tognum’s resilience business model unicredit german ... · pdf filetognum’s...

TRANSCRIPT

Tognum’s resilience business modelUniCredit German Investment Conference

Joachim Coers Achim SchneiderExecutive Vice President & CFO Head of Investor Relations

September 24/25, 2008

Slide 2 | Tognum – UniCredit GIC 2008 | September 2008

Legal disclaimer

This presentation is for information purposes only and does not constitute an offer to sell or a solicitation for an offer to buy any securities. The shares of Tognum AG will not be registered under the U.S. Securities Act of 1933.

This presentation includes certain forward-looking statements. These forward-looking statements can be identified by the use of forward-looking terminology, including the words "believes", "estimates", "anticipates", "expects", "assumes", "predicts", "intends", "may", "will" or "should", and similar expressions. Such forward-looking statements involve risks and uncertainties because they relate to events and depend on circumstances that may or may not occur in the future. Such forward-looking statements do not represent any guarantees of future performance. Tognum's actual results of operations, including its financial condition and profitability as well as the development of the general economic conditions in which it operates, may differ materially from (and be more negative than) those made in or suggested by the forward-looking statements contained in this presentation.

This presentation also includes certain market and market share data. To our knowledge, there is no single, comprehensive source that reliably describes the overall market and its sub-markets or the competitive situation in the market breakdown presented herein. Unless indicated otherwise, all the statements herein concerning the market and competition are therefore based on our own estimates, some of which have in turn been derived from a variety of sources. It is possible that the actual market conditions and competition may differ from the situation described herein, or that other market participants may come up with different estimates of the market and competitive conditions.

Slide 3 | Tognum – UniCredit GIC 2008 | September 2008

Strategic summary and outlook

Slide 4 | Tognum – UniCredit GIC 2008 | September 2008

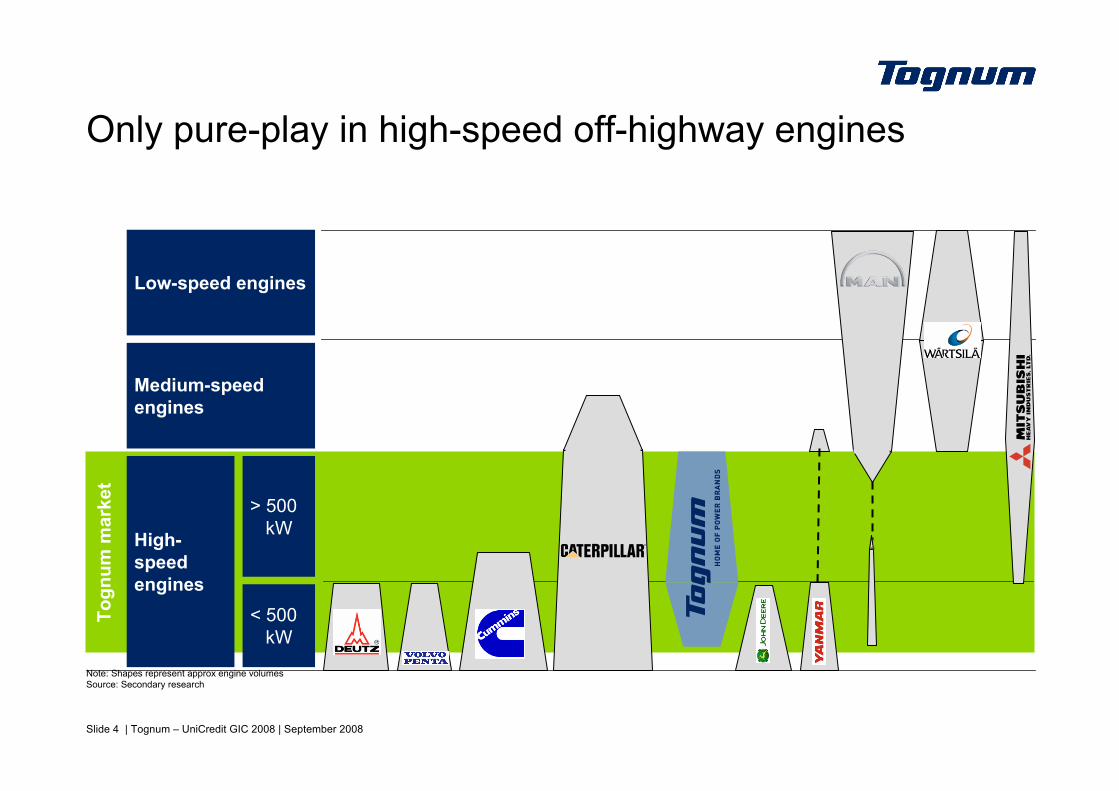

Only pure-play in high-speed off-highway enginesTo

gnum

mar

ket

Low-speed engines

Medium-speed engines

> 500kW

< 500kW

High-speed engines

Note: Shapes represent approx engine volumesSource: Secondary research

Slide 5 | Tognum – UniCredit GIC 2008 | September 2008

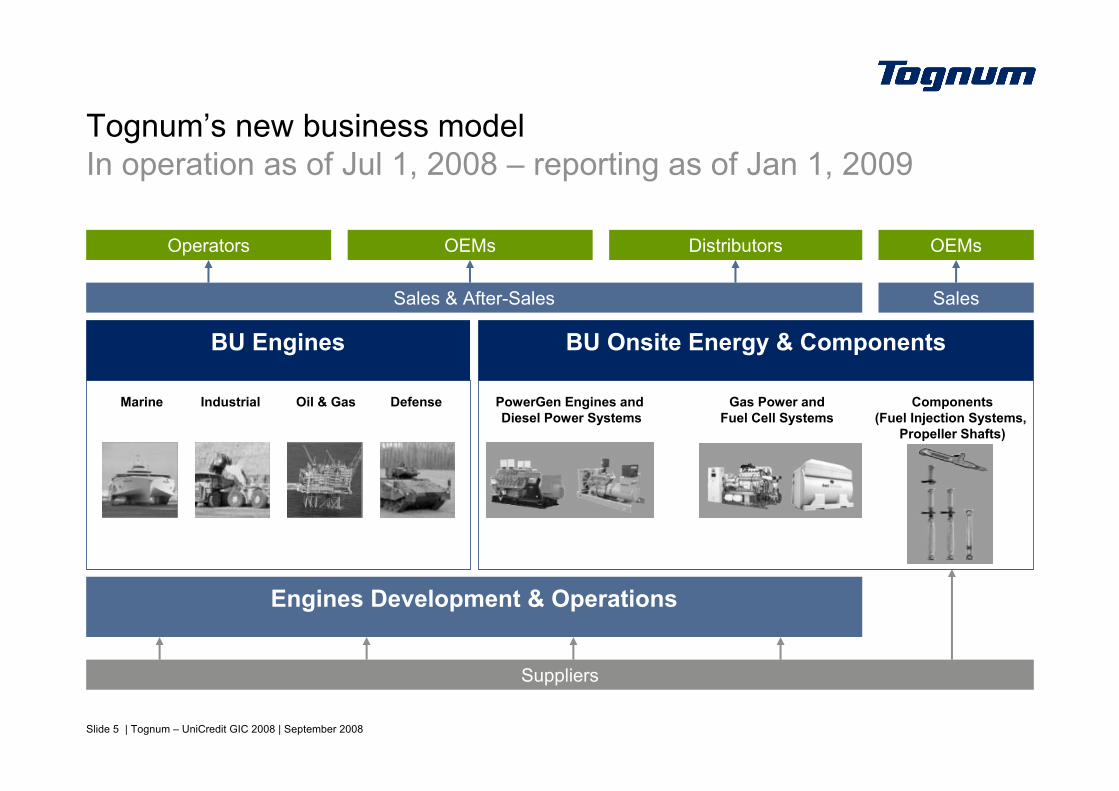

Tognum’s new business modelIn operation as of Jul 1, 2008 – reporting as of Jan 1, 2009

Marine Industrial Oil & Gas Defense PowerGen Engines andDiesel Power Systems

Gas Power andFuel Cell Systems

Components(Fuel Injection Systems,

Propeller Shafts)

Operators OEMs Distributors OEMs

Sales & After-Sales Sales

BU Engines BU Onsite Energy & Components

Engines Development & Operations

Suppliers

Slide 6 | Tognum – UniCredit GIC 2008 | September 2008

Consolidated group performanceFY 2007 and H1 2008

200-916199EBIT adj.

€1.58EPS adj.

€1.01EPS adj.

1,517

1,648

390

2,835

3,107

Tognum Group

300

317

31

527

539

OES&C

-701,401Order intake

-1172,684Order intake

-1082,416Revenue

-14373EBIT adj.

H1 2008 (Jun 30)

-691,286Revenue

FY 2007 (Dec 31)

Consolidation/Corp. Service

Enginesin €m

Slide 7 | Tognum – UniCredit GIC 2008 | September 2008

Outlook FY 2008Adj. EPS target confirmed at >€2.00

+25 % to >€ 2.0013–15 %11–13 %

8.0–9.0 %6.5–7.0 %

1.38$/€ - 1.45 $/€

2008 GuidancePlan 12/07 - 05/08

+25 % to >€ 2.00≥ 13 %≥ 11 %

~8 %~7 %

1.55 $/€

2008 OutlookUpdate 08/08

€ 1.5813.8 %

+11.8 %

~9.5 %~8 %

1.37 $/€

2007 Actual

Revenue growth rate

Avg. USD/EUR fx rate*Market growth diesel engines

Return on Sales (adj.)Earnings per share (adj.)

Market growth OES business

* Tognum estimates based on banks consensus

Slide 8 | Tognum – UniCredit GIC 2008 | September 2008

Source: Company data, Analyst estimates

Limited regional riskGlobal footprint supports stable growthRevenue split 2007 [%]

RoW

AsiaNorth America

Europe

0

10

20

30

40

50

60

70

80

90

100

Tognum MAN Diesel Deutz Wärtsilä Cummins CaterpillarEngines

Slide 9 | Tognum – UniCredit GIC 2008 | September 2008

Uniquely balanced portfolio mitigates cyclical sensitivity45-50% of sales are non-cyclical

Service / Repairs

Split byregion

Europew/o Germany

After Sales/Others

Defense

Marine

PowerGen

Components

OES

CommercialRail

Yacht

C&IAgricultureTrucks

Mining

HeavySpare parts

Medium / Light

Naval / Governmental

Oil & Gas IndustryGas PowerGenDiesel PowerGen

Propeller Shafts

Fuel CellDiesel Genset

Injection SystemsGas Genset

– Broad & well balanced portfolio with >20 different application areas– Financially highly attractive end markets with some high barriers to entry– Excellent growth perspectives regarding energy/power, raw materials/

transportation and industrial development in emerging countries

Rest of World

27%

17%

28%

7%

21%

Asia/Pacific

NAFTA

Germany

Components

OES

Split by subapplication

Split by end markets

After Sales/Others

Defense

Industrial

Marine

PowerGen

Components

OES

Split by subapplication

Split by end markets

After Sales/Others

Defense

Industrial

Marine

PowerGen

Components

OES

Split by subapplication

Split by end markets

After Sales/Others

Defense

Industrial

Marine

PowerGen

Components

OES

Slide 10 | Tognum – UniCredit GIC 2008 | September 2008

Flexible engine & production concept

Gas Marine Mining Rail Genset

Core engine (S4000)

Slide 11 | Tognum – UniCredit GIC 2008 | September 2008

Rail / Locomotives Mining trucks

Why do our customers pay premium prices?

Tognum’s customers benefiting from MTU strengthsin reducing their life cycle costs and engine emissions

– Initial purchase price often makes up only approx. 1.5-2.0% of total life cycle costs– The fuel price is the determining factor for life cycle cost of engines with very long running hours – Accordingly, fuel consumption is a major decision factor when buying engines for applications such as

– Rail (Locomotives)– Mining trucks– Work boats and ferries– PowerGensets (for permanent power)

Fuel 90.5%

Preventive Maintenance 6.8%

Corrective Maintenance 1.1%

Engine price 1.7%

Fuel 92.5%

Preventive Maintenance 4.9%

Corrective Maintenance 0.8%

Engine price 1.8%

Source: MTU FN, customer feedback

Slide 12 | Tognum – UniCredit GIC 2008 | September 2008

Resilient business model succeeds in challenging environmentFY08 guidance confirmed despite currency and cost headwinds

After-Sales

Asia/China

Portfolio

PG/OES

After-Sales

Asia/China

Portfolio

PG/OES

Uniquely balanced portfolio

USD weakness Rising input costs Business units realignment, Rotorion spin-off

Management of mitigating factors:+++ Flexible hedging policy +++ Price increases 2008 and 2009 +++ 2008 sourcing secured for higher volume +++ TOP program execution +++ Increasing global sourcing & production +++

Split by sub-application

Split by end markets

Split byregion

– Balanced geographical split– Diversified product and

production mix– ~22 different subapplications– Flexible production

and allocation set-up

– Financially attractive end markets– Long-term growth perspectives– Turning established positioning into

sustainable earnings growth

Strategic growth initiatives

Slide 13 | Tognum – UniCredit GIC 2008 | September 2008

Product portfolio After Sales

PowerGen/Onsite Energy SystemsAsia & China strategy

Strategic growth initiativesReview of YTD 2008 measures

– New organization structure implemented effective July 1st; reporting to change per January 1, 2009

– R&D for gas engines to enable all engine versions for PowerGen applications

– Initiative to further build out diesel systems– Increased capacity at Katolight installed,

preparation for export (50Hz) in 2009

– JV w/ Hug for exhaust gas after treatment – Delivered propulsion system for the world’s

cleanest Diesel locomotive– Upgraded “Iron Man” (16V4000) for workboats to

higher power output at even lower fuel consumption– First “HotModule Hybrid” offered, a cogeneration

heat/power unit based on gas engine and fuel cell

– Development & production JV concluded and subsidiary established

– First major NPP contracts expected in 2008– Growing demand of premium engines for Chinese

market, e.g. Industrial and PowerGen– Growing export of engines from Asia into other

regions, e.g. PowerGen

– Spare parts centre for improved availability and reduced response times

– SKL expands remanufacturing business for MTU, expecting major order for PowerGen engines

– Malaysian JV for Asian remanufacturing centre – Strengthening European distribution and after sales

Slide 14 | Tognum – UniCredit GIC 2008 | September 2008

Tognum‘sproduct

portfolio

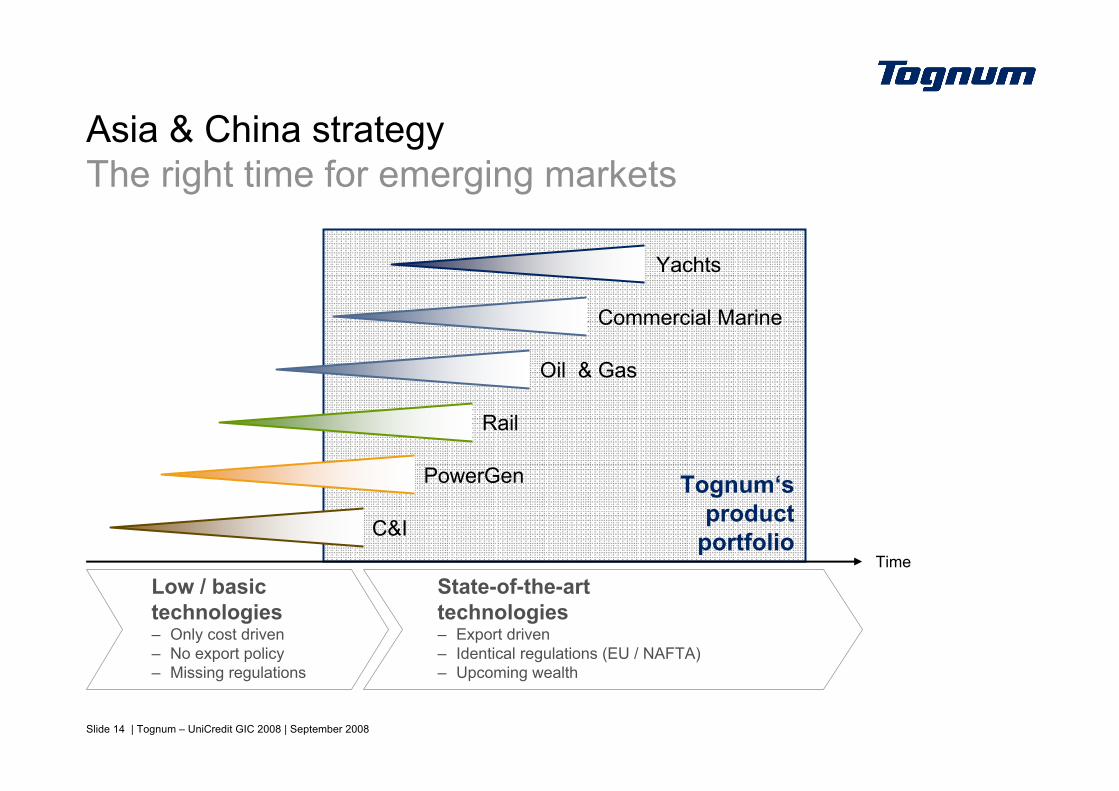

Asia & China strategyThe right time for emerging markets

Time

C&I

PowerGen

Rail

Oil & Gas

Commercial Marine

Yachts

Low / basictechnologies– Only cost driven– No export policy– Missing regulations

State-of-the-arttechnologies– Export driven– Identical regulations (EU / NAFTA)– Upcoming wealth

Slide 15 | Tognum – UniCredit GIC 2008 | September 2008Existing Next step Flexibility

USA(New)

Further expansion of manufacturing capacity to secure growth, flexibility and localisation

Germany(Friedrichshafen)

Asia/Pacific(Suzhou)

Implementation

– Install components manufacturing in Turkey at existing facility

– Selection of new site in USA as first step to built-up components manufacturing in the USD area

– Increase manufacturing capacity in Germany for key components

– Expansion of local sourcing in respective regions

Internationalization of components manufacturing

Existing global assembly footprint

North America(Detroit)

Europe(FN, Turkey)

Turkey(New)

Focus on internationalization

– Install manufacturing capacity first-time outside Germany and increase global sourcing

– Transition to flexible manufacturing sites– Increase local content to further improve sales

(e.g. governmental projects) and natural hedging– Strengthening competitiveness (efficiency, wages)

Investment rationale

– Added capacity in 2008 >25% higher than in 2006– In 2007/2008, Tognum grows faster than expected– In 2009, max. utilization again incl. 3-shift operation

and extended Sunday work in bottleneck areas– Decision taken to further expand capacity now in

order to meet market demand in 2010

Slide 16 | Tognum – UniCredit GIC 2008 | September 2008

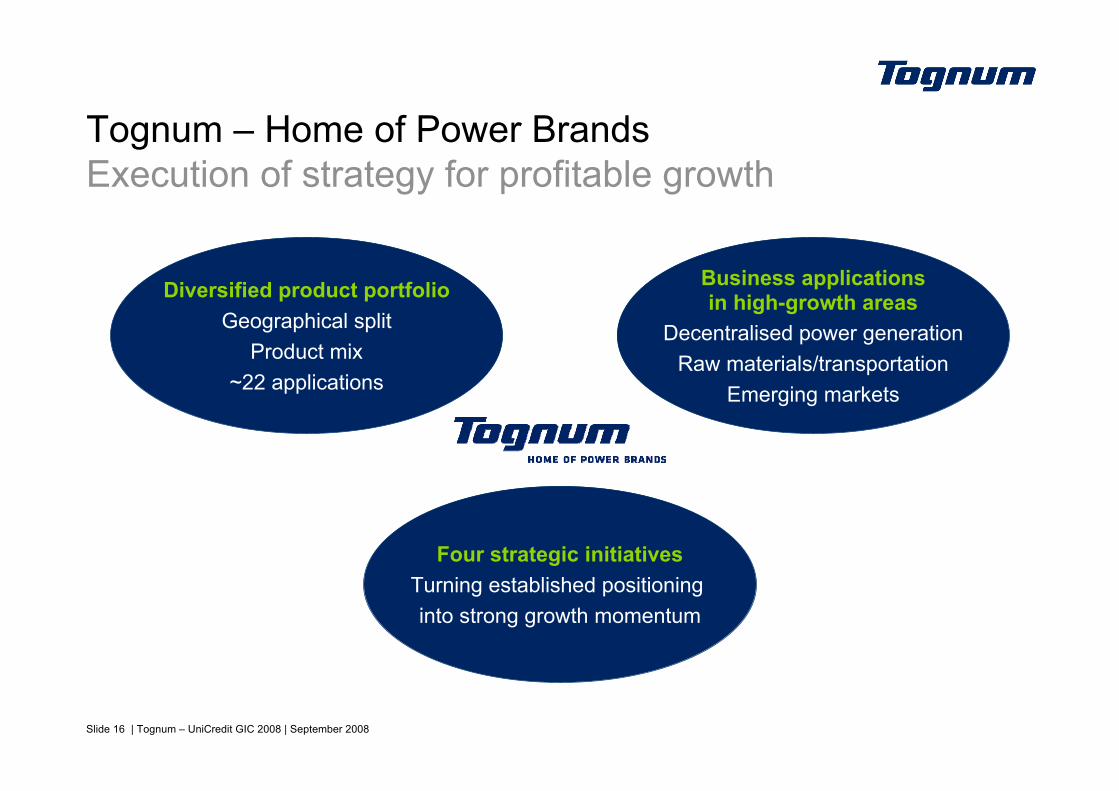

Tognum – Home of Power BrandsExecution of strategy for profitable growth

Diversified product portfolioGeographical split

Product mix~22 applications

Four strategic initiativesTurning established positioninginto strong growth momentum

Business applicationsin high-growth areas

Decentralised power generationRaw materials/transportation

Emerging markets

Slide 17 | Tognum – UniCredit GIC 2008 | September 2008

Tognum AG shareholder structureTotal free float of 65.5%*; MDAX weight ~2%**

Daimler AG25.0 % + 1 Share*

Seeker Management-beteiligung GmbH & Co. KG9.5 % (Group Management)

Schmid Maybach LLC2.7 % (Free float)

Others62.8 % (Free float)

Including– ING Groep > 5 %*– FIL/Fidelity > 3 %*

* According to their releases of Voting Rights (Article 21, Section 21 of the German Securities Trading Act, WpHG) until Sep 17, 2008** As of Sep 22, 2008 according to Deutsche Börse AG

Slide 18 | Tognum – UniCredit GIC 2008 | September 2008

Engines Development & Operations

Slide 19 | Tognum – UniCredit GIC 2008 | September 2008

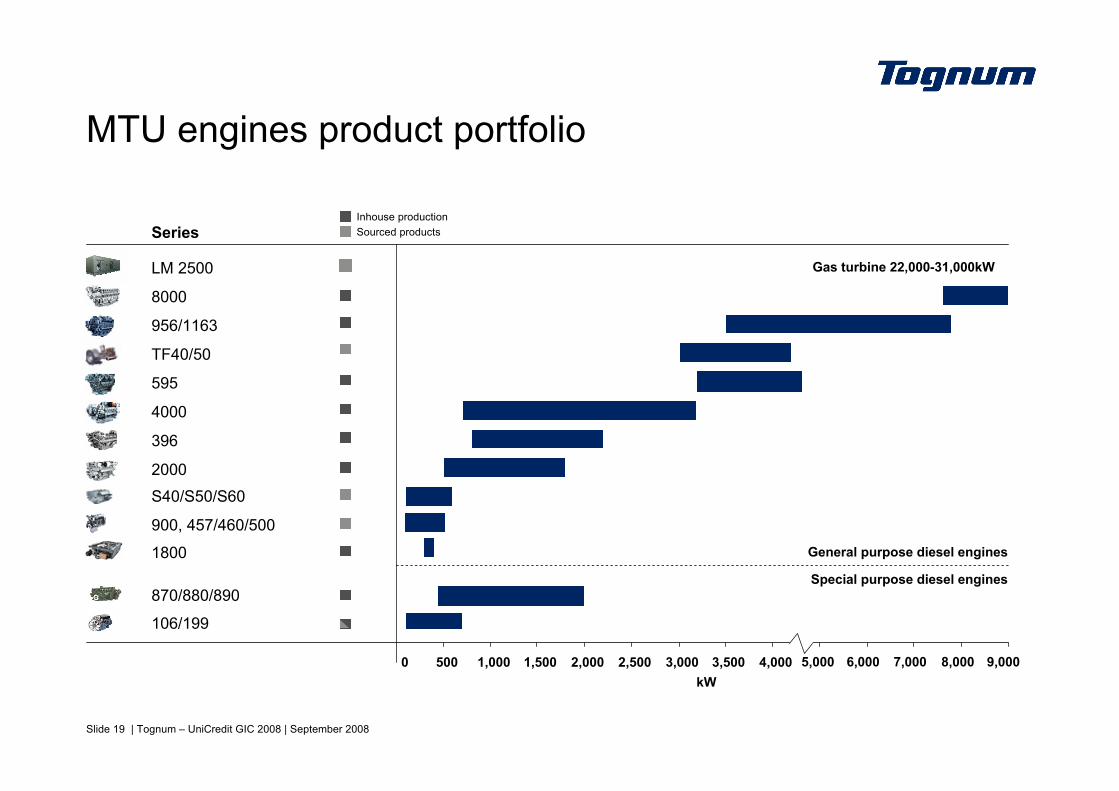

MTU engines product portfolio

870/880/890

900, 457/460/500

S40/S50/S60

2000

396

4000

595

TF40/50

956/1163

8000

LM 2500

1800

Inhouse production

General purpose diesel engines

Special purpose diesel engines

Gas turbine 22,000-31,000kW

5,000 6,000 7,000 8,000 9,0000 500 1,000 1,500 2,000 2,500 3,000 3,500 4,000kW

Series Sourced products

106/199

Slide 20 | Tognum – UniCredit GIC 2008 | September 2008

IN PROGRESS: Exhaust aftertreatment

Benefits– Fuel consumption– Cost– Maintenance– Size and weight

EXISTING: Combustion process

Fuel injection Turbo charging Electronics

Reducing LCC (life cycle cost)

+Build-up of R&D capacity and know-how + JV in exhaust after treatment (with CH-based Hug Engineering)

+

NO2O2NO

Exhaust before Treatment

N2 H2O

after Treatment

SCR-Kat

(NH2)2CO+ H2O

Add-onUrea

NO2O2NO

Exhaust before Treatment

N2 H2O

after Treatment

SCR-Kat

(NH2)2CO+ H2O

Add-onUrea

Meeting emission regulations by – Developing engine and exhaust aftertreatment as one system– System optimization

Key technologies in diesel enginesTognum with internally integrated approach

Slide 21 | Tognum – UniCredit GIC 2008 | September 2008

Benchmarking S4000 vs. competition– Analysis of fuel consumption in same truck model,

in same mine and at same power rating– Long-term fuel economy advantage of 2.5%– At $2.50 per gallon and 6,500 operating hours per

year, this represents annual savings to the customer of ~$23,000 per each haul truck powered by a MTU 16V4000 engines

70.0%

75.0%

80.0%

85.0%

90.0%

95.0%

100.0%

Goldmine -USA

High A ltitude(1) - Chile

High A ltitude(2) - Chile

High A ltitude(3) - Chile

Other

Higher operational availability of trucks High fuel savings for mining companies

Superior characteristics of MTU engines leadingto lower fuel consumption and less service time

Benchmarking S4000 vs. competition– Additional availability of mining fleets

Source: MTU FN, customer feedback

Competition

S4000 2700 HP

CompetitorS4000

Source: MTU FN, customer feedback

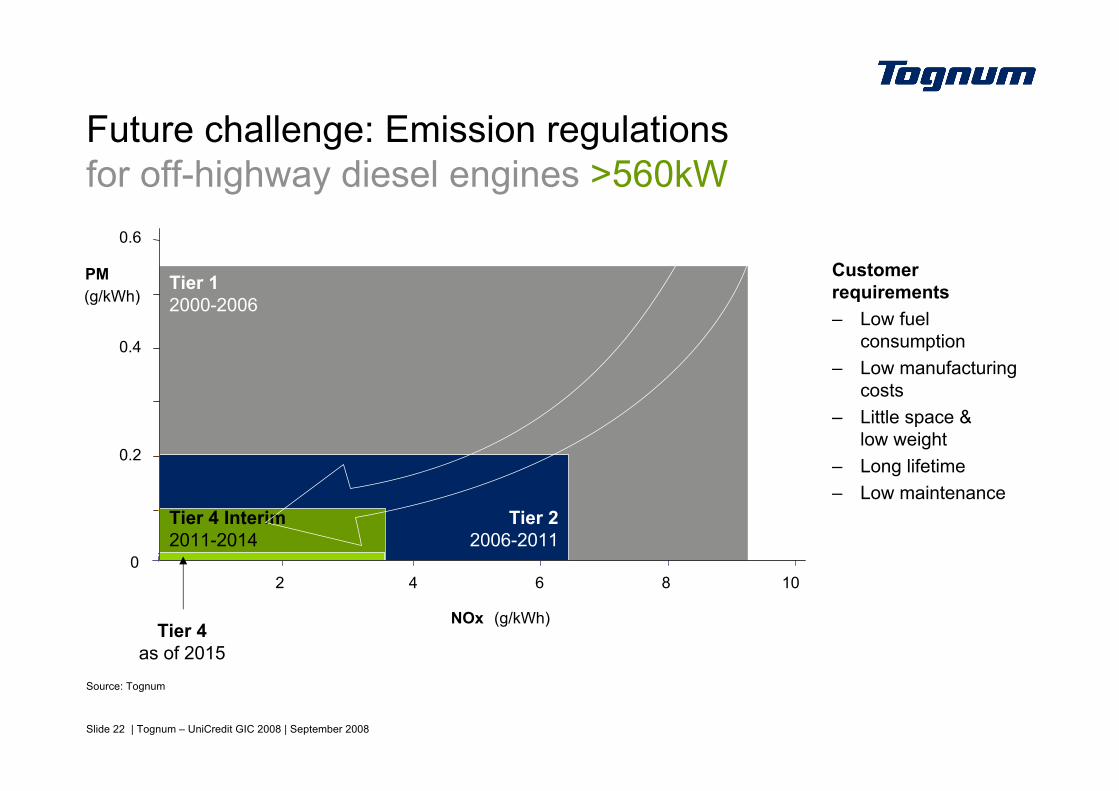

Slide 22 | Tognum – UniCredit GIC 2008 | September 2008

Customer requirements– Low fuel

consumption– Low manufacturing

costs– Little space &

low weight– Long lifetime– Low maintenance

Future challenge: Emission regulationsfor off-highway diesel engines >560kW

(g/kWh)

NOx

PM Tier 12000-2006

2 4 6 8

0.2

0.4

0.6

100

(g/kWh)Tier 4

as of 2015

Tier 4 Interim2011-2014

Tier 22006-2011

Source: Tognum

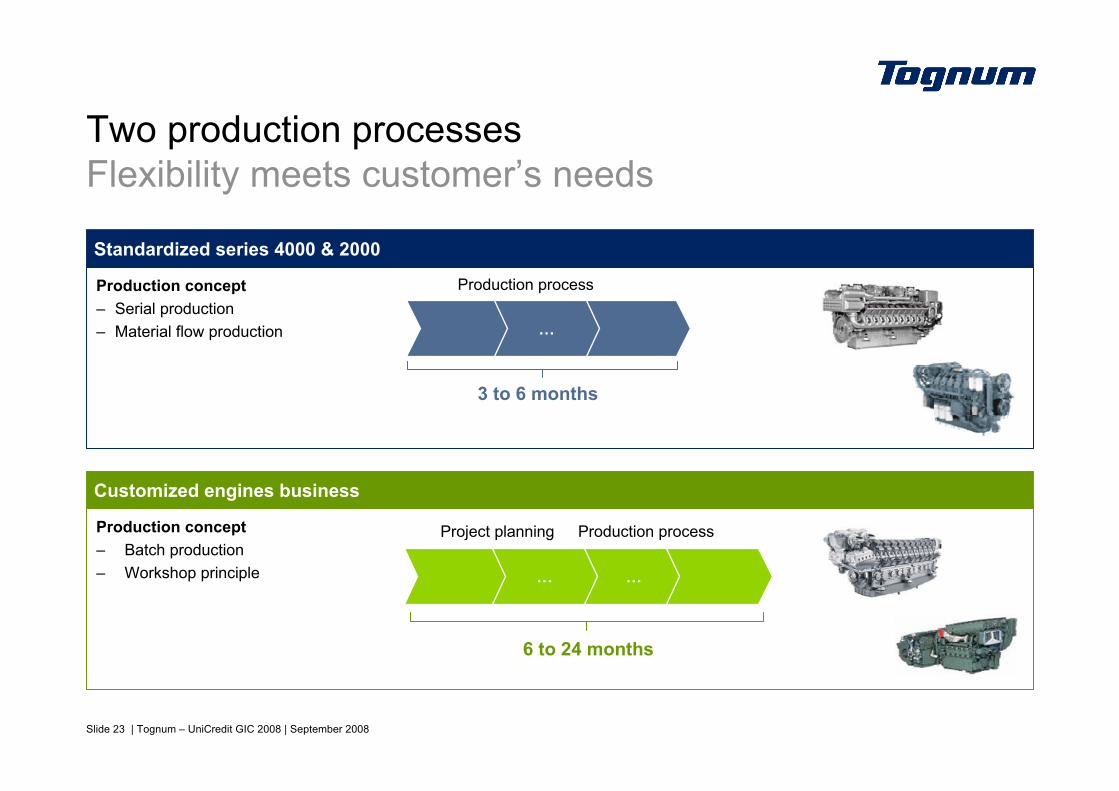

Slide 23 | Tognum – UniCredit GIC 2008 | September 2008

Production concept– Batch production– Workshop principle

Production concept– Serial production– Material flow production

Two production processesFlexibility meets customer’s needs

3 to 6 months

Project planning Production process

Standardized series 4000 & 2000

Customized engines business

……

Production process

…

6 to 24 months

Slide 24 | Tognum – UniCredit GIC 2008 | September 2008

Business Unit Engines

Slide 25 | Tognum – UniCredit GIC 2008 | September 2008

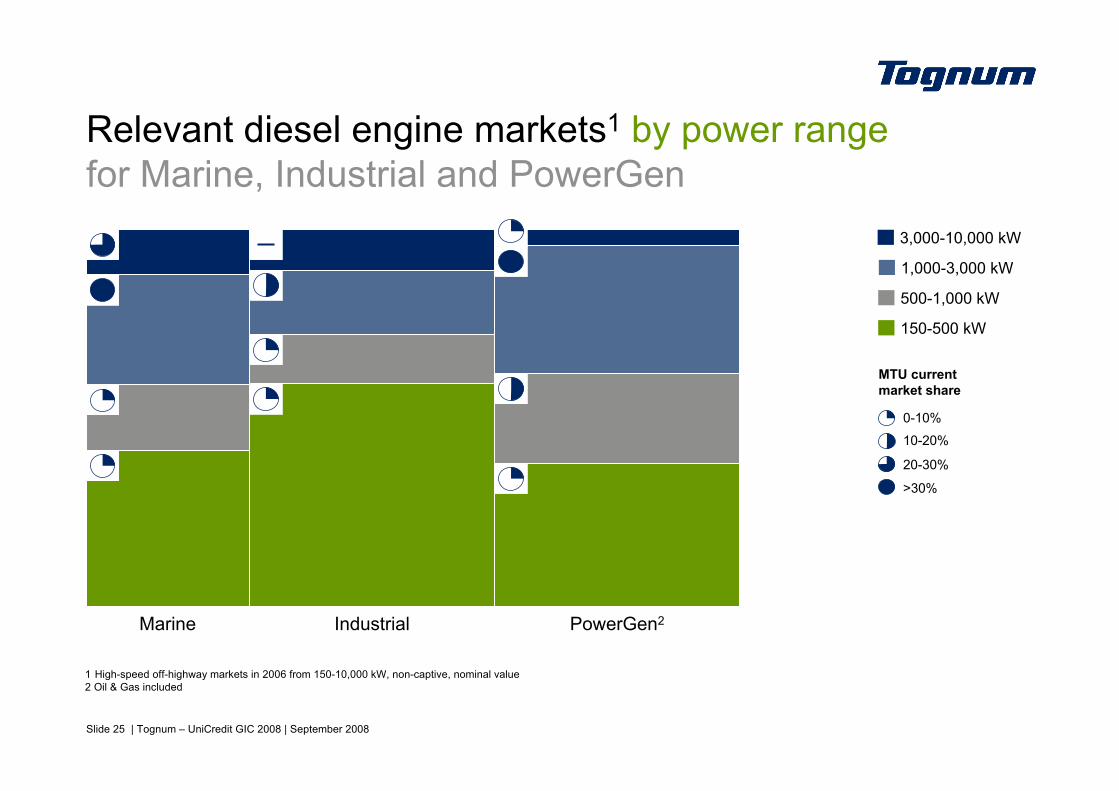

IndustrialMarine PowerGen2

500-1,000 kW

1,000-3,000 kW

3,000-10,000 kW

Relevant diesel engine markets1 by power rangefor Marine, Industrial and PowerGen

150-500 kW

20-30%

>30%

0-10%

10-20%

MTU current market share

1 High-speed off-highway markets in 2006 from 150-10,000 kW, non-captive, nominal value2 Oil & Gas included

Slide 26 | Tognum – UniCredit GIC 2008 | September 2008

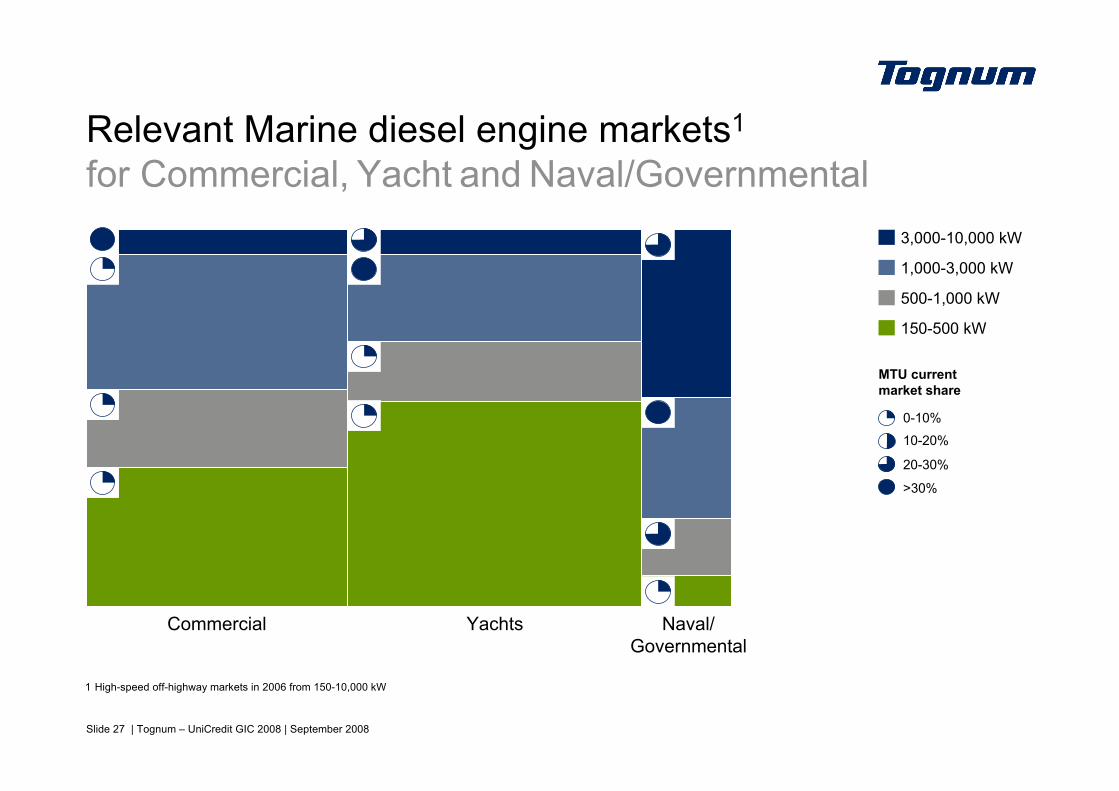

Application Marine

1 Freight boats include a.o. freighter, tanker and container vessels; work boats include a.o. tug, fishery and fire-fighting

YachtMega Yachts, Customised and Serial Yachts, Race Boats, Sport Fishing Boats

CommercialFerries, Freight and Work Boats1, Tug and Crew Boats

NavalFrigates, Coast Guards, Submarines

Slide 27 | Tognum – UniCredit GIC 2008 | September 2008

Relevant Marine diesel engine markets1

for Commercial, Yacht and Naval/Governmental

500-1,000 kW

1,000-3,000 kW

3,000-10,000 kW

150-500 kW

Commercial Yachts Naval/Governmental

1 High-speed off-highway markets in 2006 from 150-10,000 kW

20-30%

>30%

0-10%

10-20%

MTU current market share

Slide 28 | Tognum – UniCredit GIC 2008 | September 2008

Applications Industrial and Oil & Gas

Construction & Industry

Mining Rail Oil & GasExploration

Agriculture

Slide 29 | Tognum – UniCredit GIC 2008 | September 2008

500-1,000 kW

1,000-3,000 kW

3,000-10,000 kW

Relevant Industrial diesel engine markets1

for Agriculture, C&I, Mining, Rail, Oil & Gas

150-500 kW

Agriculture C&I Mining Rail

1 High-speed off-highway markets in 2006 from 150-10,000 kW

20-30%

>30%

0-10%

10-20%

MTU current market share

Oil & Gas

Slide 30 | Tognum – UniCredit GIC 2008 | September 2008

C&I and MiningMTU’s positionTognum benefits from high reliability and durability of its products

Position– Clear #1 supplier for surface mining with

– Premium product position– Unmatched Time Between Overhaul (TBO)

– European leader in mobile cranes– Product innovation leader– mtu Engines renown for consistent performance in extreme

conditions

– Key product offering: – Customised engineering– Flexibility in engine application

Selected customers

Product example

Slide 31 | Tognum – UniCredit GIC 2008 | September 2008

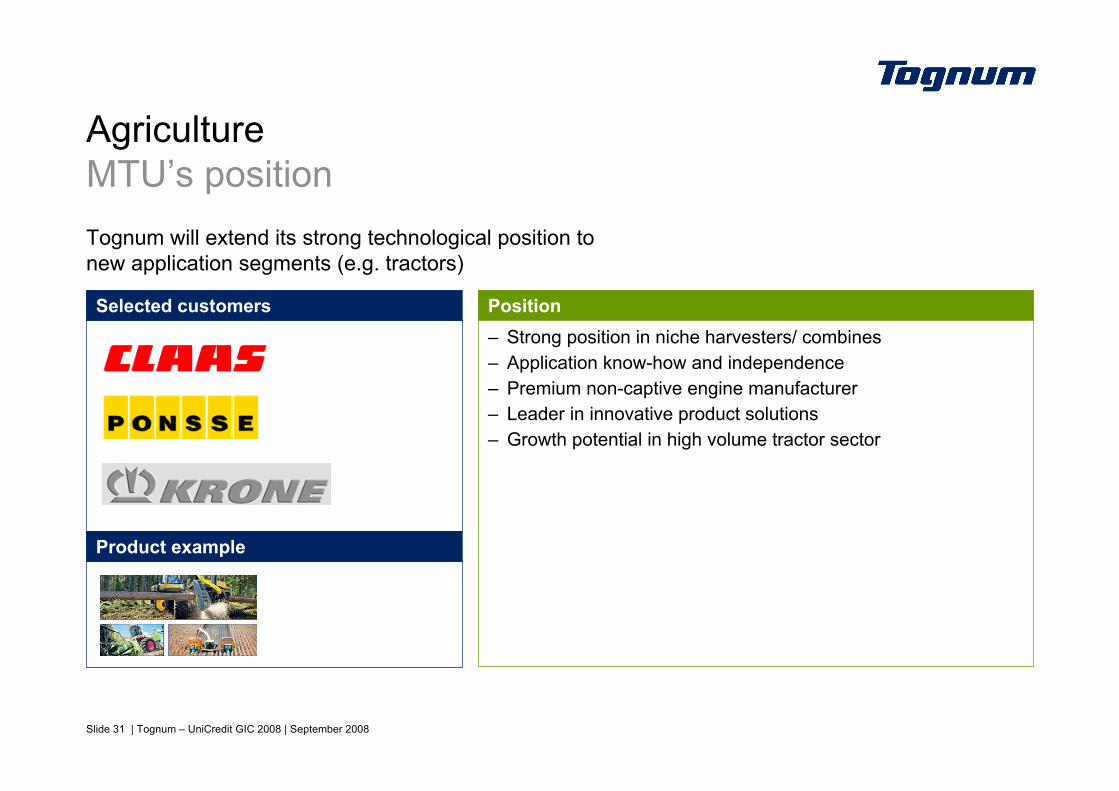

AgricultureMTU’s positionTognum will extend its strong technological position to new application segments (e.g. tractors)

Position– Strong position in niche harvesters/ combines– Application know-how and independence– Premium non-captive engine manufacturer– Leader in innovative product solutions– Growth potential in high volume tractor sector

Selected customers

Product example

Slide 32 | Tognum – UniCredit GIC 2008 | September 2008

RailMTU’s positionTognum will leverage its strong European position and advanced system offerings competence into North American and Emerging Markets

Position– Strong position in European rail market

(esp. rail cars and shunting locomotives)– Market leader for rail powerpacks– Benchmarks for fuel consumption by fulfilling

NOx and particulate emissions standards– In 2007, U.S. locomotive market was entered successfully with

first independently certified EPA Tier 2 (green) engine– Key product offering:

– PowerPack 1800– Series 4000 (e.g. 12V, 2.250 HP/1.680 kW)– Rail automation

Selected customers

Product example

Pacific Harbour Lines (California)

Slide 33 | Tognum – UniCredit GIC 2008 | September 2008

Application Defense

Heavy Medium Light Heavy Truck

Slide 34 | Tognum – UniCredit GIC 2008 | September 2008

DefenseMTU’s premium position and long-standing clientsGlobal defence market to benefit from replacement and repowering activities aswell as new programs

OverviewMTU’s position– #1 in heavy vehicles, #3 in medium/light vehicles– Focus on high-tech solutions with premium engines– Only supplier with system offering (powerpacks, consisting

of engine, gearbox, cooling system and air filtration plant)– Long-standing client relationships

Key success factors– Systems competence– Customised Engineering– Design to power, weight and size– Power density

Key competitors (mainly for medium & light equipment)CAT, Cummins, Deutz, L3, Honeywell

Selected business partners

Key markets

Slide 35 | Tognum – UniCredit GIC 2008 | September 2008

Further growth potential in services & remanSpare parts w/ high market share– Competition generally limited– No access to Daimler engines– Grey market <5%

– Attractive monopoly business model– Potential to further reduce cost

– Proactive business model towards self-servicing end-customers, OEMs and 3rd parties

– Now fully exploiting business potential– Installed MTU engine base ~40,000 engines

After SalesNew growth strategy with focused services

New Services– Service contracts– Remanufacturing– …

Enhancement of organisationand processes– After Sales sales force– Logistics– Network (density, quality)

+ +

Slide 36 | Tognum – UniCredit GIC 2008 | September 2008

Business Unit Onsite Energy & Components

Slide 37 | Tognum – UniCredit GIC 2008 | September 2008

Onsite EnergyA main growth initiative for Tognum Group

Slide 38 | Tognum – UniCredit GIC 2008 | September 2008

Drivers

– Globally increasing energy demand– Resources (oil, gas, renewables) are less readily available– Climate discussion will be impacting markets

Diesel Gas Fuel Cell

Emergency powerPeak power

Continuous power

Decentralised energy systemsDrivers for profitable growth

Tognum focus– Efficient technologies– Growing demand for decentralized energy

Strong upside potential for Tognum as focused and growing technology player

Consequence: energy price for consumers will rise further

Slide 39 | Tognum – UniCredit GIC 2008 | September 2008

– Reliability, availability,maintainability

– Cost of ownership

– Rental and construction companies< 3,000 kW< 3,000 hrs of operation p.a.

Diesel Prime PowerDiesel

– Price-performance ratio– Availability, reliability– Service network

– Hotels, casinos, government, retailstores, data centres, hospitals

– Agricultural (lifestock)

< 3,000 kW< 500 hrs of operation p.a.

Diesel Stand-By Power

– Exceptional availability– Certification, reference

requirements– Application engineering

– NPPs/Nuclear Power Plants< 500 hrs of operation p.a.Diesel Stand-By Power for NPPs

– Reliability, availability, maintainability

– Life Cycle Cost (TBO/time between overhaul,specific fuel consumption)

– Service network

– Decentralised power supply companies

> 3,000 hrs of operation p.a.as combined heat and power(CHP)

Continuous base load power station

Diesel/ Gas

– Cost of ownership– Reliability, availability– Efficiency

– Municipalities– District heating, swimming pools,

sports facilities, facility supply

< 3,000 kWNatural GasGas

– Efficiency– Sustainability– Image: environmental aspects

– Cost of ownership– Reliability, availability; efficiency

Key buying criteria

Fuel Cell(Gas)

– Agriculture– Municipalities

< 3,000 kWBiogas

– Cogen/Trigen applications with biogas, natural gas (and other fuels)

– Hospitals, hotels, industry, data centres, airports

250–2000 kWHot Module

Typical applicationCharacteristics

Onsite Energy Systems Differentiation of market segments

Slide 40 | Tognum – UniCredit GIC 2008 | September 2008

Relevant PowerGen and Onsite Energy markets1

for diesel engines, diesel and gas power, fuel cells

500-1,000 kW

150-500 kW

1,000-3,000 kW

3,000-10,000 kW

20-30%

>30%

0-10%

10-20%

Tognum currentmarket share

Diesel PowerSystems

Gas PowerSystems

FuelCells

1 High-speed off-highway market in 2006/2007 from 150-10,000 kW, nominal value

Diesel PowerGenEngines

Slide 41 | Tognum – UniCredit GIC 2008 | September 2008

PowerGen Engines(Part of Engines Segment until Dec 31, 2008)

Electrical power generation

Airports Office buildings Nuclear power plants,Independent power producers

Slide 42 | Tognum – UniCredit GIC 2008 | September 2008

Cogeneration based on decentralised systemsoffers highest energy efficiency solutions

Losses from transmission and conversion100% Prime energy Usable energy

+

+

NuclearPower Plant

DistrictCogeneration

Plant

LocalCogeneration

Plant

-68%

-25%

-4%

Slide 43 | Tognum – UniCredit GIC 2008 | September 2008

Tognum’s HotModule fuel cell systemis ready to enter the commercial level– Accumulated operating experience

of ~41 years

– > 20 installations in Europe

– Demonstrated co-generation, tri-generation,DC applications and multi fuel capabilities

Slide 44 | Tognum – UniCredit GIC 2008 | September 2008

Injection SystemsL‘Orange (Components)

Slide 45 | Tognum – UniCredit GIC 2008 | September 2008

L‘Orange market positioningoffers further growth opportunities

Engine speed (rpm)

20 – 150

Low-speed< 300

150 – 500 500 – 1,000 1,000 – 3,0003,000 – 5,0005,000 – 7,5007,500 – 10,00010,000 – 15,00015,000 – 30,000> 30,000

Medium-speed 300 – 1,000

High-speed > 1,000Power range (kW)

Tognum’sengine market

Engine market

~ 1,000 ~ 10,000 ~ 30,000*~ number of rel. engines per year * Off-highway > 800kW

Main growth options:

- Medium-speed areas

- MTU’s expansion in high-speed area

- Spare part business

Slide 46 | Tognum – UniCredit GIC 2008 | September 2008

34%

20%14%

6%

14%

6%6%

L’Orange is the leading supplier in its core marketsMarket participants in focused diesel engine areas*

Estimated market volume for fuel injection equipment- Total: < € 600m- Non-captive: > € 400m

Bosch 20%

Woodward 14%

Duap 6%

L‘Orange 34%

OMT 6%

Others 14%

Nico 6%

* Source: Tognum market intelligence, best estimates

On-high-way

Automotive

Off-high-way

Trucks

Truck derivatives(industrial applicat.)

High-speed

Medium-speed

Low-speed

Slide 47 | Tognum – UniCredit GIC 2008 | September 2008

Propeller ShaftsRotorion (Components)

Slide 48 | Tognum – UniCredit GIC 2008 | September 2008

PCs~75%

LCVs~25%

Propeller shaft customer portfolio

Revenues 2007 of > € 200mn

MercedesC-Class

Volvo V70

Mercedes E-Class

Alfa Spider

Mercedes S-Class

Maybach

Mercedes Viano

Mercedes Sprinter

VW Crafter

Mercedes VITO

Luxury Class

High Luxury Class

Medium LCV

Heavy LCV

Upper Medium Near Luxury Class

Vehicle examplesPassenger Cars (PCs) incl. SUVs

Light Commercial Vehicles (LCVs)

Slide 49 | Tognum – UniCredit GIC 2008 | September 2008

FinancialsTognum Group

Slide 50 | Tognum – UniCredit GIC 2008 | September 2008

Business model allows for high visibilitydriven by frame agreements and projectsHigh visibility of sales expectation not fully captured in order backlog

= Business set-up allows for high visibility of salesBacklog not representative because not all elements of sales visibility included !

– Marine– High-power range engines

+ Long delivery periods

– Industrial– Propeller Shafts

+ Close connection and interdependence with OEMs

Level of visibilityMost applicable for application

DriversOrder sizeDelivery pointDuration

– C&I– PowerGen

Order backlog

– Yacht+ Long-term Memorandum of Understanding

– Defense– Navy

+ Long-term contracts

( )( )( )– All applications+ System businessStrongly dependent on specific client

Slide 51 | Tognum – UniCredit GIC 2008 | September 2008

667 727

669790

709

790

815 875

785 773

828

679

2007 2008

Revenues (in €m)

Strong topline growth in H1/08

Order intake (in €m)

+3%

790

709

22%

27%

25%

26%

2,8353,107

28%

25%

24%

23%

1,648 1,517

+14%

Q4

Q3

Q2

Q1

2007 2008

Q4

Q3

Q2

Q1

Slide 52 | Tognum – UniCredit GIC 2008 | September 2008

Outlook development: Revenue guidanceH1/08 growth rate ex-USD headwinds at +18%

2007Actual

Aug ’08Outlook

FX Adj.Outlook

2008Outlook

FX Impact(€7m/$ct)

Add. Volume

€ 2,835 m

1.37

Lower range of 11–13% corridor

FX $/€ 1.38 1.45 1.55

+12%(+/-1pp)

Additional volume compensates partly for fx-related impact

Y-y growth ratesabove > / below < group average

> Marine> PowerGen> OES

< Industrial< Defense< After Sales< Components

Slide 53 | Tognum – UniCredit GIC 2008 | September 2008

48 58

5775

51

44

100 100

107 100

96

88

EBIT adj.1 (in €m) Net profit adj.1 (in €m)

Continued earnings momentum in H1/08Despite USD/EUR fx rate at 1.53 vs. 1.33 in H1/07

1 Excludes any effects from purchase price allocation and one-off items 1 Excludes any effects from purchase price allocation and one-off items

+28%

4451

88

96

RoSH1 15.5% 13.2% EPS

adjH1

€0.87 €1.01

390199

23%

25%

27%

26%

22%

26%

29%

24%

- 3%

200133

2007 2008 2007 2008

Q4

Q3

Q2

Q1

Q4

Q3

Q2

Q1

Slide 54 | Tognum – UniCredit GIC 2008 | September 2008

Outlook development: Adj. EBIT guidanceAdj. EPS guidance stable at >€ 2.00

2007Actual

Aug ’08Outlook

FX Adj.Outlook

2008Outlook

Add. volume

7x77x10

13.8% 14%(+/-1 pp)

Bottom of 13-15%

corridor

€ 390 m

RoS (in %) Additional volume compensates partly for fx-related impact

Deterioratingfactors

– Cost drivers- Commodities- Labour cost

– Expenses for US sourcing & cap. expansion

– BUs realignment– Rotorion

- Spin-off- Warranty

1.37 1.38FX $/€

FX Impact(€2m/$ct)

1.45 1.55

Det.Factors

Slide 55 | Tognum – UniCredit GIC 2008 | September 2008

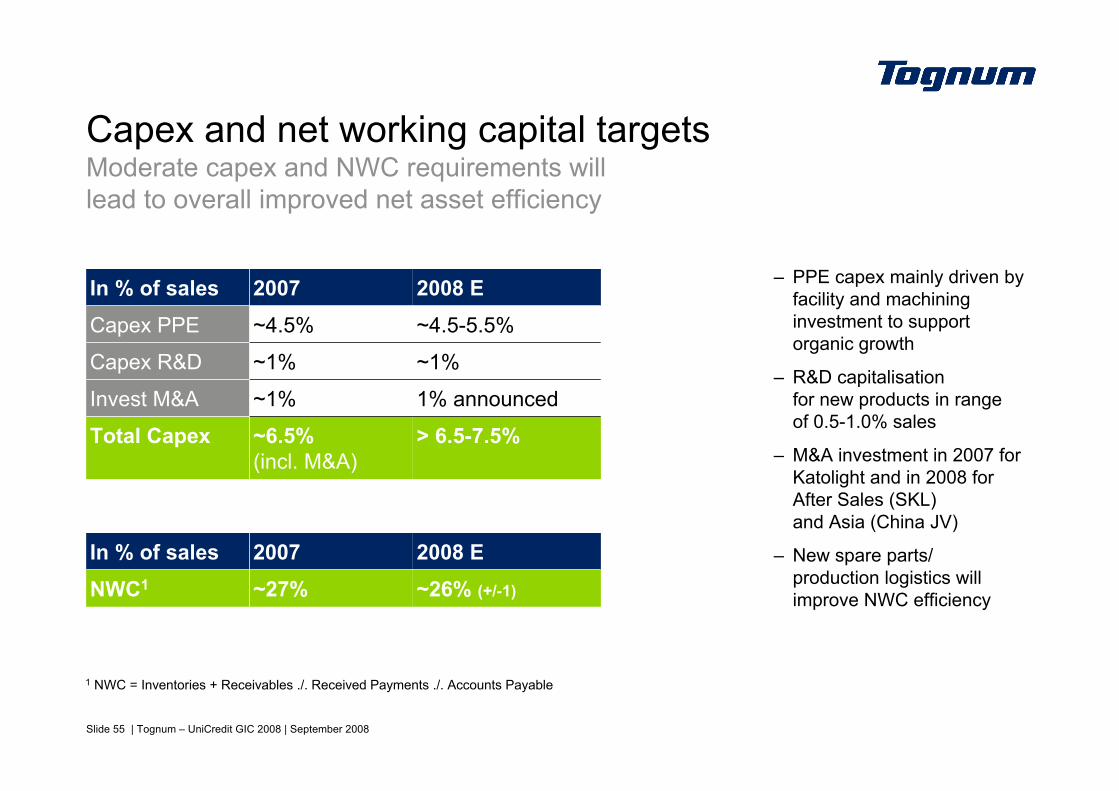

Capex and net working capital targetsModerate capex and NWC requirements will lead to overall improved net asset efficiency

> 6.5-7.5%~6.5%(incl. M&A)

Total Capex1% announced~1%Invest M&A

~1%~1%Capex R&D

~4.5-5.5%~4.5%Capex PPE

2008 E2007In % of sales

~26% (+/-1)~27%NWC1

2008 E2007In % of sales

– PPE capex mainly driven by facility and machining investment to support organic growth

– R&D capitalisationfor new products in rangeof 0.5-1.0% sales

– M&A investment in 2007 for Katolight and in 2008 for After Sales (SKL) and Asia (China JV)

– New spare parts/ production logistics will improve NWC efficiency

1 NWC = Inventories + Receivables ./. Received Payments ./. Accounts Payable

Slide 56 | Tognum – UniCredit GIC 2008 | September 2008

Q2 segmental performance Engines

+19%653549External revenues

15.4%

25%

10%

18%

21%

26%

% of revenue

17.0%

29%

9%

18%

21%

22%

% of revenue

+8%10395Adj. EBIT

+2%

+32%

+17%

+18%

+43%

+20%

-2%

Change

669558Segment revenues

174122Marine

141120PowerGeneration

119102Industrial

7053Defense

165162After Sales/Other

650664Order intake

Q2/2008Q2/2007in €m

Slide 57 | Tognum – UniCredit GIC 2008 | September 2008

Q2 segmental performance Onsite Energy Systems & Components

+14%137120External revenues

3.8%

42%

25%

33%

% of revenue

7.3%

41%

26%

33%

% of revenue

-40%610Adj. EBIT

+20%

+11%

+18%

+16%

+13%

Change

157135Segment revenues

5244Onsite Energy

3935Injection Systems

6655Propeller Shafts

161143Order intake

Q2/2008Q2/2007in €m

Slide 58 | Tognum – UniCredit GIC 2008 | September 2008

Q2 consolidated group performance

100-96103EBIT adj.

790

773

107

669

785

Tognum Group

157

161

10

135

143

OES&C

-38650Order intake

-22664Order intake

-23558Revenue

295EBIT adj.

Q2/2008

-36669Revenue

Q2/2007

Holding/ Consolidation

Enginesin €m

Slide 59 | Tognum – UniCredit GIC 2008 | September 2008

Q2 2008 adjustment bridge

(1) PPA depreciation & amortisation(€ 11.1m)

Adjusted forhedges for FX cashflows (€ 5.7m)

(2) Valuation of FX loans (-€ 0.3m)

(3) Higher incometaxes resulting fromlower EBIT at 25% tax rate (€ -4.6m)

(4) PPA depreciation & amortisation(€ 11.1m)

in €mReported

Q2/2008 AdjustmentsAdjusted Q2/2008

Revenues 790.2 790.2Cost of sales (617.1) 16.8 (1) (600.3)Gross profit 173.1 16.8 189.9SG&A (68.5) (68.5)

(21.4) (21.4)Other operating expenses 0.5 0.5

83.7 16.8 100.5(1.2) (1.2)

Other financial income 3.6 (0.3) (2) 3.3Other financial expenses (2.4) (2.4)

83.7 16.5 100.2Interest income 0.8 0.8Interest expenses (1.3) (1.3)Earnings before taxes 83.2 16.5 99.7Income taxes (20.3) (4.6) (3) (24.9)Net profit / loss 62.9 11.9 74.8

Depreciation and Amortization (28.5) 11.1 (4) (17.4)EBITDA 112.2 5.4 117.6

Research and development costs

Results from operating activitiesShare of profit from investments (equity method)

Earnings before interest and taxes

Slide 60 | Tognum – UniCredit GIC 2008 | September 2008

Tognum Group balance sheet 31.12.2007 vs. 30.06.2008

30.06.200831.12.2007€m

827743Inventories

462465Accounts receivables

5661Cash & cash equivalents

1,4861,385Total short-term assets2,4872,361Total assets

430407PP&E

9591Other long-term assets

Assets

1,001976Total long-term assets141116Other short-term assets

475478Intangible assets

30.06.200831.12.2007€m563535Shareholders' equity394389Pension provisions

268241Accounts payables

445449Short-term provisions and received payments

1612Other short-term liabilities

899782Total short-term liabilities2,4872,361Total liabilities

297345Long-term financial liabilities

135125Other long-term liabilities

Liabilities

1,0251,044Total long-term liabilities17081Short-term financial and

other liabilities

199185Other provisions

Slide 61 | Tognum – UniCredit GIC 2008 | September 2008

294326

389394

31.12.2007 30.06.2008

(245)

(326)

(38)

(79)

36

Net debt/adj. LTM EBITDA

H1 (Q2) 2008 net (financial) debt development€ 79m dividend payment Q2 2008 for FY 2007

Net debt31.03.08

CF fromoperatingactivities

Dividendpayment

Net debt30.06.08

CF frominvestingactivities

Net financial debt (in €m) and leverage

1.6x1.5x

Pensions

Net financialdebt

0.6x 0.7x

Investor contact

Achim SchneiderHead of Investor Relations (CIR)

Phone: +49 (0)7541 90-3318Fax: +49 (0)7541 9090-3318mailto:[email protected]://www.tognum.com

Tognum AG88040 Friedrichshafen/Germany

Financial calendar *Nov 11, 2008 Q3/08 final report & conf. call

Mar 26, 2009 Release of Annual Report 2008

May 13, 2009 Q1/09 final report & conf. call

Jun 09, 2009 Annual General Meeting 2009

* All dates are preliminary and subject to change

Thank you very much!