the utah health exchange ten lessons learned from the utah experience

TRANSCRIPT

The The Utah Utah Health Health ExchangeExchange

Ten Lessons Learned from the Utah Ten Lessons Learned from the Utah ExperienceExperience

Ten Lessons LearnedTen Lessons Learned

1. Support and Cooperation Within 1. Support and Cooperation Within and Across State Government is and Across State Government is KeyKey

2. Begin with the End in Mind2. Begin with the End in Mind

3. Develop a General Timeline3. Develop a General Timeline

4. Identify Specific Problems to be 4. Identify Specific Problems to be AddressedAddressed

5. Demography is Destiny5. Demography is Destiny

Ten Lessons LearnedTen Lessons Learned

6. Engage Stakeholders Early and 6. Engage Stakeholders Early and Often and in a Cooperative Often and in a Cooperative DynamicDynamic

7. Deadlines Can Be Your Friends7. Deadlines Can Be Your Friends

8. Consider A Phased Approach8. Consider A Phased Approach

9. Leverage Existing Resources9. Leverage Existing Resources

10. Commit to Systemic Change10. Commit to Systemic Change

Begin With The End In Begin With The End In MindMind

• Greater Choice• Expanded Access• Individual Responsibility• Increased Affordability• Higher Quality• Improved Health

Develop a consumer driven health care and Develop a consumer driven health care and insurance market that provides:insurance market that provides:

Develop a General Develop a General TimelineTimeline

1-3-6-10 Plan1-3-6-10 Plan

• During the 11st year, take specific actions to establish a foundation for future success

• Understand it may take as many as 33 years to fully develop a plan of action

• Focus on 66 critical areas of need• Further understand it may take as long as 1010 years to fully

implement reforms

Identify Specific Identify Specific ProblemsProblems

• Too Many Uninsured• Employers Dropping Insurance• Escalating Premium Costs• Consumers Increasingly Detached from the Market• Misaligned Incentives

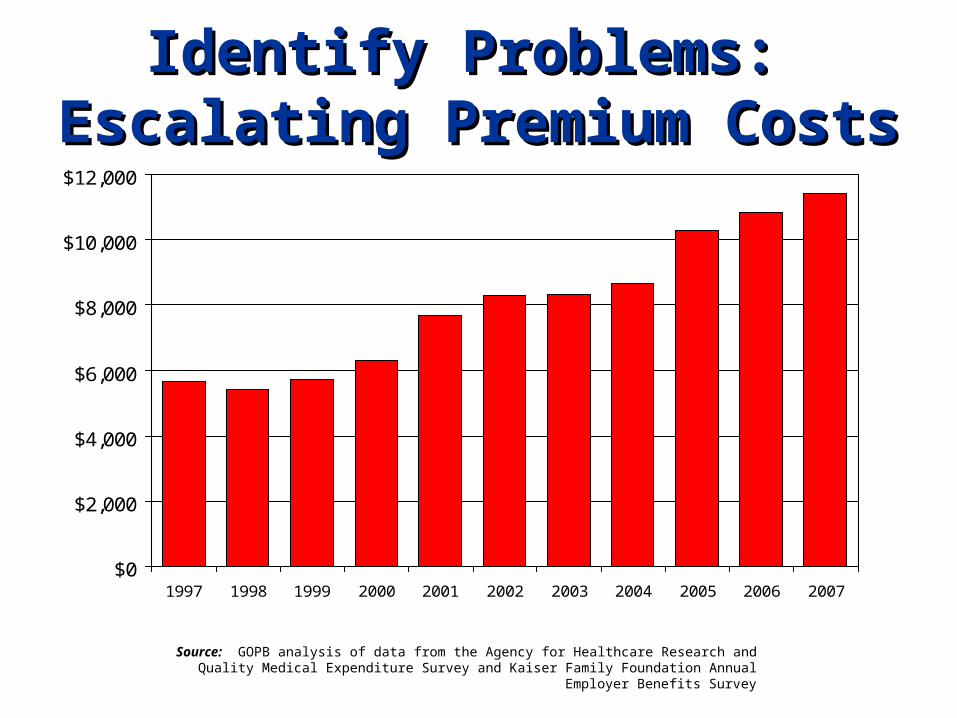

Identify Problems: Identify Problems: Escalating Premium CostsEscalating Premium Costs

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Source: GOPB analysis of data from the Agency for Healthcare Research and Quality Medical Expenditure Survey and Kaiser Family Foundation Annual Employer Benefits Survey

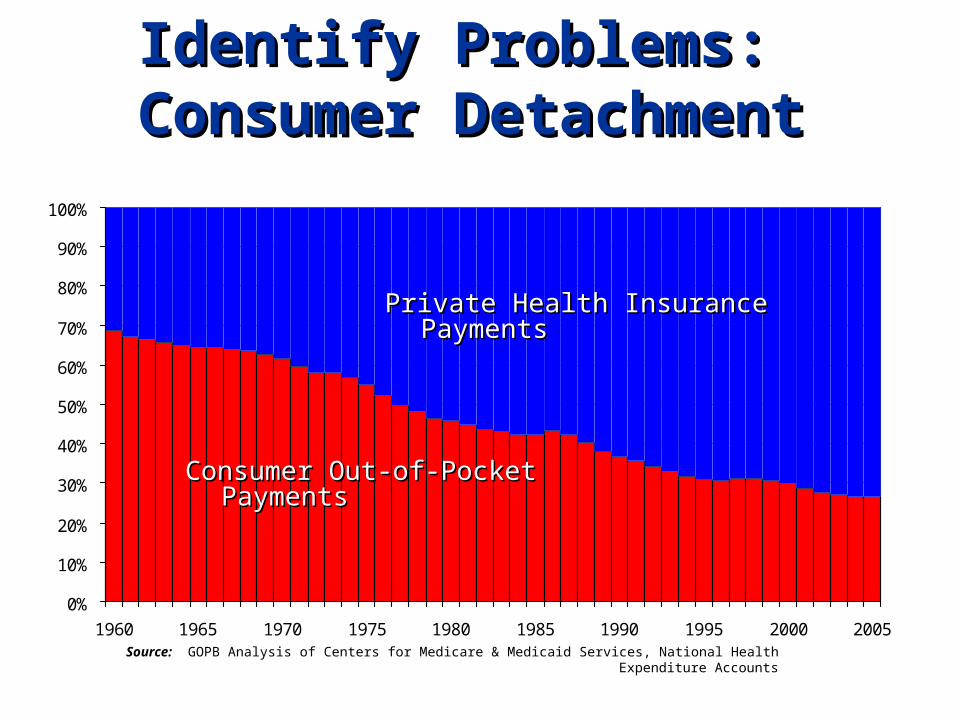

Identify Problems: Identify Problems: Consumer DetachmentConsumer Detachment

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

Private Health Insurance PaymentsPrivate Health Insurance Payments

Source: GOPB Analysis of Centers for Medicare & Medicaid Services, National Health Expenditure Accounts

Consumer Out-of-Pocket PaymentsConsumer Out-of-Pocket Payments

Identify Problems: Identify Problems: Fewer Firms Offering Fewer Firms Offering

CoverageCoveragePercent of US Firms Offering Health Benefits

54%

56%

58%

60%

62%

64%

66%

68%

70%

2000 2001 2002 2003 2004 2005 2006 2007

Source: Kaiser Family Foundation

Identify Problems: Identify Problems: Fewer Firms Offering Fewer Firms Offering

CoverageCoveragePercent of Utah Firms Offering Health Benefits

40%

42%

44%

46%

48%

50%

52%

54%

56%

58%

2000 2001 2002 2003 2004 2005

Source: Agency for Healthcare Research and Quality Medical Expenditure Survey

Demography Is DestinyDemography Is Destiny

Utah’s Uninsured Population in 2007Utah’s Uninsured Population in 2007• 10.6% rate of uninsured in the state

– Roughly 300,000 individuals• Majority were employed• Many were part-time workers

– Workforce has a large percentage of part-time workers– Many had multiple part-time jobs

• Most worked for small firms– Less than 50% of small firms offering health insurance

as a benefit• Many were young immortals

– Age 18-34

Engage the StakeholdersEngage the Stakeholders

20072007 Formed CoalitionsFormed CoalitionsExecutive BranchLegislative BranchSalt Lake Chamber of CommerceUnited Way of Salt Lake

20082008 Formed Perspective-Oriented Work Formed Perspective-Oriented Work GroupsGroups

Community GroupBusiness GroupHospital GroupNon-hospital Provider GroupInsurance Group (carriers and producers)

20092009 Formed Task-Oriented Work GroupsFormed Task-Oriented Work GroupsAffordability and Access GroupTransparency and Quality GroupOversight and Implementation Group

Utah Health Exchange Utah Health Exchange TimelineTimeline

March 2008March 2008 HB 133 HB 133 establishes the Utah Health Exchangeestablishes the Utah Health ExchangeOn-line mechanism that allows consumers to compare, shop for, and On-line mechanism that allows consumers to compare, shop for, and enroll in a health planenroll in a health plan

Will incorporate All Payer Database so patients may access info about Will incorporate All Payer Database so patients may access info about providersproviders

Includes a multiple source premium aggregatorIncludes a multiple source premium aggregator

March 2009March 2009 HB 188 HB 188 establishes the Utah Defined Contribution establishes the Utah Defined Contribution MarketMarket

Employer offers a pre-determined level of funding, rather than a pre-Employer offers a pre-determined level of funding, rather than a pre-determined benefitdetermined benefit

Utah Defined Contribution Risk Adjuster Board establishedUtah Defined Contribution Risk Adjuster Board established

Three carriers announce participation in the Exchange (Select Health, Three carriers announce participation in the Exchange (Select Health, Regence BlueCross Blue Shield, Humana)Regence BlueCross Blue Shield, Humana)

August 2009August 2009 Utah Health Exchange Limited LaunchUtah Health Exchange Limited LaunchExchange is open to limited number of small employers (2-50 Exchange is open to limited number of small employers (2-50 employees)employees)

Purpose is to test dynamics of the new defined contribution market as Purpose is to test dynamics of the new defined contribution market as well as the processes of the Exchange technology well as the processes of the Exchange technology

Utah Health Exchange Utah Health Exchange TimelineTimeline

March 2010March 2010 HB294 includes provisions intended to correct and HB294 includes provisions intended to correct and enhance the defined contribution market and the Exchangeenhance the defined contribution market and the Exchange

Pricing parity between traditional small group market and defined Pricing parity between traditional small group market and defined contribution marketcontribution market

Two additional carriers (Altius, United Healthcare) announce Two additional carriers (Altius, United Healthcare) announce participation in the Exchange (total of 5 carriers) participation in the Exchange (total of 5 carriers)

April 2010April 2010 Large Group Pilot Project launchesLarge Group Pilot Project launchesFull year earlier than anticipated, per requests from large employers Full year earlier than anticipated, per requests from large employers (50 or more employees)(50 or more employees)

Approximately 50,000 covered livesApproximately 50,000 covered lives

August 2010August 2010 Full scale launch to all Utah small employersFull scale launch to all Utah small employers

Leverage Existing Leverage Existing ResourcesResources

TechnologyTechnology• Private-sector vendors

– Enrollment and Plan Selection—bswift, Inc.– Financial/Banking Function—HealthEquity, Inc.

Marketing and OutreachMarketing and Outreach• Chambers of Commerce• Professional and Trade Associations• Earned Media

Education and AdoptionEducation and Adoption• Brokers and Consultants• Human Resource Managers

Commit to Commit to Systemic ChangeSystemic Change

Six Areas of EmphasisSix Areas of Emphasis

• Health Insurance Reform• Personal Responsibility• Transparency and Value• Maximize Tax Advantages• Optimize Public Programs• Modernize Governance

Advantages of the Advantages of the Utah Health ExchangeUtah Health Exchange

EMPLOYERSEMPLOYERS

• Simplified Benefits Management

• Predictable costs• Expanded Coverage

Choices• Preserve Tax Benefits

EMPLOYEESEMPLOYEES

• Individual Control and Choice

• Pay with Pre-tax dollars• Plan Portability• Premium Aggregation

How does the Exchange How does the Exchange work?work?

• Step 1Step 1 – Employer signs up

• Step 2Step 2 – Employee enters information

• Step 3Step 3 – Premiums are generated

• Step 4Step 4 – Employee comparison shopping and open enrollment period

• Step 5Step 5 – Finalize enrollment

• Step 6Step 6 – Plans go into effect on designated date

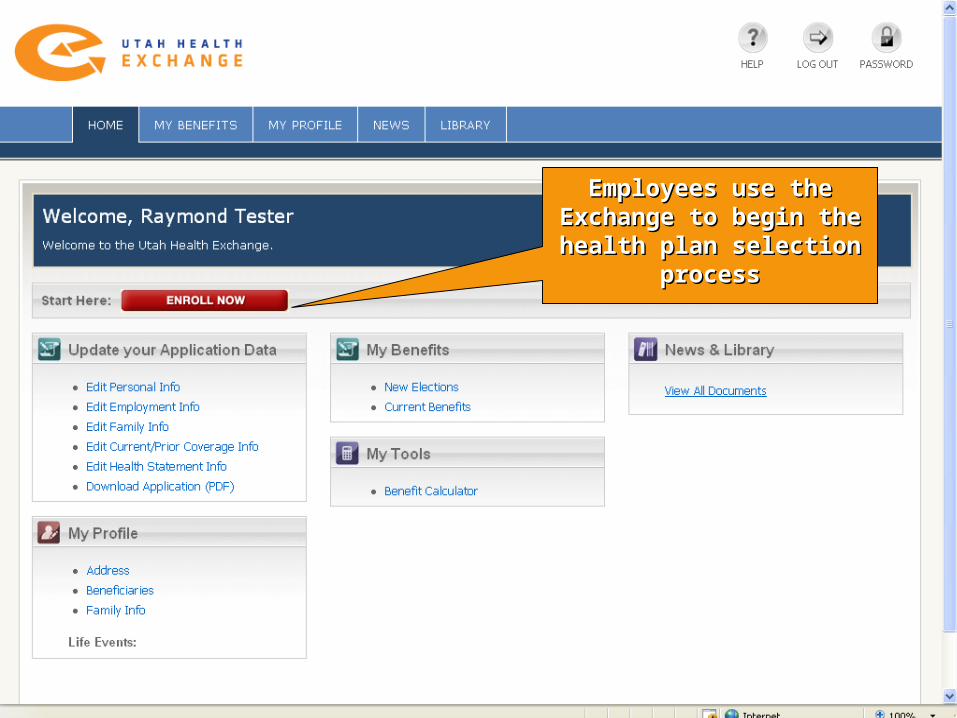

Employees use the Employees use the Exchange to begin the Exchange to begin the health plan selection health plan selection

processprocess

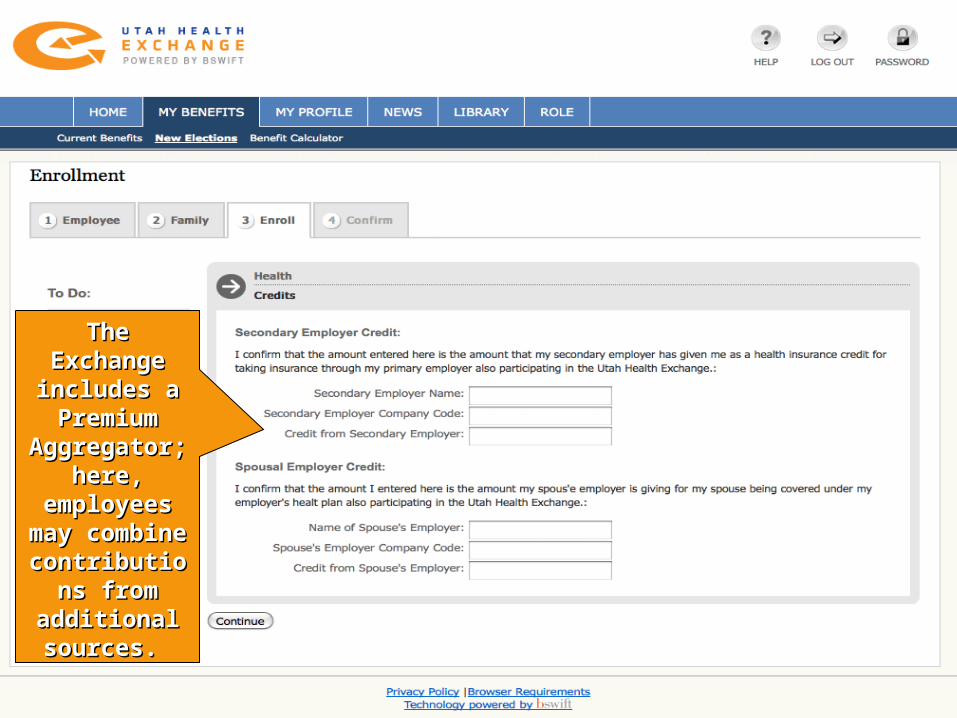

The Exchange The Exchange includes a includes a Premium Premium

Aggregator; Aggregator; here, here,

employees employees may combine may combine contributions contributions

from from additional additional sources. sources.

The Exchange provides a tool that helps The Exchange provides a tool that helps employees compare health plan options. employees compare health plan options.

3) The 3) The employee employee may choose may choose up to four up to four plans for a plans for a more more detailed detailed side-by-side side-by-side comparisoncomparison

1) Employees can narrow down choices or see 1) Employees can narrow down choices or see all available plans. At this stage, employees all available plans. At this stage, employees may:may:

•filter plans by preference for doctor, filter plans by preference for doctor, hospital, or insurance carrierhospital, or insurance carrier•select applicable family statusselect applicable family status•opt to display only HSA-qualified health opt to display only HSA-qualified health plansplans•waive coveragewaive coverage

2) Employees 2) Employees may sort plans may sort plans according to according to priorities or priorities or preferencepreference

Those plans Those plans selected by the selected by the employee are employee are displayed in a displayed in a side-by-side side-by-side

matrix for matrix for summary-level summary-level

or detailed or detailed comparison comparison purposes.purposes.

Employees may estimate total cost for health care Employees may estimate total cost for health care expenditures (premium, deductible, co-pays, etc.) expenditures (premium, deductible, co-pays, etc.)

based on each family member’s health status. based on each family member’s health status.

Employee chooses a planEmployee chooses a plan

The The Exchange Exchange provides a provides a tool to help tool to help employees employees track their track their monthly monthly payroll payroll

deduction as deduction as they go along they go along

in the in the process.process.

If the If the employee employee selects a selects a qualified qualified HDHP, an HDHP, an

HSA option is HSA option is presented.presented.

Employees are provided with detailed plan cost Employees are provided with detailed plan cost information, including the total monthly information, including the total monthly

premium, the employer’s monthly contribution, premium, the employer’s monthly contribution, and the employee’s monthly cost.and the employee’s monthly cost.

The employee The employee confirms confirms covered covered

individuals individuals and saves and saves

selected plan.selected plan.

The final step The final step is to simply is to simply

enroll.enroll.

Similarities: Similarities: MassachusettsMassachusetts and Utahand Utah

MassachusettsMassachusetts• State-based solution

designed to be responsive to state-specific issues, customs, business practices, etc.

• Consumer-centered approach

• Achieved broad, bipartisan consensus supporting the basic reform elements

UtahUtah• State-based solution

designed to be responsive to state-specific issues, customs, business practices, etc.

• Consumer-centered approach

• Achieved broad, bipartisan consensus supporting the basic reform elements

Differences: Differences: Massachusetts and UtahMassachusetts and Utah

MassachusettsMassachusetts• Individual mandate• Employer mandate• Government role is

contracting agent• Established Massachusetts

Connector Authority with broad regulatory responsibilities

• Acted first on public sector reforms; now rolling out private insurance market reforms

UtahUtah• No individual mandate• No employer mandate• Government role is market

facilitator• Regulatory authority

strictly limited to establishment of electronic data standards

• Began by implementing private market reforms first; public sector reforms to follow

Differences: Differences: Massachusetts and UtahMassachusetts and Utah

MassachusettsMassachusetts• No risk adjustment

mechanism included

• Upfront appropriation of $25 million; ongoing funding through retention of a portion of premium

• Staff of approximately 45

employees

UtahUtah• Risk adjustment

mechanism established to deal with adverse selection issues

• Upfront appropriation of $600,000; ongoing funding through annual appropriation and technology fees

• Staff of 2 employees

For more information:For more information:

Utah Health ExchangeUtah Health Exchangeexchange.utah.gov