rout china, asia-pacific (bi china) * china stocks in...

TRANSCRIPT

China, Asia-Pacific (BI CHINA)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2016 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Themes > Chapter: Growth and Value Consequences of China's Market Slump >> Exhibit 1 of 13

China Stocks' Precarious Start to 2016 Brings Valuation ChangesAnalysts: Tim Craighead & Elaine TungJan 8, 2016China's stock market has stayedvolatile as 2016 begins, continuingthe swings between elation anddepression experienced last year.The plunge during the first fourtrading days erased almost 12%from the CSI 300 index, led by majorreversals in the winners from late2015. Valuation has slipped closerto the levels of the MSCI World.Many "new economy" sectors aretrading below global norms whenrelatively lofty earnings growthexpectations are considered. HongKong shares continue to lag.

Key Points:* China's Stock Reversal Rattles Sectors as 4Q Leaders Fall Hard* China Small Caps in the Vanguard of Stock Performance,Valuation* Rout Brings China P/E Near Earth, Amid Higher EstimatedGrowth* Growth at a Reasonable Price More Evident After China StockRout* China Stocks in Hong Kong Are Ugly Stepchild Even WithMakeover

China TeamBloomberg Intelligence

China, Asia-Pacific (BI CHINA)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2016 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Themes > Chapter: Growth and Value Consequences of China's Market Slump >> Exhibit 2 of 13

China Yuan and Stock Drop; Causes and Consequences: BI WebinarAnalysts: Tim Craighead & Tom OrlikJan 8, 2016The Chinese market's start to2016 won't soon be forgotten. A12% plunge over four days trippednew circuit breakers, leading toearly closures on two days. OurBloomberg Intelligence webinarexplores the dynamics behind thedramatic drop in China's mainlandstock markets and currency. Welook at the economic links betweena weaker yuan and falling shares,and also examine performance,earnings growth expectations andvaluations in the selloff's wake. Clickthe exhibit to register and listen.

Economic and Market Considerations

China Team For interactive exhibit on Bloomberg, run:Bloomberg Intelligence HTTP 4568119<GO>

China, Asia-Pacific (BI CHINA)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2016 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Themes > Chapter: Growth and Value Consequences of China's Market Slump >> Exhibit 3 of 13

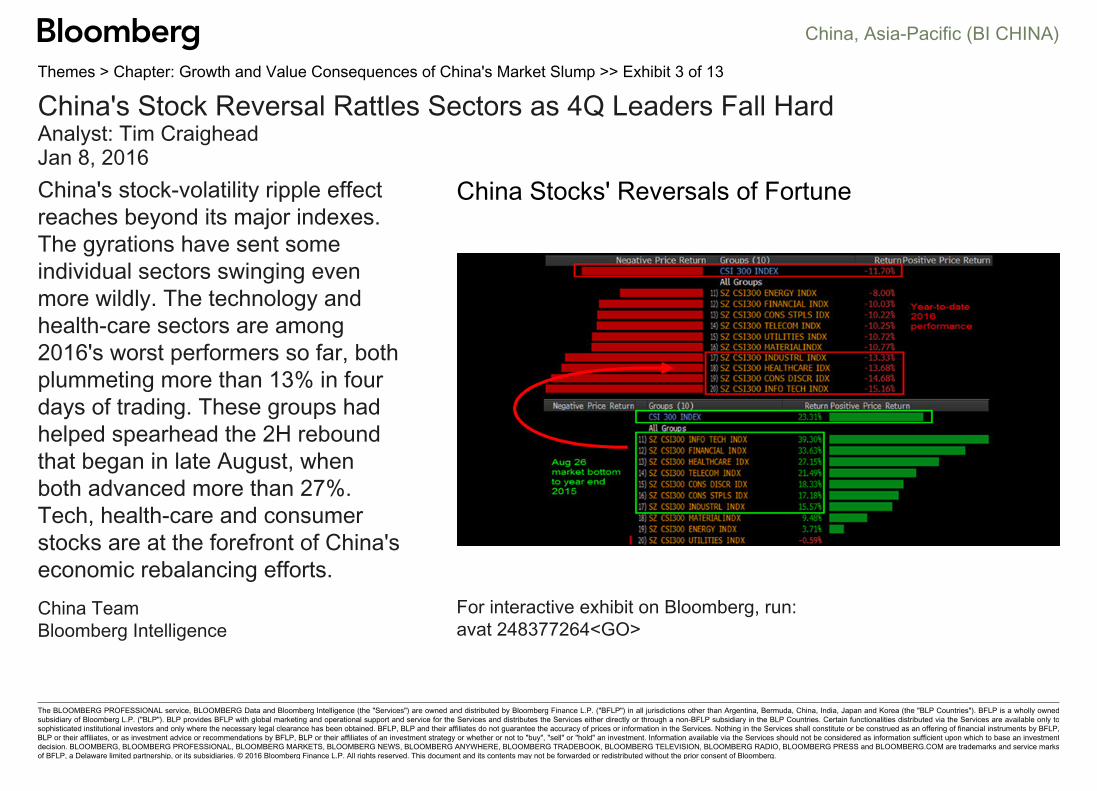

China's Stock Reversal Rattles Sectors as 4Q Leaders Fall HardAnalyst: Tim CraigheadJan 8, 2016China's stock-volatility ripple effectreaches beyond its major indexes.The gyrations have sent someindividual sectors swinging evenmore wildly. The technology andhealth-care sectors are among2016's worst performers so far, bothplummeting more than 13% in fourdays of trading. These groups hadhelped spearhead the 2H reboundthat began in late August, whenboth advanced more than 27%.Tech, health-care and consumerstocks are at the forefront of China'seconomic rebalancing efforts.

China Stocks' Reversals of Fortune

China Team For interactive exhibit on Bloomberg, run:Bloomberg Intelligence avat 248377264<GO>

China, Asia-Pacific (BI CHINA)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2016 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Themes > Chapter: Growth and Value Consequences of China's Market Slump >> Exhibit 4 of 13

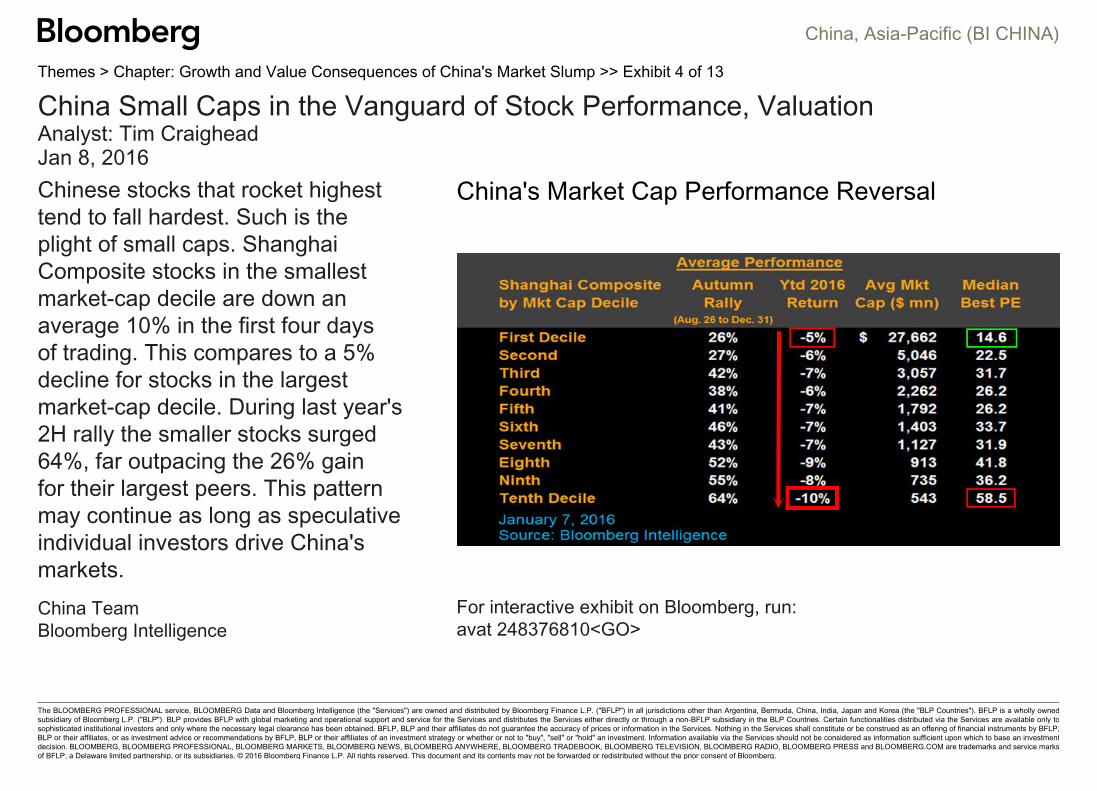

China Small Caps in the Vanguard of Stock Performance, ValuationAnalyst: Tim CraigheadJan 8, 2016Chinese stocks that rocket highesttend to fall hardest. Such is theplight of small caps. ShanghaiComposite stocks in the smallestmarket-cap decile are down anaverage 10% in the first four daysof trading. This compares to a 5%decline for stocks in the largestmarket-cap decile. During last year's2H rally the smaller stocks surged64%, far outpacing the 26% gainfor their largest peers. This patternmay continue as long as speculativeindividual investors drive China'smarkets.

China's Market Cap Performance Reversal

China Team For interactive exhibit on Bloomberg, run:Bloomberg Intelligence avat 248376810<GO>

China, Asia-Pacific (BI CHINA)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2016 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Themes > Chapter: Growth and Value Consequences of China's Market Slump >> Exhibit 5 of 13

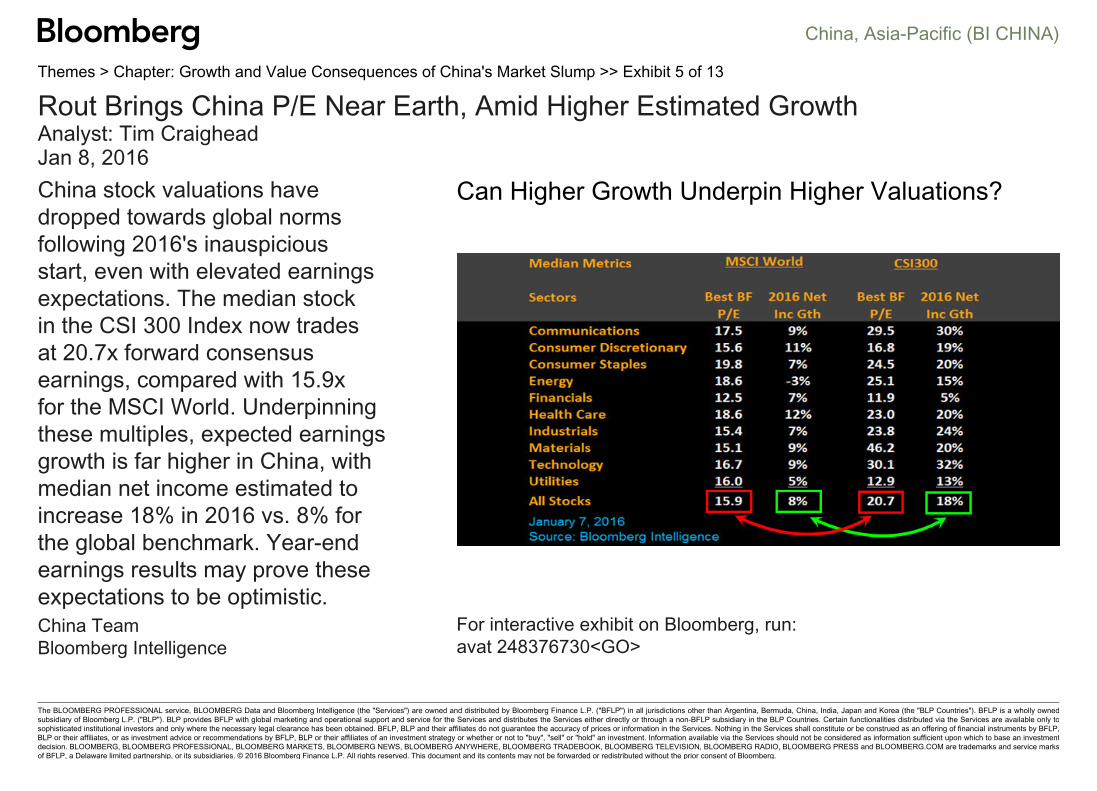

Rout Brings China P/E Near Earth, Amid Higher Estimated GrowthAnalyst: Tim CraigheadJan 8, 2016China stock valuations havedropped towards global normsfollowing 2016's inauspiciousstart, even with elevated earningsexpectations. The median stockin the CSI 300 Index now tradesat 20.7x forward consensusearnings, compared with 15.9xfor the MSCI World. Underpinningthese multiples, expected earningsgrowth is far higher in China, withmedian net income estimated toincrease 18% in 2016 vs. 8% forthe global benchmark. Year-endearnings results may prove theseexpectations to be optimistic.

Can Higher Growth Underpin Higher Valuations?

China Team For interactive exhibit on Bloomberg, run:Bloomberg Intelligence avat 248376730<GO>

China, Asia-Pacific (BI CHINA)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2016 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Themes > Chapter: Growth and Value Consequences of China's Market Slump >> Exhibit 6 of 13

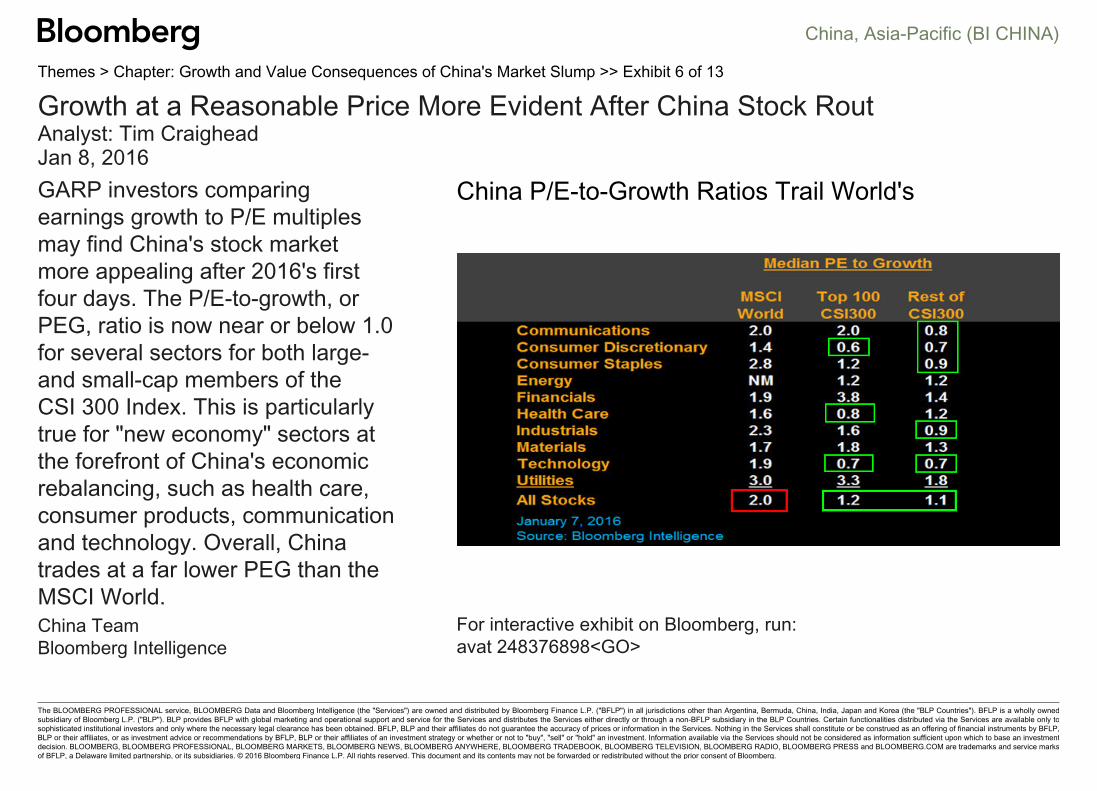

Growth at a Reasonable Price More Evident After China Stock RoutAnalyst: Tim CraigheadJan 8, 2016GARP investors comparingearnings growth to P/E multiplesmay find China's stock marketmore appealing after 2016's firstfour days. The P/E-to-growth, orPEG, ratio is now near or below 1.0for several sectors for both large-and small-cap members of theCSI 300 Index. This is particularlytrue for "new economy" sectors atthe forefront of China's economicrebalancing, such as health care,consumer products, communicationand technology. Overall, Chinatrades at a far lower PEG than theMSCI World.

China P/E-to-Growth Ratios Trail World's

China Team For interactive exhibit on Bloomberg, run:Bloomberg Intelligence avat 248376898<GO>

China, Asia-Pacific (BI CHINA)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2016 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Themes > Chapter: Growth and Value Consequences of China's Market Slump >> Exhibit 7 of 13

China Stocks in Hong Kong Are Ugly Stepchild Even With MakeoverAnalyst: Tim CraigheadJan 8, 2016The MSCI China Index remainsrelegated at an extreme discountto mainland China valuations, evenafter rebalancing. Adjustmentswere made in late-2015 to reflectthe changing nature of China'seconomy. Consumer, technologyand other "new economy" shareswere a welcome addition tothis globally-accessible index.Nonetheless, it trades at only 9.6xforward earnings, which is oneof lowest PEs among regionalindices globally. This may changewhen, and if, global investors regainconfidence in China's economy.

China Multiples Differ Widely, H.K. Lags

China Team For interactive exhibit on Bloomberg, run:Bloomberg Intelligence G BI3 1665<GO>

China, Asia-Pacific (BI CHINA)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2016 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Themes > Chapter: Growth and Value Consequences of China's Market Slump >> Exhibit 8 of 13

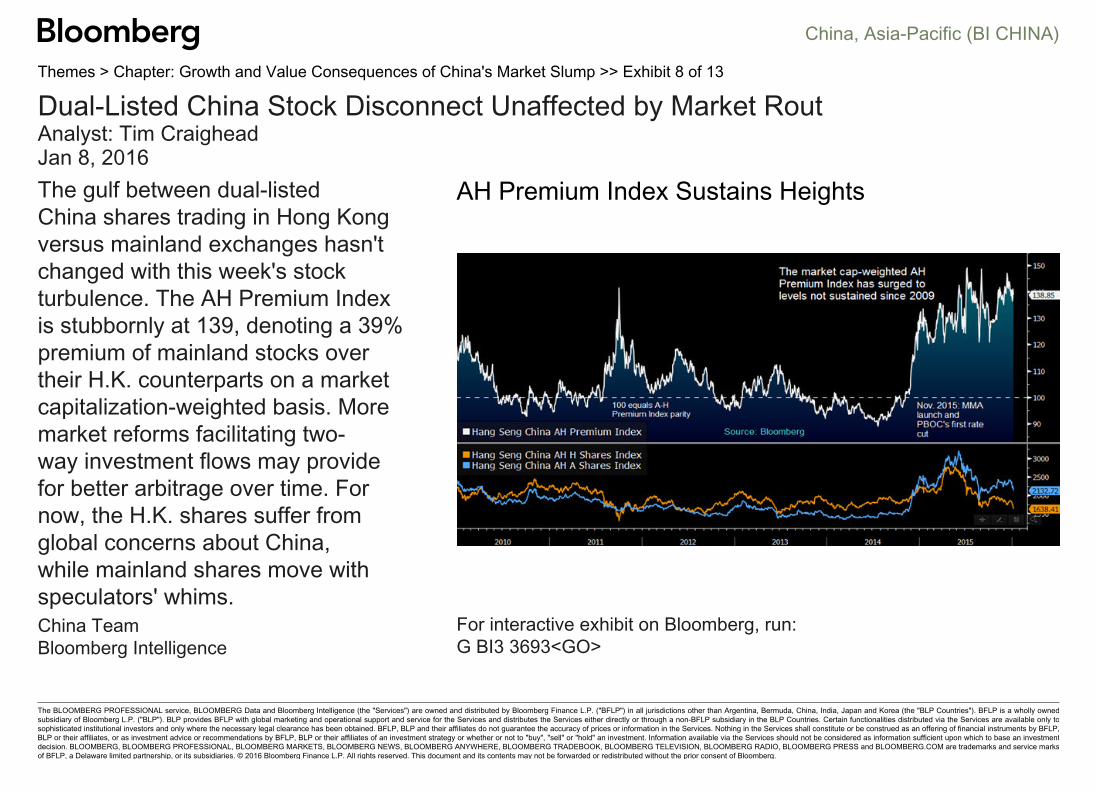

Dual-Listed China Stock Disconnect Unaffected by Market RoutAnalyst: Tim CraigheadJan 8, 2016The gulf between dual-listedChina shares trading in Hong Kongversus mainland exchanges hasn'tchanged with this week's stockturbulence. The AH Premium Indexis stubbornly at 139, denoting a 39%premium of mainland stocks overtheir H.K. counterparts on a marketcapitalization-weighted basis. Moremarket reforms facilitating two-way investment flows may providefor better arbitrage over time. Fornow, the H.K. shares suffer fromglobal concerns about China,while mainland shares move withspeculators' whims.

AH Premium Index Sustains Heights

China Team For interactive exhibit on Bloomberg, run:Bloomberg Intelligence G BI3 3693<GO>

China, Asia-Pacific (BI CHINA)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2016 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Themes > Chapter: Growth and Value Consequences of China's Market Slump >> Exhibit 9 of 13

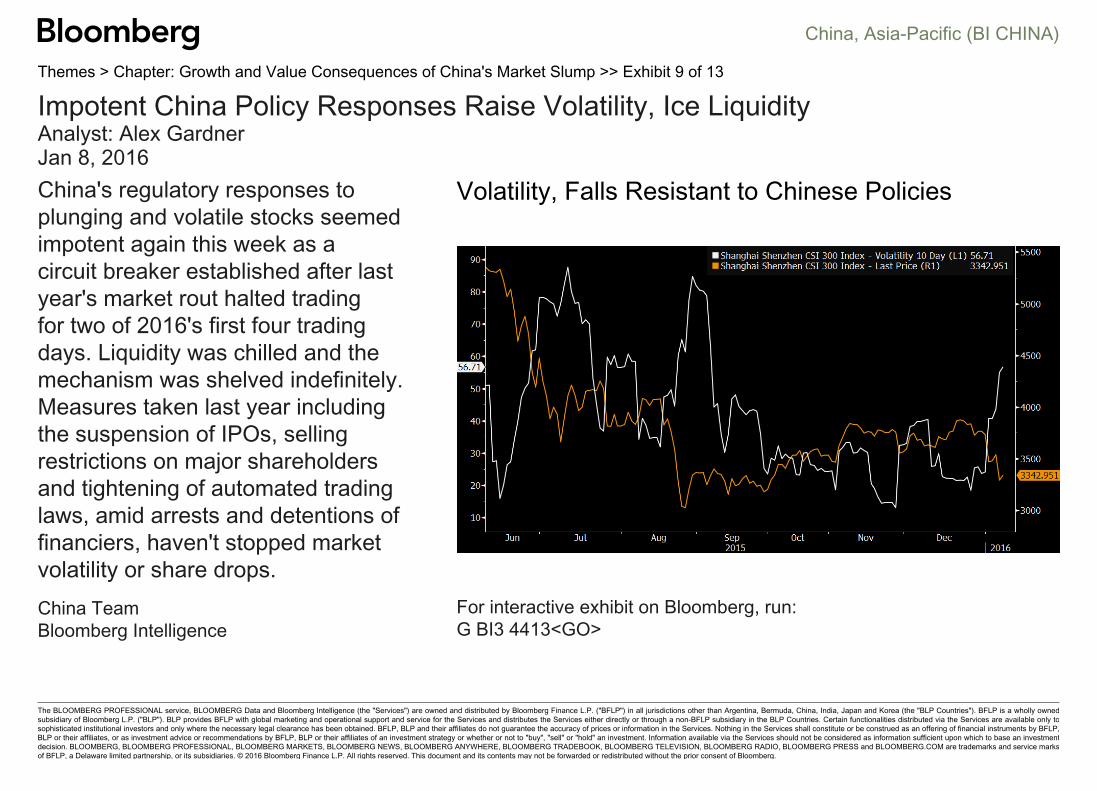

Impotent China Policy Responses Raise Volatility, Ice LiquidityAnalyst: Alex GardnerJan 8, 2016China's regulatory responses toplunging and volatile stocks seemedimpotent again this week as acircuit breaker established after lastyear's market rout halted tradingfor two of 2016's first four tradingdays. Liquidity was chilled and themechanism was shelved indefinitely.Measures taken last year includingthe suspension of IPOs, sellingrestrictions on major shareholdersand tightening of automated tradinglaws, amid arrests and detentions offinanciers, haven't stopped marketvolatility or share drops.

Volatility, Falls Resistant to Chinese Policies

China Team For interactive exhibit on Bloomberg, run:Bloomberg Intelligence G BI3 4413<GO>

China, Asia-Pacific (BI CHINA)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2016 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Themes > Chapter: Growth and Value Consequences of China's Market Slump >> Exhibit 10 of 13

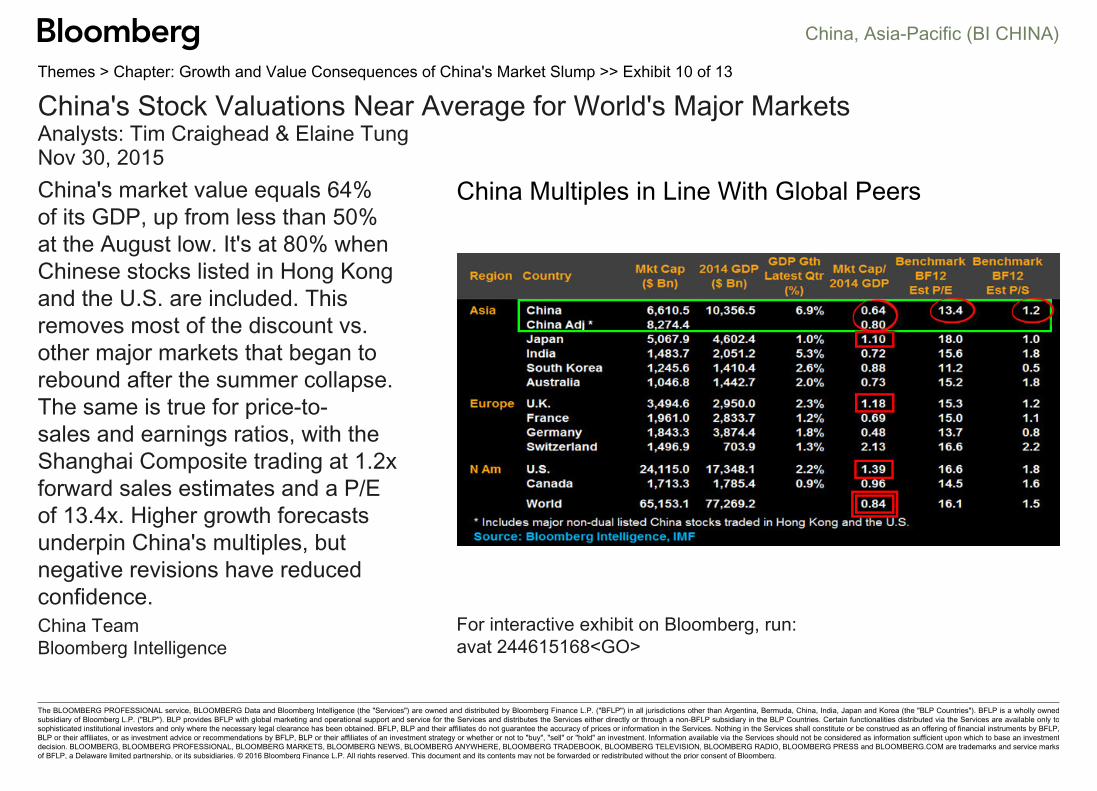

China's Stock Valuations Near Average for World's Major MarketsAnalysts: Tim Craighead & Elaine TungNov 30, 2015China's market value equals 64%of its GDP, up from less than 50%at the August low. It's at 80% whenChinese stocks listed in Hong Kongand the U.S. are included. Thisremoves most of the discount vs.other major markets that began torebound after the summer collapse.The same is true for price-to-sales and earnings ratios, with theShanghai Composite trading at 1.2xforward sales estimates and a P/Eof 13.4x. Higher growth forecastsunderpin China's multiples, butnegative revisions have reducedconfidence.

China Multiples in Line With Global Peers

China Team For interactive exhibit on Bloomberg, run:Bloomberg Intelligence avat 244615168<GO>

China, Asia-Pacific (BI CHINA)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2016 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Themes > Chapter: Growth and Value Consequences of China's Market Slump >> Exhibit 11 of 13

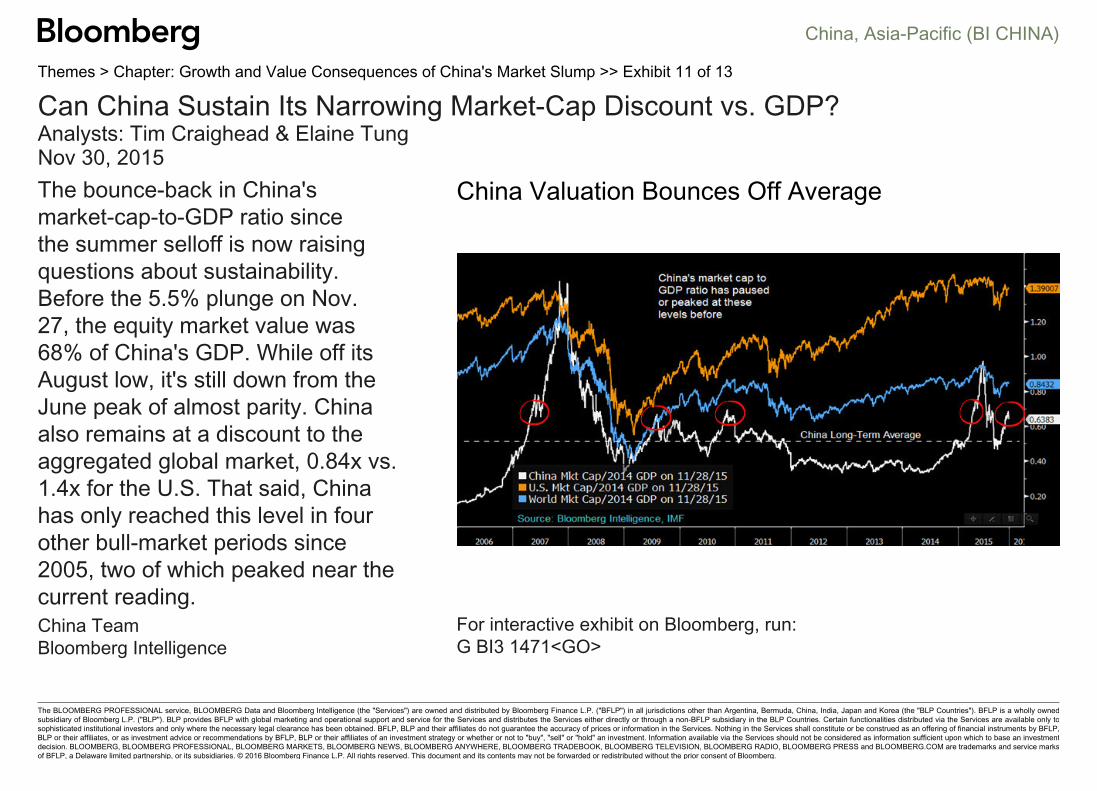

Can China Sustain Its Narrowing Market-Cap Discount vs. GDP?Analysts: Tim Craighead & Elaine TungNov 30, 2015The bounce-back in China'smarket-cap-to-GDP ratio sincethe summer selloff is now raisingquestions about sustainability.Before the 5.5% plunge on Nov.27, the equity market value was68% of China's GDP. While off itsAugust low, it's still down from theJune peak of almost parity. Chinaalso remains at a discount to theaggregated global market, 0.84x vs.1.4x for the U.S. That said, Chinahas only reached this level in fourother bull-market periods since2005, two of which peaked near thecurrent reading.

China Valuation Bounces Off Average

China Team For interactive exhibit on Bloomberg, run:Bloomberg Intelligence G BI3 1471<GO>

China, Asia-Pacific (BI CHINA)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2016 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Themes > Chapter: Growth and Value Consequences of China's Market Slump >> Exhibit 12 of 13

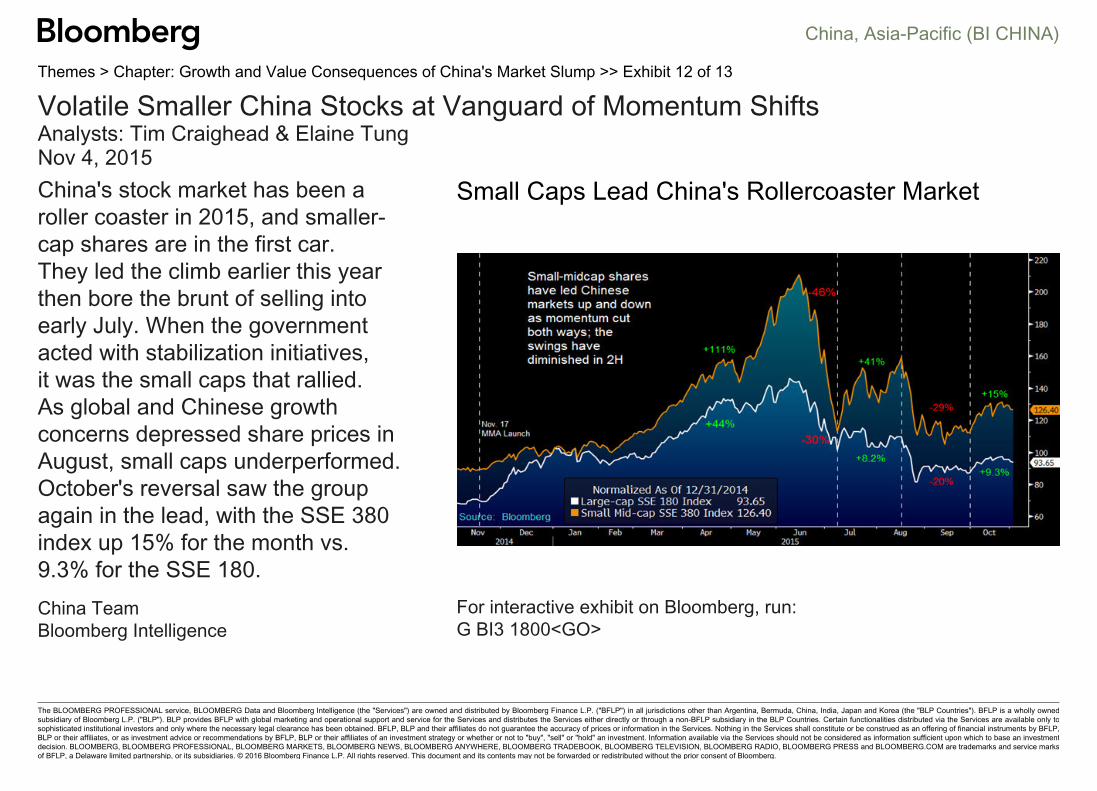

Volatile Smaller China Stocks at Vanguard of Momentum ShiftsAnalysts: Tim Craighead & Elaine TungNov 4, 2015China's stock market has been aroller coaster in 2015, and smaller-cap shares are in the first car.They led the climb earlier this yearthen bore the brunt of selling intoearly July. When the governmentacted with stabilization initiatives,it was the small caps that rallied.As global and Chinese growthconcerns depressed share prices inAugust, small caps underperformed.October's reversal saw the groupagain in the lead, with the SSE 380index up 15% for the month vs.9.3% for the SSE 180.

Small Caps Lead China's Rollercoaster Market

China Team For interactive exhibit on Bloomberg, run:Bloomberg Intelligence G BI3 1800<GO>

China, Asia-Pacific (BI CHINA)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2016 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Themes > Chapter: Growth and Value Consequences of China's Market Slump >> Exhibit 13 of 13

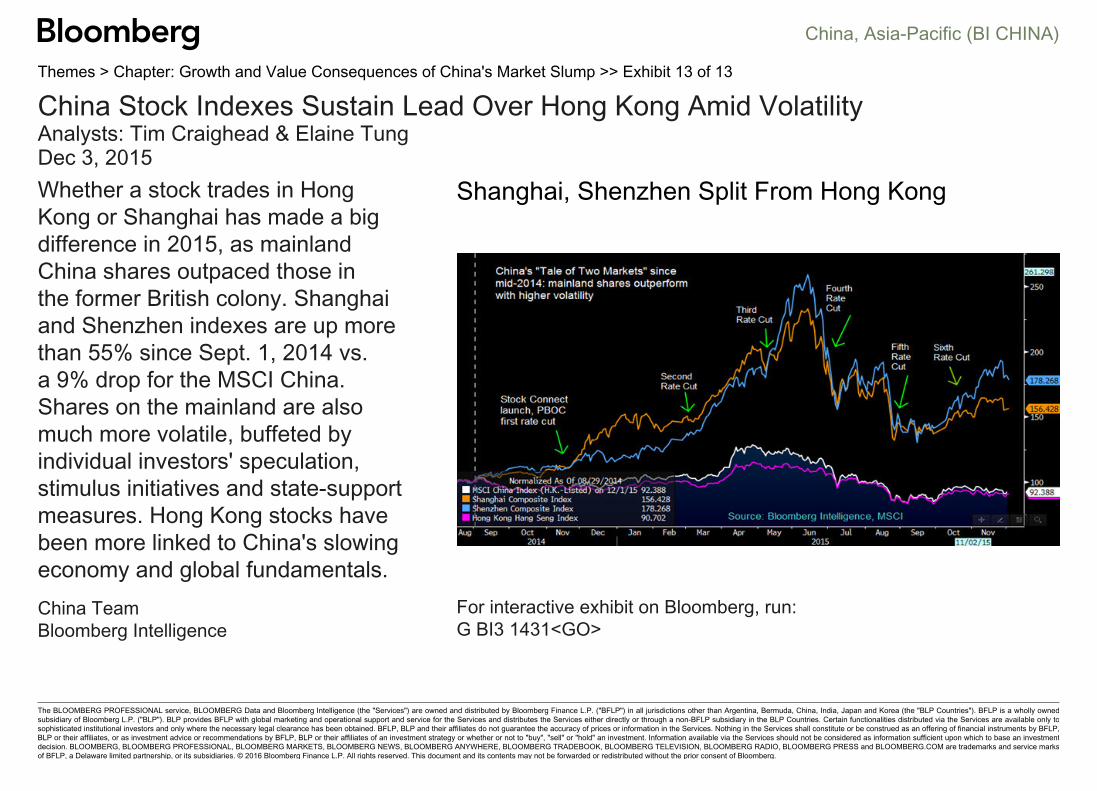

China Stock Indexes Sustain Lead Over Hong Kong Amid VolatilityAnalysts: Tim Craighead & Elaine TungDec 3, 2015Whether a stock trades in HongKong or Shanghai has made a bigdifference in 2015, as mainlandChina shares outpaced those inthe former British colony. Shanghaiand Shenzhen indexes are up morethan 55% since Sept. 1, 2014 vs.a 9% drop for the MSCI China.Shares on the mainland are alsomuch more volatile, buffeted byindividual investors' speculation,stimulus initiatives and state-supportmeasures. Hong Kong stocks havebeen more linked to China's slowingeconomy and global fundamentals.

Shanghai, Shenzhen Split From Hong Kong

China Team For interactive exhibit on Bloomberg, run:Bloomberg Intelligence G BI3 1431<GO>