tone is

dependent on firm fundamentals compared to analyst forecast. Under these circumstances, she explains

that tone management could be achieved by describing outcomes and events with a positive language and

provides positive comments about the future. Furthermore, Davis and Tama-Sweet (2012) emphasize that

management have incentives to manage tone in earnings press releases to minimize stock price effects on

negative news by applying less pessimistic language. This reasoning by Davis and Tama-Sweet (2012) is

in accordance with both Huang et al. (2014) and Tan et al. (2014), who argue that negative financial

performance may be disguised using positive tone.

2.1.1 The CEO Letter

The reviewed studies in above sections use different channels of management communication when

assessing tone management. Several scholars (e.g. Li, 2010; Davis & Tama-Sweet, 2012) apply the

MD&A report when determining the implications of tone management, because of the voluntary nature of

its content and excessive room for management discretion. Other scholars (e.g. Huang et al., 2014; Henry,

2008; Davis & Tama-Sweet, 2012), analyzing tone management effect on stock prices, target earnings

press releases as source of management communication. Earnings press releases are widely used due to

6

investors’ timely reactions, creating incentives for management to act strategic in their use of language

(Davis & Tama-Sweet, 2012).

Other authors (e.g. Hildebrandt & Snyder, 1981; Amernic & Craig, 2007; Amernic et al., 2010; Patelli &

Pedrini, 2014) rely on the annual letter to shareholders (hereafter CEO letter) when studying tone

management. In general, the CEO letter includes statements summarizing past events and future prospects

(McConnell, Haslem & Gibson, 1986). The CEO letter is neither audited, nor are there specific

requirements regarding its content and shape (Fisher & Hu, 1988). Management is thereby free to provide

statements of anything it considers important (McConnell et al., 1986). Thereof, CEO letters contain other

information than provided in the financial statements, along with explanations and interpretations

(Abrahamson & Amir, 1996).

As presented in section 1.1, the CEO letter is claimed by several authors to be the main communication

channel for management to review firm performance to shareholders. Amernic et al. (2010) claim “CEO

letters to shareholders in annual reports are important instances of the use of language in the disclosure of

senior corporate leaders. Such letters are narrative accountability texts offering valuable insights to the

motives, attitudes and mental models of management” (p.26). In accordance, Abrahamson and Amir

(1996) argue for the importance of CEO letters, implying that CEO letters include useful information in

making investment decisions. McConnell et al. (1986) state that CEO letters should not be disregarded

exclusively as the users of the documents otherwise could lose important signals. However, the authors

together with Fisher and Hu (1988) dissuade analysts and investors to solely rely on CEO letters when

making earnings forecasts or investment decisions. More so, McConnell et al. (1986) encourage investors

to read between the lines and take a “hard look” at the language of the CEO letter, since the language

could differ dependent on the financial performance of the firm. Additionally, McConnell et al. (1986)

present a relation between the assessment of prospective performance in CEO letters, and the firm’s

actual performance. Concluding, these results point to the usefulness of the CEO letter since it could be

used to assess future performance (McConnell et al., 1986).

2.2 Earnings Management

Earnings management is a notion that has been quite popular among researchers to explore (Healy &

Wahlen, 1999). One particular study that has been cited by several scholars (e.g. Leuz, Nanda &

Wysocki, 2003; Burgstahler, Hail & Leuz, 2006) is the literature review on earnings management by

Healy and Wahlen, conducted in 1999. Healy and Wahlen (1999) define earnings management as the

situation when management abuses the opportunity of judgment, either to mislead stakeholders about firm

fundamentals or to influence contractual outcomes. Accounting standards are constructed to fit different

accounting environments, and the element of judgment is therefore necessary (Healy & Wahlen, 1999).

However, this requires users to make accounting decisions based on privately held information, which

potentially creates discretionary reporting situations and agency problems (Burgstahler et al., 2006).

Burgstahler et al. (2006) further explain that management, consequently, either can construct earnings as

less or more informative dependent on the usage of privately held information.

In addition, the desire to mislead stakeholders could according to Healy and Wahlen (1999) include

limiting stakeholders’ access of information in order to reduce transparency of information. In

7

accordance, Leuz et al. (2003) argue that firms have incentives to mislead stakeholders by misrepresent

firm performance, thereby mask true performance through earnings management as a result of conflicts

between firms and their stakeholders. Similarly, Schipper (1989) possess a view of accounting numbers as

information and relates earnings management to “disclosure management”, emphasizing that managers

intervene financial reporting to obtain private gain. Schipper (1989) further argues that earnings

management could occur everywhere in external reporting and undertake all shapes.

The incentives to manipulate earnings are widely explored in previous literature. Dechow and Skinner

(2000) emphasize that capital market incentives for earnings management is the most accurate focus since

stock market prices and their relation to earnings has become increasingly important. In turn, managers

have incentives to manage earnings to both maintain and improve stock price valuation, which is

supported in the review by Healy and Wahlen (1999). While these studies connect the capital market to

earnings management, Leuz et al. (2003) link how incentives to manage earning could be associated with

institutional factors. Leuz et al. (2003) investigate how the level of earnings management could vary

across clusters and find that investor protection rights is a key determinant for earnings management.

Additionally, Dechow et al. (2010) indicate that when firms have targets to meet or beat, set by them or

by outside parties, they also have incentives to manage earnings.

2.2.1 Accruals-Based Earnings Management

Earnings consist of total accruals and cash flow from operations, and the amount of accruals therefore

affect the amount of reported earnings (Teoh et al., 1998). Teoh et al. (1998) explain that by upwardly

adjust accruals today; managers can increase current reported earnings at the expense of future reported

earnings. However, Richardson (2003) informs that high levels of accruals could be unintentional due to

the accounting environment of the firm, and thereby not a result of earnings management. In fact, accruals

are the core of the modern accounting system and are used to prevent mismatches between short-term

transactions (Runesson, 2014). Nevertheless, the nature of accruals require high amount of estimation of

future events and subjective allocation of past transactions, and are therefore subject to earnings

management behavior (Richardson, 2003).

Due to the role of accruals within the accounting system, scholars generally decompose accruals into two

separate components, normal (non-discretionary) and abnormal (discretionary). Normal accruals are those

related to the fundamental performance of the firm, and, abnormal accruals are in contrast those

exceeding the normal (Dechow et al., 2010). Hence, abnormal accruals are not explained by firm

fundamentals and can therefore function as indicator of management’s abuse of reporting flexibility

(Healy & Wahlen, 1999; Geiger & North, 2011). In accordance, both prior and recent scholars (e.g.

Godfrey et al., 2003; Li 2010; Huang et al., 2014) argue that management uses abnormal accruals as tools

to manipulate investor perception about true firm performance. Hence, research indicates that abnormal

accruals are used to manage earnings, and abnormal accruals are therefore considered an appropriate

proxy for earnings management among researchers.

Subsequently, the effect of accruals has been widely explored within earnings management literature.

Previously mentioned Teoh et al. (1998) examine whether income-increasing accruals accounting leads to

overly optimistic investor judgments of stock issues. The authors both predict and conclude that

overvaluation of performance leads to poor earnings and stock return performance in subsequent periods.

8

By decomposing earnings into accruals and cash flow from operations, the authors find that the

overvaluation and the subsequent earnings underperformance are caused by accruals. These findings are

in accordance with Sloan (1996), who finds that earnings are less persistent when highly dominated by

accruals. After further decomposing the accrual component into abnormal and normal, Teoh et al. (1998)

provide evidence consistent with earnings management that abnormal accruals both predict

underperformance of post-issue earnings and post-issue stock returns. Additional evidence of the

connection between low persistence of earnings and earnings management is provided by Dechow, Sloan

and Sweeney (1995). The authors present empirical evidence of the reversal effect of accruals, i.e.

increase (decrease) in year zero followed by decrease (increase) thereafter. According to Sloan (1996), the

reversal effect is a sign of earnings management contributing to the lower persistence of the accrual

component of earnings.

The low persistence of earnings dominated by accruals has more recently been explored by Dechow et al.

(2010). The authors examine the notion of earnings quality and present a review of its proxies,

determinants and consequences. High quality earnings are defined as earnings highly informative about

the firm’s financial performance (Dechow et al., 2010). Thereby, proxies for earnings quality are

transactions that might lower the informational use of earnings. One such category of proxies are

according to Dechow et al. (2010) the property of earnings, including among others earnings persistence,

accruals and target beating. Furthermore, the authors mention that the majority of studies published on the

subject, view abnormal accruals as the determinant of earnings quality since abnormal accruals are

assumed to erode decision usefulness. Thereby, accruals-based earnings management is assumed to erode

earnings quality since manipulated earnings have low persistence (Dechow et al., 2010).

2.3 Hypotheses Development

Throughout the literature supporting this thesis, researchers have highlighted the relationship between

firm performance and tone in various types of management letters. For example, Davis and Tama-Sweet

(2012) test the use of language in financial reports where they expect current firm performance to be the

significant determinant of the use of positive versus negative language. In connection, authors (e.g.

Amernic & Craig, 2007; Merkl-Davies & Brennan, 2007; Henry, 2008) express that tone is managed

depending on whether companies face high or low profits, arguing that when profits are high,

management tend to use a positive tone in accounting narratives as a result of good management. Huang

et al. (2014) state that when presentation of information is neutral, the optimism in tone is positively

correlated with performance. This reasoning is in accordance with Davis and Tama-Sweet (2012), who

provide similar evidence regarding optimistic tone and financial performance. Thereof, the common

thought among previously mentioned scholars appears to be that the tone in CEO letters is generally

positive, and that the association between tone and financial performance consequently is positive.

However, the above noted studies present empirical results on firms listed in the US whilst investigating

various management communication channels. Thus, the thought of a similar association between tone in

CEO letters and financial performance of firms listed on the London Stock Exchange is thereby justified,

and presented as H1.

H1 - Tone in CEO letters is positively associated with financial performance

9

In contrast to above, Hildebrandt and Snyder (1981) conclude that positive words are more frequently

present in CEO letters than negative words, regardless of financial results. The authors explain that a

financially bad year will include positive statements that do not reflect firm fundamentals, i.e. abnormal

usage of tone. Similarly, Rutherford (2005) presents results indicating that management letters are

dominated by positive words, which justifies the reasoning by Hildebrandt and Snyder (1981).

Furthermore, Rutherford (2005) argues that loss making firms employ word such as profit and profits,

more frequently than profit making firms. The research by Hildebrandt and Snyder (1981) and Rutherford

(2005) legitimate the thought of potential usage of abnormal positive tone when firm performance is

negative. Drawing on Huang et al. (2014), one can assume that loss making firms have incentives to

change users’ perceptions, and thereby more prone to employ abnormal positive tone in CEO letters

compared to profit making firms. The following hypothesis is thereof presented:

H2 - The probability of observing abnormal positive tone in CEO letters increases as financial

performance decreases

Referring to previously presented descriptions of tone management and earnings management, mutual for

both management behaviors is the intent to affect or shape perceptions about financial performance.

Adding the resembling incentives behind the two behaviors, the thought of coexistence is justified. Li

(2010) explains that both accruals and tone could by managers signal future firm performance. In

addition, when incentives to mislead investors are present, there may be a positive association between

accruals and the tone of MD&As (Li, 2010). Similarly, Huang et al. (2014) investigate, in additional

analysis, the co-occurrence of tone management and earnings management to provide evidence on

whether the two behaviors complement or substitute each other when manipulating investor perceptions

through earnings press releases. In sum, the authors found that the association between abnormal accruals

and abnormal tone is statistically significant, proving management's’ usage of both behaviors

simultaneously in earnings press releases. These evidence are also provided by Schrand and Walther

(2000) stating “strategic disclosure in earnings announcements is related to earnings management…”

(p.3). Hence, one can predict a similar association between abnormal tone in CEO letters and abnormal

accruals of firms listed in UK. The third and last hypothesis is thereby proposed as:

H3 - Abnormal tone in CEO letters is positively associated with abnormal accruals

10

3. Methodology The aim of this chapter is firstly to present the research design, which is illustrated in figure 3.1.1 and

aims to serve as guidance throughout the thesis. Thereafter follows a description of the sampling process.

Subsequently, the chosen variables are presented in table 3.3.1 and described one by one. Thereafter,

models regarding measurements of the variables tone and accruals are of particular importance for this

thesis and therefore presented in detail in section 3.4. Afterwards, the selected statistical analyses for this

thesis are presented and followed by the data collection. Finally, comments about validity, reliability and

limitations are provided in the last subsections.

3.1 Research Design

Quantitative research methods are perceived as most suitable when testing the developed hypotheses.

Thereby, aligned with positivism, the research is based on a theoretical structure, which subsequently is

tested through empirical observations. In other words, the logic of the research could be identified as

moving from the general to the specific (Collis & Hussey, 2014). The magnitude of the variables is tested

through the use of hypotheses, which guide the research forwards. Thus, the outcome of the statistical

tests will through analysis contribute to fulfill the purpose of the thesis. The hypotheses are constructed

through in-depth review of existing literature, and thereby test theoretical propositions against empirical

evidence (Collis & Hussey, 2014). The hypotheses, developed in section 2.3, are presented below:

H1 - Tone in CEO letters is positively associated with financial performance

H2 - The probability of observing abnormal positive tone in CEO letters increases as financial

performance decreases

H3 - Abnormal tone in CEO letters is positively associated with abnormal accruals

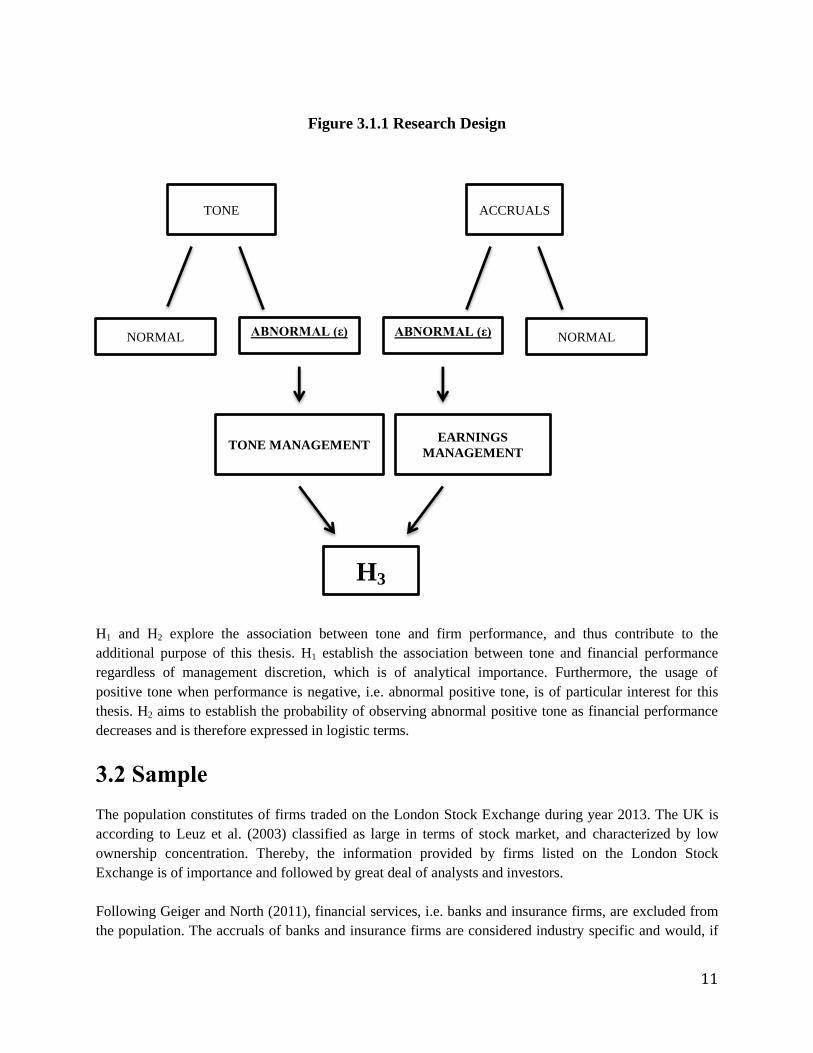

The below figure (3.1.1) functions as guidance towards the main purpose of the thesis, which is stated as

H3. As illustrated, tone and accruals, which are measured separately, both constitute of a normal and an

abnormal component. The abnormal components, calculated as regression residuals, are subsequently the

main elements when testing H3, which explores a potential association between abnormal tone (ABTONE)

and abnormal accruals (ABACC). Abnormal tone and abnormal accruals thereby functions as proxies for

discretionary management behavior.

11

Figure 3.1.1 Research Design

H1 and H2 explore the association between tone and firm performance, and thus contribute to the

additional purpose of this thesis. H1 establish the association between tone and financial performance

regardless of management discretion, which is of analytical importance. Furthermore, the usage of

positive tone when performance is negative, i.e. abnormal positive tone, is of particular interest for this

thesis. H2 aims to establish the probability of observing abnormal positive tone as financial performance

decreases and is therefore expressed in logistic terms.

3.2 Sample

The population constitutes of firms traded on the London Stock Exchange during year 2013. The UK is

according to Leuz et al. (2003) classified as large in terms of stock market, and characterized by low

ownership concentration. Thereby, the information provided by firms listed on the London Stock

Exchange is of importance and followed by great deal of analysts and investors.

Following Geiger and North (2011), financial services, i.e. banks and insurance firms, are excluded from

the population. The accruals of banks and insurance firms are considered industry specific and would, if

TONE ACCRUALS

NORMAL ABNORMAL (ε)

ABNORMAL (ε) NORMAL

TONE MANAGEMENT EARNINGS

MANAGEMENT

H3

12

included, disturb the measurement of accruals (Stubben, 2010). The firms are identified through using

two-digit Industry Classification Benchmark (ICB) code2 and thereafter deleted from the population.

A prerequisite of this thesis is that the required data exist in the Datastream database. Therefore, in order

to preserve the sample consistent, observations with missing values related to the dependent, independent

and control variables are eliminated. In order to limit the risk of potential comparison issues, the currency

of the variables are, through functions of Datastream, converted into GBP (£) before choosing a sample.

Moreover, firms with no available annual report or no CEO letter or equivalent letter are excluded. Based

on the mentioned restrictions, the final sample consists of 415 firms (see Appendix1). The sample size is

believed to be suitable since the authors execute the content analysis of the CEO letters manually. The

sampling process is visualized below.

Table 3.2.1 The Sampling Process

Initial number of firms provided by ESMA 1410

Firms categorized as financial services - 34

Deleted due to missing values - 827

Deleted due to annual report not found - 36

Deleted due to no CEO letter or equivalent - 98

FINAL SAMPLE 415

2 Firms classified with two-digit ICB code, 8300, 8500 or 8700.

13

3.3 Variables Table 3.3.1 Summary of Variables

Name Abbreviation Type of Variable Proxy for Measurement

Tone TONE Dependent Level of Tone

(Positive words-negative

words)/(positive

words+negative words)

Abnormal Tone ABTONE Dependent Tone

Management Regression residual

3

Abnormal Positive

Tone ABPOS Dependent

Tone

Management

1=Abnormal tone >0

0=Abnormal tone ≤0

Abnormal Accruals ABACC Independent Earnings

Management Regression residual

Performance LOSS Independent/Dummy Financial

Performance

1=EARN<0

0=EARN≥0

Profitability EARN Independent/Control Financial

Performance Net income/total assets

Size SIZE Control External

Attention

Log(market value of

equity)

Book-to-Market

Ratio BTM Control

Growth

Potential

Book value of

equity/market value of

equity

Annual Stock

Return RET Control

Growth

Potential ((P1-P0)+Div)/P1

4

Tone, TONE

Drawing on the research by Huang et al. (2014), the firm’s total level of tone is interpreted as the normal

level of tone together with the abnormal level (ABTONE). Normal level of tone symbolizes the neutral

description of firm fundamentals, and is expressed through the control variables of regression (1) (see

section 3.5.3.1). Accordingly, the TONE variable expresses the tone level including both the normal level

and the abnormal level. TONE is used in H1 to calculate ABTONE and to establish the association

between tone and financial performance. The procedure of measuring TONE is further described in

section 3.4.1.

Abnormal Tone, ABTONE, and Abnormal Positive Tone, ABPOS

ABTONE is considered the dependent variable in regression (3). Following Huang et al. (2014) ABTONE

is calculated as the residual value when deducting the normal level of tone from the total level of tone,

and thereby proxies for the strategic usage of tone, i.e. tone management. If tone is expected to be

consistent throughout the years, the change in tone could also proxy for tone management (Huang, et al.,

2014). However, as this thesis only considers one firm year (2013), tone management is better indicated

3 Regression residual from regression (1)

4 P0=Stock price year-end, 2012, P1=Stock price year-end, 2013, Div=Dividends per share 2013.

14

by ABTONE. In contrast to Huang et al. (2014), ABTONE is considered to be both negative and positive

abnormal tone. The value of ABTONE is expressed through the error term in regression (1) (see section

3.5.3.1), and thereby calculated as the residual value.

In order to test the probability stated in H2, the ABPOS variable is created as a dummy variable set to 1 (0)

if ABTONE is positive (negative). The intention is to isolate the firms with positive abnormal tone in

order to test the probability of observing ABPOS (i.e. ABPOS = 1) as financial performance decreases.

Since ABPOS is derived from ABTONE, ABPOS also functions as proxy for tone management.

Abnormal Accruals, ABACC

Following previous literature, abnormal accruals (ABACC) are used as proxy for earnings management.

The variable is considered independent due to its use in H3, and is identified as the error term in the

Cross-Sectional Modified Jones Model (see section 3.4.2).

Financial Performance, EARN and LOSS

EARN and LOSS capture current financial performance, which according to the literature (e.g. Davis and

Tama-Sweet, 2012; Huang et al., 2014) is considered to affect the level of tone. The EARN variable is

calculated as the net income divided by total assets, also known as the Return on Assets (ROA). LOSS is a

dummy variable set to 1 when EARN is negative and 0 when EARN is equal to zero or positive. Following

Huang et al. (2014) EARN intents to measure profitability, whilst LOSS act as a performance benchmark.

EARN is included in regressions (1)-(3), and its correlation with TONE is tested in H1. LOSS is included

in regressions (2) - (3) and serves as the main independent variable along with EARN in H2.

As the value of LOSS is dependent on EARN, an interaction effect arises (Wooldridge, 2013). The

interaction variable, EARN_LOSS is the product of multiplying EARN with LOSS, and is used in

regressions (2) and (3) in order to control for the interaction effect.

SIZE

Following prior literature on tone management, size is generally controlled for as the external attention

drawn to the firm due to its size could affect the level of tone. For instance, Li (2010) bases his reasoning

on previous studies stating that larger firms may be more cautious in their expressions to avoid political

and legal costs. Moreover, Courtis (1998) suggests that firms subject to media attention might have

motives to influence readers’ perceptions, which is further reasoning for including size as a control

variable. Following Huang et al. (2014), SIZE is calculated as the logarithm of market value of equity

year 2013.

Future Growth Opportunities, BTM and RET

In accordance with Li (2010) and Huang et al. (2014), the Book-to-Market ratio (BTM) is controlled for

as it represents investment opportunities and growth potential, which could affect the level of tone.

Accordingly, Davis and Tama-Sweet (2012) expect that managers of high-growth firms have incentives to

report information strategically, which might affect the tone level. BTM is therefore considered an

appropriate control variable when investigating tone, and included in all tone regressions.

15

Similar to BTM, RET is also considered to capture future performance opportunities (Huang et al., 2014),

and is included in previous tone studies as a control variable. The RET variable is therefore included as a

control variable in all tone regressions. Hence, both BTM and RET are calculated based on the current

financial position. Nevertheless, the ratios include information about future performance beyond what is

conveyed in EARN, and thus represent future growth opportunities (Huang et al., 2014).

3.4 Measuring Tone and Abnormal Accruals

3.4.1 Tone (TONE) Scholars have used different approaches in order to measure the tone of various management documents;

however, there are two general approaches for conducting content analysis: the dictionary approach and

the statistical approach (Li, 2010). Out of these two, the dictionary approach appears more commonly

within financial research and “maps” words into different categories based on predefined rules (Li, 2010;

Loughran & McDonald, 2011). The statistical approach, on the other hand, relies on statistical techniques

such as measuring the correlation between the frequencies of certain key words (Li, 2010).

For the purpose of this thesis, the dictionary approach is considered appropriate, mainly as it is the most

commonly used approach within textual analysis (Li, 2010). Furthermore, the purpose is to measure

percentages of words within specific categories, i.e. positive and negative, which justifies the dictionary

approach (Li, 2010). The tone of CEO letters is thus measured by the amount of positive and negative

words included in the text by using a predetermined word list, i.e. dictionary. Within the dictionary

approach, the Harvard Psych sociological Dictionary (General Inquirer, GI) and the software program

DICTION are frequently used as categorization tools to evaluate the tone of financial texts (e.g. Henry,

2008; Loughran & McDonald, 2011; Craig & Brennan, 2012). However, Loughran and McDonald (2011)

found that particularly the GI dictionary is not designed with the purpose to fit financial research since

several words identified as negative (73.8%), typically are not considered negative in financial contexts.

The authors therefore address this issue and develop a word list, based on GI, more suitable to financial

research. Although the dictionary has been used in previous research, it is not considered appropriate for

the purpose of this thesis due to its magnitude. Henry (2008) studies the tone of earnings press releases

and its impact on investors, and provides a more manageable dictionary. Thereof, the dictionary provided

by Henry (2008) is used and serves as the foundation for the development of the customized dictionary

used in this thesis (words marked with asterisk in Appendix 2).

The dictionary of this thesis is created by manually reviewing CEO letters of various firms listed on the

London Stock Exchange. The letters are manually analyzed by their content in order to detect and classify

words as either positive (e.g. delighted, pleased, excellent) or negative (e.g. disappointed, unfavorable,

weak). In order to avoid bias, these letters do not refer to the firms included in the sample of this thesis.

The advantage with manual content analysis is that the content analysis becomes more precise, detailed

and tailored with regards to the specific research setting (Li, 2010). The final dictionary is presented in

Appendix 2. In line with Loughran and McDonald (2011) and Huang et al. (2014), if negations (no, not,

none, neither, never and nobody) are used immediately before a positive word, the positive word is

counted as negative. To the extent possible, grammatical and linguistic features are taken into

consideration with the purpose to capture the style of writing.

16

Due to access limitations, computer software such as DICTION is not used in this thesis. Instead, the

execution phase is conducted manually using a spreadsheet software searching for predetermined words.

Subsequently, the CEO letters of the sample firms are imported into the spreadsheet software and scanned

for words based on the customized dictionary. The tone of the text (TONE) is thereafter measured as a

frequency count of the words included in the dictionary. The TONE variable is calculated based on the

equation provided by Henry (2008):

𝑇𝑂𝑁𝐸 = (#𝑝𝑜𝑠𝑖𝑡𝑖𝑣𝑒 𝑤𝑜𝑟𝑑𝑠 − #𝑛𝑒𝑔𝑎𝑡𝑖𝑣𝑒 𝑤𝑜𝑟𝑑𝑠) / (#𝑝𝑜𝑠𝑖𝑡𝑖𝑣𝑒 𝑤𝑜𝑟𝑑𝑠 + #𝑛𝑒𝑔𝑎𝑡𝑖𝑣𝑒 𝑤𝑜𝑟𝑑𝑠) (𝑎)

The above equation equals to a scale within a minimum value of -1 and a maximum value of +1. TONE

equal to 0 suggests a neutral usage of positive and negative words whereas -1 (+1) suggests no usage of

positive (negative) words. The result from the above equation is thereafter used in the regression model to

identify the abnormal level of tone (see 3.5.2.1).

3.4.2 Abnormal Accruals (ABACC)

In order to measure the magnitude of accruals-based earnings management, a calculation of total accruals

is firstly executed, followed by a model to measure abnormal accruals (Healy & Wahlen, 1999). Total

accruals are subsequently regressed in order to identify which accruals that belong to the operating

activities of the firm e.g. sales revenue, accounts receivables and fixed assets (Healy & Wahlen, 1999).

Remaining accruals left undefined thus exceed the normal and could indicate earnings management.

Based on this along with prior studies on accruals-based accounting, the chosen models to measure

abnormal accruals for this thesis are presented below. Following previous studies, the accruals regression

is run for each one-digit ICB code combination in order to control for industry differences.

𝑇𝐴𝑐𝑐𝑗𝑡 = 𝐸𝐵𝐸𝐼𝑗𝑡 − 𝐶𝐹𝑂𝑗𝑡 (𝑏)

Where:

TAcc = Total accruals scaled by lagged total assets,

EBEI = Earnings before extraordinary items,

CFO = Cash flow from operations,

j= firm; and

t= year

𝑇𝐴𝑐𝑐𝑗𝑡 = 𝛽0 (1

𝐴𝑠𝑠𝑒𝑡𝑠𝑗,𝑡−1

) + β1(∆Sales𝑗𝑡 − ∆AR𝑗𝑡) + β2𝑃𝑃𝐸𝑗𝑡 + ε𝑗𝑡 (c)

Where:

Assets = Total assets,

ΔSales= Change in sales scaled by lagged total assets,

ΔAR= Change in accounts receivable from operating activities scaled by lagged total assets; and

PPE= Gross property, plant and equipment scaled by lagged total assets

ε= Regression residual5

5 Abnormal Accruals (ABACC)

17

Both models are extracted from Huang et al. (2014). The cross-sectional modified Jones model (c) is

chosen to measure abnormal accruals, firstly, as it is commonly used within accruals-based accounting

studies, and secondly, as the model takes credit sales manipulation into account (Teoh et al., 1998; Geiger

& North, 2011; Huang et al., 2014).

Following Huang et al. (2014), a constant (1/Assets) is included in the model. The inclusion of the

constant varies among scholars. However, Kothari, Leone and Wasley (2005) state the constant to be

important for the model, as the exclusion of it would bias the result and make the accruals measure less

symmetrical. The inclusion of the constant would thus enhance the ability to address the research problem

(Kothari et al., 2005). Additionally, abnormal accruals are expressed through the error term (ε). The

advantage with measuring accruals as the residual value (ε) is, according to Dechow et al. (2010), that

such models attempt to isolate the managed or error component of accruals, and the models have become

accepted within financial research. Thus, the identification of abnormal accruals is simplified.

3.5 Statistical Analysis

3.5.1 Initial Data Analysis An initial analysis of the variables is performed before executing further statistical analyses in order to

identify potential outliers, or extreme values, that might bias subsequent analyses. Variables that show

extreme skewness and kurtosis diverge from the normal distribution (Collis & Hussey, 2014) and are thus

winsorized to suit future analyses. The essence of winsorization is not excluding extreme values, but

rather alters the original data by setting extreme values equal to specified percentiles of the distribution

(Leone, Minutti-Meza & Wasley, 2014). In this thesis, extreme values are winsorized to the 1 and/or 99

percentiles. Although winsorization of data is common among researchers, Leone et al. (2014) emphasize

the potential problems with winsorizing data. The extreme values might not be results from error

computations, but could rather be effects of the business environment and thereby improve estimation

efficiency if kept unadjusted (Leone et al., 2014). Nevertheless, Newbold, Carlson and Thorne (2010)

present descriptive evidence of the problematic with extreme values, or outliers, and the winsorization

level is therefore set to 1%. Because of the debate concerning ad hoc data modifications, such as

winsorization (see Leone et al., 2014), the statistical analyses containing non-winsorized data is presented

in Appendix 3.

3.5.2 Correlation Analysis

Drawing on the research design and the quantitative characteristics of this thesis, statistical analyses of

variables are conducted. Firstly, bivariate analyses including all variables are executed in order to gain

additional information about the associations of two variables. As the majority of the variables are

continuous and parametric, i.e. ratios or intervals, the Pearson’s correlation coefficient is applied. The

correlation intends to measure the strength and direction of a linear relationship (Collis & Hussey, 2014).

Although, correlation analyses do not determine the causation of dependent and independent variables

respectively, it is of particular use for this thesis as it enables the authors to avoid issues related to

multicollinearity. Multicollinearity is the situation when two variables are highly correlated and could

thus damage the effect of multiple regressions (Blumberg, Cooper & Schindler, 2011).

18

In accordance with Collis and Hussey (2014), Pearson’s correlation analysis is complemented with

bivariate scatterplot analysis, which allows for additional interpretation of associations between two

variables visually (see Appendix 3). This enables the authors to study patterns of points in graphs, which

give an indication of the strength and direction of a linear relationship (Collis & Hussey, 2014) and

detects potential extreme values that could affect the correlation.

3.5.3 Multiple Regression Analysis

The Pearson’s correlation analysis is of importance when examining the correlation between two

variables. However the analysis fails to explain the correlation between several variables (Blumberg et al.,

2011). Instead, the multiple regression analysis is used as complement to examine the association between

the dependent variables and several independent variables. Thus, the multiple regression analysis allows

the user to explicitly control for several factors that simultaneously might affect the outcome of the

dependent variable (Wooldridge, 2013).

Multiple factors could affect the level of tone in CEO letters, and it is therefore advantageously to test

associations between variables through multiple regression analysis. H1 and H3 are tested using Ordinary

Least Square (OLS) regressions. The OLS regression enables the user to determine the effect of the

independent variables on the dependent variables whilst simultaneously controlling for factors that might

influence the association (Wooldridge, 2013). Hence, referring to H1 and H3, the OLS regression analysis

is considered an appropriate statistical analysis method based on the normally distributed dependent

variables. Furthermore, the model is considered particularly appropriate when identifying abnormal

values since the model generates an error term (ɛ), which count for the value unexplained by the control

variables and thus classifies as abnormal (Wooldridge, 2013).

The dependent variable in H2 is ABPOS, a dummy variable derived from ABTONE. The ABPOS variable

is further characterized as binary since the outcome of the variable is either 1 or 0, which disables the use

of OLS regression analysis. The distribution is further identified as binomial (Rabe-Hesketh & Everitt,

2004), and logistic regression analysis is therefore appropriate in order to test H2. Whilst the OLS

regression calculates the correlation between the dependent and independent variables, the logistic

regression calculates the probability of receiving a certain event of interest (Rabe-Hesketh & Everitt,

2004). The interpretation of the logistic regression model therefore differs from the OLS regression

model.

The issue with multicollinearity, which is often related to multiple regression analysis, is prevented

through conducting bivariate analysis (see section 3.5.2). Furthermore, in order to control for

heteroskedasticity, and increase the robustness of the findings, the robust standard error is included when

running the OLS regressions (Wooldridge, 2013). Due to the composition of the logistic regression

model, the heteroskedasticity issue is automatically counted for (Wooldridge, 2013).

19

3.5.3.1 Regression models Similar to previous tone studies (e.g. Davis & Tama-Sweet, 2012; Huang et al., 2014) the regressions of

this thesis are annual cross-sectional regressions of TONE, ABPOS and ABTONE on determinants

previously explained in section 3.3. Specifically, the regressions are6:

𝐻1: 𝑇𝑂𝑁𝐸 = 𝛽0 + 𝛽1𝐸𝐴𝑅𝑁 + 𝛽2𝑆𝐼𝑍𝐸 + 𝛽3𝐵𝑇𝑀 + 𝛽4𝑅𝐸𝑇 + 𝜀 (1)

𝐻2: 𝑃(𝐴𝐵𝑃𝑂𝑆 = 1) = 𝛽0 + 𝛽1𝐸𝐴𝑅𝑁 + 𝛽2𝐿𝑂𝑆𝑆 + 𝛽3𝑆𝐼𝑍𝐸 + 𝛽4𝐵𝑇𝑀 + 𝛽5𝑅𝐸𝑇 + 𝛽6𝐸𝐴𝑅𝑁_𝐿𝑂𝑆𝑆 + 𝜀 (2)

𝐻3: 𝐴𝐵𝑇𝑂𝑁𝐸 = 𝛽0 + 𝛽1𝐴𝐵𝐴𝐶𝐶 + 𝛽2𝐸𝐴𝑅𝑁 + 𝛽3𝐿𝑂𝑆𝑆 + 𝛽4𝑆𝐼𝑍𝐸 + 𝛽5𝐵𝑇𝑀 + 𝛽5𝑅𝐸𝑇 + 𝛽6𝐸𝐴𝑅𝑁_𝐿𝑂𝑆𝑆 + 𝜀 (3)

3.6 Data Collection

The collected data have both quantitative (numbers) and qualitative (narratives) characteristics (Collis &

Hussey, 2014). The quantitative data refers to the financial figures needed to measure earnings

management and tone management, and is collected from the database Datastream, provided by Thomson

Reuters. The variables used to collect firm information from Datastream are provided in Appendix 4. Due

to the limitation of Datastream, the sample firms are collected through MiFID Database, provided by the

European Securities and Markets Authority (ESMA). The version date is set to 31-12-2013 in order to

capture the firms listed on the London Stock Exchange by the end of year 2013.

The qualitative data refer to the measurement of tone, which is executed using the CEO letters of annual

reports (see section 3.4.1), as annual reports are accessible and directed to the firm’s most important

audience, i.e. its stakeholders (Hildebrandt & Snyder, 1981). Further on, the textual information will be

translated into numerical form in order to determine the tone variable. In other words, the qualitative data

will transform into quantitative.

3.7 Reliability and Validity

In general terms, quantitative studies possess high levels of reliability and relatively low levels of validity

(Collis & Hussey, 2014). The reliability of this thesis is strengthened by the providence of the word list

and sample used to calculate tone (see Appendix 1 and 2), which otherwise could affect the degree of

reliability.

To enhance the validity of this thesis, several aspects are taken into consideration throughout the

execution phase. Firstly, only CEO letters or equivalent letters signed by the CEO or the President are

included in the final sample in order to increase validity and secure consistent application. Secondly,

equal amount of positive and negative words is used to ensure that no category is overly represented.

Also, to the extent possible, the power of the words balances each other (for example fortunately and

unfortunately). Thirdly, regarding certain words, the spelling of both American and British English is

acknowledged with the purpose to capture these words. Finally, as stated in section 3.4.1, if negations

appear immediately before a positive word, the positive word is characterized as negative.

6 Industry variables are included in all regressions, but not reported.

20

3.8 Limitations

Additionally, it is acknowledged that this thesis involves limitations. Firstly, the classification of positive

and negative words partly involves judgments made by the authors. Moreover, the meaning of some

words might not be fully captured since the meaning is determined by the context. For example, the

directional words increase and decrease could appear in both positive and negative circumstances due to

their ambiguous nature. However, Henry (2008) provides results confirming that increase (decrease) in

majority appears in a positive (negative) context. Despite its limited nature, the approach is commonly

applied and thereby considered appropriate for the purpose of this thesis.

Finally, a final sample of 415 firms can be perceived as small in order to make generalizations about a

population. Furthermore, the sample size is considered large enough to address the research problem

(Collis & Hussey, 2014), and test the hypotheses.

21

4. Empirical Results and Analysis

This chapter presents the empirical results of the statistical tests performed in this thesis, and their

implications for the tested hypotheses. The introductory part of the chapter presents descriptive statistics,

which aim to present a numerical summary of the variables used in the statistical analysis. The

introductory part is followed by a presentation of the correlation analysis, which thereafter concludes in

the multiple regression analysis. Throughout the chapter, empirical results are analyzed with regards to

previous literature.

4.1 Descriptive Statistics

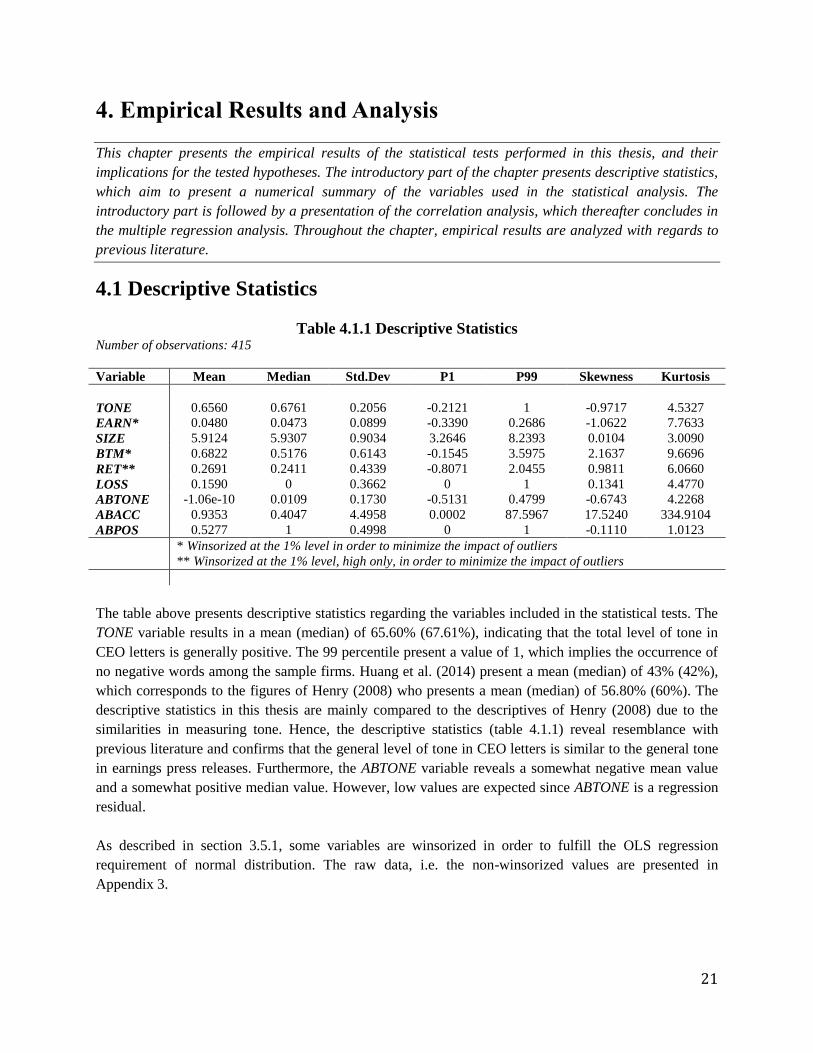

Table 4.1.1 Descriptive Statistics Number of observations: 415

Variable Mean Median Std.Dev P1 P99 Skewness Kurtosis

TONE 0.6560 0.6761 0.2056 -0.2121 1 -0.9717 4.5327

EARN* 0.0480 0.0473 0.0899 -0.3390 0.2686 -1.0622 7.7633

SIZE 5.9124 5.9307 0.9034 3.2646 8.2393 0.0104 3.0090

BTM* 0.6822 0.5176 0.6143 -0.1545 3.5975 2.1637 9.6696

RET** 0.2691 0.2411 0.4339 -0.8071 2.0455 0.9811 6.0660

LOSS 0.1590 0 0.3662 0 1 0.1341 4.4770

ABTONE -1.06e-10 0.0109 0.1730 -0.5131 0.4799 -0.6743 4.2268

ABACC 0.9353 0.4047 4.4958 0.0002 87.5967 17.5240 334.9104

ABPOS 0.5277 1 0.4998 0 1 -0.1110 1.0123

* Winsorized at the 1% level in order to minimize the impact of outliers

** Winsorized at the 1% level, high only, in order to minimize the impact of outliers

The table above presents descriptive statistics regarding the variables included in the statistical tests. The

TONE variable results in a mean (median) of 65.60% (67.61%), indicating that the total level of tone in

CEO letters is generally positive. The 99 percentile present a value of 1, which implies the occurrence of

no negative words among the sample firms. Huang et al. (2014) present a mean (median) of 43% (42%),

which corresponds to the figures of Henry (2008) who presents a mean (median) of 56.80% (60%). The

descriptive statistics in this thesis are mainly compared to the descriptives of Henry (2008) due to the

similarities in measuring tone. Hence, the descriptive statistics (table 4.1.1) reveal resemblance with

previous literature and confirms that the general level of tone in CEO letters is similar to the general tone

in earnings press releases. Furthermore, the ABTONE variable reveals a somewhat negative mean value

and a somewhat positive median value. However, low values are expected since ABTONE is a regression

residual.

As described in section 3.5.1, some variables are winsorized in order to fulfill the OLS regression

requirement of normal distribution. The raw data, i.e. the non-winsorized values are presented in

Appendix 3.

22

Table 4.1.2 Binary Variables

Variable Count

ABPOS

1 = ABTONE > 0 219

0 = ABTONE ≤ 0 196

TOTAL 415

LOSS

1 = EARN < 0 66

0 = EARN ≥ 0 349

TOTAL 415

The above table presents the distribution of the binary variables. The numbers reveal that just over half of

the sample firms employ abnormal positive tone according to the chosen proxy (ABTONE >0). The table

is not involved in the hypotheses tests, but contributes to the discussion in chapter five.

4.2 Correlation Analysis

Table 4.2 Pearson’s Correlation Analysis

Number of observations: 415

TONE EARN SIZE BTM RET LOSS ABTONE ABACC ABPOS

TONE 1

EARN 0.2969* 1

(0.0000)

SIZE 0.3787* 0.2313* 1

(0.0000) (0.0000)

BTM -0.3721* 0.4034* -0.4444* 1

(0.0000) (0.0000) (0.0000)

RET 0.2483* 0.3297* 0.0138 -0.3406* 1

(0.0000) (0.0000) (0.7795) (0.0000)

LOSS -0.2535* -0.6714* -0.2710* -0.3134* -0.2217* 1

(0.0000) (0.0000) (0.0000) (0.0000) (0.0000)

ABTONE 0.8414* 0.0000 0.0000 -0.0000 0.0000 -0.0291 1

(0.0000) (1.0000) (1.0000) (1.0000) (1.0000) (0.5540)

ABACC 0.0114 0.0448 -0.0193 0.0489 -0.0326 -0.0415 0.0400 1

(0.8165) (0.3630) (0.6945) (0.3206) (0.5084) (0.3991) (0.4158)

ABPOS 0.6242* -0.0395 -0.0542 0.0202 -0.0394 0.0155 0.7694* 0.0277 1

(0.000) (0.4224) (0.2708) (0.6818) (0.4229) (0.7536) (0.0000) (0.5734)

* Indicate significance at the 5% level

23

The purpose of the Pearson’s correlation analysis is as described in section 3.5.2 to explore the correlation

between two variables, and further to detect issues of multicollinearity before conducting the multiple

regression analysis. The correlation coefficient expresses the relationship between two variables given

different levels of significance (Blumberg, 2011). The intercorrelations are presented in table 4.2 and

reveal no indication of multicollinearity, as the majority of the correlation coefficients are considered low

(Collis & Hussey, 2014)7. Although, the variables TONE, ABTONE and ABPOS are arguably highly

intercorrelated, however this result is expected since ABTONE is the residual from regressing TONE, and

ABPOS is a dummy variable generated from ABTONE. The issue of multicollinearity is thus not present

since the variables are not used simultaneously in the regressions.

The correlation between LOSS and EARN (-0.6714) is according to Collis and Hussey (2014) interpreted

as medium and the question to include both variables simultaneously in the multiple regression analysis

therefore arises. This potential issue is considered by including the interaction variable EARN_LOSS in

regressions (2), (3) where both variables are used simultaneously. Furthermore, Collis and Hussey (2014)

state that variables with low or medium correlation coefficients will not create bias in subsequent

statistical analyses.

4.3 Multiple Regression Analyses

The below tables present the empirical data resulting from the multiple regression analyses. The aim of

the regression on total accruals (see 3.4.2) is to collect the variable ABACC, and the regression is

therefore not presented in this context. The dummy variable ICB is included in all regressions, but not

further reported in tables 4.3 (I), (II). The p-values are used in the decision to accept or reject the null

hypotheses regarding both the OLS regressions and the logistic regression. The alternative hypotheses are

considered supported if p < the level of significance. The regression models used in the statistical tests are

presented below.

𝐻1: 𝑇𝑂𝑁𝐸 = 𝛽0 + 𝛽1𝐸𝐴𝑅𝑁 + 𝛽2𝑆𝐼𝑍𝐸 + 𝛽3𝐵𝑇𝑀 + 𝛽4𝑅𝐸𝑇 + 𝜀 (1)

𝐻2: 𝑃(𝐴𝐵𝑃𝑂𝑆 = 1) = 𝛽0 + 𝛽1𝐸𝐴𝑅𝑁 + 𝛽2𝐿𝑂𝑆𝑆 + 𝛽3𝑆𝐼𝑍𝐸 + 𝛽4𝐵𝑇𝑀 + 𝛽5𝑅𝐸𝑇 + 𝛽6𝐸𝐴𝑅𝑁_𝐿𝑂𝑆𝑆 + 𝜀 (2) 𝐻3: 𝐴𝐵𝑇𝑂𝑁𝐸 = 𝛽0 + 𝛽1𝐴𝐵𝐴𝐶𝐶 + 𝛽2𝐸𝐴𝑅𝑁 + 𝛽3𝐿𝑂𝑆𝑆 + 𝛽4𝑆𝐼𝑍𝐸 + 𝛽5𝐵𝑇𝑀 + 𝛽5𝑅𝐸𝑇 + 𝛽6𝐸𝐴𝑅𝑁_𝐿𝑂𝑆𝑆 + 𝜀 (3)

7

(-)0.90 to (-)0.99 (very high correlation)

(-)0.70 to (-)0.89 (high correlation)

(-)0.40 to (-)0.69 (medium correlation)

0 to (-)0.39 (low correlation)

24