the end of the innocence: supply and demand in a stagnant production environment

TRANSCRIPT

The End of the Innocence Supply and Demand in a Stagnant Production Environment Jack Weixel, Vice President, Analysis

Introducing – PointLogic Energy!

And in the blue corner…….

• Full service, energy fundamental data service provider.

• 30 employees consisting of both

upstream, midstream and downstream experts with offices in Houston, Denver, El Paso and Gaithersburg, MD.

• Started over 18 years ago as Lippman Consulting (later renamed LCI Energy Insight).

• Purchased by OPIS in December 2012 and renamed PointLogic Energy in January 2015.

• Over 350 years of combined industry experience.

• Detailed basin, regional and macro

reports spanning multiple delivery platforms.

First off, who is PointLogic Energy?

PointLogic Energy Services

• Detailed Flow Data – Production, Demand, Compressors and Custom Throughputs for Every Interstate Pipeline at Every State Border.

• Notice Service

• Searchable, Interactive IOC Database

• Pipeline Project Data and Details

• Interactive Client Variable Modeling, No Black Boxes

• Customized Subscription Packages and Enterprise Pricing

• Best in Class Customer Service

• Top tier data interface, data delivery in easy to use formats.

PointLogic Energy Data Suite

Easily drill into essential data and generate the analysis you need to boost your bottom line.

Pipelines

Production

Power

Excel Add-In

Forecast Models

More To Come

Energy Data Suite

PointLogic Energy Data Suite

We've taken cumbersome yet critical energy market fundamental data and delivered it in a filterable, mapped web application. www.pointlogicenergy.com

Get the Point PointLogic Energy’s FREE Weekly Trend Report

• Examines key energy market drivers

• Written by veteran energy experts and analysts

• Each weekly issue explores new trends in oil and gas supply, demand and prices

• Trend analyses leverages proprietary PointLogic Energy data, maps and other intelligence

Reliable insight you won’t find anywhere else!

Sign up for free today @ www.PointLogicEnergy.com/Get-the-Point.html

Remember this guy?

Agenda

• Where are we now?

• Supply Expectations

• Demand Expectations

• Impact on 2015 Supply and Demand Balance

• What about price?

4.8

0.0 0.1

4.9

1.8

0.0

-3.3

0.4

-1.1

Dry

Pro

d

LNG

Can

Impo

rts

Supp

ly

Pow

er

Indu

stria

l

Res

/Com

Mex

Ex

Dem

and

2014-15 Winter vs. 2013-14 Winter

Supply Demand

Source: PointLogic Energy Supply & Demand Report

Market Was 6.0 Bcf/d Long Versus Winter 13/14

3.1

-0.1

0.5

3.5 3.0

1.3

-3.4

0.6 1.5

Dry

Pro

d

LNG

Can

Impo

rts

Supp

ly

Pow

er

Indu

stria

l

Res

/Com

Mex

Ex

Dem

and

2015 Summer td vs. 2014 Summer td

Supply Demand

Source: PointLogic Energy Supply & Demand Report

Season to date: 2.0 Bcf/d Long Versus Summer 14 to date

Was 3.1 Bcf/d Long on May 22nd

What’s Going On Production?

63.0064.0065.0066.0067.0068.0069.0070.0071.0072.0073.0074.0075.00

Lower 48 Dry Production (Bcf/d)

2015 2014

Production grew 3.3 Bcf/d from Jan to May 14

Production struggling to grow 0.6 Bcf/d Jan to May 15

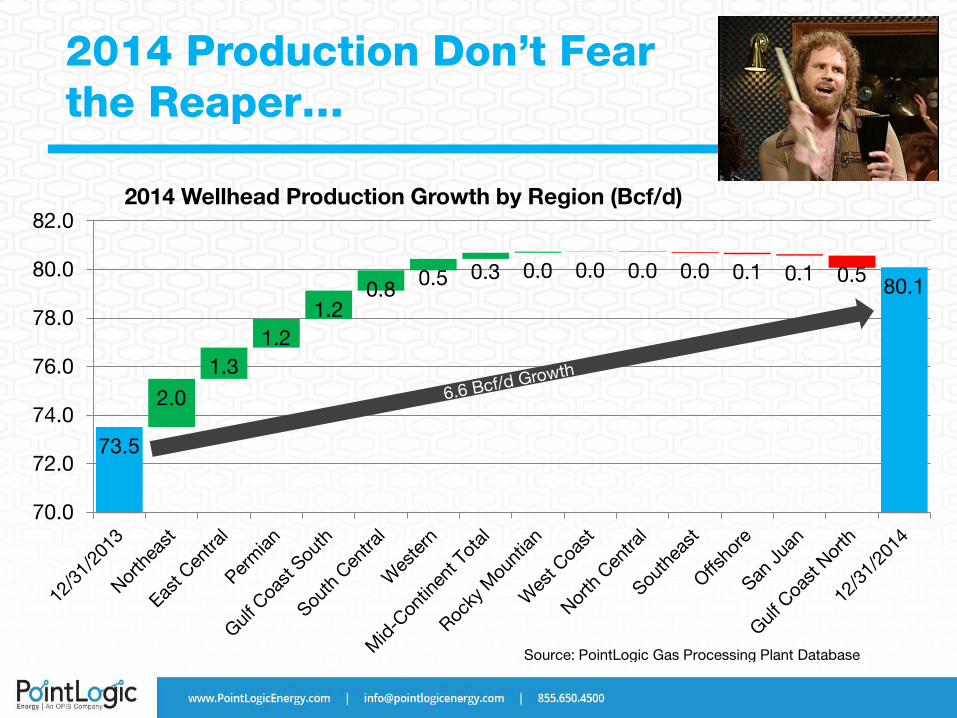

2014 Production Don’t Fear the Reaper…

0.0 0.0 0.1 0.1 0.5

2.0

1.3 1.2

1.2 0.8 0.5 0.3 0.0 0.0

73.5

80.1

70.0

72.0

74.0

76.0

78.0

80.0

82.02014 Wellhead Production Growth by Region (Bcf/d)

Source: PointLogic Gas Processing Plant Database

2015 Production Got a Fever..

0.8 0.1 0.0 0.1 0.1 0.0 0.0 0.5 0.4 0.1 0.1 0.0 0.4 0.0 80.1 79.5

70.0

72.0

74.0

76.0

78.0

80.0

82.02015 Year to Date Production Growth by Region (Bcf/d)

Source: PointLogic Gas Processing Plant Database

2015 Wells First Delivered

53 0 236

176

318 0 18 20 94

2,963

2,048

0

500

1000

1500

2000

2500

3000

3500All Wells First Delivered by Region

I got a fever…

Source: Drilling Info, PointLogic Estimates

35 5 71

62

117 0 9

145 2

1,124

678

0

200

400

600

800

1000

1200

All Gas Wells First Delivered By Region

2015 Production Got a Fever.. …and the only prescription is higher prices!

Source: Drilling Info, PointLogic Estimates

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

MM

cf/d

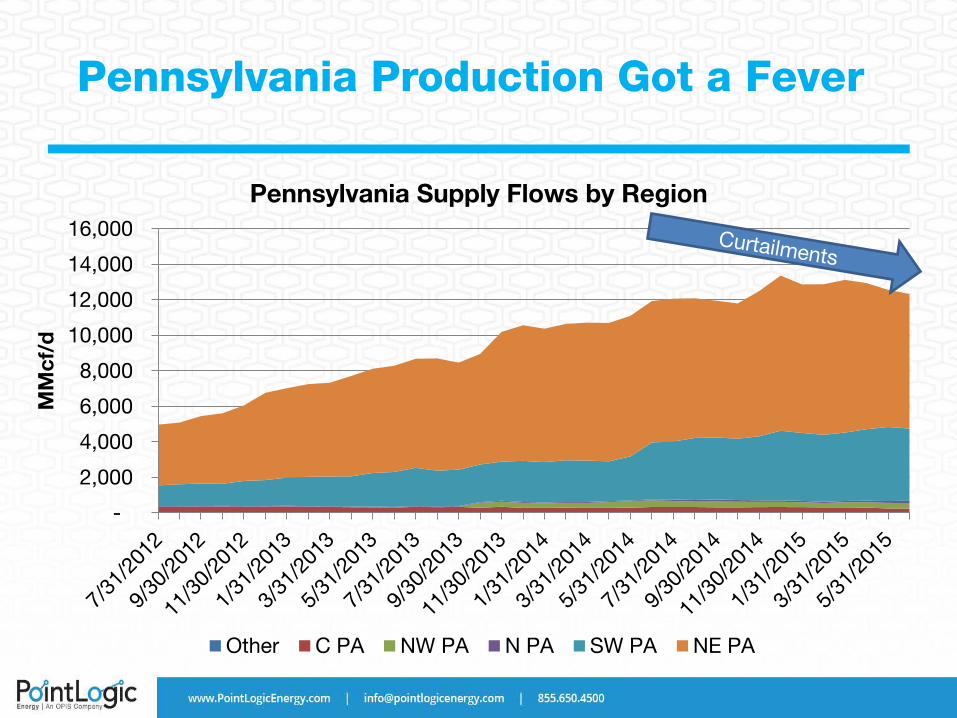

Pennsylvania Supply Flows by Region

Other C PA NW PA N PA SW PA NE PA

Pennsylvania Production Got a Fever

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

MM

cf/d

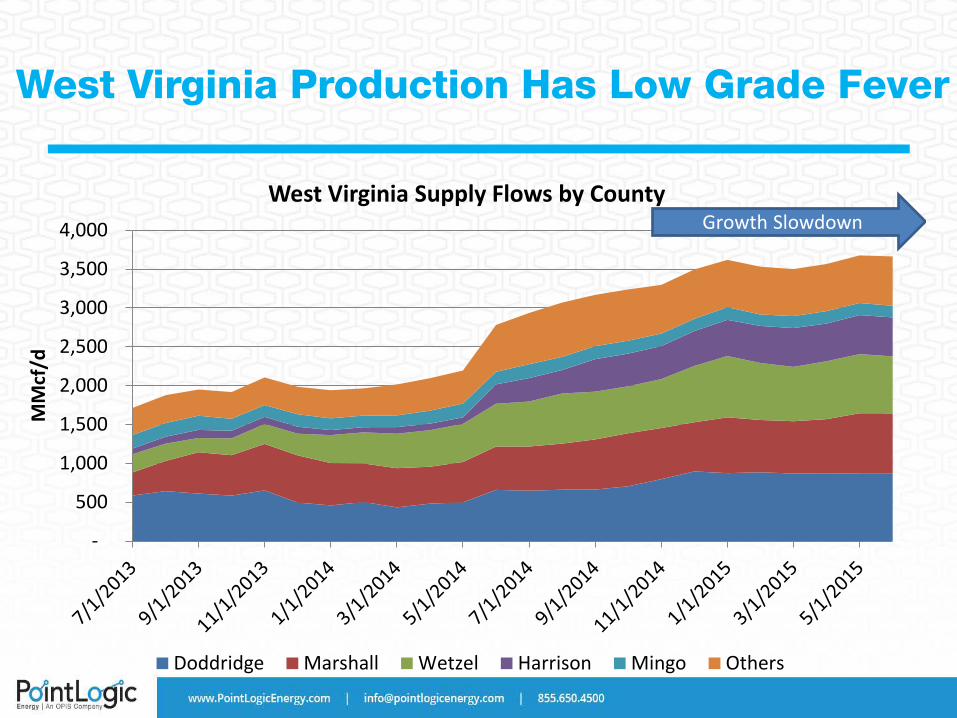

West Virginia Supply Flows by County

Doddridge Marshall Wetzel Harrison Mingo Others

Growth Slowdown

West Virginia Production Has Low Grade Fever

-

500

1,000

1,500

2,000

2,500

3,000

MM

cf/d

Ohio Supply Flows by County

Monroe Columbiana Noble Carroll Mahoning Others

Oh Way to Go Ohio – Not a Pretender

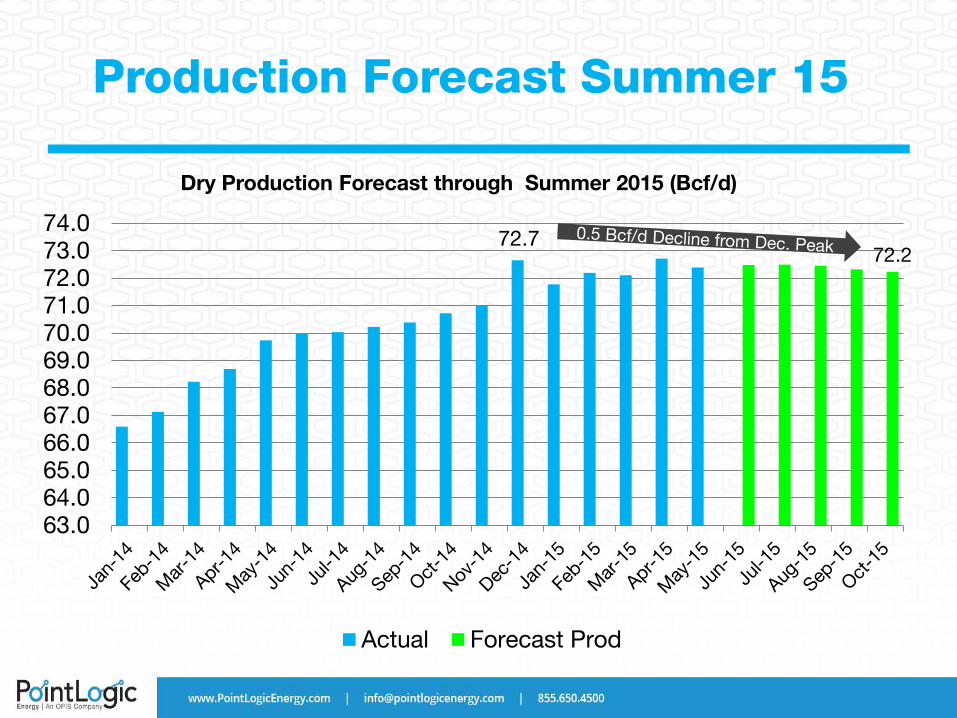

Production Forecast Summer 15

72.7 72.2

63.064.065.066.067.068.069.070.071.072.073.074.0

Dry Production Forecast through Summer 2015 (Bcf/d)

Actual Forecast Prod

21

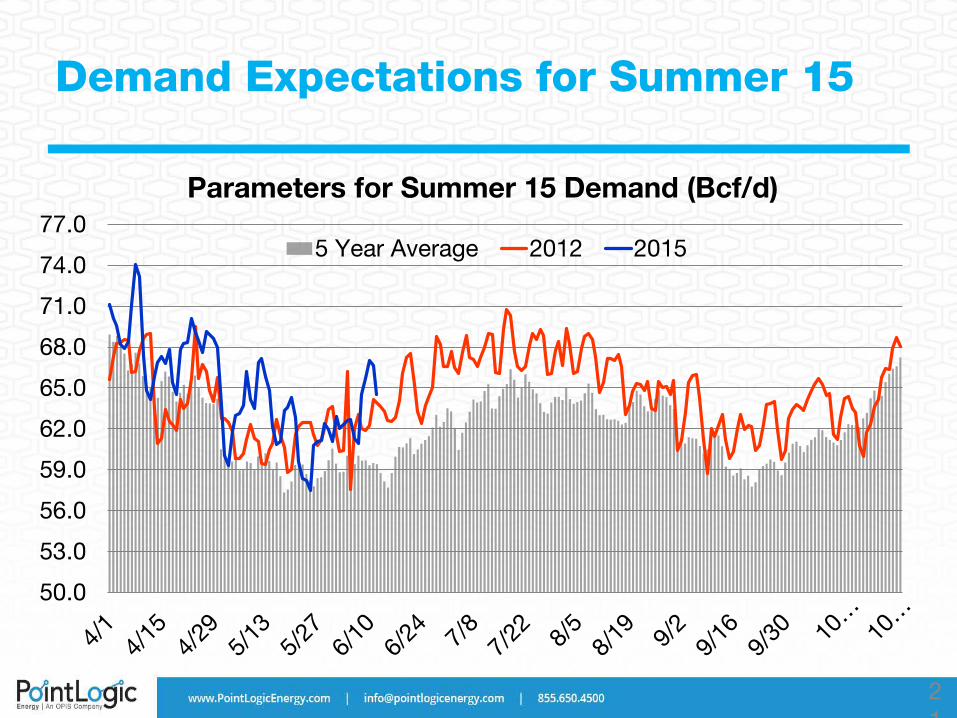

Demand Expectations for Summer 15

50.0

53.0

56.0

59.0

62.0

65.0

68.0

71.0

74.0

77.0Parameters for Summer 15 Demand (Bcf/d)

5 Year Average 2012 2015

22

Demand To Date for Summer 15

0

7

14

21

28

35

42

49

56

63

70

2010 2011 2012 2013 2014 2015

Average Summer Demand to date (Bcf/d)

Power Industrial Res/Com Mexico 5 Year Average

Power: up 2.3 Bcf/d vs. 5 Year Avg

Mexico: up 1.0 Bcf/d vs. 5 Year Avg

Res/Com: off 0.5 Bcf/d vs. 5 Year Avg

Industrial: up 2.8 Bcf/d vs. 5 Year Avg

5 Year Avg Demand = 55.2 Bcf/d Summer 2015 = 60.9 Bcf/d Summer 2012 = 58.4 Bcf/d

Power and Industrial Demand Driving the Bus…

23

5.2

3.6

4.2 4.3

2.5 2.1

3.3

3.9

0.0 0.1

4.9

Week on Week Power Demand Delta Summer 15 Versus Summer 14

(Bcf/d)

0.6 0.7

0.5

1.7 1.8 1.6

1.5

1.8 1.9 1.9

Week on Week Industrial Demand Delta Summer 15 Versus Summer 14

(Bcf/d)

Industrial Demand Has Proven to Be Resilient through June

June 14 -- 19.79

Forecast -- 21.50

15.0

16.0

17.0

18.0

19.0

20.0

21.0

22.0

23.0

Summer Industrial Burn (Bcf/d) 2012 Peak Months vs. June 2015td

2012 June - Aug 2015 Jun Forecast 2014 June - Aug

EIA Forecasts 21.8 Bcf/d for full year 2015

Industrial Demand Has Proven to Be Resilient through June

-50 50 150 250 350 450 550 650 750 850 950

Northwest

Western

California

Rocky Mountain

Southwest

San Juan

North Central

Mid-Continent

Permian

Gulf Coast Onshore

Southeast

South Central

East Central

Northeast

Delta Industrial Demand by Region May 15 vs. May 14 (MMcf/d)

Power Burn Up In All Regions – Gulf, Southeast and Midcon Are Overachievers

26

0 100 200 300 400 500 600 700

Northwest

Western

California

Rocky Mountain

Southwest

North Central

Mid-Continent

Permian

Gulf Coast Onshore

Southeast

South Central

East Central

Northeast

Average Delta Power Burn (MMcf/d) Season to Date

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Georgia Ohio Alabama Illinois Utah Iowa Florida Minnesota Kentucky

Mar-May 2015 Coal Gen Capacity (MW) Retired

Coal Retirements Through May 2015

Significant retirements include Georgia Power units in Georgia, First Energy units in Ohio and TVA Widow’s Creek in Alabama.

4.0 GW ~ 0.36 Bcf/d at 50% Capacity and 7.5 Heat Rate

Source: PointLogic Energy research and EIA

0

200

400

600

800

1,000

1,200

1,400

1,600

Coal Retirements Balance of 2015 (MW)

Jun-15 Dec-15

Coal Retirements Summer 2015

Includes AEP units in West Virginia and Ohio, Appalachian Power units in West Virginia and Virginia, Dayton Power units in Ohio, Indiana Michigan Power units in Indiana and Cane Run in Kentucky plus conversion of Big Sandy in Kentucky. 6.1 GW in June 2015 = 0.55 Bcf/d at 50% Capacity and 7.5 Heat Rate

Source: PointLogic Energy research and EIA

July 6 -- 37.5 July 25th -- 38.1

June 25 -- 34.8

July -- 33.00

August -- 30.00

20.0

22.0

24.0

26.0

28.0

30.0

32.0

34.0

36.0

38.0

40.0

Summer Power Burn (Bcf/d) 2012 Peak Months vs. June 2015td

2012 June - Aug 2015 Jun Forecast

Power Burn Through June, July and August Will Be Critical

If June forecast plays out, June 2015 average power demand is short of June 2012 average by 0.05 Bcf/d (29.39 Bcf/d).

And Mexico Has a Plethora from US Exporters…

30

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Net Mexican Exports from the U.S. (Bcf/d)

Mexican Exports Al Rojo Vivo! Up 31% Summer to date vs.

2014

0

100

200

300

400

500

600

700

800

900

NET Mexico and KM Sierrita Exports (MMcf/d)

NET Mexico KM Sierrita

0

7

14

21

28

35

42

49

56

63

70

2012 2014 2015 est 5 Year Average

Forecast Summer Demand (Bcf/d)

Power IndustrialRes/Com Mexico

31

Demand Expectations for Summer 15

Power: down 1.9 Bcf/d vs. 2012 and up 2.3 Bcf/d vs. 5 Year Avg.

Mexico: up 0.8 Bcf/d vs. 2012 and up 1.0 Bcf/d vs. 5 Year Avg.

Res/Com: up 0.9 Bcf/d vs. 2012 and up 0.3 Bcf/d vs. 5 Year Avg.

Industrial: up 2.5 Bcf/d vs. 2012 and up 2.8 Bcf/d vs. 5 Year Avg.

Total Demand Summer 2015 averages 61.5 Bcf/d vs. 2012 level of 59.2 Bcf/d – Δ of 2.3 Bcf/d

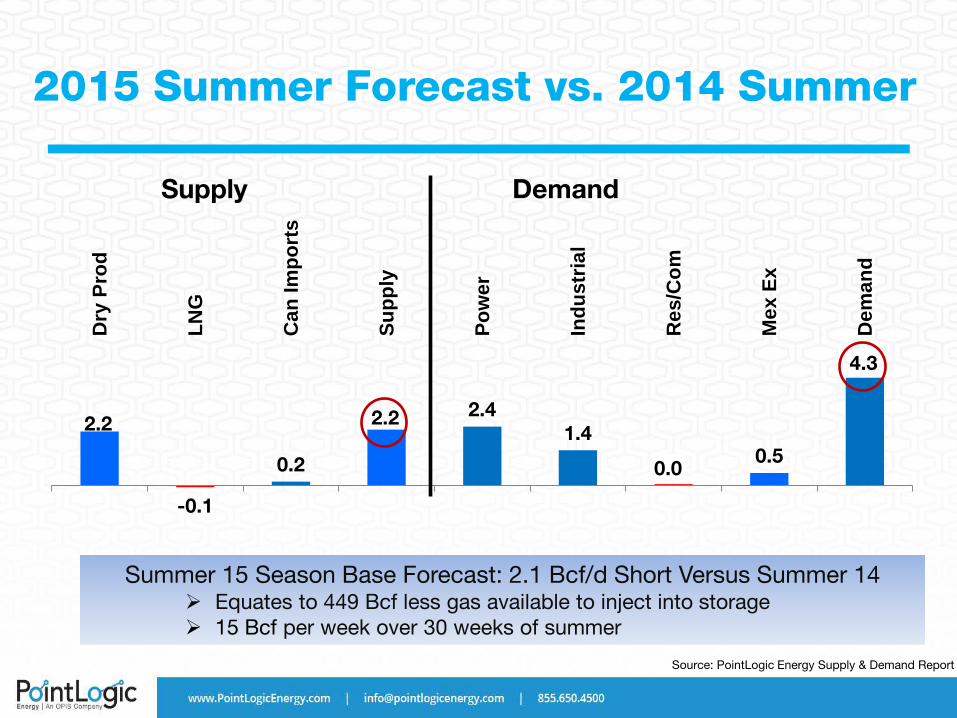

2.2

-0.1

0.2

2.2 2.4 1.4

0.0 0.5

4.3

Dry

Pro

d

LNG

Can

Impo

rts

Supp

ly

Pow

er

Indu

stria

l

Res

/Com

Mex

Ex

Dem

and

2015 Summer Forecast vs. 2014 Summer

Supply Demand

Source: PointLogic Energy Supply & Demand Report

Summer 15 Season Base Forecast: 2.1 Bcf/d Short Versus Summer 14 Equates to 449 Bcf less gas available to inject into storage 15 Bcf per week over 30 weeks of summer

7501,0001,2501,5001,7502,0002,2502,5002,7503,0003,2503,5003,7504,000

5 Yr Avg

5 Yr Min

2014/15

Base Forecast

Storage Injections Could Match 5 Year Average, but that Would Be Boring!

US Storage Inventories (Bcf)

Source: PointLogic Daily Market Report & EIA

Assuming 5 year average injection rate puts inventories at 3,826 Bcf, a mere 44 Bcf above the 5 year average, but

230 Bcf ahead of last year.

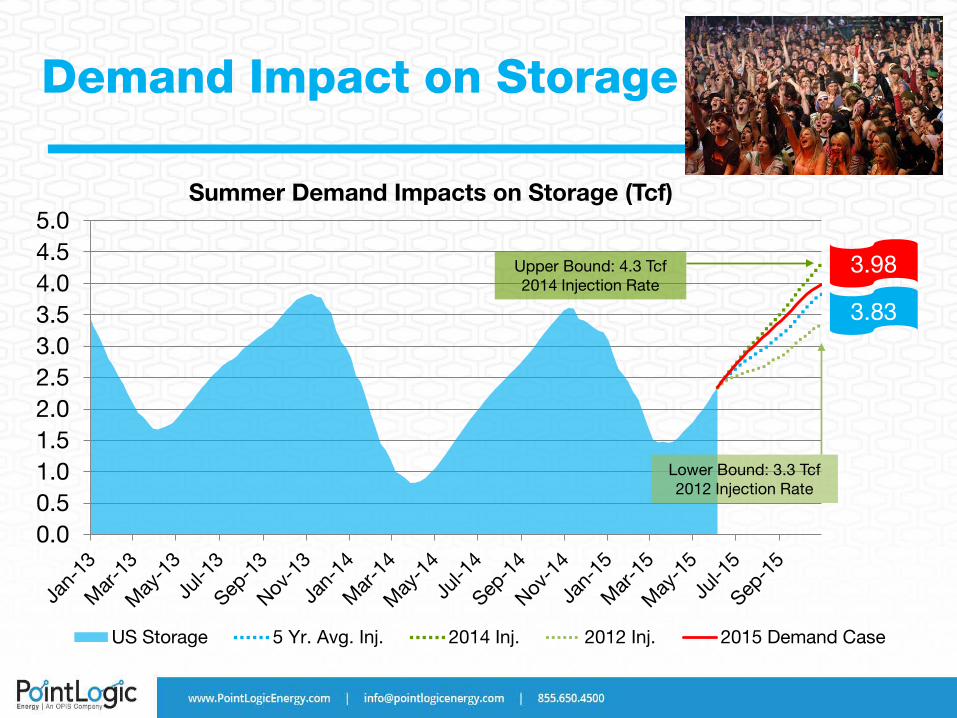

Demand Impact on Storage

0.00.51.01.52.02.53.03.54.04.55.0

Summer Demand Impacts on Storage (Tcf)

US Storage 5 Yr. Avg. Inj. 2014 Inj. 2012 Inj. 2015 Demand Case

Upper Bound: 4.3 Tcf 2014 Injection Rate

Lower Bound: 3.3 Tcf 2012 Injection Rate

3.98

3.83

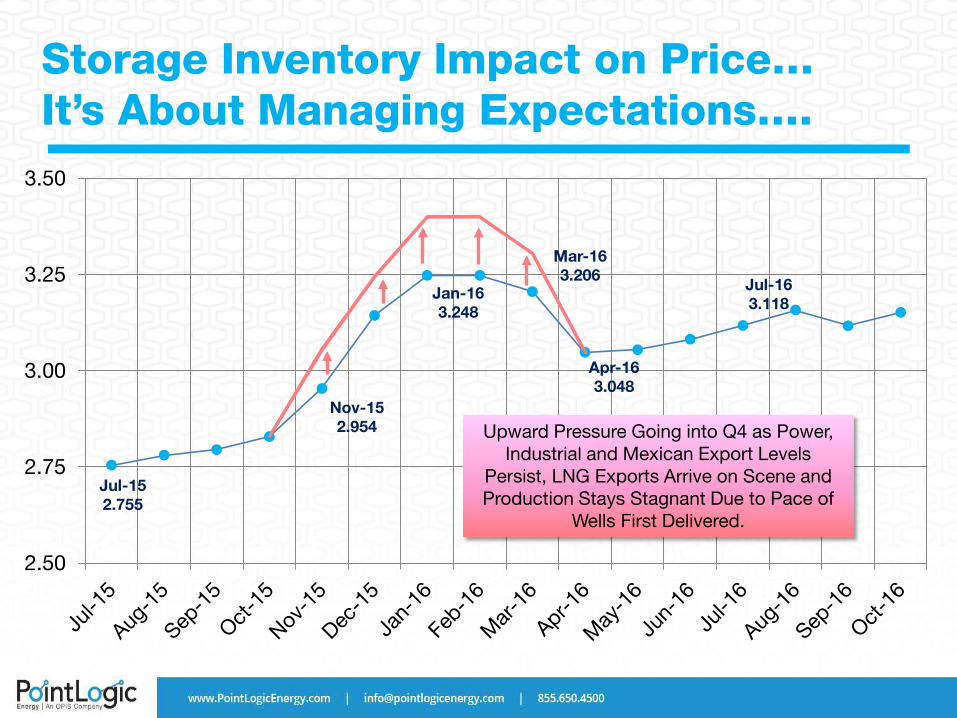

Storage Inventory Impact on Price… It’s About Managing Expectations….

Jul-15 2.755

Nov-15 2.954

Jan-16 3.248

Mar-16 3.206

Apr-16 3.048

Jul-16 3.118

2.50

2.75

3.00

3.25

3.50

Upward Pressure Going into Q4 as Power, Industrial and Mexican Export Levels

Persist, LNG Exports Arrive on Scene and Production Stays Stagnant Due to Pace of

Wells First Delivered.

Key Takeaways

Sustained production and normal winter drives market towards equilibrium.

Production stagnation is evident across most regions of the country.

Summer demand increases in power, industrial and Mexico mark beginning of systemic increases and transition to demand driven market.

Impact on storage is marginal in Summer 15 – market can handle this level of demand in current production environment.

Upward Price Pressure Heading Into Winter 15/16.

Contact Us Today!

Jack Weixel Vice President, Analysis 202.607.6354 [email protected] Customer Support Phone: 855.650.4500 ext. 1 [email protected] Sales Phone: 855.650.4500 ext. 2 [email protected]

Gaithersburg HQ: 9737 Washingtonian Blvd.

Houston Office: 1155 Dairy Ashford Rd.