the world banwifc1m.i.g.a. office memorandum · balance of the gef funds would then be released on...

TRANSCRIPT

THE WORLD BANWIFC1M.I.G.A.

OFFICE MEMORANDUM DATE: August 6, 1997

TO: Mohamed T. El-Ashry, Chief Executive Officer, GEF

Rc- FROM: Robin Broadfield, Acting Chief, ENVGC

EXTENSION: 34355

SUBJECT: Renewable Energy and Energy Efficiency Fund (REEF) Final Council ReviewICEO Endorsement

1. Please find attached two copies of the draft GEF document for this project for the Secretariat's clearance to circulate to the Council and seek your endorsement.

2. As requested by the Council, the IFC's investments in the REEF Equity Fund and Debt Facility have been approved by the IFC Board prior to the submission of this document to the GEF. The details of these investments, which were approved by the IFC Board on June 25th, 1997, are outlined in paragraph 8 of the document.

3. As noted in paragraph 9, we propose a slight modification to the formula for release of the GEF funds, relative to theproposal previously endorsed by the Council. The intent of this modification is to accelerate the Fund's start-up. In place of the original proposal that the first $20 million of GEF resources be released when the REEF mobilizes $100 million in equity andlor debt resources, we now propose that the first $10 million of GEF funds be released once a target of $50 million in the Equity Fund has been met. The balance of the GEF funds would then be released on a prorata basis as we progress towards the original non-GEF capital target of $200 million. This change does not materially alter the project's design, but we think will enhance it's prospects of success.

4. We look forward to receiving word from the Secretariat that we can send the 75 copies for dispatch to the council. *

Attachments +.

cc. MessersMmes Duda, Rittner (GEFSEC); Boorstin, Riddle, Rubino, Younger, Nyirjesy (IFC); Vidaeus (olr), Feinstein (olr), Nikolov (ENVGC)

GLOBAL ENVIRONMENT

FACILITY

RENEWABLE ENERGY .4ND ENERGY EFFICIENCY FUND (REEF)

Project Document ~ e ~ t e m b e r 1997

International Finance Corporation Technical and Environment Department

Environment Division Environmental Projects Unit

INTERNATIONAL FINANCE CORPORATION GLOBAL ENVIRONMENT FACILITY

RENEWABLE EPERGY AND ENERGY EFFICIENCY FUND W E F )

PROJECT DOCUMENT T-4BTa3? OF CONTENTS

Grant Summary

I. Executive Summary

II. Project Background

III. Project Objectives and Rationale for GEF Funciing . -

IV. Project Description

V. Uses of the GEF Support

VI. Sustainabiliry and Pankipation . -.

VII. Lessons Learned

WII. Project Risks

APPENDICES

A. Incremental Cost Analysis B. Summary oiDisbunement Amngements C. REEF Impiementation Timetable .

INTERNATIONAL FINANCE CORPORATION GLOBAL ENVIRONME-YT FACILITY

RENEWABLE ENERGY AND ENERGY EFFICIENCY FUND (REEF)

Project Title:

G W T SUMMARY

Renewable Ene rg and E n e r g Efficiency Fund (REEF)

GEF Focal Area: climate

Eligible Recipient Countries: All GEF-EligZ~le Countiies

GEF Financing: USSlO to USS30 million

Other Financing: USSSO to USS210 million from investors in REEF, including IFC USS100 to USS600 million for projects fiom other sources

Beneficiaries:

Terms:

private sector renewable energy and e n e r a efficiency project sponsors, including independent power producers, energy services companies, energy end users. and specialized financial intermediaries.

Grant and non--pnt(loan, guarantee, equirv) financing for sub- projects; p u t s for project management and administration.

Executing Agency: International Finance Corporation P C )

Estimated Starting Date: January1998 -

Project Duration: Ten to thirteen years

1. THE Renewable Energy and Energy Efficiency Fund (REEF) will invest in private sector projects in the renewable energy (RE) and energy efficiency (EE) sectors in emerging markets. REEF will consist of an Equity Fund targeting USS110 million in capitalization and a Debt Facility with USSlOO million in loan commitments. REEF is expected to invest its resources over a 5-year period and to liquidate the portfolio within 10 to 13 years of its first closing date. Investors in the Equity Fund will include International Finance Corporation (IFC) and various institutional and srrategc investors targeting the REEE sectors on the basis of their commercial merits. positive impact on the zlobal environment and other benefits. The Debt Faciiity will be funded by E C and international - commercial banks.

- I

2. REEF will be managed by a Fund Management Company (FMC) formed by a consortium of Energy Investors Funds (EIF), Environmental Enterprises Assistance Fund (EEAF), E & Co and a major Europem international bank.

- 2. The Global Environiient Faciiiry (GEF) will provide up to USS30 million in grant support to help broaden REEF'S scope of investment, enabling it to consider importvlt REEE market se-ments '

and catalytic projects that, absent such supporc, are less like!y to receive significant anention from a commercial invesunent fund, due to their small size, complexiry, risk profiies and other factors that prevent them ifom generating an acceptable risk-adjusted rare of rerurn. The GEF support will seek to ~5nanct the incremental cost andlor mitigate the incremental risk of invesnng in such projects.

4. The USS3O million GEF - m t is expected to leverage invesunents of USS210 million in the RUZF Fund and Debt Facility, which in rum will sliuport projects with total costs-of USS300-800 million, yielding a leverage ratio on GEF funds ranging from twelve to one to up to menty-seven to one (10:l to t7:l). This esrinate does not take into account the strong potential for a multipiier effect from expansion or repiication of successful prqects.

5. The GEF funds will be used: (i) to provide direct co-financing to select REEF investee projects in the form oi,mt, debt parantee, andior equity financing (up to USS2S million), (ii) to support the FMC's incremental management costs of idenrifiing, analyzing and investing in a portfolio of REEE projects (up to USS5-6 million during - the 5-year investment period pursuant to annual budgets), and (iii) to cover IFC's eligible costs for co-administeriig the GEE suppon as GEF Executing Agency (up to US51 million).

6. The GEF support will be administered by a four-member IFC-REEF-GEF Committee (IRGC) composed of one representative each from IFC's Technical and Environment Department, IFC's Power Department, the World Bank's Global Environment Division and a member selected from outside the World Bank Group and GEF. The IRGC will approve the terms of each GEF co-financing transaction on the basis of investment proposals developed by the FMC in conjunction with REEF'S investments in the proposed projects. It will also consult with the GEF Secretariat when a new non-,mt financial instrument is used for the first time under the co-financing arrangement.

7. The use of the GEF funds is consistent with the GEF Operational Strategy and Operational Pro-puns in climate change. The projects and GEF co-financing instiuments selected wiil be consisrenfwith GEF Council policies resarding financing modalities and with specific investment guidelines to be adopted by the LRGC. REEF will also adhere to the Worid Bank Group Environmental Policies and Guidelines in all of its investment activities.

8. The GEF suppore for REEF was endorsed in principle by the GEF Council in .April 1996. The Council required that the IFC iilvestment in REEF be approved by IFC's Board of Directors prior to submission of a Project Document to Council members prior to endorsement by its CEO. The IFC Board approved the proposed JFC investments in the REEF Equity Fund and Debt Faciiity on June 25, 1997. E C wiil subscribe to an equity commitment of up to USS15 million of the Equity Fund's target USS110 million capitalization. IFC will also previde a USS20 million -4 loan and an USS80 million B loan u part of the Debt Faciliry's target USS 10C million capitalization. IFC's comrnitrnent to the Equity Fund will be limited to USS10 million unless at least one other investor exceeds that amount.

9. The original proposal endorsed by the GEF Council contempiated that the firsr USS20 million in GEF funds wouid be made avaiiable once REEF mobilizes USS 100 million in equity andlor debt capital fiom non-GEF sources. The remaining C'SS 10 million in potential GEF suppon wouid be provided on a prorated basis in relation to the next USS 100 million in non-GEF ~hnding mobilized. In order to ecsure the earliest possible s m - u p for REEF, IFC and the FMC are now targering a fust closing of at least CSSSO million for the Equity Fund, with the balance to be raised wirhm twelve months thereafier. The first closing .of the Debt Facility mayar may not be simultaneous with the Equity Fund's first closing. once the fund is established, it is genertlly easier ro raise additional . . capital. The availability of some GET funds at the b e g m n g of REEF'S operating life would ensure that all zspecn ofthe proposed investment s c a t e g can be launched kom the outset. Therefore, it is now proposed that the first USSIO million of G E F funding be made available once the Equity Fund's minimum first closing target of USS50 million is met. An additional US S10 million of GEF funding would be made available when USSI-00.million in non-GEF capital is mobilized with the remaining USSIO million in GEF funding to be provided on a prorated basis thereafter until the non-GEF capital mobiIizarion target of 'C'SS200 million is reached. Thus the project objective of raising CTSSlOO milIion to USS2lO million and the project's scope and overall design remain the same, but an intermediate step has been added to give REEF a better chance to reach the objective target size more quickly. GEF funds made available to REEF at each of thc above- described investment levels will be allocated to the uses of GEF funds listed in paragraph 5 on a pro rata basis (i.e., to co-financing, fund management and administration costs).

. 10. This project stems from IFC's feasibility smdy focusing on the RE and EE markets in developing counmes, which reviewed about 100 projects under development in 1995 with some US52 billion in total costs'. The study conilnned that there is gowing private investment activity in the target sectors in many developing countries and that a dedicated investment fund could achieve

'

competitive r e m s while helping to accelerate the flow of commercial financing.

11. The study was followed by the detailed strucmring of the proposed REEF Equity Fund and Debt Facility by IFC and the prospective management team. REEF is expected to pursue the following types of invesments:

kd-connected and "inside-the-fence" private power projects using uind, biornws, m a l l hydro, - eeothemal, soiar and other RE resources to sell power to eiectric utilities and other end users under b

power purcnase agreements;

private sector projecrs and companies supplying solar home systems, small cennal siations and other "distiibuted" RE applicatioris in off-grid communities;

energy service companies ("FSCOs") and end usen themselves undertaking EE investments in such areas as industry, buildings, public lighting, and district heating; and

ii~ select czses, local manufacrurers of REEE equipment and local financial inremediaries focusing on the REEE sectors.

. . i2. From a commercial perspective, advantages of-a RF, projec~s include tneir zero or low he1 costs and otherwise low operating costs and their smaller scale in relation to conventional e n e r g - . . projects, often providing for more rapid installation and replication. Qft-ma RF rechnoiogies offer higher quality energ at a! increasingly competitive cost in reiation to diesel generators, kerosene lanterns, batteries and other conventional energy sources. FF proiects typically use well-proven equipment and techniques and can offer attractive renuns to all panicipants if well strucrured.+All three sectors are in a relatively early stage of development, especially in emerging markets which is one of the principal reasons fir the establishment of E E F as a global, multi-sectoral fund. However, all three sectors have the potential for rapid commercial expansion in a wide range of countries throughout the developing world.

13. Achieving sustainable growth in the development and financing of RE and EE projects is a critical objective of the GEF Operational Strategy, since they offer direct alternatives to the combustion of fossil fuels, a major source of GHG emissions implicated in global warming phenomena. The expansion of power generation capacity through construction of fossil fuel plants remains the leading

' The srudy was funded by the governments of France. Germany, the Netherlands. Nonvay and the United States, and by IFC's Technical and Environment Depamnent and Power Deparrment.

solution to meeting energy needs in most developing countries, so that GHG emissions are expected to increzse significantly in the years ahead. The FCCC seeks to address this threat through broad-based internatidiial coopemion, notably through financial suppon from the GEF for GHG-mitigating projects . in eligible counmes.

14. In addition to their positive environmental impact, REEE projects can add value to underutilized local energy resources and unexploited potential for ene rz savings, help defer new investments in larger-scale centralized energy generation and distribution capaciry, diversify 2

country's energy profile and provide a hedge azainst currency and fuel price flucruations, improve productivity and social conditions by introducing or raising the aualiry of energy supply in off--grid cominunities, and encourage local entrepreneurial ,panicipation.

- /FE Market Profile

15. Grid-connected RE proiects constitute the largest and most advanced market se-ment targe~ed by REEF. Frivate developers have gained considerable experience in the design, Iinmcing and operation of RE projects. For example, in the United States alone, nevly 10,000 MW oiXE power plants are cmently on-line or under construc:ion (not including large hydro plants). Nonetheless, the RE market only accounts for about 1 % of the estimated USSSO billion in annual investment in grid-connected power ih developing counmes, and is espected to increase its market share substvltially over time. Favorable conditions in an increuing number of countries inciude =owing experience with private power projects, market b a e d power purchase prices. streamlined "

approval procedures for smaller projects and prior experience with andlor lncreued acceptance of RE technoiogies. The fastest growth recently has been in India and Central America, but on-gnd RE projects are being pursued by qualified sponsors in many other markets. The investment potential in deveioping countries is estimated at USS3-5 billion over the next 5 years. Most on-gid R E projects are in the 5-30 range, with costs typically berwetn USS 1-2 million per MW (as compared to large thermal power plants with costs of VSSO.5-1 million per M W but which typically hzve significantly higher fuel costs).

16. Off-orid RF businesses target the potential mass market of households, enteqrises and communities in regions unlikely to be served by the gnd in the foreseeable future (affecting some 1.5 to 2 billion people). The two major sub-sectors are: (a) small power plants, generally in the 50 kW to 5 MW rarge, with project sponsors typically seeking to develop a series of such projects, o h with active community participation (e.g. as minority owners, guarantors or operators), and (b) commercial deployment of solar home systems (SHS), typically costing several hundreds or thousands of dollars each. Most of the SHS sales have been on a cash basis to higher-income clients in leading markets such u India, Indonesia, Kenya, lMexico and Brazil, butthere is growins evidence that lower-income consumers are also willing and able to pay when suitable after-sale service and medium-term Iinancing are in place. This mvket can only deepen as system prices decline. REEF expects to complement a mowing number of other initiatives seeking to stimulate private entrepreneurship and the development - of effective consumer financing schemes in these sectors (including GEF, IBRD, ADB and other projects).

17. EE investment o ~ ~ o r t u n i t i e s are being pursued both directly by end users and by multinational - and local equipment suppliers and energy service companies (ESCOs). Demand for EE projects ijl growing as a result of energy price reforms, EE and environmental regu1atior.s. increzsed indusmal competition, government budget constraints, and other factors that make the nigh e n e r g

* intensity of many non-OECD economies increasingly unsustainable. since energy consumption u a percentzge of GDP can be several times higher rhan in OECD countries. IFC's market smdy conservatively estimates equity and debt investment potential for EE projects at USSZ billion over the next five years, without including the larger "passive sales" of EE goods and services. The investment and sales potential in this sector is typically mewured in the hundreds of billions of dollars. Central and Evtern Europe and India are leading EE mariters today, but considerable sector improvements are taking place in most developing regions. EE projects offer paybacks in the range of 1 to 5 years, often using simple and we11 proven technologies, such:zs meters and controls, efficient indusirial motors, furnaces, boilers, lighting and appliances. However, EE financing is a specialized and relatively

. complex area Since EE projects generate r e m s through energy cost savings, which u e less visible than incremental revenues, ESCOs often seek to overcome client reticence by providing or arranging - - up to 100% "performance- based" debt or lease finz?cing, to be repaid &om measured energy savings. In addition, while large EE projects can be found in rne inciuseal and energy sectors, much of the oppormniry iies in the development and financing of smaller projects (e.g., US$100,000 to USS3 million).

Financinv Weeds and Constraints

18. IFC's feasibility smdy found that while there are numerous equity investment opporrunities in these emer,$.ng seczors, more frequently there is icsufficient debt finmcing. For s n - e d W proiecq, the scarcest resource is long-tern debt, as it is for many private inhsmcrure projecs. REEF'S abiiity to provide some of ;his debt directly through the Debt Faciliry will help amact other lenders and generate more equity investment opporrunities h r REEF. Debt plays a1 even more in~orrant role in

. -

the F-= 2nd OF-~ci - RF sectors, where' many typical vonsors are enerE service companies andior equipment vendors. Their principal need is for more hghly leveraged meaium-tem or revolving debt or lezse financing for their clients, the energy end users.

19. RE and EE projects face diEcult financing challenges. Relatively few commercial sources of fmancing worldwide have experience in these sectors, and even fewer have turned their atrention. to the opporrunities in developing ciunmes. Unique con&aints relative to conventional energy projects include: the lack of familiarity with the technologies andlor project strucrures involved on the part of potential project sponsors, cl&s and financial institutions; the fact that the projects are typically smaller with proporrionately higher transaction costs, so that they are generally beyond the direct reach of international sources of financing, and some may not.obviously provide attractive remrns; the generally low collateral value and high - services content of many EE investments; and the need in some cases for longer-term financing than is generally available in a given market. For example, RE technologies genenlly have higher capGal cosG than conventional systems and therefore require long-term financing to capture the benefit of their rypically lower operating costs. -4dequate medium-term financing is also needed to overcome the "first cost" bamer facing lower-income purchasers of solar home systems, as well as to help persuade ene rg end users of the value of energy

efficiency investments, whose returns are measured not in terms of incremental revenues but of less visible cost savings. ...-

20. In many instances, financing is also impeded by the lack of information on and unfamiliar risk profiles of prospective clients in important market segments, such as state-owned utilities, municipalities and rural consumers; by currency convembility, devaluation and other economic risks; and by subsidized energy prices, high taxation and various administrative bottlenecks in many countries. many of these constraints are not necessarily unique to the RE and EE sectors, but they impose additional smcturing costs that can be absor~ed more readily by larger, more conventional projects. In much the same way as other IFC-supponed initiatives, REEF should help lower some of these barriers and encourage investment by other lntemational and domestic financial institutions.

111. PROJECT OBJECTTVES AND R4TTOV.4i.E FOR GEF FUNDTNG

Global Environment Obiectives and Benefits

2 1. REEF wiil channel new financial resources to investments in privately-sponsored projects in the RE and EE sectors in non-OECD counmes. The projects sup~oned by REEF will generate global environmental benests as a result of avoided GHG emissions. REEF is expected to catalyze iiuther private invesrment in GHG-mitigating projects by heiping to inuoauce proven F C and EE technologies and project structures in new markets, supporting new types of pro_iects and engaging new sources of commercial financing. . -

S~ecific Project Obiectives and Benefits

22. REEF's principal objective will be to generate a competitive risk-adjusted rate of rerurn fiom geogra~hcally and sectorally diversified equity and debt portfolios. REEF'S manazement team is expecred to seek out sound investment oppormniries being deveioped by highly qualified. project sponsors and to work ciosely with local financial intermediaries and sources of expertise as it siructures, implements, monitors and ultimately exits its investments. It is expected that the management team will seek to raise addition21 financing and expand its REEE investment activities on the basis of REEF'S commercial success and a continuing strong pipeline of investment opportunities.

. +

Rationale for GEF Fundino

23. REEF responds to the GEF's objectives of promoting sustainable energy proauction and use. The use of the GEF funds is consistent with the GEf Operational Strategy and Prosarns which call for the GEF to suppox innovative measures to leverage additional finance from the privare sector. It is estimated that the proposed USS30 million GEF grant could leverage investments of USS300-SO0 million from REEF 2nd other sources, or 10 to 27 times the amount provided by GEF, assuming that REEF's investments will represent between 25% and 33% of project costs on average. These estimates do not take into account the strong potential for a multiplier effect kom expansion or replication of successful projects.

24. ?here are virtually no major institutional investors focusing exclusively on the RE and EE sectors, even in developed countries. Commercial investment in these areas is generally pursued along with broa&r activities in the power, technology or other sectors and few of the active institutions have turned their artention to the opportunities in developing countries. Nevertheless, market development

. has reached a point where commercial investors can readily expect a fund dedicated to the RE and EE sectors to earn a competitive risk-adjusted rate of rerurn. However, a conventional fund would normally focus on projects that are larger andlor have lower transaction costs and lower risk profiles than many of the RE and EE projects currently under development.

25. The GEF support will allow REEF'S scope of investment to include promising RE and EE projects that might otherwise receive little or no attention because they aresmaller, risiuer, more complex andlor newer in a given market. REEF-will thereby make a greater contribution to RE and EE sector development prospects by mobilizing a greater number and wider variety of private sponsors and sources of cornmex-cia1 financing.

26. In the project review stage, GEF resources will enable the FMC to provide greater than normal advisor): suppon to project sponsors in resolving srmcturing issues and in mobilizing the necessary financing for their projecrs. This activity can help reduce market barriers by demonsrating eri'ective strucnuing techniques that can be aciapted by other entrepreneurs and financiers pursuing similar projects. With respect to project financing per se, GEF funds will be applied in innovative ways to help reduce ris'ks and otherwise improve marginal risk-adjusted rates of return that are preventing projects from going forward. . -

IV. PROJECT D E S C I ~ T T O N I

F Investment Vehicles

27. E E F ' s capital and mvlagement structure a n d h e GEF support seek to combine the diverse resources required to address the primary financing needs of rhe M E sectors in a dynamic and cost-effective manner. REEF will consist of two investment vehicles: (i) a closed-end Equity Fund with 2 term of 10 years (with 3 possible one-year extensions for liquidation purposes only), with a target capitalization of US51 10 million in equity commitments, and (ii) a parallel Debt Faciliry of USS100 million, to be used to extend loans of varying maturities to investee companies. Minimum commitments of US550 million each will be targeted for a first closing of the Equity Fund and Debt Faciliry, respectively. The iind closings are expected to occur within 12 months of the first closings. The Debt Facility will be organized as a "club" of participating lenders (commercial banks and IFC). Loans will be extended to projects in which the REEF Equity Fund invests pursuant to investment proposals resulting from detailed due diligence and structuring conducted by the FMC. It is expected that the banks' participation in a - oiven project will be extended under the umbrella of an F C B-Loan, where IFC acts as lender of record.

28. .4 wide range of potential investors expressed an interest in REEF during the course of IFC's market researcn, including electric utilities and independent power producers, insurance companies

concerned about global warming, commercial banks contacted during the fund management selection and fund structuring process and multilateral and bilateral investment agencies. IFC will invest in both the ~ q u i t f ~ u n d and Debt Facility and will assist in raising investor commitments outside of the United States, includin: those from commercial banks parricipating in the Debt Facility.

*

The Fund Manaoement Com~anv

29. The tern competitively selected by IFC to form the FMC is a consortium that combines extensive experience in equity fund management, commercial lending and the RE/EE sectors, including considerable experience in invesring in small-and-medium size projects. The consortium includes Energy Investors Funds (EIF), Environmental Enterprises Assistance Fund (EEAF) and E & Co, ex~ected to be joined by a major European international bank. EEAF and E 8: Co will focus on developing and managing REEF'S investments in smaller projects. E & Co will also play a key role in developing proposals for the use of the GEF co-financing resources, given its experience in the use of concessional resources in private sector FWEE projects.

30. . EIF is ,an investment management company focused exclusively on the management of power sector investment fui~ds and controlled by John Hancock Insurance and Indeck Capital Corporarion EIF's f s s ~ two established in 1988 and 1992 respecrively, have invested USS325 million in 30 power projects (1 8 in renewable eneigy) and 13 power projec~ development companies. Investors in EIF's funds have inciuded banks, pension funds and insurance compmy affiliates. EIF has 19 professionals on staff, with offices in Boston and San Francisco.

3 1. EZAF is a non-profit entity dedicated to managing for-profit environmental investment h d s in developi~g counmes. Established in 199 1, it has Aready invested in some 25 small projects, including 10 in the E / E Z sectors, and it currently has USSi 5 inillion under management, with funds provided by multilateral and bilateral agencies, foundations private investors, including a USS800,OOO line of credit korn the GC/GEF SME pro-gram. EEPLF is also serving as venrure capital advisor to the manzgement of the proposed IFC/GEF Teria Capital Fund to be headquartered in Brazil. EEAF is baed in .klingron, Virginia, with regional offices in Costa Rica, Indonesia and the Philippines.

32. E & Co is also a commercially-oriented non-profit entiry dedicated to the RE/EE sectors in developing counmes, sponsored by the Rockefeller Foundation and specialized in providing feasibility stage and early starr-up venrure capital financine. E & Co has made about 28 investments in both off-*d RE and smaller on-grid RE projects in i 6 countries and has an active pipeline under ,

consideration in over 20 developing counuies. E & Co has field representation in Costa %c& Bolivia, India Nepal and Zimbabwe.

- - 2 . Professional staff from the FMC already have substantial experience in the target sectors and emerging mar~ets counmes. The consonium members will both allocate existing staff to the REEF management effort and recruit additional staff and consultants as needed. Management resources will be available from the principaI offices 'of the FMC members and a proposed dedicated office in Washington, D.C.

Investment Policies and A ~ ~ r o v a l ~ . .4-

34. REEF'S principal investment objectives are long-term capital appreciation ftom t!e Equity Fund's equity and equity-type investments and current income irom the dividend and interest earnings - respectively of the Equity Fund and Debt Facility. Both vehicles will invest primarily in projects with total costs below US550 million and the Equity Fund will seek to allocate at least 20% of its resources to smaller projecs of less than USS5 million. REEF will seeic to develop diversified ponfolios in terns of both sectoral and geographic coverage. The proposed investment guidelines specify that the Equity Fund and Debt Facility will invest no more than 80% of their resources in one of the three principal target sectors (on-grid RE. off--gid RE and EE) and no more than 60% in a given region, defined as one or': (i) Asia, (ii) Latin America and.the Caribbean, (iii) -4fnca and the Middle East, and (iv) Central and Eastern Europe and the'Newly Independent States. The Debt Facility will have several additional investment criteria, including minimum debt service coverage ratios and maximum debt:equity levenge ratios at the project level.

35. REEF will not act u tine principal sponsor of any project and will invest in projects where the sponsor has relevant experience and retains a si-&Scant finulcial interesi. Ln reco-enition of the vital role being played by project developers in all three targer sectors, notably in tcnns of aggegaring smaller investment ooppomnities into financeable portfolios oi'pro_iecrs, up to 15% ofthe Equity Fund portfolio could rvresent investmenrs made in the fezsibility and struc&.g stages oiprojects.

36. REEF will adhere to th; world Bank Group's environmental policies and pideiines. IFC will assess the FMC's capability to carry out environmental reviews of eacn investee project and will periodically review REEF'S and the M C ' s acrivities in this respect. Staff ofthe FMC will be required to attend a standard IFC training program on the Bank's environmental policies and guidelines.

37. The Equiry Fund will have an Invesunent Coxunittee that will nzke investment and sales . .

decisions by unanimous vote. IFC will have the right to appoint a representative to thls Committee. Lending decisions by the Debt Facility will be subject to approval by eacn of the participants and no

. loan will be made to an investee company without a loan fiom IFC. The FMC will also have an internal investment committee that will recommend investments for the above-mentioned equity and debt approvals. As an incentive for the FMC to pursue smaller investments, this internal corriittee wiil be empowered to approve certain categories ofEquity Fmd investments below USS500,OOO.

38. The Equity Fund will have an Advisory Committee, consistiig of members appointed by .IFC, the FMC participants, other "core" investors (defined as investors commining si-enificant investment to the fund) and one outside member unaffiliated with the managers andlor investors. The Advisory Committee will meet on an annual basis to review the fund's investment policies, strategies and performance and to approve any changes to the investment policies.

V. USES OF= GEF SUPPORT

39. The GEF funds will be used to: (i) to provide direct co-financing for select REEF investee projects in the form of grant, debt and/or equity financing, (ii) support the FMC's incremental

management costs of investing in such projects, and (iii)'cover IFC's eligible costs for co-administering the GEF support as GEF Executing Agency. (Set project budget in paragraph 49 below.) -

11

40. It is proposed that the first USSlO million in GEF funds be made available upon successful first closing of the REEF Equity Fund of at least USS50 million. An additional USS10 million of GEF funds would be made available to REEF once USS 100 million in non-GEF funding is mobilized with the remaining USS10 million in GEF support be provided on a prorated basis in relation to the next USS 100 million in capital raised for the Equity Fund and Debt Facility. Capital (equity or debt) will be defined as mobilized or committed to the fund when a signed lerter of commitment to invest in the Equity Fund or to panicipate in the Debt Facility is received by the fund manager. GEF h d s made avaiiable to REEF at each of the above-described investment levels will be allocated to the uses of

, GEF funds listed in para=ga~h 39 on a pro rata b&is. The project objective, scope, design, and size (USS 100 million to USS2 10 million in non-GEF investment) remain the same. However, an intermediate step has been added to give REEF a better chance to reach the objective target size quickly. Once REEF is established with a quick Srst closing of USSSO million, it is expected (based on FC 's experience with many other funds) that the fund manager will be able to more quickly raise additional capital. For tlxs rewon, frst closings are common. There is little risk that the amount of non-GEF investment raised will be limited to USS50 million. Ii is in the fund manager's best interest to raise w large a fund u possible u quickly as possi'ole. For a,? innovative fund like REEF, the management fee on a small fund of US950 million is not sufficient to cover the manager's costs.

41. The bulk of the GEF support, up to USS24 million under REEF'S full capitalizzrion scenario, will be channeled directly to REEF investee projects as co-fmancing to help meet-the incremental costs or risks involved when compared to non-GHG-mitigating altmarive or "bzseline" projects (see the Incremental Cost h a l y s i s in Appendix A). Potendal forms of GEF co-iinancing may include -grants, loans, guarantees, equity or hybrid instruments. The specific hmcing modality used for a given project will seek to address as closely as possible the pamcular mar~e t banier(s) or other disadvantage it faces, on a bwis that can produce an acceptable risk-adjusted rate o i r en t z to its shareholders.

42. Only investments that meet the criteria below will be eligible for GEF co-financing support: 4

Investments must be in countries that have ratified the FCCC and are eiigible for World Bank/lFC financing.

Investments must be in activities that are consistent with internationally agetd p r o - m s for sustainable development, achieve global - environmental benefits and are consistent with a countq's climate chmge action plan. Tne appropriate national GEF "counuy focal points" will be notified when a project in a particular country has been approved for GEF co-financing.

Investments must be in projects in which the REEF Equity Fund andlor Debt Facility has made a formal commitment to invest.

In accordance with the GEF Operational Strategy (Feoruary 1996) and its related Operarional Programs for the climate change focal area, GEF support must be j.ustified by: (a) a reco-pized markei barrier, in the c u e of projects utilizing competitive technologies and/or appiications thereof described in Operational Program 3 (most energy efficiency projects) and Operational Pro-gram +6 (most renewable energy technologies and applications), andlor (b) the opportunity to promote a technoloq or application that is nor fully cost-competitive, as defined in Operational Pro-gram $7.

Invesments must be "close to maricet ready", in that they meet the criteria for professional, commercial investing, but for a particular m a r ~ e t barrier or cost disadvantage that prevents them from obtaining all of the needed financing on terms *at produce an acctprable risk-adjusted rate of return.

-.

. Investments must be in amactive markets, GEF co-financing wiIl not be applied to compensate for .market distomons, including situations where: (a) e n e r 9 prices are not close to long-run marginal

. costs, (b) import and orner taxes are excessively high, (c) market demand is inherently weak and GEF support is unlikely to catalyze funher commercial investmentt and (d) ve? Senerous incentives already exist and should be pursued as a matter of priority by the projecr under considerzrion.

43. The FMC will develop detailed proposals for investment of the GEF co-fmancing resources and submit them for approval to a four-member IFC-REEF-GEF Committee (IRGC), composed of one representative each h m EC's Techniczl and Environment Ceparanenr, E C ' s Power Dqarmient, the World B a d ' s Global Environment Division and a member seiected fiom outside the World Bank Group and GEF. The IRGC will approve the tenns of each GEF co-financing rransaciion p m t to ,~delines that will take inro account such factors as the size of the project, the narure and extent of the incremental costs and risks ro be mitigated with GEF s u p p o ~ , the potential for expansion and replication and other criteiia Tne R G C will consult with the GEF Secretariat when 2 new non-"grant financial instrument is used for the first rime under the co-financing arrangement.

. IFC will manage the co-financing funds in accordance with IRGC decisions in a manner that seeks to recover a reasonable amount of funds to be retuned to GEF at the end of REEF'S life, consistent with the purposes of REEFana the pioneering role of the GEF funds. The GEF co- financing guidelines will encourage the FMC to maximize rhe amount of co-financing that is ixtended to eligible projects on a non---t basis. Tine objective is not simply to recover a reasonable ponion of the GEF resources, but also to help demonstrate the financial sustainability of projects and thereby catalyze similar creative financing £rom other sources. As an incentive to focus on such opportunities and in keeping with commercial fund management practices, it is proposed that the FMC be entitled to retain a small share of the non--mt GEF co-financing effectively recovered froin investee projects. This incentive provision is similar in principle to the incentive given to the FMC to man2ge and recover the commercial in\:estment positions of the REEF and is similar in principle to the incentive given to intermediaries pmicipating in the IFC/GEF Small 2nd Medium Scale Enterprise Program. Without this incentive, experience suggests the FMC would likely focus on the more commercial part of the Fund's portfolio and would lack an adequate incentive to recover the GEF funds.

Manaoement - Costs

45. T ~ ~ F M C will earn market-based compensation for the management of the Equity Fund portion of REEF, including an annual management fee designed to cover the FMC's reasonable . operating costs and incentive compensation for achieving the market rates of returns targeted by the Equity Fund (see Appendix A for additional information). However, an FMC investing in a diversified range of projects and markets in the RE and EE sectors can be expected to incur higher than normal costs for a number of reasons. With average investments likely to be under USS5 million, the Fund's portfolio may consist of30 or more projects. Since commercial investment funds typically invest in no more than 15-20 projects, the Fund's personnel requirements are likely to be geater than usual. The potentially wide range of markets, technologies, projects and financing tecimiques also calls for a broad base of skills within the FMCand rezular use of outside specialists. The pioneering name of many REEE transactions currently under development and the inadequate attention to date from ..; ; commercial sources of financing is also likely to require that the FMC provide eater than normal f , project suucturing, technical vsistance and advisory support to project sponsors. . .

46. Up to USS5-6 million of GEF grant funds will therefore be used to cover the FMC's .

incremental costs of identifiing, analyzing, investing in and adding value to projects qualifying for GEF co-financing support and of meeting addidonal monitoring and reporcing requirements axising from the GEF support. The GEF , m t s will cover the additional staff, consultants, mvel and other costs associated with these ac:i\ities. The FMC's staff is expected to include several professionals specifically focusing on EE, off-grid RE andlor smaller on--&d RE projects (e-g. beiow USS5 million total cost). It is anticipated that'the grant support will be disbursed to the FMC during its 5-year invesment pexiod on the basis of annual budgets approved and closely monitored by the IRGC. The IRGC will assess the appropriateness of all incremental costs funded by GEF. -

R e ~ o ~ i n o -.

47. The FMC will submit an annual report to the IRGC coveri?~: (i) the status of the GEF co- financing portfolio, (ii) the penbrmance of the GEF-supported projects in terms of meeting GEF objectives, and (iii) related e~vironmental and other beneiits being generated by the projects. It is expected that the reporting work will be carried out largely by the FMC and the investee companies themselves. The reporting wiil be consistent with GEF's own monitoring and evaluation practices and information disclosure requirements. The R G C may also call upon independent experts as needed for technical assistance and for verification, evaluation and interpretation of reported results. Any incremental costs of reporting will be covered by the GEF co-financing support.

Administration

38. IFC will administer the GEF funding as GEF Executing Agency, acting in accordance with decisions of the proposed IRGC (see para. 6 and 43). IFC's costs of administering the GEF funds over 10 yean are estimated at USSl million. Following completion of the final GEF endorsement process and the Fund's mobilization process, the GEF funds will be made available to IFC from the GEF Trust Fund through the World Bank's Trust Funds Division. Commitments against these funds will be made in accordance with IFC's arrangement with the World Bank as GEF Implementing -4gency.

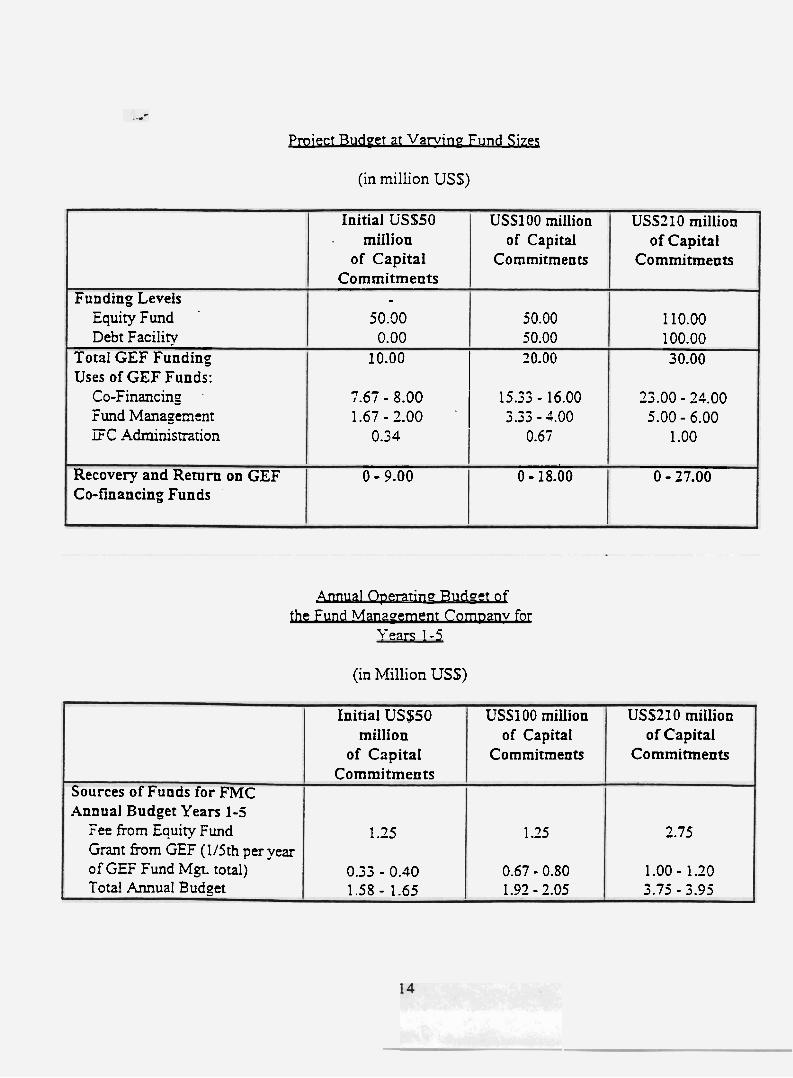

Proiect Budoet

49. TM uses of the GEF funds at three possible levels of GEF involvement are outlined in the Project Budget table below. In addition, the sources of annual budgetary suppon to the FMC are listed in the second table. The tables are based on the following assumptions:

a) Capital commitment levels: (i) the initial USS50 million is the first closing of the Equiry Fund; (ii) USS100 million capital commitment level includes the initial USSSO million Equity Fund and USSSO million mobilized for the Debt Faciliry; and (iii) the USS210 million commitment level includes a USS 1 10 million Equiry Fund and a USS 100 million Debt Facility.

b) Uses o'f GEF funds: Use of GEF funas at the USSlO million and USS20 million GEF funciin3~ levels are adjured proportionally ffom rhe total porential allocanons at the USS30 million funding level.

c) Recovery and remrn on GEF funds: The worst case scenario zssumes that none ofthe GEF co-financing invested in sub-projects as loans, equiry or guaiantees is recovered (i-e., all loans and all equiry arc a total loss and all guarantees are exercised). -2 best czse scenario is based on &e following assumpnons: (i) 30% of the GEF co-5nancing is advanced as loans, 30% as loan guarantees, 30% as equiry, and 10% u -efanrs; (ii) reasonable or conservative assumpdons on interest, capital gains, and dividends; (iii) a provision 5 r losses; and (iv) an incentive payment to the FMC.

d) Sources of funds for FMC budget: (i) the FMC's annual management fee chuged to the Equiry Fund is expecred to be 2.5% of the Equity Fund's capital commiunents; (ii) the FMC is nor expecred to receive fees from the Debt Faciiity; and (iii) the GEF funding for fund management will be disb~tsea to L Q ~ FMC during the fm five yezn of REEF'S operation--thus on zverage one fifth of the. total amount will be disbursed to the FMC per year for years 1-5. The GEF contribution to the h n d mulz_gement cosrs is discussed further in paragraphs 9 and 10 of Appendix -4.

Proiect Budeet at Varvino Fund Sizes

(in million USS)

m a 1 Operatbc Budaet of u ~e F nd Manaeement Com~anv for

>'ears 1-5

Funding Levels Equity Fund Debt Facility

Total GEF Funding Uses of GEF Funds:

Co-Financing Fund Mana, oement F C -4dmnistrarion

Recovery and Return on GEF Co-financing Funds

(in Million USS)

USSt 10 million of Capital

Commitments

1 10.00 100.00 30.00

25.00 - 24.00 5.00 - 6.00

1 .OO

0 - 37.00

Initial USS50 . million

of Capital Commitments

- 50.90 0.00

USSl 00 million of Capital

Commitments

50.00 50.00

USS210 million of Capital

Commitments

2.75

1-00 - 1.20 3.75 - 3.95

Sources of Funds for FMC Annual Budget Years 1-5

fee from Equity Fund Grant from GEF (115th per year of GEF Fund Mg. total) Total Annual Budget

10.00 20.00 I 7.67 - 8.00 15.53 - 16.00 1.67 - 2.00 1 333 - 4.00

Initial US$50 million

of Capital Commitments

1.25

0.33 - 0.40 1.58 - 1.65

0.34

0 - 9.00

USS100 million of Capital

Commitments

1.25

0.67 - 0.80 1.92 - 2.05

0.67

0 - 18.00

e

.

VI. SUSTATNABTLITY AND P.4RTTCIPATTOTV

50. REEF will bring together an investor group and management team with a clear commitment to RE and EE market q o w h through profitable private investment. It will support RE and EE project . sponsors who are actively engaged in client and market education as they promote cost-effective and environmentally sound approaches to meeting and managi~g energy demand. REEF'S investments will support national climate change action stratezies in a concrete way by engaging utiiities, municipalities, rural populations and other EE and off-gid RE clients more deeply in seiecting the best options for a more sustainable e n e r g future. ,411 of these factors will help build a commercial investment track record and accelerate the gowth of the R E and EE sectors on a sustainable long-term basis.

-. 5 1. Given the relatively small project sizes, the REEF'S success will depend on and can be instrumental in encouraging co-investment and value-added support from local comrnercia! and development bankmg institutions. small business and rurzl consumer financing entities, community and consume: goups, NGOs and others corniiined to developing the RE and EE sectors. The smaller projects can also obtain business planning and finance mobilization assistance fiom various ShE suppon pro-grams, inciuding IFC1s several regionally-operzred Project Development Facilities.

52. REEF will offer many opporrunities for stakeholder panicipation. It wiil have access to an extensive nerwork of organizations and individuals who u e willing and able to direct its artention to specific invesrment oppomnities and to provide ad hoc advice. These sources of "deal flow" and broader support include host country utilities, RE and EE trade associations, NGOs, foundations, development banks, govemnent and donor agencies, and others. Many such organizations were consulted during F C ' s feasibility srudy and many members of IFC and FiviC staff u e also actively involved in these neworics. .hy activities to monitor the environmentzl and economic benefits of REEF investec projects will also offer oppomir ies for consultation with locai utilities, comrnuniries and other client bues, with host country authorities, responsi'ole for implementing country strategies on climate chmge, u well as with other host government agencies and international institutions and experts working in the area of energy sector deveiopmenr and environmental protection.

W. J .F.SSOYS T .F, 4RNEQ 4

53. IFC is a leading investor in the emerging private power markets in developing counmes, through direct loan and equity financing, syndicated loans and panicipation in several imhtrucrure investment funds. While most of the activity concerns large conventional power plants, IFC has also financed a number of small hydro, biomass and geothermal projects and is appraising potential investments in wind power piants. IFC has invested in energy conservation projects and is considering investments in the off--grid renewable enerzay sector. This experience confirms that well-designed projects in these areas can be commercially viable under price and other conditions prevailing in various markets. However, given the small project sizes relative to other LFC power sector invesrments, IFC is seeking oppomnities-in addition to its direct financing activities--to channel resources through other financial intermediaries who can reach such projects cost-effectively: not only the proposed Fund. but also local commercial banks and leuing companies. The lessons leaned fiom IFC's extensive participation in venture capital and investment funds and from its leadership role in

private power project financing have been incorporated in the proposed structure of REEF and the design of the proposed GEF support.

,I

VIII. PROJECT RISKS

54. Mobilization Risk: The REEF Equity Fund and Debt Facility may not achieve their respective capitalization targets totaling USS2 10 million. Risk factors include the relatively early stage of development of the target sectors, small project sizes, potential investment in a wide range of countries with dirTerent risk profiles and the relative lack of experience among commercial banks with debt facilities of the type envisioned. ow ever, prior to any formal marketing having been conducted, the initiative h u drawn considerable interest from a wide variery of potential investors. The mobilization risk is also mitigated by IFC's participation and by the prospective use of GEF fun& to broaden the scope of available investment oppomrnities and to cover a ponion of the larger-than-ordinary fund management costs.

55. Debt Facili*: Since sub-loans under the Debt Facility must be approved by each participating lender through the Debt Facility Investment Committee, there can be no assurance that all of the Debt Facility will be drawn down and used by REEF withm the Debt Facility's life. Funhennore, the abiliry of each pamcipant bank to opt out of a given loan could rtsult in iess than USS100 million being made available to REEF. This risk will be mitigated by the clear definition in advance of the range of transactions that will be considered aila specific criteria to be met. In addition, penalties may be applied to Debt Facility participants who reject two or more proposed transactions that aie approved by IFC.

RENEWABLE ENERGY .4ND ENERGY EFFICIENCY FUND (REEF)

Appendix A 1 1 s

Global Environment Obiectives and the.Baseiine

1. The proposed GEF support for REEF is designed to help expand the market for commercial financing of RE and EE projec~s in emerging m x ~ e t counmes, thereby accelerating the pace and improving the sustainability of development of these sectors. An intern2iional investment fund seeking to earn a risk-ad-iuted commercial rate of return would normally focus on projects that are larger andlor have lower transaction costs and lower risk ?rofiles than many RE and EE projects currently under development. The impact of such larger prajects may be less than that of smaller. riskier andlor more complex projects in terms of the deeper market penetration needed for accelerated RE/Er , sector development. Support for such projects could have a strong multiplier effect on private investment and sales in potentially large maiket se-ments currently in earlier sages of development.

7 -. -4bsent the successful inplemen~a~ion of GHG reduction strategies, GHG emissions are expected to rise from 6.5 Gigatonnes (Gt) per year in 1995 to 1 1.1 Gt in 2025. A mzssive expansion of the RE azld EE sectors, among other developmenn, will be needed to s~zbilize concenrarions of GHGs in the aunosphere, the long-term objective of the FCCC. .4ccording to [he Inter-Governmental Panel on Climate Change, stabilization could evenrually require an estimated 60-70% cut in annual GHG emissions relative to tadav's emissions level^.^

,4lternative witb GEF SUDDOK

. J. The GEF funds wiil help: (i) compiete the financing required for &e developmem andfor implementation of e i i g ~ l e projects that are unlikely t3 proceed in timeiy fvhion without support from concessional sources due to unacceptable incremental costs or riskscs: and (ii) defray the incremental management costs of invexing in such projects.

4. As a result of the GEF support, REEF is likely to invest in a larger number and greater diversity of projects in a wider range of countries than a convenrional fund, to provide greater than no&al advisory support to project sponsors, and to have a ;tronger demonstration effect with respect to the commercial investment opporruniry and the documentation of environmental and economic benefits of RE and EE private sector projects.

incremental Costs and Risks

5 . GEF funds will be used ro fund increment21 costs of: a) the REEF'S additional higher administrative costs of processins and suoervising a portfolio of renewz'ble energy a - N

2~nrer-~overnmen~al Panel on Ciimare Change, Climare Change 1992: m e S ~ q i e m e n m l Repon ro rhe IPCC Scienrific Assessmenr. Cambridge University Press. Cambridge, UK

efficiency projects, and b) for co-financing the i n c r e r ~ ~ = ~ l r ~ l costs of the smaller, riskier, and more 6 innovative projects financed by REEF. - * . .. .

Manaoement and Administration

6. The incremental costs related to the management of REEF are the additional operating costs expected to be incurred by the FMC due to REEF'S anticipated investments in projects that would not normally be considered by a commercial investment fund due to their small size, complexity and/or other factors previously mentioned. In addition, the FMC, F C and the investee companies will incur incremental costs in administering the GEF funds. Removal of barriers at the level of the fund (these incremental manazement and administrative costs) is consistent with GEF Operational Pro-grams g5 and S6 on barrier removal. - 8. .4 private equity fund mznager typically charges an annual fee to the fund of 2% to 3% of commirted capitzl to cover fund management costs (if the fee is higher than this, it becomes difficult to attract investors to the fund due ro the adverse impact on their expected returns). Tnis fee covers stafc consultants, tiavei, overnead and other costs associzted with m&g investments and maxiaging the ponrblio. However, an FMC iilvesting in a diversified range of projects and markets ir; the RE and EE sectors, with artention to smaller and/or pioneering projects, can be expected to incur higher than normal costs for 2 number of reasons (set para 46 above).

9. The estimated budget for managing the REEF is berwctn USS3.75 and USS3.95 million per year, or 3.4% to 3.6% of the Eauiry Fund's target equity capital of USS110 million, b a e d on projections deemed consistent with IFC's experience with invesunmt funds in emer=@g markers and more specifically wi& investment in small-and-medium size enterprises and projects. The expected annual management fee of 2.5?4 of ca?ital will therefore be suppiemented by up to USS 1 to US5 1.2 million per year in GEF -grant suppon (at REEF'S USS200 million in capital commiunent level) to cover the additional operating costs associated wirh.icvesrment in pro-iecn e!igible for GEF co- financing. It is anticipated thai the grant support will be disbursed to the FMC during its 5-year invesrment period on the basis of annual budges approved and closely monitored by rhe IRGC. The' R G C will assess the zppropriateness of all incremental costs funded by GEF. If the costs incurred by the FMC in excess of 2.5% of committed capital are not deemed to be justified by IFC, subsequent disbursements oiGEf funding to the FMC will be reduced accordingly. . i

10. Note that the Debt Faciiiry porcion of REEF does not figure into estimation of the FMC'S budget (as outlined in parasauh 49 above). Each participating lender in the Debt Faciliry will likely charge front end and commitment fees to each project receiving deb!. -4lthough fee arrangements will depend upon the final negotiations concerning the Debt Faciliry, the FMC is not likely to receive fees from the Debt Faciliry. The FMC may charge the investee company or project a closing fee for putting together the debt ponion of the investment.

1 1. As an incentive to focus on the GEF porcion of the REEF ponfoIio and in keeping with commercial fund management practices, it is proposed that the FMC be entitled to retain a small share (to be negotiated with the FMC) of the non--mt GEF co-financing effectively recovered from invest'ee projects (see paragraph 44 above for funher explanation). This incentive is an incremental

cost. The incentive will not be paid unless non-grant GEF co-financing funds are recovered from projecrs. The incentive amount paid to the FMC (and the amount cjf the incremental cost) will

I thereforedepend upon the amount recovered from projects and the FMC incentive share.

Co-Financinv

12. In the case of incremental risks and costs for the project co-financing, the GEF funds will suppon projects that are commercially viabie or nearly so, but that would produce unacceptable risk- adjusted rates of rerun without some degree of concessional support. It is expected that the buik of the GEF co-financing will take the form of loans, guarantees, equiry investments, and -pnts for transaction cosrs (consistent with GEF Operational Programs =5 and S6). In addition grants may be used for capital cost buy-downs involving techn~iogies descri'oed in Operational Progzm $7 where a ,pnt is the only insirument reasonably capable of delivering the incentive needed to produce an acceptable risk:return rario for the project

1 . T i e prolect sponsors will be required to make a proposal to the FMC and the LRGC justifying why they u e asking for the parcicular type. terms, and amount of GEFsuppon. The form and terms of' GEF co-financing in E E F invesunent projects will be developed and approved in accordance with investment pidelines to be adopted by the IRGC, in keeping with the criteria set out in para-pph 42 of Project Document. The FMCand IRGC will review a number of factors in determining the amounr in terms of GEF funding, including: ji) the regular ways that investment h a s and IFC do business with investee companies; (ii) a consideration of a reasonable target risk-adjusted rate of return on equiry (R4RR) of the proje6q (iii) the pricing of' the debt and equiry co-financing available to the project; (iv) the amount and type of commercial funding available to the project; (v) the relation~hip of the GEF co-financing to the esrinared level of incremental risk and cost associated with a possible invesrrncnt taking into consideration the expected risk-adjusted rates of return and cosrs of altenative (non-GXG abating) projects; (vi) the desire to ensure that the project sponsors, other financiers and other ?artkipants nzve a strong commercial incentive-not only to invest in the supported projects but also to expand their efforts in the target - F Z and EE sectors to the fullest of their capabi!ities (vii) the form of the invesrment whicb should correspond as closely u possible to the parcicular marice: barrier creating the need and justification for the GEF support, such as a loan that extends the repayment period if the market bamer is lack of access to long-term credit, or a partial guarantee if the impediment is the credit profile of a particular cliest or clzss of clients, u is often the case in EE and ofi,gid RE transactions; and (viii) cost-effective use of the GEF funds.

14. There is no firm basis rbr estimating a priori the amount of actual incremental cost to be met by the GEF funds used for project co-financing since the bulk of' the GEF co-financing will be in the form of loans. loan guarzntees. and equity investments. Incremental costs in this context are defined as GEF funds going to the sub-projects that are not recovered and returned to the GEF. It will only be after a period of eight to thircetn years (after REEF has exited investments) that good information on actual outcomes will be available. Theoretically, the amount of incremental cost could range irom a worst case scenario of up to USS23 million (the total amount of GEF co-financing) if all loans. equity investments and guarantee arrangements are a total loss to the percentage of co-financing advanced in the form of grants (for example USS2.S million if 10% of co-financing goes to ,orants). Under a best case scenario. there is a possibility under resonable assumptions that the amount of funds repaid to

GEF from loans and equity investments and income thereon, and unutilized guarantees and will exceed the USS24 million in GEF co-financing.

i ...-

b

Appendix B a Summ y of Disbursement Arrartyernenfi

The GEF _mant of up to USS30 million will be made available to IFC from the GEF Trust Fund through the World Bank's Trust Funds Division. Disbursements are expected to take place as follows: -

co-fins-: invested during the course of REEF'S normal five-year investment period as needed for projects approved by the IRGC.

FMC Cosrs: paid semi-annually in advance to the FMC during its first five years of operation. pursuant to budgets approved by the BGC.

. . -: drawn down as required over a ten-year period.

As discussed in para,pphs 9 and 40 above, it is proposed that the Zirst 'L'SS10 million in GEF funds be made available upon successfd first closing oithe REEF Equity Fund of at least USSjO million of non-GEE: capital an additional USS10 million in GEF supporr be provided when USS100 of non-GEF capital is mobilized, with the remaining USS 10 million of GEF h d s provided on a prorared bzsis in relation to the next VSS100 miilion in capital raised for the Equity Fund and Debt-Facility.

Appendix C Tm~lementation Timetable

Time taken to prepare project IFC management approval granted to project concept Launching of feasibility study GEF Council initial endorsement Selection of REEF ihnd management team Completion of REEF structuring and appraisal Approval of F C investment by IFC Board of Directors

- 4

2.5 years December 1994

March 1995 April 1996 July 1996 May 1997 June 1997