the “truth” about growth niri senior roundtable december 10, 2010 ed hess professor of business...

TRANSCRIPT

THE “TRUTH” ABOUT GROWTH

NIRI Senior RoundtableDecember 10, 2010

Ed HessProfessor of Business AdministrationBatten [email protected]

1

THE DNA OF GROWTH

2

RESEARCH FINDINGS

5 research projects

The Organic Growth Index ( “OGI”)

The Characteristics of High Organic Growers (“HOGS”)

The Challenges of Managing Private Company High

Growth

The Myths of Growth

The Risks of Growth

3

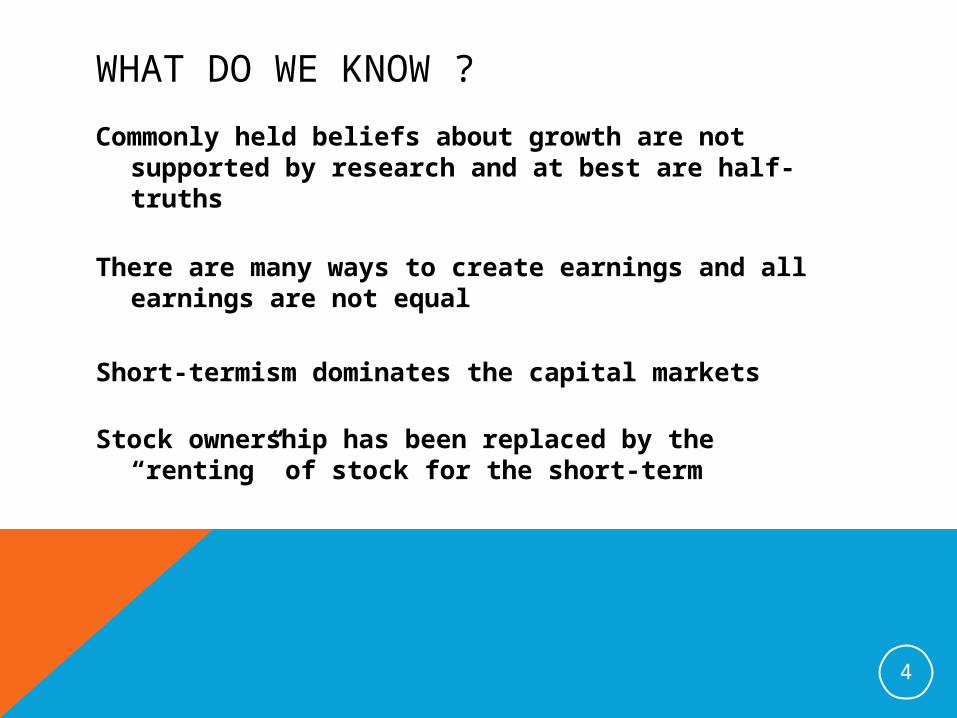

WHAT DO WE KNOW ?

Commonly held beliefs about growth are not supported by research and at best are half-truths

There are many ways to create earnings and all earnings are not equal

Short-termism dominates the capital markets

Stock ownership has been replaced by the “renting” of stock for the short-term

4

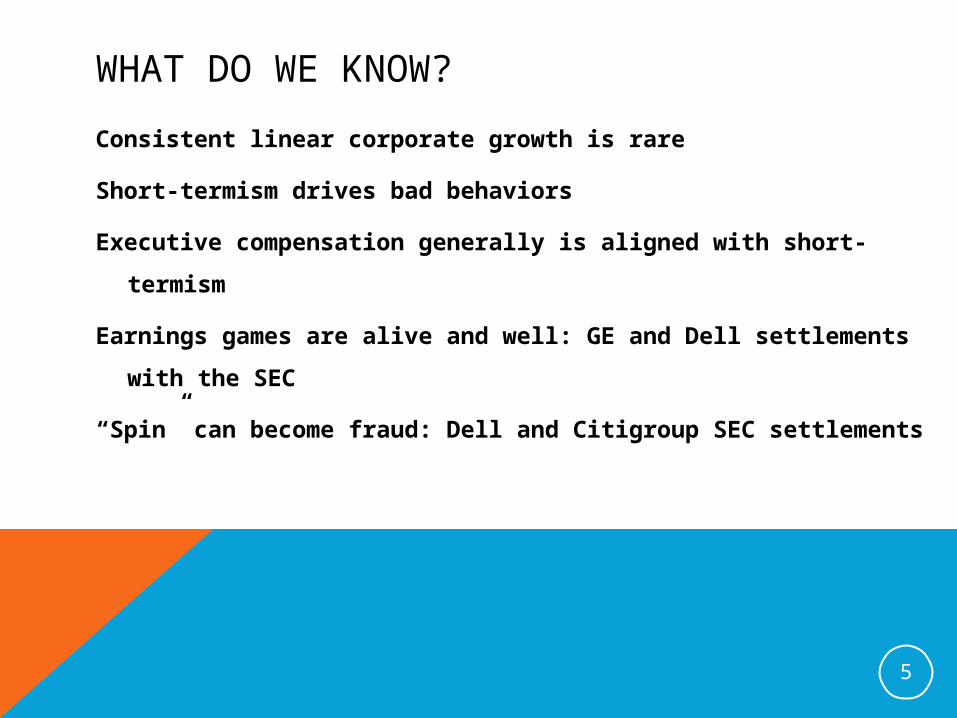

WHAT DO WE KNOW?

Consistent linear corporate growth is rare

Short-termism drives bad behaviors

Executive compensation generally is aligned with short-

termism

Earnings games are alive and well: GE and Dell settlements

with the SEC

“Spin” can become fraud: Dell and Citigroup SEC settlements

5

WHAT DO WE KNOW?

Growth and Innovation are complex people

dependent processes

Growth and innovation are not linear mechanistic

processes

6 different research reports conclude that above industry average or average GDP growth occurs in less than 10% of the samples studied

6

WHAT DO WE KNOW?

Consistent above average growth for seven years or more occurs less than 3 % of samples

Sustainable competitive advantage is a dying

strategic theory

Growth is much more than a strategy: it is a System

Growth results from the right leadership, culture,

and processes

7

WHAT DO WE KNOW?

Growth results from experimental learning

Good growth companies have high employee engagement and are customer centric

Good growth companies create a 2 X 2 X 4 Growth Portfolio

Growth can create material risks that if not properly managed can lead to value destruction: Toyota, Starbucks, BP

8

CAN THIS BE TRUE?Our Capital markets are controlled by short-term

interests that do not care about the long-term health of your business;

Executive compensation has been aligned with those interests;

We have a large professional services industry ( lawyers, IBs, management consultants, accountants) whose income depends on volatility and transactions not stability and patient growth; and

All of this is masked behind the theoretical concept that the sole purpose of a business is to create shareholder value now regardless of the long-term ramifications.

9

SAD BUT TRUE?

Does Wall Street control the investment policy of

U.S. business ?

Has the fundamental principles of capitalism as espoused by Adam Smith been corrupted by short-termism and sole stakeholder theory?

How are the assumptions underlying our capital markets reconciled with the realities of business growth and innovation?

10

THE ROLE OF INVESTOR RELATIONS

Let’s explore this together taking into account the above and the SEC settlements with Dell and Citigroup?

“Strategic management responsibility that integrates finance, communication, marketing and securities law compliance….that contributes to …fair valuation”

11

QUESTIONS

Does the SEC view IR as a financial disclosure quality control function?

Is there a conflict between what the SEC wants (“fair”) and what your “shareholders” want (‘high”)?

Is there a conflict between what the SEC wants and what some executives want ? Dell case

Does who you report to increase those conflicts?

What are the implications of the Citigroup SEC case for you?

12

QUESTIONS

Do these SEC settlements make knowledge a personal risk ?

Does a company have a duty to disclose the character or quality of its earnings?

Do you have an independent duty of due diligence to confirm ?

Should IR report to the Board of Directors or the General Counsel ?

How does the recent evolution in corporate governance interact with the notion of short-termism and growth?

13

IS YOUR PROFESSION UNDERGOING A SEA CHANGE?

From communications and marketing

To fiduciary to the public ?

Or, fiduciary to whom?

Where is your ethical compass?

14