third quarter 2011 and the years to come - vestas | home/media/vestas/investor/investor...

TRANSCRIPT

Third quarter 2011 and the years to come9 November 2011 │ Vestas │ Aarhus │ Denmark

Agenda

Third quarter 20112

1. Introduction

2. Nine months 2011

3. Guidance 2011

4. Vestas as of today

5. Challenging 2012 and 2013

6. Financial priorities and goals

7. Q & A

Mr Engel

Mr Nørremark

Mr Nørremark

Mr Engel

Mr Engel

Mr Engel

Mr Engel and Mr Nørremark

Third quarter 20113

This presentation contains forward-looking statements concerning Vestas' financial condition, results ofoperations and business. All statements other than statements of historical fact are, or may be deemed to be,forward-looking statements. Forward-looking statements are statements of future expectations that are basedon management’s current expectations and assumptions and involve known and unknown risks and uncertaintiesthat could cause actual results, performance or events to differ materially from those expressed or implied inthese statements.

Forward-looking statements include, among other things, statements concerning Vestas' potential exposure tomarket risks and statements expressing management’s expectations, beliefs, estimates, forecasts, projectionsand assumptions. There are a number of factors that could affect Vestas' future operations and could causeVestas' results to differ materially from those expressed in the forward-looking statements included in thispresentation, including (without limitation): (a) changes in demand for Vestas' products; (b) currency and interestrate fluctuations; (c) loss of market share and industry competition; (d) environmental and physical risks; (e)legislative, fiscal and regulatory developments, including changes in tax or accounting policies; (f) economic andfinancial market conditions in various countries and regions; (g) political risks, including the risks of expropriationand renegotiation of the terms of contracts with governmental entities, and delays or advancements in theapproval of projects; (h) ability to enforce patents; (i) product development risks; (j) cost of commodities; (k)customer credit risks; and (l) supply of components.

All forward-looking statements contained in this presentation are expressly qualified by the cautionarystatements contained or referenced to in this statement. Undue reliance should not be placed on forward-lookingstatements. Additional factors that may affect future results are contained in Vestas' annual report for the yearended 31 December 2010 (available at www.vestas.com/investor) and these factors also should be considered.Each forward-looking statement speaks only as of the date of this presentation. Vestas does not undertake anyobligation to publicly update or revise any forward-looking statement as a result of new information or futureevents others than required by Danish law. In light of these risks, results could differ materially from those stated,implied or inferred from the forward-looking statements contained in this presentation.

Disclaimer and cautionary statement

Introduction

Third quarter 20115

It no longer makes sense to talk about revenues of EUR 15bn

four years from now.

Triple15: Cancelled.

Third quarter 20116

This is aboutimproving profit andsecuring cash flow.

Major changes in major markets

Third quarter 20117

Two years ago Today

North AmericaNo PTC extension expected.

No Federal Renewable Energy Standard.

EuropeSovereign crises in Europe.

AsiaIntense competition.

Third quarter 20118

New opportunitiesin new markets.

Third quarter 20119

Wind Power becomes more and more

competitive. Day-by-Day!

Third quarter 201110

Our Vision:Wind, Oil and Gas.

INTACT!

Third quarter 201111

2012 and 2013:

Challenging years due to macro economic outlook.

Third quarter 201112

Our Mission:Failure is not an option.

INTACT!

Third quarter 201113

Our high ambitionsare not cancelled.

International Energy AgencyAs of this morning, 9 November 2011

‘Delaying action is a false economy:For every $1 of investment avoided in the power sector before 2020 an additional $4.3 would need to be spent after 2020 to compensate for the increased emissions.’

Source: IEA, World Energy Outlook 2011

Third quarter 201114

Nine months 2011

Third quarter 2011

Third quarter 201116

Activity level increased.

Margins reflect mix and volume.

Strong operating cash flow performance.

387

588

1,456

634

1,4171,525

Q1 Q2 Q3 Q1 Q2 Q3

2010 2011

Activity at VestasOur main cash driver

ShipmentsMW

Q3 2011 vs. Q2 2011:Shipments up 8%.

Q3 2011 vs. Q3 2010:Shipments up 5%.

9M 2011 vs. 9M 2010:Shipments up 47%.

Third quarter 201117

Q3 2011 vs. Q2 2011:Deliveries up 13%.

Q3 2011 vs. Q3 2010:Deliveries down 25%.

9M 2011 vs. 9M 2010:Deliveries down 1%.

Deliveries to customers

Third quarter 201118

The main revenue driver

758839

1,688

864

1,127

1,270

Q1 Q2 Q3 Q1 Q2 Q3

2010 2011

DeliveriesMW

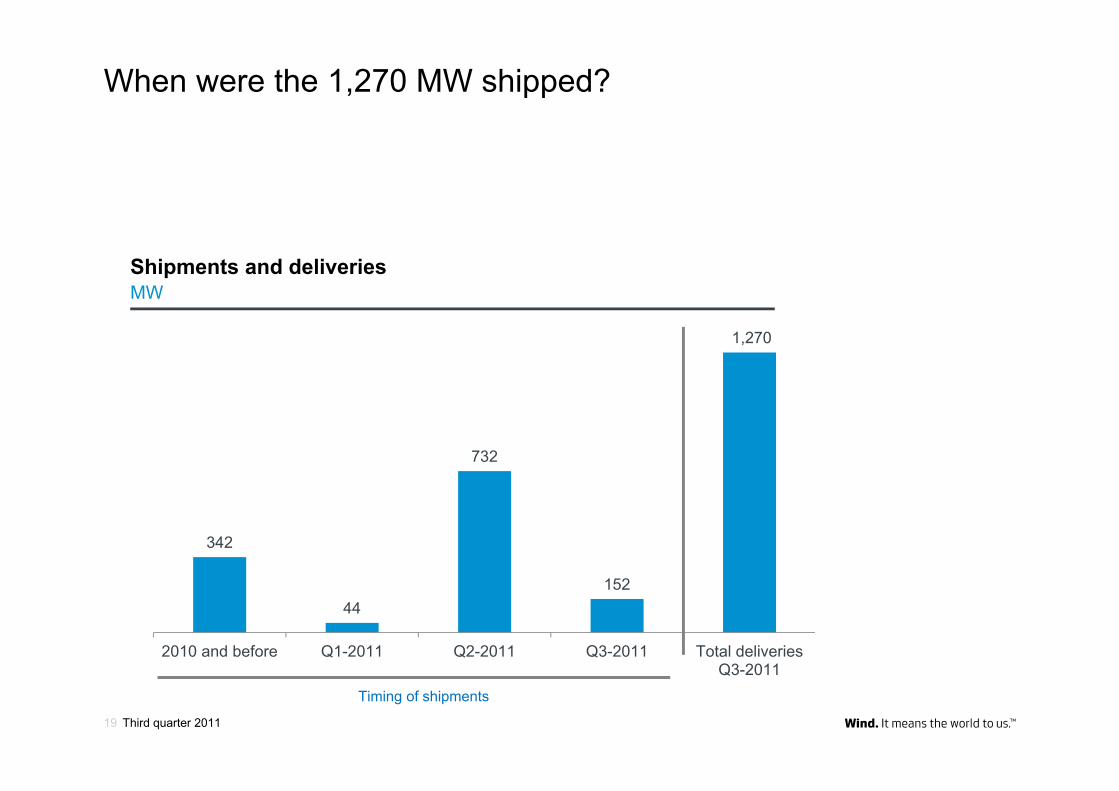

When were the 1,270 MW shipped?

Shipments and deliveriesMW

342

44

732

152

1,270

2010 and before Q1-2011 Q2-2011 Q3-2011 Total deliveriesQ3-2011

Timing of shipments

Third quarter 201119

Profit and loss account versus cash flowMajor fluctuations in earnings Q-on-Q

mEUR Q32011

Q22011

Change

Revenue 1,337 1,401 (5)%

Cost of sales (1,227) (1,153) 6%

Gross profit 110 248 (56)%

Fixed costs *) (202) (171) 18%

Operating profit/(loss) (92) 77 -

Profit/(loss) for the period (60) 55 -

Gross margin 8.2% 17.7% (9.5) pts.

EBITDA margin 0.1% 10.7% (10.6) pts.

EBIT margin (6.9)% 5.5% -

*) Sum of research and development costs, selling anddistribution expenses and administrative expenses.

Gross margin down due to mix of projectsand lower volume.

Cost of sales and fixed costs increased by depreciation and amortisation.

mEUR Q32011

Q22011 Change

Operating cash flow 407 126 223%

CF from investments (131) (189) (31)%

Free cash flow 276 (63) -

Third quarter 201120

Third quarter 201121

Every contract has its own characteristics.

Third quarter 201122

1. Scope – type of contract.2. Uniqueness of offering.3. Value of revenue.4. Scale.5. OPEX/CAPEX allocation.6. Design lifetime.7. Cost differentiation.8. Risk allocation.9. Early generation sharing.10. Relationship efficiency.

Quarterly profit & loss fluctuations driven by mix of contracts

Distribution of margins+200 projects a year

Pricing and risk variablesNot exhaustive

258

394

357

719

656

0

200

400

600

800

1,000

1,200

1,400

Q2-2011 Q3-2011

Turnkey/EPC Supply-and-installation Supply-only

14

Variations in revenue recognition between contract types

Third quarter 201123

However, risk element in each contract is the primary margin explanatory variable

Delivery split on contractsMW

From 1% turnkey/EPC in Q2 to 20% in Q3.

Turnkey projects generate higher margins when shipped and lower margins when delivered.

Transfer of risk.

Transfer of risk.

Percentage of completion.

Revenue: 80Cost: 55Profit 25Profit (%) 31

Project profitability

Third quarter 201124

Illustrative example

• Nacelle• Blades• Tower• Installation• Transport

Supply & Installation

• Foundations• Roads• Civil works• Cranes• Installation• Transport

• Nacelle• Blades• Tower

Revenue: 100Cost: 70Profit 30Profit (%) 30

Revenue: 50Cost: 45Profit 5Profit (%) 10

Revenue: 130Cost: 100Profit 30Profit (%) 23

EPC Contracts / Turnkey

In principle, cash flow is identical in either case.

Fixed cost base

Third quarter 201125

Depreciation and amortisation explain most of the increase from Q2-2011 to Q3-2011

140

192178

197

169 171

202

Q1-2010 Q2-2010 Q3-2010 Q4-2010 Q1-2011 Q2-2011 Q3-2011

Fixed costmEUR

Net working capitalMake-to-order pays off

mEUR 9M2011

Q2 2011 Change

9M2010

Inventories 2,608 2,545 2% 4,000

Trade receivables 591 629 (6)% 791

Construction contracts in progress 188 113 66% 172

Other receivables 350 379 (8)% 352

Prepayments from customers (1,794) (1,452) 24% (3,097)

Trade payables (1,276) (1,090) 17% (1,258)

Other current liabilities (267) (252) 6% (264)

Net working capital 400 872 (54)% 696

As per cent of revenue 6% 14% 8 %-pts. 10%

Stable inventories and increased prepayments reflect that make-to-order is paying off.

Net working capital ratio to be further improved by reducing inventories and by higher order intake.

Third quarter 201126

Net working capital items – deeper dive

Third quarter 201127

Inventories consisting of:1. Contract-related inventories.2. Components.

Prepayments consisting of:1. Milestone payments.2. Down payments and prepayments.

Balance sheet

Assets (mEUR) Q32011

Q22011

Change Q32010

Change

Intangible assets 1,177 1,145 3% 966 22%

• Completed development projects 512 170 201% 144 256%

• Development projects in progress 257 568 (55)% 423 (39)%

Property, plant and equipment 1,816 1,755 3% 1,680 8%

Other non-current assets 358 290 23% 336 7%

Current assets 4,099 3,954 4% 5,596 (27%)

Total assets 7,450 7,144 4% 8,578 (13%)

Equity and liabilities (mEUR) Q32011

Q22011

Change Q32010

Change

Equity 2,618 2,707 (3%) 2,587 1%

Non-current liabilities 1,237 1,396 (11%) 995 24%

Current liabilities 3,595 3,041 18% 4,996 (28%)

Total equity and liabilities 7,450 7,144 4% 8,578 (13%)

Increase in completed development projects and decrease in development projects in progress primarily due to V112 being put into serial production.

Third quarter 201128

Net debt

Third quarter 201129

To be further reduced

404

896

727

579

1,000 1,071

834

Q1 Q2 Q3 Q4 Q1 Q2 Q3

2010 2011

Net debtmEUR

Net debt reduced by 22% from Q2-2011 to Q3-2011

Warranty provisions and quality

6.6%

4.5%

5.7%

2.8%2.4%

2007 2008 2009 2010 9M 2011

Warranty provisionPer cent of revenue

0

1

2

3

4

5

6

7

Lost Production FactorPer cent

Failure is not an option Quality / Lost Production

Factor

Third quarter 201130

Cash flow statementMain lines

mEUR Q32011

Q22011

Q32010

9M2011

9M2010

Profit for the period (60) 55 187 (90) 5

Adjustment for non-cash transactions 15 69 263 161 141

Corporation tax paid (11) (25) (23) (43) (79)

Interest received and paid (net) (9) (11) (24) (34) (33)Cash flow from operating activities before change in working capital (65) 88 403 (6) 34

Change in working capital 472 38 (41) 272 (379)

Cash flow from operating activities 407 126 362 266 (345)

Cash flow from investing activities (131) (189) (182) (484) (533)

Free cash flow 276 (63) 180 (218) (878)

Cash flow from financing activities (158) 63 (225) 188 543

Free cash flow improvement of EUR 660m from 9M 2010 to 9M 2011.

Third quarter 201131

Shipments main determinant of cash flow

Third quarter 201132

Cash flow from operationsmEUR

ShipmentsMW

‐400

‐200

0

200

400

600

800

‐

500

1,000

1,500

2,000

2,500

3,000

Shipments (quarterly) MW Cash flow from Operations

Key takeaways

Shipments generate cash flow.Deliveries generate revenue.

Activity in Vestas is reflected in ’Inventories’ and ‘Prepayments’ rather than in Profit & Loss account.

Projects stay longer in ‘Order backlog’ and on ‘Inventories’.

Third quarter 201133

Guidance 2011

Third quarter 201135

Why did we adjust our guidance?

Third quarter 201136

The reason to adjust guidance: Our new generator plant in Travemünde, Germany

Generators are being produced every day

– but not in the expected quantities.

The reason to adjust guidance: Our new generator plant Delivery interaction

Raw material & suppliers

Manufac-turing

Factory assembly & testing

Transport Installation Operation

Gear

Generator

Hydraulic

Electrical

Controls

Mechanical

Raw material

Raw material

Hydraulic systems

Electrical components

Electrical, electronically

Steel, cast, fasteners

Blades

Towers

Controls

Blades

Towers

Controls

Nacelle

Composite, paint

Steel

Electrical, electronically

Nacelle

Cranes

Lifting equipment

Manpower

Tools

Mechanical completion

Commis-sioning

Goods receipt

Schedule

Regular operation

Third quarter 201137

The reason to adjust guidance: Our new generator plant

Raw material & suppliers

Manufac-turing

Factory assembly & testing

Transport Installation Operation

Gear

Generator

Hydraulic

Electrical

Controls

Mechanical

Raw material

Raw material

Hydraulic systems

Electrical components

Electrical, electronically

Steel, cast, fasteners

Blades

Towers

Controls

Blades

Towers

Controls

Nacelle

Composite, paint

Steel

Electrical, electronically

Nacelle

Cranes

Lifting equipment

Manpower

Tools

Mechanical completion

Commis-sioning

Goods receipt

Schedule

Regular operation

Delivery interaction

Third quarter 201138

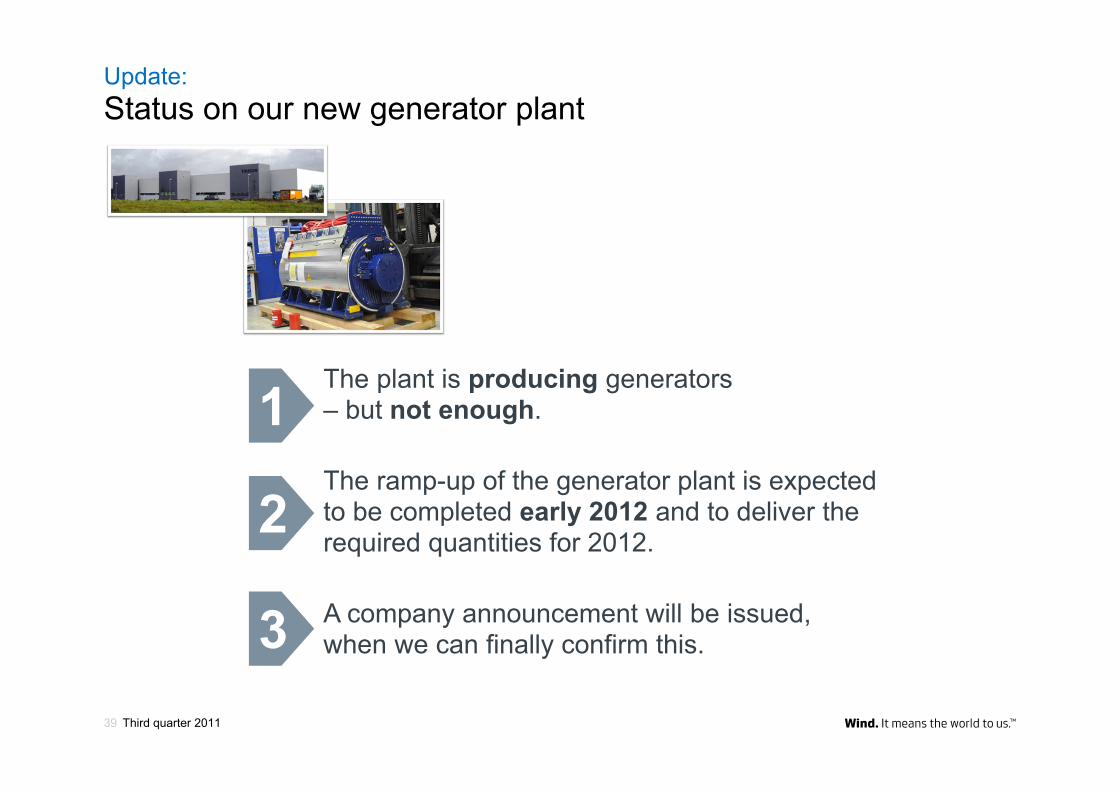

Update:Status on our new generator plant

Third quarter 201139

The plant is producing generators– but not enough.

The ramp-up of the generator plant is expected to be completed early 2012 and to deliver the required quantities for 2012.

A company announcement will be issued, when we can finally confirm this.

1

2

3

Guidance 2011

Order intake, firm and unconditional (MW) 7,000-8,000

Production and shipments (MW) ~5,500

Revenue (mEUR) ~6,400

- of which service revenue (mEUR) 700

EBIT margin (%) ~4

EBIT margin, service (%) 15

Financials, net (mEUR) (60)

Tax rate (%) 28

Investments (mEUR) 850

Free cash flow (mEUR) > 0

Warranty provisions (%) < 3

Industrial injuries (per one million working hours) ≤ 5

Customer loyalty (index) 72

Share of renewable energy (%) 40

Share of renewable electricity (%) 95

Quality level (Sigma) ≥ 5

EBIT margin in Q4 of ~13%.

Third quarter 201140

630 2,265 1,316 863

2,426

Q1 Q2 Q3 Oct Nov. - Dec.

Order intake of 7,000-8,000 MW in 2011

Third quarter 201141

Stable average selling price despite market sentiment

Order intake 2011MW

Mid-range

Average selling price of order intakePrice/MW

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

FY FY FY FY FY Q1 Q2 Q3 Q4 Q1 Q2 Q3

2005 2006 2007 2008 2009 2010 2011

Announced orders

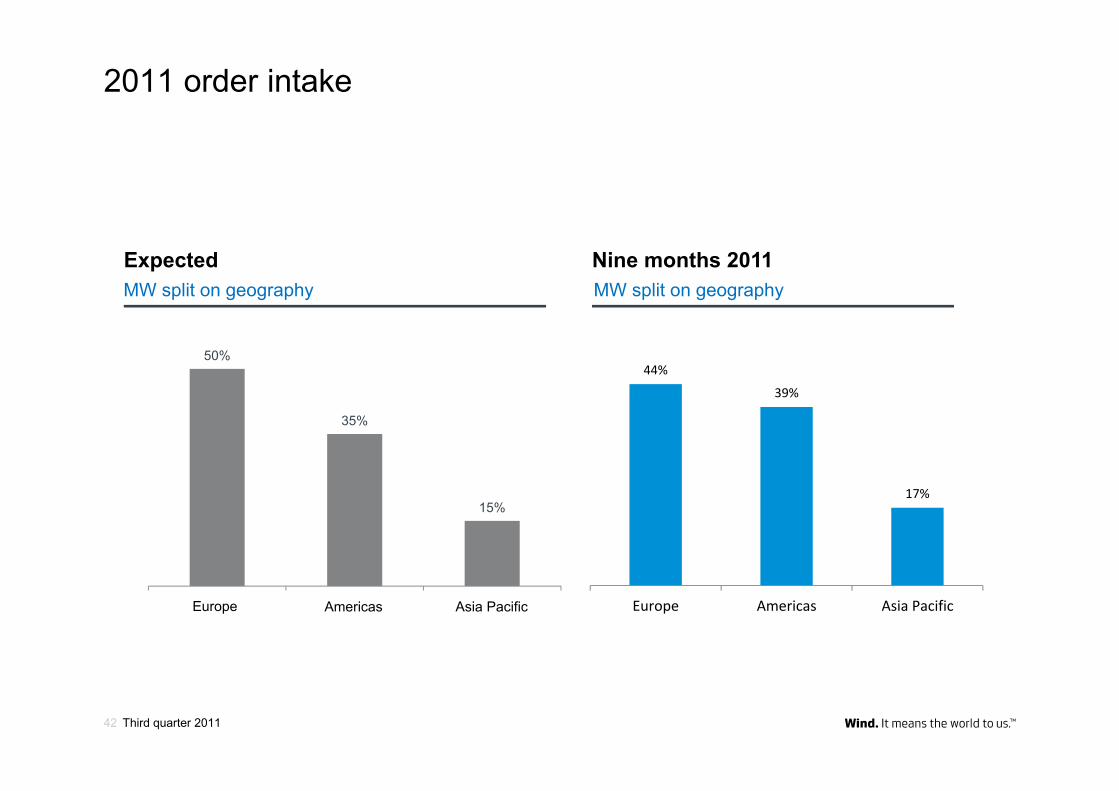

2011 order intake

ExpectedMW split on geography

Nine months 2011MW split on geography

44%

39%

17%

Europe Americas Asia Pacific

50%

35%

15%

Europe Americas Asia PacificEurope Americas Asia Pacific

Third quarter 201142

The back-end loaded 2011 means that recognition of revenue and EBIT relies on smooth project execution in Q4.

Please still remember!

Third quarter 201143

(1,000)

(800)

(600)

(400)

(200)

0

200

400

600

800

1,000

2007 2008 2009 2010 2011

Cash generationStrong working capital improvement

InvestmentsmEUR

Free cash flow

Cash flow from operationsmEUR

Third quarter 201144

Vestas as of today

Qualified

Third quarter 201146

Global presence.

In the region for the region.

Most versatile product platform.

Strong IPR giving freedom to operate.

Product roadmap matching future demand.

Global presence

Third quarter 201147

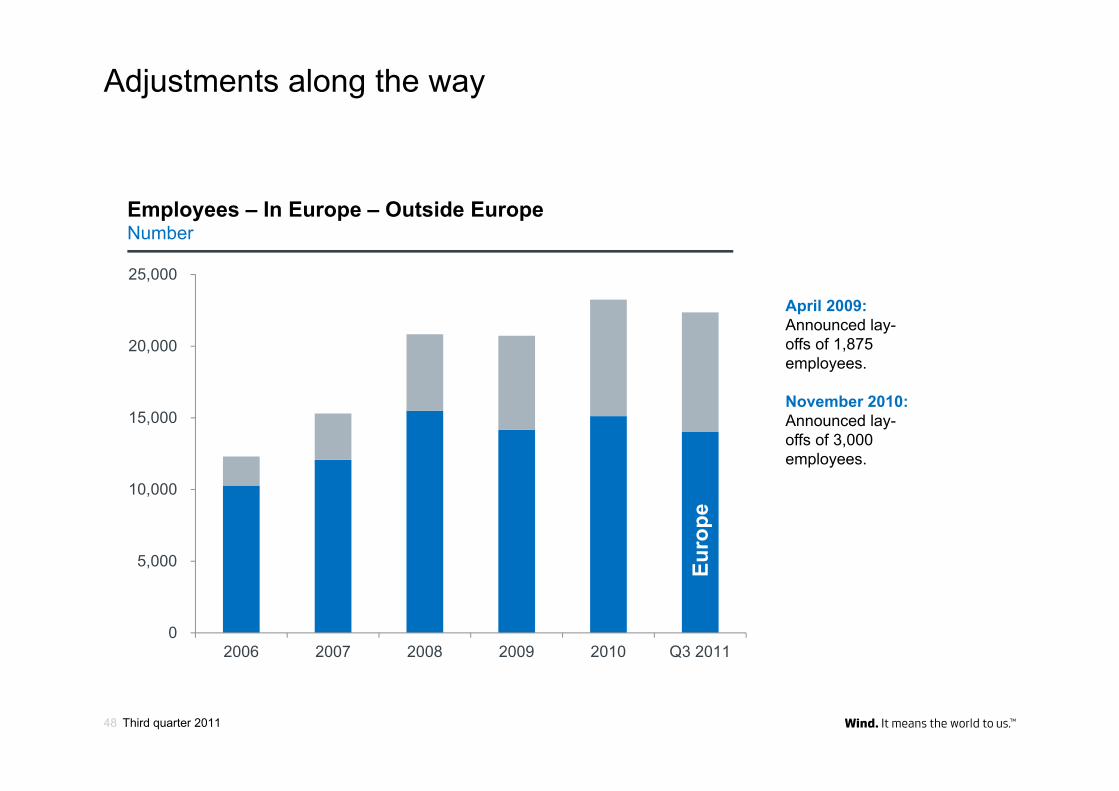

Adjustments along the way

Third quarter 201148

April 2009:Announced lay-offs of 1,875 employees.

November 2010:Announced lay-offs of 3,000 employees.

0

5,000

10,000

15,000

20,000

25,000

2006 2007 2008 2009 2010 Q3 2011

Employees – In Europe – Outside EuropeNumber

Euro

pe

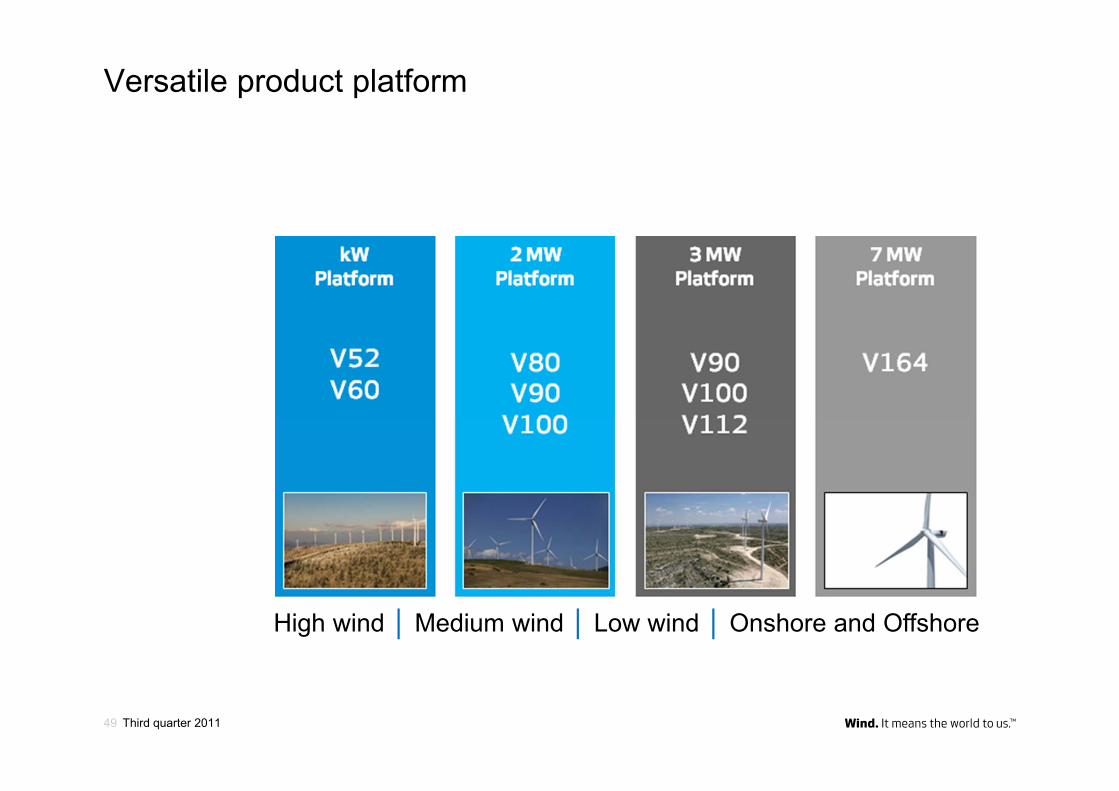

Versatile product platform

Third quarter 2011

High wind │ Medium wind │ Low wind │ Onshore and Offshore

49

Service business still more important

Service revenuemEUR per year

214

298

396

504

623

700

2006 2007 2008 2009 2010 2011E

Strategic agreement with Caterpillar.

Third quarter 201150

Recent service offerings

Third quarter 201151

SiteHunt®

SiteDesign®

Electrical PreDesign

Power Plant Controller

VestasOnline® Business (SCADA)version 3.9 – Enhanced data.

Installed capacity giving sizable base for service business

Third quarter 201152

10 largest manufacturers in 2010Accumulated installed capacity (MW)

Source: Vestas

47,375

Enlarging the scope of our business

Third quarter 201153

Constantly improving quality and efficiency

Third quarter 201154

+40 per cent more per line in three years.

SafetyInjuries per one million working hours

Patent applicationsNumber

EfficiencyBlades, 44 metres

LPF target 2012: < 2

Lost Production FactorPer cent

25.3

20.8

15.6

8.15.0 3.3

2006 2007 2008 2009 2010 2011 -9M

1550

100

153 165

227

2005 2006 2007 2008 2009 2010

What customers demandReliable technology.► Track record of installed capacity of design platforms offered.► Turbine development plans.

Relevant capability.► Worldwide manufacturing capacity.► Existing sub-supply chain management.► Past experiences in up-scaling capacity.

Sufficient organisational strength.► Offshore wind experience.► Relevant manpower in place.► Flexibility in scope of supply.

Sufficient financial strength.Convincing track record.► Onshore & offshore project references.

Third quarter 201155

Competition remains fierce.

Third quarter 201156

Challenging 2012 and 2013

We are – right now – preparingVestas for a situation

without a PTC in 2013.

Third quarter 201158

Third quarter 201159

To be here in the long run– we cannot fail in the short run.

We are not adjusting– we are changing.

Third quarter 201160

COSTS INVESTMENTS REVENUE

Third quarter 201161

Higher degree of capacity utilisation.► Use all of our endeavours to create valuable order intake.

► If orders are lacking, capacity will be reduced.

More efficient use of resources.► Leverage successful implementation of shared services.

► Sharper focus on the return on our efforts.► Improved scalability.

Third quarter 201162

New organisational set-up.► Taking even more care of our customers.

► New organisational and management structure► to be initiated on 8 February 2012.

Third quarter 201163

Investments will be reduced and directed towards intangible assets.

► Sub-suppliers/partners to carry more investments.► Investing in new service offerings to our customers.

► Supply chain, production and quality testing facilities are in place.

Third quarter 201164

1

40

8

28

V112 – an important part of our future

Third quarter 201165

Adjacent technology includes:

New generator technology GridStreamer™ technology Test and verification facilities and equipment

Adjacent technologies developed in connection with one new WTG platform will be used across old and future platforms.

Development cost

Production capacity conversion and ramp-up

V100-2.6 MW2 MW GridStreamer™

12

2 MW MK7 (V100-1.8)

16

V112

111

8

32

Adjacent technologydevelopment

Index figures

Incremental innovationNew platform

0

3,000

6,000

9,000

12,000

15,000

18,000 2 MW PlatformAccumulated installed base (MW)

Third quarter 201166

Leveraging a new platform2004

As a further development, the V90-1.8 MW combines a 90 metre-rotor with the well-tested V80 nacelle.

2000

First V80-2.0 MW wind turbine installed.

2005

Installed in challenging conditions both onshore and offshore.

MK4 MK6 MK7

2008

V90-1.8 MW 60 Hz (US) version introduced.

2009

The V100 is introduced.

2010

2 MW GridStreamer™. Adapt to new grid requirements

MK8MK5MK3MK2

1995

V63-1.5 MW and V66-1.65, first multi-MW was the basis for the 2 MW platform.

Track Record• More than 8,100 V80s/V90s/V100s are

producing power in 21 countries around the world.

• Almost 800 V63/V66 have been installed worldwide.

Upgrades focus on:• Safety• Quality• Reliability, Lost Production Factor• Accessing new market requirements• Maintaining competitiveness

Cost-out on products, without loss of quality.

Third quarter 201167

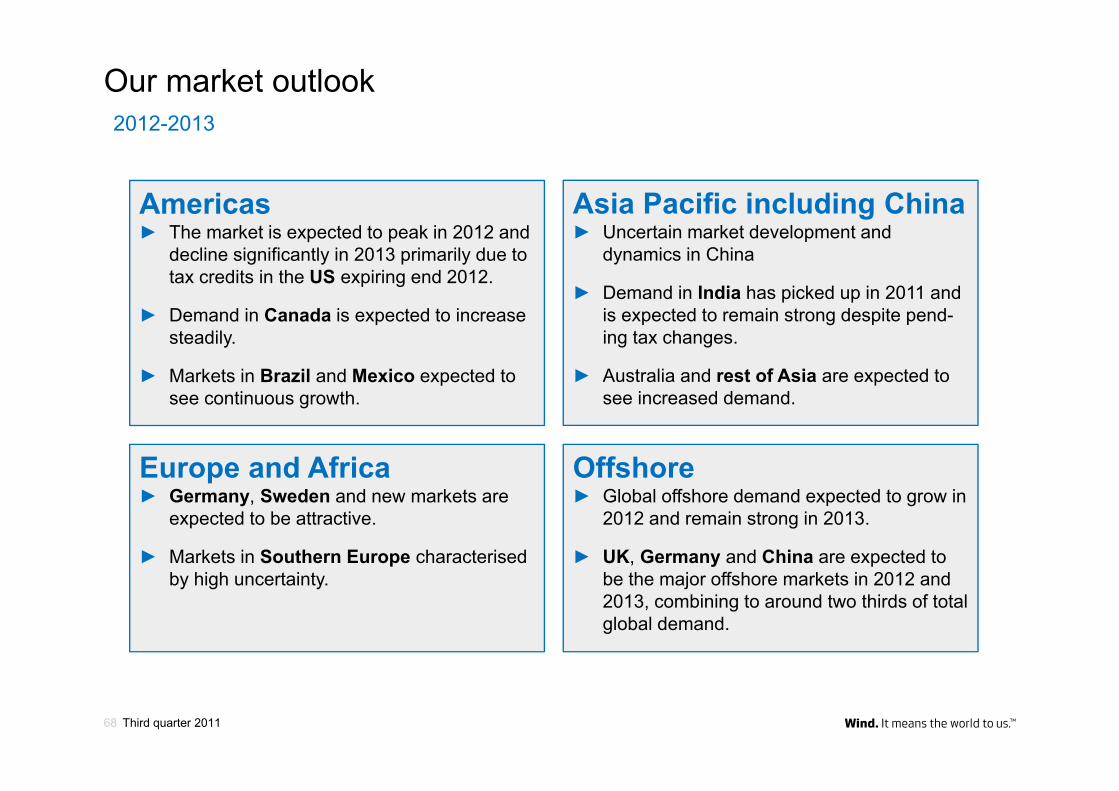

Our market outlook2012-2013

Third quarter 201168

Europe and Africa► Germany, Sweden and new markets are

expected to be attractive.

► Markets in Southern Europe characterised by high uncertainty.

Americas► The market is expected to peak in 2012 and

decline significantly in 2013 primarily due to tax credits in the US expiring end 2012.

► Demand in Canada is expected to increase steadily.

► Markets in Brazil and Mexico expected to see continuous growth.

Asia Pacific including China► Uncertain market development and

dynamics in China

► Demand in India has picked up in 2011 and is expected to remain strong despite pend-ing tax changes.

► Australia and rest of Asia are expected to see increased demand.

Offshore► Global offshore demand expected to grow in

2012 and remain strong in 2013.

► UK, Germany and China are expected to be the major offshore markets in 2012 and 2013, combining to around two thirds of total global demand.

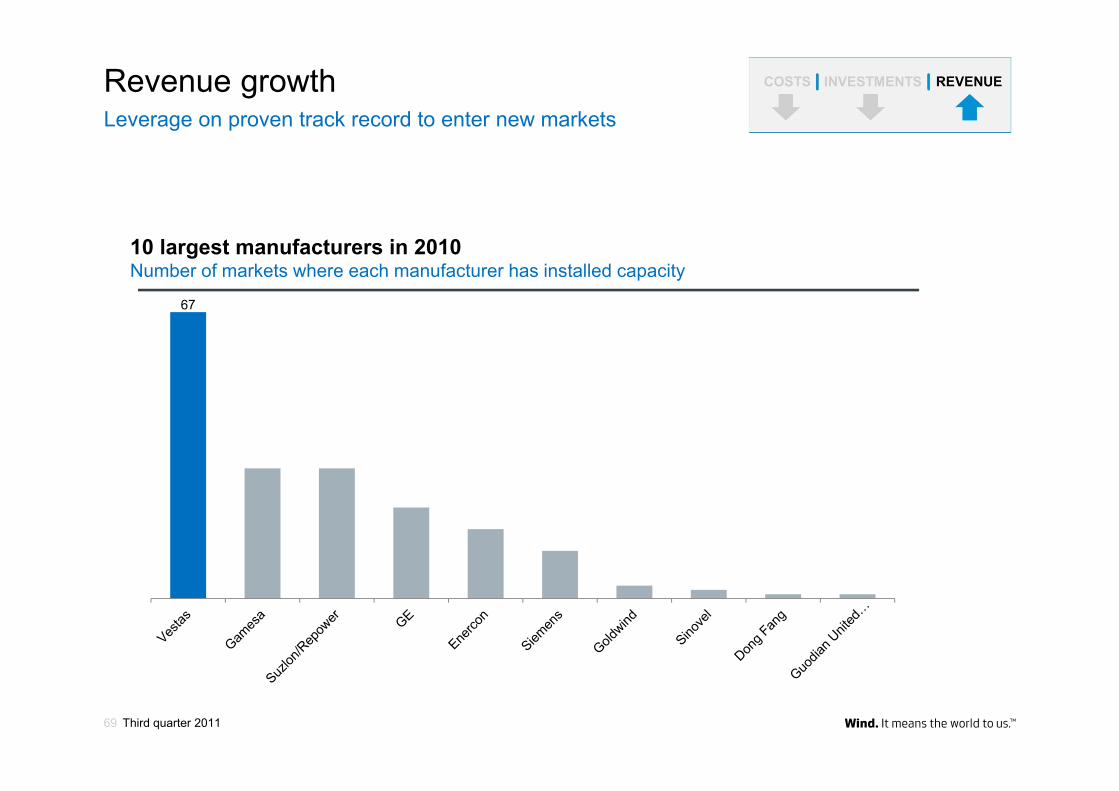

Revenue growthLeverage on proven track record to enter new markets

67

10 largest manufacturers in 2010Number of markets where each manufacturer has installed capacity

Third quarter 201169

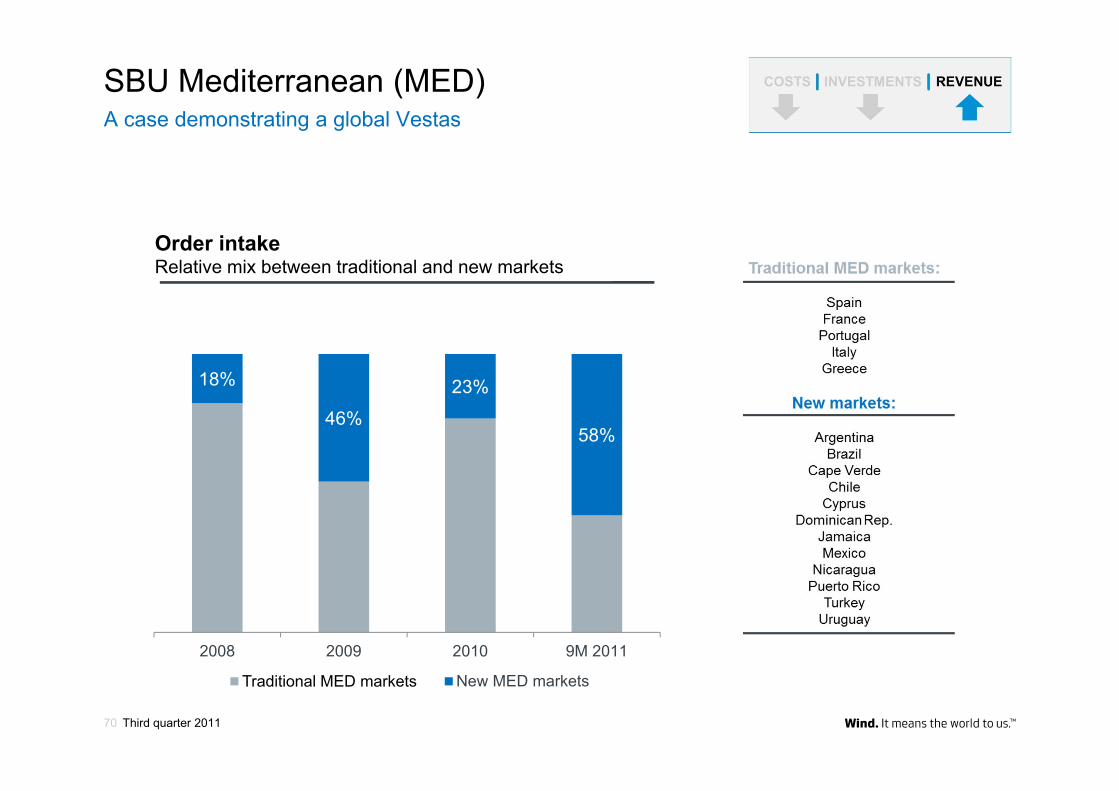

A case demonstrating a global Vestas SBU Mediterranean (MED)

18%

46%

23%

58%

2008 2009 2010 9M 2011

Traditionel MED markets New MED markets

Order intakeRelative mix between traditional and new markets

Traditional MED markets

Third quarter 201170

New andexistingTurbines

New Services

New Upgrades

New Offerings

…while constantly lowering the Cost of Energy.

Revenue sources to expand

Third quarter 201171

Developingcustomer landscape.

Pension funds.CaCoCos.Carbon Conscious Companies.

Third quarter 201172

Inclusiveness.

Vestas will be sustainable in every aspect of the way we do business.

Third quarter 201173

Financial priorities and goals

For the benefit of primarilyFOUR STAKEHOLDERS:

1. CUSTOMERS │ 2. SHAREHOLDERS │ 3. EMPLOYEES │ 4. POLITICIANS

Third quarter 201175

Guidance for 2012New guidance principles to be announced on 8 February 2012We will also evaluate our communication principles

Reducing costs by at leastEUR 150m end 2012.

Investments of EUR 650m.Tangibles: EUR 200m │ Intangibles: EUR 450m

Positive free cash flow.

Third quarter 201176

Mid-term guidance

Vestas expects to gain market share and to deliver a high single-digit

EBIT margin with a normalised US market.

Third quarter 201177

Investing in offshore

Third quarter 201178

The V164 will be put into production in 2015 when the required orders

have been received.

Vestas and the USA

Third quarter 201179

Preparing for no PTC in the USA in 2013

2012 2013

Vestas TOTAL Cost reduction of at least EUR 150m

Huge impact for Vestas

Vestas USA End 2012: Decision ?

Vestas expects to enter 2012 with the largest order backlog ever.

Third quarter 201180

This is about improving profit and securing cash flow.

Third quarter 201181

Financial Calendar

Third quarter 2011

1st Quarter 2012

2 May 2012

New York CityUSA

4th Quarter 2011

8 February 2012

LondonUnited Kingdom

82

Q & A

Copyright NoticeThe documents are created by Vestas Wind Systems A/S and contain copyrighted material, trademarks, and other proprietary information. All rights reserved. No part of the documents may be reproduced or copied in any form or by anymeans - such as graphic, electronic, or mechanical, including photocopying, taping, or information storage and retrieval systems without the prior written permission of Vestas Wind Systems A/S. The use of these documents by you, oranyone else authorized by you, is prohibited unless specifically permitted by Vestas Wind Systems A/S. You may not alter or remove any trademark, copyright or other notice from the documents. The documents are provided “as is” andVestas Wind Systems A/S shall not have any responsibility or liability whatsoever for the results of use of the documents by you.

In case we have unintentionally violated copyrighted material, we want to be informed immediately in order to straighten things out and thus to honour any obligatory fees.

Third quarter 201184