three year plan: vancity's strategic plan for 2015 to 2017

TRANSCRIPT

1 of 22

Our Three Year Plan is a roadmap

that charts a course for us as we work towards redefining wealth. 2015 - 2017

2 of 22

Table of Contents

I Our vision: Redefining Wealth 3

II Our priorities: More opportunities better executed 4

III Our plan: Lean in today and plan for tomorrow 12

IV Our resources: Develop and redeploy 16

V Our risk: Eyes wide open 20

VI Our opportunity 21

3 of 22

Our vision: Redefining Wealth

Over the past year, we’ve been inspired by the wisdom of our members and communities as they help us see, hear and experience how the real needs of the economy are being translated on the ground. We’ve seen that the deeper and broader our connectivity, the greater the opportunity we have to meet unmet needs and grow the real economy. We’ve also been inspired by our staff, mindful that it’s through our people that we’re able to translate our insights into impact.

We’ve been getting stronger in terms of engaging our members and communities as well as our staff. As a result, our membership is growing. We welcomed 21,997 new members to Vancity as of the end of September 2014, while holding market share in the overall deposit and lending markets – an impressive accomplishment given the competitive environment we’re facing. All this points to the fact that our brand is resonating, members are responding and our communities are reaping the benefits.

So what have we learned about building healthy communities and the real economy?

Building healthy communities is not a one-size-fits-all approach. Rather than focusing on what the markets can give us, building healthy communities requires focusing on member and community needs to define the nature of the opportunity we have. This means that how we engage with members and communities will vary based on our understanding of the underlying systemic issues impacting each community.

Building healthy communities requires social capital. Delivering financial services is not sufficient. To achieve impact at scale, we need more than a strong balance sheet. We need to leverage our convening power to create social networks where community resources and knowledge are used to identify innovative ways to meet needs. This means partnering with business and community leaders, community organizations, associations, government and stakeholder groups to help create the social infrastructure needed to build healthy communities.

Building healthy communities requires investing for the long term. Building relationships takes time and the needs of the real economy are complex. Ironically, the current financial economic system that was originally intended to create value through others is now an end in itself. The focus is on efficient transactions at scale that will maximize financial returns. In the real economy, the focus is on creating long term value by preserving natural capital and building social capital that, in turn, will create a sustainable economy that meets the needs of all its citizens. In short, this means that achieving sustainable growth requires a longer time horizon.

Building healthy communities requires a holistic view of the economy. A healthy society has an economic system that takes into account the principles of financial inclusion, social justice and environmental sustainability.

We are learning how all the connections in the real economy actually work but we understand that if we don’t find ways to re-link financial wealth and social well-being, we will not achieve our vision. We’re also at risk of contributing to the current financial system in a way that moves us away from our vision – of doing what is “good enough” in the community rather than focusing on what is in the long term best interests of our members.

4 of 22

Our priorities: More opportunities better executed

Our understanding of the real economy is growing and we are seeing the opportunities more clearly. At the same time, we continue to operate in a challenging business environment that requires the ability to be agile and disciplined in the face of competitive and regulatory pressures.

• We need to keep the business we have.

We are tracking greater market share because we are acting in ways that are consistent with what makes us different. The result is that we are standing out in our communities and it is driving business. At the same time, given the current pressures on margin, increased volumes are not translating into increased income. The pressure on our balance sheet is compounded by the fact that over the next two years, a significant portion of our mortgage business is maturing as a result of the success of our 2010-2011 mortgage campaigns.

We need to think about how to do things differently in order to keep the business we already have. We know that the members we don’t lose are the best ones to grow with. That said, there is a lot of work required to keep the business we have so we need to be thoughtful about how we engage with our members and bring them along the journey with us.

• We need to renew our infrastructure.

The BAR program will change our banking system and related processes, making it easier for employees to interact in a more meaningful way with our members. In 2015, we will focus on the design, build and test phases of this work keeping in mind our end goal – that we will have a sufficiently robust infrastructure in place to enable us to achieve our vision. The implications for the organization will be a continued draw on resources and a focus on managing the impact of changes associated with the program.

• We need to continue to deliver a values-based differentiated member experience.

We have been doing a lot of good work for our members. We need to continue to leverage the investments we’ve made to accelerate the impact already underway while meeting the needs of our growing membership. Communities are not getting healthier: the income inequality gap is growing; B.C. continues to have the highest rate of child poverty in the country; wage levels are not keeping pace with housing prices; and consumer debt remains at an all time high. The demand for our services continues to grow, our members expect us to be there for them and there is a need for our approach.

2015-2017 Strategic priorities

The strategic priorities outlined in our 2015-2017 Three Year Plan reflect our commitment to continue pushing forward on our transformation agenda. We see evidence of the economic model changing. The disconnect between financial wealth and social well-being is growing. Public discourse highlights the rising discontent with the current financial economy and the social costs of increasing inequality, excessive consumption and environmental breakdown. We know as an organization that convening, collaboration and the needs of the real economy are the places we need to focus. We now see our business model working.

5 of 22

We also see emerging technologies blurring boundaries and redefining who and what influences and shapes society. Technology has exploded the channels of influence and is now a compelling force that is changing how people connect, share and have impact – how people engage to create social capital. Status quo is not a long term option.1 If we want to continue to meet our members where they are, we need to make sure we’re well-positioned to respond to these changes so that we are able to provide value and build healthy communities in ways that our members expect.

What all this means is that we cannot continue to do things incrementally by working at the margins of our business model. We have many strengths to draw upon. We see many opportunities to accelerate impact and build healthy communities and we need to begin thinking about what our business model might look like in the long term in order to achieve our vision.

Lastly and equally important, we know that member and community needs are motivating people to join Vancity. This is a call to action. We need to continue to deliver on the commitments we have already made – to deliver quality financial services and advice to our members in a highly competitive business environment and get the foundational work done without losing sight of the importance of linking everything we do to our vision.

With this context in mind, the priorities in our plan focus on three key themes:

1. We need to put a more intentional focus on innovation to diversify our balance sheet growth. This requires that we lean further into our vision and begin exploring new ways to identify opportunities to accelerate impact that are bold, that we can implement faster, and that support our values-based differentiated member experience.

2. We need to more fully leverage our BAR program to drive internal efficiencies that will in turn generate greater benefits. There is an opportunity here to get more than a core banking system. We can leverage BAR to achieve a significant lift in productivity and agility.

3. We need to transform the way we work to more fully leverage our strengths. We have the talent we need but we need to put more focus on mobilizing the insights and momentum of our people to bring our vision to life.

The following three strategic priorities focus on diversifying our balance sheet growth:

Strategic priorityEstablish leadership in the small and medium-sized enterprise market in Surrey

Surrey is the third fastest growing city in Canada and is expected to have a population of more than 800,000 by 2046. With rapid growth comes an increasing need for social infrastructure. Members, business and community leaders and other stakeholders have shared with us the complex social challenges facing Surrey. Included among them are violent crime, public safety, a growing sex trade, homelessness, poverty, the diverse settlement needs of recent immigrants, and the corrosive effects that urban sprawl is having on transportation and sustainability in this region.

We have been active in Surrey since Vancity opened its first branch in 1990. However there is an opportunity to increase our presence here by focusing on the small business sector which represents the primary vehicle for growth (e.g., job creation) and for creating social capital. More specifically, we want to build a community prototype for activating our business model in Surrey similar to what we have already done with our prototype branches on the retail side.

1 According to Viacom’s Millennial Disruption Index, 73% of Millennials would be “more excited about a new offering in financial services from Google, Amazon, Apple, PayPal or Square than from their own nationwide bank” (JWT Intelligence, October, 2014, p.42).

6 of 22

This community prototype gives us an opportunity to test our business model and explore a new way of working. This includes using our staff differently and experimenting with our credit policies as well as exploring different ways of engaging with partners and stakeholders. Over time, as we dig deeper into what our business members are seeing and experiencing on the ground, we will not only discover innovative ways to meet the unmet needs that are already there, but also uncover opportunities to help build the kind of sustainable community that Surrey residents say they want.

We expect to double our market share in community business in Surrey over the next three years which will allow us to diversify our balance sheet. Equally important, we expect to gain insights that will enable us to use our resources, our brand and our convening power to activate our business model in other communities.

Strategic priority Build a values-based investment portfolio

We have an opportunity to think about our assets in a different way. Currently, our investments are primarily held in liquid assets, of which about 5% are considered impact investments by Treasury. Rather than the current business model that relies on a 96% real-estate secured balance sheet to support our vision, we want to explore how we might build a values-based investment portfolio for Vancity with the goal of diversifying our balance sheet and ultimately earning greater return on our assets in service of the real economy.

As an institution, Vancity can make investments that our members cannot make and given our credibility, we assume we have opportunities that few others would have. The question we want to explore is what kinds of investment models are available to us? There are many opportunities to invest on the environmental side but what is available in terms of investing in our social economy?

We have a strong liquidity position that we can draw upon to leverage our balance sheet differently. In the first quarter of 2015, we want to share our initial thinking around potential options with the Board.

Strategic priority Implement a future proofing strategy

Meeting the needs of the real economy requires that we understand emerging and future trends beyond banking and how they’ll impact our members and communities. To do this, we need to develop an internal future proofing capability. Future proofing refers to the process of anticipating and understanding emerging and future trends in order to stimulate flexibility, agility and adaptability.

In the coming year, we want to focus on emerging and future trends in IT and payments. We are making investments in our core banking system in order to build a platform that will allow us to deliver a values-based differentiated member experience but many members will not see these investments. The real pieces that will differentiate Vancity and that our members will see have more to do with payments and other emerging technologies that are expected to have a significant structural impact on the banking industry as we know it today. The goal of this work is to ensure that once our BAR program is successfully implemented, our thinking will have advanced and Vancity will be well-positioned to respond to new opportunities to grow via impact. Given that Citizens Bank (CB) is the regulatory vehicle for this work, we will be building in connection points with the CB Board to share insights and get feedback as this work unfolds.

7 of 22

An important part of our future proofing strategy will be to enhance our ability to think differently and to encourage the kind of innovative and entrepreneurial thinking and experimenting that our vision requires. To that end, this work will be organized around three key work streams:

1. Trend watching – understanding the intersection between advancements in technology and theirimpacts on human behaviour and social systems using a variety of research and engagementapproaches to gather and synthesize learnings.

2. Disruptive Partnerships – exploring potential partnership opportunities as new technologies areidentified.

3. Rapid Prototyping – engaging employees in designing, developing and testing new solutions foraccelerating impact using an agile, iterative methodology.

Rather than setting up a conventional research and development model2 where a small group of subject matter experts lead this work, we want to build on the approach we have been using over the past year to create meaningful development opportunities for employees to participate. In addition, we’ll also be looking for opportunities to engage with members and community partners who can keep us honest and ensure this work remains grounded.

The strategic priorities described thus far all focus on finding ways to identify more opportunities that are bold and that allow for revenue diversification consistent with our vision.

The remaining two priorities focus more on the foundational work of building our capacity and capability to deliver a values-based differentiated member experience.

Our strategy to simplify the way work gets done looks at more fully leveraging the BAR program to drive internal efficiencies. Embedding the differentiated member experience into our daily practice will be used to transform the way we work to more fully mobilize our talent in service of our vision.

Strategic prioritySimplify the way work gets done

Through the work of our BAR Explorers3 earlier this year, we confirmed that our processes are not simple and get in the way of spending time with members. Rather than creating processes that prescribe a certain behaviour (which has been our pattern), we need to create processes that enable our people to do the right thing. We have the opportunity to optimize our investment in our BAR program by changing the way we work – how we understand the role of processes through the lens of the differentiated member experience as well as how we leverage the knowledge and experience of our people to improve them.

This year we will be implementing a Process Simplicity initiative that will focus on the key processes associated with the implementation of T24. The goal is to create a simple, repeatable, agile methodology (rapid cycle innovation) that will create more opportunity for our people to exercise their judgment and discretion in improving work processes. Once the initial phase of this work is completed, the methodology will then be applied more broadly across the organization so it becomes an integral part of the way we do our work.

By building our capacity to simplify work processes, we will become more productive and more flexible. We will reduce the effort and stress associated with getting work done by eliminating unnecessary

2Research and Development model3A group of staff were asked to participate in some ethnographic work over a two wek period that involved observing member interactions through the lens of the differentiated member experience

8 of 22

steps, decreasing the number of policies employees need to reference, reducing the number of pages in the forms that members are asked to review and sign, etc. For example, we expect that by applying the tools of process simplicity to our mortgage renewal process, we will be able to alleviate the pressure on employees when a large portion of our mortgage business comes up for renewal over the next two years. Rather than simply increasing our staffing levels to handle the workload (as we would have done in the past), we will simplify the work required to process a mortgage renewal.

Ultimately, this work will ensure that no matter where a member interacts with Vancity, there will be one consistent process for all basic banking transactions and staff will have more time to discuss members’ financial health and explore innovative ways to build healthier communities.

Strategic priorityEmbed the differentiated member experience into our daily practice

Delivering a values-based differentiated member experience (DME) is ultimately what we are asking our staff to do. Just as the brand is translating what we do for members, the DME is translating the way we need to work together. It is the unifying framework that will drive behaviour and decision making.

When our people see how what we are doing connects together, the opportunity for integration and collaboration is greater. The gap between front office and back office employees is shored up. Most importantly, employees will be better able to work together to innovate for impact if they have a deeper understanding of how their work links to our vision.

While there are many things we could do to more fully embed the differentiated member experience into our practice, we have identified three key starting points that we believe will offer the greatest opportunity to accelerate our efforts and achieve our goals as set out in this plan. The components are described separately here but they are part of a highly integrated strategy to ensure that employees understand the DME in the same way, see the link to their work and are able to embed it in their daily practice.

Through our leadership We expect to place great demands on our leaders going forward as they play a key role in releasing the creativity and commitment of our employees. In 2015, we will be implementing an experiential learning prototype for executive development. A key objective of this work will be to have a strong talent pool of executives-in-waiting and other high potential leaders within the next 12 months who understand how to incorporate the DME into their work. Over time, it’s expected that through this work we will discover different approaches to experiential learning that will give us flexibility in how we develop our talent in the future.

Through our talentWe’ve done a lot of good work providing core people services to our employees. The time is right to focus on developing our talent. We want to implement a more focused talent strategy that takes the momentum we’ve achieved through our orientation immersion program and extends into the kinds of developmental experiences employees have on the job. The goal of this work is to build a flexible workforce that we can redeploy quickly to respond to emerging opportunities. This means ensuring our people have the skills (e.g., judgment and discretion) and the opportunities to learn and grow with the organization.

9 of 22

Through our credit practices and policiesUnlike other business models that view credit as something exclusive, we believe that where, how and to whom Vancity extends credit describes, in tangible terms, one of the ways we bring our commitment to building healthy communities to life. This requires thinking differently about how credit decisions are made so that we can meet members where they are at and help them achieve their goals. The goal of this work is to translate the DME into operational terms for our end-to-end credit process so members have access to innovative credit solutions that meet their needs and that regardless of the size of the loan being funded, members are confident that Vancity will treat them with the same respect and commitment to their long term success.

In 2015, we will be leveraging the community prototype in Surrey and simplifying our processes and building our capacity to meet the diverse needs of our members and grow the real economy.

Building sustainment into our plans

Last year, our plan spoke to a variety of initiatives undertaken to accelerate impact already underway and build our capacity to do more. These included meeting the needs of the underserved through our new market strategy, leveraging the branch prototypes we launched in 2012 and implementing our new Loans Origination System (LOS). Since that time, we have made considerable progress on all three fronts.

As of November this year, the final suite of the LOS project was delivered, providing significant enhancements to back and mid-office processes and ultimately making it easier for members to do business with us. This year our two prototype branches have been testing different ways of bringing our business model to life including a wrap around service approach and a Business to Business Mentorship program.4 The goal is to leverage these learnings across the branch network and create more opportunities to deliver a values-based differentiated member experience. Our work with the underserved is continuing to deliver new insights into the needs of the real economy. In 2015, we will be looking to raise the profile of our Fair & Fast loan and cheque cashing offerings by considering ways to speed up the process and being a little more open about who gets loans.

While we have already realized impressive benefits from these initiatives, we need to ensure that we are able to fully leverage these investments on a longer term basis. This involves ensuring that they are effectively transitioned into the ongoing operations of the organization so that we do not end up with a growing list of executive sponsors and special projects. In addition, we need to ensure that this work is focused on finding ways to achieve the scale that our vision requires.

In order to ensure the hand-off between strategy and operations is effective, we introduced a stage-gating process last year as part of our new executive committee structure. We have now incorporated sustainment planning as a key stage gate for every strategic investment we make. Key components of our sustainment plans will include a disciplined change management process for ending projects, ensuring the needed capacity within operations is in place to sustain and scale the work and the redeployment of project teams so that we can continue to leverage the knowledge and skills of our people.

In 2015, sustainment plans will be developed and implemented for our branch prototypes, our new LOS system and our Fair & Fast loans offering.

4Experienced business members partnering with newer business owners to provide advice.

10 of 22

Building continuous improvement into our operations

We have invested in Sustainable Wealth Management (SWM) addressing many of the inefficiencies that were holding back the team. We have been leveraging our Good Money Plan and looking for more impact investing. In addition, we redesigned our Community Business platform and worked to make our IT department BAR-ready. We also implemented a retail-focused community investment plan to better leverage the assets of our Community Investment team across the organization and we established a review process for effectively assessing and responding to public policy and public advocacy opportunities for impact.

We need to continue to get value from the investments we have already made in our operations. This requires making continuous improvement an integral part of our operational discipline. We need to make sure there is a strong link between our operational priorities and our strategy so that we continue to improve our ability to execute against our business model and increase our capacity to deliver on our vision.

Advocating for a more co-operative economy

Advocacy is part of our DNA. We do this every day and in many different ways across the organization. We are on the ground with our members and with partners such as the Immigrant Services Society, an organization committed to financial inclusion for those who have difficulty accessing and using financial services.5 We are advocating for social justice. For example, we recently brought public attention to the problem of seniors and financial abuse by commissioning a survey that represented one of the first attempts to uncover the prevalence of this problem in B.C.

We continue to be a strong advocate for the advancement of co-operative principles and practices. Vancity has been a supporter of the Living Wage for Families Campaign since it started in 2008. Since that time a growing number of employers are interested in hearing more about what it means to become a living wage employer. As a result of the investment we have made through our Bologna Co-operative Studies program, more of our staff are seeing the potential of the co-operative model to grow the real economy. Their insights and their passion are inspiring a renewed commitment to finding innovative ways to advance co-operative practices in the communities we serve.

We advocate for community development and social enterprise in a variety of ways. For example, this year we partnered with the City of Vancouver through our Foundation to open a Technology and Social Innovation Centre at 312 Main that will provide a platform to attract and support business and social entrepreneurs committed to social impact and economic growth in the local economy. We look forward to seeing more new opportunities emerge through our work in Surrey. At the same time, we will continue to support green businesses, a sustainable food system, community development and independence, and stable and affordable housing through the variety of impact lending and investment programs we provide to non-profit organizations, community partners, small business and social entrepreneurs.

In addition to working on the ground to support co-operation and co-operative development, Vancity is also committed to working with our colleagues to strengthen the credit union system and advocate for regulatory change in support of a more co-operative economy. In May of this year, we published our position regarding the national credit union legislation and since that time, we have been actively consulting with our colleagues in the system as well as with legislators regarding the role of credit unions and their importance to the future development of the province.

5Last year, more than 10,000 people participated in Vancity’s financial literacy workshops.

11 of 22

Advocacy is core to the work we do every day. In order to remain relevant, we must be connected to our members and to the communities in which they live and work. It is through our advocacy, that we gain the insights we need to activate our business model in service of building healthy communities that are inclusive, just and sustainable.

Summary

In 2012, we added the title Accelerating Impact to describe our plan. At that time, we outlined a plan comprising two parallel tracks: a focus on accelerating growth via impact and a focus on building our capacity to deliver more impact through our people, processes and systems. We acknowledged the challenges associated with balancing the need to maintain our business while continuing to move forward on transforming our business (e.g., putting more of our balance sheet in service of impact). The same challenges hold true for this plan. We are continuing to look for new ways to accelerate growth via impact and we continue to focus on fully activating our business model – member-led innovation – by aligning our people, processes and systems to deliver a values-based differentiated member experience that will help our members make Good Money and build healthy communities.

So what is different in this plan? First, it reflects the insights we have gained about the needs of the real economy and what is required to create impact. As a result, our work is more focused on key areas where we believe we have the greatest opportunity to achieve the scale our vision requires. For example, exploring options for how we might invest our assets in a different way supports the work we are already doing in SWM to diversify our balance sheet away from margin-based income. We are focusing on our values-based differentiated member experience because we expect our future growth to come through this vehicle; the DME will ensure that we use the tools we have to meet the diverse needs of the real economy eco-system.

We are implementing a process simplicity initiative because we need to make sure we can respond quickly to the opportunities that will emerge as a result of our community prototype in Surrey. Through this work, we are taking the next step in terms of leaning into community to activate our business model on a larger scale where we will learn more about how to identify, develop and leverage financial, social and natural capital in service of building healthy communities. We see opportunities for growth here but they require that we build our capacity and improve our productivity.

This plan also places more emphasis on thinking longer term. Our future proofing work will require the ability to internalize insights quickly, prototype concepts and rapidly deliver solutions to members so we can test and learn. Once again, our investments in the BAR program and process simplicity are foundational pieces to creating the capacity we need to fully activate our business model.

12 of 22

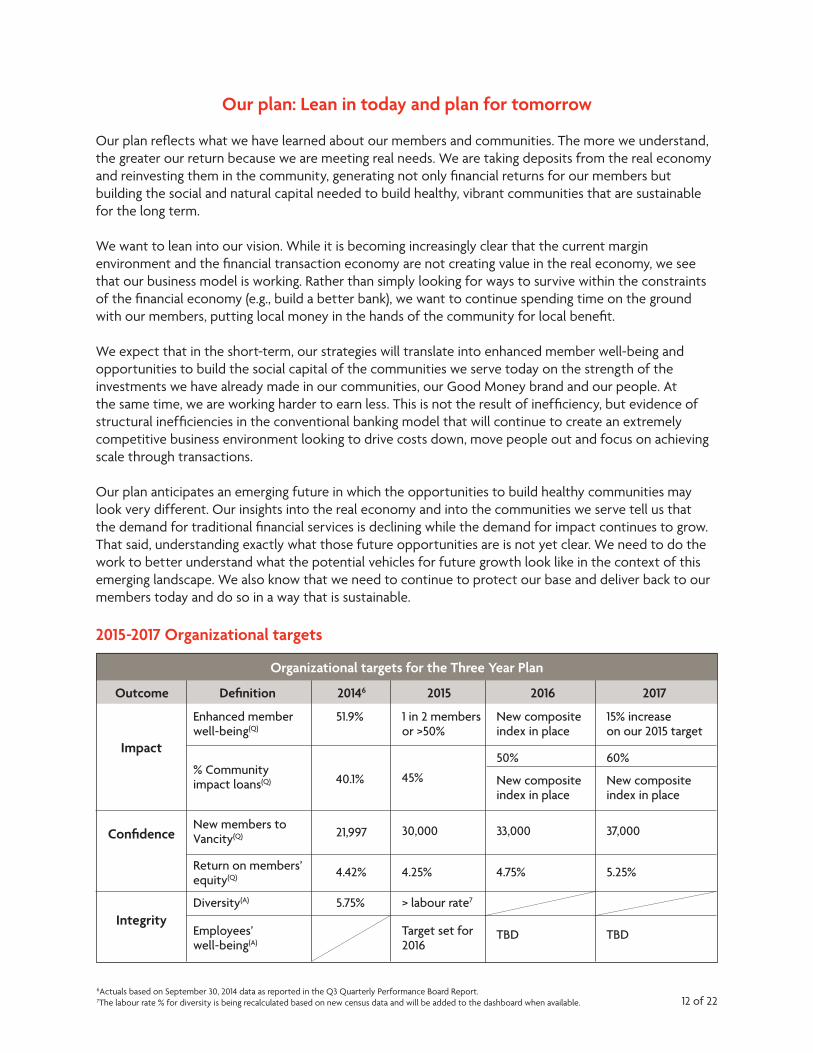

Our plan: Lean in today and plan for tomorrow

Our plan reflects what we have learned about our members and communities. The more we understand, the greater our return because we are meeting real needs. We are taking deposits from the real economy and reinvesting them in the community, generating not only financial returns for our members but building the social and natural capital needed to build healthy, vibrant communities that are sustainable for the long term.

We want to lean into our vision. While it is becoming increasingly clear that the current margin environment and the financial transaction economy are not creating value in the real economy, we see that our business model is working. Rather than simply looking for ways to survive within the constraints of the financial economy (e.g., build a better bank), we want to continue spending time on the ground with our members, putting local money in the hands of the community for local benefit.

We expect that in the short-term, our strategies will translate into enhanced member well-being and opportunities to build the social capital of the communities we serve today on the strength of the investments we have already made in our communities, our Good Money brand and our people. At the same time, we are working harder to earn less. This is not the result of inefficiency, but evidence of structural inefficiencies in the conventional banking model that will continue to create an extremely competitive business environment looking to drive costs down, move people out and focus on achieving scale through transactions.

Our plan anticipates an emerging future in which the opportunities to build healthy communities may look very different. Our insights into the real economy and into the communities we serve tell us that the demand for traditional financial services is declining while the demand for impact continues to grow. That said, understanding exactly what those future opportunities are is not yet clear. We need to do the work to better understand what the potential vehicles for future growth look like in the context of this emerging landscape. We also know that we need to continue to protect our base and deliver back to our members today and do so in a way that is sustainable.

2015-2017 Organizational targets

6Actuals based on September 30, 2014 data as reported in the Q3 Quarterly Performance Board Report.7The labour rate % for diversity is being recalculated based on new census data and will be added to the dashboard when available.

Outcome Definition 20146 2015 2016 2017

Impact

Confidence

Integrity

Enhanced member well-being(Q)

% Community impact loans(Q)

New members to Vancity(Q)

Return on members’ equity(Q)

Diversity(A)

Employees’ well-being(A)

51.9%

40.1%

21,997

4.42%

5.75%

1 in 2 members or >50%

45%

30,000

4.25%

> labour rate7

Target set for 2016

New composite index in place

50%

New composite index in place

33,000

4.75%

TBD

15% increase on our 2015 target

60%

New composite index in place

37,000

5.25%

TBD

Organizational targets for the Three Year Plan

13 of 22

Impact

We have been working on the development of our impact metrics for some time and we are making progress with the benefit of our colleagues in Bologna and in the Global Alliance for Banking on Values. Our goal for this work is to have a way of understanding how outcomes change as a result of our presence in community over time.

For this year of the plan, we will continue to use our existing methodology but will look to set baselines using our new indices in 2015 and then set impact targets using these indices for 2016 and 2017.

Enhanced member well-beingWe expect that over the duration of our plan, our efforts will significantly affect members’ overall well-being because of doing business with us. Why? Because of our investments in the community prototype in Surrey and our continuing work evolving our brand and leveraging our branch prototypes, we will have better conversations with our members. We will be more connected to our members and we will be more embedded in community.

Our staff will have a deeper understanding of what our values-based differentiated member experience really means and why it matters. The credit solutions we provide will be more aligned with the needs of our members and we will have more partners helping us tell the story. As a result, our members will see and feel something different and will understand why we do what we do.

The better we get at connecting the way we act to what is important to our members, individually and collectively, the more member well-being will improve and we expect that it will continue to get better over time.

For 2015, we will leave the target the same as what we set for 2014: 1 in 2 members will strongly agree that their relationship with Vancity improved their well-being. By 2017, we expect to see a 15% increase on our 2015 target.

% Community impact loansWe are making investments in Community Business and we are embedding our differentiated member experience into our daily practice. As a result, we expect that over the next three years, the opportunities to invest in community will increase as our insights into the needs of the real economy deepen and our ability to translate those insights into innovative solutions is enhanced.

For 2015, we expect 45% of our total business lending portfolio will be invested in community impact.8 By 2017, we expect to be at 60% with the caveat that the new composite indices will result in a change to this measure.

Confidence

We measure confidence in two ways: membership growth and return on member equity (ROME). We have already seen that our members, community partners and stakeholders have a growing confidence in what we are doing, want to do more business with us and are more likely to recommend us to others. This is creating new opportunities to invest our capital in building healthy communities and in turn, more opportunities to achieve impact.

8Based on when the first funding happens for the full approved amount.

14 of 22

New members to VancityIn the fall of 2014, we launched our brand campaign and although it will take time before we see results, we do expect it will perform well. That said, we are focusing on more than the brand. The community prototype work will raise our profile in Surrey, generating new partnerships with businesses, community groups and stakeholders. As our story evolves, we expect it will translate into more new members coming to Vancity. Also, our investments in the differentiated member experience in combination with our work on simplifying our processes will allow us to connect more deeply with existing members while responding more quickly to the emerging needs of new members. In sum, we expect our current trajectory in membership growth to continue.

For 2015, we expect to see 30,000 new members come to Vancity. By the end of 2017, we anticipate an increase of 100,000 new members over three years.

Return on members’ equity (ROME)ROME is an indicator of how we will achieve our top line growth and preserve our capital while still being able to deliver on our commitment to Shared Success.9 A key assumption of our fiscal framework is that in the long run, our capital accumulation must be equal to our asset growth rate. Our focus is on driving profitability through acquiring, attracting and retaining members who share the same values and who want to do business with us; this allows us to build our capital base through retained earnings and create a runway for future growth opportunities.

Our plan assumes a prolonged path to economic recovery with traditional forms of revenue generation producing more shallow returns than in the past. That said, the business is producing. The fact that we choose to share our earnings with front-line employees through profit share, our communities through a portion of Shared Success and our members through patronage and dividends is a conscious choice we make, but the productivity and output of the business is very high.

As of September 2014, we are projecting ROME at 4.25% for 2015, increasing to 5.25% in 2017 as we begin to realize the benefits of our investments in our infrastructure and our differentiation, and position ourselves to take the next step in bringing our business model to scale. Based on the results of our stress testing, our planning assumption is a capital adequacy ratio of 13 percent.

Integrity

It is through demonstrating integrity that we build our members’ trust in who we are. We do this by being transparent and accountable about the way we do business.

In 2013, we selected diversity as a key indicator of integrity. Our goal was to address the diversity gap in our workforce by focusing first on persons with disabilities. While the indicator we selected was not ideal (i.e., labour rates at Vancity), it gave us a starting point for addressing an important issue. Since that time, we have achieved our goal of exceeding the labour rate for persons with disabilities and through the process, learned a great deal about the role of diversity in bringing our vision to life. For 2015, we will keep our diversity target of exceeding the labour rate but this will be the final year. This does not mean we are taking our foot off the gas. We will continue to monitor and report on this metric.

As part of this year’s plan, we want to develop and launch a new indicator of integrity–employees’ well-being. Unlike employee engagement which is the result of what we have done in the past, we want to develop a leading indicator so we have the ability to be more proactive in supporting and developing our talent. We also want a measure that focuses more on employees collectively than individually so we have

930% of our net earnings are distributed to our members and communities through the Shared Success program.

15 of 22

more opportunity to reinforce working collaboratively. This does not mean that we will ignore individual voices – only that we want to be more intentional about breaking down silos and working collectively in service of our members.

In 2015, our goal is to be able to set a target for employees’ well-being that we can then report against in 2016.

Summary

We are growing our assets in a values-aligned way but margins are at a historic low. This trend is not expected to change in the near future and regulatory pressures on our business model will continue. That said, we believe our plan is the right one for our members and the communities in which they live and work.

We see short term opportunities to achieve growth via impact, as our vision continues to resonate with our members and in the communities we serve. We also see longer term systemic challenges that require being more thoughtful about our future. Given the rapid pace of change we are seeing and experiencing, the time is right to begin exploring different kinds of business services/models that will allow us to meet the needs of our members and communities in the future.

16 of 22

Our resources: Develop and redeploy

Last year, our focus was on making the shift from “resource ownership” to “resource sharing” by leveraging the knowledge and skills of our staff through redeployment and training while controlling expenses at the same time. We focused on using short-term assignments and cross-functional teamwork to engage staff in our transformation agenda and begin breaking down divisional silos. In addition, BAR gave us a unique opportunity to begin working differently. We can leverage the infrastructure we are already building, including our accountability framework, in service of promoting the collaborative teamwork and continuous learning we need to deliver a values-based differentiated member experience.

This plan builds on the successes we have had over the past year. We want to continue creating new opportunities to move our people around and build critical skills that will increase our capacity to innovate for impact. While we are delivering on BAR, we will look to keep our organization vital and maintain the engagement we have built up over the past several years. We will continue pressing for agility, timeliness and the clarity needed to execute well. Ultimately, this will allow us to not only to be more efficient in the way we work, but more effective in terms of the benefits we are able to realize against the investments we are making.

2015-2017 Financial plan

Our balance sheet is growing. We welcome more members each year, yet the yield we generate is declining as a result of a very low interest rate environment. A key underlying assumption of our financial plan is that the current rate environment is the “new normal” and access to finances will continue to be easy, convenient and inexpensive creating pressure on earnings and return on members’ equity.

Our plan focuses on continuing to look for ways to accelerate impact and accept a lower pace of asset growth while holding the line on expenses. In the short term, we want to maintain our relationship in the market and keep our current structure intact. We will look to focus on one or two opportunities in the strategic space and will reallocate from within our own resources to explore them. At the same time, we will retain our commitments to invest in our people and our infrastructure as we know this is what will set us up for longer term success. For example, we believe Process Simplicity will help free up our capacity for growth.

We expect to see a healthy lending growth level of $655 million annually. Asset growth is expected to range between 3.15% and 4.25% over the next three years. We will invest our capital in retail and the business community, particularly in Surrey, while maintaining our capital adequacy ratio at 13% over the next three years.

As the balance sheet growth expectation is somewhat subdued over the next three years compared to recent history, we believe an 80% new growth funding ratio10 is achievable but will require focused attention on delivering a values-based differentiated member experience and strengthening our ability to respond quickly to the needs of our growing membership.

10A key assumption in our fiscal framework is that we will fund at least 80% of new member loans with new member deposits and the remaining 20% through wholesale funding. This ensures the member engagement and connectivity we need to build healthy communities.

17 of 22

Sustainable growth targets

A breakdown of funds under administration (FUA) and assets under management (AUM) is summarized below:

Community Member Services (CMS) – The underlying assumption regarding retail lending is that we will continue to grow with a growing housing market. While the new volume forecasted is higher than past years11, the significant amount of upcoming mortgage maturities, particularly over the next two years will result in a marginally lower level of retail loan net growth than in recent history. Our goal is to renew at least 90% of these mortgages and may require more resources be deployed to maintain this target.

Community Business Banking (CBB) – We expect to increase our lending in the Surrey market as a result of our work with small and medium sized businesses and the activation of our community prototype. We also anticipate growth in the co-operative housing sector as many housing co-operatives are nearing the end of their federal operating agreements which threatens their existence as a provider of affordable housing.

Community Real Estate (CRE) – The subdued CRE growth is primarily driven by the need to maintain our capital adequacy ratio at 13% over the next three years.12 That said, by scaling back non-impact lending, we will also create more capacity to partner with Community Investment and Community Business Banking to explore co-operative housing opportunities and create a more integrated deal flow across the lines of business.

Visa* – We have a significant portion of our membership actively using their Vancity enviro™ Visa cards (148,000 as of September 30). The portfolio is relatively mature. The successful financial literacy programs we implemented over the last three years resulted in more knowledgeable members many of whom do not carry a balance from month to month. As a result, the FUA growth performance of this portfolio is expected to remain stable with modest growth.

Sustainable Wealth Management (SWM) – Given the extremely strong performance of capital markets in 2014, we are reluctant to predict a similar performance in 2015. The 6% year over year increase represents the growth we anticipate in our net new volume to our members.

Net growth projections 2013 2014 2015 2016 2017 $ millions Actual Forecast Plan Plan Plan Members’ lending CMS $ 389 $ 408 $ 343 $ 353 $ 400 CBB 87 105 189 218 214 CRE 206 150 75 75 75 VISA 9 1 8 8 8 Total lending – net growth 691 664 615 654 697 Members’ deposits CMS 381 282 370 393 419 CBB 310 194 122 130 138

Total deposits – Net growth 691 476 492 523 557

SWM assets under management 507 392 220 224 238

Total FUA growth 1,889 1,531 1,326 1,401 1,492

11Estimated at a 7% year over year growth in new volume.12This reduction in new business volume in CRE corresponds to 8-12 loans per year and will have minimal impact on the department.*Visa Int./Vancity, Licensed User.™enviro is a trademark of Vancouver City Savings Credit Union.

18 of 22

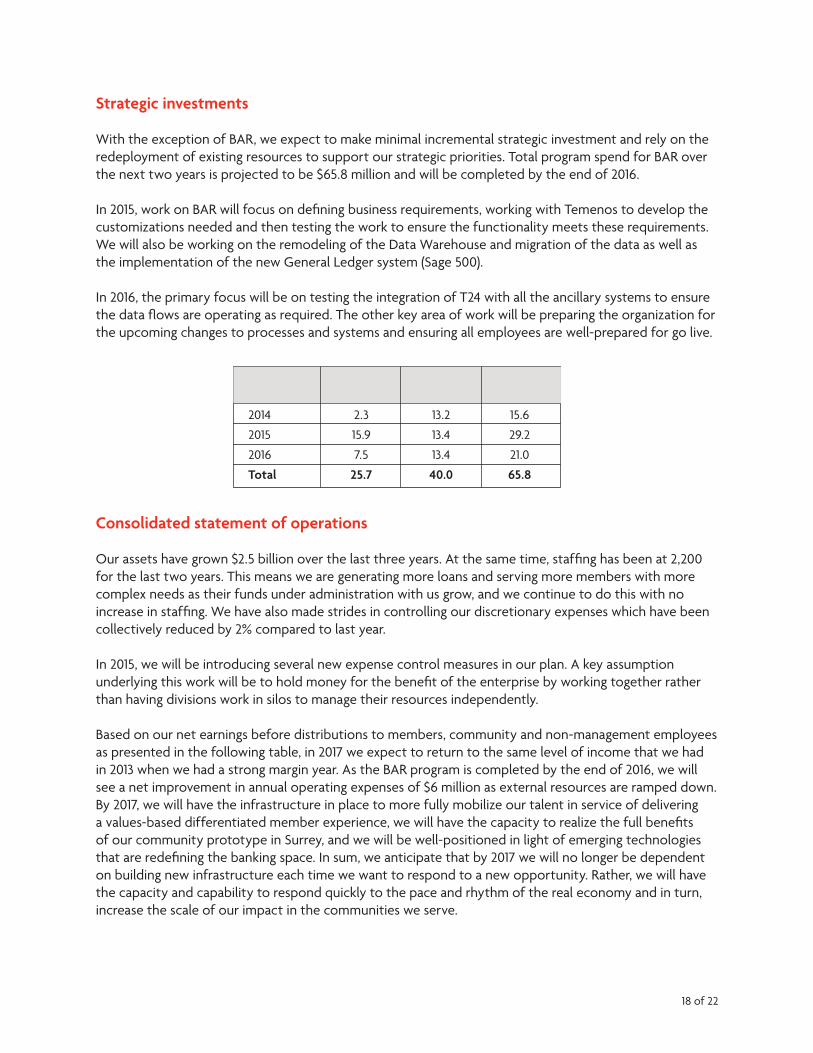

Strategic investments

With the exception of BAR, we expect to make minimal incremental strategic investment and rely on the redeployment of existing resources to support our strategic priorities. Total program spend for BAR over the next two years is projected to be $65.8 million and will be completed by the end of 2016.

In 2015, work on BAR will focus on defining business requirements, working with Temenos to develop the customizations needed and then testing the work to ensure the functionality meets these requirements. We will also be working on the remodeling of the Data Warehouse and migration of the data as well as the implementation of the new General Ledger system (Sage 500).

In 2016, the primary focus will be on testing the integration of T24 with all the ancillary systems to ensure the data flows are operating as required. The other key area of work will be preparing the organization for the upcoming changes to processes and systems and ensuring all employees are well-prepared for go live.

Consolidated statement of operations

Our assets have grown $2.5 billion over the last three years. At the same time, staffing has been at 2,200 for the last two years. This means we are generating more loans and serving more members with more complex needs as their funds under administration with us grow, and we continue to do this with no increase in staffing. We have also made strides in controlling our discretionary expenses which have been collectively reduced by 2% compared to last year.

In 2015, we will be introducing several new expense control measures in our plan. A key assumption underlying this work will be to hold money for the benefit of the enterprise by working together rather than having divisions work in silos to manage their resources independently.

Based on our net earnings before distributions to members, community and non-management employees as presented in the following table, in 2017 we expect to return to the same level of income that we had in 2013 when we had a strong margin year. As the BAR program is completed by the end of 2016, we will see a net improvement in annual operating expenses of $6 million as external resources are ramped down. By 2017, we will have the infrastructure in place to more fully mobilize our talent in service of delivering a values-based differentiated member experience, we will have the capacity to realize the full benefits of our community prototype in Surrey, and we will be well-positioned in light of emerging technologies that are redefining the banking space. In sum, we anticipate that by 2017 we will no longer be dependent on building new infrastructure each time we want to respond to a new opportunity. Rather, we will have the capacity and capability to respond quickly to the pace and rhythm of the real economy and in turn, increase the scale of our impact in the communities we serve.

($millions) Capital Operating Total expenses expenses

2014 2.3 13.2 15.6

2015 15.9 13.4 29.2

2016 7.5 13.4 21.0

Total 25.7 40.0 65.8

19 of 22

Summary

We have made good progress in defining and achieving community and member impact and we have done so largely through lending growth. The regulators worldwide are signaling that this is precisely the type of change that will build a more sustainable financial system – a more inclusive, more trustworthy form of banking that addresses the needs of the real economy. That said, the practical application of this new direction is still evolving and current rules and procedures still align with a status quo banking environment.

Our definition of sustainable growth is that we are able to meet our capital requirements with retained earnings as long as the needs of the community are met and we maintain our commitment to Shared Success. In the short term, we are dependent on a highly commoditized retail model in which our asset growth is driven exclusively by our margin income. In the past, this model produced enough income to allow us to experiment. It no longer does and given the current business environment, we see no relief in the future. We do not see strong underpinnings in our current economic system; rather we see a more fundamental structural problem that will ultimately change the way people access financial services.

With this context in mind, we have prepared a fiscally responsible plan that includes a subdued ROME projection over the next three years. This will allow us to protect our capital and retain the ability to serve our members today while leveraging BAR to accelerate our transformation agenda. In addition, our plan makes room to begin work on the bigger question of whether or not we see a different future for our members and communities over the next five to ten years. As well, we will explore opportunities to evolve the composition of our balance sheet so that we are well-positioned to meet the changing needs of the real economy.

Consolidated statement of operations 2013 2014 2015 2016 2017 $ millions Actual Forecast Plan Plan Plan

Net interest income $ 341 $ 341 $ 351 $ 365 $ 373

Loan impairment expense 7 15 16 16 16

Fees and other income 74 73 71 82 89

Total operating income 408 399 406 431 446

Operating expenses 315 333 345 356 355

Net earnings from operations 93 66 61 75 91

Distribution to members 10 7 7 8 10

Distribution to community 10 7 7 8 10

Net earnings before tax 73 52 47 59 71

Income tax 12 8 4 8 12

Net earnings 61 44 43 51 59

Net earnings before distributions 82 60 62 71 80

20 of 22

Our risk: Eyes wide open

Low risk does not equal better risk. The key to effectively managing risk is understanding. This requires having sufficient insight into the nature of risk so that we can knowingly go into situations that others might consider high risk. We can do this as long as we have the appetite, mitigating actions, follow-up, deployment capability and level of collaboration needed to address the risk.

Our risk appetite framework gives us the insights we need to ensure we make decisions with our eyes wide open. It does so in the following ways:

1. By aligning our risk appetite with our strategic goals – making transparent the level of risk we want to take as well as the risks we do not want to take in service of building healthy communities.

2. By strengthening our decision making – providing the rigor and discipline needed to make informed decisions.

3. By reducing operational losses – providing the capability to identify and respond to unexpected events and minimizing associated losses.

4. By providing an integrated view of risk – understanding the interdependencies across the organization and facilitating integrated responses to multiple risks that may be occurring at the same time.

5. By identifying opportunities – providing insights into a full range of potential events and proactively defining the nature of potential opportunities.

6. By optimizing the deployment of capital – assessing overall capital requirements and enhancing capital utilization.

We have nearly completed the work we began last year to review our risk appetite statements which describe what we will be monitoring against and how we will be reporting to the Board. We will be bringing this forward to the Risk Committee in the new year.

21 of 22

Our opportunity

Credit unions – A heritage asset

Credit unions are wholly “creatures” of the provincial government. Back in the 1940s, some foresighted legislators understood that we would need to finance our community and economic growth as a province. They understood that we would be well-served if that growth were financed locally and the proceeds of those efforts stayed local to be reinvested yet again.

As co-operatives, our capital is permanent. It cannot leave the province. This is a fundamental difference from banks. Our capital deployment is democratically overseen by community electors who come from a broad range of backgrounds ensuring the diversity of our communities is reflected in the long term. At $60 billion collectively, credit unions are one of the key heritage assets of this province.

Credit unions have played a key role in building the province we have today, and will play a key role in developing the province for the future. Young people are attracted to our business model and values, and we are healthy, vital and innovative leaders in our communities.

Helping communities thrive and prosper by redefining wealth

Vancity is committed to helping communities thrive and prosper by using financial tools in innovative ways that make society better for more people (inclusive), for better outcomes (well-being), and for greater sustainability (environmental outcomes). This is the essence of what our business model, member-led innovation, is intended to do. Since November 2008 when the Board approved a new vision for redefining wealth, we have been working hard to leverage our unique strengths as a financial co-operative to build healthy communities.

Much of our transformation journey has focused on embedding our values and guiding principles in everything we do. More recently, our external focus has expanded including more dialogue with the credit union system as well as more engagement with stakeholders and community partners in service of meeting the needs of the real economy and advancing the values-based banking movement. As a result, our leadership role in the system and beyond is growing.

From scarcity to abundance

We see momentum building within the organization and in the community as well as internationally. “ Markets are beginning to give way to networks, ownership is becoming less important than access, the pursuit of self-interest is being tempered by the pull of collaborative interests, and the traditional dream of rags to riches is being supplanted by a new dream of a sustainable quality of life.”13

We are going in the right direction, leaning into community to understand the needs of the real economy and focusing on accelerating impact. That said, we are facing a highly competitive, regulated market and do not expect the current low growth trend to abate any time soon. Are we strong enough to carry on? The answer is yes, but the underlying structural shifts we are seeing require that we begin asking a bigger question. What will our role as facilitators of community development look like in ten years? As emerging technologies change the social fabric of society, how will we leverage the strengths of our financial co-operative in service of our vision?

13Jeremy Rifkin, The Zero Marginal Cost Society, 2014, p.19.

22 of 22

For some, this may seem like a time to pull back but we believe this is a time for us to continue pressing forward by investing in our business model. We are making progress and it is working but we need to carve out more time to think more boldly. We have the talent we need and we have a growing membership that believes in what we are doing.

Rather than focusing on our constraints, we want to focus on the opportunities we see to accelerate impact. The collaborative nature of our financial co-operative and the willingness of our members to share their ideas and experiences offers an inexhaustible supply of opportunities to innovate for impact. Rather than trying to do many things, we want to build the discipline and agility we need to leverage our resources to achieve the greatest impact. To that end, we have prepared a plan that is focused and connected to what we have learned about the needs of the real economy while also creating space to consider an emerging future where the role of banking and the current financial economic system may look very different.

Make Good Money (TM) and Good Money (TM) are trademarks of Vancouver City Savings Credit Union.