platinum group minor metals & palladium: this is where the ......platinum group minor metals...

TRANSCRIPT

Platinum Group Minor Metals

& Palladium:

This Is Where The Action IsMatt Watson

Precious Metals Commodity Management LLCJune 16, 2019

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 2

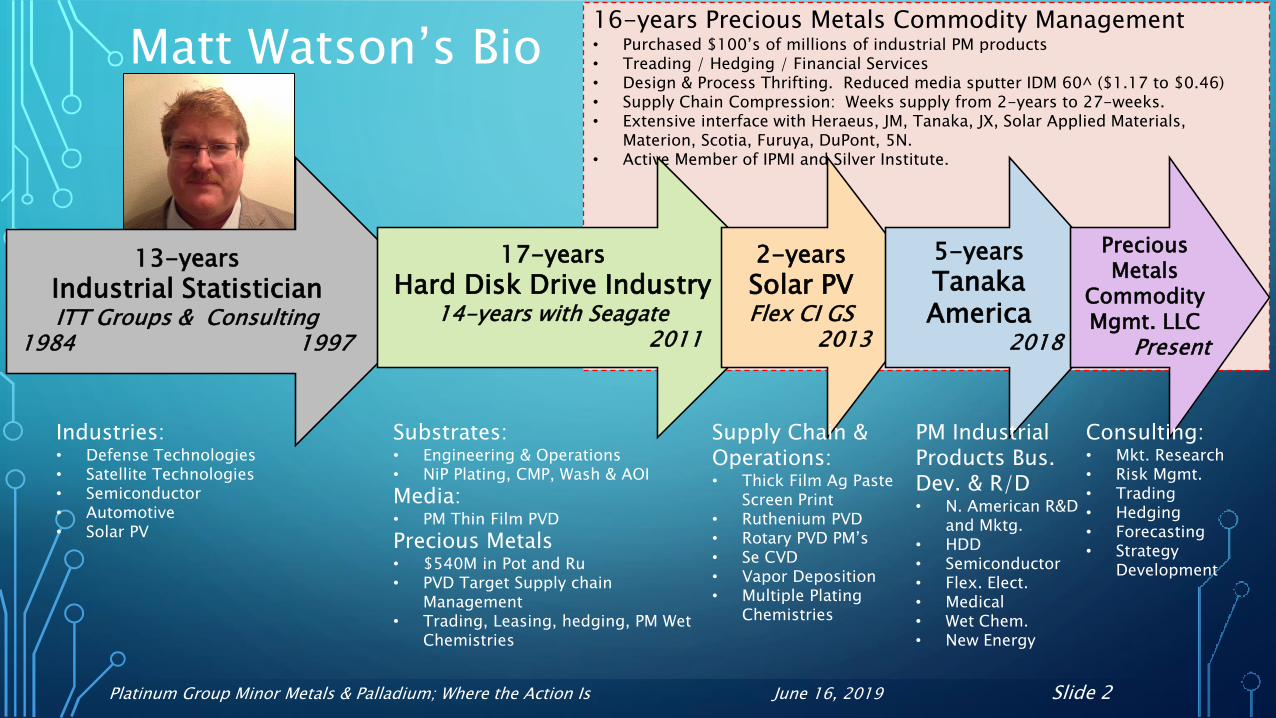

16-years Precious Metals Commodity Management• Purchased $100’s of millions of industrial PM products• Treading / Hedging / Financial Services• Design & Process Thrifting. Reduced media sputter IDM 60^ ($1.17 to $0.46)• Supply Chain Compression: Weeks supply from 2-years to 27-weeks.• Extensive interface with Heraeus, JM, Tanaka, JX, Solar Applied Materials,

Materion, Scotia, Furuya, DuPont, 5N.• Active Member of IPMI and Silver Institute.

Matt Watson’s Bio

13-years

Industrial StatisticianITT Groups & Consulting

1984 1997

Industries:• Defense Technologies• Satellite Technologies• Semiconductor• Automotive• Solar PV

17-years

Hard Disk Drive Industry14-years with Seagate

2011

Substrates:• Engineering & Operations• NiP Plating, CMP, Wash & AOI

Media:• PM Thin Film PVD

Precious Metals• $540M in Pot and Ru• PVD Target Supply chain

Management• Trading, Leasing, hedging, PM Wet

Chemistries

2-years

Solar PVFlex CI GS

2013

Supply Chain & Operations:• Thick Film Ag Paste

Screen Print• Ruthenium PVD• Rotary PVD PM’s• Se CVD• Vapor Deposition• Multiple Plating

Chemistries

5-years

Tanaka America

2018

PM Industrial Products Bus. Dev. & R/D• N. American R&D

and Mktg.• HDD• Semiconductor• Flex. Elect.• Medical• Wet Chem.• New Energy

Precious Metals

Commodity Mgmt. LLC

Present

Consulting:• Mkt. Research• Risk Mgmt.• Trading• Hedging• Forecasting• Strategy

Development

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 3

Precious metals Commodity management

PM Market Research, Hedging Strategies,

Thrifting Strategies, Trading Support, Risk Management

Started August 2018

Utilizing extensive experience in the Precious Metals Commodity markets to help clients make better decision, reduce costs, drive thrifting activities, improve trading performance, reduce risks, create and implement hedging strategies.

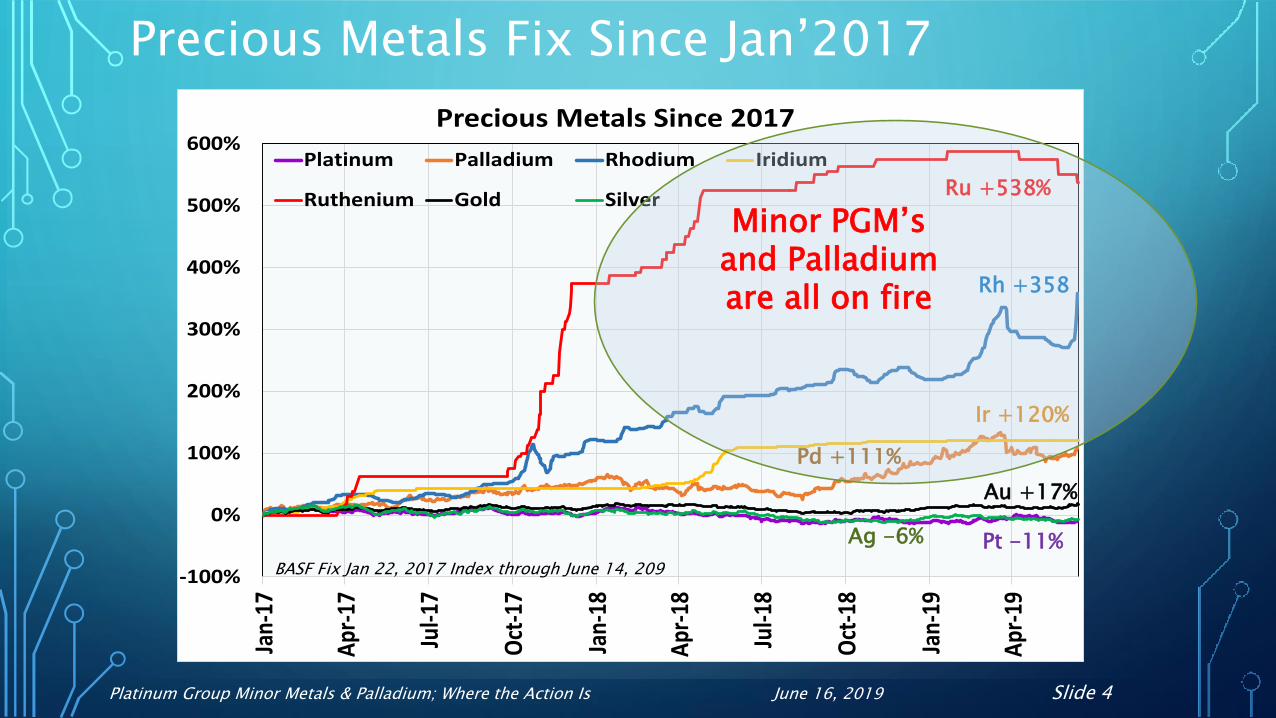

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 4

-100%

0%

100%

200%

300%

400%

500%

600%

Jan-

17

Apr

-17

Jul-1

7

Oct

-17

Jan-

18

Apr

-18

Jul-1

8

Oct

-18

Jan-

19

Apr

-19

Precious Metals Since 2017

Platinum Palladium Rhodium Iridium

Ruthenium Gold Silver

Ag -6% Pt -11%

Ru +538%

Rh +358

Ir +120%

Pd +111%

Au +17%

Minor PGM’s and Palladium are all on fire

Precious Metals Fix Since Jan’2017

BASF Fix Jan 22, 2017 Index through June 14, 209

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 5

-

200

400

600

800

1,000

1,200

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

f

Mill

ion

s To

z

Global Mined Precious Metals (Toz)

Gold Silver Platinum Paladium Rhodium Ruthenium Iridium Osmium

Silver #1 Abundance

Gold #2 Abundance

All 6 PGM’s Combined – Trivial Abundance

-

10

20

30

40

50

60

70

80

90

100

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019f

Mil

lio

ns

Toz

Global Precious Metals Recycle (Toz)

Gold Silver Platinum Paladium Rhodium Ruthenium Iridium Osmium

Silver Recycle

Gold Recycle Volume

Mined Volume Recycled Volume

Mined & Recycle Precious Metals Volume

PGM’s Recycle

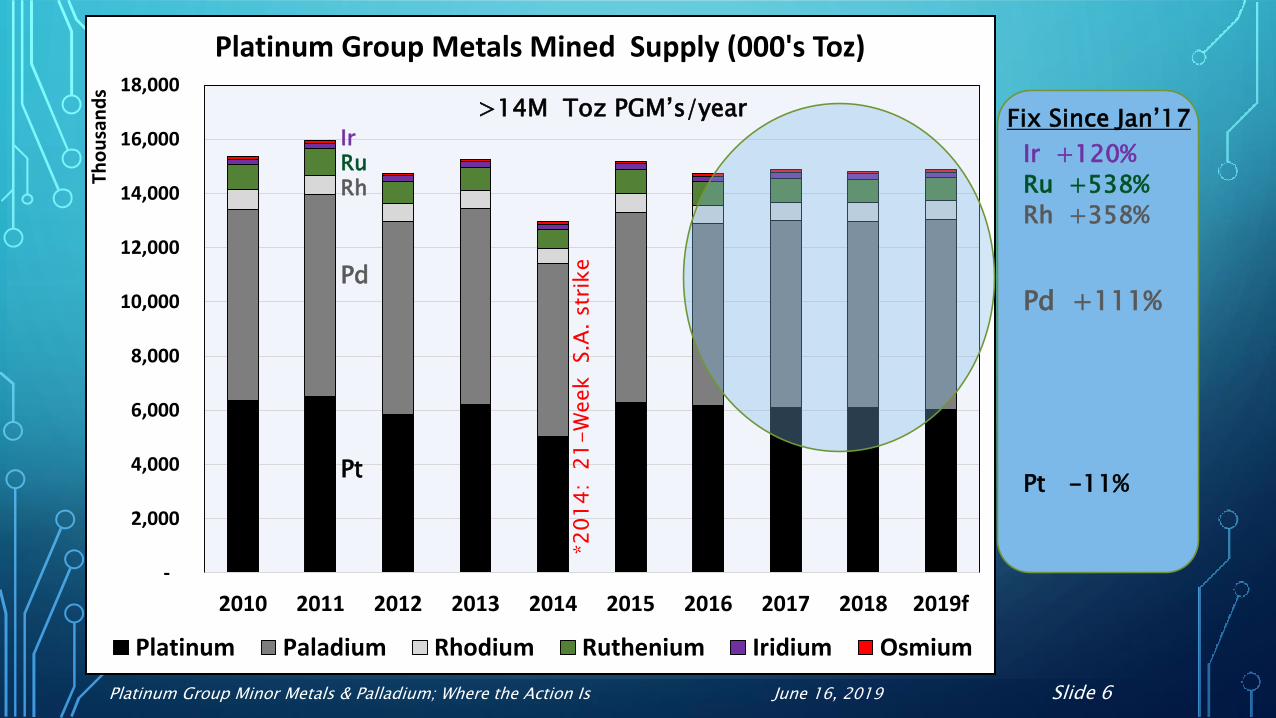

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 6

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019f

Tho

usa

nd

s

Platinum Group Metals Mined Supply (000's Toz)

Platinum Paladium Rhodium Ruthenium Iridium Osmium

>14M Toz PGM’s/year

*2014:

21

-W

eek

S.A

. str

ike

Pd

RhRuIr

Pt

Pd +111%

Rh +358%

Ru +538%

Ir +120%

Pt -11%

Fix Since Jan’17

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 7

Palladium & The PGM MinorsRhodium, Ruthenium and Iridium

• Palladium & Rhodium• Both 85%+ of supply towards top demand category - auto catalyst

• Tightness in the global auto catalyst smelting capacity is a new concern to meeting short

term demand

• Big Auto OEM’s working to finalize Pt Pd design swaps in gasoline catalyst designs.

Swaps likely starting in 2022-23 to leaner Pd designs.

• Ruthenium • Recent surge in secondary production meeting what would otherwise be a structural

deficit.

• Iridium • Near market balance

• O/L for more demand from several categories.

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 8

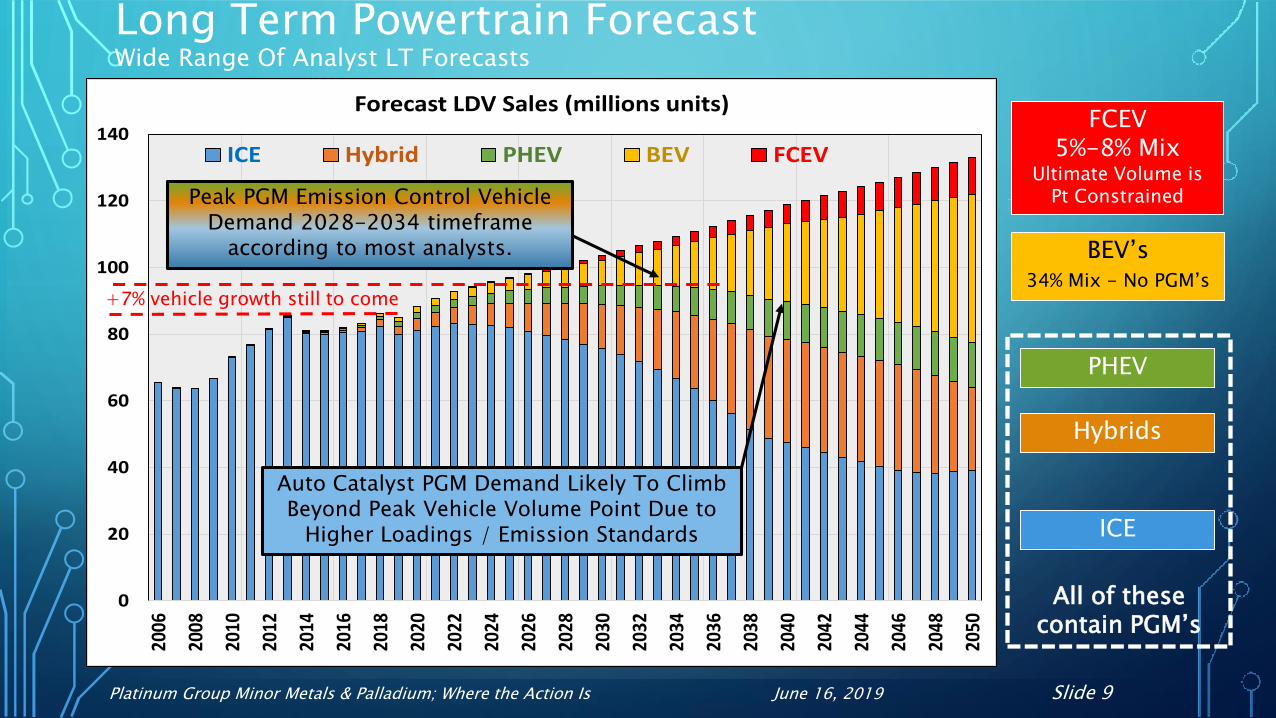

Previous IPMI Auto Catalyst Seminar Highlights

Increasing vehicle sales over next decade

Tightening vehicle emission standards - continuous

NOx standards are dramatically lower – impacts Rh

Much more stringent RDE (Real World) testing conditions – EU & China

Transition from LDV Diesel to Hybrids (Reduced Pt more Pd), but Hybrids

use 0%-15%+ or more PGM’s

Emerging BEV market (No PGM’s)

PGM Demand Impact

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 9

Long Term Powertrain ForecastWide Range Of Analyst LT Forecasts

0

20

40

60

80

100

120

140

2006

2008

2010

2012

2014

2016

2018

2020

2022

2024

2026

2028

2030

2032

2034

2036

2038

2040

2042

2044

2046

2048

2050

Forecast LDV Sales (millions units)

ICE Hybrid PHEV BEV FCEV

FCEV 5%-8% Mix

Ultimate Volume is Pt Constrained

BEV’s 34% Mix - No PGM’s

PHEV

Hybrids

ICE

Auto Catalyst PGM Demand Likely To Climb Beyond Peak Vehicle Volume Point Due to

Higher Loadings / Emission Standards

Peak PGM Emission Control Vehicle Demand 2028-2034 timeframe

according to most analysts.

+7% vehicle growth still to come

All of these contain PGM’s

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 10

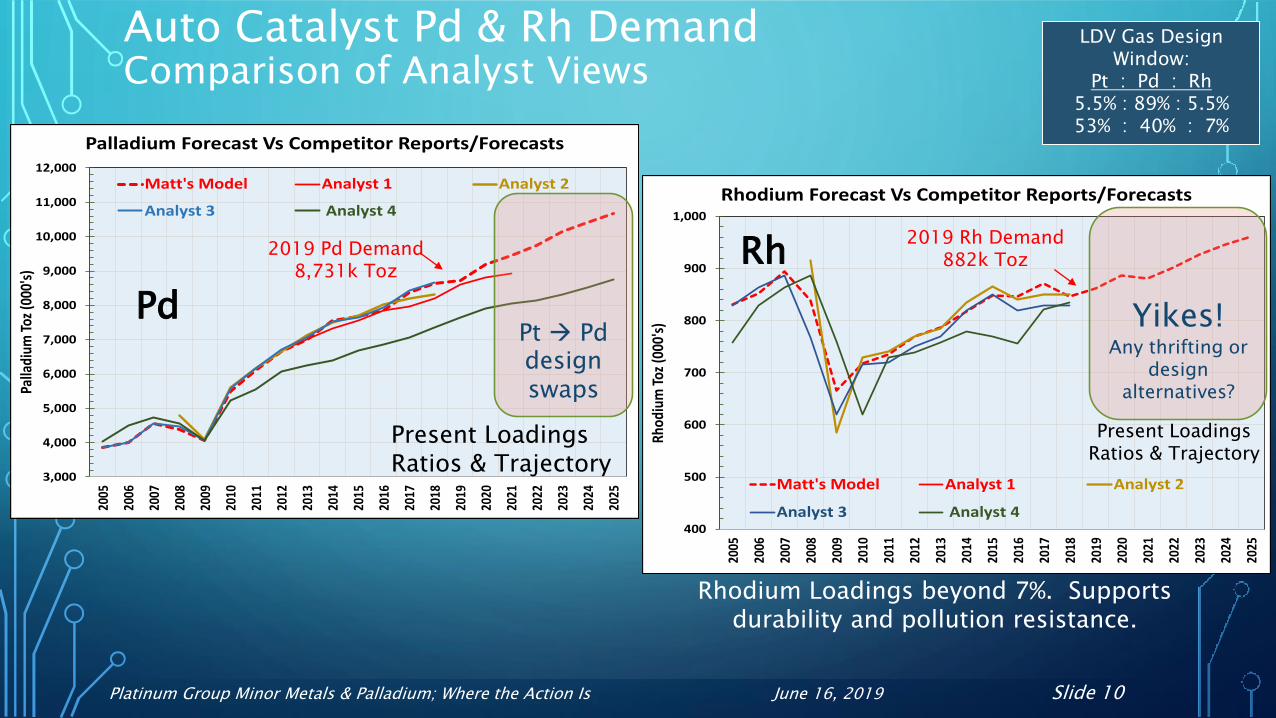

Auto Catalyst Pd & Rh Demand Comparison of Analyst Views

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

Palla

dium

Toz

(000

's)

Palladium Forecast Vs Competitor Reports/Forecasts

Matt's Model Analyst 1 Analyst 2

Analyst 3 Analyst 4

LDV Gas Design Window:

Pt : Pd : Rh5.5% : 89% : 5.5%53% : 40% : 7%

Pt Pddesign swaps

Present Loadings Ratios & Trajectory

2019 Pd Demand 8,731k Toz

400

500

600

700

800

900

1,000

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

Rhod

ium

Toz

(000

's)

Rhodium Forecast Vs Competitor Reports/Forecasts

Matt's Model Analyst 1 Analyst 2

Analyst 3 Analyst 4

Yikes!Any thrifting or

design alternatives?

Present Loadings Ratios & Trajectory

2019 Rh Demand 882k Toz

Pd

Rh

Rhodium Loadings beyond 7%. Supports durability and pollution resistance.

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 11

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

200

400

600

800

1,000

1,200

1,400

19

75

19

77

19

79

19

81

19

83

19

85

19

87

19

89

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

20

07

20

09

20

11

20

13

20

15

20

17

20

19

f

20

21

f

20

23

f

20

25

f

Rh

od

ium

De

man

d %

of Su

pp

lyRh

od

ium

Su

pp

ly (

00

0's

To

z)

Rhodium Autocat Demand as Percent of Supply

Rh Mined Supply

Rh Recycle

Rh Demand % Supply

PGM Total Supply Since 1980 Illustrating PGM Mining Growth + Importance of Recycle

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

19

75

19

77

19

79

19

81

19

83

19

85

19

87

19

89

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

20

07

20

09

20

11

20

13

20

15

20

17

20

19

f

20

21

f

20

23

f

20

25

f

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Pa

lla

diu

m S

up

ply

(0

00

's T

oz)

Pa

llad

ium

De

ma

nd

% O

f Sup

ply

Palladium Autocat Demand as Percent of Supply

Pd Mined Supply Pd Recycle

Pd Demand % Supply

Pd Rh

Pd Mining growth from Russia, N. America, &

Zimbabwe,. SA decline.SA dominate mined supply will taper off without more

mining projects.

Global Pd & RH Auto Catalyst Recycle Risks Will Likely Further Increase Overall Supply Risk

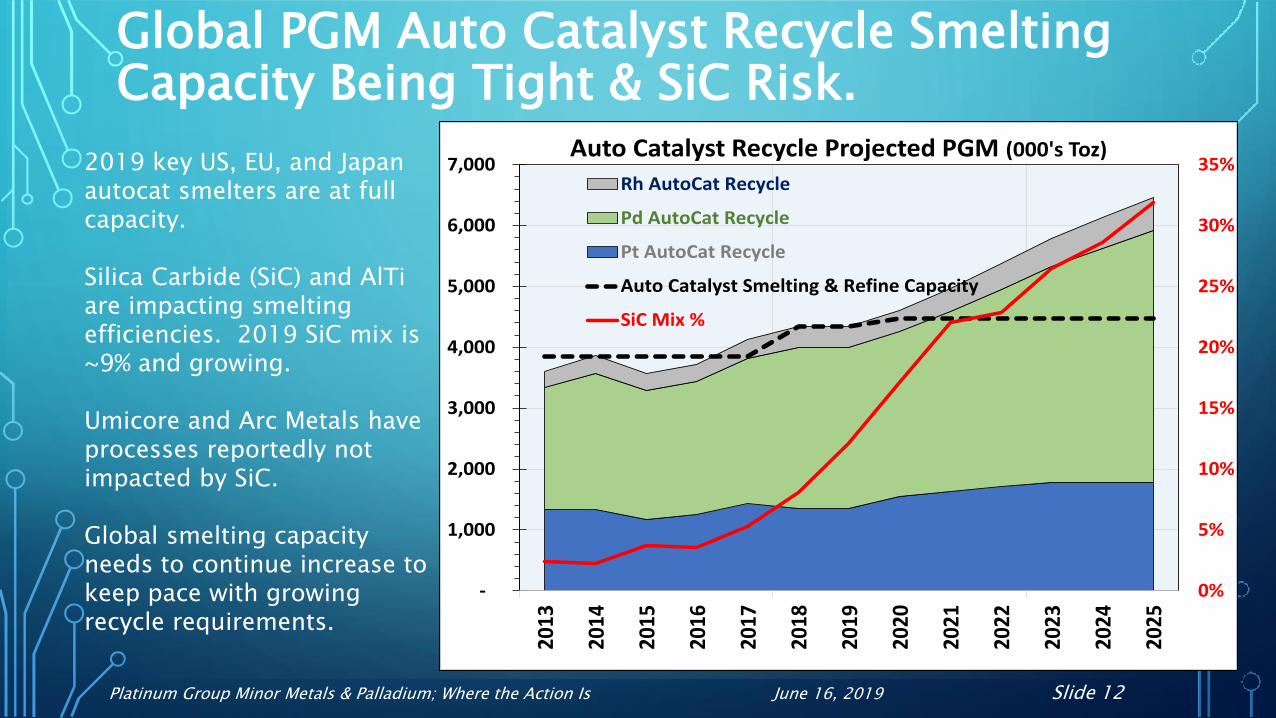

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 12

0%

5%

10%

15%

20%

25%

30%

35%

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

Auto Catalyst Recycle Projected PGM (000's Toz)

Rh AutoCat Recycle

Pd AutoCat Recycle

Pt AutoCat Recycle

Auto Catalyst Smelting & Refine Capacity

SiC Mix %

Global PGM Auto Catalyst Recycle Smelting Capacity Being Tight & SiC Risk.

2019 key US, EU, and Japan autocat smelters are at full capacity.

Silica Carbide (SiC) and AlTiare impacting smelting efficiencies. 2019 SiC mix is ~9% and growing.

Umicore and Arc Metals have processes reportedly not impacted by SiC.

Global smelting capacity needs to continue increase to keep pace with growing recycle requirements.

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 13

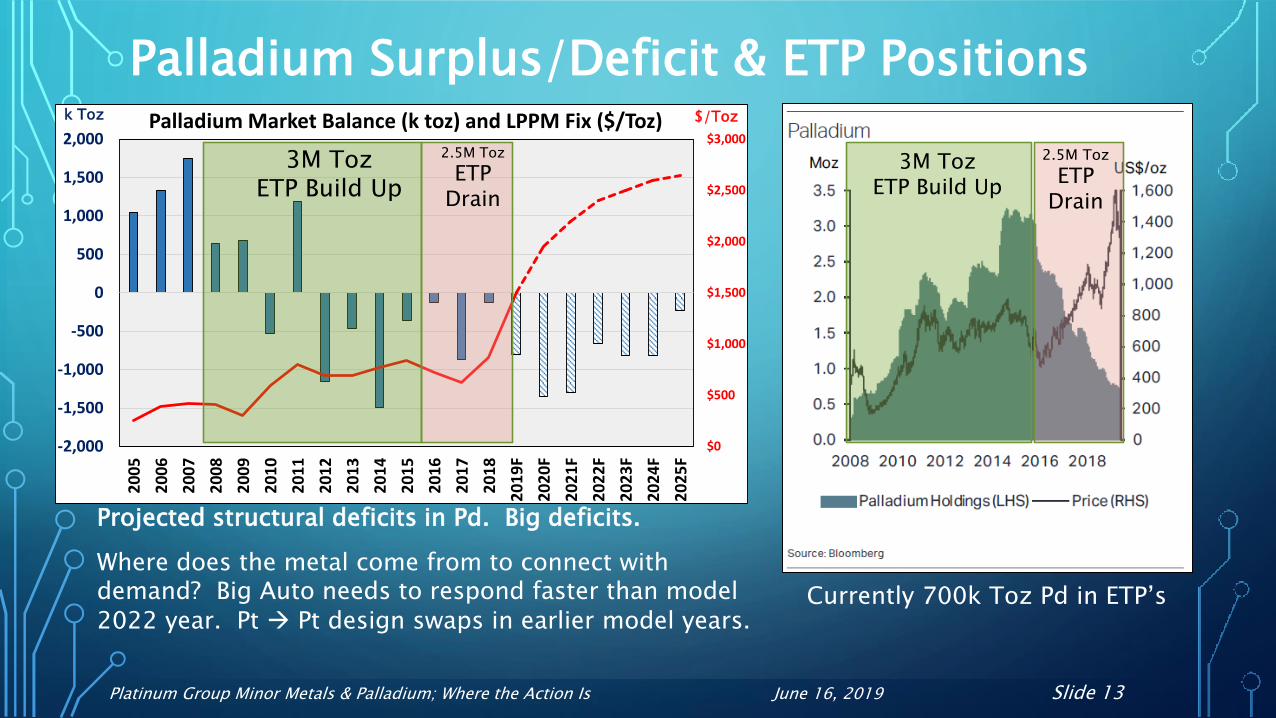

Palladium Surplus/Deficit & ETP Positions

Currently 700k Toz Pd in ETP’s

Projected structural deficits in Pd. Big deficits.

Where does the metal come from to connect with demand? Big Auto needs to respond faster than model 2022 year. Pt Pt design swaps in earlier model years.

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

-2,000

-1,500

-1,000

-500

0

500

1,000

1,500

2,0002

00

5

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

F

20

20

F

20

21

F

20

22

F

20

23

F

20

24

F

20

25

F

Palladium Market Balance (k toz) and LPPM Fix ($/Toz)

3M TozETP Build Up

2.5M Toz

ETP Drain

2.5M Toz

ETP Drain

3M TozETP Build Up

$/Tozk Toz

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 14

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

(350)

(300)

(250)

(200)

(150)

(100)

(50)

-

50

100

1502

00

1

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

F

20

20

F

20

21

F

20

22

F

20

23

F

20

24

F

20

25

F

Rhodium Market Balance (k toz) and BASF Fix ($/Toz)

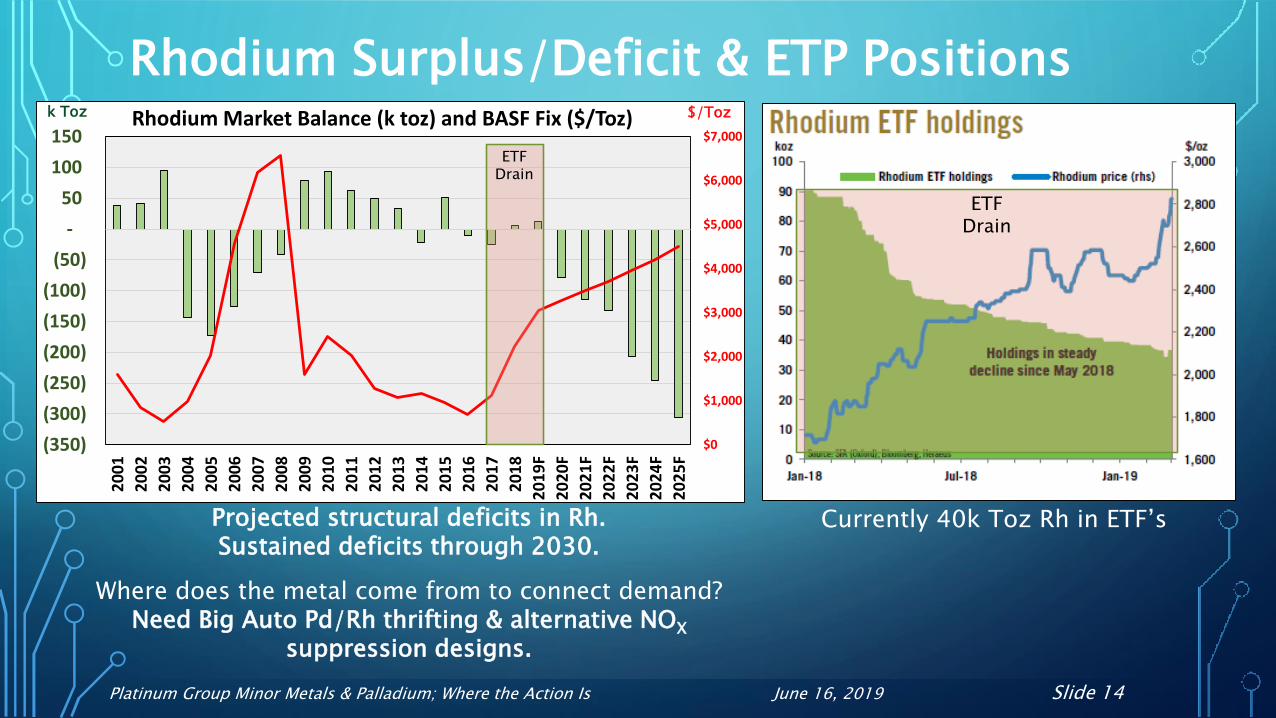

Rhodium Surplus/Deficit & ETP Positions

Currently 40k Toz Rh in ETF’sProjected structural deficits in Rh. Sustained deficits through 2030.

Where does the metal come from to connect demand? Need Big Auto Pd/Rh thrifting & alternative NOX

suppression designs.

$/Tozk Toz

ETFDrain

ETFDrain

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 15

Palladium & The PGM MinorsRhodium, Ruthenium and Iridium

• Palladium & Rhodium• Both 85%+ of supply towards top demand category - auto catalyst

• Tightness in the global auto catalyst smelting capacity is a new concern to meeting short

term demand

• Big Auto OEM’s working to finalize Pt Pd design swaps in gasoline catalyst designs.

Swaps likely starting in 2022-23 to leaner Pd designs.

• Ruthenium • Recent surge in secondary production meeting what would otherwise be a structural

deficit.

• Iridium • Near market balance

• O/L for more demand from several categories.

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 16

S. African Bushveld Complex

Rustenberg

Kroondall

Mototolo

Marula

Lease Area

Planned slowdown 2020-2027 leading to EOL maintenance mode

Most near term EOL slowdowns and shutdowns on UG2 Reef

Prill Table Reef Summary

Prill Table Reef SummaryTwo new S. African mines by 2025

Zimbabwe low minor PGM content too.

1 : 4.2

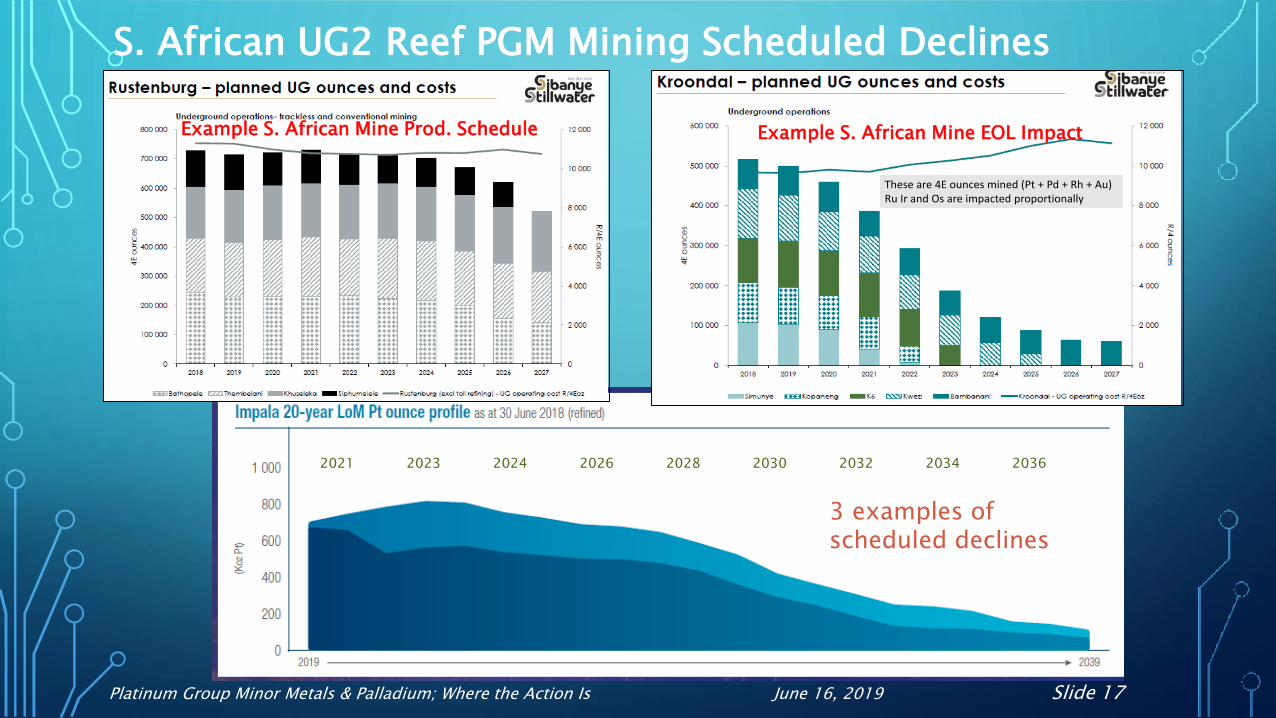

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 17

These are 4E ounces mined (Pt + Pd + Rh + Au)Ru Ir and Os are impacted proportionally

S. African UG2 Reef PGM Mining Scheduled Declines

Example S. African Mine EOL ImpactExample S. African Mine Prod. Schedule

2021 2023 2024 2026 2028 2030 2032 2034 2036

3 examples of scheduled declines

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 18

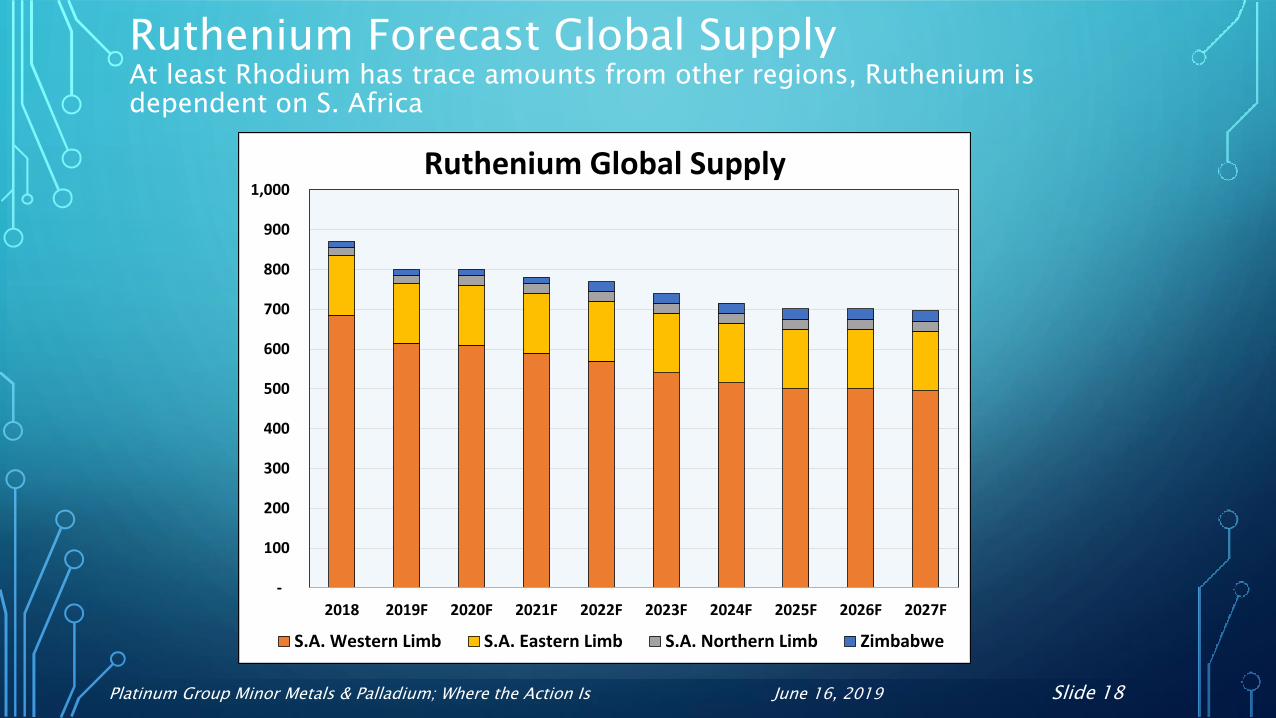

Ruthenium Forecast Global SupplyAt least Rhodium has trace amounts from other regions, Ruthenium is dependent on S. Africa

-

100

200

300

400

500

600

700

800

900

1,000

2018 2019F 2020F 2021F 2022F 2023F 2024F 2025F 2026F 2027F

Ruthenium Global Supply

S.A. Western Limb S.A. Eastern Limb S.A. Northern Limb Zimbabwe

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 19

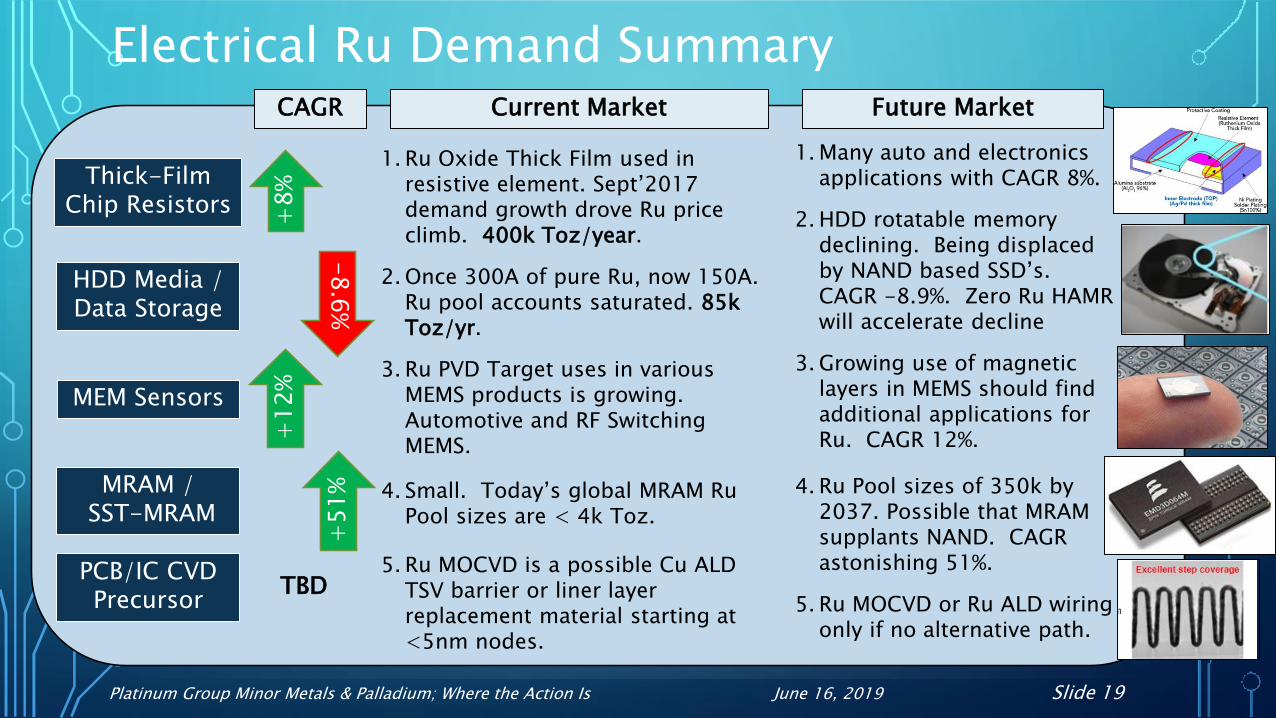

Electrical Ru Demand Summary

-8

.6%

+8

%+

12

%

Thick-Film Chip Resistors

MEM Sensors

HDD Media / Data Storage

MRAM /SST-MRAM

Current Market Future MarketCAGR

1. Ru Oxide Thick Film used in resistive element. Sept’2017 demand growth drove Ru price climb. 400k Toz/year.

2. Once 300A of pure Ru, now 150A. Ru pool accounts saturated. 85k Toz/yr.

3. Ru PVD Target uses in various MEMS products is growing. Automotive and RF Switching MEMS.

4. Small. Today’s global MRAM Ru Pool sizes are < 4k Toz.

5. Ru MOCVD is a possible Cu ALD TSV barrier or liner layer replacement material starting at <5nm nodes.

1. Many auto and electronics applications with CAGR 8%.

2. HDD rotatable memory declining. Being displaced by NAND based SSD’s. CAGR -8.9%. Zero Ru HAMR will accelerate decline

3. Growing use of magnetic layers in MEMS should find additional applications for Ru. CAGR 12%.

4. Ru Pool sizes of 350k by 2037. Possible that MRAM supplants NAND. CAGR astonishing 51%.

5. Ru MOCVD or Ru ALD wiring only if no alternative path.

+5

1%

PCB/IC CVD Precursor

TBD

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 20

Ruthenium Price History – Why Did this Happen?

HDD PMR Transition

HDD Pure Ru Refill

Transition

Ru Thick Film Resistor Boom 2027

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 21

-

200

400

600

800

1,000

1,200

1,400

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

f

2020

f

2021

f

2022

f

2023

f

2024

f

2025

f

2026

f

2027

f

2028

f

Thou

sand

s

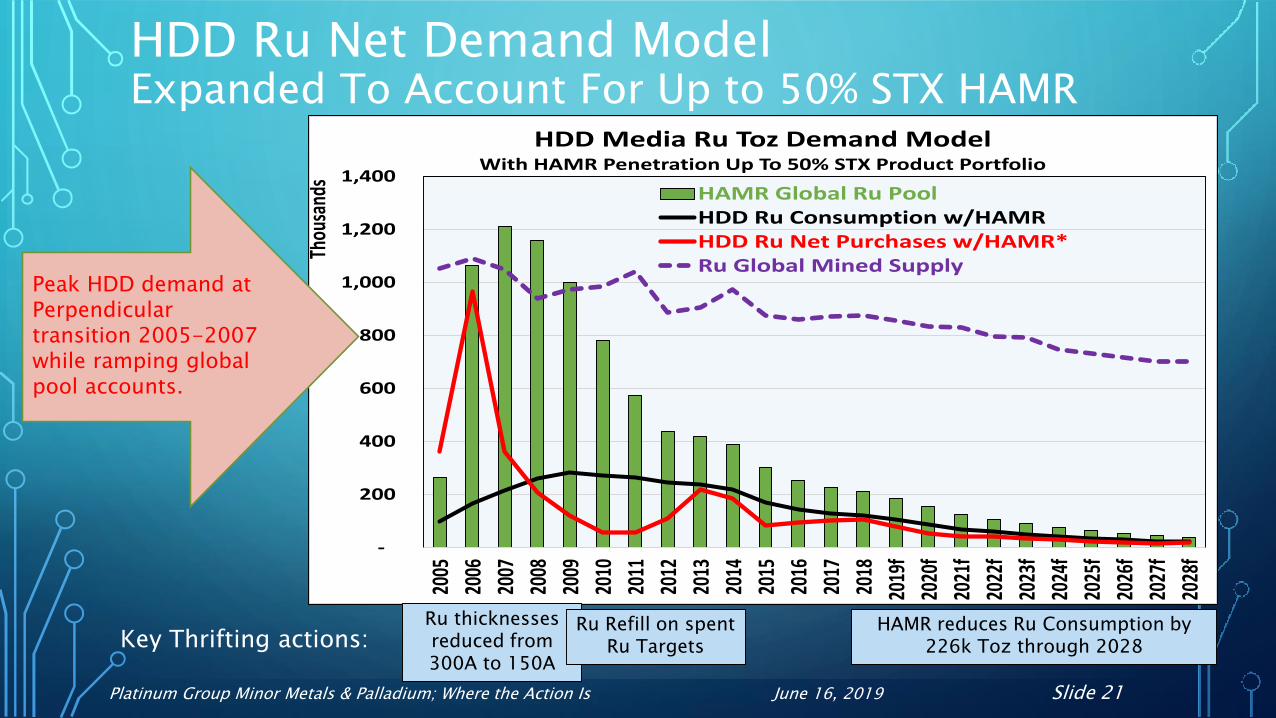

HDD Media Ru Toz Demand ModelWith HAMR Penetration Up To 50% STX Product Portfolio

HAMR Global Ru PoolHDD Ru Consumption w/HAMRHDD Ru Net Purchases w/HAMR*Ru Global Mined Supply

HDD Ru Net Demand Model Expanded To Account For Up to 50% STX HAMR

HAMR reduces Ru Consumption by 226k Toz through 2028

Peak HDD demand at Perpendicular transition 2005-2007 while ramping global pool accounts.

Ru thicknesses reduced from 300A to 150A

Ru Refill on spent Ru TargetsKey Thrifting actions:

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 22

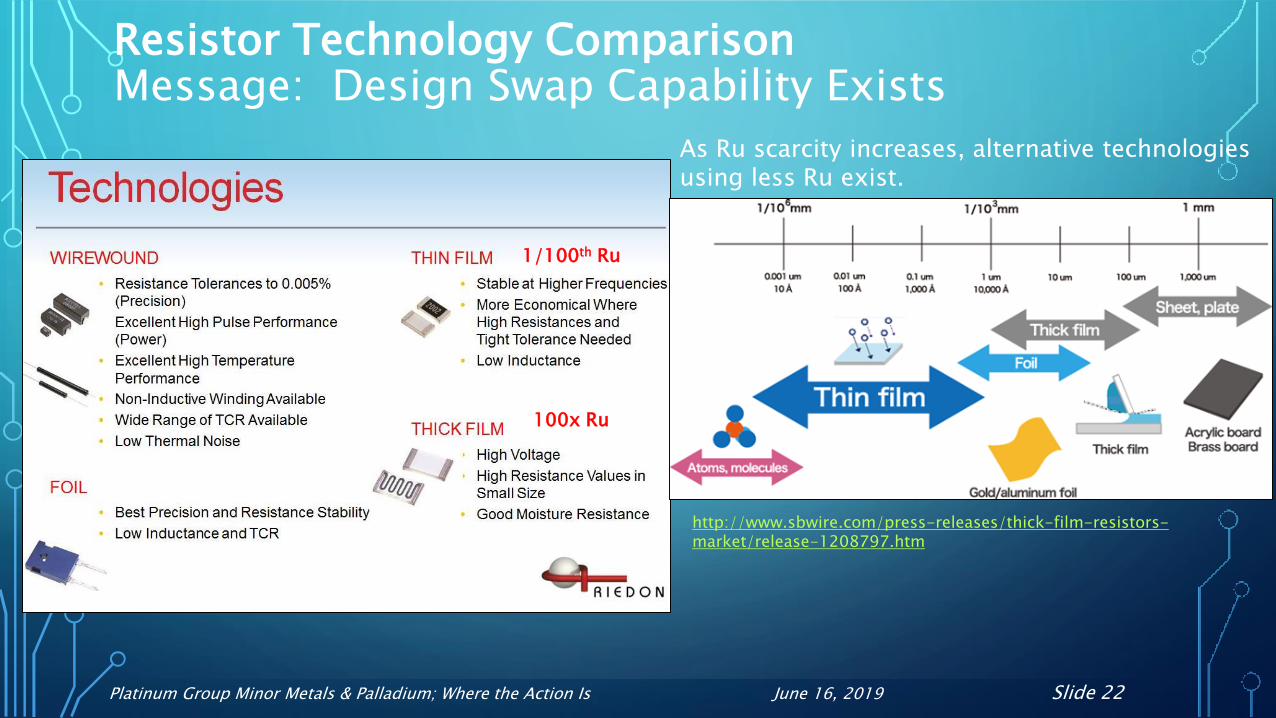

Resistor Technology ComparisonMessage: Design Swap Capability Exists

http://www.sbwire.com/press-releases/thick-film-resistors-market/release-1208797.htm

1/100th Ru

100x Ru

As Ru scarcity increases, alternative technologies using less Ru exist.

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 23

Chemical Ru Demand Summary

+8

%+

9%

Caprolactam / Nylon

Acetic Acid

Current Market Future MarketCAGR

1. Demand for compound is ~5 million tons per year, and the vast majority is used to make Nylon 6 filament, fiber, and plastics.

2. Acetic acid demand is 17,808 kilo metric tones in 2019. Used in rubber, plastics, pharmaceutical, construction, paint & other app’s.

3. Ammonia synthesize using Ru NanoParticle Catalyst.

4. Catalyst used in electrolysis for hydrogen production.

1. $14.9 billion by 2019, CAGR 8.1% through 2022 with increasing auto, CE and electronic applications.

2. $11.6 billion by 2019 with CAGR of 8.7%. One risk of decline is the environmental efforts to reduce plastics.

3. Significant technology conversion for cost will grow this application 9% CAGR.

4. $200 billion by 2025 @ 6.1% CAGR. Upside growth possible.

Ammonia Catalyst +

9%

Ru Catalyst

H2 Electrolysis Catalyst

+6%

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 24

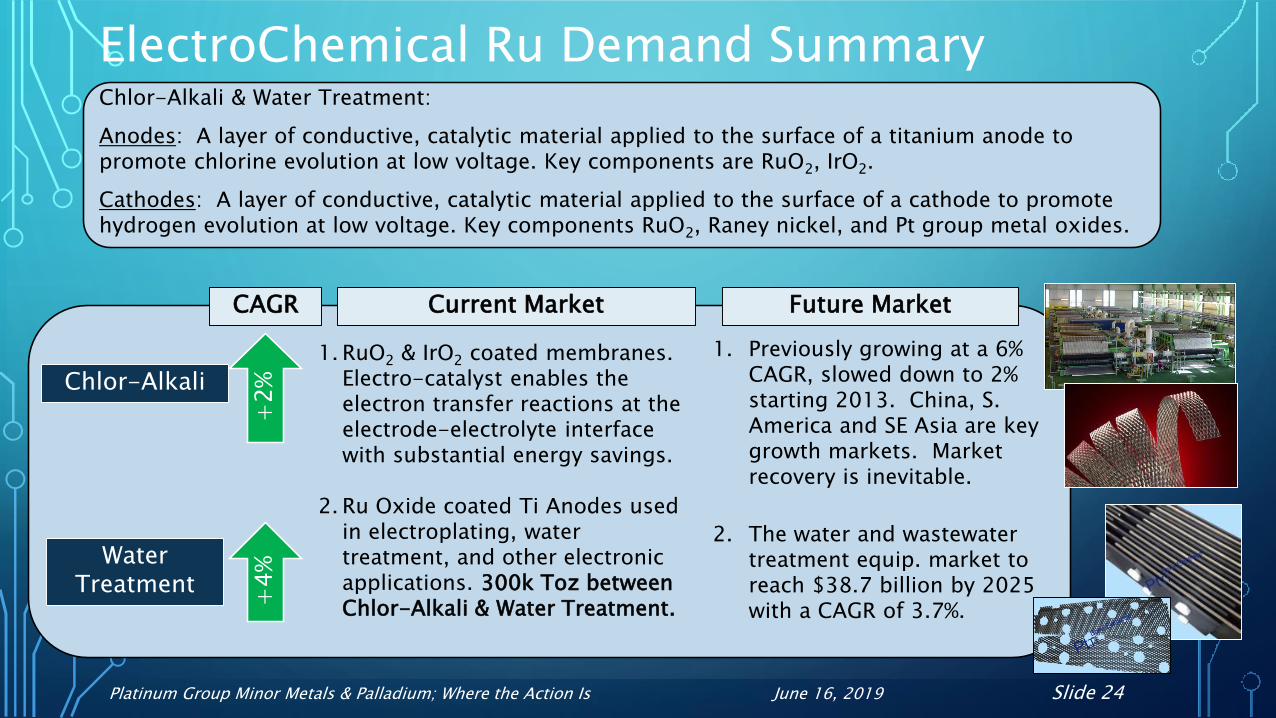

ElectroChemical Ru Demand Summary

+2

%+

4%

Chlor-Alkali

Chlor-Alkali & Water Treatment:

Anodes: A layer of conductive, catalytic material applied to the surface of a titanium anode to promote chlorine evolution at low voltage. Key components are RuO2, IrO2.

Cathodes: A layer of conductive, catalytic material applied to the surface of a cathode to promote hydrogen evolution at low voltage. Key components RuO2, Raney nickel, and Pt group metal oxides.

Water Treatment

Current Market Future MarketCAGR

1. RuO2 & IrO2 coated membranes. Electro-catalyst enables the electron transfer reactions at the electrode-electrolyte interface with substantial energy savings.

2. Ru Oxide coated Ti Anodes used in electroplating, water treatment, and other electronic applications. 300k Toz between Chlor-Alkali & Water Treatment.

1. Previously growing at a 6% CAGR, slowed down to 2% starting 2013. China, S. America and SE Asia are key growth markets. Market recovery is inevitable.

2. The water and wastewater treatment equip. market to reach $38.7 billion by 2025 with a CAGR of 3.7%.

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 25

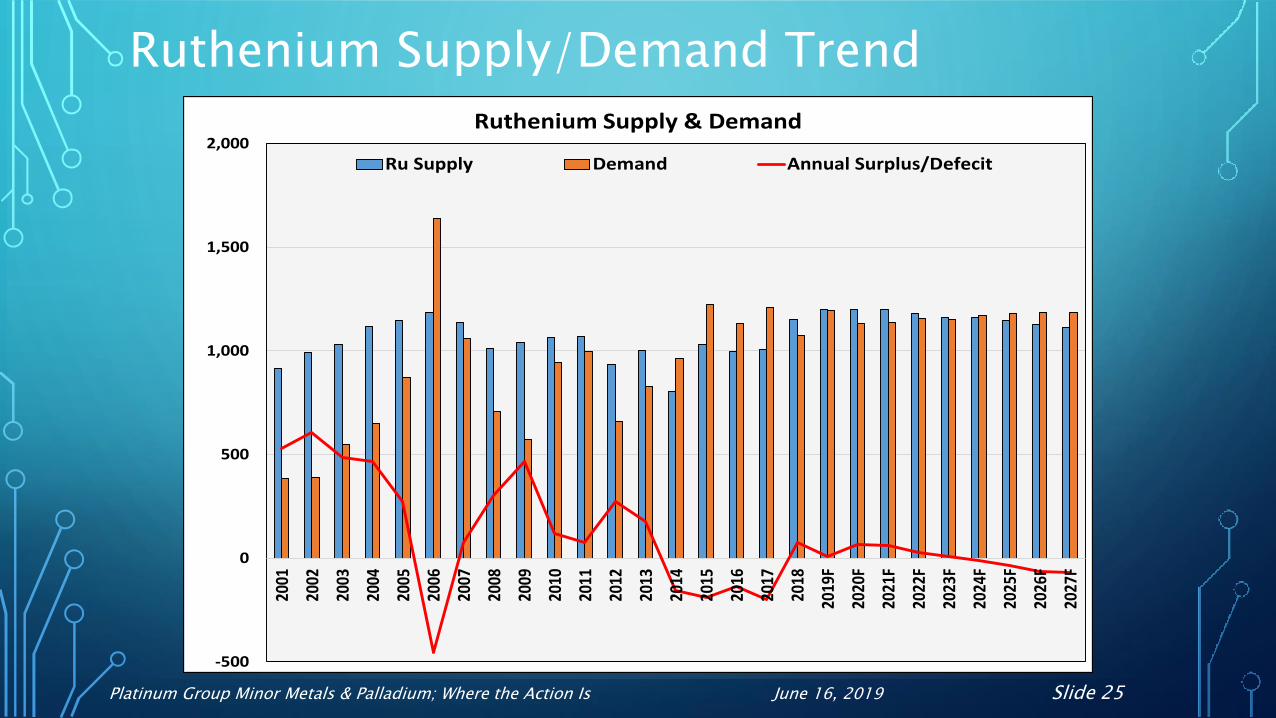

Ruthenium Supply/Demand Trend

-500

0

500

1,000

1,500

2,000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

F

2020

F

2021

F

2022

F

2023

F

2024

F

2025

F

2026

F

2027

F

Ruthenium Supply & Demand

Ru Supply Demand Annual Surplus/Defecit

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 26

Ruthenium – Why Such Liquid Physical Supply?

• Several large PGM trading firms with on-hand inventories of Ru.

1. Growing industrial demand

2. Oct’2017 Thick Film Resistors surge.

3. Dec’2017 surge in Japan industrial Ru buys.

4. Secondary Ru Refine Expansion and Movement of excess Ru positions.

5. Mined concentrate refining in Japan

12

3

45

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 27

Ru Market Complication: 2017-18 HDD Ru Target Supply Chain Realignment

• Ruthenium PVD Target Market Disruption

• Exit Heraeus Tuas Singapore HDD Target Div. – sold Chinese firm Vital.

• Solar Applied Materials Technology - $100M financial loss, reset of the

business and management team. Is it worth it to do business with

Solar?

• Furuya Metals – sudden dominate sole source with capacity limits and

unwillingness to support some Ru Alloys.

• Need for Ru Refill on pure Ru for cost/thrifting.

• Tanaka Tsukuba factory entry into the Ru Alloy PVD market.

• Materion re-entry into limited HDD Ru target support.

• Materion suffered from a devastating Ru Refine Si Contamination

issue in 2007/8.

#1

HDD Ru PVD Secondary RefineMoving The Lawn Chairs

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 28

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

F

2020

F

2021

F

2022

F

2023

F

2024

F

2025

F

2026

F

2027

F

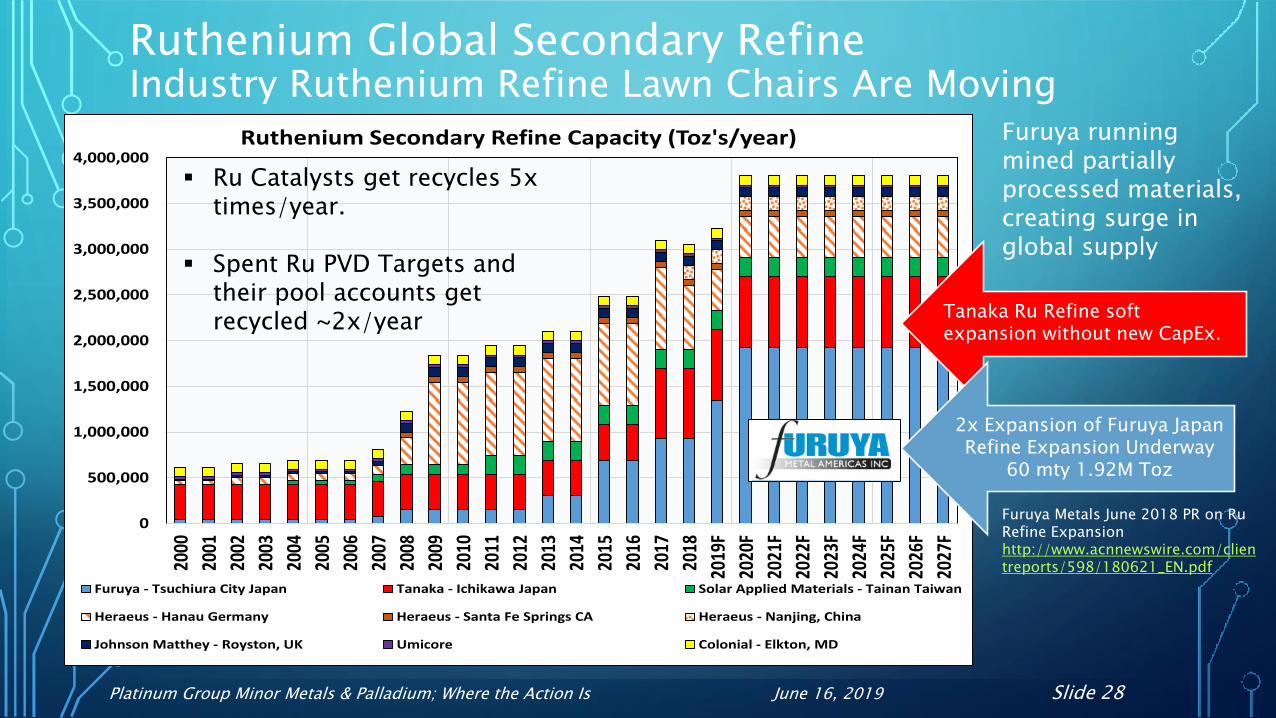

Ruthenium Secondary Refine Capacity (Toz's/year)

Furuya - Tsuchiura City Japan Tanaka - Ichikawa Japan Solar Applied Materials - Tainan Taiwan

Heraeus - Hanau Germany Heraeus - Santa Fe Springs CA Heraeus - Nanjing, China

Johnson Matthey - Royston, UK Umicore Colonial - Elkton, MD

Ruthenium Global Secondary RefineIndustry Ruthenium Refine Lawn Chairs Are Moving

Tanaka Ru Refine soft expansion without new CapEx.

2x Expansion of Furuya Japan Refine Expansion Underway

60 mty 1.92M Toz

Ru Catalysts get recycles 5x times/year.

Spent Ru PVD Targets and their pool accounts get recycled ~2x/year

Furuya Metals June 2018 PR on Ru Refine Expansionhttp://www.acnnewswire.com/clientreports/598/180621_EN.pdf

Furuya running mined partially processed materials, creating surge in global supply

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 29

(500)

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

F

2020

F

2021

F

2022

F

2023

F

2024

F

2025

F

2026

F

2027

F

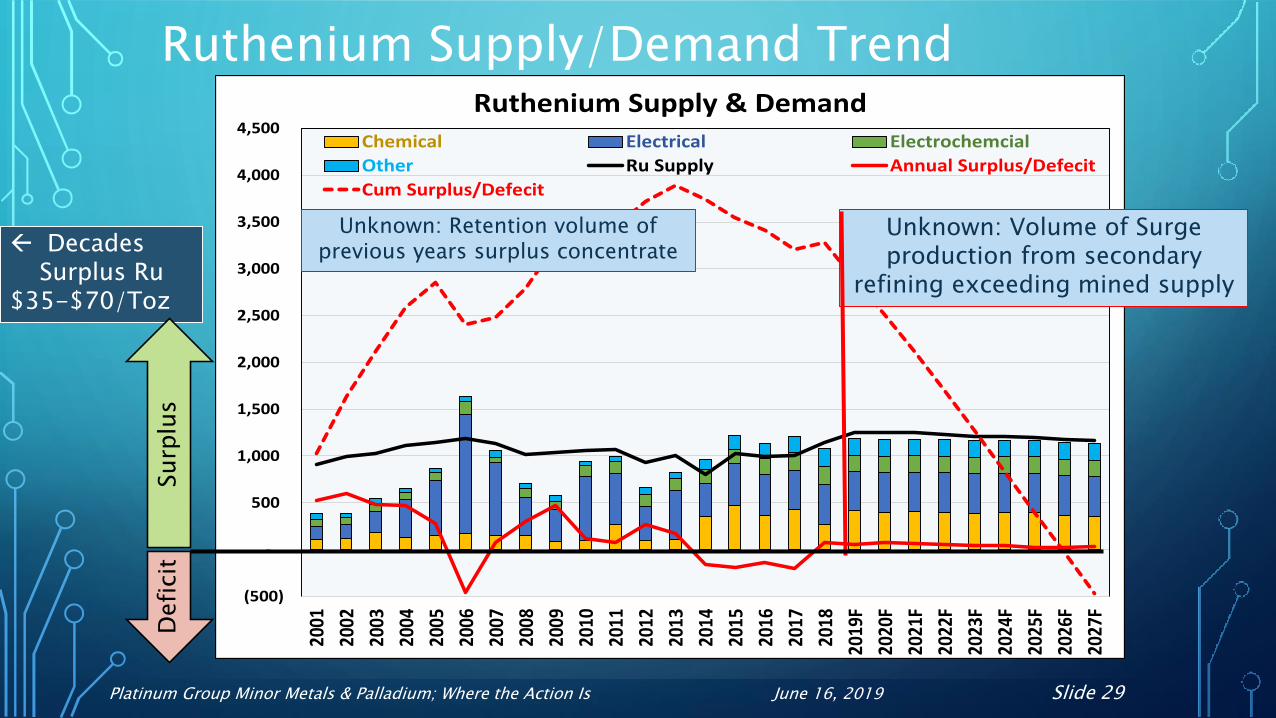

Ruthenium Supply & Demand

Chemical Electrical Electrochemcial

Other Ru Supply Annual Surplus/Defecit

Cum Surplus/Defecit

Ruthenium Supply/Demand Trend

Unknown: Volume of Surge production from secondary

refining exceeding mined supply

Unknown: Retention volume of previous years surplus concentrate Decades

Surplus Ru$35-$70/Toz

Defi

cit

Surp

lus

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 30

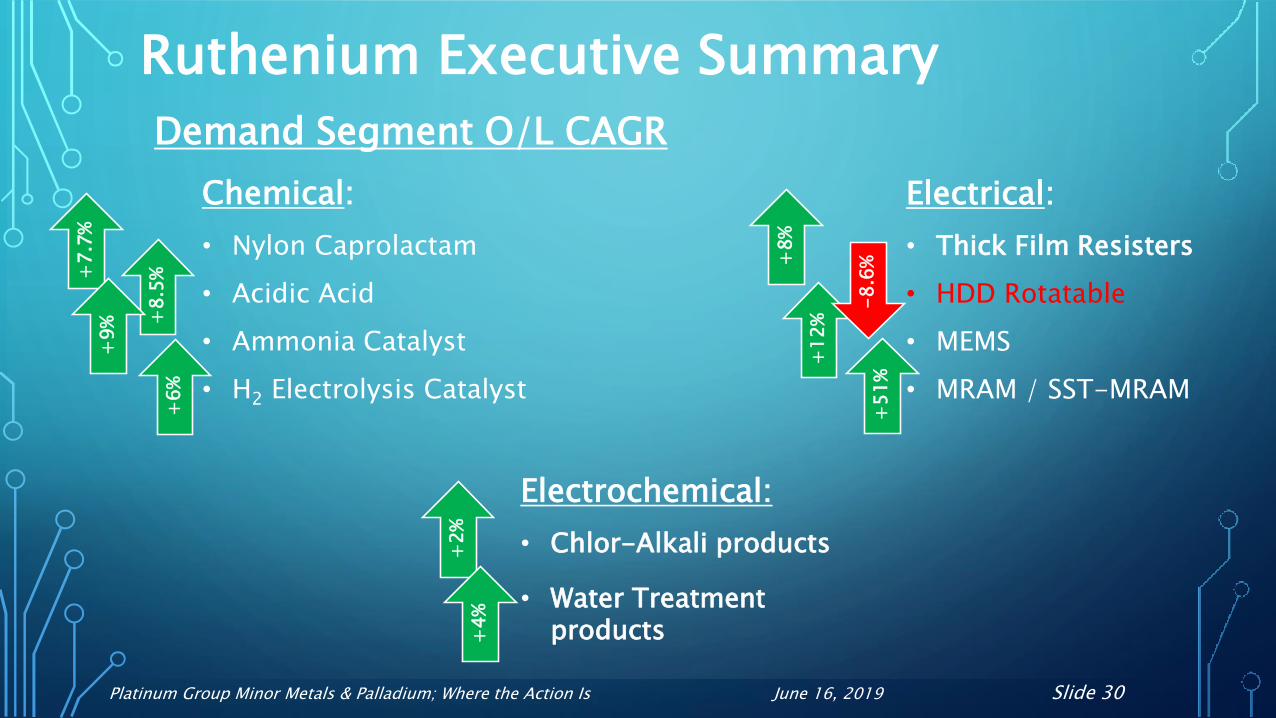

Ruthenium Executive Summary+

7.7

%

Electrical:

• Thick Film Resisters

• HDD Rotatable

• MEMS

• MRAM / SST-MRAM

+8

.5%

+8

%

+1

2%

-8

.6%

+5

1%

+9

%

Demand Segment O/L CAGR

Chemical:

• Nylon Caprolactam

• Acidic Acid

• Ammonia Catalyst

• H2 Electrolysis Catalyst

Electrochemical:

• Chlor-Alkali products

• Water Treatment products

+6

%

+2

%+

4%

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 31

Palladium & The PGM MinorsRhodium, Ruthenium and Iridium

• Palladium & Rhodium• Both 85%+ of supply towards top demand category - auto catalyst

• Tightness in the global auto catalyst smelting capacity is a new concern to meeting short

term demand

• Big Auto OEM’s working to finalize Pt Pd design swaps in gasoline catalyst designs.

Swaps likely starting in 2022-23 to leaner Pd designs.

• Ruthenium • Recent surge in secondary production meeting what would otherwise be a structural

deficit.

• Iridium • Near market balance

• O/L for more demand from several categories.

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 32

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600J-

00

J-01

J-02

J-03

J-04

J-05

J-06

J-07

J-08

J-09

J-10

J-11

J-12

J-13

J-14

J-15

J-16

J-17

J-18

J-19

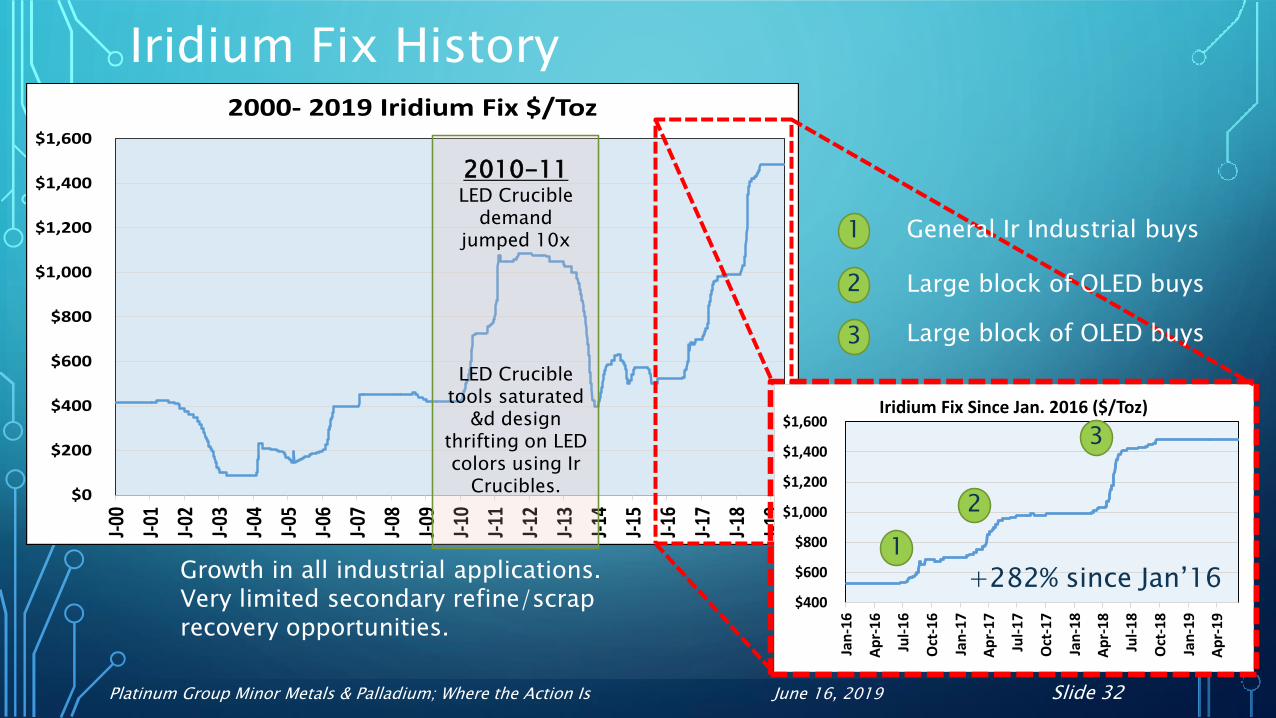

2000- 2019 Iridium Fix $/Toz

Iridium Fix History

Growth in all industrial applications.Very limited secondary refine/scrap recovery opportunities.

2010-11 LED Crucible

demand jumped 10x

LED Crucible tools saturated

&d design thrifting on LED colors using Ir

Crucibles.

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

Jan

-16

Ap

r-1

6

Jul-

16

Oct

-16

Jan

-17

Ap

r-1

7

Jul-

17

Oct

-17

Jan

-18

Ap

r-1

8

Jul-

18

Oct

-18

Jan

-19

Ap

r-1

9

Iridium Fix Since Jan. 2016 ($/Toz)

+282% since Jan’16

3

2

1

3

2

1 General Ir Industrial buys

Large block of OLED buys

Large block of OLED buys

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 33

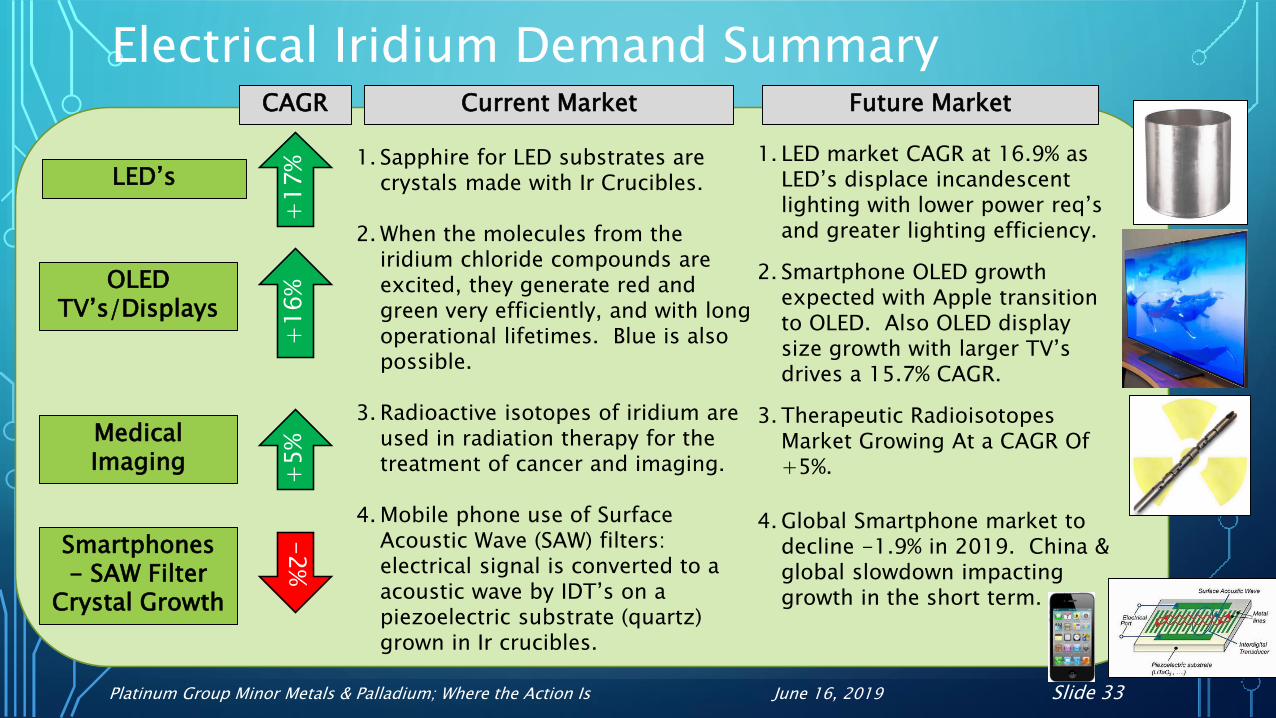

Electrical Iridium Demand Summary

+1

7%

+1

6%

LED’s

Medical Imaging

OLED TV’s/Displays

Smartphones- SAW Filter

Crystal Growth

Current Market Future MarketCAGR

1. Sapphire for LED substrates are crystals made with Ir Crucibles.

2. When the molecules from the iridium chloride compounds are excited, they generate red and green very efficiently, and with long operational lifetimes. Blue is also possible.

3. Radioactive isotopes of iridium are used in radiation therapy for the treatment of cancer and imaging.

4. Mobile phone use of Surface Acoustic Wave (SAW) filters: electrical signal is converted to a acoustic wave by IDT’s on a piezoelectric substrate (quartz) grown in Ir crucibles.

1. LED market CAGR at 16.9% as LED’s displace incandescent lighting with lower power req’sand greater lighting efficiency.

2. Smartphone OLED growth expected with Apple transition to OLED. Also OLED display size growth with larger TV’s drives a 15.7% CAGR.

3. Therapeutic Radioisotopes Market Growing At a CAGR Of +5%.

4. Global Smartphone market to decline -1.9% in 2019. China & global slowdown impacting growth in the short term.

+5

%

-2

%

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 34

Chemical Iridium Demand Summary

+9

%

The most important iridium compounds in use are the salts and acids it forms with chlorineIridiumcatalyzed carbonylation process for the production of acetic acid.

Iridium chemical oxidation state influences the performance and durability of oxygen evolution catalysts in PEM electrolysis.

Acetic Acid

Current Market Future MarketCAGR

1. Acetic acid demand is 17,808 kilo metric tones in 2019. Used in rubber, plastics, pharmaceutical, construction, paint & other app’s.

2. Oxygen evolution catalysts in PEM electrolysis

1. $11.6 billion by 2019 with CAGR of 8.7%. One risk of decline is the environmental efforts to reduce plastics.

2. $200 billion by 2025 @ 6.1% CAGR. Upside growth possible.

H2 Electrolysis Catalyst +

6%

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 35

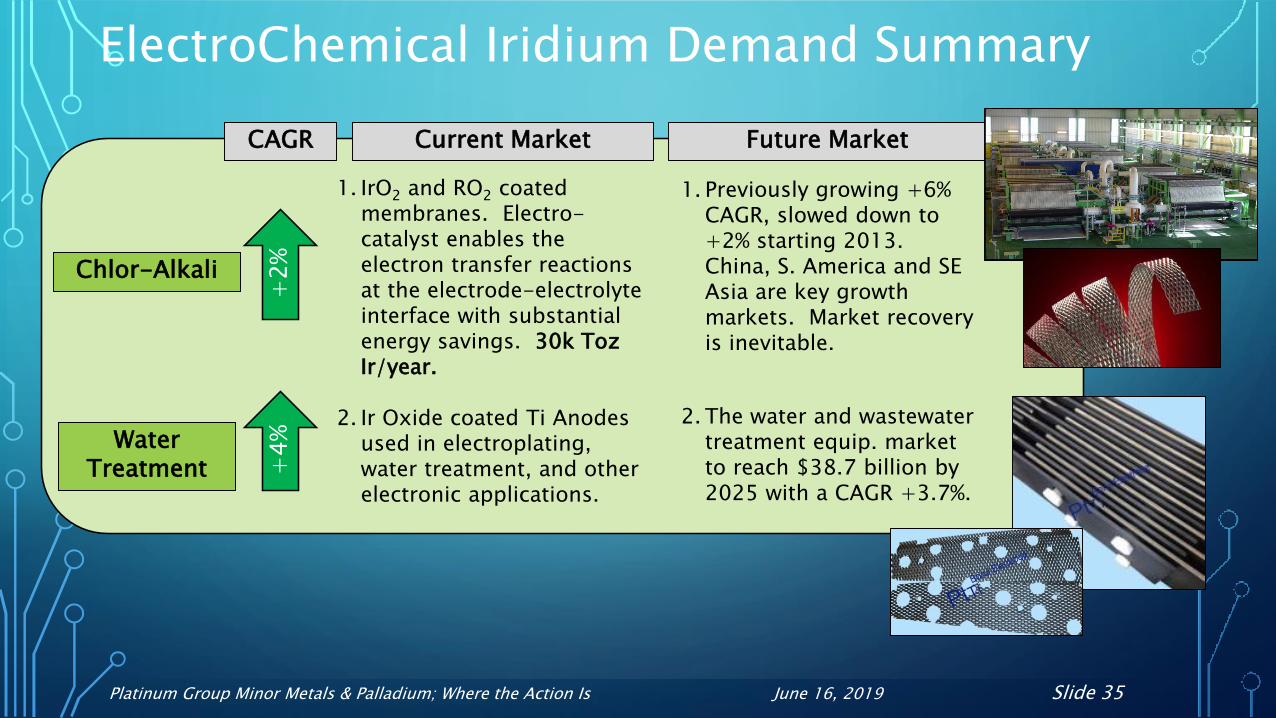

ElectroChemical Iridium Demand Summary

+2

%+

4%

Chlor-Alkali

Water Treatment

Current Market Future MarketCAGR

1. IrO2 and RO2 coated membranes. Electro-catalyst enables the electron transfer reactions at the electrode-electrolyte interface with substantial energy savings. 30k TozIr/year.

2. Ir Oxide coated Ti Anodes used in electroplating, water treatment, and other electronic applications.

1. Previously growing +6% CAGR, slowed down to +2% starting 2013. China, S. America and SE Asia are key growth markets. Market recovery is inevitable.

2. The water and wastewater treatment equip. market to reach $38.7 billion by 2025 with a CAGR +3.7%.

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 36

Other Iridium Demands - Summary

+6

%Spark Plugs

Current Market Future MarketCAGR

1. Ir tipped spark plugs for automotive / ICE.

2. Ir alloy used in long-life parts for aircraft engines. Thermo-electric generators are produced using Ir. Plutonium-238 fuel encapsulated using Ir.

3. High melting point and low reactivity make it perfect for use as a primary crucible material.

4. Used in special alloys and forms an alloy with Os, used for pen tips and compass bearings.

1. Resurgence in Ir Spark Plug demand due to declining diesel and for ICE fuel efficiency & emission perf. Showing +5.9% CAGR.

2. Mil/Aero sector continued to growth. Satellites and airplanes +9% CAGR.

3. Alt. materials including Platinum are gaining share due to Ir price. CAGR on general lab Ir crucibles -3%.

4. Most other app’s flat CAGR.

Military / Aerospace

+9

%

Crucibles

Unique App’s

-3

%

+0%

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 37

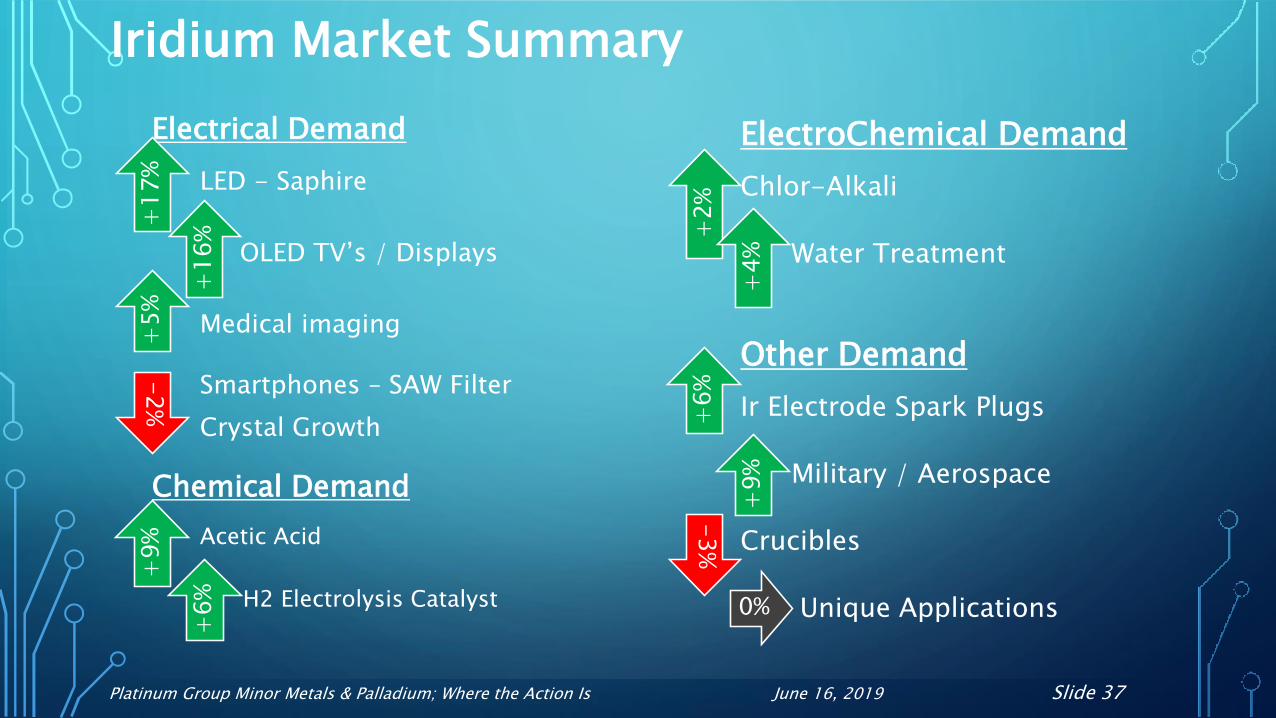

Iridium Market Summary

Electrical Demand

LED - Saphire

OLED TV’s / Displays

Medical imaging

Smartphones – SAW Filter

Crystal Growth

Chemical Demand

Acetic Acid

H2 Electrolysis Catalyst

+1

7%

+1

6%

+5

%

-2

%

ElectroChemical Demand

Chlor-Alkali

Water Treatment

Other Demand

Ir Electrode Spark Plugs

Military / Aerospace

Crucibles

Unique Applications

+2

%

+4

%

+9%

+6%

+6

%

+9

%

-3

%

0%

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 38

$-

$500

$1,000

$1,500

$2,000

$2,500

$3,000

-250

-150

-50

50

150

250

350

450

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

F

20

20

F

20

21

F

20

22

F

20

23

F

20

24

F

20

25

F

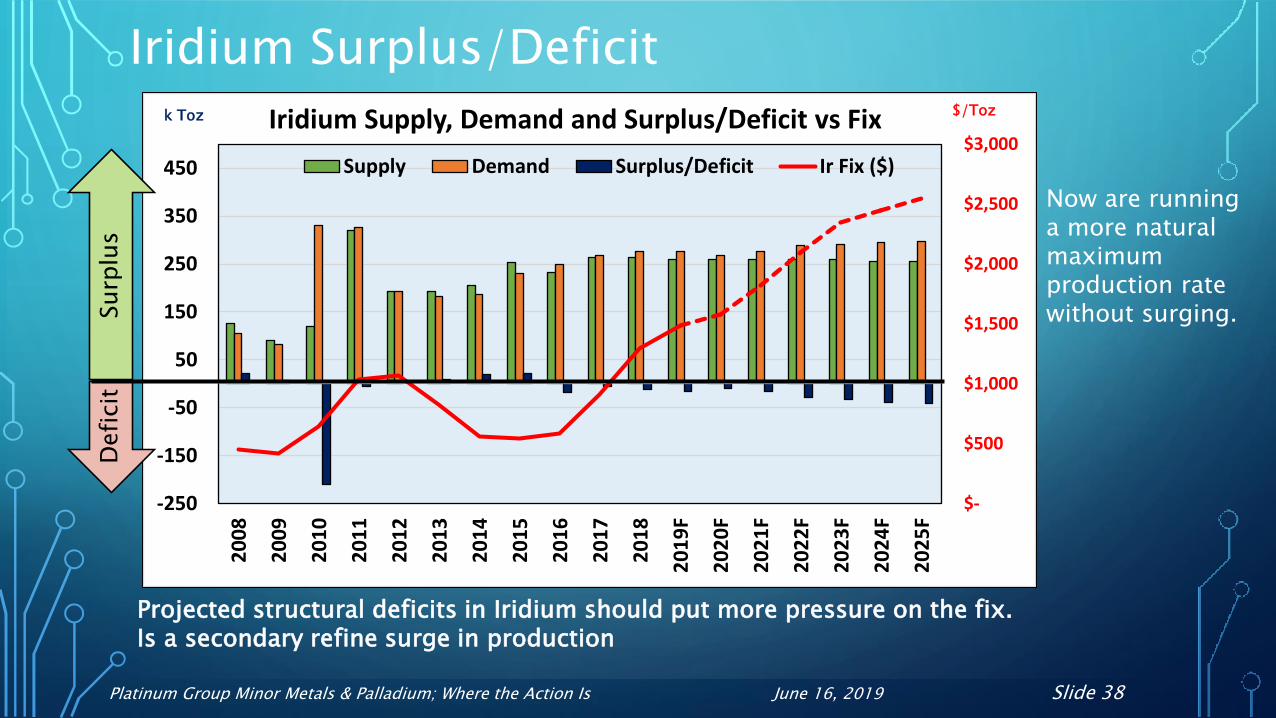

Iridium Supply, Demand and Surplus/Deficit vs Fix

Supply Demand Surplus/Deficit Ir Fix ($)

Iridium Surplus/Deficit

Projected structural deficits in Iridium should put more pressure on the fix.Is a secondary refine surge in production

$/Tozk TozD

efi

cit

Surp

lus

Now are running a more natural maximum production rate without surging.

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 39

Executive Summary• PGM’s, and specifically PGM Minor markets, are totally driven by supply and demand

fundamentals.

• Palladium – will remain in structural deficit for the foreseeable future. Design swaps towards

Platinum can alleviate some pain, but above grounds stocks are very transparently declining.

• Rhodium – Like an MMA fighter, this market will need to “Tap Out” by 2023 at current trajectory.

• Design work arounds for this Thelma and Louise act need to come rapidly. Secondary Refine is

more critical than ever during the life of this catalyst material.

• Ruthenium & Iridium – The forgotten minor metals. Both have critical industrial demand that

exceeds annual mined supply, with no end in sight.

• No ETF’s and little investment demand coupled with poor above ground stocks transparency.

• Processing of previous years surplus is connecting 2019 demand.

• Decades of mined surplus – what partially processed materials were saved for processing?

• Need to dramatically improve the transparency in reporting of above ground stocks. Also need to detail

secondary refine of PVD and Catalyst materials.

• Projected declines in S. African Platinum mining on the UG2 Reef in particular, leave us with a declining

supply outlook over the next 15 years as older/deeper mines approach scheduled end-of-life.

Platinum Group Minor Metals & Palladium; Where the Action Is June 16, 2019 Slide 40

Disclaimer

• Precious Metals Commodity Management LLC works to ensure the accuracy of the information and materials contained in this report, but makes no warranty as to accuracy, completeness for any particular purpose. PMCM LLC accepts no liability whatsoever in respect of reliance placed by the user on information and materials contained in this report, which are utilized expressly at the user’s own risk.

• A decision to invest in any regulated precious metal related products or any other regulated products, securities or investments should not be made in reliance on any of the information or materials in this report. Before making any investment decision, prospective investors should seek advice from their financial, legal, tax and accounting advisers, take into account their individual financial needs and circumstances and carefully consider the risks associated with such investment decisions. This report does not, and should not be construed as acting to, sponsor, advocate, endorse or promote any regulated precious metal related products or any other regulated products, securities or investments.