the history of captive insurance taxation · ─ accounting consulting ... – agreed upon...

TRANSCRIPT

Captive Academy of the 14th Annual Executive Educational Conference

THE HISTORY OF CAPTIVE INSURANCE TAXATION

Presented by:

Dan Kusaila, Tax Partner, Saslow Lufkin & Buggy, LLP

September 16, 2013

Captive Academy of the 14th Annual Executive Educational Conference

Agenda

─ Role of Accounting Firm

─ Types of Taxes

─ The importance of Qualifying as Insurance for Tax

─ History of the war with the IRS

─ What constitutes insurance for tax

─ Ways to achieve risk distribution

─ 831(b) Captives

2

Captive Academy of the 14th Annual Executive Educational Conference

Role of Accounting Firm

3

Captive Academy of the 14th Annual Executive Educational Conference

Role of Accounting Firm

─ Auditing

─ Accounting Consulting

─ Tax Compliance

─ Tax Consulting

4

Captive Academy of the 14th Annual Executive Educational Conference

Role of Accounting Firm (Cont’d)

Auditing

─ Annual Compliance with Audited Financial Statements • Due June 30th of each year

─ Non-Qualified Opinion desired • Qualified= not necessarily bad, but not clean

Loan Backs

No actuary report

Taxes

• Disclaimer= can not give an opinion

─ Assist with Footnote Disclosure

5

Captive Academy of the 14th Annual Executive Educational Conference

Auditing- Process

─ Planning

• Review for risk areas

─ Test of Controls

• Walk through

• Claims testing

• Expense testing

─ Year end field work

• Testing and sample of transactions

─ Financial Statement preparation

─ Captive manager/client review

─ Issue

6

Role of Accounting Firm (Cont’d)

Captive Academy of the 14th Annual Executive Educational Conference

Auditing- Process (Cont’d)

─ Financial Statement preparation

─ Captive manager/client review

─ Rep Letter- Issue

Role of Accounting Firm (Cont’d)

7

Captive Academy of the 14th Annual Executive Educational Conference

Auditing, Other Functions

– Assistance with Feasibility Studies

– Assistance Structuring Captive Arrangements

– Technical Accounting Assistance

– Agreed Upon Procedures

• Internal Control Testing

• Ensure internal policies and procedures are being followed

• Review of bookkeeping

8

Role of Accounting Firm (Cont’d)

Captive Academy of the 14th Annual Executive Educational Conference

Tax

– Tax compliance

• Tax return preparation

– Tax Accrual Assistance for Audited Financial Statements

– Assistance structuring captive companies and transactions

– Tax Consulting

– Private Letter Rulings

– Tax Opinions

Often act as Client’s tax department

Role of Accounting Firm (Cont’d)

9

Captive Academy of the 14th Annual Executive Educational Conference

Types of Taxes

─ Federal Income Taxes

─ Federal Excise Taxes

─ State Premium Taxes

─ Self-Procurement Taxes

─ State Income Taxes

10

Captive Academy of the 14th Annual Executive Educational Conference

Types of Taxes (Cont’d)

Federal Income Taxes

─ Non-Insurance Company • Form 1120 • Form 1065 • Form 990 • Others

─ Insurance Company- Form 1120-PC

11

Captive Academy of the 14th Annual Executive Educational Conference

Tax Reporting Requirements

– Consolidated Returns

• Parent and subs (including captive) file consolidated

• Tax year can follow parent’s tax year

• 1120PC form will be prepared until taxable income; included by “stacking”

• Estimated tax payments done at corporate level

• Captive will still need separate tax ID (EIN)

Types of Taxes (Cont’d)

12

Captive Academy of the 14th Annual Executive Educational Conference

Tax Reporting Requirements (Cont’d)

– Stand Alone Returns

• Parent and subs all file separately

• Tax year must follow calendar year pursuant to section 843 of Code

• 1120PC form will be filed stand alone

• As part of “controlled group” rules only 1 entity in group receives graduated rates

• Estimated tax payments done at captive level

– Same reporting rules apply to non-insurance captives (“regular” 1120 corporate return)

13

Types of Taxes (Cont’d)

Captive Academy of the 14th Annual Executive Educational Conference

Federal Income Taxes

─ Captive subject to tax on worldwide income

─ Special treatment:

• Loss reserves (discounting)

• Unearned premiums

Advanced Premium

• Deferred acquisition costs

• Capital losses

• Proration

─ Consolidated tax returns

Types of Taxes (Cont’d)

14

Captive Academy of the 14th Annual Executive Educational Conference

Federal Excise Tax - Basics Federal excise tax (“FET”) applies to premiums paid to foreign

insurer/reinsurer covering U.S. risks

4% FET on direct property and casualty policies

1% FET on reinsurance of U.S. risks

Withheld and remitted quarterly by U.S. premium payer

Not applicable if captive makes an IRC § 953(d) onshore tax election

IRS “cascading” theory for applying FET

15

Captive Academy of the 14th Annual Executive Educational Conference

Rev. Rul. 2008-15 – Federal Excise Tax

Excise tax under § 4371 has a “cascading” effect

─ Tax applies to premiums paid to cover U.S. risks regardless of the nationality of the insuring and/or reinsuring entities

• Applies to payments from one foreign insurance company to another foreign insurance company if the underlying risks are U.S. situs risks

• Ann. 2008-18 sets out a voluntary compliance initiative for foreign insurers and reinsurers that owe FET on foreign-to-foreign reinsurance transactions

Applies to FET on premiums received on or after October 1, 2008

IRS will not examine cascading tax liabilities from prior periods

16

Captive Academy of the 14th Annual Executive Educational Conference

─FET applies to both transactions ─US Insured and Foreign Insurer are both liable for tax on first

transaction ─US Insured NOT liable for tax on second transaction per Treas. Reg. §46.4374-1(a)

US Insured with US risk

Foreign Insurer Foreign Reinsurer

Rev. Rul. 2008-15: Scenario 1

17

Captive Academy of the 14th Annual Executive Educational Conference

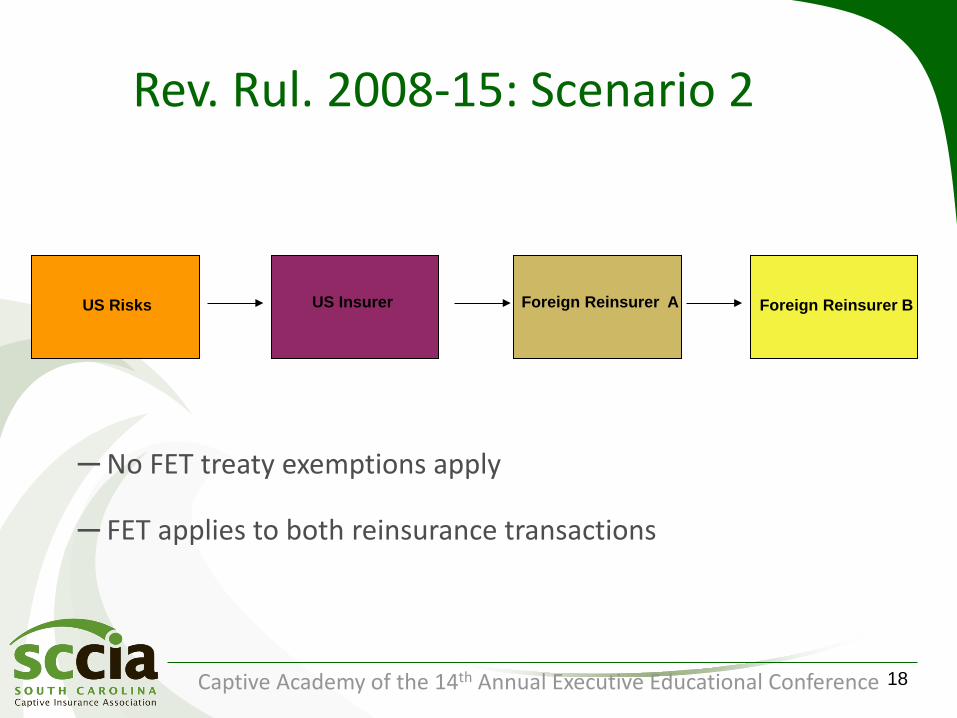

─ No FET treaty exemptions apply ─ FET applies to both reinsurance transactions

US Risks US Insurer Foreign Reinsurer A Foreign Reinsurer B

Rev. Rul. 2008-15: Scenario 2

18

Captive Academy of the 14th Annual Executive Educational Conference

─Foreign Insurer is eligible for FET treaty exemption but Foreign Reinsurer is not

─FET applies to both transactions ─The reinsurance transaction with the ineligible Foreign Reinsurer

nullified the treaty exemption with respect to the first transaction

US Insured with US risk Foreign Insurer Foreign Reinsurer

Rev. Rul. 2008-15: Scenario 3

19

Captive Academy of the 14th Annual Executive Educational Conference

─Foreign Insurer is eligible for FET treaty exemption but only if the insurance transaction is not part of a “conduit arrangement”

─Direct insurance transaction is assumed to not be a conduit arrangement

─No FET applies to the direct insurance transaction ─FET applies to the reinsurance transaction

US Insured with US risk Foreign Insurer Foreign Reinsurer

Rev. Rul. 2008-15: Scenario 4

20

Captive Academy of the 14th Annual Executive Educational Conference

Interim Guidance Memo SBSE-04-0909-045 (Excise Taxes)

─Procedures for excise tax examiners ─ IRS indicated it will be auditing foreign captive subsidiaries ─Forward all information to International excise tax group

• Name and employer identification number (EIN) of the parent company;

• Full name and EIN of the captive subsidiary;

• Location or country of the captive subsidiary;

• Amount of premiums insured with the captive subsidiary; and

• Amount of premiums reinsured by the captive subsidiary to reinsurance companies (if known).

─Looking to enforce “cascading theory” under Rev. Rul. 2008-15

21

Captive Academy of the 14th Annual Executive Educational Conference

Types of Taxes Excise Taxes

─ Premium = The agreed upon price or consideration for assuming or carrying the risk. It includes any additional charge or assessment payable under the agreement

─ The liability attaches when the premium is transferred to the foreign insurer or foreign reinsurer

─ Paid Quarterly ─ Insurance vs. Non-Insurance

22

Captive Academy of the 14th Annual Executive Educational Conference

Types of Taxes (Cont’d)

─ Self Procurement Taxes: • Also called:

Direct Placement taxes. Direct Procurement Taxes. Taxes on independently procured insurance.

─ Statutes preserve right of insureds to place insurance

outside state.

─ Tax imposed on transaction where in-state customer deals directly with non-admitted insurance company; no regulation.

23

Captive Academy of the 14th Annual Executive Educational Conference

─Florida

─Illinois

─Indiana

─Louisiana

─Michigan

─Mississippi

─Nebraska

─New Hampshire

─Oregon

─Wisconsin

State Income Taxes

24

Captive Academy of the 14th Annual Executive Educational Conference

State Income Taxes (Cont’d)

25

Captive Academy of the 14th Annual Executive Educational Conference

The Risk of Not Qualifying

26

Captive Academy of the 14th Annual Executive Educational Conference

Insurance vs. Non-Insurance

─ More beneficial to be treated as insurance:

• Accelerated tax deductions (i.e. loss reserves).

• State tax benefits – Depends on each state’s definition.

─ Single Parent Captives most significant:

• Taxes are significant reasons the captive was formed.

• Insurance expense deduction would be denied at parent level.

• State income tax savings.

27

Captive Academy of the 14th Annual Executive Educational Conference

Premium Considerations

─ If captive qualifies for tax position, premiums will be deductible from any brother-sister entities

─ Recommend arm’s length treatment

• Keep premium in captive until such time it’s prudent to dividend back

• Settle the premium with cash at front end of policy

─ Deductibility of premium is a wash between parent and captive at consolidation

28

Captive Academy of the 14th Annual Executive Educational Conference

Premium Deductibility

“Brother-Sister” Insurance

Insurance

Parent

Oper. Sub

Oper. Sub

Oper. Sub

100%

Oper. Sub

Oper. Sub

Insurance Subsidiary

100% 100% 100% 100% 100%

29

Captive Academy of the 14th Annual Executive Educational Conference

Insurance vs. Non-Insurance ─ 831(b):

• Small Company Election to be taxed on investment income only.

• Greater of direct written premium or net written premium cannot exceed $1.2 million.

─ 501(c)(15): • Extremely small insurance companies can apply to

be taxed exempt. • Gross receipts cannot exceed $600,000 (aggregated

for entire controlled group). • Greater than 50% of gross receipts must be from

premium.

30

Captive Academy of the 14th Annual Executive Educational Conference

Tax Treatment of Captives

* Self-Insurance Vehicle (IRS)

31

Captive Academy of the 14th Annual Executive Educational Conference

Ins. Vs. Non

32

FACTS -

• Premiums 1,000,000

• Unearned Premiums ( 200,000)

• Total Earned Premium 800,000

• Change in unpaid Loss Reserves (400,000)

GAA Expenses (200,000)

Net Income 200,000

***FIRST YEAR OF OPERATIONS

Captive Academy of the 14th Annual Executive Educational Conference

Insurance Company

Book Income 200,000

Adjustments:

Loss Res. Disc 40,000

UPR 40,000

Taxable Income 280,000

Ins. Vs. Non (Cont’d)

33

Non-Insurance Company

Book Income 200,000

Adjustments:

Premium (800,000)

Loss incurred 400,000

Taxable Income (200,000)

Captive Academy of the 14th Annual Executive Educational Conference

Tax Treatment of Captives 831(b) election No election

Affiliate Captive Affiliate Captive

Premium (1,200,000) 1,200,000 (1,200,000) 1,200,000

Book/Tax Adj

(1,200,000)

1,200,000

(1,200,000)

Taxable Income

1,200,000 0

0 0

Tax Rate 0.34 0.34 0.34 0.34

Total Benefit 408,000

0

0

0

34

Captive Academy of the 14th Annual Executive Educational Conference

The History of the War with the IRS

Common Law - ─ Helvering v. LeGierse– 1941 Supreme Court estate tax

case which established ground works to what defines insurance. • Insurable risk • Risk shifted to insurer • Pooled

35

Captive Academy of the 14th Annual Executive Educational Conference

The History of the War with the IRS (Cont’d) IRS Strikes - The Economic Family Theory: ─ Revenue Ruling 77-316 – An insurance arrangement

between related corporations should be re-characterized as a “self-insurance” reserve within an “economic family”.

36

Captive Academy of the 14th Annual Executive Educational Conference

Industry Fights Back - The Courts rule favorably: ─ Humana Inc. v. Commissioner ─ Gulf Oil Corp. v. Commissioner ─ AMERICO, Inc. v. Commissioner ─ The Harper Group v. Commissioner ─ Sears, Roebuck & Co. v. Commissioner ─ Hospital Corp. of America v. Commissioner

37

The History of the War with the IRS (Cont’d)

Captive Academy of the 14th Annual Executive Educational Conference

The Courts Rule - Brother-Sister Insureds: ─ Humana Inc. v. Commissioner ─ Hospital Corp. of America v. Commissioner

38

The History of the War with the IRS (Cont’d)

Captive Academy of the 14th Annual Executive Educational Conference

Brother-Sister Approach

Not Tax-Deductible Tax-Deductible (Note: Subsidiaries must be legal C corporations or other qualifying “associations” but NOT disregarded entities for tax purposes)

Parent

Captive

Sub Sub Sub Sub Sub Sub Sub Sub Sub Sub Sub Sub Sub Sub 12 Subsidiaries inferred from Revenue Ruling 2002-90

Premium Payments

39

The History of the War with the IRS (Cont’d)

Captive Academy of the 14th Annual Executive Educational Conference

The Courts Rule - Unrelated Third Party Risk: ─ Gulf Oil Corp. v. Commissioner ─ AMERICO, Inc. v. Commissioner ─ The Harper Group v. Commissioner ─ Sears, Roebuck & Co. v. Commissioner

40

The History of the War with the IRS (Cont’d)

Captive Academy of the 14th Annual Executive Educational Conference

Common Mid Size Company Example Brother-sister and third-party risk

Parent

Captive

Sub Sub Sub Sub Sub Sub Sub Sub Third Party/ Pool Risk

50% unrelated risk stated as a safe harbor from Revenue Ruling 2002-89

Tax-Deductible

Premium Payments

LLC

Ceded Premium

41

Third Party Risk

The History of the War with the IRS (Cont’d)

Captive Academy of the 14th Annual Executive Educational Conference

IRS Concedes – ─ Revenue Ruling 2001-31 – The IRS will no longer invoke the

economic family theory. • However, they will continue to challenge certain captive

insurance transactions based on facts and circumstances.

42

The History of the War with the IRS (Cont’d)

Captive Academy of the 14th Annual Executive Educational Conference

IRS Provides Guidance - ─ IRS & Treasury attempts at defining insurance: Rev. Rul. 2002-89 Rev. Rul. 2002-90 Rev. Rul. 2002-91 Rev. Rul. 2005-40 Rev. Rul. 2009-26

43

The History of the War with the IRS (Cont’d)

Captive Academy of the 14th Annual Executive Educational Conference

─ Revenue Ruling 2002-89

• No insurance when 90% of the captive’s premium comes

from the parent. • Insurance - 50% of the captive’s premium are from the

parent, while the remaining 50% is from un-related business.

44

The History of the War with the IRS (Cont’d)

Captive Academy of the 14th Annual Executive Educational Conference

─ Revenue Ruling 2002-90

• Captive with 12 brother-sister entities. • No related entity accounted for less than 5% and more

than 15% of the total risk.

45

The History of the War with the IRS (Cont’d)

Captive Academy of the 14th Annual Executive Educational Conference

─ Revenue Ruling 2002-91

• Group captive involving a small group of unrelated

businesses. • No member owned more than 15% of the captive and

no member’s individual risk exceeded 15% of the total risk insured.

46

The History of the War with the IRS (Cont’d)

Captive Academy of the 14th Annual Executive Educational Conference

─ Revenue Ruling 2005-40

• Risk Distribution (4 scenarios) No insurance- 1 unrelated insured No insurance- 2 insureds whereby one insured makes

up 90% of the premium No insurance- 12 brother/sister entities in which they

are disregarded entities for tax purposes Insurance- 12 SMLLC’s in which they all elect

to be taxed as a corporation

47

The History of the War with the IRS (Cont’d)

Captive Academy of the 14th Annual Executive Educational Conference

Rev. Rul. 2009-26: Scenario 1

─ Assumptions: • Z is adequately capitalized

• Z operates at arms length with Y

• Z operates in accordance with state law

─ Ruling: Z is an insurance company because it has risk distribution as if it had insured 10,000 policyholders directly

10,000 Policyholders Commercial

multiline 10 states

Reinsurer

Z

Insurance Company

Y

90% premiums

90% risks

48

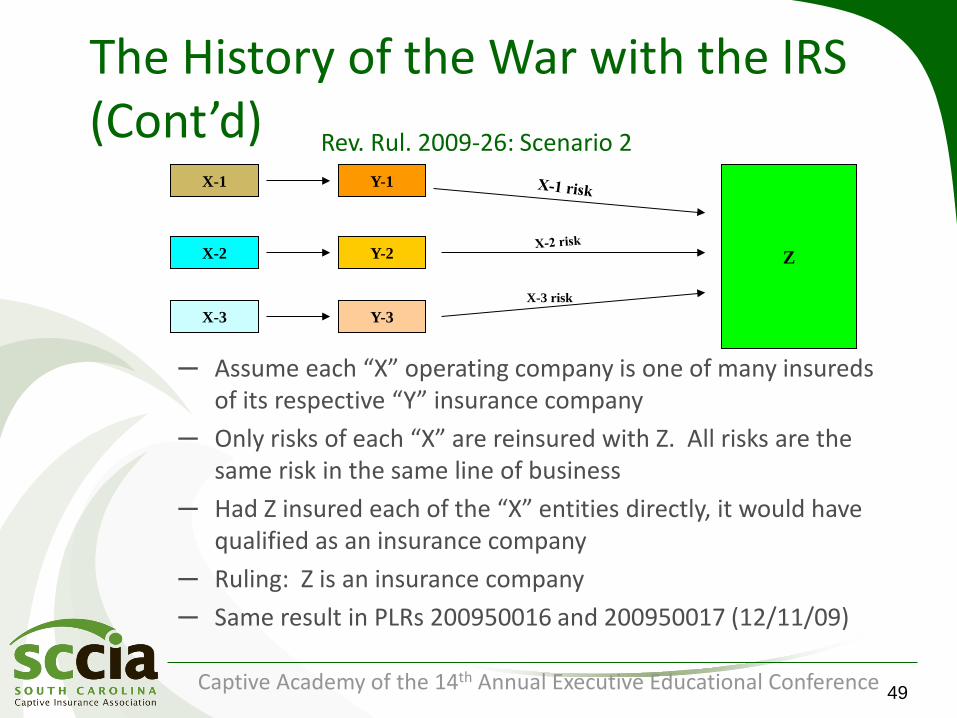

The History of the War with the IRS (Cont’d)

Captive Academy of the 14th Annual Executive Educational Conference

─ Assume each “X” operating company is one of many insureds of its respective “Y” insurance company

─ Only risks of each “X” are reinsured with Z. All risks are the same risk in the same line of business

─ Had Z insured each of the “X” entities directly, it would have qualified as an insurance company

─ Ruling: Z is an insurance company

─ Same result in PLRs 200950016 and 200950017 (12/11/09)

Z

X-3 risk

X-1

X-2

X-3

Y-1

Y-2

Y-3

49

Rev. Rul. 2009-26: Scenario 2

The History of the War with the IRS (Cont’d)

Captive Academy of the 14th Annual Executive Educational Conference

What Constitutes Insurance for Tax purposes

50

Captive Academy of the 14th Annual Executive Educational Conference

What Constitutes Insurance?

─ The IRS definition of an insurance company: • For purposes of the preceding sentence, the term

"insurance company" means any company more than half of the business of which during the taxable year is the issuing of insurance or annuity contracts or the reinsuring of risks underwritten by insurance companies.

─ The IRS does not define insurance contract! Therefore we

must look to the courts: • Insurance contract must have: Risk Shifting. Risk Distribution.

51

Captive Academy of the 14th Annual Executive Educational Conference

Risk Shifting

─ In Helvering v. LeGierse, the Supreme Court said that for a transaction to be considered insurance, it must transfer the risk of loss from one party to another, among other points. That is Risk Shifting.

─ How risk shifting is defined by law, courts, and the IRS is the subject of much time and money. Captives have been at the center of this issue.

─ Have you shifted the risk? How much is needed to qualify (5, 10, 50 percent)? What about reinsurance? Who owns the captive?

─ Rev. Ruling 2002-89 states that 50% of unrelated business will

suffice for Risk Shifting.

─ Rev. Ruling 2002-90 states 12 subs whereby no one sub makes up more than 15% of the premium or less than 5% of the premium will qualify.

52

Captive Academy of the 14th Annual Executive Educational Conference

Risk Distribution

─ Rev. Rul. 2002-90 indicates 12 insureds are enough. ─ Rev Rul. 2005-40 was issued as guidance for Risk Distribution:

1 insured is not enough.

─ Risk Distribution= Law of Large numbers: No 1 insured will pay for their own losses. 2 insureds may be enough (My personal interpretation). 90% of premium from one insured is not enough. SMLLC’s are parent risk.

─ FSA 200202002 states 1 insured which makes up between 86% to 88% of the premium is not enough risk distribution.

─ Homogeneous.

53

Captive Academy of the 14th Annual Executive Educational Conference

50% or More

─ If at least 50% of your business is issuing insurance contracts you will qualify for insurance company status.

• Investment income cannot outweigh underwriting income:

Watch for SMLLC’s owned by the captive.

─ If circumstances are right, an argument can be made that investment income which outweighs underwriting income can qualify as insurance.

54

Captive Academy of the 14th Annual Executive Educational Conference

Other Considerations

─ Capitalization

─ Business Purpose

─ Indemnifications & Guarantees

─ Commonly Accepted as Insurance

55

Captive Academy of the 14th Annual Executive Educational Conference

What Constitutes Insurance?

─ If you have risk shifting & risk distribution you should have an insurance contract for IRS purposes.

─ If at least 50% of your business is issuing insurance contracts you will qualify for insurance company status.

56

Captive Academy of the 14th Annual Executive Educational Conference

Not Qualifying?

─ Reasons for not wanting to be taxed as an insurance company:

• Tax Exempt Members

• REIT members

• Short tail property (not a big deal)

• Fully Reinsured

57

Captive Academy of the 14th Annual Executive Educational Conference

Ways to Achieve Risk Distribution

58

Captive Academy of the 14th Annual Executive Educational Conference

Ways to Achieve Risk Distribution

─ Brother-Sister organizational structure

─ Third Party

• Customer Risk

• Pooling Arrangements

• Employee Benefits

59

Captive Academy of the 14th Annual Executive Educational Conference

RED INSURANCE LTD.

$49X of risk from Red Co.

YELLOW INSURANCE LTD.

$42.5X of risk from Yellow Co.

BLUE INSURANCE LTD.

$30X of risk from Blue Co.

RED INSURANCE LTD.

49% of pooled risk

YELLOW INSURANCE LTD.

42.5% of pooled risk

RED INSURANCE LTD.

30% of pooled risk

Pooling

$49x Red Co Risk $42.5x Yellow Co.

Risk $30x Blue Co. Risk

Pooling of Risks

60

Captive Academy of the 14th Annual Executive Educational Conference

Pooling of Risks Chief Counsel Advice 200844011

─ Members cede into the pool and reinsure the pool • Provided for the conduct of pool business

• Pool spread risk of loss among members

─ Found the pool to be an insurance company for tax purposes • The Pool operates separately from each member

• Members of the Pool exercised mutual control over the operations and management of the Pool through Participants’ committee

• Various committees oversaw pool operations No single pool member could prevent the pool from acting on its determinations

• Maintained separate account books Reinsurance premium was actuarially determined

─ Excise taxes were found to be applicable

61

Captive Academy of the 14th Annual Executive Educational Conference

Pooling of Risks Private Letter Ruling 200907006 ─ A foreign company providing business insurance coverage

and participating in a reinsurance pool will be treated as an insurance company for tax purposes

─ IRS concluded – provided the company is adequately capitalized, the arrangement between the company and its insureds constitutes insurance • Company is in the business of issuing insurance and reinsurance

contracts.

Open Question

Does the Risk have to be homogeneous?

62

Captive Academy of the 14th Annual Executive Educational Conference

Pooling of Risks Risk Mixers

PLR 201030014 (7/30/10) – Risk Mixers

─ Involved a sole proprietor that insured with a captive owned by a trust for the proprietor and his spouse

─ The captive reinsured its risks with a Pooling Company (risk mixer entity) which pooled numerous risks and reinsured a proportionate part of several pools (a pool for each coverage)

─ No captive in the pool insured more than 15% of the pool’s total risks

─ Same result in PLR 200907006 (2/13/09)

63

Captive Academy of the 14th Annual Executive Educational Conference

Employee Benefits

─ Revenue Ruling 80-95 (Excise Taxes)

─ Facts: • An employee benefits contract with a domestic corporation.

• A foreign insurer covers the domestic corporation’s contract for all payments in exchange for an annual payment.

─ Outcome: • Employee benefits contracts act like 3rd party contracts and are

considered insurance for tax purposes.

64

Captive Academy of the 14th Annual Executive Educational Conference

Questions

Captive Academy of the 14th Annual Executive Educational Conference

831(b) Captives

66

Captive Academy of the 14th Annual Executive Educational Conference

831(b) Captives

67

Captive Academy of the 14th Annual Executive Educational Conference

Alternative Tax for Small Insurance Companies

Small Corporations can “elect” to be taxed on their taxable investment income.

Must meet the tax qualifications to be taxed as an insurance company in order to make the election.

68

Captive Academy of the 14th Annual Executive Educational Conference

Alternative Tax for Small Insurance Companies (Cont’d)

What is Small?

Section 831(b)(2)(A)(i) states that the net written premiums (or, if greater, direct written premiums) for the taxable year do not exceed $1,200,000

Company must elect and can only be revoked by the Commissioner or if the Company fails to meet the criteria

69

Captive Academy of the 14th Annual Executive Educational Conference

– Net written premiums and direct written premiums are not defined by the Internal Revenue Code or regulations. However, the IRS Manual has determined that the IRS will look to the NAIC definition of these terms.

• Direct written premiums = all premiums arising from policies

issued by the company as the primary insurance carrier, adjusted for any return or additional premiums arising from endorsements, audits, and retrospective rating plans.

• Net written premiums = the sum of direct written premiums plus assumed reinsurance premiums, less ceded reinsurance premiums.

70

Alternative Tax for Small Insurance Companies (Cont’d)

Captive Academy of the 14th Annual Executive Educational Conference

─ Investment expenses also can include general expenses properly allocable to investment activities.

─ Section 1.822-8(c)(2) (ii) defines “general expenses” to mean “any expense paid or incurred for the benefit of more than one department of the company rather than for the benefit of a particular department thereof.”

• Auditing Expenses

• Management Fees

• Tax Fees

• Etc.

─ See Letter Ruling 9609003

71

Alternative Tax for Small Insurance Companies (Cont’d)

Captive Academy of the 14th Annual Executive Educational Conference

─ Controlled Group:

─ If there is more than 1 insurance company that is part of a consolidated return or member of a controlled group, the premiums of all insurance companies must be aggregated in order to determine if the $1.2 million threshold has been exceeded.

See Section 831(b)(2)(B)

72

Alternative Tax for Small Insurance Companies (Cont’d)

Captive Academy of the 14th Annual Executive Educational Conference

─ Net Operating Losses:

─ Can not be carried to or from a year in which the company is taxed under Section 831(b)

─ Can not be carried to any taxable year if, between the taxable year from which such loss is being carried and such taxable year, there is an intervening taxable year for which the insurance company was not subject to the tax imposed by subsection (a)

73

Alternative Tax for Small Insurance Companies (Cont’d)

Captive Academy of the 14th Annual Executive Educational Conference

Frequently asked Questions:

─ One the election is made, can I decide not to make the election due to losses?

─ Can you flip/flop between 831(b) years and traditional years?

─ Are the 831(b) captives more vulnerable to IRS scrutiny?

─ Will congress increase the premium threshold anytime soon?

Alternative Tax for Small Insurance Companies (Cont’d)

74