the global economic crisis: asia and the role of china

TRANSCRIPT

11

The Global Economic Crisis: The Global Economic Crisis: Asia and the role of ChinaAsia and the role of China

Elliott School of International Affairs,Elliott School of International Affairs,George Washington UniversityGeorge Washington University

March 31, 2009March 31, 2009

Anoop SinghAnoop SinghAsia and Pacific DepartmentAsia and Pacific Department

IMFIMF

22

Five key questionsFive key questions

Why has Asia been hit so hard?Why has Asia been hit so hard?

What is the outlook for Asia?What is the outlook for Asia?

What are the main risks to Asia?What are the main risks to Asia?

What is the role for policies in the region?What is the role for policies in the region?

Is China different?Is China different?

Why has Asia been hit so hard?Why has Asia been hit so hard? 33

A sharp and synchronized collapse in A sharp and synchronized collapse in global growth...global growth...

World Real GDP growthYear-on-year percent change

-2

-1

0

1

2

3

4

5

6

7

8

1970

1973

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

2006

2009

First oil price shock Banking crisis IT bust

Source: IMF, World Economic Outlook database.

Latin America debt crisis and contractionary policies in industrialized economies

Why has Asia been hit so hard?Why has Asia been hit so hard? 44

...has hit Asia more than we expected...has hit Asia more than we expected

-20

-15

-10

-5

0

G-2 Asia (excl. China and

India)

Asia (excl. China and

India)

2008Q4 GDP Growth1

Quarter-on-quarter percent change, SAAR

Sources: Haver Analytics; and IMF, World Economic Outlook database and staff estimates. 1 PPP GDP Weighted. Does not include New Zealand and Vietnam.

The surprise in actual G-2 growth overNov-08 WEO forecast

…would have implied this revision for Asia based on the model.

But the actual revision was much larger-30

-25

-20

-15

-10

-5

0

Euro

Are

a

Uni

ted

Stat

es

Hon

g Ko

ng S

AR

Japa

n

Sing

apor

e

Kore

a

Taiw

an P

rovi

nce

of C

hina

2008Q4 GDP GrowthQuarter-on-quarter percent change, SAAR

Sources: Haver Analytics; and IMF staff calculations.

Why has Asia been hit so hard?Why has Asia been hit so hard? 55

...reflecting its specialization in ...reflecting its specialization in advanced manufacturingadvanced manufacturing

Canada

United States

Japan

Korea

France

GermanyItalyUnited Kingdom

Netherlands Spain

Mexico

Australia

Taiwan Province of China

Singapore

Malaysia

-30

-25

-20

-15

-10

-5

00.0 2.5 5.0 7.5 10.0 12.5 15.0 17.5 20.0

Share of high and medium-high tech manufacturing value added in GDP

GD

P G

row

th Q

4/20

08 (

SAAR

)

Sources: Haver Analytics; OECD; and IMF staff estimates.

Q4 GDP Growth vs. Share of Advanced Manufacturing in GDP

Why has Asia been hit so hard?Why has Asia been hit so hard? 66

Exports have declined through the Asian Exports have declined through the Asian supply chain, and more than in other regionssupply chain, and more than in other regions

-40

-30

-20

-10

0

Asia (excl. China andIndia, Jan-09)

Major LatinAmerica (Dec-08)

Euro Area(Dec-08)

Exports of Goods1

Year-on-year change; US$ basis

Sources: Haver Analytics; and IMF, World Economic Outlook database and staff calculations. 1 Nominal export share weighted for Asia and Latin America.

-80

-60

-40

-20

0

20

40

60

Jan-

07

Mar

-07

May

-07

Jul-

07

Sep-

07

Nov

-07

Jan-

08

Mar

-08

May

-08

Jul-

08

Sep-

08

Nov

-08

Jan-

09High value-added exporters 1/

Low value-added exporters 2/

Asia: Exports of Goods 3-month percent change of 3-mma, SAAR; US$ basis

Sources: Haver Analytics; CEIC Data Company Ltd.; and IMF staff calculations. 1/ Japan, Hong Kong SAR, Korea, Singapore,Taiwan Province of China and Thailand. 2/ China, India, Indonesia, Malaysia, Philippines, and Vietnam.

Why has Asia been hit so hard?Why has Asia been hit so hard? 77

A double hit for Asia: itA double hit for Asia: it’’s s bothbothexports and domestic demandexports and domestic demand

-6

-4

-2

0

2

4

6

8

1991

Q1

1992

Q1

1993

Q1

1994

Q1

1995

Q1

1996

Q1

1997

Q1

1998

Q1

1999

Q1

2000

Q1

2001

Q1

2002

Q1

2003

Q1

2004

Q1

2005

Q1

2006

Q1

2007

Q1

2008

Q1

ExportsDomestic demand

Japan and NIEs: Contribution to GDP growthYear-on-year, in percent

Asian Crisis

Sources: Haver Analytics; and IMF, World Economic Outlook database and staff calculations.

2000-01 recession

What is the outlook?What is the outlook? 88

Global recovery is expected only in midGlobal recovery is expected only in mid--2010 and risks are on the downside2010 and risks are on the downside

3.5 to 4.53.5 to 4.52.0 to 2.52.0 to 2.56.16.1Emerging and Emerging and developing economiesdeveloping economies

0.10.1--5.85.8--0.70.7JapanJapan

0.20.2--2.62.61.11.1Euro AreaEuro Area

0.30.3--3.23.20.80.8USUS

1.0 to 2.01.0 to 2.0--1.5 to 1.5 to --0.50.53.23.2World OutputWorld Output

201020102009200920082008

What is the outlook?What is the outlook? 99

What does this mean for Asia? What does this mean for Asia? Growth will fall sharply this year and Growth will fall sharply this year and

recovery will be slowrecovery will be slow

0.6 to 3.1 0.6 to 3.1 --5.8 to 5.8 to --3.93.91.71.7NIEsNIEs

2.5 to 4.12.5 to 4.10.4 to 2.70.4 to 2.74.94.9ASEANASEAN--55

5.4 to 6.45.4 to 6.43.4 to 4.23.4 to 4.26.96.9EmergingEmerging

0.0 to 0.80.0 to 0.8--5.0 to 5.0 to --2.22.2--0.30.3IndustrialIndustrial

4.2 to 5.24.2 to 5.21.4 to 2.71.4 to 2.75.15.1AsiaAsia

201020102009200920082008y/yy/y in in percentpercent

What are the risks to Asia?What are the risks to Asia? 1010

Risk 1: A much slower recovery of the Risk 1: A much slower recovery of the G2G2

95

100

105

110

115

t=0

t=1

t=2

t=3

t=4

t=5

t=6

t=7

t=8

t=9

t=10

t=11

2008Q1-2010Q42001Q1-2003Q41997Q3-2000Q2

United States: Gross Domestic ProductRebased at the beginning of each time period = 100

Source: IMF, World Economic Outlook database.

95

100

105

110

115

t=0

t=1

t=2

t=3

t=4

t=5

t=6

t=7

t=8

t=9

t=10

t=11

2008Q1-2010Q42001Q1-2003Q41997Q3-2000Q2

Euro Area: Gross Domestic ProductRebased at the beginning of each time period = 100

Source: IMF, World Economic Outlook database.

What are the risks to Asia?What are the risks to Asia? 1111

Risk 2: Intensified feedback loop Risk 2: Intensified feedback loop between corporates and banksbetween corporates and banks

0

100

200

300

400

500

600

700

Jan-

08

Feb-

08

Mar

-08

May

-08

Jun-

08

Jul-08

Sep-

08

Oct

-08

Dec

-08

Jan-

09

Feb-

09

Asia excl. Japan

Japan

Credit Risk: iTraxx Indices1

Sources: Bloomberg LP; and Datastream. 1 iTraxx Indices are a set of credit default swap indices covering regions or sectors and contain the most liquid names in that market, based on a dealer poll.

0 0.5 1 1.5 2

Hong Kong SAR

Thailand

Philippines

Korea

Malaysia

India

Australia

Indonesia

Sources: CEIC Data Company Ltd; and IMF staff calculations. 1 A ratio greater than unity implies a higher relative loss for the financial sector stocks. A ratio between zero and one implies financial sector stocks losing less than market since January 2008.

Selected Asia: Drop in Financial Sector Stocks vis-à-vis Overall Stock MarketRatio of change since January 2008

Worse than marketBetter than market

What are the risks to Asia?What are the risks to Asia? 1212

Risk 3: Much larger unemployment Risk 3: Much larger unemployment lies aheadlies ahead

-50

-40

-30

-20

-10

0

10

20

30

-4.5

-3.6

-2.7

-1.8

-0.9

0

0.9

1.8

2.7

Industrialproduction (LHS) Employment(RHS)

Selected Asia: Industrial Production and EmploymentYear-on-year percent change; January 2006 to January 2009

Sources: CEIC Data Company Ltd; and IMF staff calculations.

Japan Korea Taiwan Province of China

What are the risks to Asia?What are the risks to Asia? 1313

Risk 4: LongRisk 4: Long--term consequences of the term consequences of the end of the easy credit finance eraend of the easy credit finance era

600

800

1000

1200

1400

Jan-04 Nov-04 Sep-05 Jul-06 May-07 Mar-08 Jan-0920000

22500

25000

27500

30000Japanese exports of motorvehicles (LHS)U.S. new car loans:financed amount (RHS)

Source: Haver Analytics.

Japanese Exports of Motor Vehicles vs. Auto FinancingIn billions of Japanese Yen (left scale); in U.S. dollars per car (right scale)

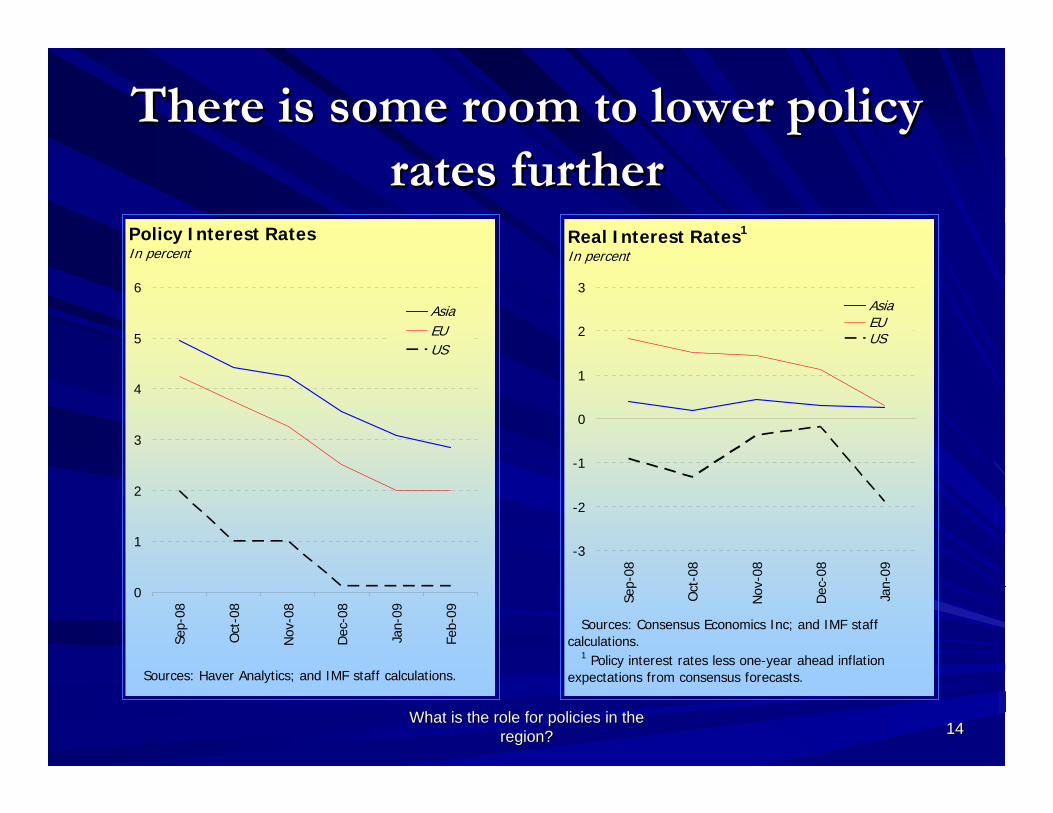

What is the role for policies in the What is the role for policies in the region?region? 1414

There is some room to lower policy There is some room to lower policy rates furtherrates further

Real Interest Rates1

In percent

-3

-2

-1

0

1

2

3

Sep-

08

Oct

-08

Nov

-08

Dec

-08

Jan-

09

AsiaEUUS

Sources: Consensus Economics Inc; and IMF staff calculations. 1 Policy interest rates less one-year ahead inflation expectations from consensus forecasts.

Policy Interest RatesIn percent

0

1

2

3

4

5

6

Sep-

08

Oct

-08

Nov

-08

Dec

-08

Jan-

09

Feb-

09

AsiaEUUS

Sources: Haver Analytics; and IMF staff calculations.

What is the role for policies in the What is the role for policies in the region?region? 1515

But unconventional policies may also But unconventional policies may also be neededbe needed

0

20

40

60

80

100

120

140

US Japan Korea

Domestic Assets on Central Bank Balance Sheets Change since June 2008, in percent

Sources: Haver Analytics; and IMF staff calculations.

3.5

4.5

5.5

6.5

7.5

8.5

9.5

Sources: CEIC Data Company Ltd; and IMF staff calculations.

Asia: Ratio of Base Money to Broad MoneyIn percent

Hong Kong SAR

Korea Japan

What is the role for policies in the What is the role for policies in the region?region? 1616

Strengthening bank capital would Strengthening bank capital would also helpalso help

0

1

2

3

4

5

6

7

Industrial Asia NIEs China and India ASEAN-4

Actual at end 2008

Expected 1-year ahead

Expected Increase in Bank Write-downs from Corporate Sector Loans1

In percent of banking sector loans

Source: IMF staff estimates. 1 Estimates are based on exposure to coporate sector loans and expected distress in corporate sector as indicated by credit default swap spreads.

What is the role for policies in the What is the role for policies in the region?region? 1717

Fiscal stimulus for 2009 is slightly Fiscal stimulus for 2009 is slightly above G20 average, butabove G20 average, but……

0

1

2

3

4

Indi

a

Indo

nesi

a

Japa

n

Aus

tral

ia

Kore

a

Chi

na

Ital

y

Braz

il

Fran

ce

Arg

entin

a

UK

Can

ada

Ger

man

y

Mex

ico

S. A

fric

a

US

Russ

ia

S. A

rabi

a

A v e r a g e ( P P P G D P w e i g h t e d )

G - 2 0 : D i s c r e t i o n a r y F i s c a l M e a s u r e s , 2 0 0 9I n p e r c e n t o f G D P

S o u r c e s : I M F , W o r l d E c o n o m i c O u t l o o k d a t a b a s e a n d s t a f f e s t i m a t e s a n d c a l c u l a t i o n s .

What is the role for policies in the What is the role for policies in the region?region? 1818

Further stimulus will be needed in Further stimulus will be needed in 20102010

- 1

0

1

2

3

4

Indi

a

Indo

nesi

a

Japa

n

Aust

ralia

Kore

a

Chin

a

Ital

y

Braz

il

Fran

ce UK

Cana

da

Ger

man

y

S. A

fric

a

US

Rus

sia

S. A

rabi

a

A v e r a g e ( P P P G D P w e i g h t e d )

G - 2 0 : D i s c r e t i o n a r y F i s c a l M e a s u r e s , 2 0 1 0I n p e r c e n t o f G D P

S o u r c e s : I M F , W o r l d E c o n o m i c O u t l o o k d a t a b a s e a n d s t a f f e s t im a t e s a n d c a l c u l a t i o n s .

1919

Is China different?Is China different?

What has its policy response been?What has its policy response been?

What is ChinaWhat is China’’s economic outlook? s economic outlook?

What are ChinaWhat are China’’s key mediums key medium--term term challenges?challenges?

Is China different?Is China different? 2020

China has not been immune to the China has not been immune to the crisiscrisis

0

5

10

15

20

25

Feb-07 Oct-07 Jun-08 Feb-09-40

-30

-20

-10

0

10

20

30

40

50

Value added

Exports (right axis)

Real Industrial Value Added and Exports(12-month growth rate)

Is China different?Is China different? 2121

But the authorities have responded But the authorities have responded proactivelyproactively

0.0

1.0

2.0

3.0

4.0

Jan-07 May-07 Sep-07 Jan-08 May-08 Sep-08 Jan-090.0

1.0

2.0

3.0

4.0

SHIBOR (7 days)

PBC Bill (3 months)

Interbank and Policy Rates

-4

-3

-2

-1

0

1

2001 2002 2003 2004 2005 2006 2007 2008 2009proj

2010proj.

0

7

14

21

Fiscal balance (left axis)

Government Debt

Debt and Fiscal Balance(In percent of GDP)

Is China different?Is China different? 2222

The stimulus is already working...The stimulus is already working...

Real Fixed Asset Investment Spending(Contribution to percent change, year-on-year)

-10

0

10

20

30

40

Jan-06 Jul-06 Jan-07 Jul-07 Jan-08 Jul-08 Jan-09-10

0

10

20

30

40

Non-SOESOETotal

-3

2

7

12

17

22

27

Jul-05 Jan-06 Jul-06 Jan-07 Jul-07 Jan-08 Jul-08 Jan-09-200

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Loan growth (y-o-y, left axis)

Loan Growth and Monthly Loan

Is China different?Is China different? 2323

...and its spillovers are benefiting ...and its spillovers are benefiting householdshouseholds

8

10

12

14

16

18

20

Jan-06 Jul-06 Jan-07 Jul-07 Jan-08 Jul-08 Jan-09-30

-10

10

30

50

70

Retail sales (left axis)No. of passenger cars (right axis)

Real Retail Sales 1/(12-month growth rate)

(In percent)

1/ January and February data are averaged.

Is China different?Is China different? 2424

The policy action is expected to The policy action is expected to support Chinasupport China’’s growth s growth

-4

-2

0

2

4

6

8

10

12

14

1998 2000 2002 2004 2006 2008 2010proj.

-2

-1

0

1

2

3

4

5

6

7

Increase in deficit (right axis)GDP growth (left axis)

Growth and Increase in Fiscal Deficit(Percent change; percent of GDP)

Is China different?Is China different? 2525

...but the spillover to the region is ...but the spillover to the region is likely to remain small likely to remain small Capital Good Imports

(In percent change year-on-year)

-30

-20

-10

0

10

20

30

40

50

60

Feb-07 Jun-07 Oct-07 Feb-08 Jun-08 Oct-08 Feb-09-30

-20

-10

0

10

20

30

40

50

60

-40

-30

-20

-10

0

10

20

30

40

50

Feb-07 Jun-07 Oct-07 Feb-08 Jun-08 Oct-08 Feb-09-40

-30

-20

-10

0

10

20

30

40

50

ASEAN Asia

Imports from Asia(In percent change year-on-year)

Is China different?Is China different? 2626

ChinaChina’’s key medium term challenge: s key medium term challenge: rebalancing growthrebalancing growth

40

50

60

70

80

90

100

0 10,000 20,000 30,000 40,000 50,000 60,000 70,000

GDP per capita (US$, 2007)

China

IrelandSingapore

Malaysia

Consumption Expenditure(In percent of GDP, avereage for 2003–07)

KoreaThailandIndia

Japan

GDP Expenditure Components(In percent of GDP)

30

35

40

45

50

1997 1999 2001 2003 2005 20070

5

10

15

20

Private consumptionInvestmentNet exports

Is China different?Is China different? 2727

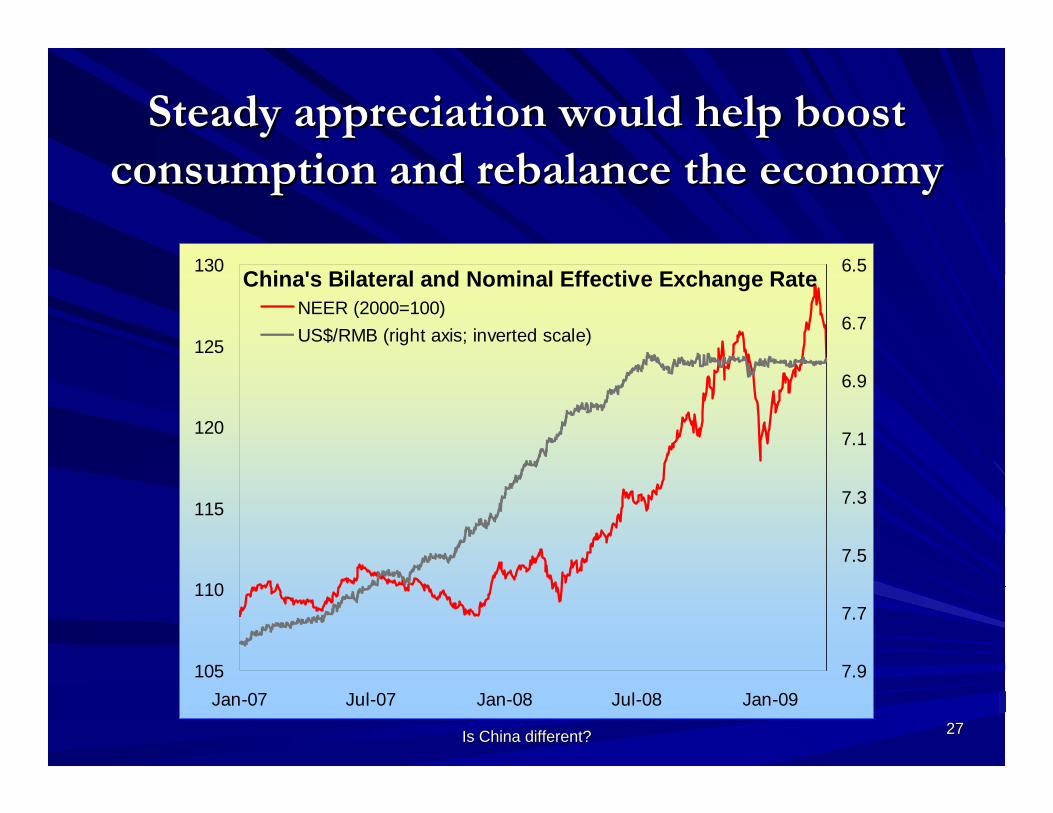

Steady appreciation would help boost Steady appreciation would help boost consumption and rebalance the economyconsumption and rebalance the economy

105

110

115

120

125

130

Jan-07 Jul-07 Jan-08 Jul-08 Jan-09

6.5

6.7

6.9

7.1

7.3

7.5

7.7

7.9

NEER (2000=100)US$/RMB (right axis; inverted scale)

China's Bilateral and Nominal Effective Exchange Rate

Is China different?Is China different? 2828

There is still scope for further fiscal stimulus There is still scope for further fiscal stimulus to reverse the decline in private consumptionto reverse the decline in private consumption

China: 2008–2010 Stimulus Package(In percent of 2008 GDP)

Infrastructure, 5.0

Healthcare and education, 0.5 Innovation and

structural adjustment, 1.2

Low-income housing support, 1.1

Environmental protection, 0.7

Rural incomes and infrastructure, 1.2Post-disaster

reconstruction, 3.3