the certainty (and uncertainty) of taxes

TRANSCRIPT

©2019 Lincoln National CorporationLCN-2414999-020719

Insurance products issued by:The Lincoln National Life Insurance CompanyLincoln Life & Annuity Company of New York

Not a deposit

Not FDIC-insured May go down in value

Not insured by any federal government agencyNot guaranteed by any bank or savings association

The Certainty (and Uncertainty) of TaxesHelp protect your lifetime income stream from tax risk

LINCOLN INCOME SOLUTIONS

For use with the general public. LCN-2414999-020719

Death and taxes

2

For use with the general public. LCN-2414999-020719

Three key concepts

• Taxes never sleep…even in retirement

• The importance of planning

• Protecting your retirement income with tax-smart strategies

3

4

Taxes never sleep… even in retirement.

For use with the general public. LCN-2414999-020719

For use with the general public. LCN-2414999-020719

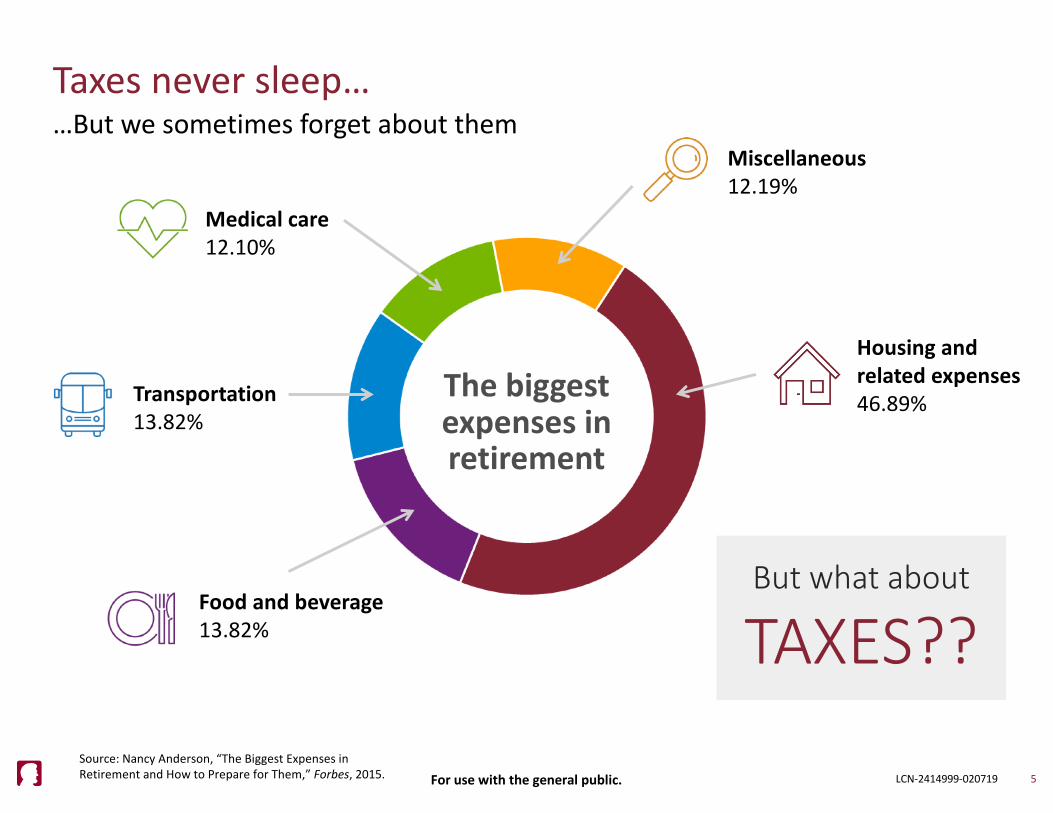

Taxes never sleep…

5

…But we sometimes forget about them

Source: Nancy Anderson, “The Biggest Expenses in

Retirement and How to Prepare for Them,” Forbes, 2015.

The biggest expenses in retirement

Housing and related expenses46.89%

Miscellaneous12.19%

Medical care12.10%

Transportation13.82%

Food and beverage13.82%

But what about

TAXES??

For use with the general public. LCN-2414999-020719

Don’t underestimate taxes in retirement

• Will you maintain your income (and lifestyle)?

• How are your various retirement assets taxed?

• What will your taxes do in the future?• What will the market do in the future?

6

Source: LIMRA Secure Retirement Institute, 2018.

“My taxes will be lower in retirement”— MYTH!

For use with the general public. LCN-2414999-020719

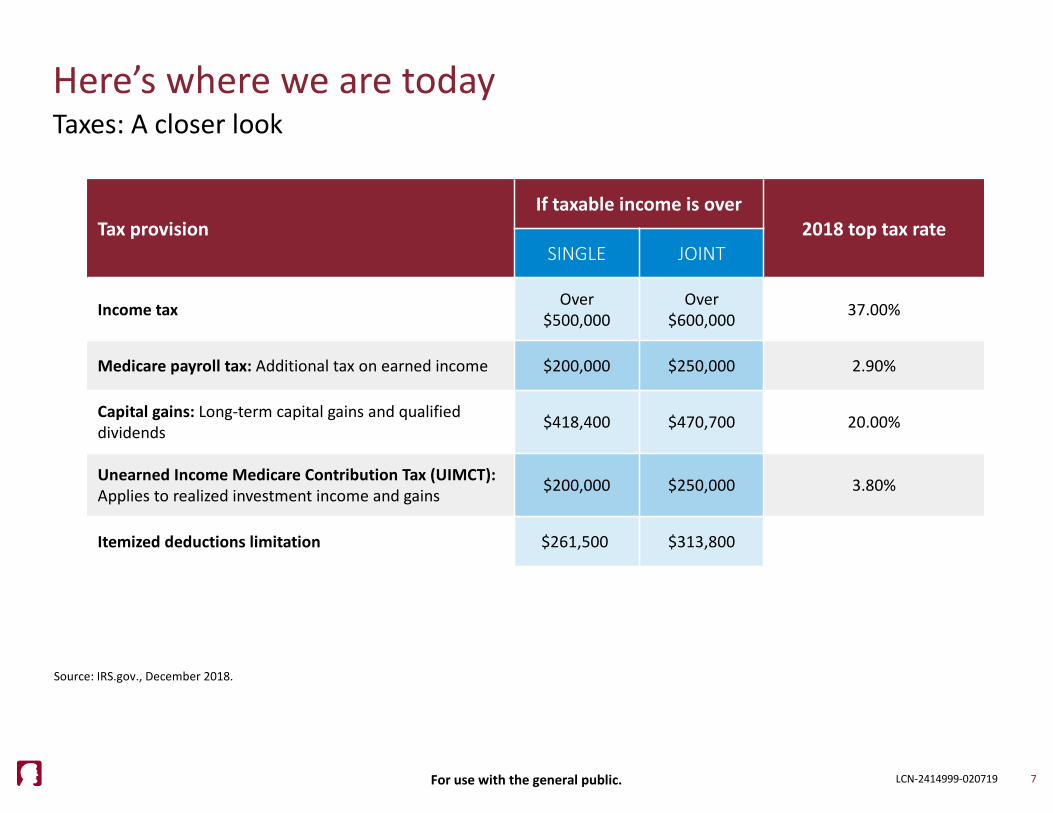

Here’s where we are today

7

Taxes: A closer look

Tax provisionIf taxable income is over

2018 top tax rateSINGLE JOINT

Income tax Over $500,000

Over $600,000 37.00%

Medicare payroll tax: Additional tax on earned income $200,000 $250,000 2.90%

Capital gains: Long-term capital gains and qualified dividends $418,400 $470,700 20.00%

Unearned Income Medicare Contribution Tax (UIMCT): Applies to realized investment income and gains $200,000 $250,000 3.80%

Itemized deductions limitation $261,500 $313,800

Source: IRS.gov., December 2018.

For use with the general public. LCN-2414999-020719

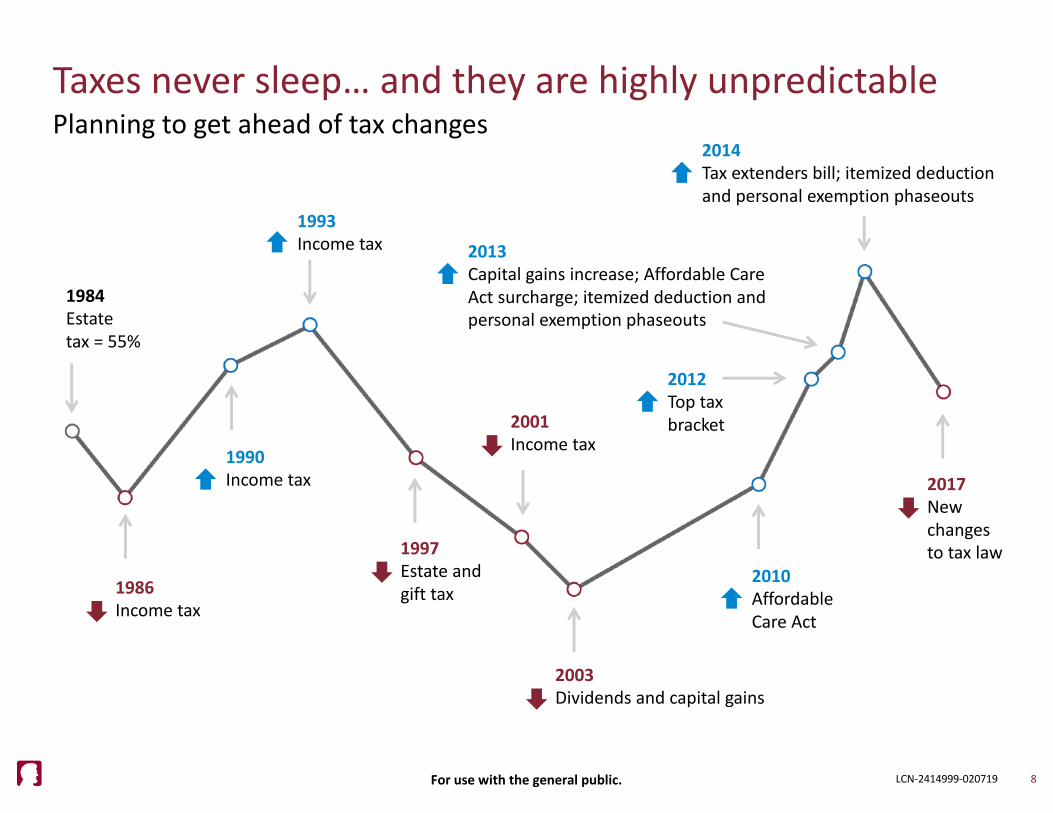

Taxes never sleep… and they are highly unpredictable

8

Planning to get ahead of tax changes

1984Estate tax = 55%

1986Income tax

1990Income tax

1993Income tax

1997Estate and gift tax

2001Income tax

2003Dividends and capital gains

2010Affordable Care Act

2017New changes to tax law

2012Top tax bracket

2013Capital gains increase; Affordable Care Act surcharge; itemized deduction and personal exemption phaseouts

2014Tax extenders bill; itemized deduction and personal exemption phaseouts

For use with the general public. LCN-2414999-020719

Taxes never sleep… and they are highly unpredictable

9

Down markets can provide the ability to harvest tax losses

Up markets can result in unexpected short-term and long-term capital gains

For use with the general public. LCN-2414999-020719

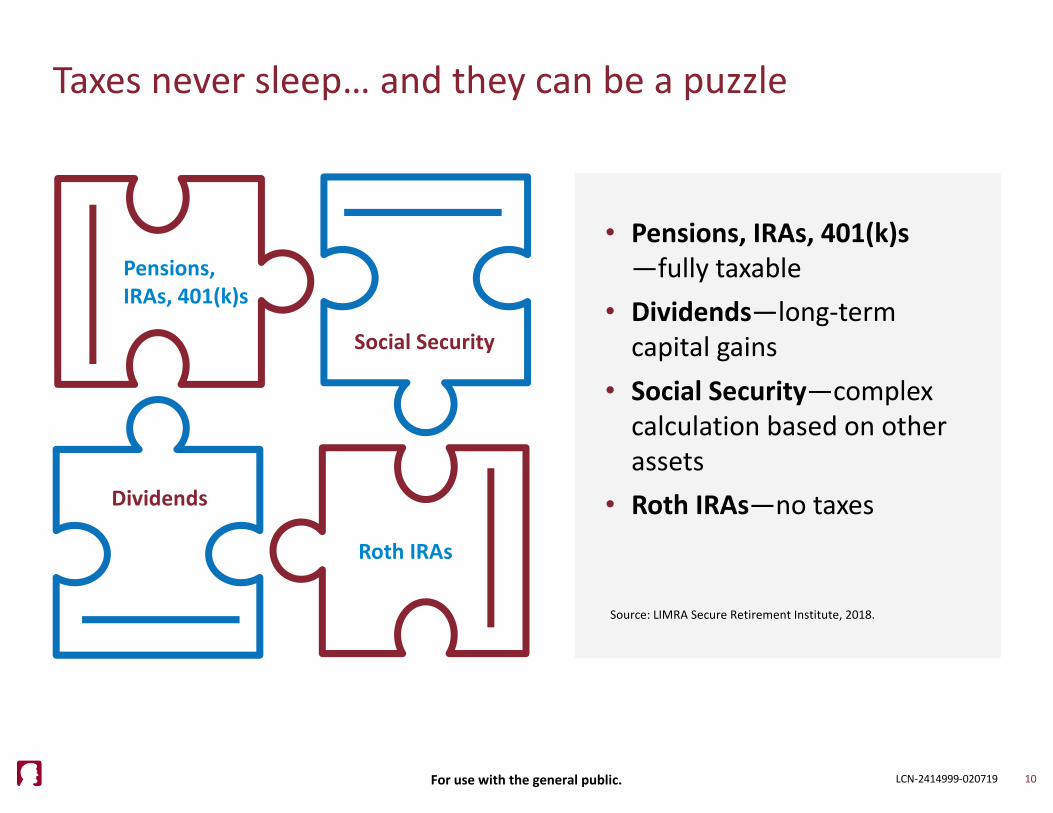

Taxes never sleep… and they can be a puzzle

10

Source: LIMRA Secure Retirement Institute, 2018.

• Pensions, IRAs, 401(k)s—fully taxable

• Dividends—long-term capital gains

• Social Security—complex calculation based on other assets

• Roth IRAs—no taxes

Pensions, IRAs, 401(k)s

Dividends

Social Security

Roth IRAs

For use with the general public. LCN-2414999-020719

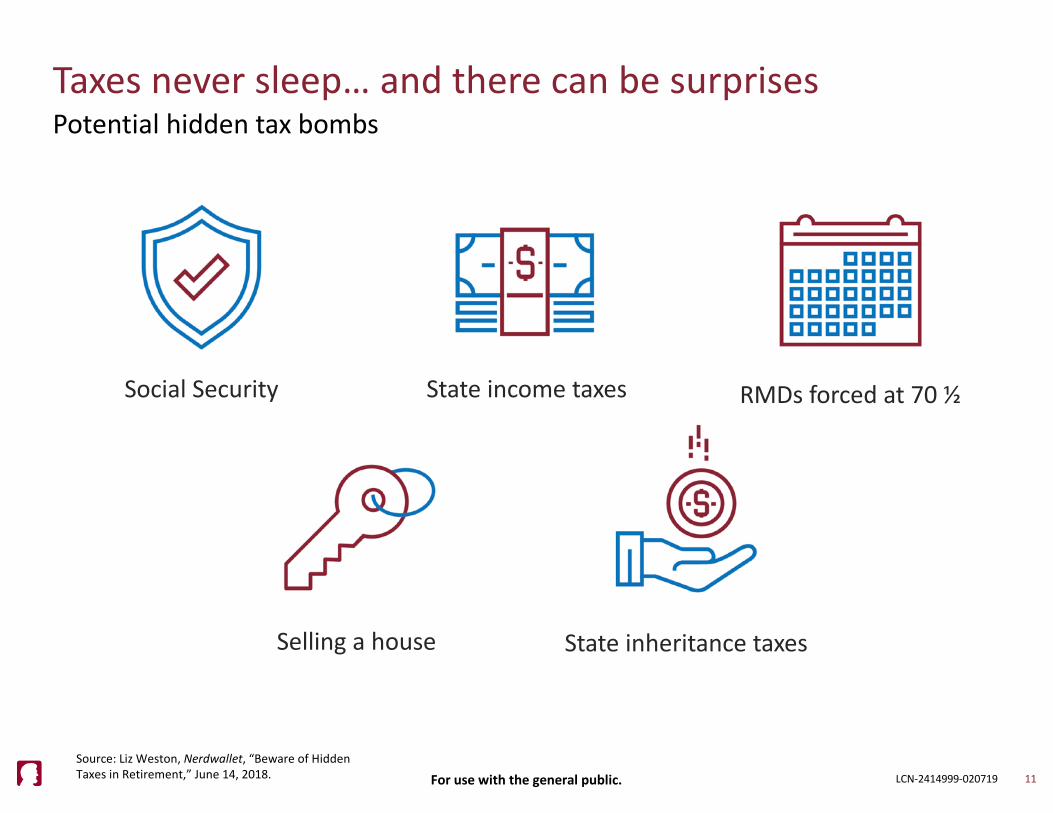

Taxes never sleep… and there can be surprises

11

Potential hidden tax bombs

Source: Liz Weston, Nerdwallet, “Beware of Hidden

Taxes in Retirement,” June 14, 2018.

Social Security State income taxes RMDs forced at 70 ½

Selling a house State inheritance taxes

For use with the general public. LCN-2414999-020719

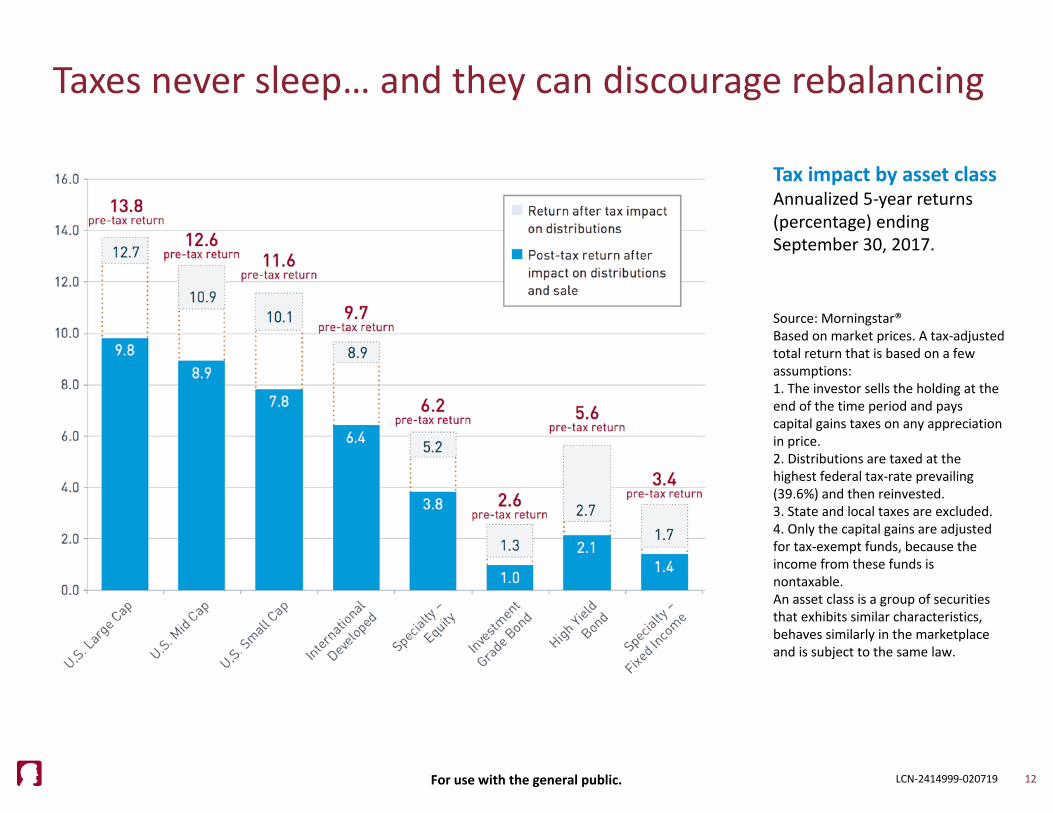

Taxes never sleep… and they can discourage rebalancing

12

Source: Morningstar®

Based on market prices. A tax-adjusted

total return that is based on a few

assumptions:

1. The investor sells the holding at the

end of the time period and pays

capital gains taxes on any appreciation

in price.

2. Distributions are taxed at the

highest federal tax-rate prevailing

(39.6%) and then reinvested.

3. State and local taxes are excluded.

4. Only the capital gains are adjusted

for tax-exempt funds, because the

income from these funds is

nontaxable.

An asset class is a group of securities

that exhibits similar characteristics,

behaves similarly in the marketplace

and is subject to the same law.

Tax impact by asset classAnnualized 5-year returns

(percentage) ending

September 30, 2017.

13

The importance of planning

For use with the general public. LCN-2414999-020719

For use with the general public. LCN-2414999-020719

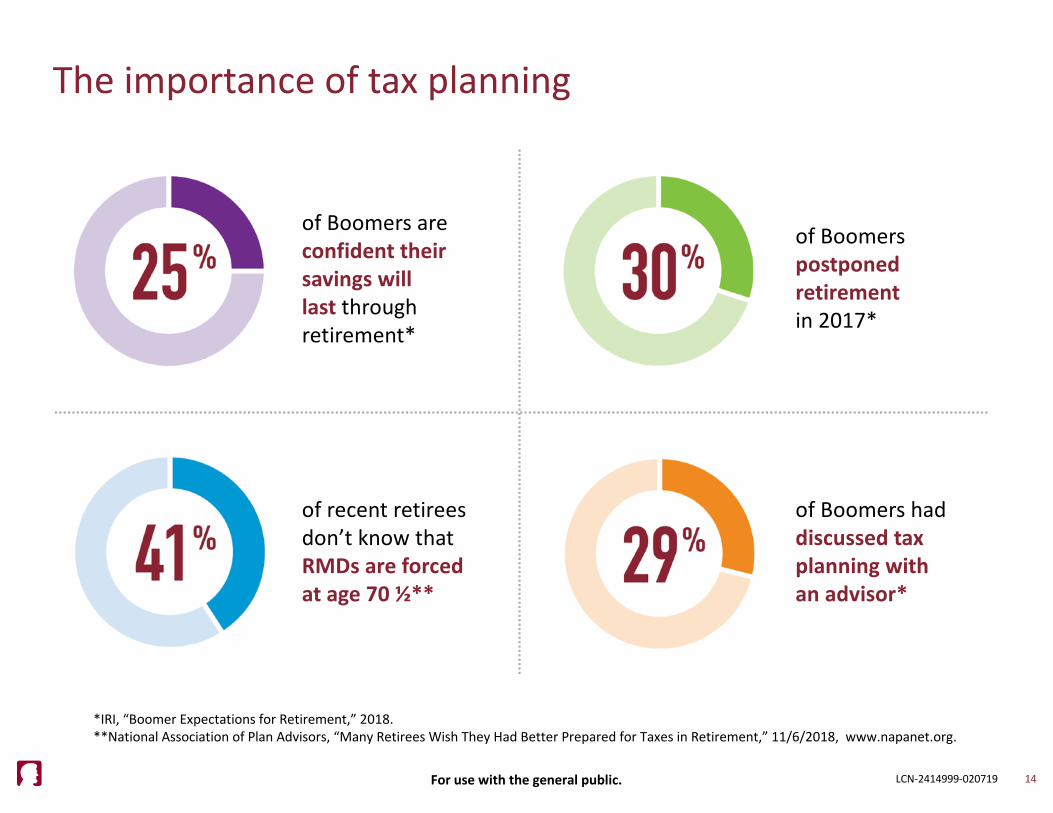

The importance of tax planning

14

*IRI, “Boomer Expectations for Retirement,” 2018.**National Association of Plan Advisors, “Many Retirees Wish They Had Better Prepared for Taxes in Retirement,” 11/6/2018, www.napanet.org.

of Boomers are confident their savings will last through retirement*

of recent retirees don’t know that RMDs are forced at age 70 ½**

of Boomers postponed retirement in 2017*

of Boomers had discussed tax planning with an advisor*

For use with the general public. LCN-2414999-020719

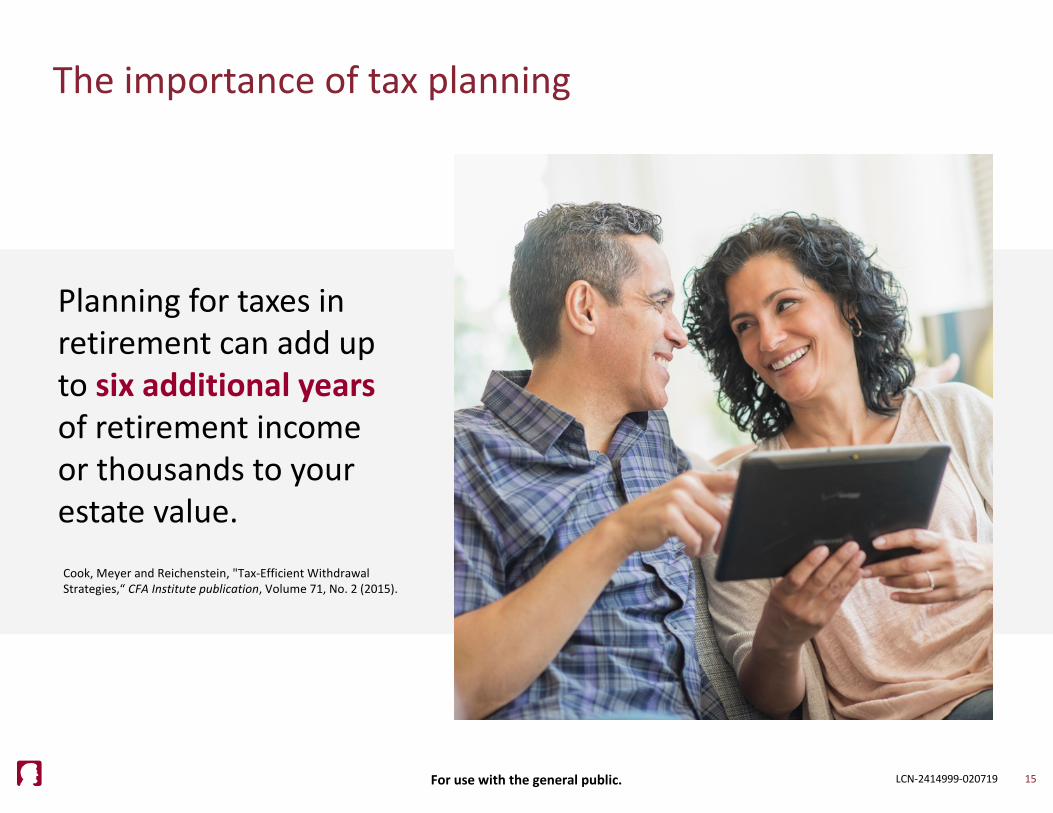

The importance of tax planning

Planning for taxes in retirement can add up to six additional years of retirement income or thousands to your estate value.

15

Cook, Meyer and Reichenstein, "Tax-Efficient Withdrawal Strategies,“ CFA Institute publication, Volume 71, No. 2 (2015).

For use with the general public. LCN-2414999-020719

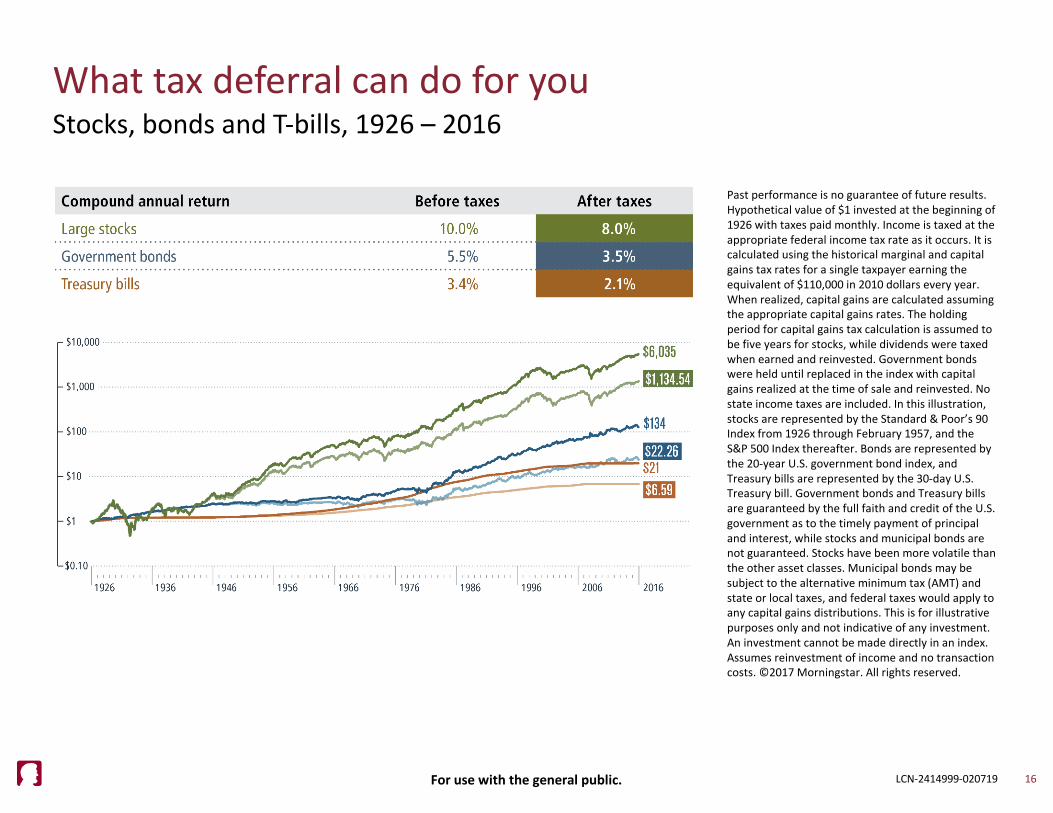

What tax deferral can do for you

16

Stocks, bonds and T-bills, 1926 – 2016

Past performance is no guarantee of future results.

Hypothetical value of $1 invested at the beginning of

1926 with taxes paid monthly. Income is taxed at the

appropriate federal income tax rate as it occurs. It is

calculated using the historical marginal and capital

gains tax rates for a single taxpayer earning the

equivalent of $110,000 in 2010 dollars every year.

When realized, capital gains are calculated assuming

the appropriate capital gains rates. The holding

period for capital gains tax calculation is assumed to

be five years for stocks, while dividends were taxed

when earned and reinvested. Government bonds

were held until replaced in the index with capital

gains realized at the time of sale and reinvested. No

state income taxes are included. In this illustration,

stocks are represented by the Standard & Poor’s 90

Index from 1926 through February 1957, and the

S&P 500 Index thereafter. Bonds are represented by

the 20-year U.S. government bond index, and

Treasury bills are represented by the 30-day U.S.

Treasury bill. Government bonds and Treasury bills

are guaranteed by the full faith and credit of the U.S.

government as to the timely payment of principal

and interest, while stocks and municipal bonds are

not guaranteed. Stocks have been more volatile than

the other asset classes. Municipal bonds may be

subject to the alternative minimum tax (AMT) and

state or local taxes, and federal taxes would apply to

any capital gains distributions. This is for illustrative

purposes only and not indicative of any investment.

An investment cannot be made directly in an index.

Assumes reinvestment of income and no transaction

costs. ©2017 Morningstar. All rights reserved.

For use with the general public. LCN-2414999-020719

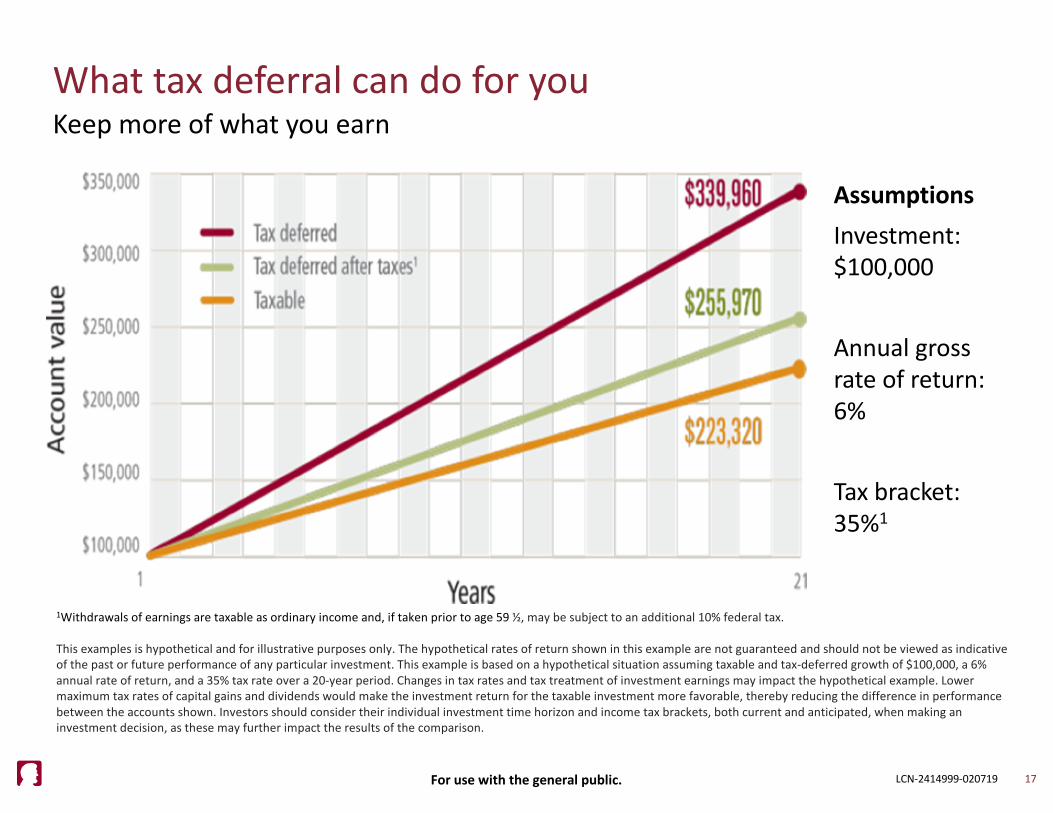

What tax deferral can do for you

17

Keep more of what you earn

1Withdrawals of earnings are taxable as ordinary income and, if taken prior to age 59 ½, may be subject to an additional 10% federal tax.

This examples is hypothetical and for illustrative purposes only. The hypothetical rates of return shown in this example are not guaranteed and should not be viewed as indicative of the past or future performance of any particular investment. This example is based on a hypothetical situation assuming taxable and tax-deferred growth of $100,000, a 6% annual rate of return, and a 35% tax rate over a 20-year period. Changes in tax rates and tax treatment of investment earnings may impact the hypothetical example. Lower maximum tax rates of capital gains and dividends would make the investment return for the taxable investment more favorable, thereby reducing the difference in performance between the accounts shown. Investors should consider their individual investment time horizon and income tax brackets, both current and anticipated, when making an investment decision, as these may further impact the results of the comparison.

AssumptionsInvestment: $100,000

Annual gross rate of return: 6%

Tax bracket: 35%1

For use with the general public. LCN-2414999-020719

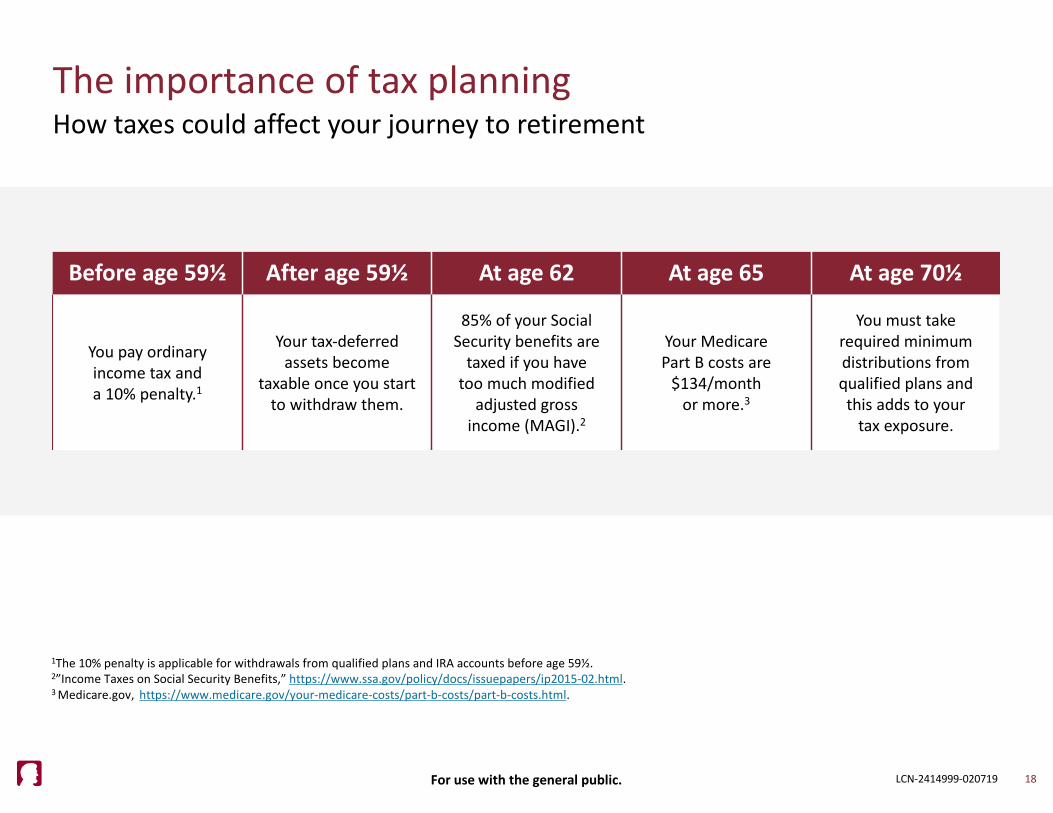

The importance of tax planning

18

How taxes could affect your journey to retirement

1The 10% penalty is applicable for withdrawals from qualified plans and IRA accounts before age 59½. 2”Income Taxes on Social Security Benefits,” https://www.ssa.gov/policy/docs/issuepapers/ip2015-02.html.3 Medicare.gov, https://www.medicare.gov/your-medicare-costs/part-b-costs/part-b-costs.html.

Before age 59½ After age 59½ At age 62 At age 65 At age 70½

You pay ordinary income tax and a 10% penalty.1

Your tax-deferred assets become

taxable once you start to withdraw them.

85% of your Social Security benefits are

taxed if you have too much modified

adjusted gross income (MAGI).2

Your Medicare Part B costs are

$134/month or more.3

You must take required minimum distributions from qualified plans and this adds to your

tax exposure.

For use with the general public. LCN-2414999-020719

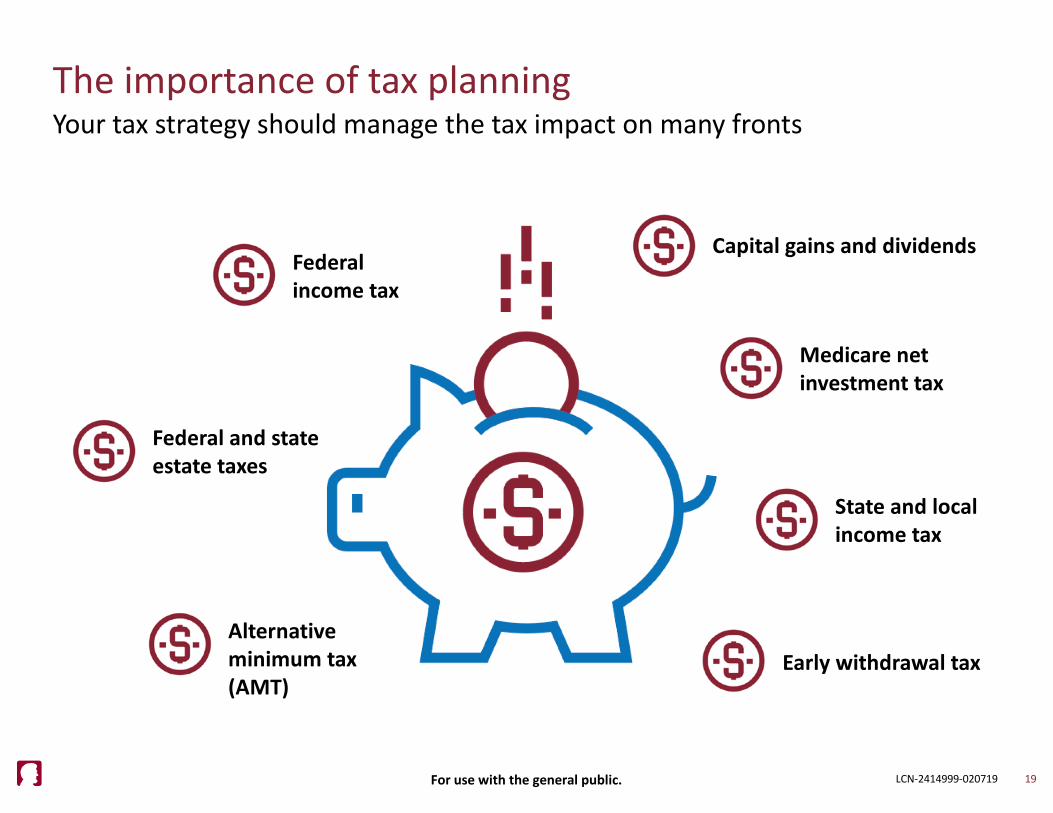

The importance of tax planning

19

Your tax strategy should manage the tax impact on many fronts

Federal income tax

Federal and state estate taxes

Alternative minimum tax (AMT)

Capital gains and dividends

Medicare net investment tax

State and local income tax

Early withdrawal tax

20

Protecting your retirementincome with tax-smart strategies

For use with the general public. LCN-2414999-020719

For use with the general public. LCN-2414999-020719

Tax-smart strategies with your 1040

21

For use with the general public. LCN-2414999-020719

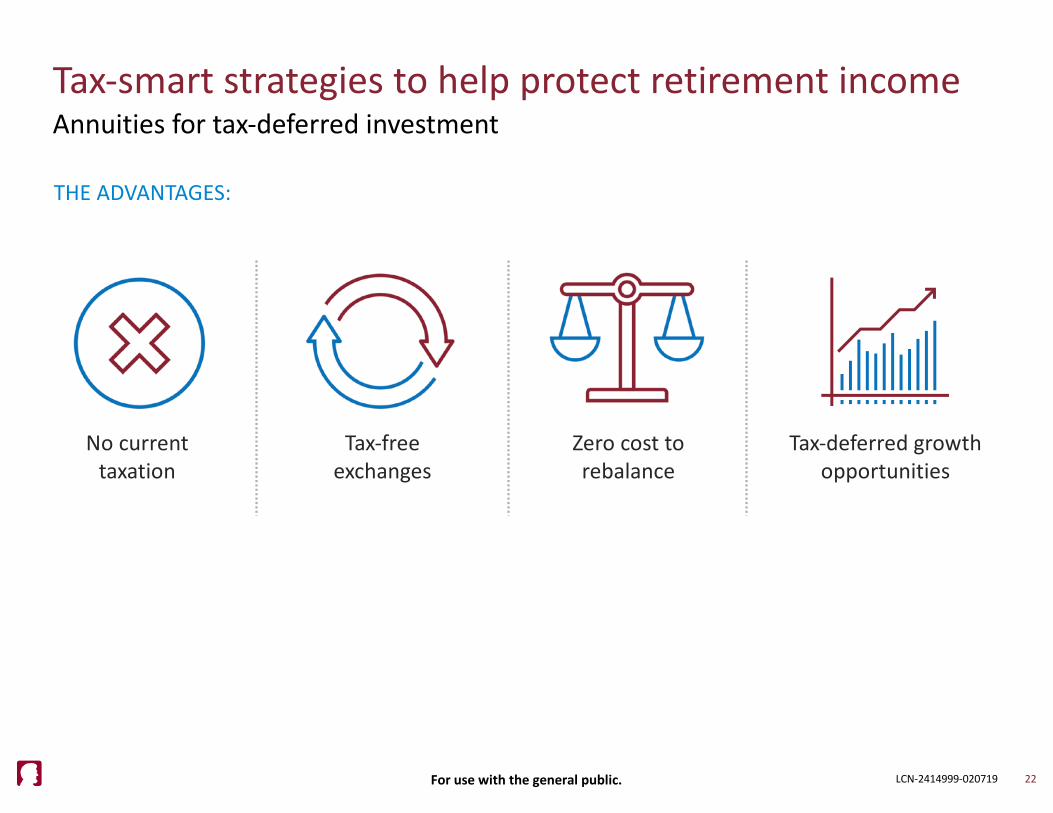

Tax-smart strategies to help protect retirement income

22

Annuities for tax-deferred investment

THE ADVANTAGES:

No current taxation

Tax-free exchanges

Zero cost to rebalance

Tax-deferred growth opportunities

For use with the general public. LCN-2414999-020719

What is a variable annuity?

Variable annuityA long-term investment product that offers tax-deferred growth, a lifetime income

stream, access to leading investment managers, options for guaranteed growth and

income (available for an additional charge), and death benefit protection.

To decide if a variable annuity is right for you, consider that its value will fluctuate; it is

subject to investment risk and possible loss of principal; and there are costs associated

such as mortality and expense, administrative and advisory fees. All guarantees,

including those for optional features, are subject to the claims-paying ability of the

issuer. Limitations and conditions apply.

The power of tax deferralDuring the accumulation phase, earnings in the annuity subaccounts grow tax-deferred.

23

24

For more information on protectingyour wealth from taxes, please call

or meet with your advisor.

For use with the general public. LCN-2414999-020709

For use with the general public. LCN-2414999-020719

Questions?

25

For use with the general public. LCN-2414999-020719

THANK YOU

26

Important disclosures

Not a deposit Not FDIC-insured May go down in value

Not insured by any federal government agencyNot guaranteed by any bank or savings association

Lincoln Financial Group is the marketing name for Lincoln National Corporation and its affiliates.

Affiliates are separately responsible for their own financial and contractual obligations.

LincolnFinancial.com

Order code:

27For use with the general public.

3/19

LFD-ALTX-PPT001

LCN-2414999-020719

Z01

Lincoln Financial Group® affiliates, their distributors, and their respective employees, representatives and/or insurance agents do not provide tax, accounting or legal advice.

Please consult an independent advisor as to any tax, accounting or legal statements made herein.

Variable annuities are long-term investment products designed for retirement purposes and are subject to market fluctuation, investment risk, and possible loss of principal.

Variable annuities contain both investment and insurance components and have fees and charges, including mortality and expense, administrative, and advisory fees. Optional

features are available for an additional charge. The annuity’s value fluctuates with the market value of the underlying investment options, and all assets accumulate tax-

deferred. Withdrawals of earnings are taxable as ordinary income and, if taken prior to age 59½, may be subject to an additional 10% federal tax. Withdrawals will reduce

the death benefit and cash surrender value.

Investors are advised to consider the investment objectives, risks, and charges and expenses of the variable annuity and its underlying investment options carefully before investing. The applicable variable annuity prospectuses contain this and other important information about the variable annuity and its underlying investment options. Please call 888-868-2583 for free prospectuses. Read them carefully before investing or sending money. Products and features are subject to state availability.

Lincoln variable annuities are issued by The Lincoln National Life Insurance Company, Fort Wayne, IN, and distributed by Lincoln Financial Distributors, Inc., a broker-dealer.

The Lincoln National Life Insurance Company does not solicit business in the state of New York, nor is it authorized to do so.

All contract and rider guarantees, including those for optional benefits, fixed subaccount crediting rates, or annuity payout rates, are subject to the claims-paying ability of the issuing insurance company. They are not backed by the broker-dealer or insurance agency from which this annuity is purchased, or any affiliates of those entities other than

the issuing company affiliates, and none makes any representations or guarantees regarding the claims-paying ability of the issuer.

Contracts sold in New York are issued by Lincoln Life & Annuity Company of New York, Syracuse, NY, and distributed by Lincoln Financial Distributors, Inc., a broker-dealer.

There is no additional tax-deferral benefit for an annuity contract purchased in an IRA or other tax-qualified plan.

For use with the general public. LCN-2414999-020719

LincolnFinancial.com

For use with the general public. LCN-2414999-020719