the importance of measuring credit risk beroepsvereniging van beleggingsprofessionals 21 april 2008...

TRANSCRIPT

The importance of measuring credit risk

Beroepsvereniging van Beleggingsprofessionals21 april 2008

Tom van Zalen

2 2

Agenda

• What is credit risk?• The importance of credit risk• Modeling credit risk• A link to the recent credit crunch

Cre

dit R

isk

Cre

dit R

isk

Cre

dit R

isk

3 3

Agenda

• What is credit risk?– Definition– Credit risk drivers– Systematic versus non-systematic risk

• The importance of credit risk• Modeling credit risk• A link to the recent credit crunch

Cre

dit R

isk

Cre

dit R

isk

Cre

dit R

isk

4 4

What is credit risk?

• Credit risk, a definition:Credit risk is the risk of loss due to a debtor's non-payment of a loan or other line of credit (either the principal or interest (coupon) or both).

But also:

The risk of value losses following from a change in external credit factors.

Cre

dit R

isk

Cre

dit R

isk

Cre

dit R

isk

5 5

What is credit risk?

• External credit factors:–Micro

• Individual risk single debt instrument = status quo firm reflected in rating (and thus the credit spread)

–Macro• Collective risk fixed income portfolio = status quo

economy reflected in business cycle

Cre

dit R

isk

Cre

dit R

isk

Cre

dit R

isk

6 6

What is credit risk?

• Micro: determinants rating:–Liability risk ~ volume debt versus equity–Asset risk ~ volume tangible or intangible–Cash flow risk ~ e.g. profitability, sales, repayment capacity

• Macro: determinants business cycle:–Inflation and economic growth: Y = C + I + G + T

• Market risk is aggregated liquidity and credit risk• Market risk is systematic or not diversifiable

Cre

dit R

isk

Cre

dit R

isk

Cre

dit R

isk

7 7

What is credit risk?C

red

it Ris

kC

red

it Ris

kC

red

it Ris

k-25

0

25

50

75

100

125

150

175

200

225

Apr-99 Oct-99 Apr-00 Oct-00 Apr-01 Oct-01 Apr-02 Oct-02 Apr-03 Oct-03 Apr-04 Oct-04

AAA AA A BBB

8 8

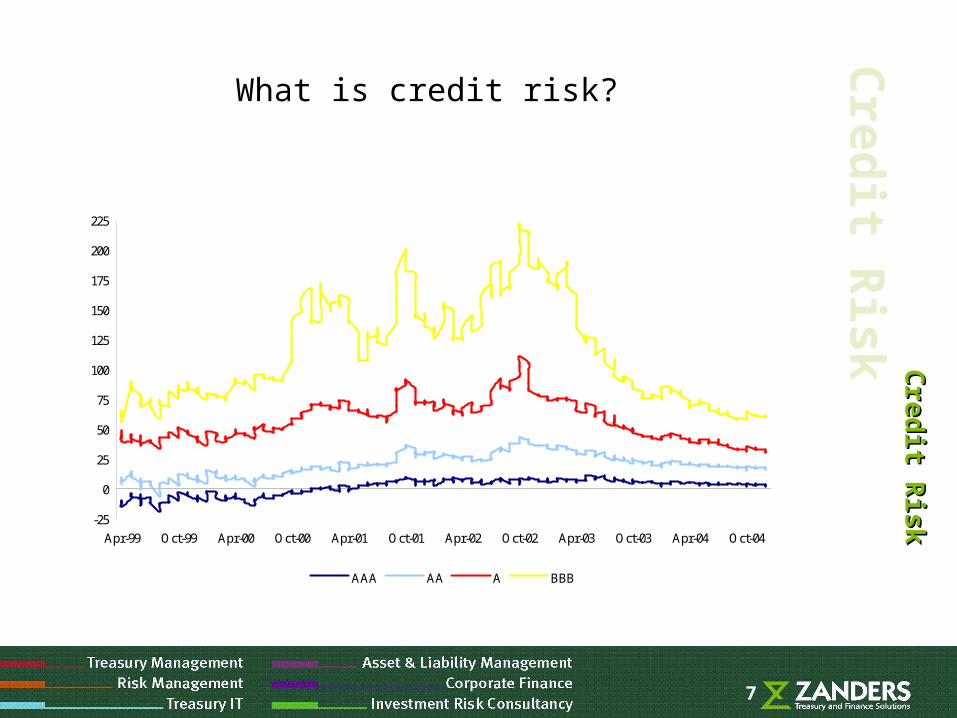

What is credit risk?

• Yield spreads largely depend upon rating, as a proxy for credit risk

–Lower ratings face higher yield spreads• Convex relation: lower ratings face relative higher

spreads

–Systematic market risk is significant• Lower ratings face relative higher non-systematic credit

risk• Cyclical behaviour credit risk (credit cycles)• Counter cyclical dependence (higher correlation during

crashes)

Cre

dit R

isk

Cre

dit R

isk

Cre

dit R

isk

9 9

Agenda

• What is credit risk?

• The importance of credit risk– Credit risk in the Euro-area– Market participants

• Modeling credit risk• A link to the recent credit crunch

Cre

dit R

isk

Cre

dit R

isk

Cre

dit R

isk

10 10

Credit risk in the Euro-area

• Market funding offsets bank lending–Monetary integration = Euro ~ Liquidity

• Deregulated capital of institutional investors goes Europe• Sovereigns face lower deficits due to disciplinary rules

Brussels• Corporate entities go public more easy

–Des-intermediation bank ~ Credit risk

• Financial regulation encourages credit risk management

–Central banking = Basel II / Solvency II–Accounting = IFRS

Cre

dit R

isk

Cre

dit R

isk

Cre

dit R

isk

11 11

Credit risk in the Euro-area

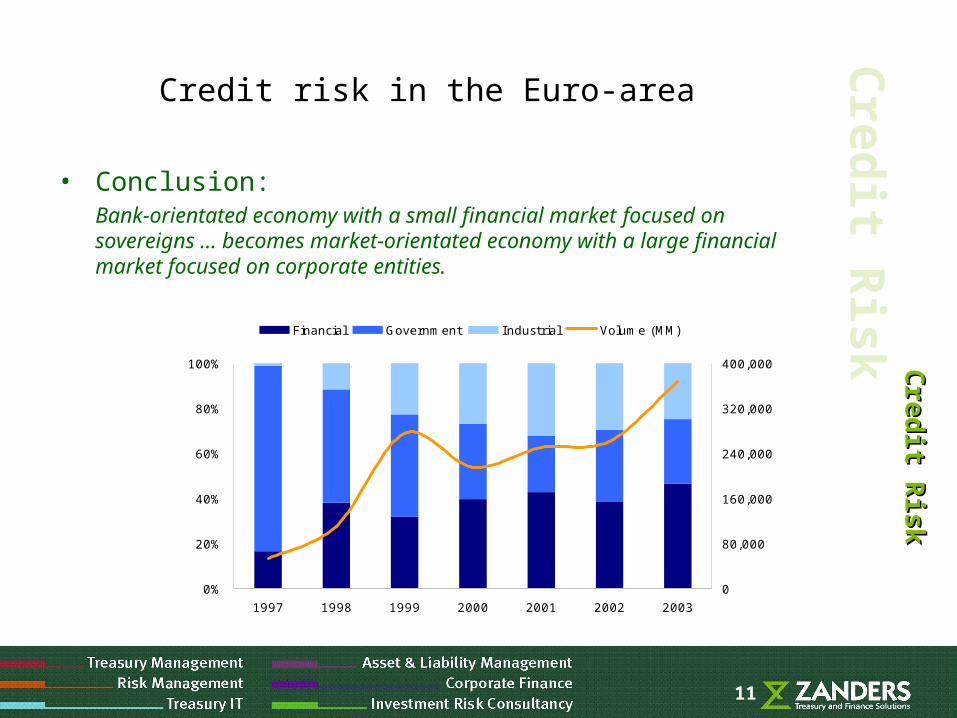

• Conclusion:Bank-orientated economy with a small financial market focused on sovereigns … becomes market-orientated economy with a large financial market focused on corporate entities.

Cre

dit R

isk

Cre

dit R

isk

Cre

dit R

isk

0%

20%

40%

60%

80%

100%

1997 1998 1999 2000 2001 2002 2003

0

80,000

160,000

240,000

320,000

400,000

Financial Government Industrial Volume (MM)

12 12

Credit risk in the Euro-area

• Conclusion:Introduction Euro eliminates foreign exchange risk, which has caused intensified focus upon credit risk. Diversification over rating classes has improved, although the average rating decreased and may explain higher price volatility.

Cre

dit R

isk

Cre

dit R

isk

Cre

dit R

isk

0%

20%

40%

60%

80%

100%

1997 1998 1999 2000 2001 2002 2003

0

80

160

240

320

400

AAA AA A BBB Issuance (#)

13 13

Market participants

• Banks (traditionally)–Pricers of risk (loan originations)–Sellers of risk (securitization = credit risk transfer of higher rated bonds)

• High-rated homogeneous asset-backed securities (e.g. mortgages)

• Medium-rated heterogeneous collateralized debt obligations (=tranching & structured)

• Asset managers–Traders of risk–Buyers of risk (investment management)

Cre

dit R

isk

Cre

dit R

isk

Cre

dit R

isk

14 14

Market participants

• Hedge funds–Traders of risk (zero-position = arbitrage = long/short strategies)–Sellers & buyers of risk

• Private equity–Pricers of risk–Sellers of risk (funding using lower-rated by issuing high-yield bonds)

Cre

dit R

isk

Cre

dit R

isk

Cre

dit R

isk

15 15

Market participantsC

red

it Ris

kC

red

it Ris

kC

red

it Ris

k

Investment grade

Non-investment grade

Banks

Private Equity

InstituionalInvestors

Buyers Traders Sellers

Hedge funds

Banks

Private equity

Institutional Investors$ Premiums

$ Savings

Accounting

Trading portfolio“Hold-to-maturity”

$

16 16

Agenda

• What is credit risk?• The importance of credit risk

• Modeling credit risk– Expected loss– Unexpected loss

• A link to the recent credit crunch

Cre

dit R

isk

Cre

dit R

isk

Cre

dit R

isk

17 17

Modeling credit risk

• Credit risk is the probability of default (PD) of a loss given default (LGD) due to changes in external credit factors

• Follows from credit loss distribution

• Measured by:– Expected loss (μ)– Unexpected loss (σ)

Cre

dit R

isk

Cre

dit R

isk

Cre

dit R

isk

18

3 bpExpected

ValuePromised

Value

SD

Frequency

Portfolio Value

Risk Capital (unexpected loss)

EL

3 bpExpected

ValuePromised

Value

SD

Frequency

Portfolio Value

Risk Capital (unexpected loss)

EL

0μ =ELEconomic capital

UL

18

Modeling credit risk- Expected lossC

red

it Ris

k

• Credit loss distribution function

Cre

dit R

isk

Cre

dit R

isk

19 19

Modeling credit risk- Expected loss

• Expected loss– Measures the expected loss on a (portfolio of) loans given

the characteristics of the counterparty and the loan conditions and the presence of collateral.

– Is the μ of the credit loss distribution.

Expected loss = probability of default x loss given defaultE[L] = PD x LGD = % x % = %

– Credit spread = E[L] + liquidity spread

Cre

dit R

isk

Cre

dit R

isk

Cre

dit R

isk

20 20

Modeling credit risk – Expected loss

• Probability of default– Probability that a firm will default on its payment obligations

(e.g. coupon payments, principal repayment) within one year.

– Often follows from rating

Cre

dit R

isk

Cre

dit R

isk

Cre

dit R

isk

21 21

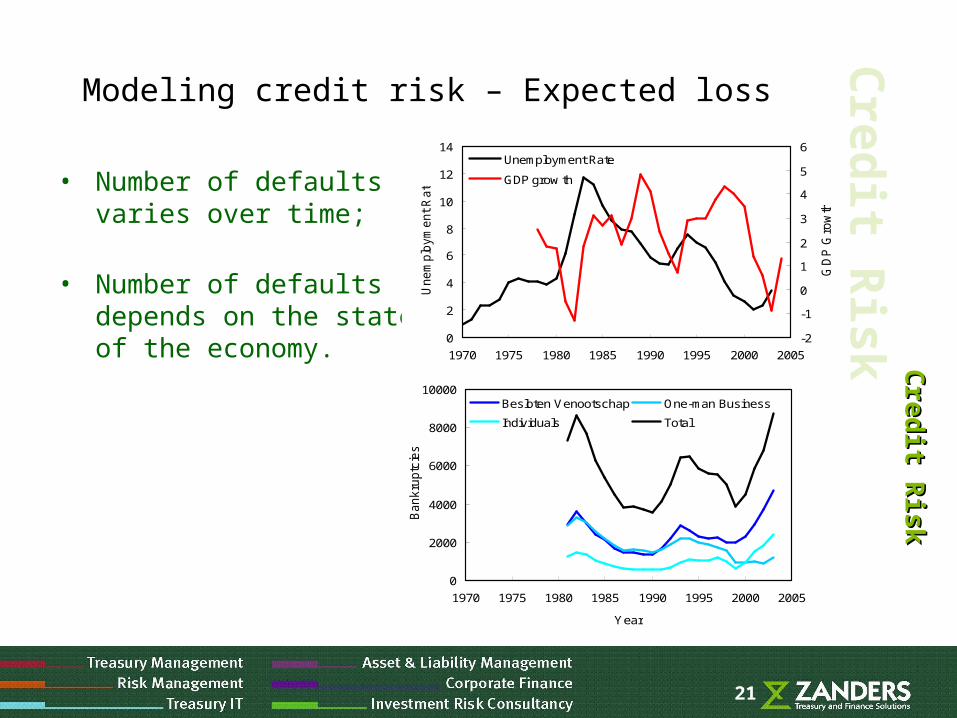

Modeling credit risk – Expected loss

• Number of defaultsvaries over time;

• Number of defaultsdepends on the stateof the economy.

Cre

dit R

isk

Cre

dit R

isk

Cre

dit R

isk

0

2

4

6

8

10

12

14

1970 1975 1980 1985 1990 1995 2000 2005

Year

Unem

plo

ym

ent R

ate

-2

-1

0

1

2

3

4

5

6

GD

P G

row

th

Unemployment Rate

GDP grow th

0

2000

4000

6000

8000

10000

1970 1975 1980 1985 1990 1995 2000 2005

Year

Bankru

ptc

ies

Besloten Venootschap One-man Business

Individuals Total

22 22

Modeling credit risk – Expected loss

• Loss given default– The fraction of the outstanding loan that will not be

recovered once default occurred.

– Influenced by:• Collateral• Guarantees

• Value of collateral may be correlated with the occurrence of default:

– Example: commercial real estate mortgages– “Haircuts” provide a correction for this issue

Cre

dit R

isk

Cre

dit R

isk

Cre

dit R

isk

23 23

Modeling credit risk – Unexpected loss

• Unexpected loss– If the realized credit loss would always equal its expected

value, then there would be no risk.– In practice however, the credit loss is stochastic in nature

and thus risk arises.– The possible deviation from the expectation is risk and is

measured by the standard deviation of the loss distribution.– Unexpected loss is the σ of the credit loss distribution

Cre

dit R

isk

Cre

dit R

isk

Cre

dit R

isk

24 24

Modeling credit risk – Unexpected loss

• Default occurrence– Occurrence of default follows a binomial distribution:

• With probability PD a default will occur• With probability 1 – PD no default will occur

– For a portfolio with n loans, all having the same PD, the total number of defaults is distributed as follows:

# defaults ~ Binomial(n, PD):

µ = n x PD σ2 = n x PD x (1 – PD)

Cre

dit R

isk

Cre

dit R

isk

Cre

dit R

isk

25 25

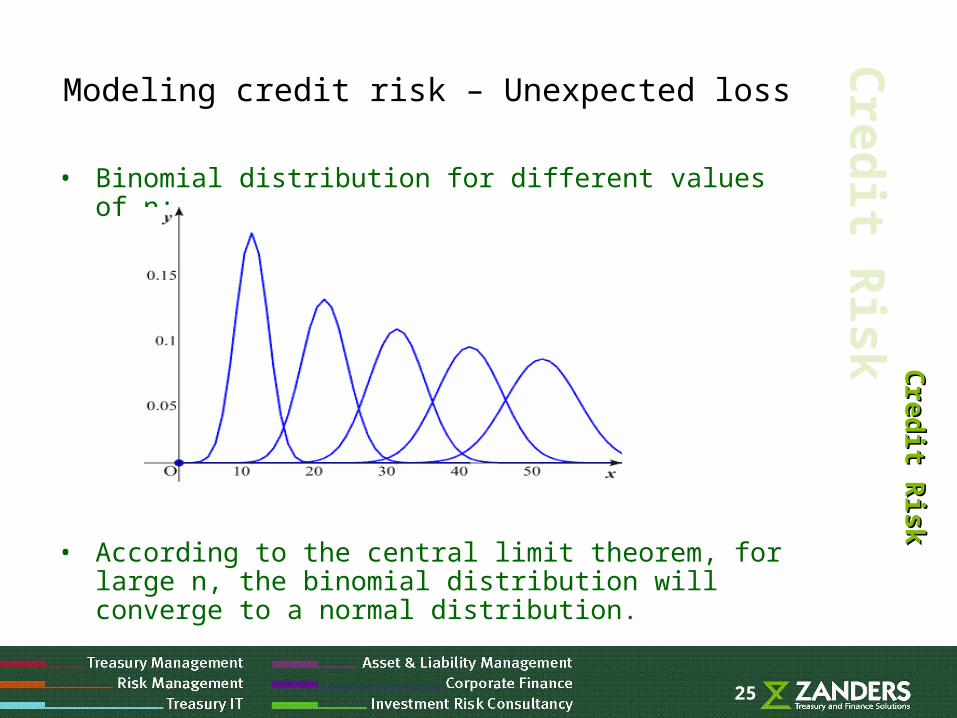

Modeling credit risk – Unexpected loss

• Binomial distribution for different values of n:

• According to the central limit theorem, for large n, the binomial distribution will converge to a normal distribution.

Cre

dit R

isk

Cre

dit R

isk

Cre

dit R

isk

26 26

Modeling credit risk – Unexpected loss

• Loss given default:– For a long time assumed constant due to:

• Complexity reasons• Little effect to loss distribution compared to uncertainty

in the default event.– Random variable with values: 0% < LGD < 100%

• Is modeled using a Beta distribution:– Distribution can be bound between two points– Distribution can have a wide range of shapes

Cre

dit R

isk

Cre

dit R

isk

Cre

dit R

isk

27 27

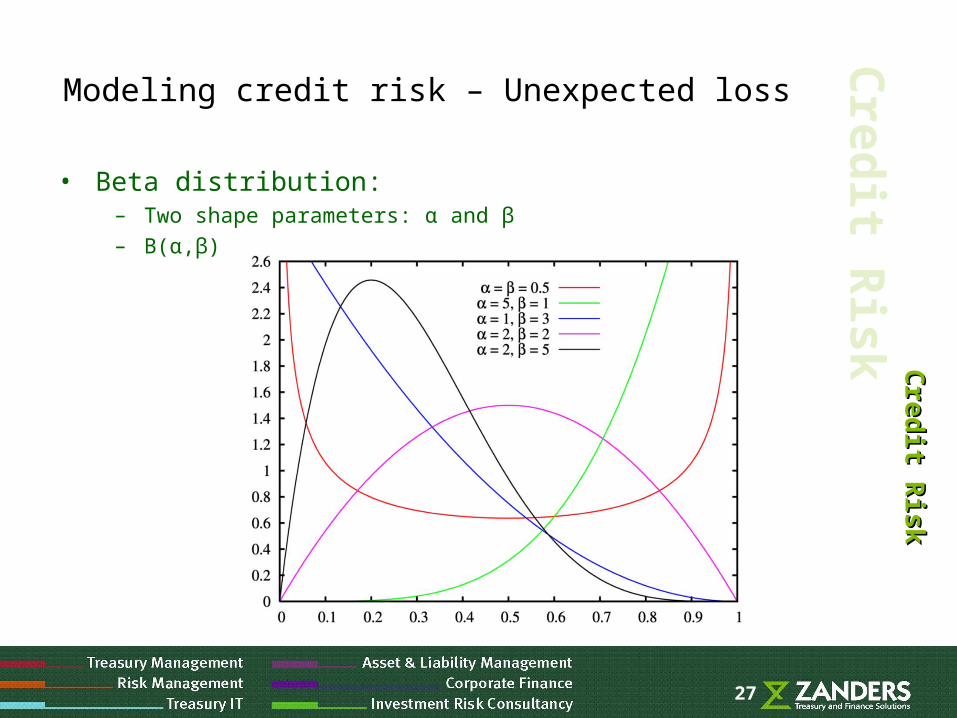

Modeling credit risk – Unexpected loss

• Beta distribution:– Two shape parameters: α and β– B(α,β)

Cre

dit R

isk

Cre

dit R

isk

Cre

dit R

isk

28 28

Modeling credit risk – Unexpected loss

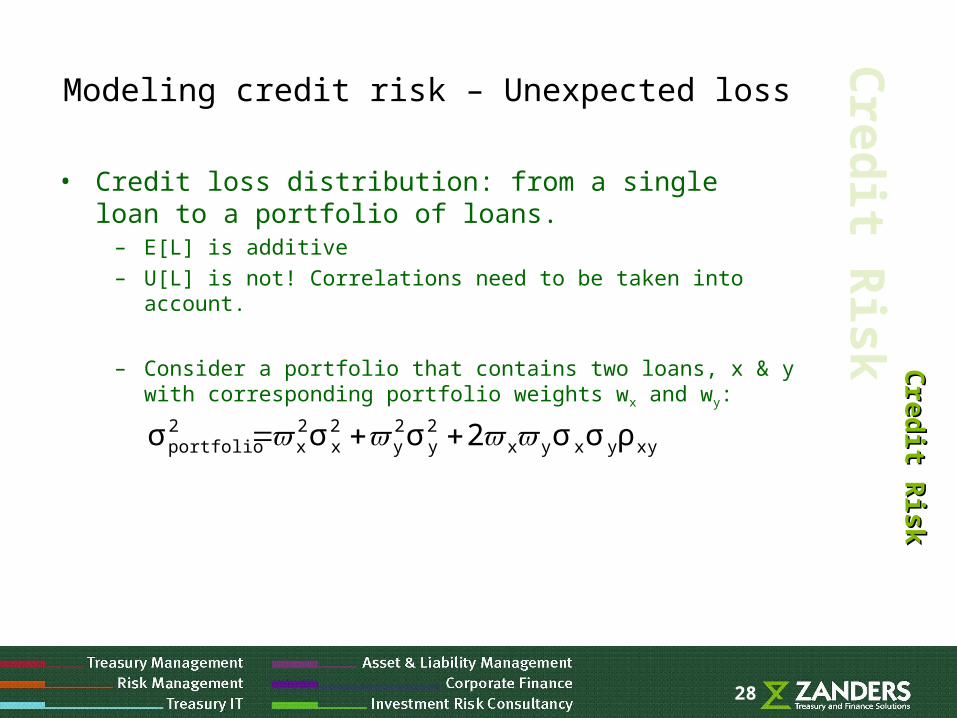

• Credit loss distribution: from a single loan to a portfolio of loans.

– E[L] is additive– U[L] is not! Correlations need to be taken into account.

– Consider a portfolio that contains two loans, x & y with corresponding portfolio weights wx and wy:

Cre

dit R

isk

Cre

dit R

isk

Cre

dit R

isk

xyyxyx2y

2y

2x

2x

2portfolio ρσσ2σσσ

29 29

Agenda

• What is credit risk?• The importance of credit risk• Modeling credit risk

• A link to the recent credit crunch– Structured finance– Correlations

Cre

dit R

isk

Cre

dit R

isk

Cre

dit R

isk

30 30

A link to the recent credit crunch

• Structured finance– Pooling of assets and the subsequent sale to investors of

tranched claims on the cash flows backed by these pools.

– Characterized by:• Pooling of assets• De-linking of credit risk• Tranching of liabilities

– Key aspect of tranching:• Create one or more classes of securities whose rating is

higher than the average rating of the underlying asset pool.

Cre

dit R

isk

Cre

dit R

isk

Cre

dit R

isk

31 31

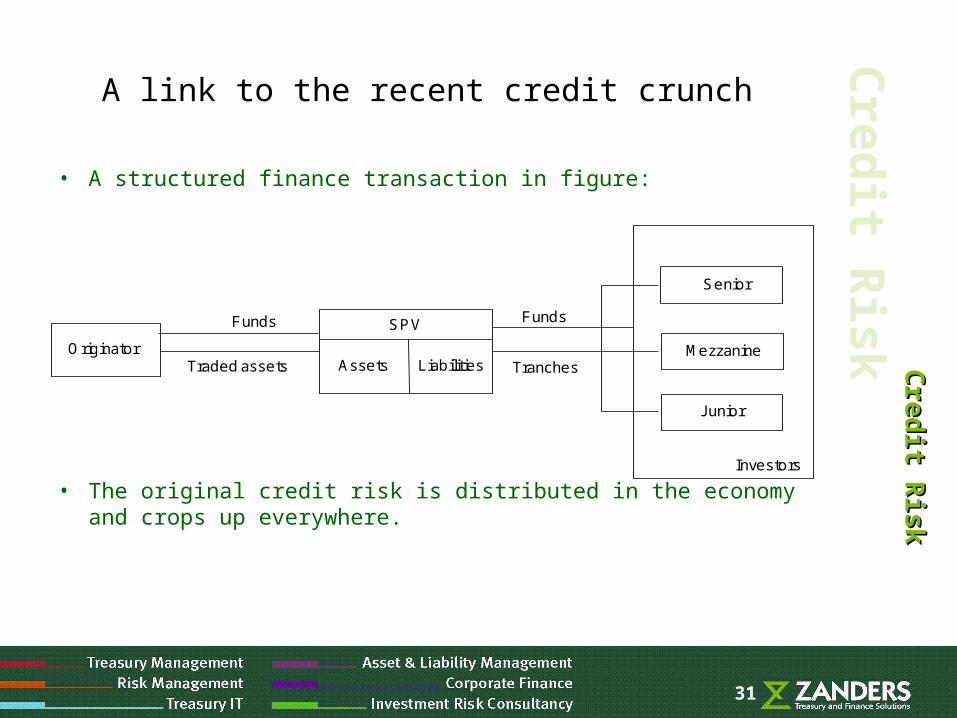

A link to the recent credit crunch

• A structured finance transaction in figure:

• The original credit risk is distributed in the economy and crops up everywhere.

Cre

dit R

isk

Cre

dit R

isk

Cre

dit R

isk

SPV

Assets Liabilities

Senior

Mezzanine

Junior

Investors

OriginatorTraded assets

Funds

Tranches

Funds

32 32

A link to the recent credit crunch

• Tranching is made possible by imperfect correlation between the assets in the original asset pool.

• A diversified pool of risky assets is expected to have a relatively predictable return pattern.

• Tranched pool is structured in such a way that:– E[L] of original asset pool = E[L] of total tranched pool– U[L] of original asset pool = U[L] of total tranched pool

• E[L] and U[L] are portioned and attributed to the different classes in the tranched pool.

Cre

dit R

isk

Cre

dit R

isk

Cre

dit R

isk

33 33

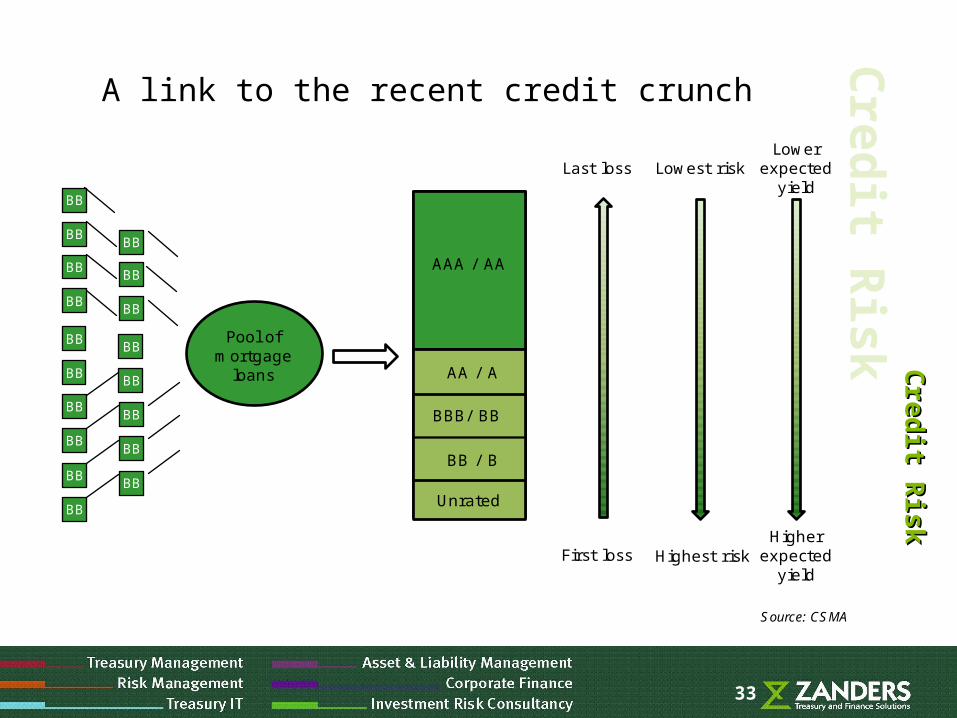

A link to the recent credit crunchC

red

it Ris

kC

red

it Ris

kC

red

it Ris

k

BB

Pool of mortgage

loans

AAA / AA

AA / A

BBB/ BB

BB / B

Unrated

Last loss Lowest riskLower

expected yield

First loss Highest riskHigher

expected yield

BB

BB

BB

BB

BB

BB

BB

BB

BB

BB

BB

BB

BB

BB

BB

BB

BB

Source: CSMA

34 34

A link to the recent credit crunch

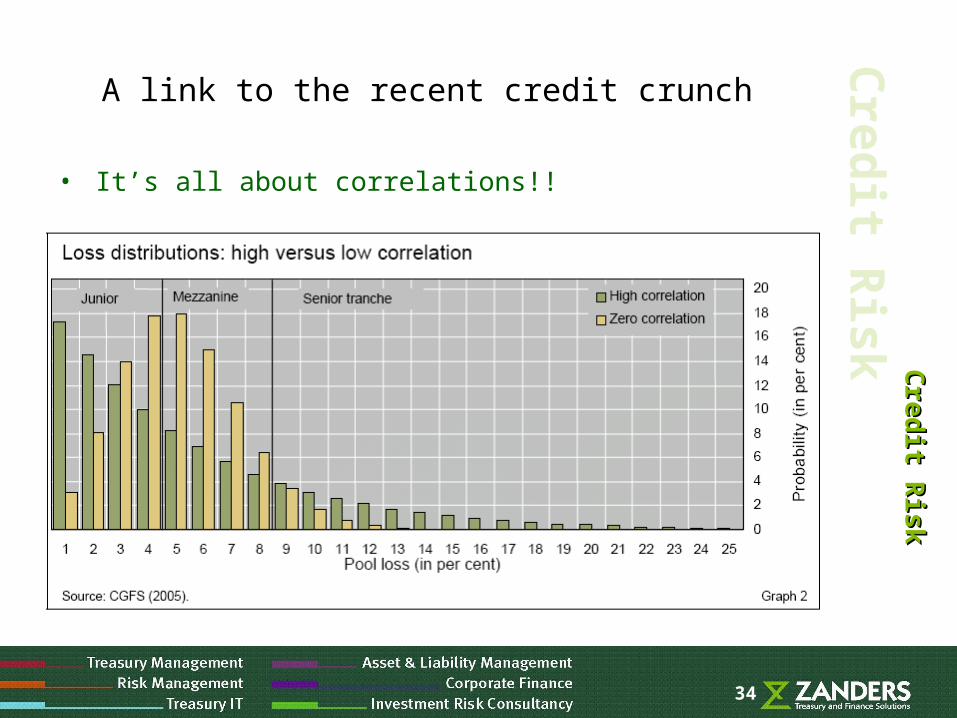

• It’s all about correlations!!

I

Cre

dit R

isk

Cre

dit R

isk

Cre

dit R

isk

35

- 0.250

0.000

0.250

0.500

0.750

1.000

1.250

1.500

Jan-0

4

Jul-0

4

Jan-0

5

Jul-0

5

Jan-0

6

Jul-0

6

Jan-0

7

Jul-0

7

Jan-0

8

sprAAA sprAA sprA sprBBB

35

A link to the recent credit crunch

• Yield spreads (Jan ‘04 – Jan ‘08):

Cre

dit R

isk

Cre

dit R

isk

Cre

dit R

isk

Madrid bombings

Credit crunch

36 36

A link to the recent credit crunch

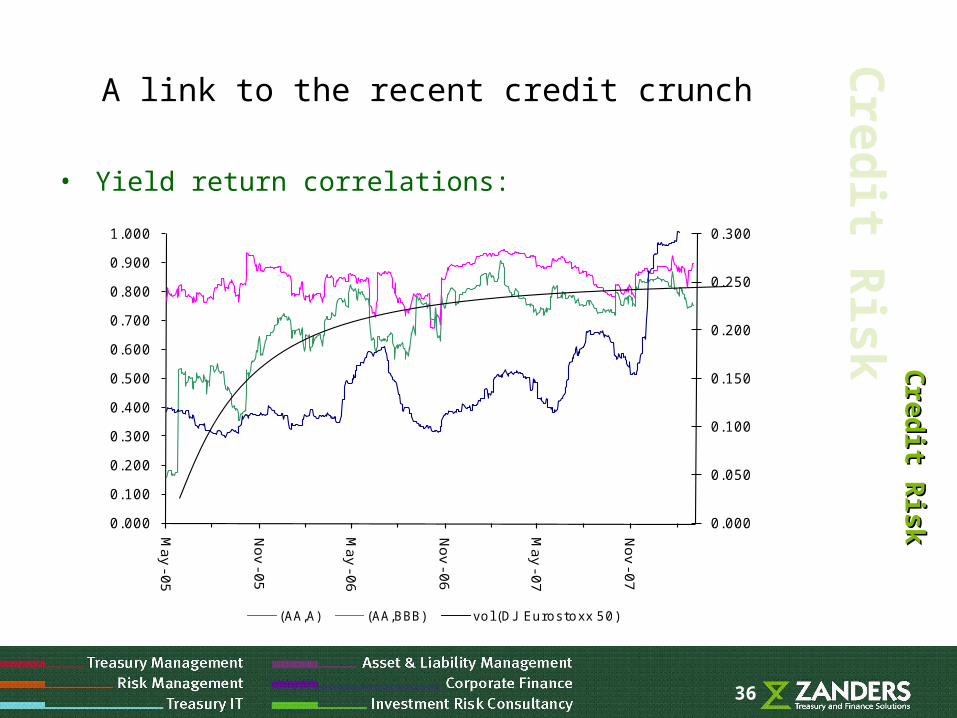

• Yield return correlations:

Cre

dit R

isk

Cre

dit R

isk

Cre

dit R

isk0.000

0.050

0.100

0.150

0.200

0.250

0.300

0.000

0.100

0.200

0.300

0.400

0.500

0.600

0.700

0.800

0.900

1.000

May

-05

Nov

-05

May

-06

Nov

-06

May

-07

Nov

-07

(AA,A) (AA,BBB) vol (DJ Eurostoxx 50)

37 37

A link to the recent credit crunch

• What happened?– US economy tightened and housing prices declined

– Correlation between high rating yield returns and the market volatility is always close to one ~ AAA/AA can serve as a proxy for the riskiness of the market.

– Correlation between high rated (= market) and lower rated was low but started to increase.

– Correlation between individual loans must then also increase.

– Credit risk in pool based on assumed low correlations ~ credit risk is underestimated!

Cre

dit R

isk

Cre

dit R

isk

Cre

dit R

isk

38 38

A link to the recent credit crunch

• Could the recent credit crunch have been prevented with adequate credit risk management?

• Lessons learned:– Don’t trust on historical correlations only– Use dynamic / stress correlations

Cre

dit R

isk

Cre

dit R

isk

Cre

dit R

isk