the innovation ecosystem of tanzania · the innovation ecosystem of tanzania 18 may 2017. this...

TRANSCRIPT

The Innovation Ecosystem of

Tanzania18 May 2017

This material has been funded by UK Aid from the UK government; however, the views expressed are those of the authors and do not necessarily reflect the UK government’s official policies.

Presentation Overview

• Research methodology• Findings - Defining innovation - Innovation ecosystem stakeholders - Connections within the ecosystem - Barriers to Innovation - Next steps• Launch of online interactive map

Guiding Research Questions

1. Who are the key players in Tanzania’s innovation ecosystem?

2. What are the gaps and opportunities in the ecosystem?

3. Where and how is the innovation ecosystem connecting?

Research Methodology

• Champion Connectors individuals or organisations in different geographies and sectors who are connected to innovation stakeholders

• Geographic spread cover every region of Tanzania (surveys) or zone (in-depth interviews)

• Stakeholder group spread cover different types of innovation ecosystem stakeholders

Research Participants

twentynineOther surveys(including international)

Tota

lin

ter

vie

ws

35329Total surveys

34surveys

Lake Zone

FIVEIn-depth interviews

111surveys

Coastal

14In-depth interviews

70 su

rv

ey

s

Northern

SixIn-depth interviews

11surveys

Central

ONEIn-depth interview

42surveys

SouthernHighlands

FourIn-depth interviews

32 su

rv

ey

s

Zanzibar

six

In-depthinterviews

GeographicDistributionof participants

Stakeholder Groups

Stakeholder groups were defined as: InnovatorIncubator / Accelerator Thought Leader / MentorFunder Hub / Living Lab Government / Policy MakersUniversity / Research Institution Networks / Associations

Sample Size Stakeholders by Group

SURVEY

Stakeholder Group Number of stakeholders participatedInnovator (Business or NGO) 217Incubator /Accelerator 22Thought Leader / Mentor 20Funder (including donor, investor, bank, or any other 8 formal financial institution)Hub / Living Lab 13Government 11University / Research Institution, Teaching Institution 17 Networks / Associations 21

Total 329

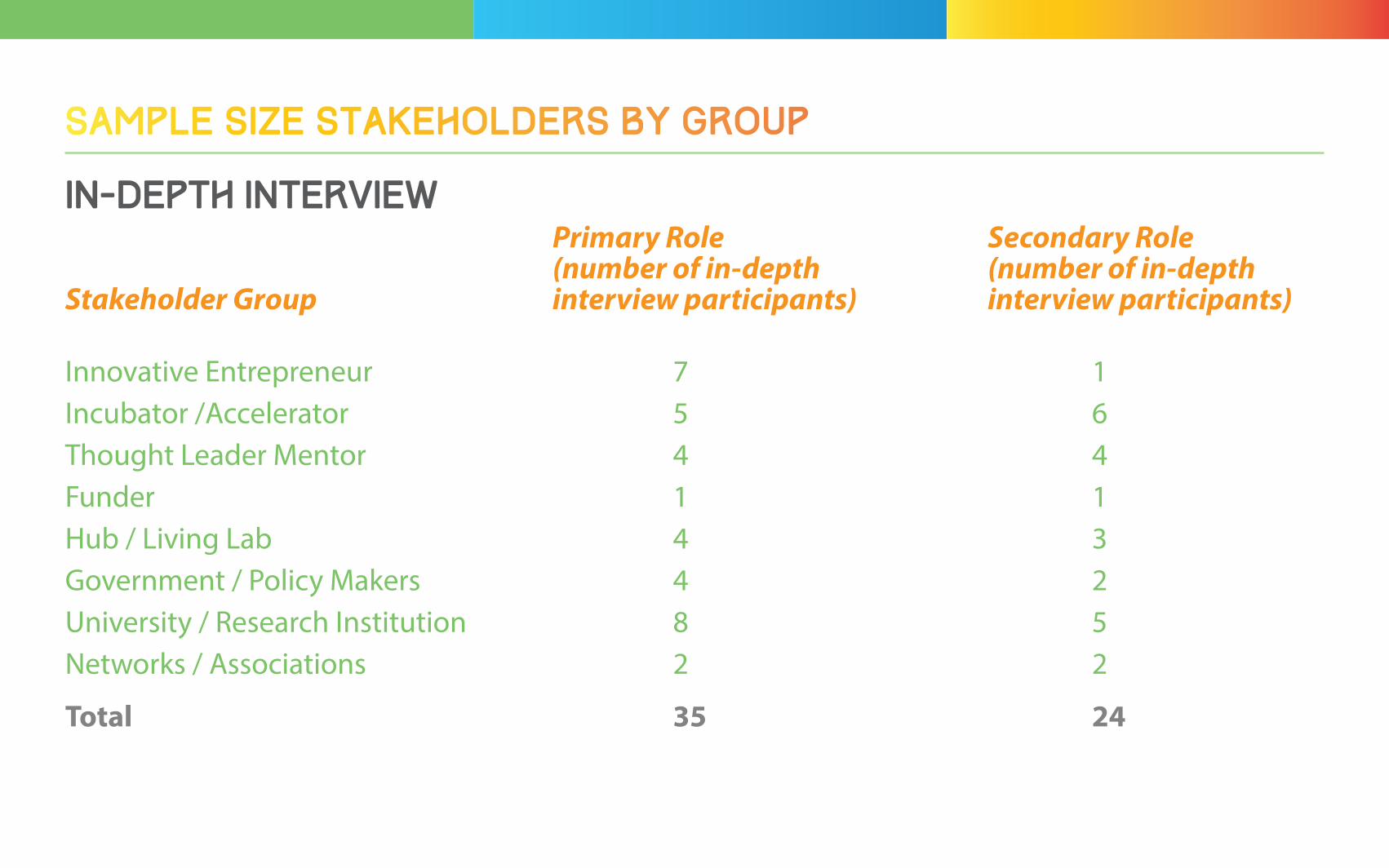

IN-DEPTH INTERVIEW Primary Role Secondary Role (number of in-depth (number of in-depthStakeholder Group interview participants) interview participants) Innovative Entrepreneur 7 1Incubator /Accelerator 5 6Thought Leader Mentor 4 4Funder 1 1Hub / Living Lab 4 3Government / Policy Makers 4 2University / Research Institution 8 5Networks / Associations 2 2

Total 35 24

Sample Size Stakeholders by Group

• Survey - 329 completed - Used an online, in-person, and over the phone

structured questionnaire• In-depth interview

- 35 completed - Used an in-person and over the phone

semi-structured questionnaire

Data Collection Tools

In-depth interviews screened for recurring themes

Research Analysis Process

In-depth interviews screened for recurring themes

Themes guide structure of report

Research Analysis Process

In-depth interviews screened for recurring themes

Themes guide structure of report

Survey data analysed for trends

Research Analysis Process

In-depth interviews screened for recurring themes

Themes guide structure of report

Survey data analysed for trends

Survey results inputted into thematic structure to clarify results

Research Analysis Process

Findings

Defininginnovation

8

innovation: A product, service, or process that is new to the world, new to Tanzania, or new to the region

Defining Innovation

“Innovation is adding value, not necessarily something completely new.”

“Innovations must be affordable, sustainable and customised. You need to make it for the community.”

Innovation ecosystem stakeholders

Innovation Ecosystem Stakeholders

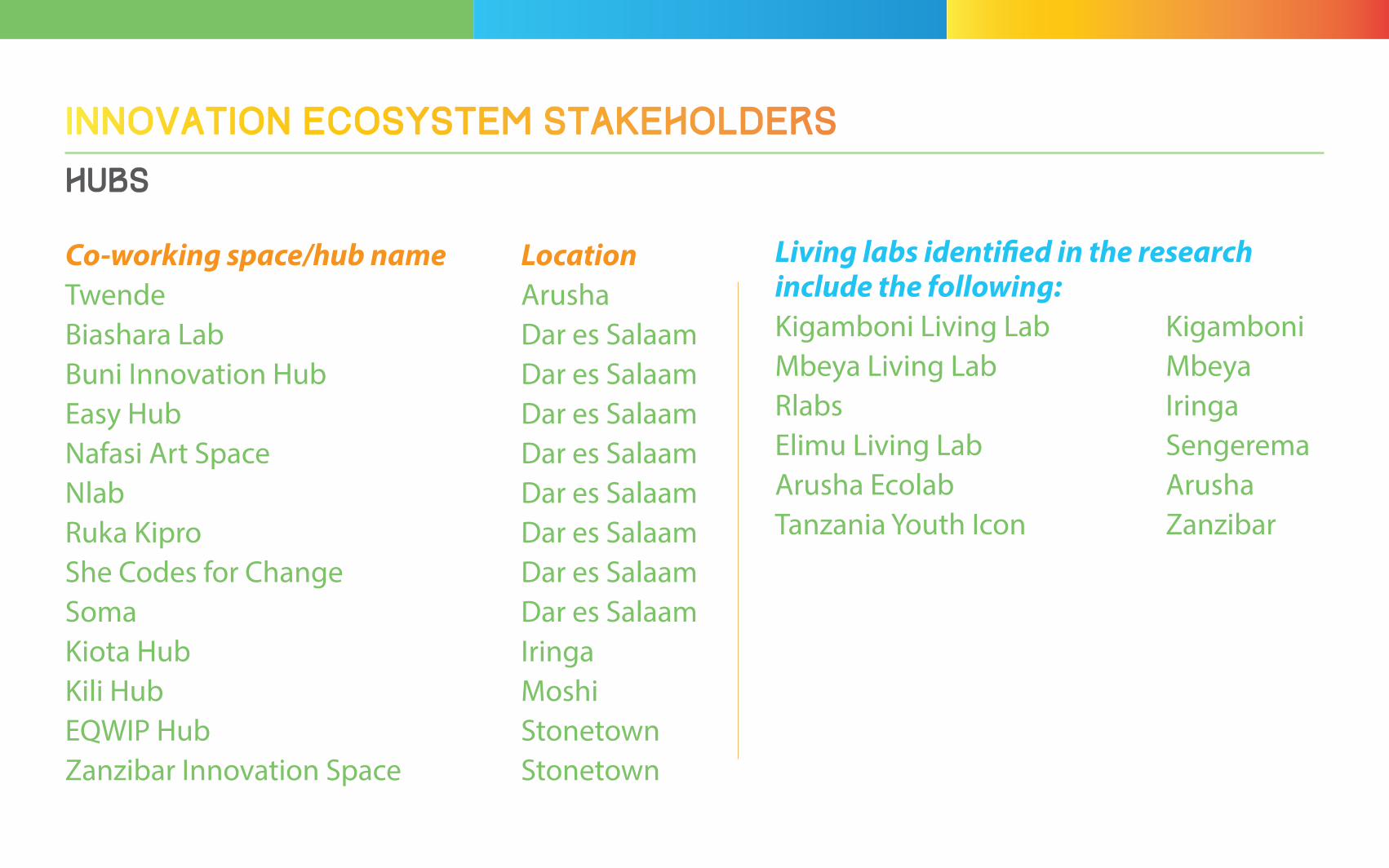

Living labs identified in the research include the following:Kigamboni Living Lab KigamboniMbeya Living Lab MbeyaRlabs IringaElimu Living Lab SengeremaArusha Ecolab ArushaTanzania Youth Icon Zanzibar

Co-working space/hub name LocationTwende ArushaBiashara Lab Dar es SalaamBuni Innovation Hub Dar es SalaamEasy Hub Dar es SalaamNafasi Art Space Dar es SalaamNlab Dar es SalaamRuka Kipro Dar es SalaamShe Codes for Change Dar es SalaamSoma Dar es SalaamKiota Hub IringaKili Hub MoshiEQWIP Hub StonetownZanzibar Innovation Space Stonetown

Hubs

New Hubsper Year

1997 | 2007 | 2008 | 2010 | 2011 | 2013 | 2014 | 2015 | 2016

1

20

10

15

56

89

11 12

1720

13

1

Fee Chargedfor Services

equity investment

Corporatesponsorship $

40%

90%

20%

0% Grants/externalfunding

$30%$tanzaniangovernment funding

30%$$

InternalRevenue

Sources of funding

Hubs

Innovation Ecosystem Stakeholders

Name of Incubator/Accelerator LocationTanzania Renewable Energy Business Incubator (TAREBI) Dar es Salaam

Anza Accelerator Moshi

Reach for Change Foundation Dar es Salaam

SPRING Accelerator Moshi, Dar es Salaam

Dar Teknohama Business Incubator (DTBi) Dar es Salaam

Zanzibar Technology Business Incubator (ZTBI) Miembeni

Ecom Research Group Dar es Salaam

Kakute Arusha

Sokoine University of Agriculture Graduate Morogoro Entrepreneurs Cooperative (SUGECO)

TLED Project (VSO International) Mtwara, Lindi, Iringa, Mwanza

Twende Arusha

Incubators and Accelerators

Innovation Ecosystem Stakeholders

Incubators and Accelerators

Innovation Ecosystem Stakeholders

Incubators and AcceleratorsStage of businesses supported by

incubators and accelerators

32%

Ideation/research

45%36%

pilot project/product

started operations/pre-revenue p

ro

fit

ab

le

Revenue-earning,not yet profitable

Percentage ofinnovation supportstakeholders*offering differenttypes of support,by zone 9%

5%

20%34%

5%9%

14%

5%

20%

Northern

8%

6%4%

16%18% 14%

15%13%8%

Zan

zib

ar

8% 6% 4%

16%18%14%

15%

13%

8%

Lake Zone

4%12% 9%

16%16% 16%

12%11%

5%

Co

as

tal

SouthernHighlands

14%

21%7%

14%14%

0%

14%

14%

0%

5%

14%

5%

14%

10%

5%19%

10% 10%

central

advocacy

WorkingOffice space

Professionaladvice

Equipment

Knowledge centre/resource library

mentorship

funding/investment

Networking/Linkages

information

$ Fee Chargedfor Servicesequity

investment

Corporatesponsorship

$ 45%

59%14%

9%

Grants/externalfunding

$9%

$tanzaniangovernment funding

$ $Internal Revenue55%

Sources of funding

Incubators and Accelerators

Innovation Ecosystem Stakeholders

Individuals

Reginald Mengi 14 mentions

Said Salim Bakhresa 8 mentions

Mohamed Dewji 6 mentions

• Only a handful of respondents self-identified as mentors in the survey

• Out of the role models mentioned by survey participants, only a few received more than five mentions

Top 3 role models mentioned by survey participants

Innovation Ecosystem Stakeholders

Funders

• Small sample size

• Included in stakeholder group: donors, angel investors, banks, investors, microfinance institutions, challenge funds, other finance institutions

• Access to finance cited as top barrier to innovation

Innovation Ecosystem Stakeholders

Government

• Several initiatives cited COSTECH, SIDO, NEEC, TIRDO, TEMDO, CAMARTEC, government ministries and research institutes

• Issues around decentralisation, taxation, business licensing and registration

“embed advisors within the government specifically focused on

public-private partnerships”

Innovation Ecosystem Stakeholders

Academia and educators

• Education considered a major factor in developing innovation attitude

• Entrepreneurship and innovation treated as

cross-curricula rather than separate subjects

“innovators need to see readily accessible success stories to encourage them to innovate”

Innovation Ecosystem Stakeholders

Media

• Missing component of initial stakeholder groups

• Integral to sharing success and failure stories and highlighting local or sector-specific role models

“international and national media does not highlight Tanzanian innovations”

Connections within the ecosystem

Where innovation ecosystemstakeholders access

information on innovation

46%

19.8

%

19.5

%

17.6

%

12.2

%

11.9

%

10%

7.9%

7.9%

5.5%

Internet Universities/education/

training centres

Peer interaction Networks Conferences/workshops/

trainings

Publications/media/booksnewsletter

Experts insector

SIDO Government/ministries

Research

50

25

Connections within the ecosystem

Connections within the ecosystem

• 58% of survey respondents indicate belonging to a network or association

• Spread – some local and some national

24%$tanzaniangovernment funding $

Grants/externalfunding

48%Fee Chargedfor Services

38%$Corporatesponsorship

14%$

equityinvestment

0%$81%Internal Revenue

Sources of funding

Networks & associations

Connections within the ecosystem

• Anecdotal evidence points to whatsapp groups and facebook groups as platforms for connection

• Kijana Jiajiri• World Beekeepers Forum• Tanzania Social Entrepreneurship Forum

Connections within the ecosystem

• 68% of survey respondents indicated working with a partner (defined by joint activities, collaboration and/or resource sharing)

• Several in-depth interview participants mentioned that partnerships were not necessarily high-value

mention working withacademia and research

60%30%mention partneringwith businesses

Among governmentministries, departments,

or agencies,thirtyfour%22%

Among innovative business participants,

indicate working in partnershipwith the government,

indicateworking withacademia/research

Among universities and research respondents,

fifteen%mentionpartneringwithbusinesses;

indicate workingwith governmentpartners 38%

Business

Government

University

Effective TripleHelix Structure& Process

Innovation-basedeconomic growth

source: Stanford University Triple Helix Research Group, “The triple helix concept.”

Connections within the ecosystem

Barriers to Innovation

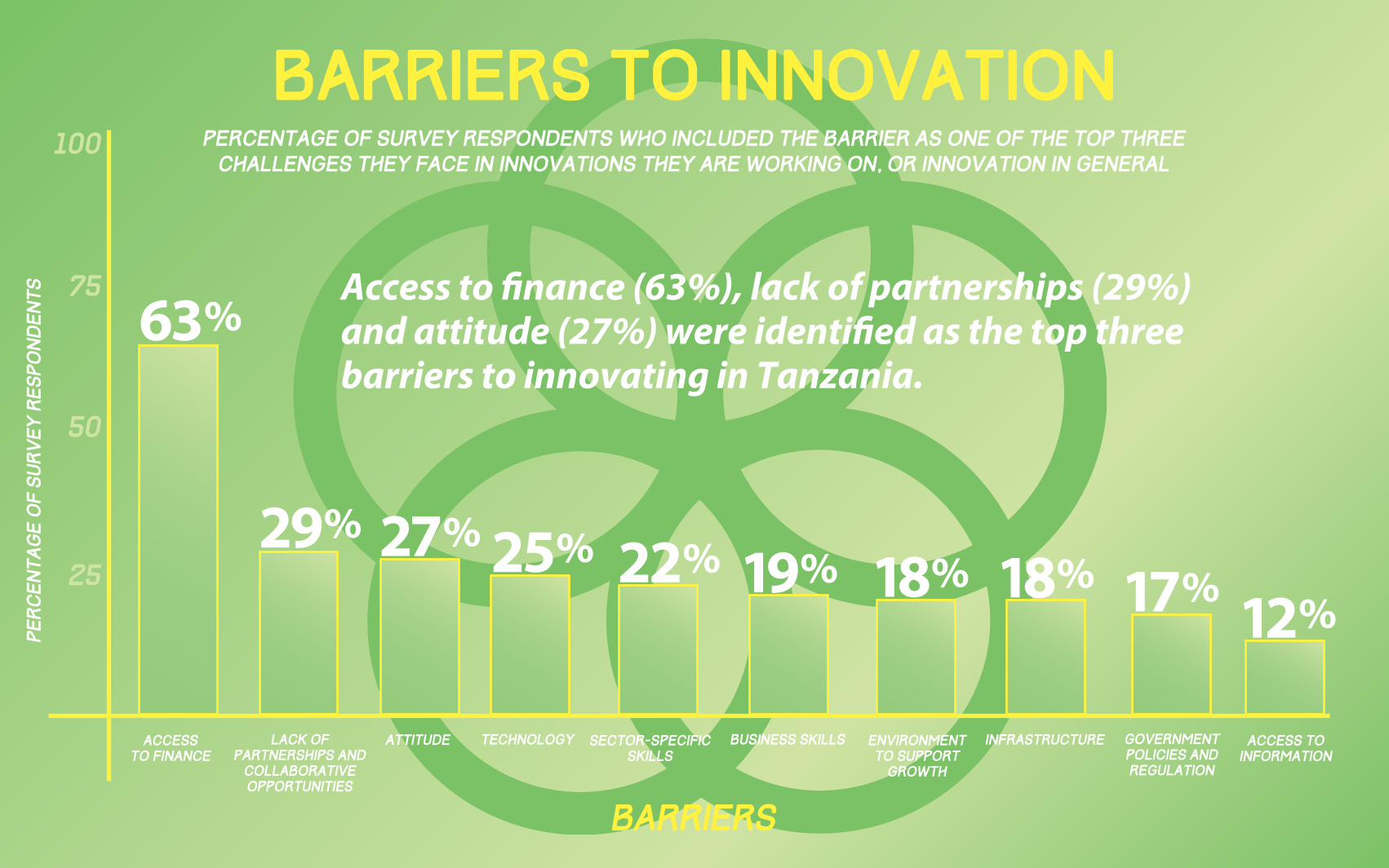

Barriers to InnovationBarriers to innovation

63%

29% 27% 25% 22% 19% 18% 18% 17% 12%

Accessto finance

Barriers

Percentage of survey respondents who included the barrier as one of the top three challenges they face in innovations they are working on, or innovation in general

Per

ce

nta

ge

of

su

rv

ey

re

spo

nd

en

ts

Access toInformation

Lack ofpartnerships and

collaborativeopportunities

Attitude Technology Sector-specificskills

Business skills Environmentto support

growth

Infrastructure GovernmentPolicies andRegulation

100

50

25

75 Access to �nance (63%), lack of partnerships (29%) and attitude (27%) were identi�ed as the top three barriers to innovating in Tanzania.

Next steps

• Awareness around different types of innovation and innovators (hubs, media, educators)

• Make local case studies available to aspiring or early-stage entrepreneurs through existing platforms

• Increase incentives for collaboration and financial access

• Delineate clear responsibilities in the ecosystem to address barriers