the global spa economy - global wellness … global spa economy the global spa summit gratefully...

TRANSCRIPT

May 2008

THE GLOBAL SPA ECONOMY

2007

May 2008

THE GLOBAL SPA ECONOMY

2007

The Global Spa Summit gratefully acknowledges the support of our sponsors who

made the research for the Global Spa Economy possible.

Raison d’Etre

THE GLOBAL SPA ECONOMY

2007

About Global Spa Summit

The Global Spa Summit is an international organization that brings together leaders and

visionaries to positively impact and shape the future of the global spa and wellness

industry. Founded in 2006, the organization hosts an annual Global Spa Summit where

top industry executives gather to exchange ideas and advance industry goals. For more

information on the Global Spa Summit, please visit: www.globalspasummit.org.

About SRI International

Founded in 1946 as Stanford Research Institute, SRI International is an independent, non-

profit organization that performs a broad spectrum of problem-solving consulting and

research and development services for business and government clients around the world.

More information on SRI is available at: www.sri.com.

Copyright

The Global Spa Economy 2007 report is the property of the Global Spa Summit LLC. None

of its content – in part or in whole – may be copied or reproduced without the express

written permission from the Global Spa Summit. Quotation of, citation from, and reference

to any of the data, findings, and research methodology from the report must be credited

to “Global Spa Summit, Global Spa Economy 2007, prepared by SRI International, May

2008.” To obtain permission for copying and reproduction, or to purchase a copy of the

report, please contact the Global Spa Summit by email: [email protected]

or through www.globalspasummit.org.

The Global Spa Economy 2007

Copyright Global Spa Summit 2008 SRI International

Table of Contents

EXECUTIVE SUMMARY ........................................................................................................ 1

I. OVERVIEW ..................................................................................................................... 4

II. ANALYTICAL FRAMEWORK .......................................................................................... 7

A. DEFINING THE SPA ECONOMY .......................................................................................................... 7

B. QUANTIFYING THE SIZE OF THE SPA ECONOMY ............................................................................. 13

III. THE 2007 SPA ECONOMY ........................................................................................... 14

A. CORE SPA INDUSTRIES ..................................................................................................................... 16

B. SPA-ENABLED INDUSTRIES ............................................................................................................... 35

C. ASSOCIATED SPA LIFESTYLE INDUSTRIES ........................................................................................... 38

D. ECONOMIC IMPACT OF THE SPA INDUSTRY..................................................................................... 40

IV. HOW TO USE THE FINDINGS TO MOVE THE SPA INDUSTRY FORWARD .................... 42

V. SPA ECONOMY RESEARCH AND ESTIMATION METHODOLOGY ............................... 45

A. DATA COLLECTION .......................................................................................................................... 45

B. ESTIMATION METHODOLOGIES ....................................................................................................... 47

VI. REFERENCES ................................................................................................................ 58

VII. ABOUT THE RESEARCH TEAM ..................................................................................... 62

The Global Spa Economy 2007 report was prepared by SRI International in agreement with the

Global Spa Summit. The study was led by Ophelia Yeung, Director of Economics Program, and

Katherine Johnston, Senior Economist, with contributions from: Nancy Chan, Economic and Technology

Policy Analyst; Li Gwatkin, Senior Consultant; Fergus Murphy, Senior Economist; and Jennifer Ozawa,

Senior Economist at SRI International; as well as over 50 spa industry executives around the world.

The Global Spa Economy 2007

Copyright Global Spa Summit 2008 1 SRI International

Executive Summary

The Global Spa Economy 2007 is a landmark first step in developing a framework to

quantify the global spa industry. The objectives of this study are:

To put forward a comprehensive framework to understand and quantify the scale

and impact of the global spa economy.

To develop high-level, global estimates that enable industry leaders, investors, and

policymakers to make informed business and policy decisions.

To stimulate dialogue among all industry stakeholders regarding the definition,

measurement, and positioning of the global spa industry going forward.

The study has taken a decidedly inclusive approach in defining the term “spa” by

considering its different interpretations by global businesses and consumers.

For the purpose of estimating the global spa economy, this study defines spas as

establishments that promote wellness through the provision of therapeutic and

other professional services aimed at renewing the body, mind, and spirit.

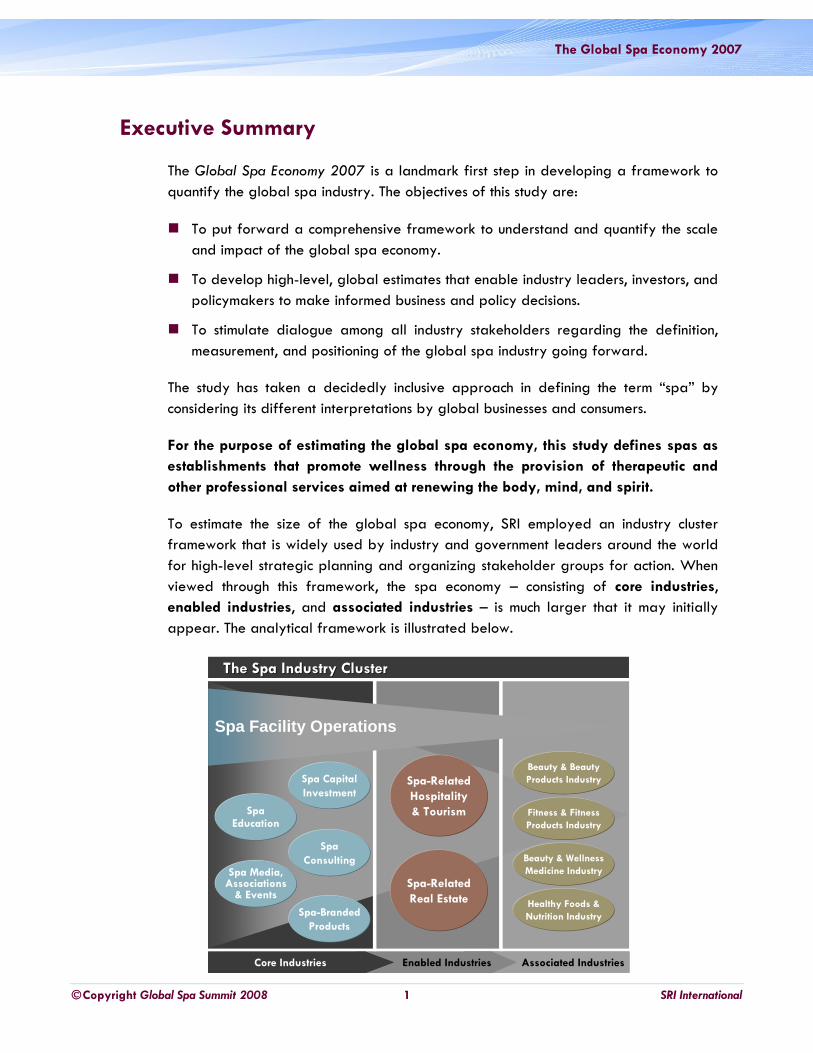

To estimate the size of the global spa economy, SRI employed an industry cluster

framework that is widely used by industry and government leaders around the world

for high-level strategic planning and organizing stakeholder groups for action. When

viewed through this framework, the spa economy – consisting of core industries,

enabled industries, and associated industries – is much larger that it may initially

appear. The analytical framework is illustrated below.

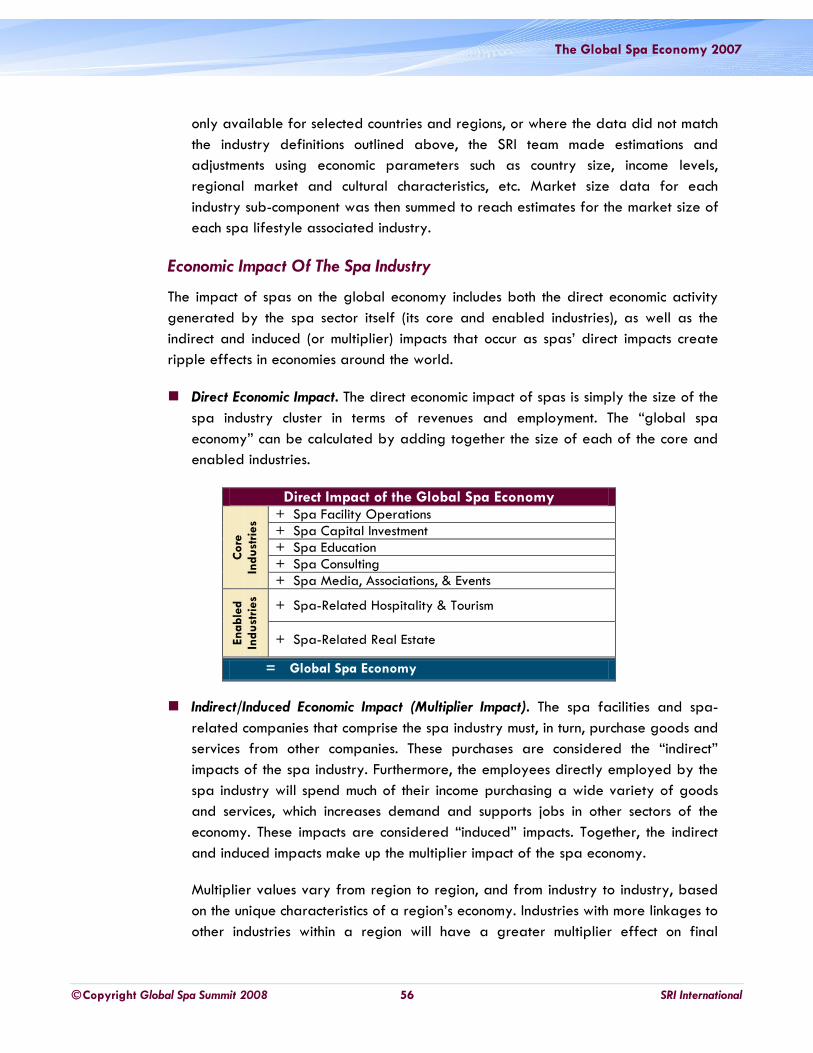

Spa-Related

Hospitality

& Tourism

Spa-Related

Real Estate

The Spa Industry ClusterThe Spa Industry Cluster

Spa Capital

Investment

Spa-Branded

Products

Spa

ConsultingSpa Media,

Associations& Events

SpaEducation

Beauty & Beauty

Products Industry

Fitness & Fitness

Products Industry

Beauty & Wellness

Medicine Industry

Healthy Foods &

Nutrition Industry

Spa Facility Operations

Associated IndustriesEnabled IndustriesCore Industries

Spa-Related

Hospitality

& Tourism

Spa-Related

Real Estate

The Spa Industry ClusterThe Spa Industry Cluster

Spa Capital

Investment

Spa-Branded

Products

Spa

ConsultingSpa Media,

Associations& Events

SpaEducation

Beauty & Beauty

Products Industry

Fitness & Fitness

Products Industry

Beauty & Wellness

Medicine Industry

Healthy Foods &

Nutrition Industry

Spa Facility Operations

Associated IndustriesEnabled IndustriesCore Industries Associated IndustriesAssociated IndustriesEnabled IndustriesEnabled IndustriesCore IndustriesCore Industries

The Global Spa Economy 2007

Copyright Global Spa Summit 2008 2 SRI International

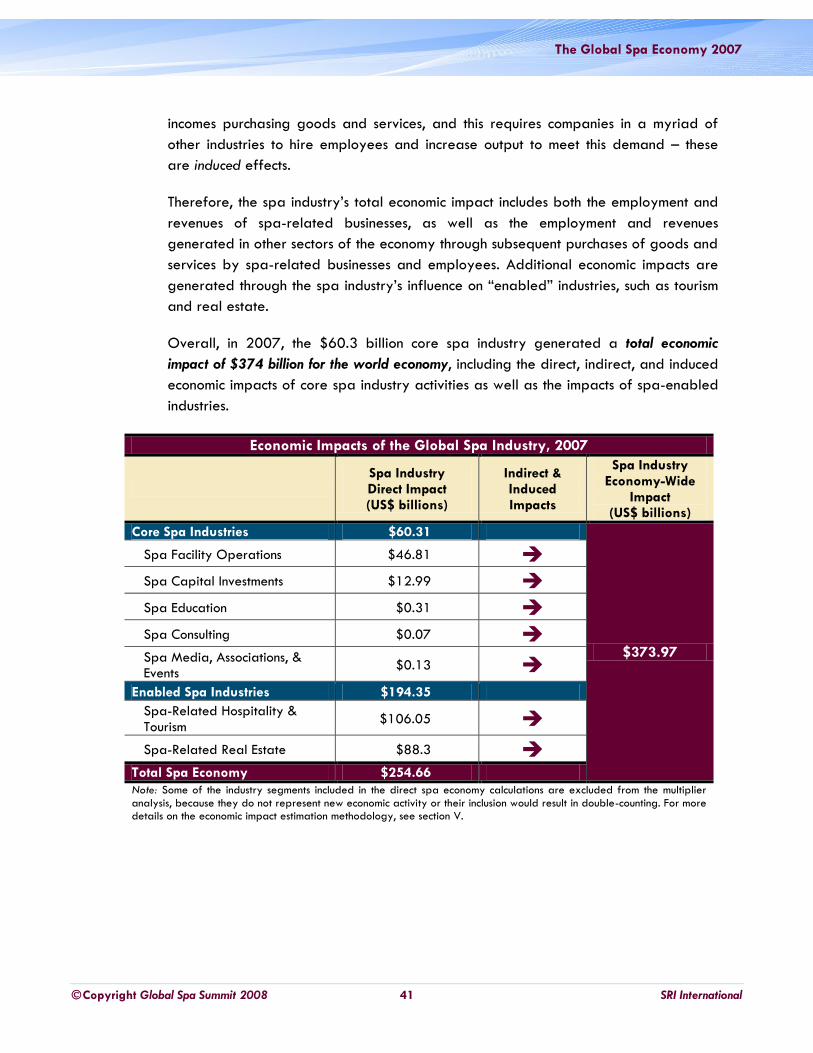

SRI estimates that the total size of the global spa economy in 2007 was $254.7

billion. This estimate includes $60.3 billion in core spa industries and an additional

$194.4 billion in spa-enabled industries, as shown in the table below.

Size of the Global Spa Industry, 2007 (US$ billions)

Core Spa Industries $60.31

Spa Facility Operations $46.81

Spa Capital Investments $12.99

Spa Education $0.31

Spa Consulting $0.07

Spa Media, Associations, & Events $0.13

Spa-Branded Products n.a.

Spa-Enabled Industries $194.35

Spa-Related Hospitality & Tourism $106.05

Spa-Related Real Estate $88.30

Total Spa Economy $254.66

Spa facility operations represent $46.8 billion in revenues, or 78% of the “core”

industry. The spa industry has been experiencing rapid growth in many regions around

the world, and this growth is reflected in a significant level of capital investment,

estimated at over $12.9 billion in 2007. The other “core” sectors – including

education; consulting; and media, associations, and events – are relatively small by

comparison, but still represent important pieces of the industry. Together, these sectors

earned an estimated $0.51 billion in revenues in 2007.

A significant amount of activities in the tourism and real estate sectors are influenced

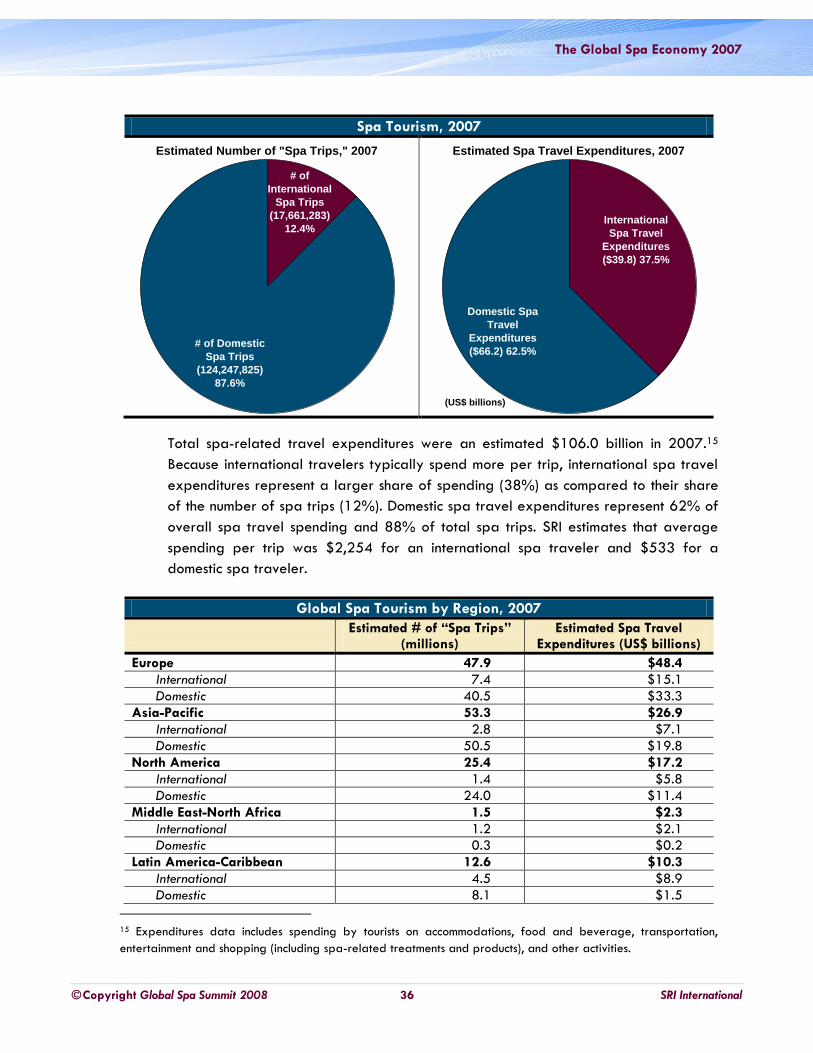

by the burgeoning spa, health, and wellness trend. SRI estimates that $106.0 billion in

global tourism and hospitality revenues were “enabled” by the spa industry in 2007.

Additionally, an estimated $88.3 billion in global real estate construction revenues

were “enabled” by the spa lifestyle concept in 2007.

The spa industry sits solidly within a broader set of lifestyle, health, and wellness-

driven industries. The four “spa lifestyle associated industries” – those industries

directly interconnected with the spa industry – represent a global market that

exceeded $1 trillion in 2007.

Global Spa Lifestyle Associated Industries, 2007

Global Market Size (US$ billions)

Beauty and beauty products industry $500.2

Fitness and fitness products industry $241.3

Beauty and wellness medicine industry $195.8

Healthy foods and nutrition industry $162.4

Total $1,099.7

The Global Spa Economy 2007

Copyright Global Spa Summit 2008 3 SRI International

The size of the spa economy and its economic impacts represent an important message

that should be communicated for purposes of:

Advocating to government leaders that the spa industry is an important and

strategic sector to be supported;

Joining industry stakeholders together to provide a stronger voice and more

collaborative action;

Reaching out to consumers by allowing for flexibility in the interpretation of “spa”

and inclusion of cultural and traditional contexts;

Informing investors of the opportunities that exist in the diverse and growing spa

industry; and

Attracting qualified professionals to the spa industry.

The SRI team has arrived at the estimates presented in this report based on a

combination of primary and secondary research and economic modeling techniques,

including: a global survey that collected approximately 1,000 responses; intensive

research and data collection from national, international, and industry sources; and

interviews with high level executives in the spa industry. Together, these lines of

research were used to craft a tailored economic estimation model that attempts to

quantify an industry where enormous information and data gaps exist. In essence, this

study provides a snapshot of the global spa economy in 2007 for 210 economies

around the world.

The Global Spa Economy 2007

Copyright Global Spa Summit 2008 4 SRI International

I. Overview

Why study the Global Spa Economy?

SRI International was commissioned by the Global Spa Summit to quantify the size of

the global spa economy. The objectives of this study are as follows:

To put forward a comprehensive framework to understand and quantify the scale

and impact of the global spa economy.

To develop high-level, worldwide estimates that enable industry leaders, company

executives, investors, and policymakers to make informed business and policy

decisions based on a comprehensive, global understanding of the spa industry.

To stimulate dialogue among all industry stakeholders regarding the definition,

measurement, and positioning of the global spa industry going forward.

Until now, no study has attempted to measure the size of the global spa industry, due

to a variety of factors, including: the diversity of the spa industry and markets across

countries and regions, the difficulty of defining a “spa,” the lack of country-level

information, and the difficulty of comparing data across countries. For the same

reasons, even attempts to count the number of spas or estimate the size of the spa

market at the country or regional level have been limited.

Few industries have organized at the global level to “measure themselves” and

present the worldwide economic impact of their industry. In fact, this study may be one

of the first attempts of its kind. In this regard, the global spa industry has a unique

opportunity to be a “pioneer” through this endeavor.

What this study is

This study is designed to be a landmark first step in developing a framework to

quantify the global spa industry and its related economy in 210 countries. The SRI

team has arrived at the estimates presented in this report based on a combination of

primary and secondary research and economic modeling techniques, including: a

global survey that collected approximately 1,000 responses; intensive research and

data collection from national, international, and industry sources; and interviews with

over 50 high-level executives in the spa industry. Together, these lines of research are

used to craft a tailored economic estimation model that attempts to quantify an

industry where enormous information and data gaps exist. In essence, this study

provides a snapshot of the global spa economy in 2007 for 210 countries, even given

the absence of data for 95% of these countries.

The Global Spa Economy 2007

Copyright Global Spa Summit 2008 5 SRI International

To conduct this study, SRI has employed an industry cluster framework that has been

widely used for more than 20 years by industry and government stakeholders around

the world. The cluster methodology is widely recognized as a useful tool for high-level

strategic planning, advocacy, and investment resource planning.

Such an approach allows industries to organize resources, structure their

collaboration, speak as one voice to policymakers and consumers, and conduct

advocacy and public relations efforts more effectively and efficiently.

What this study is not

This study is not structured as a global spa census; it does not attempt to count the

number of spas or add up their revenues across the globe. Such an approach would

be both time and cost prohibitive for any organization. In fact, the SRI team is

unaware of any industry that has conducted its own census at the global level –

precisely for this reason.

A number of high-quality national and regional spa industry studies have been

conducted by various consulting groups and associations. However, each study applies

different filters to quantify and “count” spas, and therefore such data is not

comparable across countries and regions. Furthermore, these studies have been

conducted for no more than 20 countries around the world, leaving a big gap in the

current state of knowledge regarding the global spa industry, particularly for fast

growing countries in Asia, Latin America, and the Middle East. To insist on a census

approach would thus be paralyzing and unproductive. This study is designed as an

important leap forward to provide a degree of quantification, inclusive of the 20 or

so countries where some spa industry data has been collected, as well as the 190

countries in which national-level spa industry data is nonexistent.

What we include as spas

An inherent goal of this study is to promote the value of flexibility in defining the term

“spa” and to understand its different interpretations by businesses and consumers

around the world. It is with this end in mind that we put forth the following criteria for

including spas in this study:

For the purpose of estimating the global spa economy, this study defines spas as

establishments that promote wellness through the provision of therapeutic and

other professional services aimed at renewing the body, mind, and spirit.

Most consumers and industry executives would agree that at its core – no matter its

size, form, or business model – a spa is an establishment that focuses on the promotion

The Global Spa Economy 2007

Copyright Global Spa Summit 2008 6 SRI International

of wellness. The concept of wellness, the healing traditions drawn upon, and the

therapeutic techniques applied differ dramatically from one country to the next.

Working within this framework, this study does not apply specific filters – such as

requiring therapeutic treatments to be water-based, or requiring an establishment to

be of a certain size or offer a certain combination of services – to define what is and

what is not part of the spa industry. A major value of this approach is that it allows

local, cultural, and historical wellness and healing contexts to be captured in

quantifying the size and impact of the spa economy.

Specifically, this study estimates the economic impact of establishments that consider

themselves as “spas” and market themselves as such – as well as establishments that

consumers would likely consider to be a “spa,” particularly in relation to unique

cultures and traditions – regardless of strict definitions used by the industry in other

contexts.

What this study tells us

When viewed through the industry cluster framework, the spa industry is much

larger than it may initially appear.

Given the spa industry‟s size, economic impact, and growth potential, there is a

colossal need for the industry and governments to collect and maintain

standardized information on the industry.

We believe that a more, rather than less, inclusive approach to defining “spa” best

captures the current and future potential of the industry as it is viewed by

consumers and entrepreneurs. This broader approach provides a useful umbrella

under which spas will have the flexibility to apply appropriate filters in order to

differentiate themselves for the purposes of marketing to particular consumer

niches.

The Global Spa Economy 2007

Copyright Global Spa Summit 2008 7 SRI International

II. Analytical Framework

Estimating the size of the global spa economy requires two parallel, but interrelated,

sets of inquiry, each presenting its own unique set of challenges:

1. How does one define a spa? What does the spa industry encompass?

2. How does one quantify the size of the spa industry and the economic activities

related to it?

The challenge of defining the spa industry itself compounds an already difficult task of

measuring the economic impact of an industry that is relatively young, and for which

existing data around the world is scarce. Nevertheless, the research team conducting

this study has been able to gather and produce data that results in a fair

approximation of the global spa industry‟s economic impact. Over time, the data and

estimation methods used for this study can be refined for greater accuracy.

A. Defining The Spa Economy

1. What Is A Spa?

If you ask ten consumers in ten countries – say, Germany, Italy, Russia, China, Japan,

Thailand, United States, Mexico, Morocco, and United Arab Emirates – what they

would consider to be a spa, you are likely to get ten different answers.

The inherent challenge of measuring the size and impact of the spa industry is the

difficulty of defining what constitutes a “spa.” This dilemma is not unique to the spa

industry.

In the tourism sector, for example, a very liberal and inclusive industry definition

would include not only spending by foreign visitors, but also all transportation,

retail, dining, recreation, and entertainment activities, whether these expenditures

are incurred by “real” tourists or by local residents. A more restrictive definition

might count only spending by foreign visitors or domestic residents taking a trip of

a certain distance or duration. Within the tourism community, there is no agreed

upon definition of what counts as a tourism “trip” for the purposes of measuring

tourism expenditures – does a trip have to exceed 50 miles or 60 kilometers away

from home to be counted, or does it have to involve an overnight stay? Tourism

statistics are produced by governments, nonprofits, international organizations,

and private research firms around the world, and each organization approaches

these definitional questions in a slightly different way.

The Global Spa Economy 2007

Copyright Global Spa Summit 2008 8 SRI International

Information technology is another industry that poses definitional challenges. For

some studies, the IT industry encompasses all activities that might be considered

“high-tech” – it might include computer equipment and peripherals, semiconductors,

electronics, computer programming and design, IT consulting, telecommunications

equipment and services, and much more. On the other hand, some studies may

exclude the manufacturing of “hardware” such as computers, electronics, and

telecommunications devices – as these activities are becoming increasingly

“commoditized” and “low-tech” – and instead focus only on the higher value-

added services side of IT (such as programming, design, consulting, etc.). The

definition of the IT industry changes constantly, depending on the geographic

region being studied, the organization conducting the study, and the purpose and

objectives of the study.

For the spa industry, the definitional challenge is especially complex because the term

“spa” can incorporate many elements and is open to interpretation by spa operators,

consumers, and policymakers alike. While “spa” may be viewed as a relatively young

industry in its modern, Western archetype, its association with wellness and healing

links the industry to traditions and practices that date back thousands of years in some

cultures around the world. As economies and cultures become globalized, the blending

of modern and traditional therapeutic disciplines, and the melding of the science and

heritage of healing, have enriched the spa industry and increased consumer

recognition, even as this process creates challenges for the industry to define or

measure itself.

There is an ongoing, but perhaps healthy, tension among industry operators on the

definition of a spa. Currently the term “spa” is defined in a variety of ways, both

across different countries and regions and even within countries. Even the linguistic

origin of the word “spa” seems to be debated. Below we explore some of the existing

views and debates on what is a spa.

Using water-based or not as a definition

The linguistic origin of the term “spa” and whether the word is related to water is

unclear. According to some researchers, the term was derived from the name of a

Belgian town where mineral springs were used for healing purposes since medieval

times. According to some others, the word “spa” is an acronym of various Latin phrases

that mean “health through water.” A few other accounts trace the word to the old

Walloon word espa, meaning “fountain.”1 It is true that in many cultures spas are

closely tied to therapeutic treatments associated with water. Therefore, some would

1 Jonathan Paul De Vierville, “Spa Industry, Culture, and Evolution,” Massage and Bodywork Magazine, August-

September 2003, www.massageandbodywork.com/Articles/AugSep2003/Cultureandevolution.html.

The Global Spa Economy 2007

Copyright Global Spa Summit 2008 9 SRI International

define a spa as only those establishments that offer authentic water-based therapeutic

treatments, prescribed and/or supervised by doctors or qualified professionals, in a

healing and relaxing setting. However, establishments have proliferated around the

world that offer a menu of services (including massage, body, and/or facial

treatments) that do not involve water-based therapies, and these establishments are

more often than not considered to be spas by the business operators and their

consumers.

Using size and services to identify spas for benchmarking

For the purposes of benchmarking or conducting industry censuses or counts, many

organizations have chosen to define a spa by its size (e.g., an establishment must have

at least five treatment rooms to be included as a benchmark) or by the types of

treatments offered (e.g., an establishment must provide more than one type of spa

service – facial treatments, body treatments, massage, or water-based therapeutic

treatments – to be included in the count). It should be noted that a number of

establishments that consumers around the world may consider to be “spas” may not

meet these criteria. For example, a small salon that has only four treatment rooms and

only offers facial treatments would be considered a “spa” by many consumers, but

may not be counted in benchmarking studies or censuses that use a size-based or

service-based definition.

Using an exclusive versus democratic (or mass market) definition

The proliferation of day spas, “value” spa chains, new business models such as mobile

spas, and the expansion/crossover of health clubs and beauty salons into the spa

industry have raised concerns about service quality and image amongst some in the

industry. On the high end of the market are the “brand name” and exclusive spas,

which offer ambience, luxury facilities, and high-quality service delivered by well-

trained staff at prices aimed at upscale consumers. On the other end of the market

are establishments that offer services for a fraction of the price, aimed at the mass

market and consumers seeking those price points. They may specialize and offer only

one type of service, such as massage. These market developments raise questions

about who should be qualified to use the term “spa” for marketing and promotion

purposes.

Defining spas in the local, cultural, and historical context

Rising levels of income, education, and sophistication among travelers and consumers

worldwide have dramatically elevated the consciousness and desirability of treatments

that are derived from historical and culturally based healing traditions, techniques,

and ingredients. The market potential of this development is being captured by

global, premium-brand spas that have expanded their service menus to incorporate

The Global Spa Economy 2007

Copyright Global Spa Summit 2008 10 SRI International

these kinds of treatments. At the same time, establishments that offer traditional

bathing, healing, herbal, and therapeutic treatments derived from centuries-old

practices also recognize the potential of branding themselves as spas, and some are

investing in new services, equipment, facilities, as well as modifying their ambience.

European bath houses and saunas, Japanese onsens, Turkish-style hammams, Indian

ayurveda centers, and Thai massage establishments do not necessarily fit the

traditional Western concept or business model of spas, but a certain portion of these

have begun and will continue to cross over to the spa market as they evolve and

adapt to the needs and desires of modern consumers.

Taking into account these emerging market trends, and for the benefit of the industry,

this study has adopted a decidedly inclusive approach in its estimation of the global

spa economy. As stated above, an inherent goal of this study is to promote the value

of flexibility in defining the term “spa” and to understand its different interpretations

by businesses and consumers around the world.

Spa Typologies

Working within this framework, the global spa economy model captures five general

categories, or “typologies,” of spas, as described below.

Day/Club/Salon Spas. Facilities that offer a variety of spa services (e.g.,

massage, facials, body treatments, etc.) by trained professionals on a day-use

basis. They typically offer private treatment rooms and a quiet and peaceful

atmosphere. Club spas are similar to day spas, but operate out of facilities whose

primary purpose is fitness. Salon spas are also similar in nature, but operate out of

facilities that provide beauty services (such as hair, make-up, nails, etc.).

Destination Spas and Health Resorts. Offer a full-immersion spa experience in

which all guests participate. All-inclusive programs provide various spa and body

treatments along with a myriad of other offerings such as: fitness activities, healthy

cuisine, educational classes, nutrition counseling, weight loss programs, preventive

or curative medical services, mind/body/spirit offerings, etc. Because of their

similar business structures (e.g., overnight stays in which all guests participate in

full-immersion spa and wellness-based activities), this report includes traditional

European-style health resorts and Indian ayurvedic resorts in the same category as

destination spas.2

2 The estimation methodology counts all revenues and employment for these properties as being part of the spa

economy, including room revenues, food and beverage revenues, and other non-spa service revenues.

The Global Spa Economy 2007

Copyright Global Spa Summit 2008 11 SRI International

Hotel/Resort Spas. Similar to a day spa, but the spa facility is located within a

resort or hotel property. Unlike destination spas, at hotel/resort spas services are

typically paid for on an à la carte basis, and meals are not included. Spa

treatments and services generally complement a hotel stay or a wide range of

other activities at a resort.

Medical Spas. A spa facility that operates under the full-time, on-site supervision

of a licensed healthcare professional. Provides comprehensive medical and/or

wellness care in an environment that integrates spa services with traditional or

alternative medical therapies and treatments.

“Other” Spas. This category encompasses all other spas that are not captured by

the categories described above, including the following:

Historically-/Culturally-Based Spas. These spa facilities vary from country-to-

country and have spun out of historical healing traditions, techniques, and

ingredients, such as: European bath houses and saunas, Japanese onsens and

sentos, Turkish-style hammams, Indian ayurveda centers, Thai massage

establishments, Chinese medicine/massage practitioners, etc. This study

attempts to capture the portion of such facilities that have evolved into spas by

adding spa-like services (e.g., massage, facials, body treatments, wellness

education, etc.).

Mobile Spas. Professional practitioners provide spa services on-site at a

customer‟s home or office.

Single Service Spas. Similar to a day/club/salon spa, but specializes in

providing only one type of spa service (e.g., just massage or just facial

treatments).

Cruise Ship Spas. Similar to a hotel/resort spa, but located on board a cruise

ship.

Mineral/Hot Springs Spas. A day-use spa facility with an on-site source of

natural mineral, thermal, or sea water that is used in spa treatments. “Stay”

spas that use an on-site source of mineral, thermal, or sea water for treatments

are classified as hotel/resort spas or destination spas/health resorts,

depending on their characteristics.

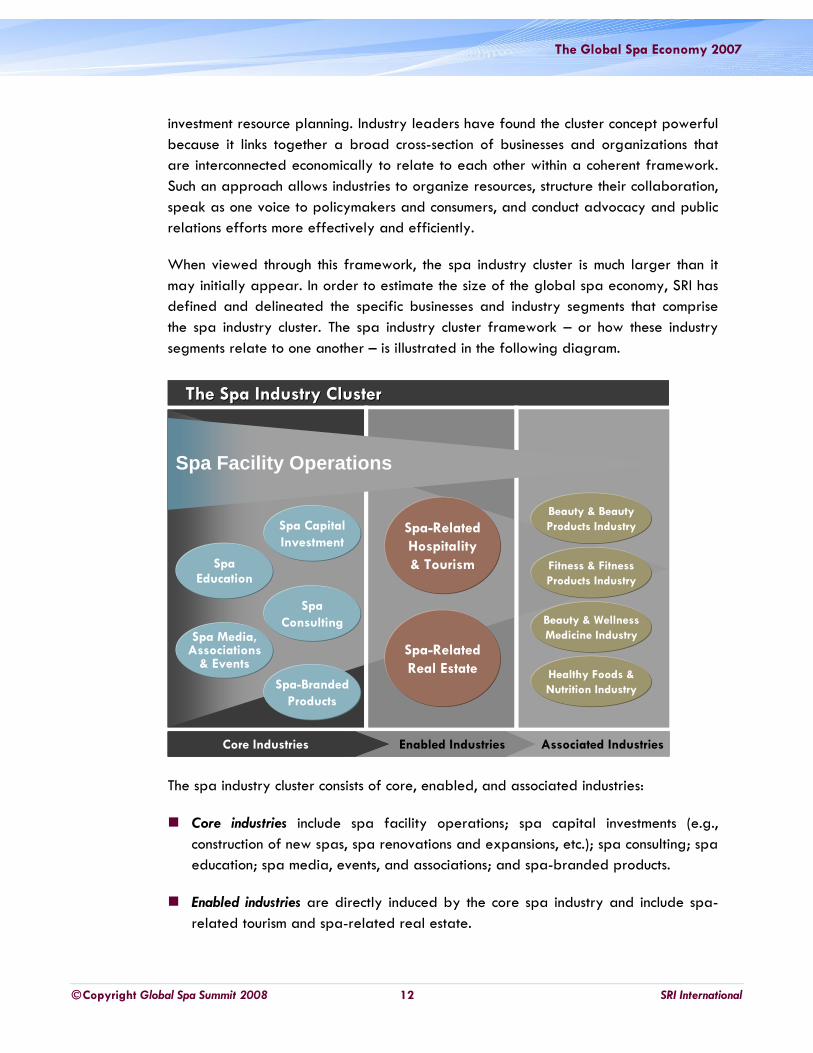

2. The Spa Industry Cluster

In this study of the global spa economy, SRI has employed an industry cluster

framework that has been widely used since the 1980s by industry and government

stakeholders around the world. The industry cluster concept is recognized as a useful

analytical and organizing mechanism for high-level strategic planning, advocacy, and

The Global Spa Economy 2007

Copyright Global Spa Summit 2008 12 SRI International

investment resource planning. Industry leaders have found the cluster concept powerful

because it links together a broad cross-section of businesses and organizations that

are interconnected economically to relate to each other within a coherent framework.

Such an approach allows industries to organize resources, structure their collaboration,

speak as one voice to policymakers and consumers, and conduct advocacy and public

relations efforts more effectively and efficiently.

When viewed through this framework, the spa industry cluster is much larger than it

may initially appear. In order to estimate the size of the global spa economy, SRI has

defined and delineated the specific businesses and industry segments that comprise

the spa industry cluster. The spa industry cluster framework – or how these industry

segments relate to one another – is illustrated in the following diagram.

The spa industry cluster consists of core, enabled, and associated industries:

Core industries include spa facility operations; spa capital investments (e.g.,

construction of new spas, spa renovations and expansions, etc.); spa consulting; spa

education; spa media, events, and associations; and spa-branded products.

Enabled industries are directly induced by the core spa industry and include spa-

related tourism and spa-related real estate.

Spa-Related

Hospitality

& Tourism

Spa-Related

Real Estate

The Spa Industry ClusterThe Spa Industry Cluster

Spa Capital

Investment

Spa-Branded

Products

Spa

ConsultingSpa Media,

Associations& Events

SpaEducation

Beauty & Beauty

Products Industry

Fitness & Fitness

Products Industry

Beauty & Wellness

Medicine Industry

Healthy Foods &

Nutrition Industry

Spa Facility Operations

Associated IndustriesEnabled IndustriesCore Industries

Spa-Related

Hospitality

& Tourism

Spa-Related

Real Estate

The Spa Industry ClusterThe Spa Industry Cluster

Spa Capital

Investment

Spa-Branded

Products

Spa

ConsultingSpa Media,

Associations& Events

SpaEducation

Beauty & Beauty

Products Industry

Fitness & Fitness

Products Industry

Beauty & Wellness

Medicine Industry

Healthy Foods &

Nutrition Industry

Spa Facility Operations

Associated IndustriesEnabled IndustriesCore Industries Associated IndustriesAssociated IndustriesEnabled IndustriesEnabled IndustriesCore IndustriesCore Industries

The Global Spa Economy 2007

Copyright Global Spa Summit 2008 13 SRI International

Associated industries represent a selected set of industries that are interconnected

with the spa industry through a common emphasis on health and wellness, and, to

some extent, common sales and marketing channels. Associated industries are

closely related to the spa industry, but not strictly a part of it; they are directly

promoted by the spa industry, and, in turn, the spa industry is promoted by them.

Associated industries include: beauty and beauty products; fitness and fitness

products; beauty and wellness medicine; and healthy foods and nutrition.

B. Quantifying The Size Of The Spa Economy

Determining what is included in the spa industry is only the first step in estimating the

size of the global spa economy. Quantifying the size of the spa industry is an

ambitious endeavor that poses another set of challenges:

There is a dearth of data on the spa industry for the majority of countries around

the world.

Within the traditional industry classification frameworks used by national

governments and international organizations, it is not possible to separate spas

from other related beauty, fitness, tourism, and medical industries. Therefore,

conventional public sector data sources are of limited use when conducting

research of this nature.

A number of high-quality spa industry studies have been conducted, but these

studies cover no more than 20 countries around the world. Big data and research

gaps exist for the fast-growing countries in Asia, Latin America, and the Middle

East. Furthermore, each of these studies utilizes different methodologies for

qualifying and quantifying spas, making it difficult to compare one study‟s findings

to another.

Faced with these challenges, the SRI team pursued multiple lines of inquiry gather data

from primary and secondary sources, including: a global survey that collected

approximately 1,000 responses; national and international-level qualitative and

quantitative data and reports; existing spa industry reports; and over 50 high-level

executive interviews. These inputs were used to create a consistent and comparable

estimation model to quantify the spa industry in 210 countries, including those where

major data gaps exist.

An important lesson that emerged from this exercise is the colossal need for the

industry and governments to collect and maintain information on the spa industry. It is

the hope of the research team that this small step is a productive one for the industry.

The Global Spa Economy 2007

Copyright Global Spa Summit 2008 14 SRI International

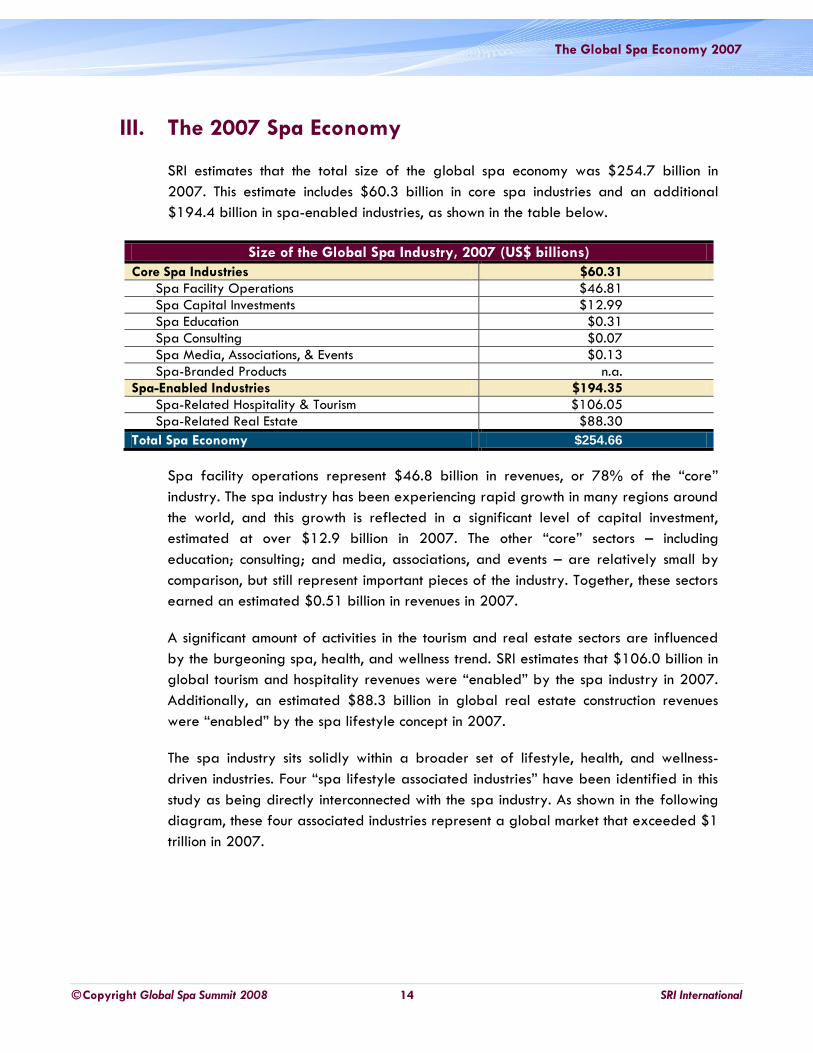

III. The 2007 Spa Economy

SRI estimates that the total size of the global spa economy was $254.7 billion in

2007. This estimate includes $60.3 billion in core spa industries and an additional

$194.4 billion in spa-enabled industries, as shown in the table below.

Size of the Global Spa Industry, 2007 (US$ billions)

Core Spa Industries $60.31

Spa Facility Operations $46.81

Spa Capital Investments $12.99

Spa Education $0.31

Spa Consulting $0.07

Spa Media, Associations, & Events $0.13

Spa-Branded Products n.a.

Spa-Enabled Industries $194.35

Spa-Related Hospitality & Tourism $106.05

Spa-Related Real Estate $88.30

Total Spa Economy $254.66

Spa facility operations represent $46.8 billion in revenues, or 78% of the “core”

industry. The spa industry has been experiencing rapid growth in many regions around

the world, and this growth is reflected in a significant level of capital investment,

estimated at over $12.9 billion in 2007. The other “core” sectors – including

education; consulting; and media, associations, and events – are relatively small by

comparison, but still represent important pieces of the industry. Together, these sectors

earned an estimated $0.51 billion in revenues in 2007.

A significant amount of activities in the tourism and real estate sectors are influenced

by the burgeoning spa, health, and wellness trend. SRI estimates that $106.0 billion in

global tourism and hospitality revenues were “enabled” by the spa industry in 2007.

Additionally, an estimated $88.3 billion in global real estate construction revenues

were “enabled” by the spa lifestyle concept in 2007.

The spa industry sits solidly within a broader set of lifestyle, health, and wellness-

driven industries. Four “spa lifestyle associated industries” have been identified in this

study as being directly interconnected with the spa industry. As shown in the following

diagram, these four associated industries represent a global market that exceeded $1

trillion in 2007.

The Global Spa Economy 2007

Copyright Global Spa Summit 2008 15 SRI International

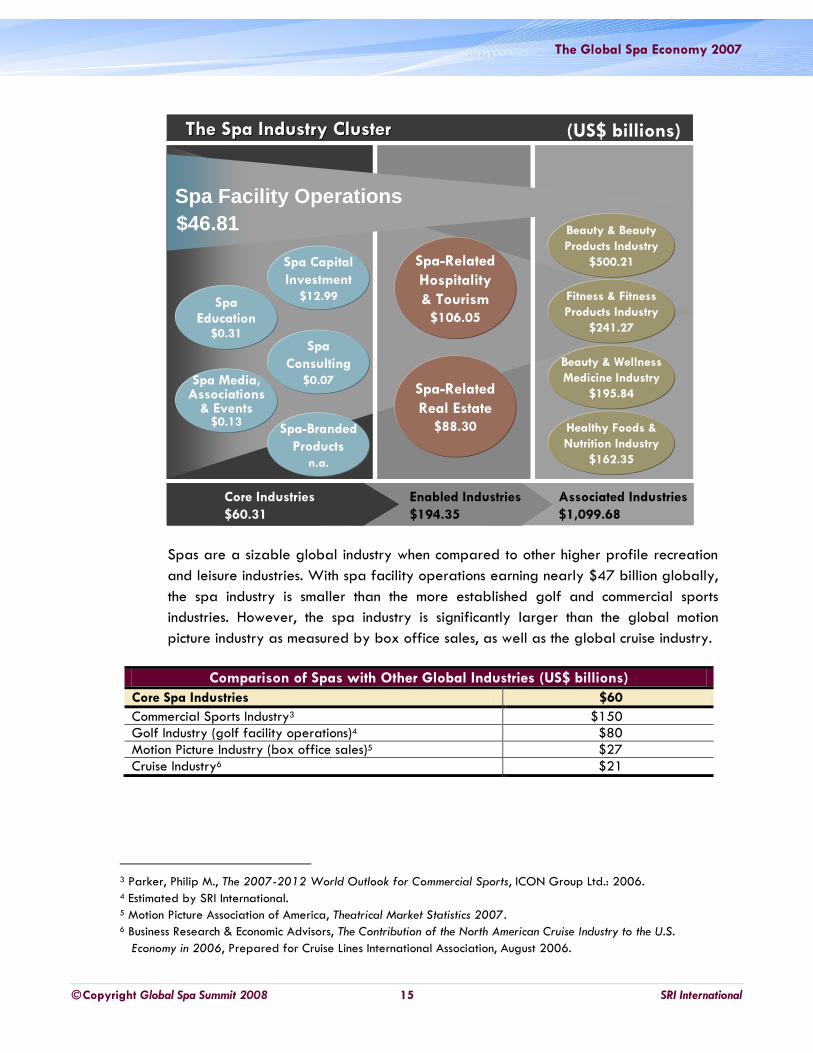

Spas are a sizable global industry when compared to other higher profile recreation

and leisure industries. With spa facility operations earning nearly $47 billion globally,

the spa industry is smaller than the more established golf and commercial sports

industries. However, the spa industry is significantly larger than the global motion

picture industry as measured by box office sales, as well as the global cruise industry.

Comparison of Spas with Other Global Industries (US$ billions)

Core Spa Industries $60

Commercial Sports Industry3 $150

Golf Industry (golf facility operations)4 $80

Motion Picture Industry (box office sales)5 $27

Cruise Industry6 $21

3 Parker, Philip M., The 2007-2012 World Outlook for Commercial Sports, ICON Group Ltd.: 2006. 4 Estimated by SRI International. 5 Motion Picture Association of America, Theatrical Market Statistics 2007. 6 Business Research & Economic Advisors, The Contribution of the North American Cruise Industry to the U.S.

Economy in 2006, Prepared for Cruise Lines International Association, August 2006.

Spa-Related

Hospitality

& Tourism

$106.05

Spa-Related

Real Estate

$88.30

The Spa Industry ClusterThe Spa Industry Cluster

Spa Capital

Investment

$12.99

Spa-Branded

Products

n.a.

Spa

Consulting

$0.07Spa Media,Associations

& Events$0.13

SpaEducation

$0.31

Beauty & Beauty

Products Industry

$500.21

Fitness & Fitness

Products Industry

$241.27

Beauty & Wellness

Medicine Industry

$195.84

Healthy Foods &

Nutrition Industry

$162.35

Spa Facility Operations

Associated Industries

$1,099.68

Enabled Industries

$194.35

Core Industries

$60.31

$46.81

(US$ billions)

Spa-Related

Hospitality

& Tourism

$106.05

Spa-Related

Real Estate

$88.30

The Spa Industry ClusterThe Spa Industry Cluster

Spa Capital

Investment

$12.99

Spa-Branded

Products

n.a.

Spa

Consulting

$0.07Spa Media,Associations

& Events$0.13

SpaEducation

$0.31

Beauty & Beauty

Products Industry

$500.21

Fitness & Fitness

Products Industry

$241.27

Beauty & Wellness

Medicine Industry

$195.84

Healthy Foods &

Nutrition Industry

$162.35

Spa Facility Operations

Associated Industries

$1,099.68

Associated Industries

$1,099.68

Enabled Industries

$194.35

Enabled Industries

$194.35

Core Industries

$60.31

Core Industries

$60.31

$46.81

(US$ billions)

The Global Spa Economy 2007

Copyright Global Spa Summit 2008 16 SRI International

A. Core Spa Industries

1. Spa Facility Operations

Spa facility operations represent the core of the spa economy. They include the wide

variety of services offered at spas – including massages, facials, body treatments,

salon services, water-based treatments, health assessments, and much more – as well

as sales of products at spas.

In 2007 there were an estimated 71,762 spas operating around the world, including:

45,113 day/club/salon spas;

11,489 hotel/resort spas;

1,485 destination spas and health resorts;

4,274 medical spas; and

9,310 “other” spas.7

Together, these spas generated an estimated $46.8 billion in revenues and employed

an estimated 1.2 million persons in 2007.

Global Spa Facilities by Type, 2007

Estimated Total Number of Spas

Estimated Total Spa Revenues (US$ billions)

Estimated Total Spa Employment

Day/Club/Salon Spas 45,113 $21.0 659,106

Hotel/Resort Spas 11,489 $12.6 269,363

Destination Spas & Health Resorts 1,485 $6.2 112,239

Medical Spas 4,274 $4.6 51,843

Other Spas 9,310 $2.4 130,958

Total 71,672 $46.8 1,223,510

7 Definitions of each type of spa are provided in section II of this report.

Global Distribution of Spas, by Type of Spa, 2007

The Global Spa Economy 2007

Copyright Global Spa Summit 2008 17 SRI International

Number of Spas Worldwide, by Type of Spa, 2007

Other Spas

(9,310) 13.0%

Medical Spas

(4,274) 6.0%

Destination

Spas & Health

Resorts

(1,485) 2.1%

Hotel/Resort

Spas

(11,489) 16.0%

Day/Club/Salon

Spas

(45,113) 62.9%

Revenues of Spas Worldwide, by Type of Spa, 2007

Other Spas

($2.4) 5.1%

Medical Spas

($4.6) 9.9%

Destination

Spas & Health

Resorts

($6.2) 13.2%

Hotel/Resort

Spas

($12.6) 26.9%

Day/Club/Salon

Spas

($21.0) 44.9%

(US$ billions)

Employment by Spas Worldwide, by Type of Spa, 2007

Other Spas

(130,958) 10.7%

Medical Spas

(51,843) 4.2%

Destination

Spas & Health

Resorts

(112,239) 9.2%

Hotel/Resort

Spas

(269,363) 22.0%

Day/Club/Salon

Spas

(659,106) 53.9%

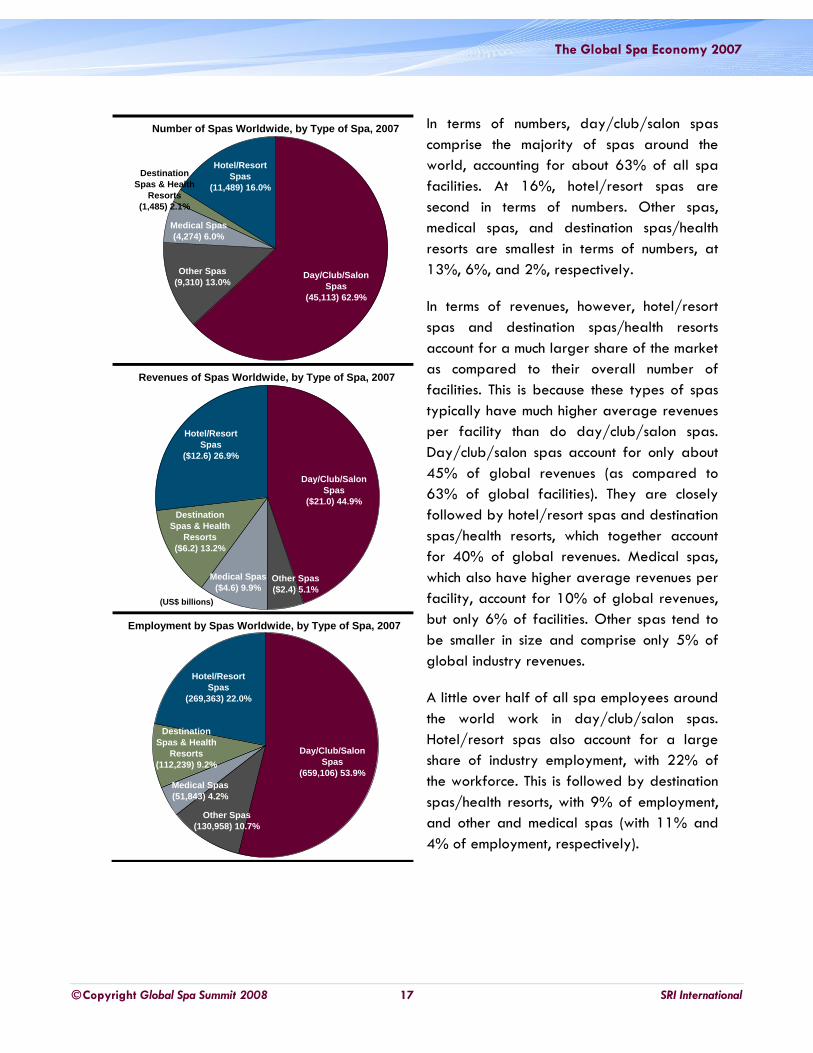

In terms of numbers, day/club/salon spas

comprise the majority of spas around the

world, accounting for about 63% of all spa

facilities. At 16%, hotel/resort spas are

second in terms of numbers. Other spas,

medical spas, and destination spas/health

resorts are smallest in terms of numbers, at

13%, 6%, and 2%, respectively.

In terms of revenues, however, hotel/resort

spas and destination spas/health resorts

account for a much larger share of the market

as compared to their overall number of

facilities. This is because these types of spas

typically have much higher average revenues

per facility than do day/club/salon spas.

Day/club/salon spas account for only about

45% of global revenues (as compared to

63% of global facilities). They are closely

followed by hotel/resort spas and destination

spas/health resorts, which together account

for 40% of global revenues. Medical spas,

which also have higher average revenues per

facility, account for 10% of global revenues,

but only 6% of facilities. Other spas tend to

be smaller in size and comprise only 5% of

global industry revenues.

A little over half of all spa employees around

the world work in day/club/salon spas.

Hotel/resort spas also account for a large

share of industry employment, with 22% of

the workforce. This is followed by destination

spas/health resorts, with 9% of employment,

and other and medical spas (with 11% and

4% of employment, respectively).

The Global Spa Economy 2007

Copyright Global Spa Summit 2008 18 SRI International

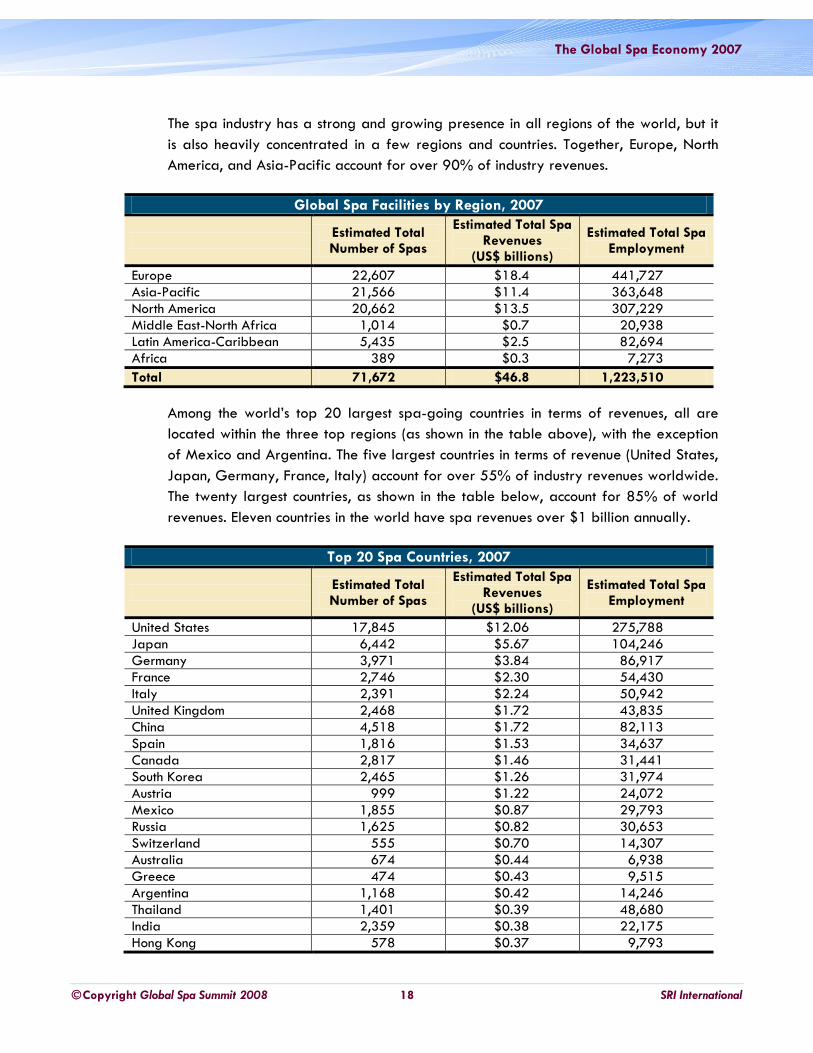

The spa industry has a strong and growing presence in all regions of the world, but it

is also heavily concentrated in a few regions and countries. Together, Europe, North

America, and Asia-Pacific account for over 90% of industry revenues.

Global Spa Facilities by Region, 2007

Estimated Total Number of Spas

Estimated Total Spa Revenues

(US$ billions)

Estimated Total Spa Employment

Europe 22,607 $18.4 441,727

Asia-Pacific 21,566 $11.4 363,648

North America 20,662 $13.5 307,229

Middle East-North Africa 1,014 $0.7 20,938

Latin America-Caribbean 5,435 $2.5 82,694

Africa 389 $0.3 7,273

Total 71,672 $46.8 1,223,510

Among the world‟s top 20 largest spa-going countries in terms of revenues, all are

located within the three top regions (as shown in the table above), with the exception

of Mexico and Argentina. The five largest countries in terms of revenue (United States,

Japan, Germany, France, Italy) account for over 55% of industry revenues worldwide.

The twenty largest countries, as shown in the table below, account for 85% of world

revenues. Eleven countries in the world have spa revenues over $1 billion annually.

Top 20 Spa Countries, 2007

Estimated Total Number of Spas

Estimated Total Spa Revenues

(US$ billions)

Estimated Total Spa Employment

United States 17,845 $12.06 275,788

Japan 6,442 $5.67 104,246

Germany 3,971 $3.84 86,917

France 2,746 $2.30 54,430

Italy 2,391 $2.24 50,942

United Kingdom 2,468 $1.72 43,835

China 4,518 $1.72 82,113

Spain 1,816 $1.53 34,637

Canada 2,817 $1.46 31,441

South Korea 2,465 $1.26 31,974

Austria 999 $1.22 24,072

Mexico 1,855 $0.87 29,793

Russia 1,625 $0.82 30,653

Switzerland 555 $0.70 14,307

Australia 674 $0.44 6,938

Greece 474 $0.43 9,515

Argentina 1,168 $0.42 14,246

Thailand 1,401 $0.39 48,680

India 2,359 $0.38 22,175

Hong Kong 578 $0.37 9,793

The Global Spa Economy 2007

Copyright Global Spa Summit 2008 19 SRI International

Spa Industry Profile: Europe

In terms of revenues, number of spas, and employment, Europe is the largest

regional spa market in the world. It had an estimated 22,607 spas in 2007,

earning $18.4 billion in revenues and employing 441,727 people.

Europe‟s massive spa market has evolved from bathing and wellness traditions that

date back to medieval, and even Roman, times. The region has a deep-rooted spa

and wellness culture that emphasizes the use of natural and water-based elements

for therapeutic, curative, and preventive treatments.

In Europe, the “other” spas category primarily captures the extensive bath house

and sauna facilities that are especially prevalent in northern and eastern European

countries and in the former Soviet Bloc. A selected portion of these facilities in each

country is estimated to have crossed over into the spa industry by adding spa

facilities and services. Because they are smaller-sized establishments, these spas

represent approximately 2% of European spa market revenues.

Europe is also unique in that it is home to a large number of health resorts that

emphasize wellness, traditional healing therapies, and medically-based services.

For instance, in Russia and eastern Europe, there are hundreds, or even thousands,

of sanatoriums dating from the Soviet era, which offer wellness-based

healing/medical services and frequently require a long-term stay. A large portion

of these sanatoriums – many of which were state-owned or subsidized and have a

hospital-like atmosphere – are now out-moded or even closed down. However, a

small number are being modernized and re-cast as higher-end health resorts and

are crossing over into the spa industry. Overall, health resorts and destination spas

represent an estimated 27% of European spa industry revenues.

Spa Facilities in Europe, 2007

Estimated Total Number of Spas

Estimated Total Spa Revenues (US$ billions)

Estimated Total Spa Employment

Day/Club/Salon Spas 14,933 $7.55 237,473

Hotel/Resort Spas 4,297 $4.61 84,117

Destination Spas/Health Resorts 1,202 $4.93 91,962

Medical Spas 913 $0.87 9,248

Other Spas 1,262 $0.39 18,927

Total 22,607 $18.35 441,727

The Global Spa Economy 2007

Copyright Global Spa Summit 2008 20 SRI International

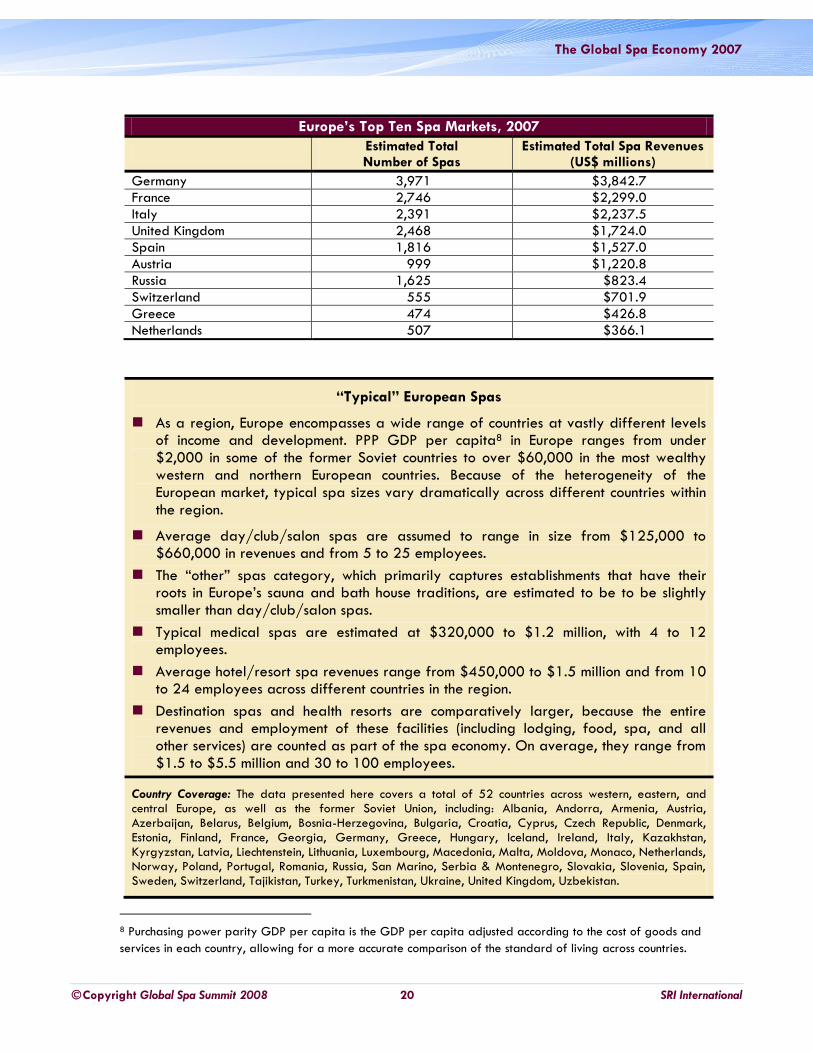

Europe’s Top Ten Spa Markets, 2007

Estimated Total Number of Spas

Estimated Total Spa Revenues (US$ millions)

Germany 3,971 $3,842.7

France 2,746 $2,299.0

Italy 2,391 $2,237.5

United Kingdom 2,468 $1,724.0

Spain 1,816 $1,527.0

Austria 999 $1,220.8

Russia 1,625 $823.4

Switzerland 555 $701.9

Greece 474 $426.8

Netherlands 507 $366.1

“Typical” European Spas

As a region, Europe encompasses a wide range of countries at vastly different levels of income and development. PPP GDP per capita8 in Europe ranges from under $2,000 in some of the former Soviet countries to over $60,000 in the most wealthy western and northern European countries. Because of the heterogeneity of the European market, typical spa sizes vary dramatically across different countries within the region.

Average day/club/salon spas are assumed to range in size from $125,000 to $660,000 in revenues and from 5 to 25 employees.

The “other” spas category, which primarily captures establishments that have their roots in Europe‟s sauna and bath house traditions, are estimated to be to be slightly smaller than day/club/salon spas.

Typical medical spas are estimated at $320,000 to $1.2 million, with 4 to 12 employees.

Average hotel/resort spa revenues range from $450,000 to $1.5 million and from 10 to 24 employees across different countries in the region.

Destination spas and health resorts are comparatively larger, because the entire revenues and employment of these facilities (including lodging, food, spa, and all other services) are counted as part of the spa economy. On average, they range from $1.5 to $5.5 million and 30 to 100 employees.

Country Coverage: The data presented here covers a total of 52 countries across western, eastern, and central Europe, as well as the former Soviet Union, including: Albania, Andorra, Armenia, Austria, Azerbaijan, Belarus, Belgium, Bosnia-Herzegovina, Bulgaria, Croatia, Cyprus, Czech Republic, Denmark, Estonia, Finland, France, Georgia, Germany, Greece, Hungary, Iceland, Ireland, Italy, Kazakhstan, Kyrgyzstan, Latvia, Liechtenstein, Lithuania, Luxembourg, Macedonia, Malta, Moldova, Monaco, Netherlands, Norway, Poland, Portugal, Romania, Russia, San Marino, Serbia & Montenegro, Slovakia, Slovenia, Spain, Sweden, Switzerland, Tajikistan, Turkey, Turkmenistan, Ukraine, United Kingdom, Uzbekistan.

8 Purchasing power parity GDP per capita is the GDP per capita adjusted according to the cost of goods and

services in each country, allowing for a more accurate comparison of the standard of living across countries.

The Global Spa Economy 2007

Copyright Global Spa Summit 2008 21 SRI International

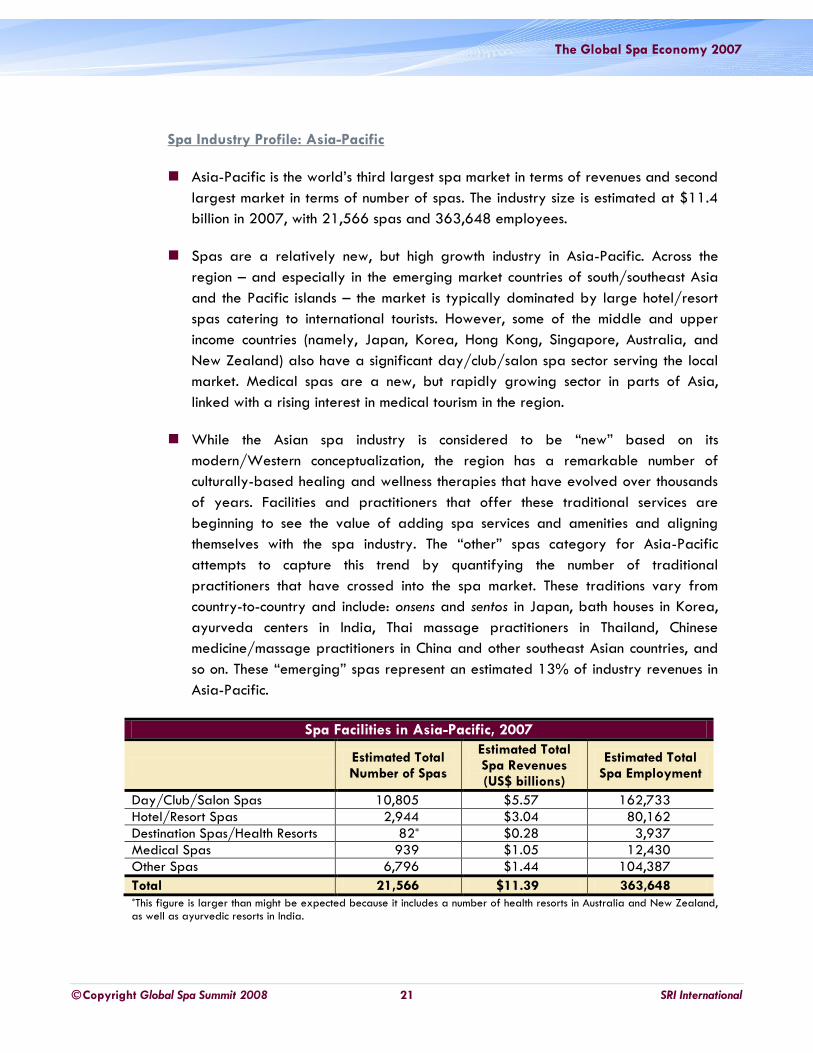

Spa Industry Profile: Asia-Pacific

Asia-Pacific is the world‟s third largest spa market in terms of revenues and second

largest market in terms of number of spas. The industry size is estimated at $11.4

billion in 2007, with 21,566 spas and 363,648 employees.

Spas are a relatively new, but high growth industry in Asia-Pacific. Across the

region – and especially in the emerging market countries of south/southeast Asia

and the Pacific islands – the market is typically dominated by large hotel/resort

spas catering to international tourists. However, some of the middle and upper

income countries (namely, Japan, Korea, Hong Kong, Singapore, Australia, and

New Zealand) also have a significant day/club/salon spa sector serving the local

market. Medical spas are a new, but rapidly growing sector in parts of Asia,

linked with a rising interest in medical tourism in the region.

While the Asian spa industry is considered to be “new” based on its

modern/Western conceptualization, the region has a remarkable number of

culturally-based healing and wellness therapies that have evolved over thousands

of years. Facilities and practitioners that offer these traditional services are

beginning to see the value of adding spa services and amenities and aligning

themselves with the spa industry. The “other” spas category for Asia-Pacific

attempts to capture this trend by quantifying the number of traditional

practitioners that have crossed into the spa market. These traditions vary from

country-to-country and include: onsens and sentos in Japan, bath houses in Korea,

ayurveda centers in India, Thai massage practitioners in Thailand, Chinese

medicine/massage practitioners in China and other southeast Asian countries, and

so on. These “emerging” spas represent an estimated 13% of industry revenues in

Asia-Pacific.

Spa Facilities in Asia-Pacific, 2007

Estimated Total Number of Spas

Estimated Total Spa Revenues (US$ billions)

Estimated Total Spa Employment

Day/Club/Salon Spas 10,805 $5.57 162,733

Hotel/Resort Spas 2,944 $3.04 80,162

Destination Spas/Health Resorts 82* $0.28 3,937

Medical Spas 939 $1.05 12,430

Other Spas 6,796 $1.44 104,387

Total 21,566 $11.39 363,648 *This figure is larger than might be expected because it includes a number of health resorts in Australia and New Zealand, as well as ayurvedic resorts in India.

The Global Spa Economy 2007

Copyright Global Spa Summit 2008 22 SRI International

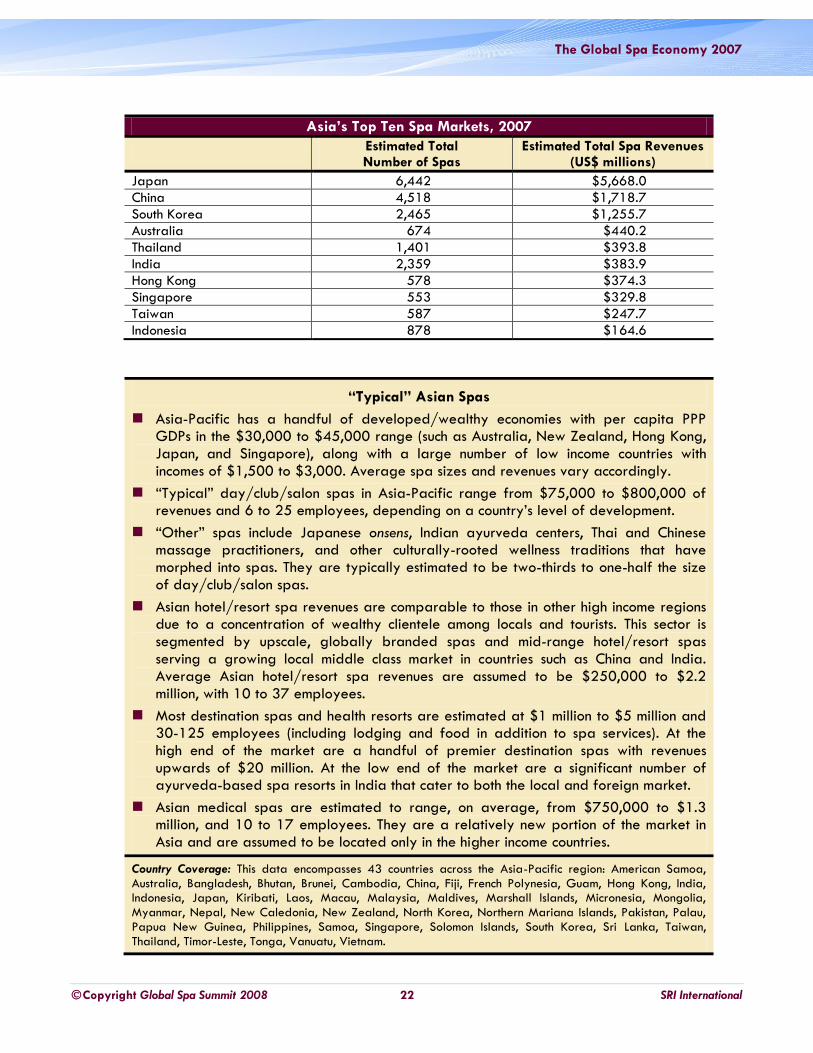

Asia’s Top Ten Spa Markets, 2007

Estimated Total Number of Spas

Estimated Total Spa Revenues (US$ millions)

Japan 6,442 $5,668.0

China 4,518 $1,718.7

South Korea 2,465 $1,255.7

Australia 674 $440.2

Thailand 1,401 $393.8

India 2,359 $383.9

Hong Kong 578 $374.3

Singapore 553 $329.8

Taiwan 587 $247.7

Indonesia 878 $164.6

“Typical” Asian Spas

Asia-Pacific has a handful of developed/wealthy economies with per capita PPP GDPs in the $30,000 to $45,000 range (such as Australia, New Zealand, Hong Kong, Japan, and Singapore), along with a large number of low income countries with incomes of $1,500 to $3,000. Average spa sizes and revenues vary accordingly.

“Typical” day/club/salon spas in Asia-Pacific range from $75,000 to $800,000 of revenues and 6 to 25 employees, depending on a country‟s level of development.

“Other” spas include Japanese onsens, Indian ayurveda centers, Thai and Chinese massage practitioners, and other culturally-rooted wellness traditions that have morphed into spas. They are typically estimated to be two-thirds to one-half the size of day/club/salon spas.

Asian hotel/resort spa revenues are comparable to those in other high income regions due to a concentration of wealthy clientele among locals and tourists. This sector is segmented by upscale, globally branded spas and mid-range hotel/resort spas serving a growing local middle class market in countries such as China and India. Average Asian hotel/resort spa revenues are assumed to be $250,000 to $2.2 million, with 10 to 37 employees.

Most destination spas and health resorts are estimated at $1 million to $5 million and 30-125 employees (including lodging and food in addition to spa services). At the high end of the market are a handful of premier destination spas with revenues upwards of $20 million. At the low end of the market are a significant number of ayurveda-based spa resorts in India that cater to both the local and foreign market.

Asian medical spas are estimated to range, on average, from $750,000 to $1.3 million, and 10 to 17 employees. They are a relatively new portion of the market in Asia and are assumed to be located only in the higher income countries.

Country Coverage: This data encompasses 43 countries across the Asia-Pacific region: American Samoa, Australia, Bangladesh, Bhutan, Brunei, Cambodia, China, Fiji, French Polynesia, Guam, Hong Kong, India, Indonesia, Japan, Kiribati, Laos, Macau, Malaysia, Maldives, Marshall Islands, Micronesia, Mongolia, Myanmar, Nepal, New Caledonia, New Zealand, North Korea, Northern Mariana Islands, Pakistan, Palau, Papua New Guinea, Philippines, Samoa, Singapore, Solomon Islands, South Korea, Sri Lanka, Taiwan, Thailand, Timor-Leste, Tonga, Vanuatu, Vietnam.

The Global Spa Economy 2007

Copyright Global Spa Summit 2008 23 SRI International

Spa Industry Profile: North America

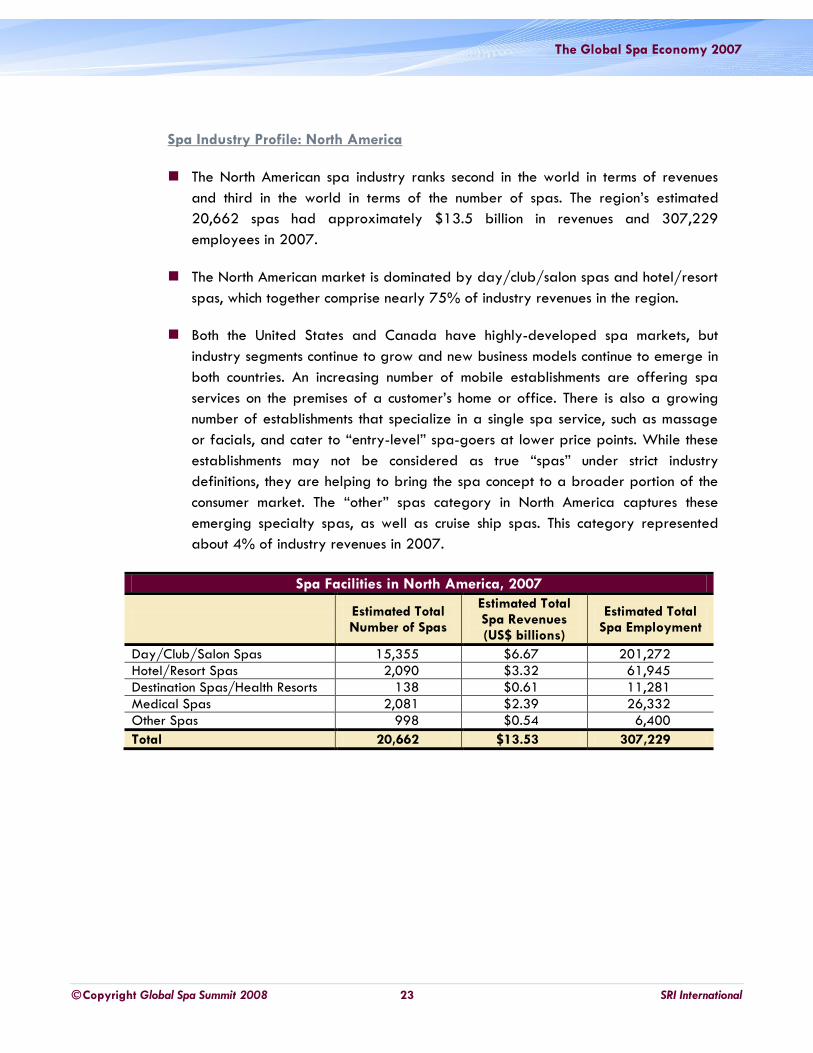

The North American spa industry ranks second in the world in terms of revenues

and third in the world in terms of the number of spas. The region‟s estimated

20,662 spas had approximately $13.5 billion in revenues and 307,229

employees in 2007.

The North American market is dominated by day/club/salon spas and hotel/resort

spas, which together comprise nearly 75% of industry revenues in the region.

Both the United States and Canada have highly-developed spa markets, but

industry segments continue to grow and new business models continue to emerge in

both countries. An increasing number of mobile establishments are offering spa

services on the premises of a customer‟s home or office. There is also a growing

number of establishments that specialize in a single spa service, such as massage

or facials, and cater to “entry-level” spa-goers at lower price points. While these

establishments may not be considered as true “spas” under strict industry

definitions, they are helping to bring the spa concept to a broader portion of the

consumer market. The “other” spas category in North America captures these

emerging specialty spas, as well as cruise ship spas. This category represented

about 4% of industry revenues in 2007.

Spa Facilities in North America, 2007

Estimated Total Number of Spas

Estimated Total Spa Revenues (US$ billions)

Estimated Total Spa Employment

Day/Club/Salon Spas 15,355 $6.67 201,272

Hotel/Resort Spas 2,090 $3.32 61,945

Destination Spas/Health Resorts 138 $0.61 11,281

Medical Spas 2,081 $2.39 26,332

Other Spas 998 $0.54 6,400

Total 20,662 $13.53 307,229

The Global Spa Economy 2007

Copyright Global Spa Summit 2008 24 SRI International

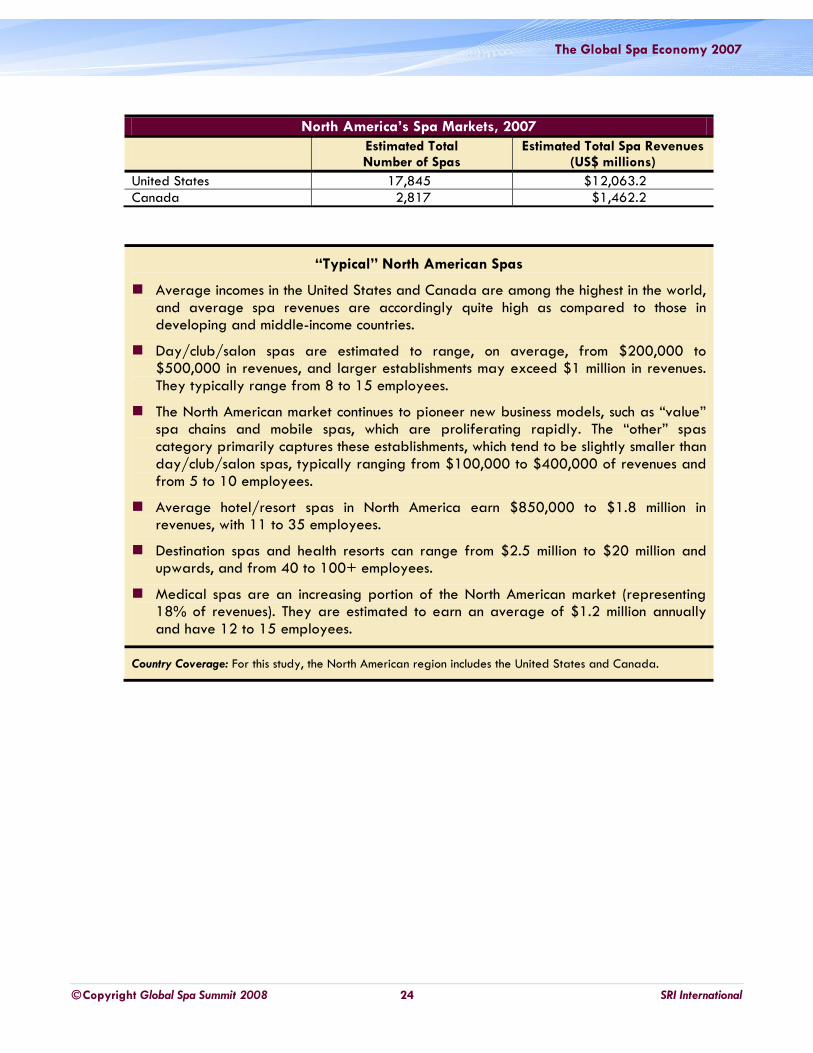

North America’s Spa Markets, 2007

Estimated Total Number of Spas

Estimated Total Spa Revenues (US$ millions)

United States 17,845 $12,063.2

Canada 2,817 $1,462.2

“Typical” North American Spas

Average incomes in the United States and Canada are among the highest in the world, and average spa revenues are accordingly quite high as compared to those in developing and middle-income countries.

Day/club/salon spas are estimated to range, on average, from $200,000 to $500,000 in revenues, and larger establishments may exceed $1 million in revenues. They typically range from 8 to 15 employees.

The North American market continues to pioneer new business models, such as “value” spa chains and mobile spas, which are proliferating rapidly. The “other” spas category primarily captures these establishments, which tend to be slightly smaller than day/club/salon spas, typically ranging from $100,000 to $400,000 of revenues and from 5 to 10 employees.

Average hotel/resort spas in North America earn $850,000 to $1.8 million in revenues, with 11 to 35 employees.

Destination spas and health resorts can range from $2.5 million to $20 million and upwards, and from 40 to 100+ employees.

Medical spas are an increasing portion of the North American market (representing 18% of revenues). They are estimated to earn an average of $1.2 million annually and have 12 to 15 employees.

Country Coverage: For this study, the North American region includes the United States and Canada.

The Global Spa Economy 2007

Copyright Global Spa Summit 2008 25 SRI International

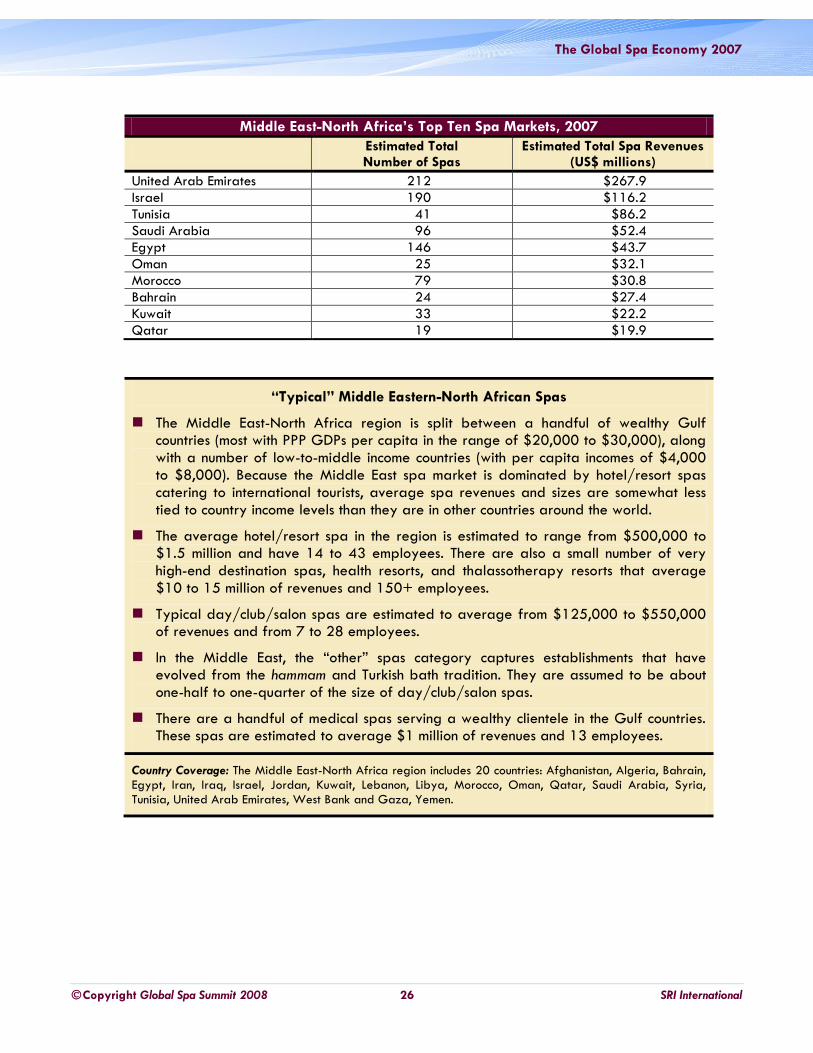

Spa Industry Profile: Middle East-North Africa

The Middle East and North Africa had approximately 1,014 spas, earning about

$747 million in revenues and employing 20,938 persons in 2007.

The spa industry in Middle East-North Africa differs significantly from that of other

regions in that it is dominated by the hotel/resort spa sector. Hotel/resort spas

represent over 60% of industry revenues in the Middle East, as compared to 25%

in North America, Europe, and Asia-Pacific. Day/club/salon spas are still a

comparatively small portion of the industry in the Middle East and North Africa,

with 19% of revenues in 2007.

The Middle East has a historic bathing tradition linked with hammams or Turkish

baths, which have their roots in the early days of Islam and which were derived

from Roman and Greek bathing traditions. Like other culturally-rooted wellness

traditions and therapies around the world, the hammams have many synergies with

the spa industry, and some are beginning to add upgraded spa facilities and

services. Conversely, many traditional day spas and hotel/resorts spas are adding

a cultural element to their services by offering specialized treatments that are

grounded in hammam bathing traditions. The “other” spas category in the Middle

East region attempts to quantify the traditional hammams and bath houses that

have crossed over to the spa sector – this category represented just over 1% of

industry revenues in 2007.

Spa Facilities in Middle East-North Africa, 2007

Estimated Total Number of Spas

Estimated Total Spa Revenues (US$ billions)

Estimated Total Spa Employment

Day/Club/Salon Spas 440 $0.14 6,259

Hotel/Resort Spas 441 $0.45 12,554

Destination Spas/Health Resorts 7 $0.11 1,300

Medical Spas 26 $0.03 331

Other Spas 99 $0.01 494

Total 1,014 $0.75 20,938

The Global Spa Economy 2007

Copyright Global Spa Summit 2008 26 SRI International

Middle East-North Africa’s Top Ten Spa Markets, 2007

Estimated Total Number of Spas

Estimated Total Spa Revenues (US$ millions)

United Arab Emirates 212 $267.9

Israel 190 $116.2

Tunisia 41 $86.2

Saudi Arabia 96 $52.4

Egypt 146 $43.7

Oman 25 $32.1

Morocco 79 $30.8

Bahrain 24 $27.4

Kuwait 33 $22.2

Qatar 19 $19.9

“Typical” Middle Eastern-North African Spas

The Middle East-North Africa region is split between a handful of wealthy Gulf countries (most with PPP GDPs per capita in the range of $20,000 to $30,000), along with a number of low-to-middle income countries (with per capita incomes of $4,000 to $8,000). Because the Middle East spa market is dominated by hotel/resort spas catering to international tourists, average spa revenues and sizes are somewhat less tied to country income levels than they are in other countries around the world.

The average hotel/resort spa in the region is estimated to range from $500,000 to $1.5 million and have 14 to 43 employees. There are also a small number of very high-end destination spas, health resorts, and thalassotherapy resorts that average $10 to 15 million of revenues and 150+ employees.

Typical day/club/salon spas are estimated to average from $125,000 to $550,000 of revenues and from 7 to 28 employees.

In the Middle East, the “other” spas category captures establishments that have evolved from the hammam and Turkish bath tradition. They are assumed to be about one-half to one-quarter of the size of day/club/salon spas.

There are a handful of medical spas serving a wealthy clientele in the Gulf countries. These spas are estimated to average $1 million of revenues and 13 employees.

Country Coverage: The Middle East-North Africa region includes 20 countries: Afghanistan, Algeria, Bahrain, Egypt, Iran, Iraq, Israel, Jordan, Kuwait, Lebanon, Libya, Morocco, Oman, Qatar, Saudi Arabia, Syria, Tunisia, United Arab Emirates, West Bank and Gaza, Yemen.

The Global Spa Economy 2007

Copyright Global Spa Summit 2008 27 SRI International

Spa Industry Profile: Latin America-Caribbean

Latin America-Caribbean is the fourth largest spa region in the world, but its

industry is significantly smaller than those of the top three regions (Europe, North

America, and Asia-Pacific). It had an estimated 5,435 spas, with revenues of $2.5

billion and employment of 82,694 persons in 2007.

The spa market in Latin America-Caribbean is evenly split between

day/club/salon spas and hotel/resort spas, each accounting for about 39-40% of

industry revenues in 2007.

The Andes region, stretching from Panama in the north to the Patagonia region in

southern Chile and Argentina, is home to thousands of hot/thermal springs. Many

of these springs have been developed into resorts and bathing facilities, primarily

catering to local and regional tourists. While many are very basic, a portion of

these establishments offer a higher grade of services, amenities, and

accommodations and have crossed over to the spa industry. The “other” spas

category in Latin America-Caribbean quantifies this very small sector of the

industry, which accounted for less than 1% of overall industry revenues in 2007.

Spa Facilities in Latin America-Caribbean, 2007

Estimated Total Number of Spas

Estimated Total Spa Revenues (US$ billions)

Estimated Total Spa Employment

Day/Club/Salon Spas 3,381 $1.00 48,480

Hotel/Resort Spas 1,539 $0.99 26,571

Destination Spas/Health Resorts 48 $0.21 3,426

Medical Spas 313 $0.29 3,478

Other Spas 154 $0.01 740

Total 5,435 $2.52 82,694

Latin America-Caribbean’s Top Ten Spa Markets, 2007

Estimated Total Number of Spas

Estimated Total Spa Revenues (US$ millions)

Mexico 1,855 $868.6

Argentina 1,168 $419.8

Brazil 643 $284.2

Puerto Rico 177 $114.8

Colombia 250 $102.6

Chile 199 $102.0

Dominican Republic 171 $75.0

Venezuela 156 $70.7

Uruguay 76 $41.7

Bahamas 66 $39.1

The Global Spa Economy 2007

Copyright Global Spa Summit 2008 28 SRI International

“Typical” Latin American-Caribbean Spas

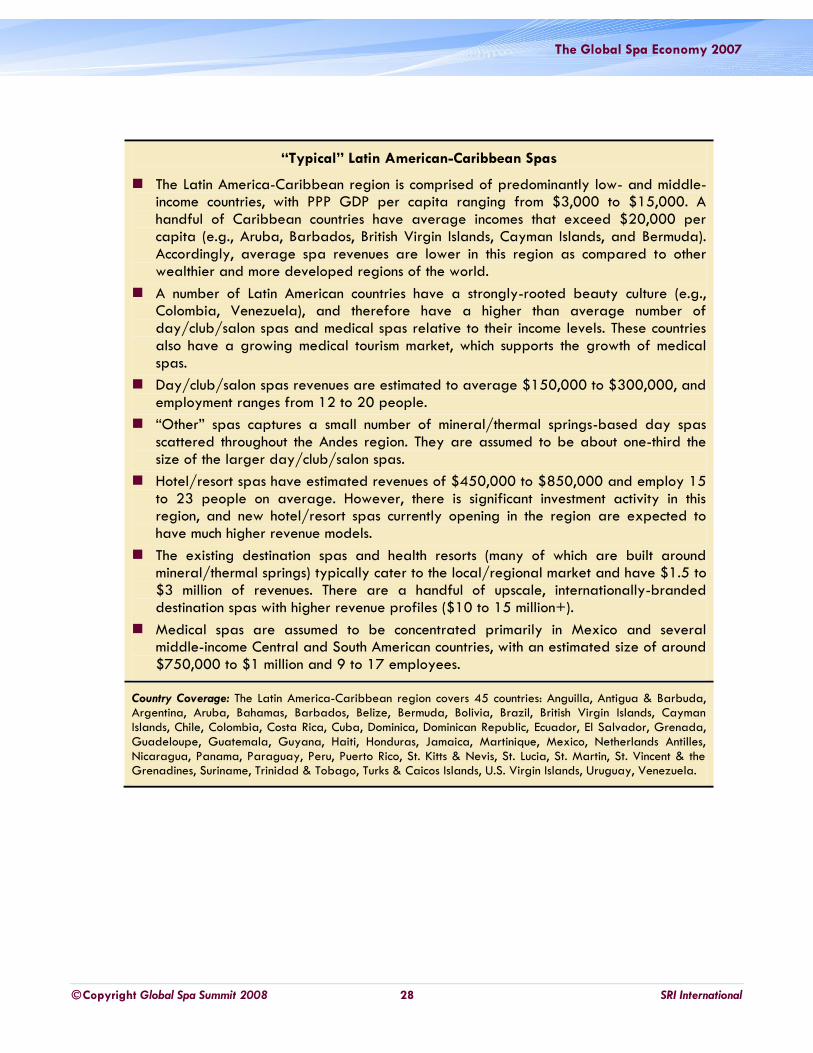

The Latin America-Caribbean region is comprised of predominantly low- and middle-income countries, with PPP GDP per capita ranging from $3,000 to $15,000. A handful of Caribbean countries have average incomes that exceed $20,000 per capita (e.g., Aruba, Barbados, British Virgin Islands, Cayman Islands, and Bermuda). Accordingly, average spa revenues are lower in this region as compared to other wealthier and more developed regions of the world.

A number of Latin American countries have a strongly-rooted beauty culture (e.g., Colombia, Venezuela), and therefore have a higher than average number of day/club/salon spas and medical spas relative to their income levels. These countries also have a growing medical tourism market, which supports the growth of medical spas.

Day/club/salon spas revenues are estimated to average $150,000 to $300,000, and employment ranges from 12 to 20 people.

“Other” spas captures a small number of mineral/thermal springs-based day spas scattered throughout the Andes region. They are assumed to be about one-third the size of the larger day/club/salon spas.

Hotel/resort spas have estimated revenues of $450,000 to $850,000 and employ 15 to 23 people on average. However, there is significant investment activity in this region, and new hotel/resort spas currently opening in the region are expected to have much higher revenue models.

The existing destination spas and health resorts (many of which are built around mineral/thermal springs) typically cater to the local/regional market and have $1.5 to $3 million of revenues. There are a handful of upscale, internationally-branded destination spas with higher revenue profiles ($10 to 15 million+).

Medical spas are assumed to be concentrated primarily in Mexico and several middle-income Central and South American countries, with an estimated size of around $750,000 to $1 million and 9 to 17 employees.

Country Coverage: The Latin America-Caribbean region covers 45 countries: Anguilla, Antigua & Barbuda, Argentina, Aruba, Bahamas, Barbados, Belize, Bermuda, Bolivia, Brazil, British Virgin Islands, Cayman Islands, Chile, Colombia, Costa Rica, Cuba, Dominica, Dominican Republic, Ecuador, El Salvador, Grenada, Guadeloupe, Guatemala, Guyana, Haiti, Honduras, Jamaica, Martinique, Mexico, Netherlands Antilles, Nicaragua, Panama, Paraguay, Peru, Puerto Rico, St. Kitts & Nevis, St. Lucia, St. Martin, St. Vincent & the Grenadines, Suriname, Trinidad & Tobago, Turks & Caicos Islands, U.S. Virgin Islands, Uruguay, Venezuela.

The Global Spa Economy 2007

Copyright Global Spa Summit 2008 29 SRI International

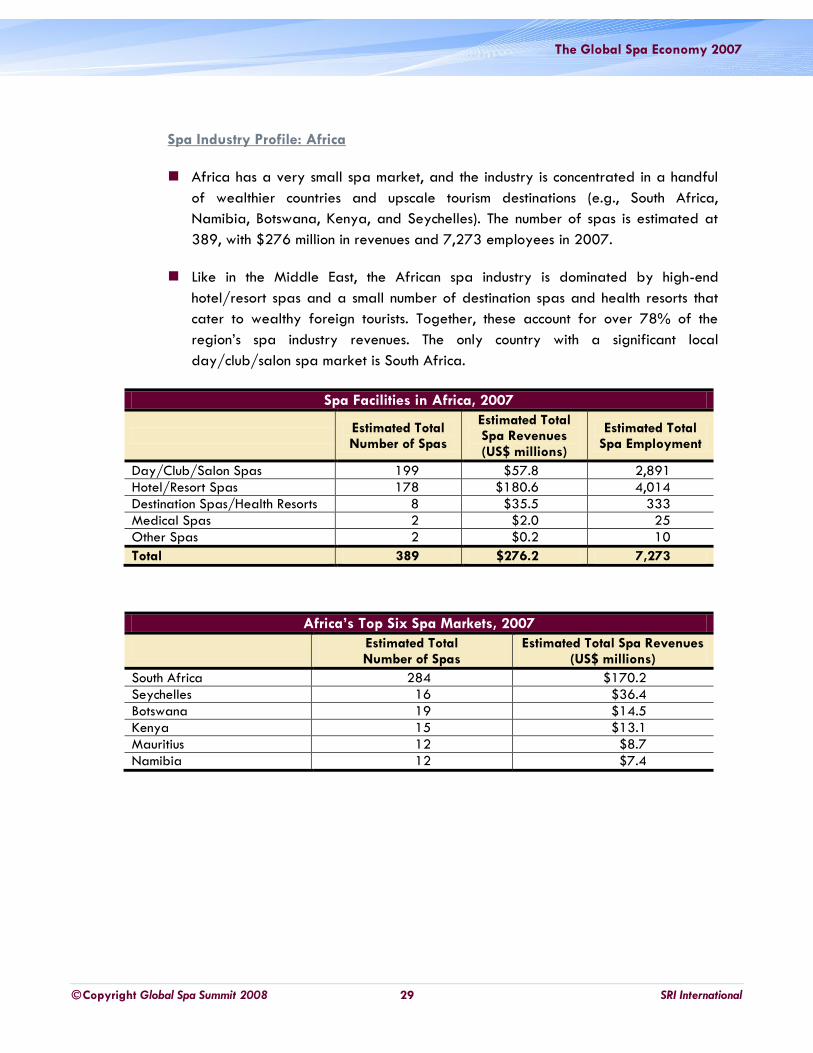

Spa Industry Profile: Africa

Africa has a very small spa market, and the industry is concentrated in a handful

of wealthier countries and upscale tourism destinations (e.g., South Africa,

Namibia, Botswana, Kenya, and Seychelles). The number of spas is estimated at

389, with $276 million in revenues and 7,273 employees in 2007.

Like in the Middle East, the African spa industry is dominated by high-end

hotel/resort spas and a small number of destination spas and health resorts that

cater to wealthy foreign tourists. Together, these account for over 78% of the

region‟s spa industry revenues. The only country with a significant local

day/club/salon spa market is South Africa.

Spa Facilities in Africa, 2007

Estimated Total Number of Spas

Estimated Total Spa Revenues (US$ millions)

Estimated Total Spa Employment

Day/Club/Salon Spas 199 $57.8 2,891

Hotel/Resort Spas 178 $180.6 4,014

Destination Spas/Health Resorts 8 $35.5 333

Medical Spas 2 $2.0 25

Other Spas 2 $0.2 10

Total 389 $276.2 7,273

Africa’s Top Six Spa Markets, 2007

Estimated Total Number of Spas

Estimated Total Spa Revenues (US$ millions)

South Africa 284 $170.2

Seychelles 16 $36.4

Botswana 19 $14.5

Kenya 15 $13.1

Mauritius 12 $8.7

Namibia 12 $7.4

The Global Spa Economy 2007

Copyright Global Spa Summit 2008 30 SRI International

“Typical” African Spas

The majority of African countries are very poor, and therefore the spa industry is assumed to be negligible throughout most of the region. South Africa is the only country in Africa with a sizeable spa industry. In 34 out of the 48 countries in this region, the spa industry is estimated to be zero for the purposes of this study.

There is also a small, but significant high-end niche tourism market in several southern African countries and islands, which supports a small sector of upscale hotel/resort spas, destination spas, and health resorts.

A “typical” day/club/salon spa in Africa is estimated to have $75,000 to $300,000 in revenues and 4 to 15 employees.

Hotel/resort spas, which almost exclusively serve wealthy international tourists, are estimated at $850,000 to $1.2 million, with 19 to 27 employees. There are a handful of small destination spas and health resorts in South Africa, along with one very upscale destination spa in Seychelles.

Country Coverage: The estimates presented here consider the following African countries: Angola, Benin, Botswana, Burkina Faso, Burundi, Cameroon, Cape Verde, Central African Republic, Chad, Comoros, Congo (Dem. Rep.), Congo (Rep.), Cote d'Ivoire, Djibouti, Equatorial Guinea, Eritrea, Ethiopia, Gabon, Gambia, Ghana, Guinea, Guinea-Bissau, Kenya, Lesotho, Liberia, Madagascar, Malawi, Mali, Mauritania, Mauritius, Mozambique, Namibia, Niger, Nigeria, Rwanda, Sao Tome & Principe, Senegal, Seychelles, Sierra Leone, Somalia, South Africa, Sudan, Swaziland, Tanzania, Togo, Uganda, Zambia, Zimbabwe.

The Global Spa Economy 2007

Copyright Global Spa Summit 2008 31 SRI International

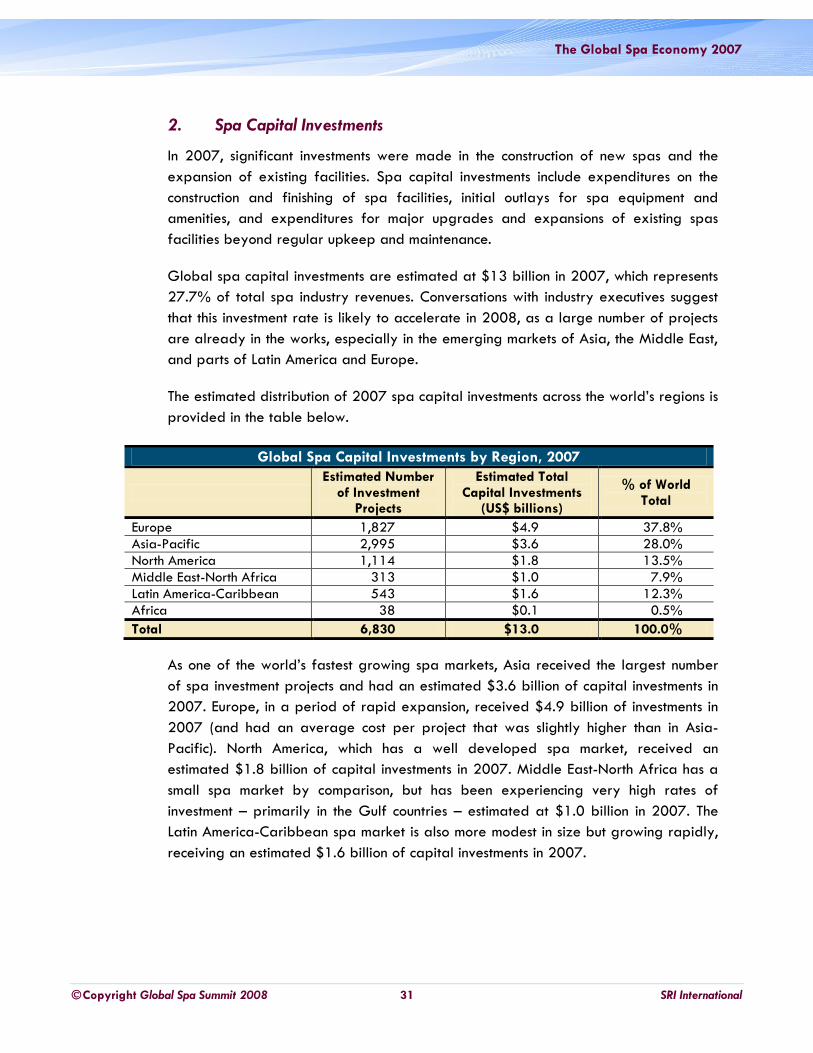

2. Spa Capital Investments

In 2007, significant investments were made in the construction of new spas and the

expansion of existing facilities. Spa capital investments include expenditures on the

construction and finishing of spa facilities, initial outlays for spa equipment and

amenities, and expenditures for major upgrades and expansions of existing spas

facilities beyond regular upkeep and maintenance.

Global spa capital investments are estimated at $13 billion in 2007, which represents

27.7% of total spa industry revenues. Conversations with industry executives suggest

that this investment rate is likely to accelerate in 2008, as a large number of projects

are already in the works, especially in the emerging markets of Asia, the Middle East,

and parts of Latin America and Europe.

The estimated distribution of 2007 spa capital investments across the world‟s regions is

provided in the table below.

Global Spa Capital Investments by Region, 2007

Estimated Number

of Investment Projects

Estimated Total Capital Investments

(US$ billions)

% of World Total

Europe 1,827 $4.9 37.8%

Asia-Pacific 2,995 $3.6 28.0%

North America 1,114 $1.8 13.5%

Middle East-North Africa 313 $1.0 7.9%

Latin America-Caribbean 543 $1.6 12.3%

Africa 38 $0.1 0.5%

Total 6,830 $13.0 100.0%

As one of the world‟s fastest growing spa markets, Asia received the largest number

of spa investment projects and had an estimated $3.6 billion of capital investments in

2007. Europe, in a period of rapid expansion, received $4.9 billion of investments in

2007 (and had an average cost per project that was slightly higher than in Asia-

Pacific). North America, which has a well developed spa market, received an

estimated $1.8 billion of capital investments in 2007. Middle East-North Africa has a

small spa market by comparison, but has been experiencing very high rates of

investment – primarily in the Gulf countries – estimated at $1.0 billion in 2007. The

Latin America-Caribbean spa market is also more modest in size but growing rapidly,

receiving an estimated $1.6 billion of capital investments in 2007.

The Global Spa Economy 2007

Copyright Global Spa Summit 2008 32 SRI International

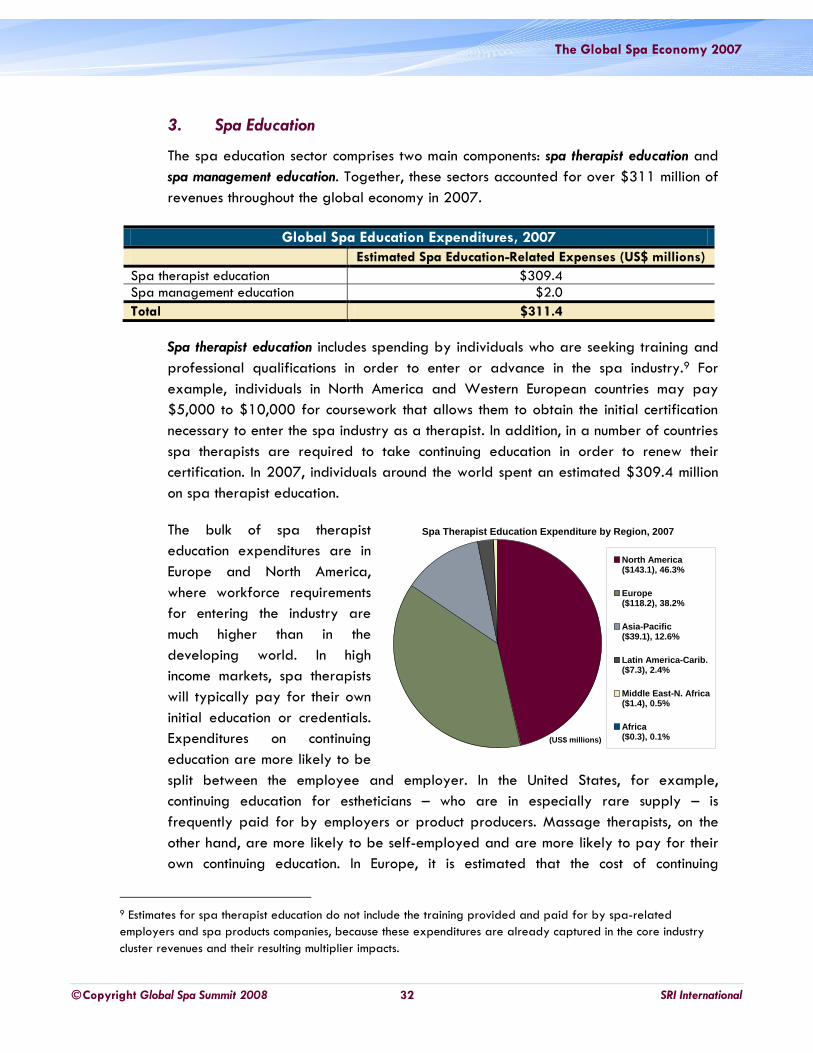

Spa Therapist Education Expenditure by Region, 2007

North America($143.1), 46.3%

Europe($118.2), 38.2%

Asia-Pacific($39.1), 12.6%

Latin America-Carib.($7.3), 2.4%

Middle East-N. Africa($1.4), 0.5%