the eu response to the crisis - circabc - welcome · outline 1. the origin of the crisis 2. the...

TRANSCRIPT

The EU response to the crisis

Riccardo DE BOSIO, European Commission, DG ECFIN

1 December 2016

The objective

A procedure to capture:

• "Macroeconomic"

• "Imbalances"

Therefore:

• How do you describe the state of the macroeconomy?

• How do you identify an imbalance?

2

Outline 1. The origin of the crisis

2. The EU's response to the crisis: enhanced economic governance

3. The (long) road to recovery

4. Macroeconomic Imbalances Procedure

5. Imbalances: where do we stand? (AMR 2017)

6. Conclusions and next steps

3

1. The origin of the crisis

4

Origin of the crisis: what went wrong?

2007 - Subprime crisis

2008 – Banking crisis

2009 – Economic crisis

2010 – Sovereign debt crisis

2011 – 2012 systemic crisis of the euro

Excess credit + prolonged upswing + expectations

Defaults cause bank losses, distrust rises

Credit crunch; high risk aversion hits trade & investment

Recession hits tax revenues; welfare spending rises; GDP denominator falls

Contagion spreads crisis through financial and economic links; speculation on exit & breakup

5

Stages of the crisis: from financial to economic to institutional crises

2007-2008: the financial crisis

What we missed: the signs • Abundant global liquidity, real estate

bubble (credit backed by the value of the collateral)

• Rapid credit growth, high leveraging

• Supervisory failures : supervision too focused on individual institutions, not the global picture

What was wrong • Originate and distribute model • Complex and opaque financial products

(CDOs…)

• Conflicts of interest of rating agencies • Incentives for short-run risk taking

(Compensation schemes…) • Maturity mismatches in banks’ balance

sheets

Domino effects and feedback loops when

bubbles pop

8

GDP in the face of crisis

-6

-4

-2

0

2

4

6

t-12 t-8 t-4 t = 0 t+4 t+8 t+12

% y

ear

on

yea

r g

row

th

113 historical crises (median)

US (current crisis)

EU (current crisis)

Note: y-o-y grow th rates during tw elve quarters before and after the beginning (0) of a

f inanical stress episode. T = 0 corresponds to 2007Q4. Dotted lines refer to forecasts.

Sources: IMF, OECD, European Commission.

2008-2009: the EU experienced the deepest slump since WWII…

….Or worse

Source: US bureau of Economic Analysis; European Commission (Autumn 2015)

0

20

40

60

80

100

120

0 1 2 3 4 5 6 7 8 9 10

GD

P,

Pre-c

ris

is=

10

0

Number of years since the start of the crisis

US, 1929-392 Greece, 2008-14

GDP in volume US vs Greece

Source: European Commission. 11

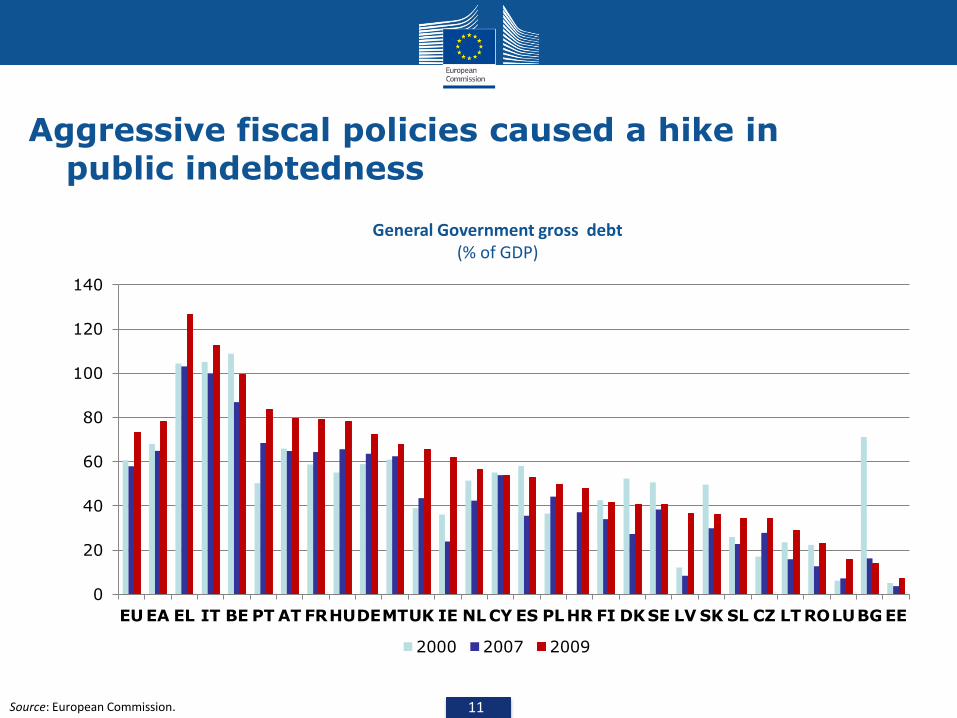

Aggressive fiscal policies caused a hike in public indebtedness

General Government gross debt (% of GDP)

0

20

40

60

80

100

120

140

EU EA EL IT BE PT AT FRHUDEMTUK IE NL CY ES PLHR FI DKSE LV SK SL CZ LT ROLUBG EE

2000 2007 2009

12

FINANCIAL

STABILITY

SOVEREIGN

DEBT

ECONOMIC

GROWTH

FINANCIAL

STABILITY

SOVEREIGN

DEBT

ECONOMIC

GROWTH

The negative feedback loop

Source: European Commission.

-150

-100

-50

0

50

100

150

200

PT ES EL EE IE SK SI IT AT

CY* FR FI

MT

NL

DE

BE*

LU*

2000 2008

2013

NIIP (% of GDP)

40

50

60

70

80

90

100

110

120

20

00

20

02

20

04

20

06

20

08

20

10

20

12

Ireland Spain Germany

Housing prices (2007=100)

(*) start in 2002

13

Meanwhile, unsustainable external positions and asset bubbles contributed to divergences in the EU

2. The EU's response to the crisis: enhanced economic governance

14

The original design of EMU was incomplete

Failure to adapt to requirements of EMU

Accumulation of unsustainable debt levels, both in public and private sector

Excessive risk-taking in the banking sector

Failing market discipline

EMU led Member States to delay necessary structural reforms

Inadequate governance framework

Insufficient monitoring and enforcement tools to safeguard fiscal discipline

No instruments available to address macroeconomic imbalances

No established sovereign-debt crisis resolution mechanism for euro-area Member States

No integrated European supervisory and regulatory architecture for financial institutions

15

Stabilisation thanks to a strong policy response

What has been done so far?

•Improved crisis management (ESM / EFSF)

•Better surveillance tools: o Stronger enforcement instruments o Extended surveillance beyond fiscal dimension o Enhanced coordination

•Banking Union

•Monetary policy (OMT, LTRO, UMP)

16

Crisis management was improved through the setup of stability funds

Non-euro area

- Balance of Payments Facility

Euro area

-Temporary: - European Financial Stabilisation Mechanism

- European Financial Stability Facility

- Permanent: - European Stability Mechanism

In case of use: macroeconomic adjustment programme and intensive monitoring by so-called Troika: COM, ECB, IMF (two pack)

17

ESM instruments: - loans under a macroeconomic adjustment programme - purchase of debt in the primary and secondary debt markets - credit lines - recapitalisations of financial institutions through loans - direct recapitalisation of banks

18

FINANCIAL

STABILITY

SOVEREIGN

DEBT

ECONOMIC

GROWTH

Improved

Governance

Structural reforms

Fiscal discipline

Differentiated fiscal consolidation & quality

of public finances

Bank funding

Bank recaps

Firewalls

FINANCIAL

STABILITY

SOVEREIGN

DEBT

ECONOMIC

GROWTH

Structural reforms

Fiscal Discipline

Enhanced rules

Differentiated fiscal consolidation & quality

of public finances

Bank funding

Bank recaps

Firewalls

Breaking the negative feedback loop

Fiscal compact

ESM

Strengthened economic governance in EMU

Prevention and

correction of macro

imbalances

New surveillance

procedure and

possible sanctions

Better enforcement of

rules

-Larger range of sanctions,

starting more gradual, quasi-

automaticity (RQMV)

-Strengthened national fiscal

frameworks

More effective

preventive arm of SGP

- Expenditure benchmark

- Draft Budget Plans

- Autonomous recommendations

Focus on debt

developments

Numerical benchmark in the

corrective arm of the SGP

Structural reforms

Europe 2020 strategy

Price stability ECB

- LTRO

- OMT

- Forward guidance

Crisis

Resolution EFSM/EFSF/ ESM

Financial Stability

Sound Fiscal Policy

Sustained Economic Growth

Banking Union •Based on a single rule book for the EU 28 •Single Supervisory Mechanism •Single Resolution Mechanism

19

Key pieces of the EU-wide Financial Reform

20

Making European banks more robust

December 2011: EBA bank recapitalisation exercise

Ensuring the medium-term funding of banks to avoid a

credit crunch

ECB support: two 3-year LTROs

EUR 489bn for 523 participating banks (21/12/2011)

EUR 529bn for 800 participating banks (29/02/2012)

Enhancing the quality and quantity of bank capital to

withstand shocks

Core Tier 1 ratio of 9% to be achieved by end-June

2012

November 2014: AQR and stress tests (comprehensive

assessment. 21

Key elements of the Banking Union

Single Rulebook for EU28 (CRD IV/CRR and BRRD)

Single Supervisory Mechanism

Effective supervision based on high

common standards

Single Resolution Mechanism Effective crisis

resolution, private sector funding

• November 2014 - the ECB becomes the supervisor of all major banks in the Euro Area (around 130) and the MS that 'opted-in'

• AQR and stress tests

• IGA Finally signed in May 2014

• January 2016 – the SRM becomes fully operational

Single Deposit Guarantee Scheme

Harmonised system for depositors

protection

• Final arrangement in 5 PR

22

Extraordinary measures by the ECB

"Securities Market Programme" (SMP)—from May 2010—limited sterilised interventions

Long-term repurchase operations (LTRO)—End 2011

OMT – 2012 - Secondary market purchase of government debt, Response to fears on the reversibility of the euro.

Stability and Growth Pact

• Each Member State required to stay within the limits of (defined in the TFEU):

o government deficit (3% of GDP) & debt (60% of GDP)

• Preventive Arm

o Submission of Annual Stability and Convergence Programmes

o Country-Specific Medium-Term Budgetary Objectives – MTO

• Corrective ('Dissuasive') Arm

o Excessive Deficit Procedure – EDP

o Sanctions

Two Arms to ensure fiscal discipline in the EMU

24

Six Pack, Two Pack & Fiscal Compact

• Preventive arm o Expenditure benchmark to prevent that spending rises faster than medium-term potential GDP

o Balanced Budget Rule - structural deficit must not exceed 0.5% of GDP (or 1.0% of GDP if debt significantly < 60% of GDP)

• Corrective arm

o Debt criterion became enforceable

→ EDP can be launched on deficit and debt criterion

→ 1/20th target - debt must decrease by 1/20th of GDP annually if > 60%

• Strengthened budgetary surveillance

o Draft budgetary plans submitted to the Commission

o Common budgetary timeline for an enhanced coordination

o Independent Fiscal Councils established in the Member States

• Strengthened enforcement o For MS in EDP the deposits and fines kick in earlier

o Reverse QMV for graduated financial sanctions

25

Lessons for economic governance •Scope and nature of surveillance

• Wider, especially on macro-financial issues and competitiveness/imbalances

• Deeper, especially on debt sustainability and key growth-enhancing reforms

• Better integrated, avoiding partial and fragmented approaches

•Follow-up and enforcement

• Stronger enforcement instruments

• Influence on economic policy debates at national level

• Taking account of Euro area dimension

Deepening EMU: 5 Presidents' report + Commission's Blueprint

Growth-enhancing reforms and EU 2020 Strategy

6

3. The (long) road to recovery

27

Policy response has led to a gradual stabilisation of financial markets

28

Financial sector repair – work in progress

0

5

10

15

20

25

EL SI BG CY IE HR

HU IT LT PT

LV CZ ES PL

BE

AT

FR DK SK EE NL

UK

DE

MT SE FI

June 2013

EA (June2013)

2008

Source: ECB consolidated banking data

Gross total doubtful and non-performing loans [% of total debt instruments and total loans and advances)

75

95

115

135

155

175

195

Jan

-04

Oct

-04

Jul-

05

Ap

r-0

6

Jan

-07

Oct

-07

Jul-

08

Ap

r-0

9

Jan

-10

Oct

-10

Jul-

11

Ap

r-1

2

Jan

-13

Oct

-13

EA

DE

IE

ES

IT

PT

Loan to deposit ratio

Source: ECB

Changes in euro area banks' aggregate CT1 ratios, 2011-2013 (% and pps)

Source: ECB, SNL Financial

29

Banking Union – work in progress Financial fragmentation & 'creditless' recovery

Source: Winter Forecast 2014

Interest rates on loans to enterprises (new business, maturity up to 1 year)

Economic and credit cycles, euro area (year-on-year %)

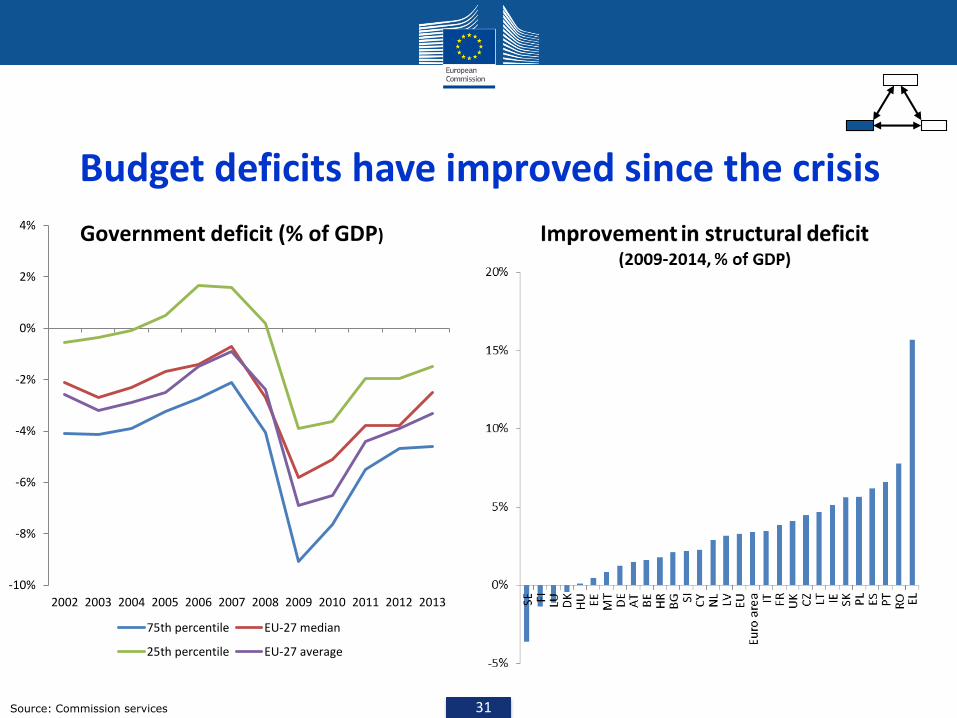

Budget deficits have improved since the crisis

Source: Commission services

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Government deficit (% of GDP)

75th percentile EU-27 median

25th percentile EU-27 average

31

Government debt is high across the EU and some countries need substantial further fiscal adjustment by 2020

32

-5,00

-3,00

-1,00

1,00

3,00

5,00

7,00

9,00

EE LV DK SE BG LT HU

RO SK DE PL

ES LU CZ

NL IT

MT

AT SI FI HR FR PT

UK IE BE

Autumn 2010

Spring 20140%

20%

40%

60%

80%

100%

120%

140%

160%

180%

EE BG LU LV RO SE LT CZ

DK PL

SK FI HR

MT

NL

DE

HU AT SI EU UK FR EA ES BE IE CY

PT IT EL

2009 2014-2009

S1 indicator: required fiscal adjustment by 2020 to reach a 60% debt-to-GDP ratio in 2030

Government debt (% of GDP)

33

Recovery takes hold, but fragile and uneven

Source: Autumn Forecast 2014

Real GDP, the whole of EU Real GDP, Selected countries 2008=100

60

70

80

90

100

110

120

130

140

BE DE IE EL ES

FR IT UK PT

0,5 2,1

1,8

-0,5

0,2 1,4

1,9 2,0

2,1

-3

-2

-1

0

1

2

3

80

85

90

95

100

105

110

Quarterly GDP growth GDP quarterly (index)

GDP annual (index) Column3

-4.4

What are the economic prospects for the upcoming five years?

34

o Signs of a turnaround in the euro area, including in vulnerable economies

o More weight of domestic demand in the core and external demand in the periphery

o But growth is still weak due, notably, to EA specific factors

96

98

100

102

104

106

108

0 1 2 3 4 5 6 7 8 9 10

previous recoveries

current recovery

index

quarters

Current recovery against past average* (GDP, euro area)

35 35

Case No 1: Full return to earlier path

Case No 2: Permanent loss in GDP level

Case No 3: Permanent loss on growth rates

Slope = long-term potential growth

No loss in potential output level after some

time

Potential output level

Same long-term potential growth after the crisis (same slope)

Potential output level

Years

Permanent loss in potential output level

Lower long-term output growth after the crisis (e.g. 1.5%)(lower post-crisis slope)

Potential growth before crisis (e.g. 2%)

Years

Potential output level

Potential output loss increasing

overtime

The medium- to long-run: possible trajectories for growth

36

4. MACROECONOMIC IMBALANCES PROCEDURE : Aiming to prevent the

next crisis

Crises illustrated gaps in economic

surveillance framework

Compliance with SGP does not guarantee overall

macro-financial stability

Large macroeconomic imbalances accumulated

ahead of the crisis that were not appropriately picked

up.

Unwinding of such imbalances contributed to

unprecedented depth of recession and weighed

heavily on public finances.

38

The macroeconomic imbalance procedure Context: Enhancing economic governance in the EU and the euro area, six-pack

Macroeconomic surveillance New regulation on prevention and correction of macroeconomic imbalances

Enforcement New regulation on effective enforcement of macroeconomic surveillance Sanctions in case of persistent inaction/insufficient action

Enforcement New regulation on effective

enforcement of budgetary surveillance

Stronger incentives & sanctions

Fiscal surveillance

- Prudent fiscal policy

- Debt criterion

- Minimum standards for fiscal frameworks

Autumn forecast

Winter forecast

Spring forecast

15 October

In-Depth Reviews

May/June

November

Annual Growth Survey

15 April

Stability/Convergence Programmes National Reform Programmes

Country-Specific Recommendations

Alert Mechanism Report

The European Surveillance Cycle

Governance architecture

Commission's opinions on Draft Budgetary Plans

Euro-area Member States: Draft Budgetary Plans

39

Challenge 1: complexity of the surveillance mechanisms

• A multiplicity of legal acts which is hard for experts to follow and emphasises process over substance

• The problem of the "complete contract": rules versus discretion

• Communication with stakeholders, especially at national level: ownership

40

Challenge 2: economic analysis in practice

• More difficult to identify problems earlier in the economic cycle, e.g. credit growth, house prices?

• Economic literature is not so conclusive on policy diagnosis and responses, especially in the aftermath of a balance-sheet crisis.

• Requires a lot of country specific knowledge. • Overall, it requires qualitative judgement to

complement quantitative analysis which is contestable.

41

Challenge 3: political economy accountability and ownership

• Respect the subsidiarity principle: when macroeconomic problems at the level of the Euro area require microeconomic actions at MS level.

• Democratic accountability and transparency at both EU and national level.

• The ins and the outs

42

The two arms of the MIP

• PREVENTIVE ARM: Ensure efficient and timely surveillance of macro imbalances where needed and bring the issues to the table. Integrated in European semester.

• CORRECTIVE ARM: Ensure efficient and timely policy action and correction when required. Follow-up by own time line.

a. Alert mechanism

report

Economic reading of the MIP

Scoreboard

November

Programme

countries

have their own

enhanced

surveillance

No risk

identified

Procedure stops

b. In-depth reviews

Commission prepares in-depth country

reviews (IDR), using a wide set of

indicators and analytical tools.

February/March

No problem

Procedure stops

Excessive

imbalances

Decision to

trigger (or not)

the corrective

arm

Imbalances

Recommendatio

ns under

European

Semester

May

The MIP procedure : a 2-step process to detect imbalances

Potential imbalance

The Corrective Arm

Member State is

placed in “Excessive Imbalance Position”

Corrective Action Plan

Surveillance of compliance with

reform commitments

Sufficient abeyance

Insufficient:

interest bearing deposit

Insufficient: Fine

0.1% of GDP

Insufficient fine 0.1% of

GDP

Reverse Qualified Majority Voting

Member State is

placed in an

Excessive Imbalance Position

Corrective Action Plan

Surveillance of compliance with

reform commitments

Sufficient abeyance

Insufficient: interest bearing deposit

Insufficient: Fine

0.1% of GDP

Fine 0.1% of GDP

a. The alert mechanism report and the

MIP scoreboard

Role and scope of the AMR

• Screening device to identify Member States for which in-depth review is warranted

• Programme countries are not assessed

• No policy conclusions or country-specific recommendations

• Based around an economic reading of a scoreboard of indicators

• Commission Report adopted by college

49

• Headline scoreboard: selected 14 indicators with indicative alert thresholds: alert thresholds based on historical data

• Scoreboard complemented by set of additional 28 "reading indicators" (including 9 of social character)

• Presented on t-1 annual statistics but the economic reading considers latest data available at any frequency

• Scoreboard may be adjusted over time (AGS 2015: promotion of some social indicators for AMR-2016)

MIP scoreboard: an analytical tool

50

It is:

• A first step (an initial filter) in the procedure

• An instrument of communication and accountability (COM needs to explain its decision taking into account the scoreboard)

• A set of indicators that helps identifying macroeconomic risks (but needs to be complemented by detailed analysis) ____________________________________________________

It is not:

• A tool for a mechanic decision on the existence of imbalances

• A tool to identify progress in reforms and developments in macro risks

What the scoreboard is and what is not

51

The scope of the scoreboard • External positions (current accounts, net international

investment positions)

• Competitiveness developments (REERs, ULCs)

• Export performance (export market shares)

• Private sector indebtedness (credit, debt)

• Public sector indebtedness

• Assets markets (housing)

• Financial sector developments (fin. Sector liabilities)

• Unemployment

• Activity rates

• Long-term unemployment

• Youth unemployment

Exte

rnal

imb

ala

nces

Inte

rnal

imb

ala

nces

Em

plo

ym

en

t

ind

icato

rs

52

Table 1.1: MIP Scoreboard 2015

Current

account

balance - % of

GDP

(3 year average)

Net

international

investment

position

(% of GDP)

Real effective

exchange rate -

42 trading

partners, HICP

deflator

(3 year % change)

Export market

share - % of

world exports

(5 year %

change)

Nominal unit

labour cost

index

(2010=100)

(3 year %

change)

House price

index

(2010=100),

deflated

(1 year %

change)

Private sector

credit flow,

consolidated

(% of GDP)

Private sector

debt,

consolidated

(% of GDP)

General

government

gross debt

(% of GDP)

Unemployment

rate

(3 year average)

Total financial

sector

liabilities,

non-

consolidated

(1 year %

change)

Activity rate - %

of total

population aged

15-64

(3 year change in

pp)

Long-term

unemployment

rate - % of active

population aged

15-74

(3 year change in

pp)

Youth

unemployment

rate - % of active

population aged

15-24

(3 year change in

pp)

Thresholds -4/6% -35%±5% (EA)

±11% (Non-EA)-6%

9% (EA)

12% (Non-EA)6% 14% 133% 60% 10% 16.5% -0.2 pp 0.5 pp 2 pp

BE -0.2 61.3 -1.2 -11.3 1.5 1.3p 4.5 166.3 105.8 8.5 -1.0 0.7 1.0 2.3

BG 0.6 -60.0 -4.1 12.8 14.9p 1.6bp -0.3 110.5 26.0 11.2 7.0 2.2 -1.2 -6.5

CZ 0.2 -30.7 -8.0 0.1 0.5 3.9p 0.9 68.6 40.3 6.1 7.7 2.4 -0.6 -6.9

DK 8.8 39.0 -1.5 -8.8 4.9 6.3 -3.3 212.8 40.4 6.6 -2.0 -0.1 -0.4 -3.3

DE 7.5 48.7 -1.4 -2.8 5.7 4.1 3.0 98.9 71.2 4.9 2.8 0.4 -0.4 -0.8

EE 0.9 -40.9 6.4 8.5 14.4 6.8 3.3 116.6 10.1 7.4 8.1 1.9 -3.1 -7.8

IE 4.7* -208.0* -5.9 38.3* -18.1 8.3 -6.7 303.4 78.6 11.3 9.5 0.8 -3.7 -9.5

EL -1.2 -134.6 -5.5 -20.6 -11.1p -3.5e -3.1 126.4 177.4 26.3 15.7 0.3 3.7 -5.5

ES 1.3 -89.9 -2.9 -3.5 -0.7p 3.8 -2.7 154.0 99.8 24.2 -2.1 0.0 0.4 -4.6

FR -0.7 -16.4 -2.7 -5.4 2.5p -1.3 4.4 144.3 96.2 10.3 1.8 0.8 0.6 0.3

HR 2.7 -77.7 0.1 -3.5 -5.0 -2.4 -1.3 115.0 86.7 17.0 2.1 2.9 0.1 0.9

IT 1.5 -23.6 -2.2 -8.9 1.5 -2.6p -1.7 117.0 132.3 12.2 1.7 0.5 1.3 5.0

CY -4.1 -130.3 -6.2 -16.8 -10.5p 2.9bp 4.4 353.7 107.5 15.7 2.8 0.4 3.2 5.1

LV -1.8 -62.5 3.1 10.5 16.0 -2.7 0.7 88.8 36.3 10.9 12.2 1.3 -3.3 -12.2

LT 0.9 -44.7 4.0 15.5 11.6 4.6 2.2 55.0 42.7 10.5 6.7 2.3 -2.7 -10.4

LU 5.3 35.8 -0.5 22.9 0.6 6.1 24.2 343.1 22.1 6.1 15.5 1.5b 0.3 -1.4

HU 3.0 -60.8 -6.9 -8.0 3.9 11.6 -3.1 83.9 74.7 8.2 0.4 4.9 -1.9 -10.9

MT 4.3 48.5 -0.2 -8.8 3.9 2.8p 5.4 139.1 64.0 5.9 1.3 4.5 -0.7 -2.3

NL 9.1 63.9 -0.6 -8.3 0.2p 3.6 -1.6p 228.8p 65.1 7.2 3.2p 0.6 1.1 -0.4

AT 2.1 2.9 1.8 -9.6 6.1 3.5 2.1 126.4 85.5 5.6 0.6 0.4 0.5 1.2

PL -1.3 -62.8 -1.0 9.7 -0.4p 2.8 3.2 79.0 51.1 8.9 2.4 1.6 -1.1 -5.7

PT 0.7 -109.3 -2.8 2.8 0.0e 2.3 -2.3 181.5 129.0 14.4 -1.6 0.0 -0.5 -6.0

RO -1.0 -51.9 2.7 21.1 0.5p 1.7 0.2 59.1 37.9 6.9 4.1 1.3 0.0 -0.9

SI 5.4 -38.7 0.6 -3.6 -0.6 1.5 -5.1 87.3 83.1 9.6 -3.4 1.4 0.4 -4.3

SK 1.1 -61.0 -0.7 6.7 2.2 5.5 8.2 81.4 52.5 13.0 4.5 1.5 -1.8 -7.5

FI -1.0 0.6 2.3 -20.5 3.6 -0.4 9.5 155.7 63.6 8.8 1.5 0.6 0.7 3.4

SE 5.0 4.1 -7.9 -9.3 3.6 12.0 6.5 188.6 43.9 7.8 2.3 1.4 0.0 -3.3

UK -4.8 -14.4 11.3 1.0 1.7 5.7 2.5 157.8 89.1 6.3 -7.8 0.8 -1.1 -6.6

Year

2015

External imbalances and competitiveness Internal imbalances Employment indicators¹

Flags: b: break in time series. e: estimated. p: provisional.

Note: * The level shift is due to relocation to Ireland of balance sheets of large multi-national enterprises and inclusion of corresponding transactions in the Irish BoP and IIP statistics. 1) See page 2 of the AM R 2016. 2) House price index e = source NCB of EL. 3) The level of TFSL in Greece is higher than would

otherwise have been recorded, due to the improved treatment o f banks' ho ldings of short-term debt securities issued by banks.

Source: European Commission, Eurostat and Directorate General for Economic and Financial Affairs (for Real Effective Exchange Rate), and International M onetary Fund

53

Table 2.1: Auxiliary indicators, 2015

Year

2015

Real G

DP

(1 y

ear

% c

hange)

Gro

ss f

ixed

cap

ital

form

ati

on

(%

of G

DP

)

Gro

ss d

om

esti

c

exp

en

dit

ure

on

R&

D (

% o

f

GD

P)

Cu

rren

t p

lus c

ap

ital

acco

un

t (N

et

len

din

g-

bo

rro

win

g)

(% o

f G

DP

)

Net

exte

rnal d

eb

t

(% o

f G

DP

)

Fo

reig

n d

irect

investm

en

t in

th

e

rep

ort

ing

eco

no

my -

flo

ws

Fo

reig

n d

irect

investm

en

t in

th

e

rep

ort

ing

eco

no

my -

sto

cks

Net

trad

e b

ala

nce o

f

en

erg

y p

rod

ucts

(% o

f G

DP

)

Real eff

ecti

ve e

xch

an

ge

rate

- E

uro

Are

a t

rad

ing

part

ners

(3 y

ears

% c

hange)

Exp

ort

perf

orm

an

ce

ag

ain

st

ad

van

ced

eco

no

mie

s

(5 y

ears

% c

hange)

Term

s o

f tr

ad

e

(5 y

ears

% c

hange)

Exp

ort

mark

et

sh

are

in

vo

lum

e

(1 y

ear

% c

hange)

Lab

ou

r p

rod

ucti

vit

y

(1 y

ear

% c

hange)

No

min

al u

nit

lab

ou

r co

st

ind

ex (

2010=100)

(10 y

ears

% c

hange)

Un

it lab

ou

r co

st

perf

orm

an

ce r

ela

tive t

o

EA

(10 y

ears

% c

hange)

Ho

use p

rice in

dex

(2010=100)

- n

om

inal

(3 y

ears

% c

hange)

Resid

en

tial co

nstr

ucti

on

(% o

f G

DP

)

Pri

vate

secto

r d

eb

t,

no

n-c

on

so

lid

ate

d

(% o

f G

DP

)

Fin

an

cia

l secto

r le

vera

ge,

no

n-c

on

so

lid

ate

d

(% d

ebt-

to-e

quity

)

BE 1.5 23.0 na 0.5 -67.7 -4.7 213.6 -2.8 0.2 -9.4 0.1 1.6 0.6 20.5 4.0 2.30p 5.8 218.8 176.5

BG 3.6 21.0 1.0p 3.5 3.4 3.7 88.9 -3.8 -3.9 15.2 3.5 3.0 3.3p 78.4p 51.2 2.00bp 1.4 121.5 494.3

CZ 4.5 26.3 na 3.2 -9.8 1.3 74.2 -2.5 -8.0 2.3 0.7 5.0 3.1 14.1 -2.8 6.60p 3.4 77.0 516.4

DK 1.0 19.0 na 9.0 3.6 0.7 49.8 0.1 -1.3 -6.8 0.7 -2.4 -0.1 26.0 7.4 15.3 4.0 218.9 159.9

DE 1.7 19.9 2.9ep 8.4 -10.2 1.4 41.0 -2.0 0.5 -0.7 2.0 2.5 0.8 15.1 -1.6 11.4 5.9 106.1 368.0

EE 1.4 23.7 1.5p 4.3 -10.3 -2.9 99.9 -1.4 1.6 10.8 2.8 -3.3 -1.4 72.0 42.1 34.5 4.4 130.9 366.1

IE 26.3 21.2 na 9.7* -289.0* 72.3* 495.9* -1.6 -1.3 41.2* 3.6 31.7 23.2 -14.9 -22.7 30.7 1.9 323.6 80.6

EL -0.2p 11.5p 1.0p 1.2 138.1 0.6 14.5 -2.2p -5.2 -18.9 5.8p 0.7p -0.7p -0.2p -12.6 -21.70e 0.7p 126.4 1359.6

ES 3.2p 19.7p na 2.0 93.1 2.1 59.8 -2.1p -1.3 -1.5 -4.7p 2.2p 0.7p 8.9p -6.2 -5.6 4.4p 173.1 468.4

FR 1.3p 21.5p na -0.1 37.3 1.5 43.3 -1.8p -0.4 -3.4 2.1p 3.4p 0.8p 17.9p 1.9 -4.9 5.8p 183.3 356.6

HR 1.6 19.5 0.85 5.6 52.7 0.4 55.0 -3.5 -1.1 -1.5 0.6 7.3 0.1 23.3 -4.1 -8.2 na 140.2 427.0

IT 0.7 16.6 na 1.8 59.7 0.7 25.6 -2.0 -0.5 -7.0 2.1 1.6 0.2 17.6 3.0 -12.20p 4.4 120.1 657.3

CY 1.7p 13.3p na -2.6 133.4 41.0 911.2 -4.2p -2.4 -15.0 -0.8p -2.7 0.9p 5.4p -4.1 -4.60bp 4.3p 354.9 85.0

LV 2.7 22.6 0.6p 2.0 28.6 2.8 60.1 -2.9 -2.0 12.8 0.2 -0.1 1.4 71.7 39.1 9.5 1.8 97.6 625.4

LT 1.8 19.3 1.0p 0.7 26.4 2.3 40.0 -3.5 -1.4 17.9 2.2 -3.1 0.5 35.3 10.0 11.7 2.8 57.5 467.9

LU 3.5 19.0 na 4.1 -2220.9 766.4 8616.9 -3.1 0.3 25.5 0.0 10.1 0.9 29.8 11.1 15.5 3.9 425.1 53.9

HU 3.1 21.7 1.38 7.8 23.0 -2.2 222.1 -4.2 -7.1 -6.0 -0.2 5.0 0.5 24.4 8.8 13.0 1.9 99.1 114.1

MT 6.2 25.4 0.8p 4.9 -262.7 25.8 1867.3 -9.8 1.0 -6.8 0.8 -0.6 2.7 29.8 10.7 6.20p 3.4 204.7 37.1

NL 2.0p 19.4p na 3.6 40.0 13.4 580.5 -1.0p 1.0 -6.4 -0.9p 2.3p 1.0p 15.3p 1.5 -1.9 3.7p 236.3p 129.7p

AT 1.0 22.6 3.1ep 1.4 20.1 1.1 80.9 -2.3 2.3 -7.7 -0.2 0.9 0.3 23.3 5.7 14.2 4.3 145.1 186.7

PL 3.9 20.1 1.01 1.7 35.7 3.0 48.6 -1.6 -1.9 12.1 2.8 5.0 2.5p 17.0p 2.5 -2.0 3.1 83.4 305.9

PT 1.6e 15.3e na 1.7 100.8 0.3 71.7 -2.3e -1.0 5.0 4.8e 3.4e 0.2e 0.6e -12.4 5.4 2.5e 195.9 372.0

RO 3.7p 24.7p na 1.2 24.5 2.4 42.6 -0.9p 2.4 23.7 6.1p 2.8p 4.6p 43.9p 23.6 0.5 na 61.2 391.5

SI 2.3 19.5 na 6.1 31.2 3.9 34.5 -2.9 -0.7 -1.5 0.7 2.9 1.2 19.9 1.1 -10.8 2.3 96.0 402.6

SK 3.8 23.0 1.18 3.8 27.3 1.3 60.5 -3.5 -1.2 8.9 -3.2 4.3 1.8 16.1 -1.2 7.8 2.3 83.7 831.7

FI 0.2 20.4 2.9p -0.3 43.9 7.3 58.0 -1.5 1.1 -18.8 2.7 -2.9 0.6 28.1 8.8 0.8 5.5 182.8 299.4

SE 4.1 23.7 na 5.0 46.3 3.4 78.0 -0.9 -7.8 -7.4 0.6 2.9 2.6 25.1 6.8 30.5 4.5 234.9 184.5

UK 2.2 16.9 na -5.4 na 1.8 74.3 -0.6 14.0 3.1 3.5 1.8 0.5 21.9 3.6 17.4 3.7 161.1 628.3

Flags: b: break in time series. e: estimated. p: provisional. na: not available.

Note: * The level shift is due to relocation to Ireland of balance sheets of large multi-national enterprises and inclusion of corresponding transactions in the Irish BoP and IIP statistics. 1) House price index e = source NCB for EL. 2) Official transmission deadline for 2015 data on Gross domestic

expenditure on R&D is 31 October 2016; data as transmitted to Eurostat by the 24 October 2016 were used for this document.

Source: Eurostat, Directorate General for Economic and Financial Affairs (for Real Effective Exchange Rate) and International M onetary Fund data, WEO (for world exports series)

54

Table 2.1 (continued): Auxiliary indicators, 2015

%3 years

change in p.p%

3 years

change in p.p%

3 years

change in p.p%

3 years

change in p.p%

3 years

change in p.p

BE 0.9 67.6 4.4 22.1 12.2 -0.1 21.1 -0.5 14.9 -0.4 5.8p -0.5p 14.9 1.0

BG 0.4p 69.3 5.6 21.6 19.3 -2.2 41.3 -8.0 22.0 0.8 34.2 -9.9 11.6 -0.9

CZ 1.4 74.0 2.4 12.6 7.5 -1.4 14.0 -1.4 9.7 0.1 5.6 -1.0 6.8 0.0

DK 1.1 78.5 1.7 10.8 6.2 -0.4 17.7 0.2 12.2 0.2 3.7 1.0 11.6 1.4

DE 0.9 77.6 2.0 7.2 6.2 -0.9 20.0 0.4 16.7 0.6 4.4 -0.5 9.8 -0.1

EE 2.9 76.7 2.4 13.1 10.8 -1.4 24.2 0.8 21.6 4.1 4.5 -4.9 6.6 -2.5

IE 2.5 70.0 5.3 20.9 14.3 -4.4 na na na na na na na na

EL 0.5p 67.8 18.2 49.8 17.2 -3.0 35.7 1.1 21.4 -1.7 22.2p 2.7p 16.8 2.6

ES 2.5p 74.3 11.4 48.3 15.6 -3.0 28.6 1.4 22.1 1.3 6.4p 0.6p 15.4 1.1

FR 0.5p 71.5 4.3 24.7 12.0 -0.5 17.7 -1.4 13.6 -0.5 4.5 -0.8 8.6 0.2

HR 1.5 66.8 10.3 43.0 18.5 1.9 29.1 -3.5 20.0 -0.4 13.7 -2.2 14.4 -2.3

IT 0.6 64.0 6.9 40.3 21.4 0.4 28.7 -1.2 19.9 0.4 11.5 -3.0 11.7 1.1

CY 0.8p 73.9 6.8 32.8 15.3 -0.7 28.9 1.8 16.2 1.5 15.4 0.4 10.9 4.4

LV 1.3 75.7 4.5 16.3 10.5 -4.4 30.9 -5.3 22.5 3.3 16.4 -9.2 7.8 -3.9

LT 1.3 74.1 3.9 16.3 9.2 -2.0 29.3 -3.2 22.2 3.6 13.9 -5.9 9.2 -2.2

LU 2.6 70.9b 1.9 16.6 6.2b 0.3b 18.5 0.1 15.3 0.2 2.0 0.7 5.7 -0.4

HU 2.6 68.6 3.1 17.3 11.6b -3.2b 28.2 -5.3 14.9 0.6 19.4 -6.9 9.4 -4.1

MT 3.4 67.6 2.4 11.8 10.4 -0.2 22.4 -0.7 16.3 1.2 8.1 -1.1 9.2 0.2

NL 0.9p 79.6 3.0 11.3 4.7 -0.2 16.8p 1.8p 12.1p 2.0p 2.5p 0.2p 10.2 1.3

AT 0.6 75.5 1.7 10.6 7.5 0.7 18.3 -0.2 13.9 -0.5 3.6 -0.4 8.2 0.5

PL 1.4p 68.1 3.0 20.8 11.0 -0.8 23.4 -3.3 17.6 0.5 8.1 -5.4 6.9 0.0

PT 1.4e 73.4 7.2 32.0 11.3 -2.6 26.6 1.3 19.5 1.6 9.6p 1.0p 10.9 0.8

RO -0.9p 66.1 3.0 21.7 18.1 1.3 37.3 -5.9 25.4 2.5 22.7 -8.4 7.9 0.0

SI 1.1 71.8 4.7 16.3 9.5 0.2 19.2 -0.4 14.3 0.8 5.8 -0.8 7.4 -0.1

SK 2.0 70.9 7.6 26.5 13.7 -0.1 18.4 -2.1 12.3 -0.9 9.0 -1.5 7.1 -0.1

FI -0.4 75.8 2.3 22.4 10.6 2.0 16.8 -0.4 12.4 -0.8 2.2p -0.7p 10.8 1.5

SE 1.5 81.7 1.5 20.4 6.7 -1.1 16.0 0.4 14.5 0.4 0.7 -0.6 5.8 0.1

UK 1.8 76.9 1.6 14.6 11.1 -2.8 23.5 -0.6 16.7 0.7 6.1 -1.7 11.9 -1.1

Flags: b: break in time series. e: estimated. p: provisional. na: not available.

Note: 1) IE: Official transmission deadline for 2015 data on People at risk of poverty or social exclusion is 30 November 2016, while data were extracted on 24 October 2016.

Source: European Commission, Eurostat

Year

2015

Employment

rate

(1 year %

change)

Activity rate - %

of total

population

aged 15-64

(%)

Long-term

unemployment

rate - % of

active

population

aged 15-74

(%)

Youth

unemployment

rate - % of

active

population

aged 15-24

(%)

Young people neither in

employment nor in

education and training -

% of total population

aged 15-24

People at risk of poverty

or social exclusion -

% of total population

People at risk of poverty

after social transfers -

% of total population

Severely materially

deprived people -

% of total population

People living in

households with very

low work intensity -

% of total population

aged 0-59

55

Evolution of the total number of flashes per Member State, AMRs from 2012 until 2016, all EU countries except for Greece

Source: DG ECFIN (based on EUROSTAT data).

The indicators are lagged 2 years, hence the AMR at year t uses scoreboard data up to year t-2.

The number of flashes is calculated based on the latest available data (July 2015).

0

1

2

3

4

5

6

7

8

Nu

mb

er

of

fla

she

s

2012 2013 2014 2015 2016

Evolution of number of Scoreboard "flashes" not showing a clear general trend

56

Evolution of flashes per scoreboard indicator, AMRs from 2012 until 2016, all EU countries except Greece

Source: DG ECFIN (based on EUROSTAT data).

The indicators are one year lagged, hence the AMR at year t uses scoreboard data from t-1.

The number of flashes is calculated based on the latest available data (July 2015).

0

5

10

15

20Cu

rren

t Acc

ount

NIIP

REER

Expo

rt m

arke

tsh

ares

ULC

Hou

se p

rices

Priv

ate

cred

it

Priv

ate

debt

Publ

ic D

ebt

Une

mpl

oym

ent R

ate

Fina

ncia

l Ser

vice

Liab

ilitie

s

Num

ber o

f fla

shes

2012 2013 2014 2015 2016

SB flashes linked to stock imbalances remain persistent

57

0

1

2

3

4

5

6

7

8

Num

ber o

f fla

shes

for e

ach

coun

try

No imbalances Imbalances Excessive Imbalances

Number of flashes for each country, by MIP imbalance category, 2012-2016

Results of the AMR 2017

• The 13 countries for which imbalances were identified in 2016 (FR, HR, BG, CY, IT, PT, SI, IE, ES, DE, NL, FI, SE)

• Six countries have been identified with excessive imbalances, and seven countries have been identified with imbalances.

• Programme countries are not under MIP surveillance.

• As was previously the case for Member States expected to exit their financial assistance programme, the situation of Greece will be assessed in the context of the MIP only after the on-going financial assistance programme.

b. In-depth reviews

IDRs in general

• Broad assessment of imbalances complemented with focused

analysis (building on AMR)

• Common framework but assessments are by nature country

specific drawing on common and national sources as well as on

relevant empirical evidence.

• Fact finding missions to Member States (ECFIN, other services,

ECB (EA), ESO)

• Use of widely available and transparent data, analytical tools and

descriptive statistics

• Methodological work progress in tandem (LIME, surplus study,

deleveraging report)

Broad structure of IDRs

• Executive summary and conclusions

• Macroeconomic developments

• Analysis of the nature and causes of imbalances

• Focused sections on key issues

• Policy challenges

62

Spillovers

• Trade linkages

• Financial linkages

EIP

Adjustment capacity

• Price and wage flexibility

• Labour market flexibility

• Financial market intermediation

• Balance sheet adjustment

Policy options and

implementation

• Wage bargaining system

• Financial market regulation

• Fiscal policy

• Growth and structural reforms

Sustainability of macro-trends

• Early warning

• Deviation from equilibrium (competitiveness, credit growth, housing prices)

• Other factors (GDP growth, demography, catching-up,

global imbalances, saving and investment imbalances,

housing and other asset markets, shocks)

• Policy determinants (fiscal policy, financial regulation, labour market institutions)

Identification

of

problematic

imbalances

Policy

Response

63

What is an imbalance? (no numerical benchmark)

• Nature of MIP

• Medium term horizon

• Pre-emptive

• Approach

• Snapshot

• Dynamics

• Reform implementation

• Objective

• Risk assessment and impact

Challenges vary significantly across

Member States

Large stocks of net liabilities concerning a wide range of sectors, both external and internal:

PT, ES, CY, EL, IE, SI, HU, HR, BG

Large and persistent current account surpluses:

DE, NL

Combination of high public debt and declining trend in potential growth or competitiveness:

IT, FR, BE

Vulnerabilities confined to a particular sector:

NL, SE, UK, AT, EE, FI

Large negative NIIP:

RO

65

Analytical tools

• External positions (CACA, CA benchmarks, NIIP stabilising CA)

• Trade performance and competitiveness (allocative

efficiency, access to finance, productivity and export performance)

• Wages and productivity (wage benchmarks)

• Deleveraging pressures

• House price cycle assessment (equilibrium, overvaluations)

• QUEST simulations (impact structural reforms)

66 0% 10% 20% 30% 40% 50% 60%

labour markets

other

financial sector

housing market

external sustainability

public indebtedness

private indebtedness

external competittiveness

average (2012-2014)

% of countries with identified imbalance in the MIP

Source: Commission services; other includes: imbalances stemming from weak domestic demand, weak corporate governance and high level of state involvement in the economy

The MIP identifies competitiveness and indebtedness as the most prevalent imbalances

66

67

Number of CSRs in 2013 and 2014, by policy area

Source: Commission services

CSRs addresses the major reform priorities

Macro imbalances & structural reforms

67

0 5 10 15 20 25 30

Fiscal Consolidation

Long-term sustainability

Taxation

Banking

Housing

Access to finance

ALMP & participation

Wage setting

Education

Social polices

Health care

Childcare

Innov. & competitiveness

Competition

Energy, networks

Public administration

Pu

blic

fin

ance

Fin

anci

al s

ecto

r

Lab

ou

rm

arke

tre

form

sH

um

an c

apit

al a

nd

soci

al p

olic

ies

Pro

du

ct m

arke

tre

form

s.

2013

2014

68

Average number of CSRs per policy area (average 2013,2014 and 2015)

Source: Commission services

In general, countries under MIP surveillance received a higher number of CSRs

Macro imbalances & structural reforms

68

0

0.2

0.4

0.6

0.8

1

1.2

Public finances andtaxation

Financial sector Labour market Social inclusion andeducation

Structural policies Publicadministration and

businessenvironment

MIP countries Non-MIP countries

69

CSR progress indicator for MIP versus non-MIP countries (aritmetic average)

Source: Commission services

And evidence indicates that compliance with CSRs was stronger in MIP countries

Macro imbalances & structural reforms

69

33

34

35

36

37

38

39

40

41

2014 2015

MIP average

Non-MIP average

Specific monitoring

• The corrective arm was not initiated either in 2013 or 2014 despite finding of excessive imbalance

• This is formally in line with legislation ("may")

• EA CSR asks for "specific monitoring" of implementation of reform commitments for countries with excessive imbalances and EA countries with imbalances requiring decisive action.

• Was done for ES and SI (first time) and HR, IT, SI and FR, IE, ES

• COM can at any moment initiate corrective arm

71

5. Imbalances: where do we stand (AMR 2017) ?

72

Macroeconomic context

• Continuing but fragile recovery

• Subdued growth, feeble domestic demand dynamics

• Historically low inflation

• Improving labour market conditions, but social distress

persists

• Tail winds are fading …

• … while uncertainties remain high: (1) geopolitical tensions; (2)

impact of normalisation of US monetary policy; (3) risks to the policy

environment amid rising populism and growing protectionist

sentiment around the world

73

Number of scoreboard flashes, 2013-2015

The same risks and challenges as in the previous year are broadly

confirmed

74

Asymmetric adjustment of CA balances persists

• Adjustment in net debtor countries has broadly run its course

• Some net creditor countries continue to run large, and in some

cases rising, current account surplus

Change in current account balances, net debtor countries

Change in current account balances, net creditor countries

75

EA rebalancing progress still needed, in a low-

inflation environment

• EA current account surplus expected to reach 3.7% of GDP in 2016

• Large surplus underpins the low growth and low inflation

• This hampers the correction of internal imbalances

Euro area current account balance Euro area GDP, aggregate demand and trade balance and core inflation

76

Stock vulnerabilities persist in debtor countries

• Net external liabilities are trending down, but progress is slow

• Vulnerabilities remain in a number of countries

NIIP and net external debt, 2015 Cyclically-adjusted and NIIP-stabilising, NIIP-converging CA balances, 2015

77

Private sector deleveraging is ongoing, but is

slow and uneven

• Deleveraging is hampered by low nominal growth

• Over-indebtedness among HH and NFCs still prevails in many MS

Drivers of HH deleveraging (2016Q1) Drivers of NFCs deleveraging (2016Q1)

78

Public and private indebtedness does not always

decline where leverage is highest Government debt: change from peak vs. 2015 level Private debt: change from peak vs. 2015 level

79

Capital ratios improve, but challenges remain in

the banking sector

• Low profitability

• In some cases, legacy of bad debts

Banks' return on equity Non-performing loans

(% of total loans and advances)

80

Housing market pressures are evident in some

Member States House prices valuation levels and variations (2015)

81

Labour market conditions continue to improve

• Unemployment rates continue to fall across the board

• Social distress persists

Evolution of the unemployment rate (20-64 years old), 2014Q1 vs. 2016Q2

82

Overall findings (1)

• External adjustment remains asymmetric, stock vulnerabilities

remain significant

• Rebalancing within euro area deserves careful consideration:

(1) large and rising CA surplus as symptom of slack in aggregate

demand, with impact on growth and inflation across the EA; (2) net

debtor countries will need to sustain CA surpluses for some time; (3)

net creditor countries have room to strengthen demand dynamics

• Private and public debt deleveraging continues but is slow and

uneven, hampered by low nominal growth: deleveraging also not

always most significant where most needed

• Banking sector faces challenges linked to low profitability and

in some cases legacy of bad debts

• House price dynamics warrant careful monitoring in some MS

83

Overall findings (2)

• MS affected by multiple and interconnected stock and/or flow

vulnerabilities: CY, HR, PT and BG, IE, SI, ES

• MS with vulnerabilities driven by large stocks of general

government debt and concerns about potential output growth:

IT and BE, FR

• MS with large and persistent current account surpluses: DK,

DE, NL, SE

• MS where developments in price or cost variabless show

potential signs of overheating: DK, LU, UK, SE and BG, EE, LV,

LT

• MS with potential vulnerabilities in specific sectors: NL and FI

84

Procedural conclusions

• IDRs are warranted for 13 countries, six fewer than last year:

BG, HR, CY, FI, FR, DE, IE, IT, NL, PT, SI, ES, SE

• All are countries identified with imbalances or excessive

imbalances in the previous cycle

• No countries will be newly subject an IDR

• The surveillance of imbalances in EL continues in the context

in the programme of financial assistance

85

6. Conclusion and next steps

Next steps

• The AMR conclusions to be discussed in the Council and Eurogroup;

• IDRs planned to be published in February, ahead of CSR package as last cycle;

• IDRs embedded in country reports

• After IDR, for some countries imbalances may not any longer be identified

• Specific monitoring is now in place for all Member States with

some level of imbalance

Opportunities

• Earlier detection of imbalances

• Ability to communicate and have impact on domestic policy debates

• Evolving over time to capture macroeconomic priorities: adjustment of flows but outstanding stocks

• Shifting emphasis to reflect topical policy issues: e.g. current account surpluses or social implications of adjustment

• Improved analytical tools

Challenges

• Given the nature of imbalances, less rules-based, more judgement

• Corrective arm not used yet

• Exploit the existing framework (repeated game with potential stigma effects) to ensure its effectiveness

• IDRs for all Member States or more selective?

• Is the framework capturing the main challenges and is it adapting in an adequate manner?

The MIP is now well-established but the full set of instruments has not yet been used

87

88

Useful links • The Macroeconomic Imbalance Procedure Rationale, Process,

Application: A Compendium (November 2016)

http://ec.europa.eu/economy_finance/publications/eeip/pdf/ip039_en.pdf

• Alert Mechanism Report 2017 (November 2016)

https://ec.europa.eu/info/publications/2017-european-semester-alert-mechanism-

report_en

• In-Depths Reviews

http://ec.europa.eu/economy_finance/economic_governance/macroeconomic_imb

alance_procedure/in-depth_reviews/index_en.htm

• Economic Governance

http://ec.europa.eu/economy_finance/economic_governance/index_en.htm

• Banking Union/SSM

http://europa.eu/rapid/pressReleasesAction.do?reference=IP/12/953&format=HTML

&aged=0&language=EN&guiLanguage=en

• Autumn 2016 Economic Forecast

http://ec.europa.eu/economy_finance/eu/forecasts/2016_autumn_forecast_en.htm

89

Thank you for your attention