the role of the bookkeeper types of businesses the concepts of business … · 2015-02-17 · the...

TRANSCRIPT

Paper B1 - Level 2 Unit 1

The Role of the Bookkeeper

Types of Businesses

The concepts of Business Entity

and Historic Cost

Setting up the Bank Account

The Analysed Cash Book

1.

Introduction

You have probably bought this course because either you are a self employed

business person who needs to be able to keep a set of financial records in order, or

because you are hoping to become a professional bookkeeper and develop your skills,

either to be able to work for someone else or to run your own bookkeeping business

and offer your services to clients.

This Unit explains the differences between bookkeepers and accountants, and

introduces the organisations who might need to see a set of accounts for a business.

It also explains the various types of businesses that operate and why it is important to

keep accurate records, and introduces the idea of creating a bank account to record

money coming in and going out of a business.

Learning Objectives

This Unit aims to:

Define the differences between a bookkeeper and an accountant

Explain the different types of businesses

Explains the concept of Business Entity

Explain the need for keeping accurate financial records

Describe the terms Income and Expenditure

Develop the layout of a bank account and its entries

Show how to balance an account

Introduce the Analysed Bank Account

What is bookkeeping?

BOOKKEEPING is the process of accurately recording day-to-day financial

transactions into pre-designed “Books of Account”. Such records will enable the

owner(s) and other interested parties to monitor funds coming in and going out of the

business and to calculate profits and losses.

ACCOUNTANCY is making use of the complete information to hand, enabling the

owner to understand the financial position of the business. The use of this information

also makes it possible to forecast for the future, analyse all areas of the business and

evaluate the business potential.

In a small company or in the case of a sole trader, there will probably be only one

person dealing with the books. In large companies the Accounts Department may be

broken down into sections. This may mean that it is the job of one person to deal with

the wages, one to deal with the cash book etc. Where actual cash is involved such as

petty cash and a bank account, two people will very often be working together to keep

these records. This cuts down on mistakes being made and the likelihood of theft.

A small business is likely to have an external accountant who is paid only for the time

they are dealing with the books. This being the case, a lot of money can be saved by

being able to complete the books on a daily basis and then hand them to the

accountant for the end of year tax computations to be made.

Many accountants may be employed in larger organisations, but again they will all be

responsible for different areas of the business (i.e. Cost Accountants, Management

Accountants and Financial Accountants). This allows each person to concentrate on

one particular field and to produce the right results.

To qualify, an accountant needs knowledge of all basic bookkeeping processes

together with other subjects such as economics, law, taxation etc.

Types of businesses

There are a number of different types of businesses that operate and the needs of the

business owner and how he or she wishes to run their business will determine the type

of organisation that will be set up.

Most people start out their working life by being employed by someone else. They are

paid a wage or salary, and Income Tax and National Insurance Contributions are

deducted from their gross salary and sent to Her Majesty’s Revenue and Customs.

This is called a PAYE (Pay as you Earn) system and is explained further in the course

when you learn how to enter salary information into your set of accounts. They might

stay employed for the whole of their working life or they might decide to start their own

business and become self employed. Note: a person can be employed and self-

employed at the same time.

The Sole Trader – most small businesses start out this way. An individual wishes to

become self-employed i.e. to work for him- or her-self and can start this up by simply

declaring themselves to be self-employed to HMRC. The sole trader is responsible for

all debts of the business and may have to pledge their personal effects (including any

property owned) as a guarantee against those debts. The sole trader is taxed on the

profits made and any funds taken out of the business by the owner are termed

drawings. From April 2013, the smallest of such businesses are allowed to keep simple

financial records and submit simplified tax returns.

Partnerships – a partnership is two or more self-employed persons working together

for the purpose of running the business. Any profits or losses made are shared

between them in an agreed proportion and each can be required to pledge their effects

in the same way as the sole trader. A partnership is not in itself taxed on its profits;

each partner is taxed individually on their own share of the profits and the simplified

tax returns for sole traders also apply to individual partners.

Limited Company – A limited company is a legal entity in its own right and information

concerning that company must be registered with both Companies House and HMRC.

Sole traders and partnerships often become limited companies to change their tax

status. The owners then become shareholders, directors and employees of their own

company. Limited companies pay corporation tax on any profits made and any

remaining profit may be distributed in the form of a dividend to its shareholders. The

shareholders have a ‘limited liability’ for covering any debts of the business to the limit

of the amount of their shareholding. However, on occasion a single

shareholder/director could be asked to give a personal assurance for future debts and

this would have to be covered from personal assets. Some self-employed persons

decide to set up a limited company from the start of their business and therefore

become shareholders and directors of their own company.

Limited Liability Partnership – There are occasions when a group of people working

together in a partnership need a limited liability but do not wish to operate as a limited

company. Groups of solicitors or accountants will often work in this way. Profits are

shared in the same way as for a standard partnership but the partners benefit from

limiting their liability for the debts of the business.

Not-for-profit organisations – Such organisations are formed for the benefit of

individuals with some common interest. For example a sports and social club, a

Parent/Teacher Association or a group of individuals wishing to raise funds to support

a particular activity. Funds are raised through membership subscriptions or fund

raising activities and any surplus made is used for the benefit of the organisation rather

than its members. Some not-for-profit organisations can become registered charities.

The concept of Business Entity

Regardless of the type of business that is opened it is important to understand that the

business affairs of the owner should be kept separate from his or her personal affairs.

This is the first of the accounting concepts that you will meet throughout your studies

and it is important to understand that it is only business transactions that can form a

part of business accounts. Accounting records reflect the financial activities of a

specific business entity, separate and distinct from the people who finance it or work

in it.

The concept of Historic Cost

Historic cost is the second concept that you will meet and this is purely a simple

definition of what historic cost represents. You will learn more about this in the next

level of your studies.

Historic cost records items that are purchased as their purchase price and not their

current market value. For example, buying a large item such as a car or piece of

machinery means that the price paid for the item in the accounts is what is recorded

rather than what it might fetch if it were sold at a later date.

Why We Need To Keep Records

Failing to keep proper records means that there is no way of checking the financial

position of the business. This, in extreme circumstances, can lead to prosecution

under the Insolvency Act and being charged with the offence of “failing to keep proper

books of account”.

There is a wide variety of organisations that have the right to look at your financial

records.

First and foremost are the people involved with the collection of the country’s taxes:

HM Revenue & Customs - Tax Assessment (income tax, corporation tax or VAT)

is calculated on a regular basis and relies on the accounts to make fair

assessments of money owed to the government

There are others who may wish to see business records. These will include:

The Bank and other Financial Institutions - If the business were in need of funds

for some reason, the accounts would need to be presented for inspection, to

check on the viability of the business

Limited Company Shareholders - year-end accounts have to be supplied to all

shareholders and investors. These accounts will confirm whether or not the

business is a good investment

Owners - They need to be able to see at a glance whether the company is

profitable or not

Company Management - They need to keep a check on the accounts so that

they can report accurately on the financial situation. This will also help them to

make the right judgement about any future plans

Trade Unions and Employees - It is important for the people who are employed

to understand the financial position of the company. It is also a marvellous boost

to staff morale when good profits can be reported

Capital

Most businesses, regardless of their “type” require money or equipment of some sort

to start operating. The amount of money needed will depend on the nature of the

business. A sole trader working from home may require very little money whilst a

limited company taking on rented premises and needing a large amount of machinery

to operate will need considerably more.

These start-up funds, put in by the owner(s) are called Capital. Other funds might take

the form of a bank loan or a mortgage.

This capital is often turned into Assets (which are things a business owns). The

business will also generate Liabilities, (which are things a business owes). Hence

the Capital of the business will be translated, in a very simple way, to these assets

and liabilities.

At this stage it is useful to give some additional definitions on assets and liabilities.

Assets are things which the business owns.

Fixed Assets are the items which add value to the business and are bought to assist

in the running of the business (premises, motor vehicles, equipment etc). They are

likely to be in the business for more than one year.

Current Assets are items which the business owns but which quickly change in value

from day to day e.g. cash in the bank, stock, amounts owed by customers (the

accounting term for which is debtors).

Liabilities are amounts which the business owes. These can also be divided into two

categories.

Current Liabilities are short-term and are normally paid off within one year, e.g. bank

overdraft, suppliers (the accounting term for which is creditors).

Long term Liabilities are items which last for more than one year, e.g. bank loans,

mortgages etc.

All of these will be covered in further detail as you work through the course.

The Accounting Equation

This can be summed up by a very simple statement

Capital = Assets – Liabilities

(ie the things the business owns less the things it owes)

The formal Accounting Equation turns this around and states it as

Assets = Capital + Liabilities

,

Financial transactions

Each time a business buys or sells something, or offers a service, or pays someone

wages, or carries out any of a huge variety of functions, it undertakes a business

transaction. Normally each business transaction involves money in some way and as

such is called a financial transaction.

Source Documents

For such a transaction to count as a true business transaction there must be a source

document. In the case of a sale this could be an invoice or a receipt; in the case of

an item of expenditure this could be a receipt for goods or services bought.

Without a source document the transaction cannot count as business transaction and

must be charged to the owner as a personal expense. As you work through the

bookkeeping in this course you will learn more about what constitutes a source

document and how to deal with any situation that does not include a source document.

The basis of double entry

Every such transaction that is made will have two elements – something comes into

the business and something goes out.

In many cases it is easy to see what comes in and what goes out

For example:

selling goods - money comes in and goods go out

buying a car - money goes out and the car comes in

However, in some cases, the “other half” of the transaction is less straightforward. An

alternative way to look at it is to say that when money goes “out”, instead of something

coming into the business a “benefit” is gained.

For example:

Paying wages – money goes out and your employee’s time is gained by the

business i.e. you receive the benefit of your employee’s time and labour

Paying rent – money goes out and you receive the benefit of using the premises

you are renting

With money coming in it can be slightly more complicated.

For example:

Receiving a loan – money comes into the bank and the business “owes” the

bank both the principal and interest on the loan.

The business now has a “liability” which means that, at some stage in the future, the

money will need to go “out” but not necessarily immediately.

One of the most difficult things to understand in the early stages of bookkeeping is

which part of the transaction is the “in” or “benefit” part and which is the “out” or

“liability” part. For now we will make this easy and stick to some simple transactions,

all of which include the handling of money.

It is always fairly straightforward to see whether the money is coming in or going out

– if you receive money it is coming in and if you spend money then it is going out. To

use a more sophisticated terminology, money coming in is termed income and money

going out is termed expenditure.

Income and Expenditure

Whatever the size of a business, the one undeniable fact is that the owner will need

to keep a close record of income and expenditure (money received and money paid

out).

Income normally arises from the sale of goods or the provision of a service (such as

bookkeeping services). In the case of someone who owns property income can come

from the rents received from letting out the property. Such income is termed Revenue

Income. On occasion income will arise if an asset is sold – in this case the income will

be termed Capital Income.

Revenue income will normally (for small businesses) be in the form of cash, cheques,

debit or credit cards. Quite often the cheques will be banked immediately, and the

cash kept by the owner to pay small bills etc. However, there is a danger in not banking

the cash promptly, as there is a strong likelihood that these amounts will not be

recorded and the details will be omitted from the books.

Expenditure

Expenditure falls into two main categories

Capital Expenditure is money spent on fixed assets that will remain in the business

for some considerable time.

Revenue Expenditure is money spent on day-to-day items like rent, wages, goods

purchased for resale etc

The Bank Account

Before looking at how the bank account works in our set of accounts it is useful to look

at the services that banks offer to their customers – the main ones are listed and briefly

described below:

Current Accounts

These are everyday accounts used for general banking. Each bank or building society

in the UK has a unique number called a sort code. It is in the form of six digits, the first

two of which identify the bank, the remaining four identify the branch. Each customer

has an account number which consists of eight digits, so a combination of the sort

code and the account number will be unique to each account.

Each bank also has an international SWIFT code which identifies it and each account

has a unique IBAN (International Banking Account Number) for international use. This

is a combination of letters to identify the bank and numbers that consist of the sort

code and account number.

Most banks currently offer free banking services for personal accounts but often

charge for business accounts, although new accounts may be offered a free banking

period of up to two years.

The bank/customer relationship

It is important to understand very early that there is a relationship between the bank

and the business that can be quite difficult to grasp when you start to look at checking

the bank statement later in your studies.

The business is a customer of the bank – any money put into a bank account is still

owned by the business so is in effect ‘loaned’ to the bank for a period of time. The

bank ‘owes’ the business the money back on demand which happens when money is

withdrawn from the bank account.

In the case of the bank, the business is a supplier of temporary funds which the bank

in effect ‘borrows’ for a short period of time.

Hence, when you start to look at how the business bank account works it is vital to

understand that the bank and the business are on opposite sides of each transaction

that is made. Hopefully this will become clearer as you progress through the course.

Statements

Bank statements will be issued regularly which include details of all receipts and

payments made. There is often a charge made for receiving paper statements but with

the increase in online banking, statements can be downloaded from the bank at no

cost to the account holder.

Paying funds into an account

Money is paid into an account in the form of:

Cheques or cash received – these will be paid in over the counter using a paying

in slip. Banks will issue paying in-books with the name of the business already

entered, or individual slips can be used at the bank itself. Details on paying in

slips should include:

o Date

o Branch name

o Account name into which the money is being paid

o Signature or name of the person paying in

o Reference (which might then appear on the statement)

o Sort Code and account number

o Amount – either notes, coins or cheques to be listed

o Summary of the above on a side slip which will be initialed and stamped

by the bank and retained

o List of individual cheques paid in on the reverse of the form

A completed sample paying in slip is shown below:

Date 15 January 201X BANK COPY

Bank giro credit

Notes £50 250 00

£20

£10 30 00

£5

Paid in by A Carstairs Coins £2 10 00

Bank Branch Details

£1 8 00

50p and 20p 1 60

10p and 5p 85

2p and 1p 9

Total

Cash 300 54

Total

Chqs 250 68

Sort Code

99-99-99

Account Number

12345678 £ 551 22

Note: if using a paying in book supplied by the bank some of the items above will

already have been entered. Banks will often make a charge for this service.

There might be a delay in up to three working days for cheques to be cleared

into the account for use by the account holder.

Amounts may be paid into the bank by someone other than the account holder if

they have all the details of the account such as the account name, the sort code

and the account number.

BACS Transfer – money is transferred directly into the account by the customer.

This service is often free of charges. Money normally arrives into the account

cleared for use immediately.

Withdrawing funds from an account

Money is withdrawn from the account in a number of ways. Funds available in an

account are “drawn” on that account by one or more of the following:

Cheques – banks will issue a cheque book for each account if required. This form

of payment is becoming less used and may be withdrawn entirely in the future.

Cheques must contain the following:

o Date of issue

o Name of payee (to whom the money is being sent)

o Amount in both words and figures

o Signature of the account holder

Cheques are normally valid up to six months from the date on the cheque but

banks can accept them after this date. Cheques are legally valid for six years

but if it has not been cashed then the issuer of the cheque may well put a stop

on it which means that the bank will not honour the amount.

Some cheques require an authorisation prior to clearing the payment. For

example, your bank may stipulate that any cheque written out over (say) £1000

may require the bank to contact you to confirm that the payment is valid. This

can help in the case of a fraudulently written cheque.

It is important to realise that a cheque can take several days to “clear” i.e. you

may not be able to draw out money from deposited funds which have not been

cleared – this means that the issuing bank may well need to check with the

account holder that the cheque is authorised for payment before you can draw

on it.

Note: banks often charge for this service for business customers.

BACS Transfer – all banks now offer online banking – by logging into your bank

online you can set up a direct transfer from your account to the payee’s account.

Most banks now operate a faster payment service which means that the money

will arrive almost instantly into the recipient’s account. Note: this service is often

free to users

CHAPS Payment – used to transfer large amounts of money quickly – often when

the amount is higher than allowed via a BACS transaction. There will always be

a charge for this service

Debit cards – banks offer a debit card service –a card with a magnetic strip is

issued which can be used at a point of sale ( a till in a shop for example). The

card is entered into the machine and a PIN number entered to finalise and

authorise the payment. Recent innovations allow touch only payment where the

amount is less than £20 and no PIN needs to be entered.

Debit cards can also be used online to make payments from internet sites or over

the telephone. Each card has a 16-digit number on the front and this plus the

expiry date and a three-digit security number on the back of the card forms the

details needed to identify the card on payments made (for example) over the

internet or by telephone. Some cards also include the valid from date and/or an

issue number. Cards can also be used to withdraw cash from a cash machine.

Money taken from an account using a debit card normally goes out of the account

either the same day or the next day depending on the time of the transaction.

Standing orders – these are regular payments which are paid out on the account

holder’s instructions to the bank. The amount is the same each time and normally

on the same day of the month.

Direct Debits – these are where the account holder signs an agreement to pay

an amount on a regular basis – forms are signed and sent to the supplier who

takes the amount they require on the stipulated date. Direct debits are used to

pay such things as rates, telephone bills, utility bills etc where the amount varies

each time and the claim is made by the supplier to the bank and not paid

automatically by the bank as in the case of a standing order.

Overdraft

Banks will sometimes offer overdraft facilities on current accounts which will allow the

balance to go negative at certain times. This can allow the business to gain short term

advantages for its cash flow, allowing it to pay bills before money due in is received.

There is often an annual fee for this service and interest will be charged on the

overdrawn balance.

Foreign Currency Accounts

If a business deals regularly in foreign transactions, it is possible to open a foreign

currency account. Money coming into the account is held in the originating currency

and can be paid out in the same way as for sterling accounts. This often means higher

banking charges for each transaction but does mean that the money held in the

account is not subject to fluctuating currency exchange rates. Funds can be

transferred to or from foreign currency accounts to sterling accounts at the exchange

rate given by the bank on the day of transfer.

Deposit Accounts

Deposit accounts are savings accounts which often attract bank interest for amounts

being deposited over a period of time. There are usually limits on the amount of

withdrawals that can be made in a year to gain the maximum interest available.

Loans and Mortgages

Banks will often lend money to businesses in the form of a loan or mortgage, many of

which have to be secured against assets owned such as property. There is a

repayment due each month which includes a percentage of interest, plus a repayment

of the principal borrowed until such time as the whole amount is paid off. Loans are

often taken out over a period of five years whilst mortgages are longer term, e.g. 25

years or more.

Online banking

All banks offer an online banking service. Each account holder has a unique logging

in number and password and once online it is possible to make payments, check

balances, print statements etc.

Telephone banking

Many banks offer a telephone banking service. Relevant passwords need to be set up

so that the bank can identify the caller.

Mobile banking

Many banks now have mobile applications that can be downloaded to smart phones

and tablets to enable banking to be carried out on the move.

Paypal

Paypal is one online money transfer system which is used to buy items online over the

internet. It is possible to set up a paypal account which operates in a similar way to a

bank account, receiving and paying out funds until such time as a balance is

transferred to a bank account. Paypal also acts as an online payment system outside

the BACS system where funds are transferred from a bank account through their

system.

Credit cards

Credit cards offer a deferred form of payment. The card is used to buy items, and a

statement sent at the end of the month showing everything that has been spent, and

the total amount owed to the credit card company. If the full amount is paid by the due

date, normally there are no further charges, However if only part of the total is paid,

the balance moves forward to the next month and an interest charge will be levied

each month until the balance is cleared.

Keeping a bank account in the accounting records

For the first few lessons in this book, we will assume that all money received is paid

immediately into the bank, and that all money paid out is by cheque. Later on we will

deal with how to treat cash and cheques separately and also debit and credit card

receipts.

The simplest way to record the payments in and out of the bank is to keep a Bank

Account and enter details at least weekly. The format shown below is only one of the

ways, and although not necessarily the simplest, it will enable you to keep on using it

when you move on to later lessons that use a full double entry system.

This system of storing details is called a “T” Account because the basic layout of the

account forms a T shape.

Bank Account

The left hand side of the T Account is used to record all items paid into the account.

The right hand side is used to record all payments out of the account.

(LHS) = money in and (RHS) = money out

For reasons that will be explained later in the course, the left hand side of the account

is called the debit side (Dr for short) and the right hand side the credit side (Cr for

short).

It is necessary to record three items of information for each transaction (receipt or

payment)

The date of the transaction

A basic description (e.g. sales, rent, wages)

The amount

The account is normally set out as follows:

Bank Account

Dr (In) Cr (Out)

Date Details £ Date Details £

Amanda and her Business

To show you how transactions are entered into the accounts, and to build a set of

records, we will use a fictional business set up by Amanda Carstairs.

Amanda has recently completed a degree in computer studies and intends to start her

own business. She will work from home and will be offering IT services to homes and

businesses within her locality. This will involve buying parts for repairs, buying

hardware and software for resale to clients, servicing equipment and training in its use.

It is likely that she will be paid for jobs in cash, by cheque and by online bank transfer.

She has arranged to buy equipment and supplies etc. from a local wholesale supplier,

but for the first three months she will have to pay by cheque when she collects her

purchases. In this lesson we will show you how to record details of money that Amanda

receives and spends.

To start her business, on 1 January, Amanda will put £10,000 of her own money into

the bank to get her going. This money represents the initial capital she has invested

in the business.

This first entry in her bank account therefore represents money coming into the

business so is entered into the left hand side of the bank account.

Bank Account

Date Details £ Date Details £

201X

January 1

Capital

10,000.00

Amanda has paid £10,000 into her bank account.

Hence the entry is on the left hand side of the account and represents the Capital

she has paid in to start the business. The word Capital, entered into the details column

is a brief explanation of what the transaction represents.

Note: when ruling the lines it is normal to put a double line down the centre to separate

out the two sides, and to use single lines elsewhere.

In order to run her business, Amanda will need some basic tools and equipment. On

2 January she buys some equipment that costs her £800 and she issues a cheque.

The money has gone out of the business and the entry will be reflected in the bank

account as follows:

Bank Account

Date Details £ Date Details £

201X

January

201X

January

1 Capital 10,000.00 2 Equipment 800.00

The original entry remains and Amanda has now paid out £800 for Equipment. The

equipment will stay in the business for some time and any type of expenditure for such

items is termed Capital Expenditure. Such items will not be re-sold to customers but

form the Fixed Assets of the business. The term Fixed Assets will be explained in

greater detail later.

On 4 January she buys £100 worth of parts from her supplier. As these supplies are

to be used up on the job she has undertaken, they are called Purchases. In

bookkeeping, the term purchase is only used for items that are bought to be re-sold

Amanda’s bank account will now look like this:

Bank Account

Date Details £ Date Details £

201X

January

201X

January

1 Capital 10,000.00 2 Equipment 800.00

4 Purchases 100.00

Buying goods that are to be used up in the day-to-day running of the business is

treated differently to buying items which will remain in the business for a long time

such as the equipment above. Expenditure on items that will be used up within a short

time is termed Revenue Expenditure.

Amanda finds her first customer, Ben. She has agreed to repair his PC. She charges

him £175 on 6th January for completing the job.

Any money charged by a business for work carried out or goods supplied are called

Sales. Amanda’s bank account will now be:

Bank Account

Date Details £ Date Details £

201X

January

201X

January

1 Capital 10,000.00 2 Equipment 800.00

6 Sales 175.00 4 Purchases 100.00

Whilst Amanda is working, she obviously has to pay her own living expenses. She is

perfectly entitled as a sole trader to take money out of the business for herself,

providing that she identifies it as such. Money taken out of an account by the business

owner for their own use is called Drawings.

It is important to realise very early on that drawings are not a business expense but a

personal one. You will learn as you work through your studies that drawings cannot

be claimed for business taxation purposes and it is vital that every bookkeeper is

aware that if the business owner cannot provide proof that the expense is a legitimate

business expense then it must be classed as drawings.

If Amanda takes out £100 on 6th January, the account will now look like this:

Bank Account

Date Details £ Date Details £

201X

January 1

Capital

10,000.00

201X

January 2

Equipment

800.00

6 Sales 175.00 4 Purchases 100.00

6 Drawings 100.00

Remember when you need to make an entry ask yourself the following question:

Is money coming INTO the account or is it going OUT?

If it is coming IN, then make the entry on the left hand side of the bank account (the

debit side).

If it is going OUT then make the entry on the right hand side of the account (the credit

side).

Source documents

Earlier in the unit we referred to the source document and the importance of obtaining

and keeping these. For example, when Amanda bought her purchases, if she did not

obtain a receipt or invoice for the goods, the payment would have to count as drawings

– i.e. these would be a personal expense and not a business expense,

NOW IT IS TIME TO START PRACTISING YOURSELF!

Level 2 Unit 1 Task 1

John Dower opens up a business selling computer software online. These are the

details of his first month’s transactions. Start a new bank account and make the

appropriate entries. All payments out are by cheque

April 201X

1 Started business with £3,000.00 in the bank

5 Received a cheque for £7,000.00 being a loan from the bank

6 Paid £1500.00 to a design company for the first stage of his new website

10 Bought a new computer and printer for £3,500.00 paid for by cheque (use the

details “Computer Hardware”)

12 Bought software for resale (use the details “Purchases”) £486.50

20 Bought further software for resale for £270.00

25 Paid for stationery for the business £85.65

30 Received a cheque for his first sale of software £125.50

Required:

Enter the details above into the bank account.

When you have finished you can check your answer with that given in the answer

section which starts at the end of Unit 9 (page A-1).

If you are happy with the result then work through the next section.

Balancing the Account

Making entries into the books, and tracking money going in and out of the business is

one thing, but every business owner needs to know how much money they have

available at any one time. Remember if you write out a cheque and do not have

enough money in the bank to cover it, the cheque may “bounce” and you will incur

bank charges which will not help the situation.

The amount of money the business has in its bank at any time is called the Balance.

The process of calculating this figure is therefore called Balancing the Account.

Remember, if the left hand side of the account shows all money paid in, and the right

hand side of the account shows all money which has gone out, the difference between

the two will be the amount of money left i.e. the balance.

If the left hand side is greater than the right hand side then less money has been spent

than received, and the business will still have money in the bank. If the right hand side

is greater than the left hand side then more has been spent than received and the

business will be in an overdraft situation i.e. it owes the bank money!

Let us calculate how much Amanda has in her account, before you learn how to

balance it in bookkeeping terms.

Amanda has paid in the following amounts: £10,000 + £175 = £10,175

Amanda has paid out the following amounts: £800 + £100 + £100 = £1,000

Hence Amanda will have £10,175 - £1,000 = £9,175 left in her account

Remember the in – it is important.

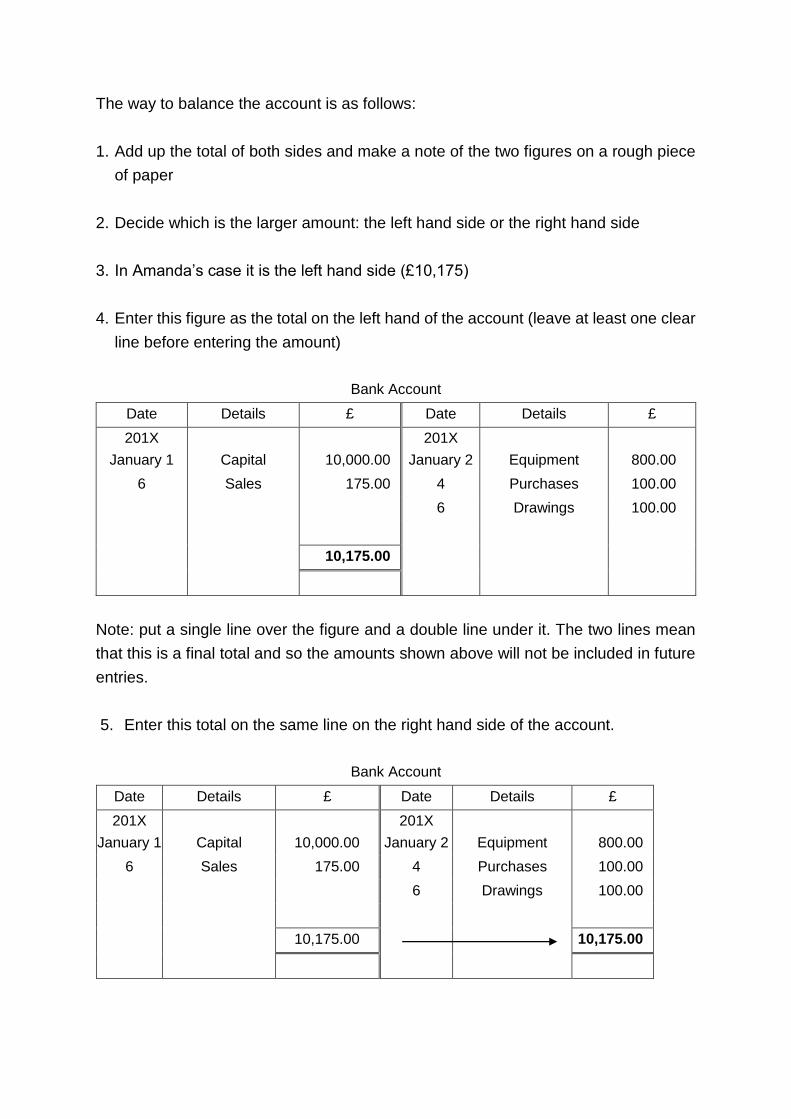

The way to balance the account is as follows:

1. Add up the total of both sides and make a note of the two figures on a rough piece

of paper

2. Decide which is the larger amount: the left hand side or the right hand side

3. In Amanda’s case it is the left hand side (£10,175)

4. Enter this figure as the total on the left hand of the account (leave at least one clear

line before entering the amount)

Bank Account

Date Details £ Date Details £

201X

January 1

Capital

10,000.00

201X

January 2

Equipment

800.00

6 Sales 175.00 4 Purchases 100.00

6 Drawings 100.00

10,175.00

Note: put a single line over the figure and a double line under it. The two lines mean

that this is a final total and so the amounts shown above will not be included in future

entries.

5. Enter this total on the same line on the right hand side of the account.

Bank Account

Date Details £ Date Details £

201X

January 1

Capital

10,000.00

201X

January 2

Equipment

800.00

6 Sales 175.00 4 Purchases 100.00

6 Drawings 100.00

10,175.00 10,175.00

Note: if you look at the right hand side of the account the three entries do not add up

to £10,175.

6. Now subtract the total of the right hand side (calculated in 1 above) from the £10,175

and enter it above the line on the right hand side. Note that this figure comes to

£9,175. This figure represents the balance that is carried forward (c/f) to the next

period.

Bank Account

Date Details £ Date Details £

201X

January 1

Capital

10,000.00

201X

January 2

Equipment

800.00

6 Sales 175.00 4 Purchases 100.00

6 Drawings 100.00

Balance c/f 9,175.00

10,175.00 10,175.00

Finally we need to bring this balance forward (b/f) to the opposite side. We now

know how much money is in the account at the start of the next period. Note that we

use the terms balance c/f (carried forward) above the total and balance b/f (brought

forward) below the total.

Bank Account

Date Details £ Date Details £

201X

January 1

Capital

10,000.00

201X

January 2

Equipment

800.00

6 Sales 175.00 4 Purchases 100.00

6 Drawings 100.00

Balance c/f 9,175.00

10,175.00 10,175.00

Jan 6 Balance b/f 9,175.00

To summarise – carry forward balances the account and brought forward brings the

balance into the next period ready to start again.

Note: sometimes the terms “carried down” (c/d) / “brought down” (b/d) are used in

place of c/f and bf. Either is acceptable but do not mix the two.

It is usual to balance accounts regularly, say at month end. Therefore the balances

would be dated at the last day of the month.

However, it is also common practise for the balance c/f to be dated on the day the

accounts are balanced, then because this balance is brought forward to the start of

the next day, the balance b/f entry is dated 1 day later.

You may see both methods used throughout this course.

Note we calculated that there is money in the bank and our balance brought down is

on the left hand side of the account which is the in side (remember above we said to

remember that Amanda has £9,175 in her account).

Sometimes, however, it is the right hand side of the account which is the larger. This

is an example of a bank account which in overdraft.

In the example shown below, the right hand side is £2,300 and the left hand side

£1,300. In this case enter the largest total on both sides and introduce the missing

balance on the smaller side (left hand side) bringing the balance down onto the right

hand side. In this case you owe the bank £1,000. The balance is on the right hand

side which means that more money has gone out than in. You are in an overdraft

situation.

Bank Account

Date Details £ Date Details £

201X

January 1

Capital

1,000.00

201X

January 2

Equipment

2,000.00

6 Sales 300.00 4 Purchases 200.00

7 Balance c/f 1,000.00 6 Drawings 100.00

2,300.00 2,300.00

7

Balance b/f

1,000.00

Earlier in the lesson we mentioned that the left hand side of the account is used to

show money coming in or a benefit to the business.

We also said that the right hand side is used to show money going out of the business.

But there is another use for this side – it records a liability that the business has

assumed. The above credit balance on the account means that the business is in

overdraft and owes the bank money – i.e. the business has assumed a liability to the

bank for the amount of the overdraft.

Level 2 Unit 1 Task 1a

Now balance the account you set out in Task 1. When you are happy that you have

done it correctly, answer the next two questions, checking your answers with those

given.

Level 2 Unit 1 Task 2

Write up the Bank Account for Mr Arnold for the month of September from the following

details. Balance off at the end of the month and carry the balance forward.

September 201X

1 Mr Arnold starts a business with £5,000 in the Bank.

2 Bought office furniture for £1,000 paying by cheque.

3 Received a loan of £5,000.00 from the Bank.

4 Bought goods for resale (purchases), paid by cheque £2,800.

10 Cash sales £600 banked.

17 Cash sales £750 banked.

22 Paid rent £250 by cheque.

26 Banked takings from sales £1,100.

28 Withdrew £200 from the bank for personal use.

Level 2 Unit 1 Task 3

Molly Bertram offers a dog walking service to local dog owners. She already has some

clients and decides that she does not need to invest any money to get started. Record

the following transactions in Molly Bertram’s bank account. At the end, balance the

account and bring the balance down.

October 201X

8 Banks money from first week’s work £75.00

10 Pays for printing of leaflets by cheque £25.00

15 Banks money from second week’s work £85.50

22 Pays for insurance premium by cheque £50.00

25 Banks money from third week’s work £80.75

30 Bought waterproof gloves and hat paid by cheque £15.00

31 Banked money from fourth week’s work £75.00

ON-GOING WORK JOE LEWEY

Your pack includes a revision section entitled “Joe Lewey”. Here you will find a set of

accounts, based on a business over a period of one year, to be worked through in

order to gain experience in bookkeeping. At this stage you can complete the work for

Unit 1 (part 1), or if you prefer, complete the entire section in one go when you have

finished all the Units.

Whichever you choose, once you have finished the work for the Unit, turn to the

answers at the back of the book and check them through thoroughly.

The Analysed Cash Book

Some businesses find it more convenient to maintain a cash book, rather than a simple

bank account, where the income and expenditure is analysed or split up under different

headings. This is because at some stage, the business will need to know how much it

has spent on various items such as purchases, stationery, wages etc. It is quite difficult

to see this easily from the bank account as described earlier.

Remember we said earlier that each transaction had two elements – something

coming in and something going out. By analysing the expenditure into columns you

can see the second half of this working.

It is still important to keep the income and expenditure columns as before, so that you

can calculate how much money is in the account. The analysis of income and

expenditure is in addition to this.

Businesses that use this system can purchase analysis paper which is divided into a

number of columns. There is still a left hand side and a right hand side as before, but

sometimes, because the paper is wide the pages are often kept separately.

Look at Amanda’s bank account from earlier.

Bank Account

Date Details £ Date Details £

201X

January 1

Capital

10,000.00

201X

January 2

Equipment

800.00

6 Sales 175.00 4 Purchases 100.00

6 Drawings 100.00

The income side consists of only the capital paid in to start the business and one sale.

In a simple business like Amanda’s the majority of income items will be for sales so

there is no need to analyse the left hand side of the account.

However there will be a number of types of expenditure so it will be useful to show the

right hand side in some form of analysed sheet.

Keep the main account the same and add columns to the right hand side, transferring

the items into each column as they are entered into the account.

Analysed Cash Book

Date Details £ Date Details £ Assets Purchases Drawings

201X

Jan 1

Cap

10,000.00

201X

Jan 2

Equipment

800.00

800.00

6 Sales 175.00 4 Purchases 100.00 100.00

6 Drawings 100.00 100.00

Balancing an analysed cash book

When balancing an analysed cash book, treat the main section of the account in the

same way as before.

Analysed Cash Book

Date Details £ Date Details £ Assets Purchases Drawings

201X

Jan 1

Capital

10,000.00

201X

Jan 2

Equip

800.00

800.00

6 Sales 175.00 4 Purch 100.00 100.00

6 Drawings 100.00 100.00

Bal c/f 9,175.00

10,175.00 10,175.00

6

Balance b/f 9,175.00

Finally, draw a single line under the analysis columns and sub total these. Do not rule

off underneath as you will carry on adding the columns after further transactions.

Analysed Cash Book

Date Details £ Date Details £ Assets Purchases Drawings

201X

Jan 1

Capital

10,000.00

201X

Jan 2

Equip

800.00

800.00

6 Sales 175.00 4 Purch 100.00 100.00

6 Drawings 100.00 100.00

Bal c/f 9,175.00

10,175.00 10,175.00 800.00 100.00 100.00

6

Balance b/f 9,175.00

The following shows a further example of some analysed expenditure, this time with

more than one entry in each column. Note that for the entry on 11 January, the total

cheque was written out for £120 but this consisted of £100 of goods that were bought

for resale, and £20 of sundries that are being used in the business.

Analysed Cash Book

Analysis Columns

Date Details £ Date Details £ Sundries Purchases Rent Drawings

201X

Jan

201X

Jan

1 Balance b/f 5,000 2 Sundries 50 50

6 Sales 650 6 Purchases 2,100 2,100

10 Sales 950 6 Rent 200 200

7 Drawings 200 200

8 Purchases 1,000 1,000

11 Sundries 120 20 100

12 Balance c/f 2,930

6,600 6,600 70 3,200 200 200

Jan 13

Balance b/f

2,930

By adding up the analysis columns, it is possible to find the total spent on each type

of expense in a given period.

e.g. Sundries = £70 (50 + 20)

Purchases = £3,200 (2,100 + 1000 + 100)

Rent = £200

Drawings = £200

It’s practice time again – the information from task 1 is re-created below – reproduce

the information in the form of an analysed cash book and then continue with the

remaining tasks

Level 2 Unit 1 Task 4

John Dower opens up a business selling computer software online. These are the

details of his first month’s transactions. Start a new bank account and make the

appropriate entries. All payments out are by cheque

April 201X

1 Started business with £3,000.00 in the bank

5 Received a cheque for £7,000.00 being a loan from the bank

6 Paid £1,500.00 to a design company for the first stage of his new website

10 Bought a new computer and printer for £3,500.00 paid for by cheque (use the

details “Computer Hardware”)

12 Bought software for resale (use the details “Purchases”) £486.50

20 Bought further software for resale for £270.00

25 Paid for stationery for the business £85.65

30 Received a cheque for his first sale of software £125.50

Level 2 Unit 1 Task 5

Draw up an analysed cash book, using analysis columns for Rent, Equipment,

Purchases, Office Expenses and Drawings and enter the following transactions for

Norman Todd:

April

1 Started with capital of £2,000 paid into business bank account

2 Paid a cheque for shop rent £500

3 Bought equipment - £600 by cheque

4 Purchased stock for resale by cheque £450

5 Returned some equipment unused. A cheque for £200 was received and paid into

the bank.

7 Sold goods for £75 - the money was paid into the bank

9 Bought business stationery (office sundries) for £12 – paid by cheque

17 Received a loan of £500 from J Blunt – the cheque was banked

24 Sold more stock for £320 and the money is paid into the bank

27 Bought goods for resale by cheque £135

28 The telephone bill (Office Sundries) of £18 was paid by cheque

30 Drew a cheque for personal use for £300

ON-GOING WORK JOE LEWEY

Turn to your practice work book and complete the work for Unit 1 (part 2). When you

are happy with what you have done, complete assignment 1 and send your completed

work to your tutor.

LEVEL 2 UNIT 1 ASSIGNMENT

PART A

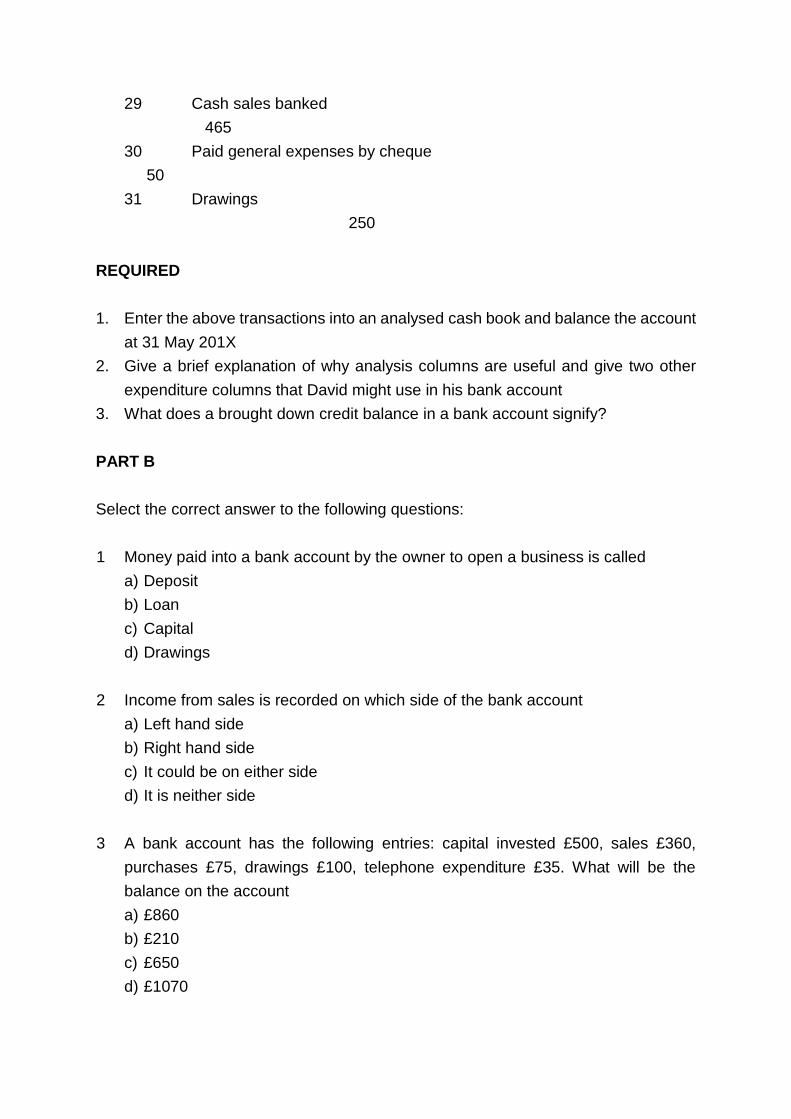

David has set up an analysed cash book for his business, with analysed expenditure

columns for drawings, purchases, wages, insurance and general expenses.

The following receipts and payments were put through the bank account for the month

of May 201X

May

1 Balance brought forward

250

2 Cash sales banked

1,725

3 Cash sales banked

465

5 Drawings

250

9 Cash sales banked

390

10 Paid R Stuart cheque for purchases

975

11 Paid wages

100

12 Paid insurance premium

450

16 Paid cash sales into bank

400

17 Received cheque for purchases returned 35

18 Paid general expenses by cheque

50

23 Cash sales banked

500

24 Received cheque from Bamett for sales made 243

27 Paid for general expenses by cheque

48

28 Paid wages by cheque

100

29 Cash sales banked

465

30 Paid general expenses by cheque

50

31 Drawings

250

REQUIRED

1. Enter the above transactions into an analysed cash book and balance the account

at 31 May 201X

2. Give a brief explanation of why analysis columns are useful and give two other

expenditure columns that David might use in his bank account

3. What does a brought down credit balance in a bank account signify?

PART B

Select the correct answer to the following questions:

1 Money paid into a bank account by the owner to open a business is called

a) Deposit

b) Loan

c) Capital

d) Drawings

2 Income from sales is recorded on which side of the bank account

a) Left hand side

b) Right hand side

c) It could be on either side

d) It is neither side

3 A bank account has the following entries: capital invested £500, sales £360,

purchases £75, drawings £100, telephone expenditure £35. What will be the

balance on the account

a) £860

b) £210

c) £650

d) £1070

4 A brought down balance on the right hand side of a bank account means

a) The business has money in the bank

b) The business has an overdraft at the bank

c) The bank has a zero balance

d) None of the above

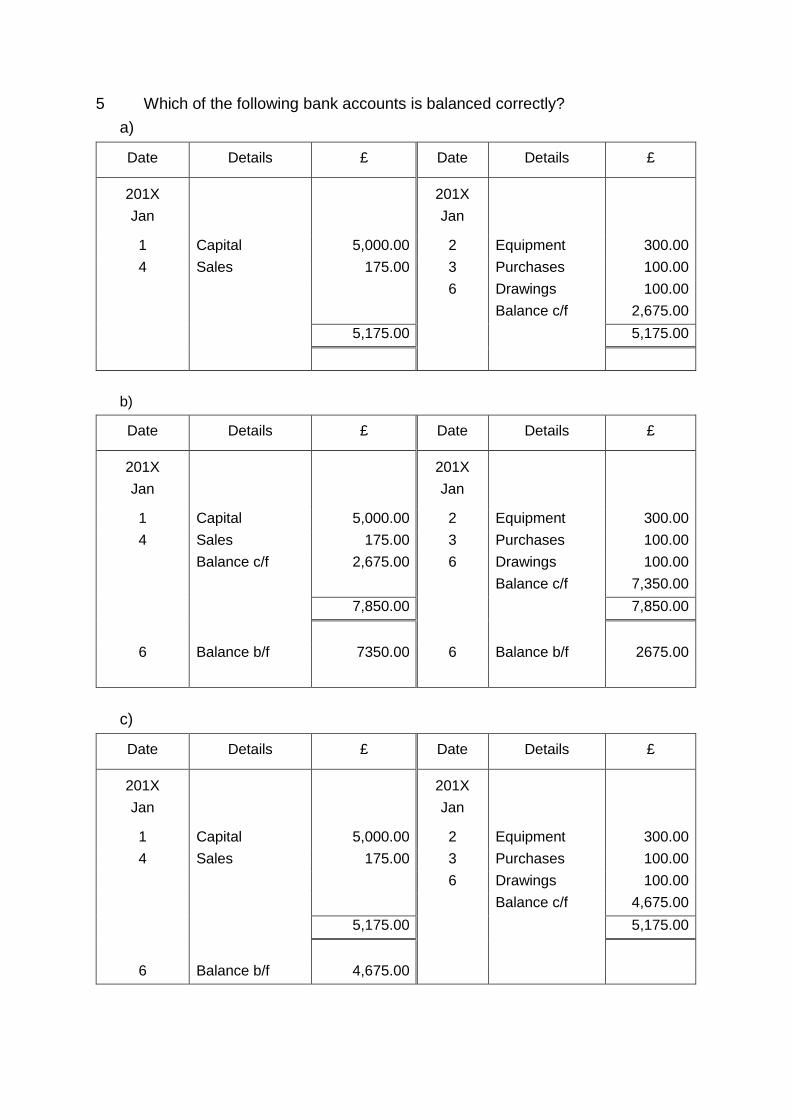

5 Which of the following bank accounts is balanced correctly?

a)

Date Details £ Date Details £

201X

Jan

201X

Jan

1 Capital 5,000.00 2 Equipment 300.00

4 Sales 175.00 3 Purchases 100.00

6 Drawings 100.00

Balance c/f 2,675.00

5,175.00 5,175.00

b)

Date Details £ Date Details £

201X

Jan

201X

Jan

1 Capital 5,000.00 2 Equipment 300.00

4 Sales 175.00 3 Purchases 100.00

Balance c/f 2,675.00 6 Drawings 100.00

Balance c/f 7,350.00

7,850.00 7,850.00

6 Balance b/f 7350.00 6 Balance b/f 2675.00

c)

Date Details £ Date Details £

201X

Jan

201X

Jan

1 Capital 5,000.00 2 Equipment 300.00

4 Sales 175.00 3 Purchases 100.00

6 Drawings 100.00

Balance c/f 4,675.00

5,175.00 5,175.00

6 Balance b/f 4,675.00

d)

Date Details £ Date Details £

201X

Jan

201X

Jan

1 Capital 5,000.00 2 Equipment 300.00

4 Sales 175.00 3 Purchases 100.00

6 Drawings 100.00

5,175.00 Balance 2675.00

6 Balance b/f 2,675.00