the world bank and the mdtf partnersdocuments.worldbank.org/curated/en/569641468270268… · ·...

TRANSCRIPT

Document of

The World Bank and the MDTF Partners

Report No: 73328-MW

PROJECT APPRAISAL DOCUMENT

ON A

PROPOSED GRANT

IN THE AMOUNT OF US$19 MILLION

TO THE

REPUBLIC OF MALAWI

FOR A

FINANCIAL REPORTING AND OVERSIGHT IMPROVEMENT PROJECT (P130878)

28 FEBRUARY, 2013

Financial Management

Core Operations Services

Africa Region

This document is being made publicly available prior to Bank approval. This does not imply a presumed

outcome. This document may be updated following Bank consideration and the updated document will be

made publicly available in accordance with the Bank’s policy on Access to Information.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

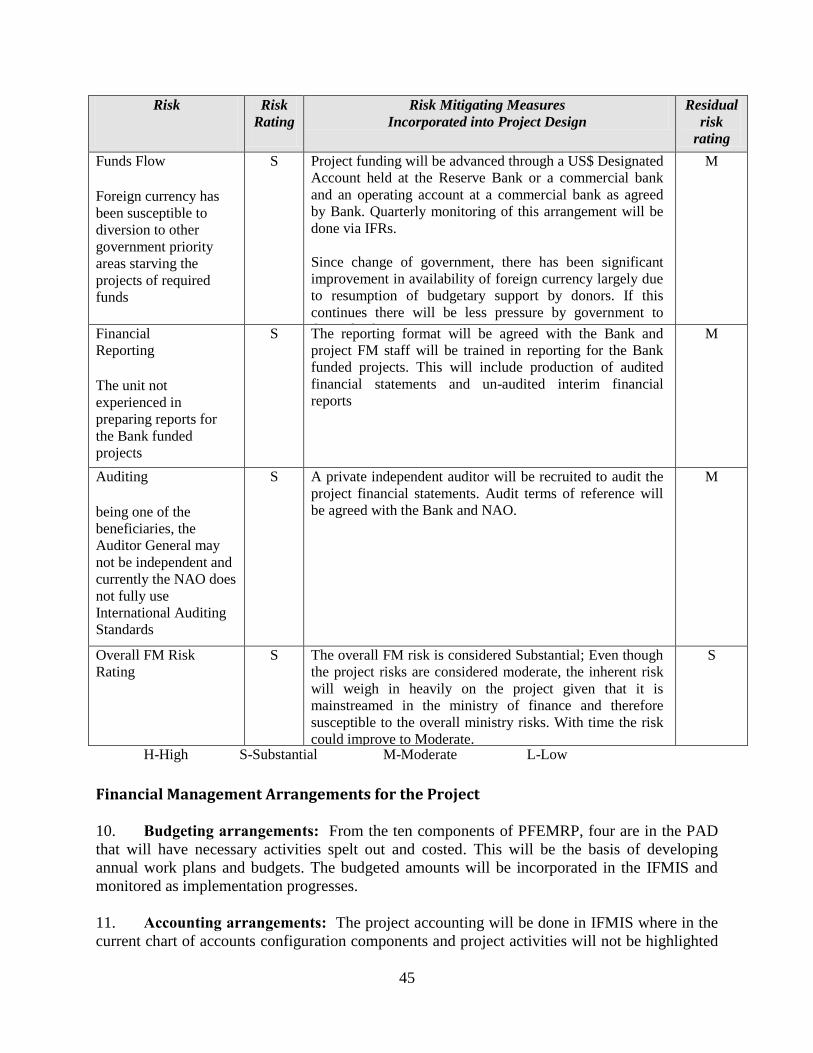

iscl

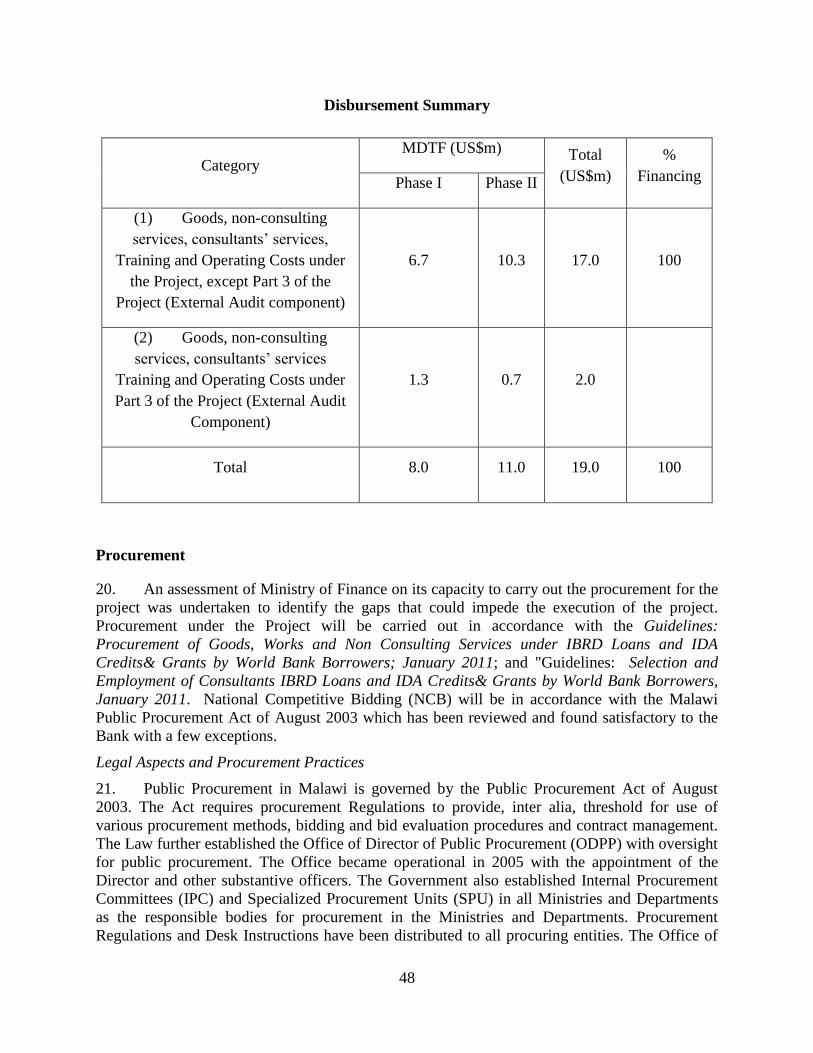

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

2

CURRENCY EQUIVALENTS

(Exchange Rate Effective {February 25, 2013})

Currency Unit = Malawian Kwacha (MK)

US$1 = 369 MK

FISCAL YEAR

July 1 – June 30

ABBREVIATIONS AND ACRONYMS

AGD

AR

CAATS

Accountant General Department

Accounts Receivable

Computer Assisted Audit Techniques

CABS Common Approach to Budget Support

CAS Country Assistance Strategy

CIAU Central Internal Audit Unit

CoA

CPD

CSA

Chart of Accounts

Continuing Professional Development

Controls Self-Assessment

DAD

DHRMD

DISTMIS

DR

ERM

Department of Aid and Debt

Department of Human Resource Management and Development

Department of Information, Systems and Technology Management Systems

Disaster Recovery

Enterprise Risk Management

FDI Foreign Direct Investment

FIMTAP Financial Management Transparency and Accountability Project

FROIP Financial Reporting and Oversight Improvement Project

GFEM Group on Finance and Economic Management

GFS

GoM

Government Finance Statistics

Government of Malawi

HIPC Heavily Indebted Poor Countries

IDEA Integrated Data Extraction and Analysis

IFMIS Integrated Financial Management Information System

IPSAS International Public Sector Accounting Standard

LG Local Government

LG&RD

MASAF

Local Government and Rural Development

Malawi Social Action Fund

MDA Ministries, Departments and Agencies

MDTF

MGDS

MoF

Multi Donor Trust Fund

Malawi Growth and Development Strategy

Ministry of Finance

MPRSP Malawi Poverty Reduction Strategy Program

MRA Malawi Revenue Authority

3

NAO

NLGFC

National Audit Office

National Local Government Finance Committee

ODPP

OPC

ORAF

PA

Office of the Director of Public Procurement

Office of the President and Cabinet

Operational Risk Assessment Framework

Performance Audit

PAC Public Accounts Committee

PAD Project Appraisal Document

PDO Project Development Objective

PEFA Public Expenditure and Financial Accountability

PFEM Public Finance and Economic Management

PFEMRP Public Finance and Economic Management Reform Program

PFEMSC

PFEMTC

PFEMU

PFM

Public Finance and Economic Management Steering Committee

Public Finance and Economic Management Technical Committee

Public Finance and Economic Management Unit

Public Financial Management

PI Performance Indicator

RBM

RBPFA

RCIP

SAICA

SN

TNA

TTL

TWG

Reserve Bank of Malawi

Results Based Process Focused Approach

Regional Communications Infrastructure Project

South African Institute of Chartered Accountants

Serenic Navigator

Training Needs Assessment

Task Team Leader

Technical Working Group

Regional Vice President: Makhtar Diop

Country Director: Kundhavi Kadiresan

Country Manager:

Sector Director:

Sandra Bloemenkamp

Edward Olowo-Okere

Sector Manager: Patricia McKenzie

Task Team Leader: Pazhayannur K. Subramanian

4

MALAWI

Financial Reporting and Oversight Improvement Project (P130878)

TABLE OF CONTENTS

Page

I. STRATEGIC CONTEXT ...............................................................................................11

A. Country Context .......................................................................................................... 11

B. Sectoral and Institutional Context ............................................................................... 12

C. Higher Level Objectives to which the Project Contributes ........................................ 14

II. PROJECT DEVELOPMENT OBJECTIVES ..............................................................15

A. PDO............................................................................................................................. 15

Project Beneficiaries ......................................................................................................... 15

PDO Level Results Indicators ........................................................................................... 15

III. PROJECT DESCRIPTION ............................................................................................16

A. Project Components .................................................................................................... 16

B. Project Financing ........................................................................................................ 18

Lending Instrument ........................................................................................................... 18

Project Cost and Financing ............................................................................................... 18

C. Lessons Learned and Reflected in the Project Design ................................................ 19

IV. IMPLEMENTATION .....................................................................................................20

A. Institutional and Implementation Arrangements ........................................................ 20

B. Results Monitoring and Evaluation ............................................................................ 24

C. Sustainability............................................................................................................... 24

V. KEY RISKS AND MITIGATION MEASURES ..........................................................25

A. Risk Ratings Summary Table ..................................................................................... 25

B. Overall Risk Rating Explanation ................................................................................ 25

VI. APPRAISAL SUMMARY ..............................................................................................25

A. Economic and Financial Analyses .............................................................................. 25

B. Technical ..................................................................................................................... 26

C. Financial Management ................................................................................................ 26

D. Procurement ................................................................................................................ 26

5

E. Social (including Safeguards) ..................................................................................... 27

F. Environment (including Safeguards) .......................................................................... 27

G. Other Safeguards Policies Triggered (if required)...................................................... 27

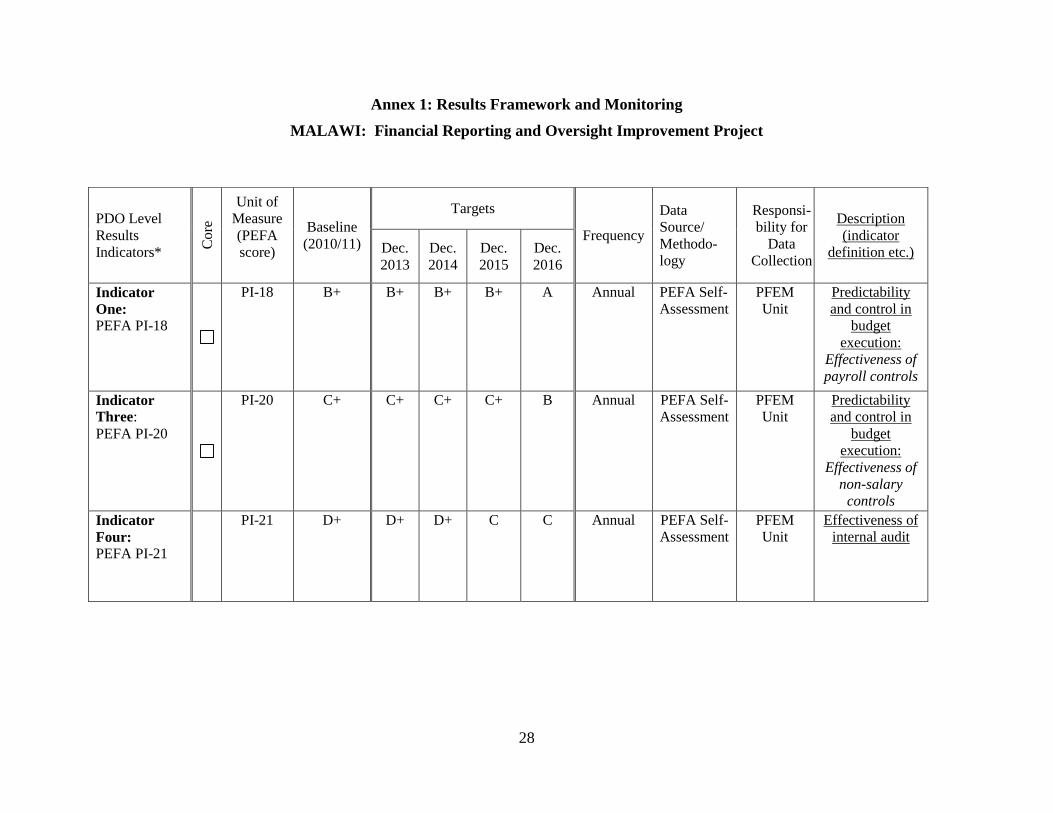

Annex 1: Results Framework and Monitoring...............................................................................28

Annex 2: Detailed Project Description ..........................................................................................30

Annex 3: Implementation Arrangements .......................................................................................39

Annex 4: Operational Risk Assessment Framework ………………………………….….…….53

Annex 5: Implementation Support Plan ……………………………………….…………..…….56

Annex 6: Project Component Cost Table ………………………………………………….. …..58

Annex 7 Country at a Glance ……………………………………………………….....…… …..59

6

PAD DATA SHEET

REPUBLIC OF MALAWI

Financial Reporting and Oversight Improvement Project

PROJECT APPRAISAL DOCUMENT .

AFRICA

AFTME

.

Basic Information

Date: 28 February, 2013 Sectors: Central Government Administration

(70%) and Local Government

Administration (30%)

Country Director: Kundhavi Kadiresan Themes: Public expenditure, financial management

and procurement (50%), Other

accountability/anti-corruption (50%)

Sector Manager/Director: Patricia Mc Kenzie /

Edward Olowo-Okere

EA

Category:

C - Not Required

Project ID: P130878

Lending Instrument: Technical Assistance

Grant

Team Leader(s): Pazhayannur K.

Subramanian

Joint IFC:

.

Borrower: Republic of Malawi

Responsible Agency: Ministry of Finance

Contact: Newby Henry Kumwembe Title: Principal Secretary Administration,

Ministry of Finance

Telephone No.: 265-1788-211 Email: [email protected]

.

Project Implementation Period: Start

Date:

11 March-2013 End

Date:

30-June-2016

Expected Effectiveness Date: March 11, 2013

Expected Closing Date: June 30, 2016 .

7

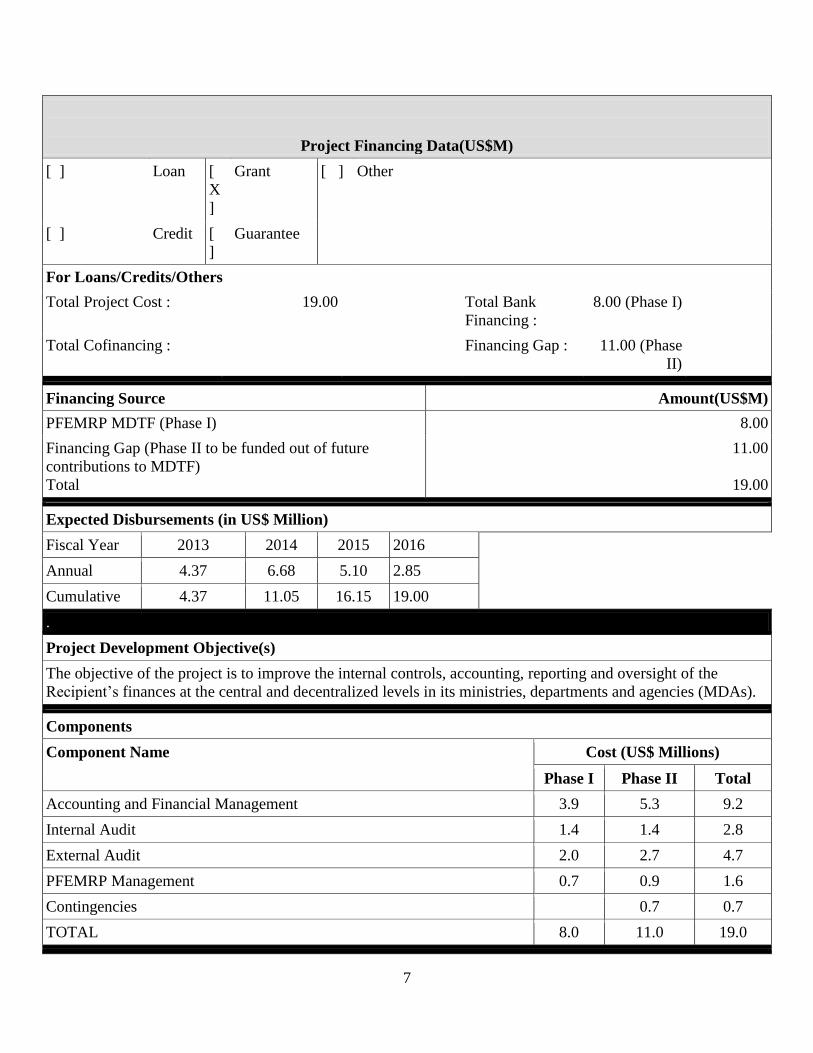

Project Financing Data(US$M)

[ ] Loan [

X

]

Grant [ ] Other

[ ] Credit [

]

Guarantee

For Loans/Credits/Others

Total Project Cost : 19.00

Total Bank

Financing :

8.00 (Phase I)

Total Cofinancing :

Financing Gap : 11.00 (Phase

II)

.

Financing Source Amount(US$M)

PFEMRP MDTF (Phase I) 8.00

Financing Gap (Phase II to be funded out of future

contributions to MDTF)

Total

11.00

19.00 .

Expected Disbursements (in US$ Million)

Fiscal Year 2013 2014 2015 2016

Annual 4.37 6.68 5.10 2.85

Cumulative 4.37 11.05 16.15 19.00

.

Project Development Objective(s)

The objective of the project is to improve the internal controls, accounting, reporting and oversight of the

Recipient’s finances at the central and decentralized levels in its ministries, departments and agencies (MDAs). .

Components

Component Name Cost (US$ Millions)

Phase I Phase II Total

Accounting and Financial Management 3.9 5.3 9.2

Internal Audit 1.4 1.4 2.8

External Audit 2.0 2.7 4.7

PFEMRP Management 0.7 0.9 1.6

Contingencies 0.7 0.7

TOTAL 8.0 11.0 19.0 .

8

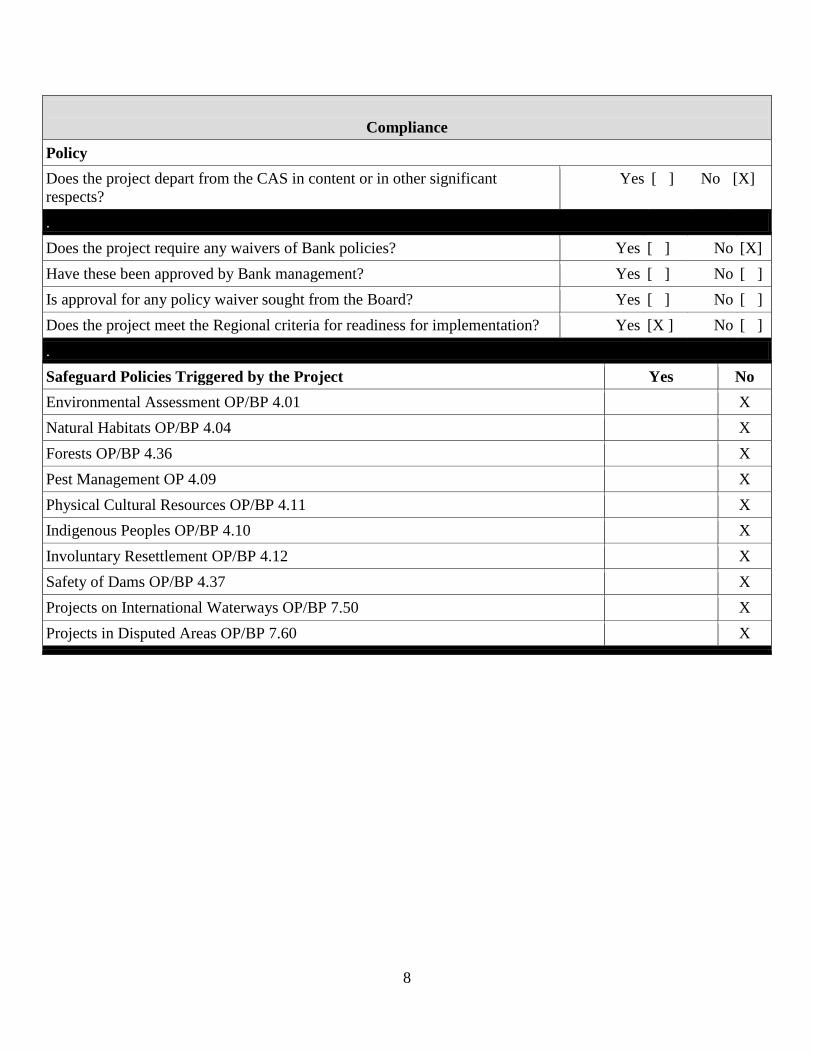

Compliance

Policy

Does the project depart from the CAS in content or in other significant

respects?

Yes [ ] No [X]

.

Does the project require any waivers of Bank policies? Yes [ ] No [X]

Have these been approved by Bank management? Yes [ ] No [ ]

Is approval for any policy waiver sought from the Board? Yes [ ] No [ ]

Does the project meet the Regional criteria for readiness for implementation? Yes [X ] No [ ]

.

Safeguard Policies Triggered by the Project Yes No

Environmental Assessment OP/BP 4.01 X

Natural Habitats OP/BP 4.04 X

Forests OP/BP 4.36 X

Pest Management OP 4.09 X

Physical Cultural Resources OP/BP 4.11 X

Indigenous Peoples OP/BP 4.10 X

Involuntary Resettlement OP/BP 4.12 X

Safety of Dams OP/BP 4.37 X

Projects on International Waterways OP/BP 7.50 X

Projects in Disputed Areas OP/BP 7.60 X .

9

Legal Covenants

Name Recurrent Due Date Frequency

1. Covenants applicable to project

implementation

Yes 1 to 3 months after

effectiveness

Ongoing

Description of Covenant

Clause B-4, Section II, Schedule 2 of the GA: The Recipient shall, by no later than three (3) months after the

Effective Date, select, engage and thereafter maintain throughout the period of project implementation, an

independent firm of professional auditors for purposes of auditing the project financial statements, with

qualifications and experience acceptable to the Association, and under terms of reference satisfactory to the

Association.

2. Effectiveness Condition No When condition

fulfilled

N/A

Description of Covenant

Section 4.01 of the GA: The project shall not become effective until satisfactory evidence has been furnished to

the World Bank that GoM has adopted the Project Implementation Manual acceptable to the World Bank.

3. Disbursement Condition on Part 3

(External Audit) of the Project

Yes When condition

fulfilled

N/A

Description of Covenant

Clause B-1 (b), Section IV, Schedule 2 of the GA: The Recipient shall appoint and maintain throughout the

project implementation, the Auditor General, with qualifications, experience and terms of reference satisfactory to

the World Bank.

4. Retroactive Financing No By effectiveness N/A

Description of Covenant

Section IV.B. 1(a) of GA: No withdrawal shall be made for payments made prior to the date of the Financing

Agreement, except that withdrawals up to an aggregate amount not to exceed $800,000 may be made for

payments made prior to this date but on or after April 1, 2012, for Eligible Expenditures under the Project.

.

10

Team Composition

Bank Staff

Name Title Specialization Unit UPI

Pazhayannur K.

Subramanian

Lead Financial

Management Specialist

Team Lead AFTME 80879

Michael John Jacobs Consultant Audit AFTME 237117

Annie Kaliati Jere Team Assistant Team Assistant AFMMW 290712

Steven Maclean Mhone Procurement Specialist Procurement AFTPE 318342

Khuram Farooq Consultant Accounting and

IFMIS

AFTME 342060

Trust Chamukuwa

Chimaliro

Financial Management

Specialist

Financial

Management

AFTME 382028

Nneoma Nwogu Counsel Legal LEGAM

Luis Schwarz Senior Finance Officer Disbursement CTRLA 82804

Non Bank Staff

Name Title Office Phone City

Twaib Ali Deputy Director, PFEM

Unit

+265-1-789337 Lilongwe

Patrick Liphava Principal Economist,

PFEM Unit

+265-999006250 Lilongwe

Elliam Kadewele Economist, PFEM Unit +265-999332705 Lilongwe

Andrew Tench PFM Advisor, MoF +265-1-788910 Lilongwe

.

Locations

Country First

Administrative

Division

Location Planned Actual Comments

Malawi MoF Lilongwe .

11

I. STRATEGIC CONTEXT

A. Country Context

1. Malawi is a landlocked low income country with an estimated Gross National Income per

capita of US$340 (in 2011), registering an average real GDP growth rate of about 7% per annum

for the last five years. It is also one of Southern Africa's most densely populated countries, with

an estimated population of 14.9 million as of 2010 and a significant percentage (50.7%) of them

currently live under the 1.25 dollar-a-day income poverty line. Income inequality also remains

high reflecting profound inequities in the access to assets, services and opportunities across the

population.

2. Until 2010, Malawi experienced solid growth through prudent macroeconomic policies

and a supportive donor environment. This performance was built on strong stabilization policies

since 2004, and the debt relief from the Heavily Indebted Poor Countries (HIPC) initiative which

helped to improve public expenditure management and created the fiscal space needed to

generate the momentum for growth. Growth was largely driven by high agricultural exports, and

rising Foreign Direct Investment (FDI) inflows related to mining and Government spending.

3. In early 2012 it was estimated that 2011 real GDP had slowed to about 1.4 percent. The

new Joyce Banda government has taken decisive policy measures to arrest the slowdown in the

economy and is already implementing a comprehensive package of economic reforms. These

reforms aim to address the current external imbalances with plans to cushion the vulnerable poor

against the impact through social protection programs, and facilitate a growth rebound in the

short term. In this regard, some decisive and credible measures have been taken by the

authorities to strengthen economic governance, while at the same time signaling to development

partners and the private sector of government's commitment to create a favorable environment

for a return to positive growth. Early indications are that the policy reforms are bearing fruit, as

many external credit lines have resumed and there is growing evidence of renewed confidence in

the management of the economy by private investors. The authorities are also committed to a

program of fiscal consolidation in their 2012/13 budget, while ensuring there is some room to

promote a private sector rebound.

4. The swift movement of President Banda’s government to approve changes and to repair

relations with donors and international financial institutions has put Malawi on a firm position to

regain macro-economic balance and return to a positive growth path. The policy reform

measures undertaken recently would now allow for a relatively quick return to a growth path that

is in line with Malawi's recent historical trend. The government's efforts to restrain fiscal and

monetary policy, in support of the recent devaluation of the Kwacha and adoption of a flexible

exchange rate regime, will support the quick recovery if sustained.

5. The Second Malawi Growth and Development Strategy (MGDS II) 2011-2016, which is

the country's second medium term plan, was approved by the Cabinet in April 2012. The MGDS

II is a medium term strategy designed to attain Malawi's long term aspirations as spelt out in its

Vision 2020 and strives to foster a more inclusive job creating growth to address the

unemployment problem as well as reduce poverty. The strategy reflects a general consensus on

12

the country's broad goals for growth, social equity, and governance. The MGDS II was

developed in an all-inclusive process. All levels of society, including women, the youth, private

sector, civil society and development partners were all involved in the MGDS II consultation

process. To respond to the need to accelerate the economic recovery process, the Government

has reprioritized the interventions in the MGDS II and has come up with a short term Economic

Recovery Plan, which was launched in late September 2012, focusing on short term measures to

restore macroeconomic stability while mitigating the impact on the poor.

B. Sectoral and Institutional Context

6. The Government of Malawi (GoM) has been reforming its public financial management

systems over the last ten years. While this has yielded significant improvements in the legal

framework, IT systems and budget procedures, the full benefits of these reforms have not yet

been felt in terms of aggregate fiscal discipline, strategic allocation of resources and effective

service delivery. The authorities and development partners recognize the need to move to a new

phase of the reforms focused in greater implementation of the new rules and regulations, tighter

internal controls, greater attention to the benefits of public financial management (PFM) reforms

for Ministries, Departments and Agencies (MDA) and sectors and capacity development in the

various PFM institutions. The management of the PFM system is mainly concentrated within the

Ministry of Finance (MoF). Within the Ministry, the Secretary to the Treasury has a key

responsibility for budget planning and execution, while the Accountant General has

responsibility for producing timely and appropriate management and financial accounts. Within

MDAs it is the Controlling Officers who have overall responsibility for effective PFM.

7. The PFM reforms were being supported previously by donors through the Common

Approach to Budget Support (CABS) Group which has been providing assistance to the GoM

since 1997. With support from CABS suspended until 2005, since then many development

partners other than the CABS group are also providing support to the reforms and many more are

expected to join in these efforts. The reform efforts are coordinated between the Government of

Malawi and donors through Group on Finance and Economic Management (GFEM) meetings

that are jointly chaired by the Secretary to the Treasury and a representative from the donors.

Through the Financial Management Transparency and Accountability Project (FIMTAP)

financed by the World Bank and the European Union, capacity development assistance was

provided to Internal Audit, External Audit and the Office of the Director of Public Procurement.

The project also supported the acquisition, installation and operationalization of the IFMIS, the

Government Wide Area Network and general governance improvement among others. Through

the Malawi Social Action Fund (MASAF), the Bank helped in building capacity including FM

capacity at the District Level. There were also significant contributions to PFEM reform from

DfID, Norway, GIZ, UNDP and the EU. The EU Capacity Building Project for Economic

Management and Policy Coordination was instrumental in developing the Public Finance and

Economic management (PFEM) reform program and strengthening capacity in both the MOF

and the Ministry of Economic Development and Planning.

8. Though progress has been registered in several areas, there is much more to achieve.

Progress has indeed been made on many of the activities in the PFEM Action Plan during the

period 2006-2011 but many activities are well behind initial target dates and insufficient

attention and resources have been given to identifying and resolving bottlenecks. Several reforms

13

and improvements have been introduced but were uncoordinated and implementation lags

behind. It is evident that there needs to be a consolidation of what has been introduced and for a

more thorough attention to implementation with an assured stream of resources. A more

comprehensive approach has been established to provide strategic direction through a sector

wide approach to PFEM reforms. The government therefore introduced a PFEM Reform

Program (PFEMRP) and the support is being provided using a common basket funding

mechanism through the PFEMRP Multi Donor Trust Fund (MDTF) administered by the World

Bank (TF071796). PFEMRP is aimed at improving GoM’s macro-fiscal management,

accountability and transparency in public financial management and public oversight.

Interventions and support happening outside the MDTF are tracked using a PFM support matrix

maintained by the PFEM Unit and updated from time to time through discussions during the

GFEM meetings. PFEMRP covers ten reform areas (planning and policy analysis, resource

mobilization, budgeting, procurement, accounting and financial management including internal

audit, cash and debt management, parastatal financing, monitoring and reporting, external

auditing, and program management). This project covers three main areas out of the PFEMRP

namely accounting and financial reporting, internal and external audit and program management.

This has been decided as the immediate focus areas by the government and the MDTF partners

based on priority, available resources, and component readiness.

9. The GFEM, originally a donor grouping, was transformed in 2006 to a joint donor GOM

forum. This provides a management steer of PFM reform through participation of both GoM and

donors. It is now co-chaired by the Secretary to the Treasury and a head of a development

agency on a rotating basis. The Ministry of Finance recognized the importance of developing a

facilitating unit for PFEM reforms and acting as a secretariat, and thus set up a PFEM Unit in

2008. This was formally established through the Ministry of Finance functional review in 2010.

With this establishment of a unit to deal with PFEM, it became possible to consider developing a

more structured approach to PFEM reform. In addition to the GFEM there is a Government

PFEM Steering Committee of senior management which approves PFEM programs which are

developed and monitored by a PFEM Technical Committee.

10. Reform reviews have shown that PFM reform requires strong political commitment,

implementation designs tailored to the country context and government led coordination

arrangements. The FROIP Trust Fund will be managed by a high level unit in the Ministry of

Finance and the project design is derived from the GoM’s comprehensive Public Finance and

Economic Management Reform Program (PFEMRP) which has culminated from an increasing

awareness within GoM for overall PFEM reforms and have been guided by the results of the

Public Expenditure and Financial Accountability (PEFA) assessments.

11. Overall, four PEFA assessments have been conducted in Malawi in 2005, 2006, 2008 and

2011. The 2011 PEFA assessment was based on an analysis of performance for the years from

2007-08 to 2009-10. The main findings relating to budget execution, accounting and financial

reporting and internal and external oversight are summarized next.

12. Predictability and control in budget execution:

Reforms are on-going in the Malawi Revenue Authority

14

The Ministry of Finance has improved the cash management process

Debt management and payroll system are being operated efficiently

The procurement system continues to be unable to provide statistics with regard to the

implementation and comprehensiveness of competitiveness in public procurement

The Integrated Financial Management Information System (IFMIS) rollout process has

been concluded to the central government and 34 local councils

Although awareness seems to be rising with regards to internal control, the evidence does

not yet support the finding of improved control and internal audit procedures and

processes being implementing and taking effect.

13. Accounting, recording and reporting: Progress in the period under review has featured the

improved timeliness of the closure of the accounts and the production of the financial statement

for audit. Also, in-year budget execution reports are produced on a timely basis and with some

improvements is quality. However, management information at service delivery units still needs

to improve. A serious control concern identified is the backlog in bank reconciliations since July

2010. Timely bank reconciliation is an essential discipline in the ongoing checking and

verification of accounting practices across Government and it also provides assurance as to the

integrity of data used for reporting.

14. External scrutiny and audit: The period covered by this assessment has seen a backlog of

external audits and Public Accounts Committee (PAC) scrutiny cleared. However, there are still

weaknesses in the actions and follow up based on the recommendations of the National Audit

Office (NAO) and PAC. In summary, NAO and PAC scrutiny has been characterized by periods

when there has been no public scrutiny followed by intense activity to clear backlogs. In respect

of the Parliamentary Finance Committee, there is more opportunity for scrutiny of the draft

budget than for budget execution.

C. Higher Level Objectives to which the Project Contributes

15. The project objective is clear, relevant and important to Malawi as articulated in the

MGDS II consistent with FY13/16 CAS and is fully aligned to the Africa Regional Strategy. It is

also consistent with strategies of the various donors contributing to the MDTF and the

framework for CABS. It is designed to help the Government achieve improved public service

delivery through strengthened public sector management systems. In achieving these outcomes,

the CAS provides for joint efforts with other development partners and has accommodated the

multi donor approach to supporting PFM reforms. In terms of policy areas, the projects under

PFEMRP will contribute towards restoring prudent fiscal policy and sound macroeconomic

management. They are consistent with the ‘governance and public sector capacity’ cross

cutting/foundational pillar of the Bank’s Africa Strategy. By strengthening human and

institutional capacity in the public service, front line service delivery will improve, thereby

indirectly addressing the cross cutting issue of capacity development in MGDS II. The renewed

engagement with Malawi by development partners includes pilot use of national PFM systems

and the project is important to assist to develop the necessary PFM assurance.

15

II. PROJECT DEVELOPMENT OBJECTIVES

A. PDO

16. The objective of the Project is to improve the internal controls, accounting, reporting and

oversight of the Recipient’s finances at the central and decentralized levels in its ministries,

departments and agencies (MDAs). Achievement of the objective will be assessed through

impact on relevant PEFA performance indicators.

Project Beneficiaries

17. The main stakeholders in this project are the ministries and budget users of the

implementing departments, agencies and districts and the beneficiaries of the results of the

internal and external audits since better oversight and management of funds means that more

resources will be available for good use across government programs. Consultations were held

with these stakeholders to understand the gaps with a view to tailor components to address the

existing deficiencies. It is also expected that the citizens of Malawi will benefit from more

effective service delivery facilitated by these reforms.

PDO Level Results Indicators

18. PEFA assessments of central government which includes the many tasks decentralized to

the districts in Malawi were carried out in 2005, 2006, 2008, and 2011. The PEFA assessments

have made an important contribution to the shaping and implementing of reforms and

improvements to the PFM system, and the GoM has expressed strong interest in using the results

of the 2011 PEFA assessment to help shape its future reform agenda. The achievement of the

project's overall development objectives will be measured by regular focused assessments of the

following key outcome indicators using the PEFA framework:

• Improved effectiveness of payroll controls and non-salary controls as measured by PEFA

PI-18 and PI-20.

• Improved compliance with rules as measured by PEFA PI-20

• Improved effectiveness of internal audit as measured by PEFA PI-21

• Improved information on resources received by service delivery units as measured by

PEFA PI-23

• Improved quality and timeliness of annual financial statements as measured by PEFA PI-

25.

• Improved scope, nature, and follow-up of external audit as measured by PEFA PI-26

• Improved scrutiny and response to external audit reports as measured by PEFA PI-28

• Improved service delivery resulting from PFM reform interventions to be defined during

the first two quarters of project implementation

16

III. PROJECT DESCRIPTION

A. Project Components

19. .This project is conceptualized to respond to the PFEMRP by focusing on improving the

Integrated Financial Management System (IFMIS) and oversight functions of internal and

external audit for better implementation of the rules and regulations, fuller utilization of IFMIS

functionalities and improved service delivery. The components for this project have been chosen

based on the joint priorities of the government and MDTF partners and readiness to implement.

The project is scalable and Phase I covers some urgent technical assistance, training and goods

procurement. The intention is to expand the reach of the project activities to Phase II with

subsequent funds once they are received.

20. Accounting and Financial Management (Component 5 of PFEMRP) US$9.2 million

(US$3.9 million in Phase I and US$5.3 million in Phase II) - This component is to improve the

systems and controls for accounting and financial management.

21. Sub-component 1- Accounting and IFMIS (Component 5.1 and 5.2 of PFEMRP) - This

sub-component would assist the Government to improve the efficiency and comprehensiveness

of Government accounting and financial management systems in its MDAs, the compliance with

the rules and regulations, and the comprehensiveness, transparency, and timeliness of fiscal

reporting. Following a yet to be concluded review of business process and functional

requirements (funded separately by EU with the consultants expected to be on board in

November, 2012), this is expected to be achieved in phases. Though phasing of activities will be

adjusted over the course of the project implementation to flexibly respond to the evolving ground

realities, a broad sequencing of activities is planned around two phases.

Phase 1 will cover: (i) the automatic capture of all Government revenues, expenditures

and financing transactions in IFMIS; (ii) ‘interfacing IFMIS with the Central Bank to

foster automation and hence efficiency in reconciliations’; (iii) implementation of an

electronic payments system (iv) implementation of Cash Basis International Public Sector

Accounting Standards (IPSAS); (v) harmonization of integrated financial management

systems at central and district levels; (vi) review of annual budgeting, accounting and

reporting processes and associated controls to be implemented through subsequent

upgrading of IFMIS to a web based version with comprehensive coverage of all relevant

modules and interfaces; (vii) purchase of new licenses if EPICOR or Serenic Navigator

(SN) softwares do not meet government requirements and ; and (viii) consulting services

to analyze expenditure arrears and make recommendations;

Phase 2 will cover: (i) roll out of budgeting module to all the MDAs; (ii) devolution of

financial management responsibility to MDAs; (iii) implementation of fixed assets

register, (iv) roll-out of business intelligence and reporting tools to select users of all the

MDAs and (v) decentralization support.

Activities that will stagger across both phases include: (i) getting government's core

IFMIS team trained in relevant technical certificate courses, (ii) improving the

competency of the accountancy service; (iii) developing the management skills to run

IFMIS effectively; and (iv) hiring of technical support staff for sustainability of the

IFMIS.

17

22. Sub-component 2 – Payroll Management (Component 5.1 of PFEMRP) - The Payroll

Management subcomponent would cover: (i) Business processes re-engineering, including

automated posting to IFMIS General Ledger through interface, follow up and cataloguing of all

processes including descriptions of operations and controls; (ii) roll-out of payroll system to the

regions; (iii) Improvement of quality of staff through specialized training for system

administrators and managers, and user training for users from various MDAs; and (iv) Adequate

audit coverage of payroll, (v) Development of payroll interface by Accountant General

Department (AGD); (vi) hardware support for decentralization of payroll operations to three

districts and (vii) support the establishment of Disaster Recovery (DR) center for payroll. This

could best be achieved through the cooperation of Department of Human Resource Management

and Development (DHRMD) staff and internal auditors in the various MDAs.

23. Sub-component 3 – IFMIS Roll out to districts (Component 5.1 of PFEMRP) – This

component would cover activities not included in GIZ funding to National Local Government

Financing Committee (NLGFC) associated with IFMIS roll-out to 8 remaining councils,

including purchase of servers and other hardware for back-up and disaster recovery, procurement

of generators, furniture, air-conditioners and networking, VPN Connectivity, laptops for

technical support team, technical training for database administrators and networking specialists.

24. Component 2 - Internal Audit (Component 5.3 of PFEMRP) US$2.8 million (US$1.4

million in Phase I and US$1.4 million in Phase II) - This component would focus on supporting

the Central Internal Audit Unit (CIAU) in further development of the Internal Audit Service

within the PFEMRP through: (i) Improvement of the governance and legal framework to provide

a wider range of internal audit services; (ii) Capacity building of the CIAU including the

development of a human resource development plan, support for the recruitment, retention and

training of CIAU staff; (iii) Establishment of quality assurance arrangements for high quality

audits and reports; (iv) Development and implementation of a system for reporting internal audit

performance to the CIAU and coordination with stakeholders.

25. Component 3 - External Audit (Component 9 of PFEMRP) US$4.7 million (US$2

million in Phase I and US$2.7 million in Phase II) - This component would focus on

strengthening the operational capacity of the National Audit Office (NAO) through:

i. Delivery of high quality and timely audit services by re-engineering audit procedures

through revision of audit manuals and training staff in new procedures including conduct

and reporting of regularity audit, performance audit, procurement audit and revenue

audit;

ii. Advising on appropriate conditions of service and training policies for competent and

motivated staff, supported by IT software for audit management and conduct;

iii. Provision of vehicles and computers for auditor operations;

iv. Provision of effective communication facilities for improved audit management and audit

reporting arrangements; and

v. Increased independence and accountability for the NAO in line with the independence

principles of ISSAI 10 of the International Standards for Supreme Audit Institutions,

annual audit of NAO, and stronger dialogue with stakeholders including PAC and donors.

18

26. Component 4 - PFEMRP Management (Component 10 of PFEMRP) US$1.6 million

(US$0.7 million in Phase I and US$0.9 million in Phase II) - The objective of the component is

to manage the agreed development program, provide procurement and financial management

support to the implementing departments and to monitor the objectives and performance against

the indicators. The PFEM unit will also be responsible for the financial management of the

overall trust fund program. Capacity building is required both in terms of staff training and also

additional appointments to support the main functions of the Unit. Main activities will include;

(i) procurement of full complement of professional staff required for the Unit either through

transfer from other units or through contract appointment; (ii) purchase of any office equipment

urgently required and incremental operating costs; (iii) training in program and project

management and procurement and/or financial management as required; (iv) annual audit of the

project by independent auditors; (v) supporting the development of ICT to enhance

communication with the other PFEM Institutions; (vi) facilitating the undertaking of PFEM

studies, reviews and assessments; and (vii) facilitating development and appraisal of remaining

components of the PFEMRP.

B. Project Financing

Lending Instrument

27. The project is an estimated US$8 million operation which is scalable to US$19 million which

will be financed by the PFEMRP Multi Donor Trust Fund administered by the World Bank.

This will be a grant executed by the Government of Malawi. To accommodate for the currently

available funds and the future pledges and funds flow to the MDTF, the project implementation

will be carried out in two phases – the first phase for a total amount of US$8 million and the

second phase for the remaining US$11 million. The initial Grant Agreement between the World

Bank with the Government will be for US$8 million which will be amended based on future

funds commitments to the MDTF.

Project Cost and Financing

28. The project costs are as follow:

Project

Components

Project Costs

(millions of US$)

MDTF Financing (millions of US$) % Financing

Phase I Phase II

1. Accounting and

Financial

Management

9.2 3.9 5.3 100

2. Internal Audit 2.8 1.4 1.4 100

3. External Audit 4.7 2.0 2.7 100

4. PFERMP

Management

1.6 0.7 0.9 100

Contingencies 0.7 0.7 100

Total Project

Costs

19.0 8.0 11.0 100

19

C. Lessons Learned and Reflected in the Project Design

29. The project design should be simple and designed for easy implementation and should

take into account the absorptive capacity of the country and the prevailing political context. The

Financial Reporting and Oversight Improvement Project (FROIP) design has been a country

product with limited guidance from the Bank. A long term in country Advisor has assisted the

GoM. The design and investment in IT infrastructure should anticipate expansion needs. The

consultant in IFMIS has long experience in this issue. FROIP includes substantial training aimed

at improving implementation capacities of relevant counterpart and implementing government

staff.

30. Capacity building should be centrally managed. FROIP has a project management unit in

the MoF. Project design should take account of grant financing from donors, which requires

more flexible design of capacity building activities. This will minimize duplication of efforts,

and encourage cost effectiveness. FROIP is funded through a Multi Donor Trust Fund with a

managing committee which will approve and monitor expenditure abased on agency request.

This will provide flexibility and control. Previous expenditures have been judged ineligible

because of differing perceptions on the provisions of allowances. The project will be clear on the

criteria for providing allowances and expenses will be closely monitored by the committee.

31. Changes in political economy are not predictable, but could be better adapted to if project

design allowed greater flexibility in implementation. It is pertinent therefore, to constantly

evaluate and adapt to change in circumstances to better maneuver public management reform

programs. The project management unit will adapt the project to such developments.

32. Recruiting specialists for M&E, IT, financial management, and procurement in the

implementing agency at the beginning of the project is very important so that there will not be

lack of skills in these matters, and implementation delays can be avoided. FROIP will address

this.

33. Inter-ministerial and donor coordination is crucial to the success of project

implementation. The MDTF management arrangement addresses this.

34. M&E technical committee meetings and annual and quarterly work plans are essential

tools for monitoring the progress of project activities. Further, regular guidance from the steering

and technical committees will facilitate smooth project implementation.

35. Based on the FIMTAP report, continuity of the team working on the project, especially

the Task Team Leader (TTL), is very important both for the Bank and the Borrower. Task

leadership of a complex project should be entrusted to senior and more experienced Bank staff,

and not to a fresh or newly recruited staff who does not have any operational experience with the

Bank projects. The FROIP is to be led by a very experienced Bank officer.

20

IV. IMPLEMENTATION

A. Institutional and Implementation Arrangements

36. The individual components will be managed by senior officers responsible to the heads of

the relevant agencies – Accountant General, Auditor General, Internal Audit Director and Head

of PFEM Unit. The project is being implemented within the framework of the PFEMRP and will

be overseen by the PFEM unit in the MoF which will also be responsible for centralized

procurement, financial management and monitoring of the overall trust fund program. Special

arrangement will be made to ensure that the independence of the National Audit Office is

respected in consultation with the MDTF partners and the NAO. Capacity building will be given

to this unit both in terms of staff training and also additional appointments to support its main

functions.

37. Project implementation arrangements have been derived from the governance

arrangements set up for the PFEMRP as a whole and will consist of: (i) PFEM Steering

Committee; (ii) PFEM Technical Committee (PFEMTC); (iii) Technical Working Groups

(TWGs) and (iv) PFEM Unit (PFEMU). In addition to this, there is also a Joint Government

Donor Committee.

PFEM Steering Committee (PFEMSC): This is the highest level government body that

provides strategic policy guidance and oversight of Malawi's overall PFEM program. The

PSC is chaired by the Secretary to the Treasury with PFEM Unit providing secretariat

services. The PFEMSC has representation from key PFEM institutions with the PS

Economic planning and Development, Office of the President and Cabinet (OPC)-PS

Finance, OPC-PS Public Sector Reform, PS DHRMD, PS Local Government and Rural

Development (LG&RD), Auditor General, Accountant General, Director-Office of the

Director of Public Procurement (ODPP), Executive Secretary NLGFC, Commissioner of

Statistics, Commissioner General of Malawi Revenue Authority (MRA), Chairperson of

the PFEM TC. The committee meets semiannually to review progress on the PFEM

reform program outcomes and to adjust and amend the strategy and work program as

necessary.

PFEM Technical Committee (PFEMTC): PFEM Technical Committee is presently

chaired by the Director, Debt and Aid Division (DAD) and consists of directors of all

divisions in MoF, senior officers of the other organizations represented at the PFEM

Steering Committee (PFEMSC) as members; the PFEM Unit acts as secretariat to this

committee. Apart from the above, membership of the PFEMTC would include

Component Coordinators and representatives from line ministries and other relevant

officials as the Chair considers necessary including representatives of the MDTF donors

and the TF Administrator. PFEMTC meets every two months and its functions include

oversight of PFEM activities and review of the implementation progress of projects under

PFEM RP MDTF with inputs from the TWGs. They will report to the PFEMSC and will

ensure that implementing units comply with the policy guidelines as directed by

PFEMSC. PFEMTC can also call technical meetings with the participation of other

project representatives and DP's technical teams to discuss issues of cross cutting nature

and interface among the projects.

21

Technical Working Groups (TWGs): In the PFEM RP there are 10 proposed working

groups which would pursue the technical work of the PFEM RP. There may be others as

required for effective implementation of the PFEMRP. Currently, there are seven TWGs

operating - those for Audit, IFMIS & Financial Reporting, Macroeconomic forecasting

(also known as the National Accounts group), Cash Management, Procurement,

Domestic Revenue and Public Expenditure Reviews. The TWGs relevant to this project

(Audit and IFMIS) will provide technical input and participate in the preparation,

appraisal and monitoring of the project. TWGs are chaired by the Directors heading the

relevant technical department/unit. Membership of the TWGs will be expanded to

include Directors, Component Coordinators and representatives from line ministries and

other relevant officials as the Chair considers necessary and the representatives of the

MDTF donors and the TF Administrator. They will report to the PFEMTC and will

ensure that implementing units/departments comply with the policy guidelines as directed

by the PFEMTC and PFEMSC. TWGs will hold monthly review meetings. Their

specific responsibilities include: (a) preparation for relevant project appraisal and review

of progress reports towards the project's objectives; (b) preparation and submission of

annual work plans, budgets and procurement plans to PTC, PSC, and Donor Project

Team; (c) review of agreed performance targets; (d) analysis of implementation issues for

achieving key outputs; and (e) identification of critical risks that could hinder efficient

implementation of project activities and draw risk mitigation measures.

PFEM Unit (PFEMU): The PFEM Unit will be the key unit which facilitates the

PFEMRP. It also acts as secretariat to the various committees and it will provide support

for managing the day to day financial management and procurement transactions of the

projects. The PFEMU will be staffed with government officials and will include Deputy

Director who will report to the Director and the PS Administration who has overall

responsibility for PFEM RP and Specialists in Procurement, Financial Management and

M&E. The main functions of the PFEMU will be to: (i) provide logistical support and

guidance to the project teams and component coordinators; (ii) compile work programs

from the various working groups, budgets and procurement plans for each project; (iii)

monitor project implementation and prepare progress reports for the PFEMTC and

PFEMSC; (iv) submit consolidated annual work programs, budget and procurement plans

for review and endorsement by the PFEMTC and PFEMSC; (v) hold regular meetings

with focus groups and component coordinators to ensure appropriate linkage in the

activities under various components; (vi) maintain project accounts, manage designated

accounts and prepare project financial statements; (vii) submit withdrawal applications to

the World Bank for replenishment; (viii) make recommendation to the PFEMTC and

PFEMSC on how to effectively implement the agreed work plan; and (ix) carry on

periodic performance evaluation of all long term consultants (both expatriate and local).

Joint Government Donor Committee: This committee will be the main oversight body

for the overall management of the trust fund. The committee will be co-chaired by the

Secretary to the Treasury and the head of one of the contributing development partners to

the MDTF on a rotating basis and will include representatives from MDTF donors,

conveners of TWGs, or their representatives, Principal Accounting Officers or

representatives of the implementing departments of relevant components and the Head of

the PFEM Unit. The main functions of this Committee will be to: (a) review and monitor

22

the implementation of the MDTF in line with GoM’s overall PFEMRP; (b) review and

approve sub-projects submitted for funding out of the MDTF; (c) monitor progress on the

annual MDTF work program/plan, budgetary allocation/funding commitments and

disbursements and any other adjustments that may be necessary. The committee will

meet as needed but no less than semiannually.

Summary of Project Implementation Arrangements

Institution

Unit

Members/Composition Tasks/Responsibilities Reporting

PFEM Steering

Committee

(PFEMSC)

Chaired by the Secretary to the

Treasury. The PFEM Unit,

Ministry of Finance will serve as

the Program Secretariat.

Members: PS Economic Planning

& Development, OPC-PS Finance,

OPC- PS Public Sector Reform,

PS DHRMD, PS LG&RD, Auditor

General, Director ODPP,

Executive Secretary NLGFC,

Commissioner of Statistics,

Commissioner General of MRA,

Accountant General, and

Chairperson of PFEMTC

Provides strategic policy

guidance and oversight of

Malawi’s overall PFEM reform

program

Review progress on the

PFEMRP outcomes

Recommend actions for

modifying work programs/plans

regulations and policy or

implementation arrangements

PFEM Technical

Committee

(PFEMTC)

Chaired by the Director, DADM.

Members: Directors of all

divisions in MFDP (including

MRA and CIAU), senior officers

of organizations represented at the

PFEMSC, Component

Coordinators, representatives from

line ministries, MDTF

Administrator and representative

from MDTF donors

Oversight of PFEM activities

Review of project

implementation progress under

PFEM RP MDTF and provide

necessary guidance

Review and approve annual

work plans, budgets and

procurement plans

Review of agreed performance

targets

Resolve critical risk including

implementation issues

Submit funding proposals to

MDTF Administrator and DPs

- Reports to the

PFEMSC

- Prepares summary

report for PFEMSC

meetings

Technical

Working Groups

(TWG)

There are ten TWGs to pursue the

technical work of PFEM RP.

TWGs are chaired by Directors

heading the relevant technical

department/unit.

Members: Directors, component

coordinators, representatives from

line ministries and other relevant

officials as the Chair considers

necessary and representatives of

MDTF donors and the TF

Preparation for project

appraisal and review of

progress reports

Preparation and submission of

annual work plans, budgets and

procurement plans to PFEMTC,

PFEMSC, and Donor Project

Team

Review of agreed performance

targets

Analysis of implementation

- Reports to the

PFEMTC

- Prepares summary

report for PFEMTC

meetings

23

Administrator. issues for achieving key outputs

Identification of critical risks

that could hinder efficient

implementation of project

activities and draw risk

mitigation measures.

Public Finance

and Economic

Management

Unit (PFEMMU)

Headed by a full time Head of the

Unit who is a serving government

official

Serves as Secretariat of the project

comprising the following: (i)

Project Director, Addl. PD,

Procurement & Finance Specialist,

M & E Specialist, and Technical

component specialists and other

support staff

A team of Management/

Implementation Support

Consultants including long and

short term consultants for

providing TA support as required

Provide logistical support and

guidance to the project teams

and component coordinators

Compile work programs from

the various working groups,

budgets and procurement plans

for each project

Monitor project implementation

and prepare progress reports

for the PFEMTC and PFEMSC

Submit consolidated annual

work programs, budget and

procurement plans for review

and endorsement by the

PFEMTC and PFEMSC

Hold regular meetings with

focus groups and component

coordinators to ensure

appropriate linkage in the

activities under various

components

Maintain project accounts,

manage designated accounts

and prepare project financial

statements

Submit withdrawal applications

to the World Bank for

replenishment

Make recommendation to the

PFEMTC and PFEMSC on how

to effectively implement the

agreed work plan

Carry on periodic performance

evaluation of all long term

consultants (both expatriate

and local).

- Reports to the

Principal Secretary,

Administration,

MoF

- Prepares progress

reports including

financial,

procurement &

monitoring reports

Joint government

DP Committee

Co-chaired by the Secretary,

Treasury and head of one of the

principal donor partners of MDTF

Members: PSC chairs, PDs and

MDTF contributing donors

Jointly review and assess

implementation progress of the

MDTF program overall against

program benchmarks

Review financing decisions

Review disbursements to date

vis-à-vis project delivery status

Discuss and agree annual work

plans, budgetary allocation and

Detailed report on

overall progress of

project implementation

and on performance of

MDTF

24

any other adjustments that

might be necessary

B. Results Monitoring and Evaluation

38. The project’s Monitoring and Evaluation (M&E) framework will be a key instrument to

monitor progress towards achieving the project development objectives and informing the

PFEMTC on project performance including potential bottlenecks as they arise. The M&E

framework presented in Annex 1 captures the high level results that are expected to be achieved

during the life of the project. The periodic performance assessment of the project and the

resulting outcomes will be carried out jointly by the World Bank and the MDTF donors with the

support of the PFEM unit. Apart from this, the government in consultation with MDTF partners

plans to develop lower results indicators to track results in service delivery or improved

efficiency arising out of the proposed interventions. This is proposed to be done during the first

six months of project implementation to come up with a baseline for future tracking.

C. Sustainability

39. The MDTF is being locally managed within the MoF and project components are being

managed by affected agencies. Substantial parts of the project are directed at building staff skills

and capacity and the expansion of the IFMIS is to be undertaken in phases that will be adjusted

over the course of the project implementation to flexibly respond to evolving ground realities.

Although the project focuses on delivery though the use of external consultancies, the

consultants will work closely with the staff and deliver training and transfer learning as needed.

In addition to including this in consultants ToRs, the review mission teams would carry out

periodic checks to ensure that this is being achieved during the period of the project so as to give

room for taking necessary action where it is not being done. This should ensure that the

increased capacity would be retained in the ministries impacted by the TA interventions. Where

the activity is geared towards the building of information databases and the building of analytical

models, the training will also ensure that the staff would be able to update and maintain these

tools. In the area of Accounting and IFMIS, much of the proposed support centers on the

development and implementation of systems to remedy shortcomings in the Government's

existing framework, and to support the Government's strategic needs over the next few years.

All of the activities proposed are structured so as to promote sustainability of the systems after

the consultants have completed the design and implementation tasks. In each of these activities,

sustainability will be promoted through the comprehensive documentation of functional and

technical requirements, system design, system configuration and construction, system testing

scripts and testing reports, system policy and procedure manuals, system user guides, system

training plans, system training materials, documentation of historical data loading and migration

documentation. In addition, each consultancy - whether they be system developments or other -

will be structured to include a comprehensive capacity building element including the production

of policy and procedure manuals, training materials and the planning and delivery of a

comprehensive, detailed training program to guarantee the transfer of expert knowledge to GOM

staff and a foundation for the training of future staff recruited into these areas. In addition,

discussions are in progress for the South African Institute of Chartered Accountants (SAICA) to

25

partner with local Malawian universities or training institutions to develop competencies in

accounting and public financial management.

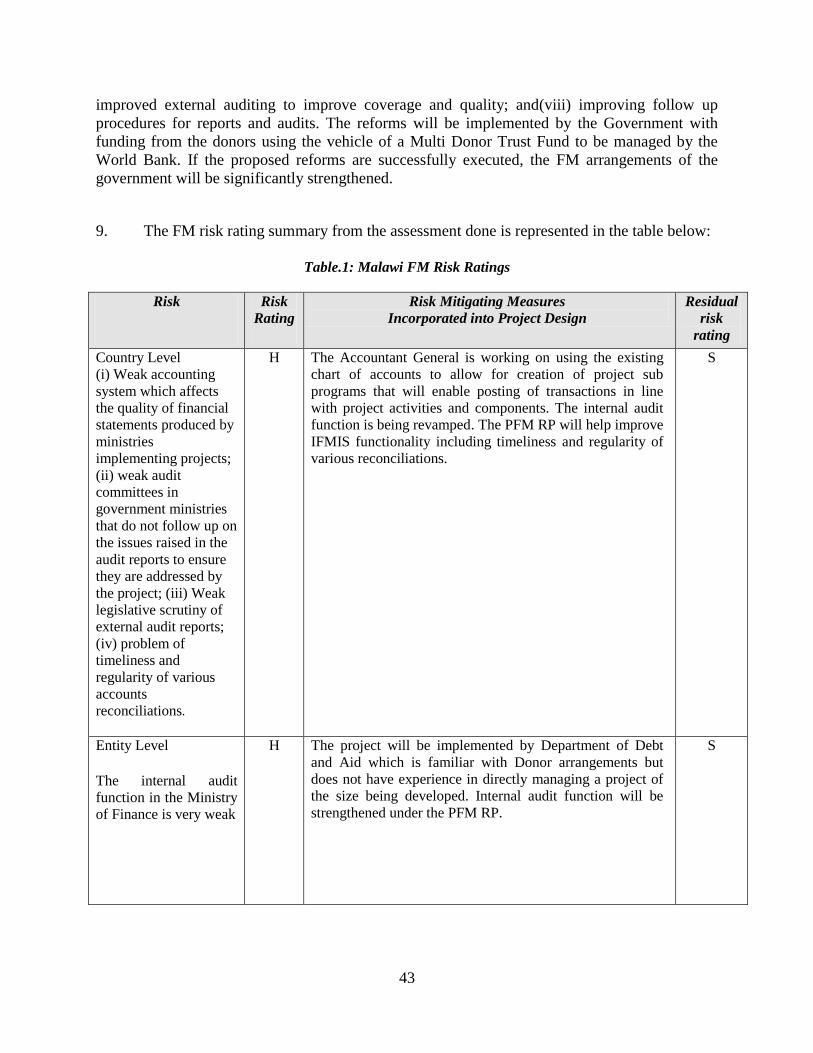

V. KEY RISKS AND MITIGATION MEASURES

A. Risk Ratings Summary Table

Risk Category Rating

Stakeholder Risk Substantial

Implementing Agency Risk

- Capacity Substantial

- Governance Substantial

Project Risk

- Design Substantial

- Social and Environmental Low

- Program and Donor Moderate

- Delivery Monitoring and Sustainability Moderate

- Other (Optional)

- Other (Optional)

Overall Implementation Risk Substantial

B. Overall Risk Rating Explanation

40. Financial management reforms involve changes in rules, processes and systems that

affect the incentives of the decision makers in allocation and use of scarce public resources. This

reform process therefore is a venture with substantial risk. However, these risks are not unique

to the Malawi program and are faced in many countries implementing a similar reform program.

In the case of Malawi, the risks which might affect the successful implementation and

sustainability of this program are: (i) risks due to changing focal point for PFM reforms rated as

substantial; (ii) weak implementation capacity rated as substantial; and (iii) risks due to poor

governance/weak fiduciary environment rated as high. The overall program risk rating during

preparation and implementation is assessed as substantial. The Operational Risk Assessment

Framework (ORAF) in Annex 4 describes the risks and the mitigation measures completed or to

be addressed during implementation.

VI. APPRAISAL SUMMARY

A. Economic and Financial Analyses

41. The project would contribute to the objective of better accounting, and reporting of public

finances using a controlled, secure, and accountable system that is less prone to manipulation.

26

The quality of expenditure audit will be significantly enhanced as a result of the use of modern

techniques in compliance, certification, and performance audits. The project will support better

fiscal and financial management decision making in government; provide timely, comprehensive

and reliable budget execution data to line ministries and other spending agencies; allow for the

timely production of accurate and meaningful financial statements, based on international

standards; raise the capacity and competencies of the manpower responsible for budget

execution, internal auditing, accounting and financial and fiscal reporting, and external auditing.

Although difficult to quantify, each of these factors has a positive economic impact.

B. Technical

42. The program does not involve introduction of complex new technologies and the

implementing agencies and contractors are familiar with these. All technical issues will be

addressed during project appraisal and would include connectivity, capacity, and reliability of

communications links and arrangement for quality control of works implemented by various

contractors.

C. Financial Management

43. The FM systems of the ministry are generally in place to process project transactions and

produce reports as required. The PFEM unit which will be directly responsible for FM

arrangements of the project has adequate number of qualified and experienced staff. The

accounting system being currently used is the automated IFMIS. The same system will be used

for the project. The current chart of accounts in IFMIS does not allow processing transactions in

accordance with project activities or components. An excel spreadsheet will be used to further

analyze information in IFMIS and allow quarterly reporting in compliance with legal

agreements. It is expected that the chart of accounts in IFMIS will later (within one year) be

reconfigured in a manner that will allow project transactions to be processed in line with

activities and components. The mitigation measures that are planned in order to strengthen the

FM arrangements are:(i) FM staff to undergo training in FM and disbursement for World Bank

funded projects; (ii) reconfigure chart of accounts in IFMIS to allow transaction processing in

line with project components; (iii) Strengthen control environment around operation of

automated IFMIS by increasing risk awareness among users of the system; (iv) minimize

frequency of staff transfers and ensure that where that happens replacement is done promptly

with at least equally qualified staff. The details of the assessment are contained in annex.

The Financial Management assessment concluded that the financial management arrangements

meet the Bank’s minimum requirements under OP/BP 10.02. With the implementation of the

financial management action plan, the financial management arrangements for the project will be

further strengthened. The residual risk rating for the department is Substantial.

D. Procurement

44. Procurement under the Financial Reporting and Oversight Improvement Project will be

carried out in accordance with the “Guidelines: Procurement of Goods, Works and Non

Consulting Services under IBRD Loans and IDA Credits& Grants by World Bank Borrowers”

published by the Bank in January 2011; and "Guidelines: Selection and Employment of

Consultants under IBRD Loans and IDA Credits& Grants by World Bank Borrowers” published

27

by the Bank in January 2011. National Competitive Bidding (NCB) will be in accordance with

the Malawi Public Procurement Act of August 2003 which has been reviewed and found

satisfactory to the Bank with a few exceptions. The overall risk of the Ministry of Finance to

carry activities under the project is substantial as currently there is inadequate qualified staff

that can undertake procurement activities under the project using World Bank guidelines and

procedures. The Procurement Section needs to be strengthened by having Technical Assistance

as an interim measure to ensure that procurement capacity is sufficient to meet procurement

demands. Details of the technical assistance required are discussed in the procurement

assessment given in Annex 3. “Guidelines on Preventing and Combating Fraud and Corruption

in Projects Financed by IBRD Loans and IDA Credits and Grants” dated October 15, 2006 and

updated in January, 2011, shall apply to the project.

E. Social (including Safeguards)

45. The project is expected to have positive social impacts through improved credibility on

government financial management. Transparent and accountable management of public

resources will lead to increased civic confidence in government. The computerization of

transactions and processes would lead to better and faster public services delivery.

F. Environment (including Safeguards)

46. As a Category C technical assistance program, the Bank’s environmental safeguard

policies are not triggered.

G. Other Safeguards Policies Triggered (if required)

47. None

28

Annex 1: Results Framework and Monitoring

MALAWI: Financial Reporting and Oversight Improvement Project

PDO Level

Results

Indicators*

Core

Unit of

Measure

(PEFA

score)

Baseline

(2010/11)

Targets

Frequency

Data

Source/

Methodo-

logy

Responsi-

bility for

Data

Collection

Description

(indicator

definition etc.) Dec.

2013

Dec.

2014

Dec.

2015

Dec.

2016

Indicator

One:

PEFA PI-18

PI-18 B+ B+ B+ B+ A Annual PEFA Self-

Assessment

PFEM

Unit

Predictability

and control in

budget

execution:

Effectiveness of

payroll controls

Indicator

Three:

PEFA PI-20

PI-20 C+ C+ C+ C+ B Annual PEFA Self-

Assessment

PFEM

Unit

Predictability

and control in

budget

execution:

Effectiveness of

non-salary

controls

Indicator

Four:

PEFA PI-21

PI-21 D+ D+ D+ C C Annual PEFA Self-

Assessment

PFEM

Unit

Effectiveness of

internal audit

29

Indicator

Five:

PEFA PI-23

PI-23 D D D D+ D+ Annual PEFA Self-

Assessment

PFEM

Unit

Accounting,

recording and

reporting:

Availability of

information on

resources

received by

service delivery

units

Indicator Six:

PEFA PI-25

PI-25 C+ C+ C+ C+ B Annual PEFA Self-

Assessment

PFEM

Unit

Accounting,

recording and

reporting:

Quality and

timeliness of

annual financial

statements.

Indicator

Seven:

PEFA PI-26 &

28

PI-26

PI-28

D+

D+

D+

D+

D+

D+

C

C

C

C

Annual PEFA

Assessment

PFEM

Unit

External audit

and legislative

scrutiny: Scope,

nature and

follow-up of

external audit &

Legislative

scrutiny of

annual audit

reports

Indicator

Eight

Improved

service

delivery

resulting from

PFM reform

interventions

Baseline

study Q 1

& 2 of

project

period

To be defined

during

implementation

30

Annex 2: Detailed Project Description

Malawi: Financial Reporting and Oversight Improvement Project

Component One: Accounting and Financial Management (Component 5 of PFEMRP)

1. The objectives of this component are to improve the systems and controls for accounting,

reporting and financial management. It has three sub-components as explained below.

Sub-component 1- Accounting and IFMIS (Component 5.1 and 5.2 of PFEMRP)

2. Objectives: This sub-component would assist the Government to improve the efficiency

and comprehensiveness of Government accounting and financial management systems in its

MDAs, the compliance with the rules and regulations, and the comprehensiveness, transparency,

and timeliness of fiscal reporting.

3. Implementation status: The Malawi IFMIS was implemented in 2005 on EPICOR Public

Sector Financials (version 7.2) platform for accounting and budgeting. Currently, EPICOR

system, upgraded to version 7.3.5 in 2007/08, being used in Malawi has the following modules

available:

a) Active Planner: used for compilation of annual budget and MTEF by only the Budget

Division users; ministries and agencies use spreadsheets to prepare budget requests;

b) General Ledger/CoA: implemented: multi-dimensional Chart of Accounts (CoA),

compliant with IMF’s Government Finance Statistics (GFS) implemented

c) Accounts Payables: implemented: being used for supplier maintenance, invoice and

payment processing

d) Commitment control/purchase orders: partially implemented with control weaknesses

e) Accounts Receivables (AR) and revenue management: Not implemented

f) Bank reconciliation: Not implemented; interfaces with central bank planned

g) Check printing: implemented; control weaknesses around handling of check books

h) Fixed Asset Management System: not implemented

i) Cash Management: partially implemented: only used for managing bank accounts,

not cash planning, forecasting and reconciliation.

4. As of now, the system has been implemented at all 52 line ministry headquarters in

Lilongwe and 3 regional treasury cashier offices. Most of the line ministries are connected to the

central servers and process their transactions on line. The Accountant General Department

(AGD) processes the transactions for a few off-line ministries. The system is primarily being

used to record current expenditures, make payments and produce reports. Donor funded project

payments are being processed outside the system. Interfaces with important external systems like

central bank, payroll, debt and aid management and revenues have not been developed.

5. Through the productive use of IFMIS, the government has been able to institute TSA

regime by centralizing the payments. The Government maintains a set of five accounts at

Reserve Bank of Malawi (RBM) for Government funds. Most individual spending Unit bank

accounts have been closed. Payments are centralized through the central payment office and are

made from one of these accounts. Remaining separate, ‘ring-fenced’ accounts relating to

31

respective projects are held at the RBM, from which checks are drawn by the respective projects

and payment information uploaded into IFMIS ex-post. Most expenditure transactions are

subject to budget availability checks before they are authorized for payment. Extra budgetary

funds are transacted outside the system.

6. The IFMIS system is not being leveraged to its full potential for a strengthened public

financial management environment due to several control weaknesses and incomplete coverage.

7. Direct payment facility, allowing users to make payment without purchase order and

commitment control, is being used without adequate access restrictions. Release of funds to

individual payments transactions without linkage to cash forecasts and commitments increases

the risk of rent seeking. There are control weaknesses in the system security involving access

rights, mostly through password sharing, to multiple users to over-ride budget availability check.

Non-tax receipts are collected by the respective field office or deposited in the designated local

bank branches through the deposit slips, which are bundled on monthly basis to be sent to the

Ministry, where they are entered in the IFMIS as monthly totals, losing voucher-wise break-up

required for bank reconciliation. Vendor creation process is ad-hoc and un-regulated. A custom

developed, home-grown system is being used to run the payroll, which is uploaded into the

IFMIS through a series of manual interventions, compromising controls at several steps along the

way.

8. The government is aware of these issues and is committed to improving the control

environment and coverage of the IFMIS through a comprehensive strategy. Key aspects of this

strategy involve urgent fixes, including strengthened system access controls, re-evaluation of

EPICOR as suitable technology platform, business process re-engineering and subsequent

revision of its accounting manual and IFMIS upgrade/re-implementation. This being supported

by funding from GIZ.

9. In this regard, the government wants to make an informed evaluation, whether EPICOR

system itself is suited to the needs of the governments or Serenic Navigator (SN), a Microsoft-

based ERP system, in operational use at the local governments with much higher level of user