the innovation journey - official website · the innovation journey: the last four years and into...

TRANSCRIPT

THE INNOVATION JOURNEY:

The last four years and into the future

Presentation to the Australian Payments Forum

Monday 15 April 2013

1

Where were we?

What’s happened since?

Where to from here?

DCITA Report 2006

APCA Innovation Report 2008/9

2

2006 DCITA “Future Electronic Payments Markets”:

5 actions for $2 billion in cost savings to the economy

1. Moving cash to debit cards

$100 billion of cash transactions with a value of over $20

Beyond $20 level, least costly real-time method is debit card

Potential savings $900m

2. Lowering the electronic payment threshold

Introducing electronic payment products that are less costly than

cash for smaller or micro-payments

Proliferation of contactless, stored-value cards in transit

functions in other countries > what about Australia?

3. Electronic bill payments

A significant proportion of bill payments still made using over-

the-counter methods and paper-based payment products

Need for data / information with payment

3

2006 DCITA “Future Electronic Payments Markets”:

5 actions for $2 billion in cost savings to the economy

4. Electronic bill presentment

Research has shown that if a bill is presented electronically, it is

significantly more likely that the bill will be paid electronically

In addition, electronic bill presentment provides other significant

benefits to the economy and to billers

– eg. direct cost reductions to a biller’s operations

5. Migrating cheques to direct entry

Still areas where direct entry has yet to replace cheques, even

though it would be advantageous to do so

B2B payments, government payments, superannuation

payments, employee expense reimbursements and bill payments

are all key areas that still rely significantly on cheques

4

The DCITA savings equated to additional economic

growth of roughly 25 basis points of GDP

Economy-wide cost savings from increasing electronic payments

$6 000

$8 000

$10 000

$12 000

$14 000

Total Costs Reductions from

micro-payment

product

Reductions from

cash migration

over $20

Cheque migration Electronic bill

presentment

reductions

Biller channel

mix reductions

Target

Co

st o

f P

aym

en

t S

yste

ms

($ m

illio

ns)

>>

>

Economy-wide cost savings from increasing electronic payments

5

2008/9 APCA review concluded that Australian consumers

are not demanding innovation in payments . . .

A high percentage of consumers are banked

Consumers have lots of choice in payment methods

Similar numbers of options by payment channel as seen in most

other developed markets

There is no overt demand

Except in mass transit

They perceive no major gaps

But take care:

Consumers don’t know what’s possible

As Henry Ford said

“If I’d asked people what they wanted,

they’d have said a faster horse”

6

. . . and that there are different types of innovation

Systemic vs Product innovation

Systemic changes require collaborative efforts

Continuous improvement vs Step change

Incremental changes are more easily understood & adopted

Repackaging vs Value Proposition innovation

B of A’s “Keep the change” debit card program changed the VP

Imitators vs Innovators

Copying ideas from elsewhere can still be original in your market

and categorisation can be a matter of perception

7

Six main drivers of innovation were discussed

1. Consumer / Merchant demand

Historically large merchants have been drivers of change

– Increased speed, convenience, consumer loyalty, hence lower costs & higher revenue

Consumers have had little direct influence

– But their choice of payment method is driven by the 6 C’s: Capability, Coverage, Cost, Confidence, Confidentiality, Convenience

2. Technological advancements

New technological capability facilitates innovation

Technology adoption tends to be part of broader strategies

3. Level of security

Confidence is one of the 6 C’s

Innovative payment systems face a challenge to convince

consumers they are secure & trustworthy

8

Six main drivers of innovation were discussed

4. Industry framework

Government has a role to play in ensuring innovation &

efficiency are driven into the payment network

Industry coordination is required for innovation shared across all

players

5. Competition / Market share

In mature markets, maintaining a competitive advantage is key to

acquiring & retaining customers

Many players seek a first mover advantage using innovations

6. Profit

Clear financial incentives spur innovation

The “business case” is King

9

Developing a business case for step change innovation is

problematic - even more so today

Profit margins on payment transactions have been decreasing

Increasing competition in the marketplace

User belief that cost of payments should be constantly reducing

Investment in payments has to compete with other investment opportunities, which tend to provide better returns

Current appetite in FI’s for investment is very low

Step change innovations bring more risk

Tend to be larger investments

Estimating the adoption curve embodies more “guess work”

Longer pay back period, due to low adoption in early years

(consumer payment habits take time to “break”)

May be eclipsed by new technology before reaching critical mass

Despite potential for higher returns, FIs are reluctant to invest

10

Hence focus is on innovation providing continuous

incremental improvement

Consumers more easily understand, accept and adopt innovations that require little change in behaviour

Investment in incremental improvement is lower, and can more easily be unwound

Easier to test market

Easier to build business case with more certainty

Leverages existing systems

Can be substantiated on the adoption by smaller market segments/niches

11

Where were we?

What’s happened since?

Where to from here?

12

Electronic forms of payment have continued to displace

paper

Particularly strong growth in debit card

transactions

Cheque volume has continued to decline

High growth in shopping over the internet

Removal of toll booths and growth in eTags

Steps toward mass transit eTicketing

Open-loop contactless has taken off, and

cash withdrawals have declined

High growth in prepaid travel cards

12

13

Debit cards have lead the recent growth in electronic

payment transaction volume . . .

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Customer Cheque

Direct Debit

Direct Credit

ATM Cash Withdrawal

Credit & Charge Cards

Debit Cards

Tra

nsa

ction

s P

er

Ye

ar

(Mill

ion

s)

Annual Transaction Volume By Type of Retail Payment 2002-2012

Source: RBA Payment Statistics

14

. . . but Direct Entry dominates transaction value

Tra

nsa

ction

Va

lue

Pe

r Y

ea

r ($

Mill

ion

s)

Annual Transaction Value By Type of Retail Payment 2002-2012

Source: RBA Payment Statistics

-

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Customer Cheque

Direct Debit

Direct Credit

ATM Cash Withdrawal

Credit & Charge Cards

Debit Cards

15

At retail level, the value of cash withdrawals has begun

to fall as card activity increases

Tra

nsa

ction

Va

lue

Pe

r Y

ea

r ($

Mill

ion

s)

Annual Transaction Value By Type of Retail Payment 2002-2012

Source: RBA Payment Statistics

-

50,000

100,000

150,000

200,000

250,000

300,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

ATM Cash Withdrawal

Credit & Charge Cards

Debit Cards

16

The second half of 2012 saw “exponential” growth in

contactless payments

Initially contactless issuance was way ahead of acceptance

Acceptance caught up in 2012, spurred by Coles & Woolworths

Public announcements include –

10+m MasterCard PayPass cards on issue

Over 120k contactless terminals deployed

40% of all MasterCard & Visa transactions in Coles are contactless

Over 10% of MasterCard transactions below $100

are contactless

Highest open-loop contactless txn per capita of any

country

In addition, anecdotally –

Many merchants adopting contactless have

removed $ minimums (e.g., Subway)

Massive growth in contactless transactions

under $20

17

$-

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

De

c 9

4

De

c 9

5

De

c 9

6

De

c 9

7

De

c 9

8

De

c 9

9

De

c 0

0

De

c 0

1

De

c 0

2

De

c 0

3

De

c 0

4

De

c 0

5

De

c 0

6

De

c 0

7

De

c 0

8

De

c 0

9

De

c 10

De

c 11

De

c 12

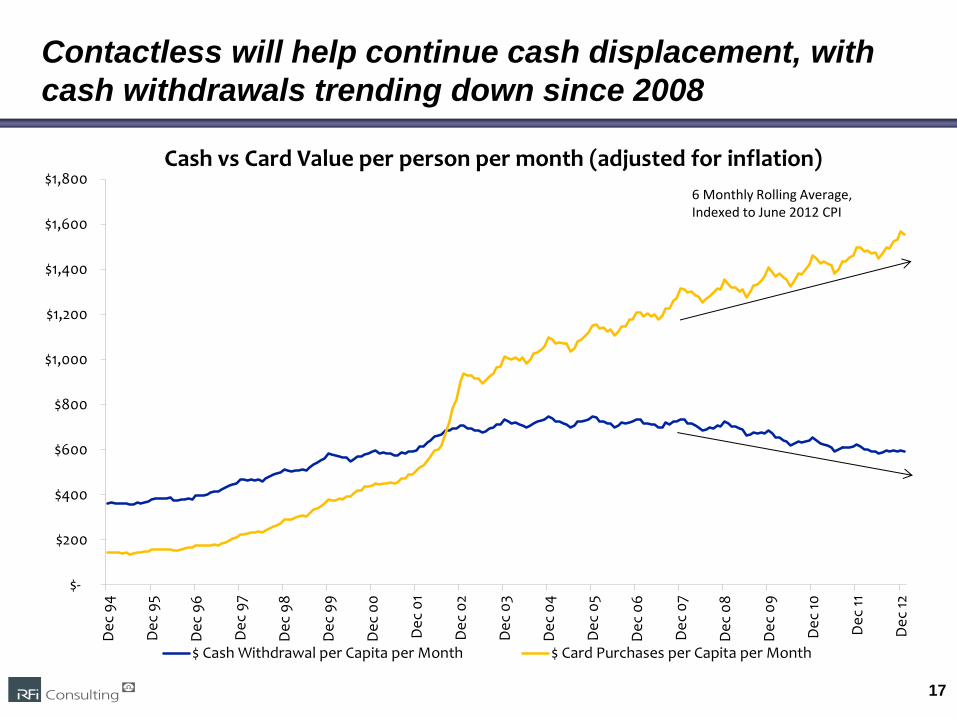

Cash vs Card Value per person per month (adjusted for inflation)

$ Cash Withdrawal per Capita per Month $ Card Purchases per Capita per Month

6 Monthly Rolling Average, Indexed to June 2012 CPI

Contactless will help continue cash displacement, with

cash withdrawals trending down since 2008

18

Online shopping is estimated to have doubled in the last

2-3 years, prompting more electronic payment growth

The online shopping market, subject to many definitions, was estimated at $60 billion in 2009/10

Dominated by the travel sector

Today estimated at around $100 billion, with the growth mainly in non-travel

The strong Australian dollar

Greater consumer comfort

Growing choice amongst

online merchants

Lower prices

NAB estimates online is about 5-6% of Australia's traditional retail sector

Growth, per cent

Number Value

Direct entry 11.8 14.5

BPAY 9.0 13.2

Credit cards, and MasterCard and Visa debit cards

25.0(a) 16.7

Specialised payments providers(b) 41.3 36.6

(a) Includes double-counting of some PayPal transactions

(b) Estimates included for one provider for the March and June quarters

2012

Sources: BPAY; RBA; specialised payments providers

Online Payments by Payment Method

2011/12

19

There have been limited market-wide innovations, but

lots of “localised” activity

Significant dabbling with new technologies/channels, especially mobile

But no coordinated industry approach, with each bank launching

its own “flavour”

Further “work arounds” on information with payment have appeared

AMP CustomSuper: direct credit with reference number

‘Payment Adviser’ linking payroll processing firms and

superannuation funds

Large number of online initiatives

Payment buttons: V.me, MasterPass, PNIPay

20

Where were we?

What’s happened since?

Where to from here?

21

The Payments System Board has outlined strategic

objectives for the future of the payments system

All Direct Entry payments should be settled on the day payment instructions are exchanged by the end of 2013

The capacity for businesses and consumers to make payments in real time, with close to immediate funds availability to the recipient, by the end of 2016

There should be the ability to make and receive low-value payments outside normal banking hours by the end of 2016

Ideally it would also involve the capacity for the settlement of

card payment receipts during weekends and public holidays

Businesses and consumers should have the capacity to send more complete remittance information with payments by the end of 2016

A system for more easily addressing retail payments to any recipient should be available. If provided by a new real-time system, it should be available by the end of 2017

22

The Real Time Payments initiative should provide a

platform on which new payment approaches can be based

The RTP’s proposed information / data with payment should tackle a need identified for many years in the B2B market

Further removing cheques (and cash)

from this sector

The “initial convenience service” aims to leverage the mobile channel

Hopefully dealing with the interbank issues of current

proprietary bank mobile payment systems

The addressing of payments without account information should:

Provide convenience / ease

Meet the security concerns of some payees

Speed per se may be less of a differentiator as DE moves to intra day settlement

23

Mobile NFC is likely to take off once mass transit

eTicketing is in place, particularly when it goes open-loop

Although contactless is becoming more widespread, the move to mobile for these transactions should not be taken for granted

Experience in other markets indicates mobile NFC payments can be driven by mass transit ePayments

Yet to see whether the Australian transit authorities will permit their proprietary applications on mobiles

Sydney transit, for one, has indicated an eventual move to open-loop card formats, leading the way for mobile NFC

24

Cheque usage will continue to decline

Generational change

Further inroads of existing electronic payment methods

RTP initiative

The issue of how to deal with the last few cheques remains

Cash usage is likely to be further attacked by cards, both contactless and contact, as well as eTicketing

Surcharging controls and removal of card minimums will help

The growth of online shopping also removes paper

The continued displacement of paper should continue

and be encouraged

25

Will innovation in payments help us capture the $2+ billion

DCITA report cost savings & drive the digital economy?

1. Moving cash to (debit) cards

This seems to be happening, major thrust of contactless

2. Lowering the electronic payment threshold

eTags, eTicketing and contactless cards are attacking this

3. Electronic bill payments

RTP initiative should help address the need for data / information

with payment

4. B2B payment opportunities

Electronic bill presentment & e-invoicing, e-conveyancing,

superstream reforms

5. Migrating cheques to direct entry

Cheques are in significant decline, and RTP initiative should help

accelerate

26

DISCUSSION