the bright future of the palladium market - lbma 2017/s5_ds.pdf · 3 palladium has become a...

TRANSCRIPT

Denis SharypinHead of Market Research, Nornickel

OCTOBER 16, 2017

BARCELONATHE LBMA/LPPM PRECIOUS METALS CONFERENCE 2017

The Bright Future of the Palladium Market

2

Stagnating Pd Mine Supply

3

Palladium has Become a Co-product of Platinum and Base Metals Mining

Source: Company estimates, Official reports

64%56%

7% 27%

18%7%1% 3%

1% 2%

8% 5%

2005 1H2017

South Africa PGM Miners

Pt Pd Rh Au Cu Ni

51%

27%

23%

26%

13%

30%

12%8%

1%9%

2005 1H2017

Nornickel

Ni Cu Pd Pt Other

Nornickel now is

neither copper,

“Nor Nickel”,

but PGMs

Pd share is equal to

the Ni share for NN

Revenues split by metal

Drivers:• African Pt:Pd output ratio has shifted from 2.0:1 to 1.7:1 in 10 years due to the shift from the Western

Limb to the Eastern and Northern Limbs coupled with higher Zimbabwean output• Higher share of disseminated ores in Norilsk with relatively higher PGM content• Lower Ni and Pt prices, but higher Pd prices

4

2017: Pd Primary Supply is Likely to be Flat or Decrease Slightly

2 618

161 2636 - 2732

2016 2017E

Production Stocks sales Production guidance

-50…-150 koz

NN sales, koz

Guidance range

Sale ofstocks

accumulatedin 2015*

Lower Pd sales by NN in 2017 due to destocking in 2016Flat SA output in 1H 2017. 2H 2017 should be impacted by Bokoni and Maseve closures

Source: Company estimates, SA Statistics Bureau

0

20

40

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

SA PGM production, excl. concentrate from Zimbabwe

2015 2016 2017

tonnes

-1%

Jan-Jul 2017 Y-o-Y

* Metal reserves, created to smooth out the transition to the new configuration of smelting and refining capacities (shutdown of Nickel Plant, increased shipments of nickel matte for processing to Kola MMC and to Harjavalta in Finland) scheduled in 2016, which is expected to result in a one-off increase in work-inprogress in transit and lower output of saleable metals(Nornickel Annual Report 2016)

5

Going Forward: NN – Flat Production Profile, SA – High Risk of Pd Supply Disruptions

0

5

10

15

20

2014 2015 2016 2017 2018 2019 2020

Nornickel CAPEX by mine

Oktyabrskiy mine

Zapolyarniy mine

Komsomolskiy mine (excluding Skalistiy)

Skalisity mine

Taimyrskiy mine

Base production without "expansion" CAPEX

mn

Source: NN estimates as of 2015

0

5

10

15

20

25

FY2008 FY2009 FY2010 FY2011 FY2012 FY2013 FY2014 FY2015 FY2016

SA Producers capital expenditure, billion ZAR

Amplats Impala Lonmin Northam

-12bn ZAR

* Excluding Bystrinsky greenfield copper project with no PGMs; including assets reconfiguration and environmental projectsSource: Company estimates, reports

Nornickel ‘Expansion’ CAPEX ($400 million in 2016*) allows to keep the output profile flat

Deferred CAPEX in SA will lead to a deterioration of the production base

6

Quartile 1 Quartile 2 Quartile 3 Quartile 4

0

5 000

10 000

15 000

20 000

25 000

2017 Producer Operating Costs - ZAR/4E oz CAPEX NCC

2017 YTD Basket (4E) Price - 12 700 ZAR

Additional Pd Supply From SA Would Result in Higher Pt Supply

Source: SFA Oxford, Company data, Consensus forecast (5 participants)

~50% of South African PGM Production is Unprofitable or on the Edge of Loss-Making … but the Pt market is more balanced than the Pd

• SA Producers cannot deliver additional Pd ounces without impacting Pt market• The risk of closures in SA is high

Market Balance Forecast Consensus(before Bokoni and Maseve closing announcements)

-200

-500

240120 150 140

280

-50

-350

-900-1000

-850-950

-1400

2015 2016 2017E 2018E 2019E 2020E 2021E

Pt Pdkoz

7

Palladium Production Growth Opportunities in North America are Limited

Source: Company estimates, Sibanye-Stillwater, NAP official statements

180 koz

-80 koz

Pd-drivenproducers

Pd production asby-product

• Pd output in N. America remains marginal

(14% of global mine production)

• Incremental supply of Pd-driven producers

partly offset by decreasing Pd by-production

from Ni mines

8

Not Only the Operation Cost That Matters

• It takes about 10 years and over US$1 bn to build a sizeable underground mine from scratch

• Increasing capital is required just to maintain production levels due to the ever-deepening nature of the

resources and decreasing metal contents in ore

• Excluding operational costs, producers have a wide range of implicit costs:

• Nornickel Sulphur project is expected to cost up to 3.5 bn USD in 2017-2023

• The new edition of the Mining Charter in South Africa might be enacted by the end of 2017:

• BEE redistribution of the capital

• Revenue taxes for the black communities development

• Procurement via BEE

• REACH and other legislation challenges

9

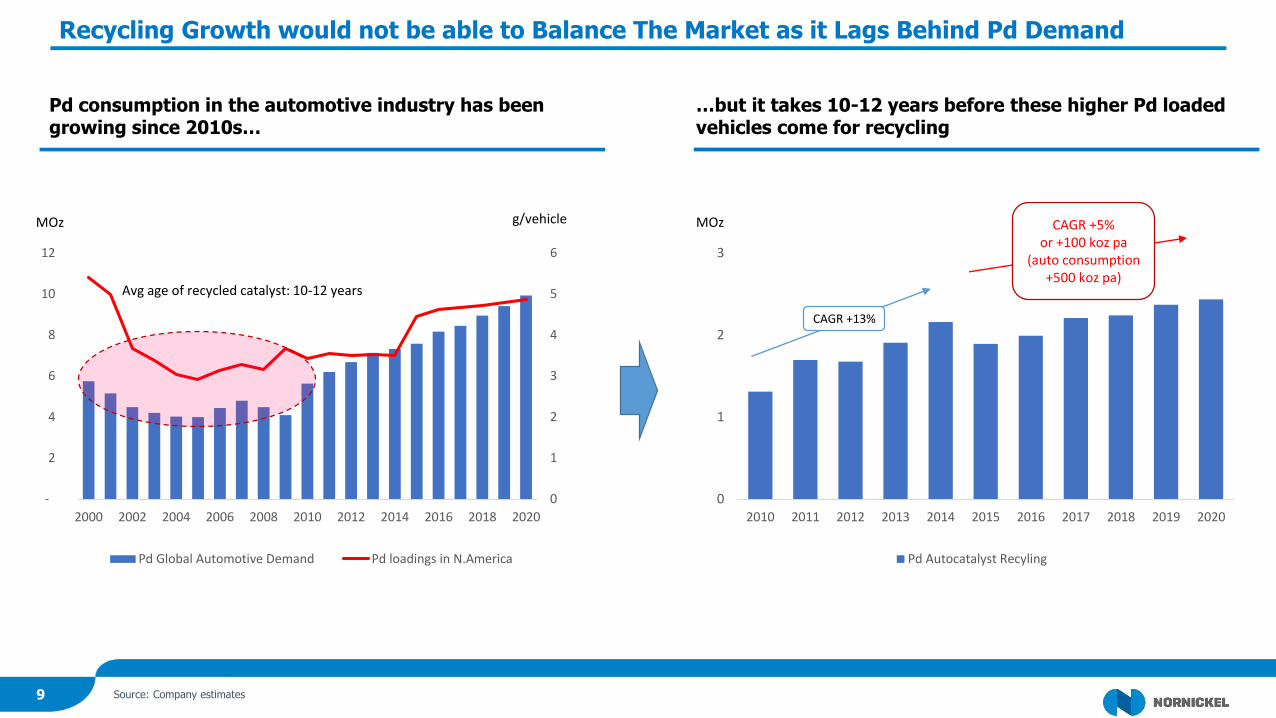

Recycling Growth would not be able to Balance The Market as it Lags Behind Pd Demand

0

1

2

3

4

5

6

-

2

4

6

8

10

12

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Pd Global Automotive Demand Pd loadings in N.America

MOz g/vehicle

Avg age of recycled catalyst: 10-12 years

0

1

2

3

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Pd Autocatalyst Recyling

MOz

CAGR +13%

CAGR +5%or +100 koz pa

(auto consumption +500 koz pa)

Source: Company estimates

Pd consumption in the automotive industry has been growing since 2010s…

…but it takes 10-12 years before these higher Pd loaded vehicles come for recycling

10

Supply

Growing Pd Demand

11

Global Vehicle Production Growth, Emission Legislation and Powertrain Shifts Drive Pd Demand

Production of Pd consuming vehicles to grow +18% by 2025

New environmental regulations, especially in

China, push automakers to increase PGM loadings

Hybridization is a key solution to meet stricter CO2 targets as the diesel

share is falling

Low oil prices and growing share of SUVs result in

engine downsizing termination. Hybrid

displacements are growing

Hybrids contain more Pd per vehicle vs conventional gasoline engines with the

same engine size

BEV is growing from a low base, penetration is limited

(Consensus FC: 5% production share in 2025)

+ 2.5 MOz of additional Pd consumption in auto industry by 2025

12

Supply

Stocks Depleted

13

Available for Consumption Palladium Stocks are Depleting

-2

0

2

4

6

8

1988 1991 1994 1997 2000 2003 2006 2009 2012 2015

Swiss & UK Palladium net trade

CH UK Cumulative total

MOz

outflow

inflow

200

400

600

2012 2013 2014 2015 2016

Palladium NYMEX Stockskoz

Potentially available stocks(price determinant)

Low-elastic stocks

Non-elastic stocks

Source: Swiss Federal Customs Administration, HM Revenue & Customs, Bloomberg, Company estimates

A very clear trend, seen since 2010, confirms that the Pd usage exceeds supply and requires involvement of the stockpiles

Palladium NYMEX stock movement also reflects depletion of on-ground stocks

Existing global stockpiles are not uniformGokhran stocks have depleted*

2013 2014 2015 2016 2017YTD

Deliveries by Gokhran

* According to Analytical agencies reports

14

PGM Market Balance

Metal Stocks, days of consumption Market Balance ForecastMedium-termFundamentals

Palladium

Platinum

(300)

(1000)

(1750)

2016 2017E 2018E

Koz

(480)

(140)(10)

2016 2017E 2018E

Koz Deficit

Balanced

81 51

Jan 2016 Aug 2017

ETF stocks Other non-elastic stocks Other elastic

-2.7moz

122 128

Jan 2016 Aug 2017

ETF stocks Other stocks

+260koz

Source: Company data

15

SupplyNN Palladium Jewellery Program is Suspended

16

Palladium Has Everything to Become a Widely-used Jewellery Metal

Source: Company estimates

Palladium has distinctively strong physical/consumer

characteristics as a jewellery material:

• Established hallmarking

• Hypoallergenic

• No lose of whiteness in everyday wear

• Stronger than gold

• Easy handling

• Easy and quickly removable surface wear

• Lower density

Nornickel’s Palladium Jewellery project was suspended due to:

• The Palladium market has experienced a structural shift since the Jewelry

project was initiated – deficit has become evident, the Pd price is at a

premium to Platinum

• Taking into account the evident market deficits, Nornickel has decided to fully

focus on supplying to the existing customer base

• The Project may be relaunched in case of the appropriate market environment

58%

35%

2%

Au Pt Pd

Share of metals used in jewellery, %

Non-jewellery Jewellery

Range in the last 20 years 50-60% 30-50% 2-20%

17

Thank you!