the brazilian business environment: reality and challenges

DESCRIPTION

This work aims at presenting the focus indicators and proposals of BRAiN – Brazil Investments & Business’ Doing Business Commission, as well as showing the new Brazil and the changes already made to the country’s business environment, which should be reflected in a better position in the Doing Business ranking of the World Bank and IFC.TRANSCRIPT

THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES

THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES

THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGESThis work aims at presenting the focus indicators and proposals of BRAiN – Brazil Investments & Business’ Doing Business Commission, as well as showing the new Brazil and the changes already made to the country’s business envi-ronment, which should be reflected in a better position in the Doing Business ranking of the World Bank and IFC.

TABLE Of CONTENTS

INTRODUCTION

WHAT IS BRAiN?

DOING BUSINESS IN BRAZIL REfORMING THE BRAZILIAN BUSINESS ENVIRONMENT

Starting a business Resolving insolvency Registering property Dealing with construction permits Getting credit Paying taxes Protecting investors Employing workers

THE RESPONDENTS’ ROLE AND DEfICIENCIES IN BRAZIL

THE NEW BRAZIL: PRESENT AND fUTURE REALITY VERSUS IMAGE Of BRAZIL IN THE WORLD ONGOING CHANGES: THE BRAZILIAN BUSINESS ENVIRONMENT

The financial sector The retail and services sector The growth of the Brazilian economy in the past decade and changes to the consumption pattern The evolution of the middle class in Brazil The transformations brought to the Brazilian scenario by social changes

CONCLUSION

8

10

14 14 15172021 22 28 29 34

37

40 40 43

43 51 53

54 56

60

THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES 9

INTRODUCTION

The World Bank and the International Finance Corporation (IFC) publish, since 2002, the Doing Business report, which assesses the ease of doing business in 183 different countries around the world through the following indicators: starting a business, dealing with construction permits, getting electricity, registering property, getting credit, protecting investors, paying taxes, trading across borders, enforcing contracts and resolving insolvency (formerly closing a business).

The Doing Business ranking is internationally used by governments in order to guide their actions and by businessmen and investors to assess the countries where they intend to invest. Obviously, capital inflows into Brazil foster the evo-lution of the Brazilian economy, generates more businesses and enables the country to expand its development. For this reason, it is extremely important to improve the country’s position in the ranking, but also to ensure that this posi-tion reflects the actual and true situation of the Brazilian business environment.

The Doing Business Commission of BRAiN – Brazil Investments & Business was created in September 2011 to assess the report and, based on it, pro-pose interventions that can contribute to the improvement of the Brazilian business environment and, of course, improve the country’s position in the Doing Business ranking. In the 2012 report, published on October 20, 2011, Brazil held the position no. 126, worse than the majority of its Latin Ameri-can neighbors and the BRIC countries, except for India. And the Commission acts to raise awareness among public managers, legislators and the Judiciary about the need to act, in a pragmatic and accurate way, to create a more friendly business environment in Brazil.

Comprised of representatives of BRAiN’s associates, the Commission identi-fied the indicators in which it is possible to achieve a rapid progress in order to enhance the Brazilian business environment and, consequently, improve Brazil’s position in the ranking, making it more attractive and less bureaucrat-ic. These indicators are: starting a business, resolving insolvency, registering property, dealing with construction permits, getting credit, protecting inves-tors, and paying taxes. The employing workers indicator is also addressed by the Commission due to its relevance to the Brazilian business environment, despite not being included yet in the Doing Business ranking.

In all aspects, there are simple initiatives in other parts of the world, and even in Brazil, that could be successfully replicated in São Paulo (Brazilian city on which the research is based, as it is the largest business city in the coun-try) and without requiring major structural changes. We noticed that the im-provement of the country’s business environment usually depends on fairly simple measures that may considerably facilitate the life of businessmen ac-ting in the financial, retail, civil construction, or other sectors. It is therefore a multisectorial agenda.

In addition to presenting the Doing Business Commission’s focus indicators and its proposals for improvement, the objective of this work is to show that a new Brazil has been emerging over the last few years, and that the recent changes in the national business environment should be reflected in a better position in international rankings, such as the Doing Business report, despite the widely known deficiencies that still affect the country. However, more than improving Brazil’s position in a specific ranking, we need to increase the potential to attract new investments to the country.

THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES 11

WHAT IS BRAIN?

Created in March 2010, BRAiN – Brazil Investiments & Business’ mission is to coordinate and catalyze the consolidation of Brazil as an international busi-ness and investment hub, with a regional focus on Latin America, but with global projection and connections. Conceived by three key entities of the country’s financial and capital markets – ANBIMA (Brazilian Association of Financial and Capital Market Entities), BM&FBOVESPA (Securities, Commodi-ties and Futures Exchange) and FEBRABAN (Brazilian Federation of Banks) – BRAiN is an association representing several sectors of society and counts on the sponsorship and participation of several private institutions.

In 2004, ANBID (National Association of Investment Banks), BM&F (Com-modities and Futures Exchange), BOVESPA (São Paulo Stock Exchange), CBLC (Brazilian Clearing and Depository Corporation), and, shortly after, FEBRABAN teamed up to launch an initiative to promote the Brazilian capital market in the international arena, called BEST, which means Brazil: Excellence in Securities Transactions.

Supported by Brazil’s Central Bank, the Brazilian Securities and Exchange Com-mission and the National Treasury, BEST promoted outreach events around the world and worked to improve the operational and regulatory features of the Brazilian market. BEST was a huge success during its first five years, reaching more than three thousand investors in 13 global financial centers.

In 2008, Brazil reached a new moment in the global financial scenario with the investment grade. Since then, several entities from the public and pri-vate sectors saw the emergence of an adequate moment to increase the in-ternational projection of the country, positioning it not only as an attractive destination for investments, but also as a business platform for the other countries in the region.

With engagement in BEST and a positive perception of the value of joint ini-tiatives by the government and the private sector, the Omega Project was born, having been developed between September 2008 and May 2009 in order to coordinate the strength of the Latin American business system and Brazil’s role in that system. In the course of the project, envisioned by ANBIMA, BM&FBOVESPA and FEBRABAN and supported by the Boston Con-sulting Group, other market entities joined and helped to found BRAiN in 2010. They are now its associates: FecomercioSP (Retail, Services and Tour-ism Federation in the State of São Paulo), Banco Bradesco, Banco do Brasil, Banco Santander, Banco Votorantim, BTG Pactual, CETIP (Brazilian Clearing-house), Citibank, HSBC and Itaú-Unibanco.

During the project, approximately 300 people from more than 70 public and private institutions were engaged, with the participation of opinion leaders from several sectors. The project was presented to directors and executives of companies, professional associations, economists and renowned technicians, as well as independent agencies and representatives of the federal, state and municipal government, including the Ministry of Finance, Brazil’s Central Bank, the Brazilian Securities and Exchange Commission – CVM, the Brazilian National Bank for Economic and Social Development, the São Paulo and Rio de Janeiro Municipal Governments and their respective State Governments.

12 THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES

Interaction with various sectors during the process made it clear that focus-ing discussions only on the financial sector would hardly be consistent with the size and diversity of Latin America and Brazil – the development of the region and the international situation generated a broader and more compre-hensive emerging view. As a result, we designed the multisectorial perspec-tive of Latin America as a strong regional business network presented herein, currently supported by BRAiN.

BRAiN is aware that a country’s growth with income distribution is directly linked to the growth of its home companies. And the growth of companies basically depends on the environment in which they are inserted and the availability of capital to promote investment.

In theory, companies have four potential funding sources: government, mul-tilateral organizations, banks and capital markets. If we draw a scenario for the next few years, we realize that three of these four options will be quite re-stricted. In the context of the current global economic crisis, the government and multilateral organizations are limited by fiscal responsibility and auster-ity plans, while banks will have major problems with the advent of Basel III and the credit constraints it will entail. The capital markets are the only left in a context of global economy with high liquidity, given developed countries’ monetary expansion plans. Thus, deepening the capital markets is essential for the Brazilian economy to grow.

Within this context, the main purpose of BRAiN is to address exactly these two issues: improvement of the business environment for companies and development of the capital market, especially in the long term, in order to increase investment. For this reason, the Doing Business Commission has an important role, as it works directly in the promotion of a business environ-ment which favors the development of its companies and attracts new invest-ments. As one of its specific goals, BRAiN intends to improve Brazil’s position in the Doing Business ranking from the 3rd to the 2ⁿd quartile until 2014.

IN THEORY, COMPANIES HAVE fOUR POTENTIAL SOURCES Of fUNDING: GOVERNMENT, MULTILATERAL ORGANIZATIONS, BANkS AND CAPITAL MARkETS

THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES 15

DOING BUSINESS IN BRAZIL

REFORMING THE BRAZILIAN BUSINESS ENVIRONMENT

The reforms implemented over the last few years in Brazil have contributed to improving the national business environment. Two good examples are the New Civil Code and the New Bankruptcy Law, which made the country safer to investors and lenders. However, deficiencies in some areas prevent Brazil from getting a better position in the Doing Business ranking.

The country bears several features that make it attractive for investments and business, such as economic growth, great availability of economically active population, large internal market, among others. Still, it lost six posi-tions in the 2012 Doing Business ranking in comparison with the previous year

because other countries moved faster with their reforms, and the business environment here, even though less and less hostile, still has execessive bu-reaucracy, discouraging businessmen.

Brazil is currently the sixth economy in the world, by its Gross Domestic Product (GDP). However, it ranks only 48th in the last World Economic Fo-rum’s Global Competitiveness Report (2012-2013) and it occupied the 126th position in the 2012 Doing Business report among 183 economies assessed, ranking among the worst economies in Latin America, behind Argentina (113th), Paraguay (102ⁿd), Uruguay (90th) and Peru (41st).

In order to reverse this scenario, BRAiN’s Doing Business Commission defined focus themes and, based on the Doing Business report, proposes interventions that may effectively improve the business environment in the country and, con-sequently, its position in the ranking. This also involves rainsing the awareness of the Doing Business contributors; so they may provide more quality answers which reflect the ongoing changes. This topic shall be discussed hereafter.

We describe below Brazil’s position in the Commission’s focus indicators and identify the areas in which it is possible to achieve rapid and effective pro-gress in order to make the Brazilian business environment more attractive, faster and less bureaucratic.

Starting a business

Doing Business assesses how big are the bureaucratic and legal challenges that an entrepreneur faces to start up and formally operate an industrial or commercial business. In the 2012 Doing Business ranking, Brazil gained five positions in this indicator, but still ranked only in the 120th position.

Brazil clearly has opportunities to develop in this respect. The ease of starting a business is essential to encourage new investments and business in the coun-try. The time it takes to start a business in the country was reduced by 27 % in the last four years, but it is still among the largest in the world, according to the report. The current 119 days were 152 in 2008, and such a number contributes to place the country among the worst in the ranking. One of the factors con-tributing the most to this number is the time it takes to request the operating license with the municipal government, which is approximately 90 days.

16 THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES 17

Registration with federal, state and municipal bodies is required to start a business in Brazil. Bureaucracy is also verified in the number of procedures (13), bigger than the average of Latin America and the Caribbean (nine) and the OECD member countries (five), what confirms the lengthy process of starting a business in Brazil. On the other hand, regarding the paid-in mini-mum capital required, which is one of the indexes that form the indicator, Brazil ranks in the 1st position, benefited by São Paulo specific laws and regu-lations, which require no minimum capital for starting up new companies.

Evaluations are still very bad and do not follow the Brazilian reality, despite an apparent improvement in the last few years’ indexes. This shows that there is still a long way to go, as shown below:

• The time and number of procedures indexes should be substantially reduced for the country to reach the second quartile in the specific ranking of the indicator;

• The cost should also be reduced, but expected increases in the GDP per capita may add to the index;

• As a whole, a 50 % improvement in the indicator is necessary to move Brazil to the second quartile.

When the theme is the establishment of foreign companies in Brazil, the case is even more alarming. It is estimated that a total amount of 166 days are nec-essary to go through all the stages for starting a foreign business, according to the Investing Accros Borders 2010 report from the World Bank. Concerning the authorization to import/export, it takes nearly 40 days to obtain a license.

When it comes to the BRIC countries, the same license takes a total of 65 days to be granted in China, 46 days in India and 31 days in Russia. Singapore still bears good numbers (nine days), as well as the European countries – France also has also nine days and the United Kingdom 14 days. In the regional analy-sis, Latin America and the Caribbean have the worst result – an average of 74 days –, while Eastern Europe and Central Asia have the best number – 22 days.

Still according to the Investing Across Borders 2010 report, in a ranking from 0 to 100 of the ease of establishing foreign companies, Brazil has numbers (62.5) similar to China’s (63.7) and the average of Latin America/Caribbean (62.8). However, developed countries remain with better scores – France (77.5), Japan (81.6), the United States (80) and the United Kingdom (85).

The Doing Business Commission identified the bottlenecks faced by entre-preneurs trying to start a business in the country, especially in the city of São Paulo, and prepared feasible alternatives to improve the Brazilian position in the indicator. So the following actions are proposed:

• Centralization of government procedures with the integration of fed-eral, state and municipal registries in a single procedure;

• Simplification of forms;

• Reduction in the time required for granting an operating license by granting a temporary license and excluding prior inspection;

• Introduction of electronic systems of payment and procedures through the automation of inspections and union classifications;

Resolving insolvency

Doing Business assesses the time, cost and outcome of insolvency proceed-ings involving domestic entities. The name of this indicator was changed from ‘closing a business’ to ‘resolving insolvency’ in order to more accurately re-flect its content. In the Doing Business 2012, Brazil gained one position in comparison with 2011, but it is still among the last ones (136th position).

In Brazil, the process of closing a business is slow and extremely bureaucratic, taking on average four years to be concluded. For example, the gap between Brazil and Japan, first in the ranking, is huge. In Japan, the same process takes only six months. This difference is mainly due to Brazilian legal requirements to finish off proceedings.

The resolving insolvency indicator consists of three indexes forming the re-covery rate, which is the real indicator counting for the rankings. Tthe recov-ery rate is recorded as cents on the dollar recouped by creditors. In the calcu-lation, all the amounts are adjusted for the present value using the country’s interest rate, which, in the case of Brazil, impairs the index – interest rates are still high, despite the recent drop trend. The recovery rate was 17.9 cents per dollar in Brazil in 2012, quite below the regional average of Latin American countries (30.7) and high-income countries (68.2).

18 THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES

In the current scenario, Brazil is classified in the third quartile, and a 60 % im-provement would be necessary to reach only the second quartile. However, it is important to highlight that Brazil has achieved significant progress with the New Bankruptcy Law or Business Recovery Law (Law no. 11,101/05). The new law regulated the judicial restructuring process and made the annual average bankruptcy rate drop to 2.7 thousand between 2006 and 2010. In 2003, this number had reached 20.7 thousand.

Therefore, the procedure for companies to resolve insolvency has been im-proving over the last few years, but there is still room for progress. Around the world, several economies made closing a business easier. The Czech Re-public is a good example; it reduced the time to close a business by 50 % and gained 83 positions in the Doing Business ranking from 2010 to 2011 with the creation of reform packages and the elimination, in some cases, of the need to file insolvency proceedings. This case shows that the indicator is very sen-sitive to the time variable. Other countries that improved the resolving insol-vency indicator were the United Kingdom (6th), Belgium (8th) and Japan (1st).

In Brazil, the Doing Business Commission suggests the following actions:

• Revision of the Business Recovery Law to make extrajudicial agree-ments feasible before any court proceedings;

• Elimination of existing ambiguities in the Business Recovery Law;

• Speeding up the business closing process, creation of special instanc-es and special courts for insolvency cases, as well as regulation of in-solvency specialists;

• Identification of ways to broaden the scope of the law in order to increase the public to which it is applicable, in addition to reviewing the parameters for approval and granting of the recovery benefit.

IT IS IMPORTANT TO HIGHLIGHT THAT BRAZIL HAS ACHIEVED SIGNIfICANT PROGRESS WITH THE NEW BANkRUPTCY LAW OR BUSINESS RECOVERY LAW (LAW NO. 11,101/05)

20 THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES 21

Registering property

Doing Business records the full sequence of procedures necessary for a busi-ness (buyer) to purchase a property from another business (seller) and to transfer the property title to the buyer’s name, so that the buyer can use the property for expanding its business, as collateral in taking new loans or, if necessary, sell it to another business.

The indicator consists of three indexes: time, cost and number of procedures. Brazil lost five positions in the 2012 report and held position no. 114 in the general ranking. To register a property in the country, there are 13 proce-dures taking 39 days on average, which is higher than the average of five procedures and 31 days of the OECD in 2012.

Brazil needs to shrink in 40 % the number of procedures to reach the third quartile, while the duration would have to drop 50 % for the country to achieve the first quartile. In terms of cost, Brazil holds a good position in the ranking and, with a slight improvement, it could be in the first quartile. In general, therefore, a 30 % improvement is required to take the country to the second quartile as to the registering property indicator.

However, it is important to notice that the registration of properties in São Paulo already counts on several online procedures, which could already au-tomatically reduce time and cost. This includes a certificate issued by Labor Courts, documents issued by protest offices and a municipal tax clearance certificate, among others.

Even with several already automated procedures, it is possible to increase efficiency, following the examples of states like Maranhão and the Fed-eral District. All around the world, economies as diverse as Cape Verde, Denmark, Portugal, Peru and Jamaica recently carried out improvements through reduced fees, increased administrative efficiency and implementa-tion of computer systems, with the introduction of online processes and the consolidation of procedures.

In the Brazilian case, the Doing Business Commission proposes the follow-ing actions:

• Reduction in the number of procedures for the registration of prop-erties by adopting the principle of concentration, in order to reduce costs and time and provide higher legal security;

• Time reduction;

• Possibility of simultaneous procedures, i.e., that different processes are executed at the same time.

Dealing with construction permits

Doing Business records all the procedures required for a business in the con-struction industry to build a standardized warehouse. The indicator consists of three indexes: number of procedures, cost and time. Brazil has improved this indicator over the last few years. It gained six positions and ranked 127th in the 2012 ranking especially due to the evolution of the cost index. Still, Brazil’s position is very bad, being adversely affected by the time variable.

It takes 469 days to build a standardized warehouse in the country, for exam-ple, and 274 days are spent only with the certificate of approval and building permit. The period for obtaining permits in Brazil is higher than the average of Latin America (221 days) and OECD high-income economies (152 days).

The cost, however, represents 40.2 % of the per capita income, better than the average of Latin America (160.3 %) and OECD countries (160.3 %). It is important to highlight that this improvement, however, may be more linked to a positive evolution of the Brazilian per capita income than to a real reduc-tion in costs. As to the number of procedures, there is a long way ahead to go. There are 17 procedures in Brazil, compared to 14 in Latin America and the Caribbean and high-income countries (OECD).

It is also worth mentioning that, in the calculation, some specific characteris-tics of the city of São Paulo may hinder the final result. In measuring the time factor, for example, inspection terms are taken into account, while the vari-able number of procedures considers any and all necessary procedures, and most of them depend on public services. Additionally, the construction code, information from experts and specific schedules for the payment of fees are used as sources of time and cost, a measure that may be influenced by the subjective perception of the Doing Business contributors.

22 THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES 23

To improve results, BRAiN’s Doing Business Commission suggests the following:

• Centralization of processes in a “single counter”, aiming to reduce the number of procedures and time. In the city of São Paulo, the proposal could be put into practice through the approval of the Bill no. 420/2006 instituting the ‘Single Counter for the Approval of Construction Pro-jects’ (‘BUAPE-HAB’);

• Concentration of workforce to encourage time saving in the city hall;

• Creation of electronic procedures and payments.

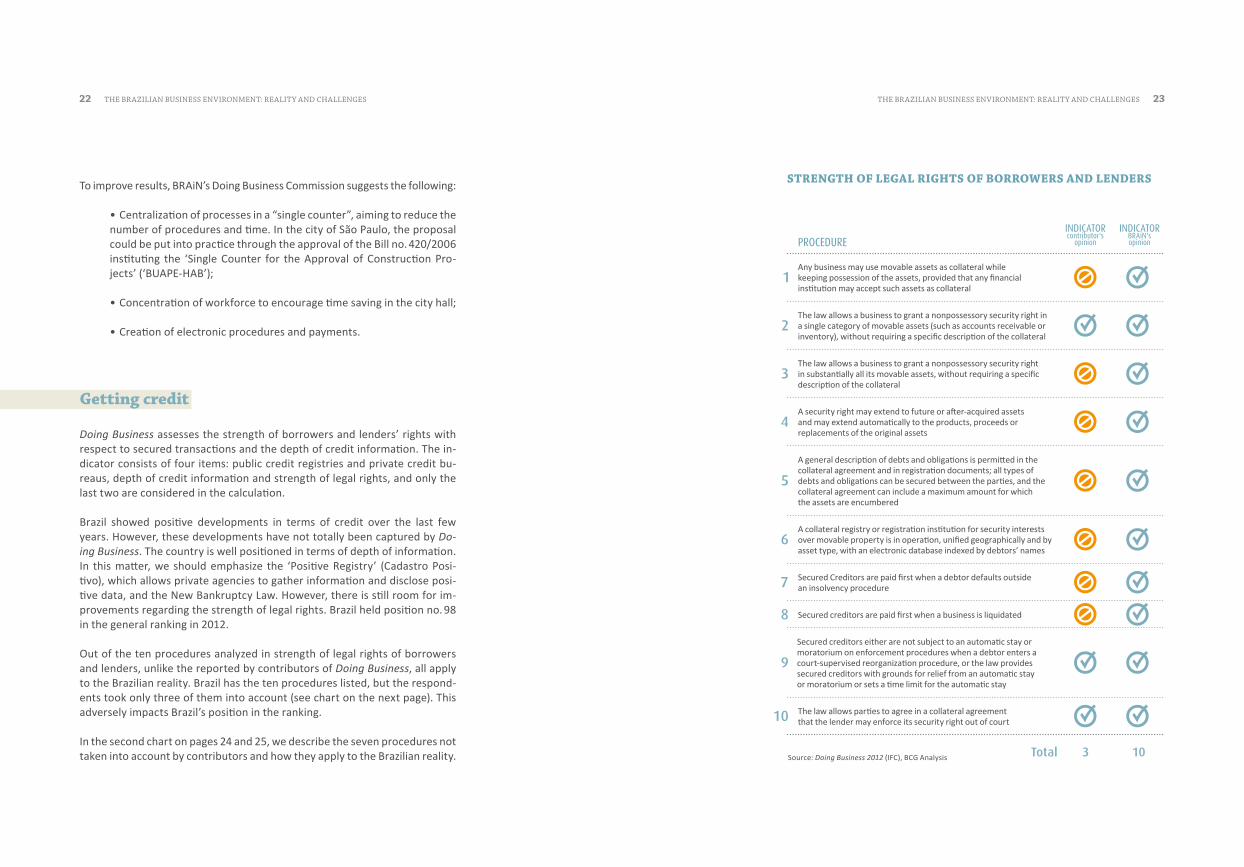

Getting credit

Doing Business assesses the strength of borrowers and lenders’ rights with respect to secured transactions and the depth of credit information. The in-dicator consists of four items: public credit registries and private credit bu-reaus, depth of credit information and strength of legal rights, and only the last two are considered in the calculation.

Brazil showed positive developments in terms of credit over the last few years. However, these developments have not totally been captured by Do-ing Business. The country is well positioned in terms of depth of information. In this matter, we should emphasize the ‘Positive Registry’ (Cadastro Posi-tivo), which allows private agencies to gather information and disclose posi-tive data, and the New Bankruptcy Law. However, there is still room for im-provements regarding the strength of legal rights. Brazil held position no. 98 in the general ranking in 2012.

Out of the ten procedures analyzed in strength of legal rights of borrowers and lenders, unlike the reported by contributors of Doing Business, all apply to the Brazilian reality. Brazil has the ten procedures listed, but the respond-ents took only three of them into account (see chart on the next page). This adversely impacts Brazil’s position in the ranking.

In the second chart on pages 24 and 25, we describe the seven procedures not taken into account by contributors and how they apply to the Brazilian reality.

STRENGTH Of LEGAL RIGHTS Of BORROWERS AND LENDERS

Any business may use movable assets as collateral while keeping possession of the assets, provided that any financial institution may accept such assets as collateral

The law allows a business to grant a nonpossessory security right in a single category of movable assets (such as accounts receivable or inventory), without requiring a specific description of the collateral

The law allows a business to grant a nonpossessory security right in substantially all its movable assets, without requiring a specific description of the collateral

A security right may extend to future or after-acquired assets and may extend automatically to the products, proceeds or replacements of the original assets

A general description of debts and obligations is permitted in the collateral agreement and in registration documents; all types of debts and obligations can be secured between the parties, and the collateral agreement can include a maximum amount for which the assets are encumbered

A collateral registry or registration institution for security interests over movable property is in operation, unified geographically and by asset type, with an electronic database indexed by debtors’ names

Secured Creditors are paid first when a debtor defaults outside an insolvency procedure

Secured creditors are paid first when a business is liquidated

Secured creditors either are not subject to an automatic stay or moratorium on enforcement procedures when a debtor enters a court-supervised reorganization procedure, or the law provides secured creditors with grounds for relief from an automatic stay or moratorium or sets a time limit for the automatic stay

The law allows parties to agree in a collateral agreement that the lender may enforce its security right out of court

Procedure

Total 3Source: Doing Business 2012 (IFC), BCG Analysis

IndIcatorBrain'sopinion

10

IndIcatorcontributor's

opinion

24 THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES 25

The law allows a business to grant a non-possessory security right in a single cat-egory of movable assets (such as accounts receivable or inventory), without requiring a specific description of the collateral.

The law allows a business to grant a non-possessory security right in substantially all its movable assets, without requiring a specific description of the collateral.

A security right may extend to future or after-acquired assets and may extend au-tomatically to the products, proceeds or replacements of the original assets.

Brazilian laws allow both fiduciary assign-ment and pledge of credit receivables.

Even though the law does not forbid the con-stitution of a non-possessory security right as specified on the left, its legal force is very questionable. Interpreting, therefore, this is-sue in literal terms, without evaluating the legal consequences of it, and given the ab-sence of express prohibition, the answer to the matter may be deemed positive.

Brazilian law expressly acknowledges that the creditor’s security rights remain pre-served until the secured debt is fully liqui-dated. So the security right remains valid for the time necessary for the full satisfac-tion of the creditor’s right. Additionally, the creditor is entitled to deem the debt over-due if the assets used as collateral deterio-rate or disappear, or if the debtor does not reinforce or replace them under the time fixed by the creditor.

Procedure IndIcator

A general description of debts and obliga-tions is permitted in the collateral agreement and in registration documents; all types of debts and obligations can be secured be-tween the parties, and the collateral agree-ment can include a maximum amount for which the assets are encumbered.

A collateral registry or registration institu-tion for security interests over movable property is in operation, unified geograph-ically and by asset type, with an electronic database indexed by debtors’ names’.

Secured creditors are paid first when a debtor defaults outside an insolvency procedure.

Secured creditors are paid first when a business is liquidated.

The Civil Code establishes that collateral agreements should include: I – the amount of the debt or its estimate; II – the expiration date of the obligation; III – the interest rate, if any; IV – the asset provided as collateral, otherwise the collateral does not have legal force. The same Code allows the parties to include in the deeds of mortgage and chat-tel mortgage the value of the assets agreed between them. Such amount, provided that it is updated, may be the basis for auctions, awards and redemptions, with no need of judicial or out-of-court assessment.

A collateral registry or registration institution is in operation for: real estate, geographically unified and by asset type, by the Registry Of-fice (CRI); movable property, like vehicles, by Detran (Traffic Bureau); other properties, in the debtor’s headquarters, by the Deeds and Documents Registry Office; and with an elec-tronic database indexed by debtors’ names by SERASA (private credit bureau), the Superior Court of Justice (TJSP) and the Board of Trade of the State of São Paulo (JUCESP).

The issue implies a subjective analysis of the creditor’s behavior with respect to its over-due credit. Empirically, the fact that a se-cured creditor is paid outside an insolvency procedure prior to an unsecured creditor is a circumstance whose verification does not depend on local laws, but on the creditor’s willingness to adopt measures of protection of his right against the debtor.

The current law changed the legal sequence of payments in bankruptcy, limiting the pri-ority of labor debts and giving preference to the payment of secured credits instead of tax credits, following the more developed systems adopted by countries like Germany, Sweden and England, and ahead of coun-tries like the United States.

26 THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES

DEPTH Of CREDIT INfORMATION

Are data on both firms and individuals distributed?

Are positive (for example, outstanding loan amounts) and negative information (for example, late payments, the number and amount of defaults and bankruptcies) distributed?

Are data from retailers and utility companies as well as financial institutions distributed?

Are more than 2 years of historical data distributed?1

Are data on loan amounts below 1 % of income per capita distributed?2

Do borrowers have the lawful right to access their data in the largest credit registry or bureau in the economy?

IteM

PrIvate credIt

Bureaus

PuBlIc credIt

regIstrIes

consolIdated IndIcator

Brain's opinion

Total 6

Regarding the depth of credit information, in opposition to what the Doing Business has been publishing, all the six features of the public credit registry or private credit bureau considered apply to the Brazilian reality, either via the private credit bureaus, or the public credit registry, as shown below:

1. Credit registries and bureaus that erase data on defaults as soon as they are repaid obtain a score of 0 for this indicator 2. A credit registry or bureau must have a minimum coverage of 1 % of the adult population to score a 1 on this indicator / Source: Doing Business 2012 (IFC), BCG Analysis

BRAZIL SHOWED POSITIVE DEVELOPMENTS IN TERMS Of CREDIT OVER THE LAST fEW YEARS. HOWEVER, THESE DEVELOPMENTS HAVE NOT TOTALLY BEEN CAPTURED BY Doing Business

28 THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES 29

This reinforces the perception that changes in the Brazilian legal scenario are not reflected in the Doing Business report. If they were taken into ac-count, Brazil would gain several positions in the general ranking, moving from position no. 120 to 106.

To improve this indicator, in addition to informing respondents, the Doing Business Commission lists the following necessary actions:

• Implementation of a unified collateral registry for different Brazilian regions, in order to facilitate the verification of properties to be ac-cepted as collaterals;

• Implementation of electronic procedures for verification and regis-tration of collaterals, aiming at increasing automation in the processes for getting credit;

• Easing of borrowing in order to allow registration of collateral with no specific description. The objective is to speed up and make the pro-cess for getting credit using properties as collateral less costly.

Paying taxes

Doing Business records the taxes, fees and mandatory contributions that a medium-size company must pay in a given year, as well as measures the ad-ministrative burden of paying taxes and contributions. Brazil is a world leader with respect to the difficulty in paying taxes, and the weight of charges, one of the heaviest in the world, is inconsistent with the global insertion of the Brazilian economy, and this is just one of the problems that businessmen face regarding taxation. Labor charges are the heaviest (40.9 %), but taxes on profit (average of 22.4 %) also impair the country’s position. In the aggregate, taxes bite 67.1 % of the companies’ profit, a much higher percentage than in neighbor countries, such as Chile (25 %), Peru (40.7 %) and Uruguay (42 %).

Of all categories, here is where the country gives its worst performance, rank-ing in the 150th position in the general ranking, with two positions lost in comparison with the 2011 report. In Brazil, it takes about three and a half months (2,600 hours) to prepare, file and pay or withhold corporate income taxes, value added tax (IPI, ICMS and PIS/COFINS) and social security con-

tributions, and this number is much higher compared to those from other developing countries, such as Mexico (404 hours), China (398 hours), Russian Federation (320 hours), Chile (316 hours), and Hong Kong (80 hours), except for the fact that the latter is not a country. In Bolivia, which ranks in the sec-ond worst position, only one and a half month (1,080 hours) is spent in this process. In Latin America and the Caribbean, it takes about 382 hours and in the OECD countries, 186 hours.

On the other hand, Brazil is well positioned (9th) regarding the number of payments per year, and online payments help the country, as, even if paid on a monthly basis, these payments are accounted for only once a year. Still the country stays behind countries such as Mexico (6th), China (7th), and Singa-pore (5th) and, with the same exception made above, Hong Kong (3rd).

Data confirm that the bureaucracy in the assessment of taxes payable, in ad-dition to tax decentralization, constant amendments to laws and regulations, as well as multiple governmental bodies, make paying taxes difficult.

Thus, the Doing Business Commission has been working on two fronts to re-verse this scenario:

• Incremental solutions (understand the division of taxes, reduce ancil-lary obligations and expand the simplified tax system);

• Radical solutions (unification of tax rates, which should be levied on the same basis, and rationalization of tax bookkeeping).

Protecting investors

In this indicator, Brazil held position no. 79 in the Doing Business 2012 gen-eral ranking, showing no evolution in the average of the last years, in spite of important changes in the domestic regulatory environment. Instead, the country lost five positions in comparison with 2011.

The indicator is comprised of three indexes (ease of shareholder suits, extent of director liability and extent of disclosure) and, iin general, Brazil is adverse-ly affected by the ease of shareholder suit index, which was poorly assessed by the Doing Business respondents.

30 THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES

A study developed by the Doing Business Commission showed that there is a series of answers that, indeed, do not reflect the Brazilian reality. If the questionnaires were correctly answered, the country’s position in the rank-ing would automatically improve. The average score in the last five years was 5.3, out of a total of 10. However, there have been recent improvements in domestic laws and regulations, as follows:

• Resolution of the Federal Accounting Council (CFC) no. 1,055/05, cre-ating the Brazilian Accounting Pronouncements Committee (CPC);

• Enactment of Law no. 11,638/07, creating a new accounting standard which follows the International Financial Reporting Standards (IFRS);

• Amendment to instruction no. 480 of the Brazilian Securities and Ex-change Commission (CVM), which regulates securities trading;

• Creation of the Reference Form, pursuant to CVM Instruction no. 480, annex 24. The document replaces the Annual Information Form (IAN) and makes information regarding the issuer available, from time to time, to investors and the market, taking the Brazilian rules to stand-ards that are very similar to those recommended by international insti-tutions specialized in capital markets.

It is possible to make a simple exercise to simulate the positions Brazil would gain only by making sure respondents have the correct perception of the actual situation of the country in the current scenario. For the ease of shareholder suits index, considered in this indicator, the diagram below shows the answers in the last questionnaires. Red circles represent an-swers that, according to a review by the Doing Business Commission, do not match the Brazilian reality.

A STUDY DEVELOPED BY THE DOING BUSINESS COMMISSION SHOWED THAT THERE IS A SERIES Of ANSWERS THAT, INDEED, DO NOT REfLECT THE BRAZILIAN REALITY

32 THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES 33

What range of documents is available to the shareholder plaintiff from the defendant and witness during trial? A score of 1 is assigned for each of the following types of documents available:

Whether the plaintiff can directly examine the defendant and witnesses during trial

Whether the plaintiff can obtain categories of relevant documents from the defendant without identifying each document specifically

Whether shareholders owning 10% or less of the company’s share capital can request that a government inspector investigate the Buyer-Seller transaction without filing suit in court

Whether shareholders owning 10% or less of the company’s share capital have the right to inspect the transaction documents before filing suit

Whether the standard of proof for civil suits is lower than that for a criminal case

• Information that the defendant has indicated he intends to rely on for his defense; • Information that directly proves specific facts in the plaintiff’s claim;• Any information relevant to the subject matter of the claim; and• Any information that may lead to the discovery of relevant information.

yes, with prior approval of the questions by the judge

yes, without prior approval

+1 point

+1 point

+1 point

+1 point

SPECIfIC POINTS AND POTENTIAL IMPROVEMENT IN THE RANkING

210 3 4

No

No yes

No yes

No

No

yes

yes

Ease of shareholder suits against directors has six components, with scores ranging from 0 to 10:

Ranking

Protecting investors

Ease of shareholder suits

Extent of director liability

Extent of disclosure

79th

156th

30th

61st

Answer corresponds to Brazilian reality

Need to evaluate the answer

Answer is not consistent with Brazilian reality

In the foregoing case, it is possible to notice an immediate increase of four points in the ease of shareholder suits index. The same exercise was made with the other two indexes. The final result with adjusted answers is pre-sented in the diagram below. Correct answers in the protecting investors indicator would make Brazil jump fourteen positions in the general ranking.

Ease of shareholder suits 3

7

6

5,3

79th

126th 112th 112th

7,3

16th

7,7

13th

7

8

7

7

9

7

Extent of director liability

Extent of disclosure

Final average

improved 14 positions

improved 14 positions

156th

30th

61st

41st

12th

38th

41st

1st

38th

SPECIfIC POINTS AND POTENTIAL IMPROVEMENT IN THE RANkING

cenarIo 1current cenarIo

classIfIcatIon In the IndIcator

IMPact on general rankIng

cenarIo 2

34 THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES

Worldwide, some economies such as Peru, Morocco and Sri Lanka improved their protection to investors by taking measures such as: regulated approval of transactions involving conflicts of interest, authorized access to internal corporate information and ease of lawsuits against officers.

In the case of Brazil, therefore, in addition to working on the respondents’ awareness, the Doing Business Commission suggests the following actions:

• Only companies listed in Novo Mercado should be taken into account;

• Assessment, together with the São Paulo Stock Exchange (BM&FBOVESPA), of the main obstacles preventing increased protec-tion of minority shareholders and the potential conflicts involving these shareholders.

Employing workers

Doing Business measures flexibility in the regulation of employment, spe-cifically as it affects the ease of doing business by measuring how difficult it is the hiring and redundancy of workers and the rigidity of working hours. Doing Business 2012 does not present rankings of economies on this in-dicator or include the topic in the aggregate ranking on the ease of doing business. The indicator will possibly be included in the next editions of the report, and will try to balance worker protection and flexibility of employ-ment laws and regulations.

In Brazil, the weight of labor laws and regulations impairs employment, damages the country’s competitiveness and adversely affects the economy. Charges upon employing a worker, for example, exceed 100 % of the salary. The Brazilian laws and regulations of 1943 were created based on a closed economy and, currently, they became archaic, counterproductive and bur-densome both for companies and workers. Laws and regulations that ensure basic and fundamental rights to employees and allow, at the same time, ne-gotiations of specific rights are required, also taking into account a series of factors, such as company’s sector, size and activity, among others.

IN BRAZIL, THE WEIGHT Of LABOR LAWS AND REGULATIONS IMPAIRS EMPLOYMENT, DAMAGES THE COUNTRY’S COMPETITIVENESS AND ADVERSELY AffECTS THE ECONOMY

36 THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES 37

In this regard, the Doing Business Commission proposes the following actions:

• Flexibilization of the provisions in the Consolidated Labor Laws (CLT), allowing a practical and effective application of the rules through elimi-nation of provisions that entail excessive bureaucracy;

• Specific laws and regulations for micro and small enterprises and the rural sector, including regarding creation of new employment terms that do not compromise the minimum rights of workers;

• Reduction of payroll taxes;

• Different rates for small-sized companies to calculate deposits to the Brazilian Unemployment Compensation Fund – FGTS;

• Enhancement of Prior Conciliation Commissions and their use prior to filing a legal action, aiming at speeding up the work of Labor Courts;

• Strengthening of the union system through regulation of article 8 of the Federal Constitution;

• Maintenance of the confederative system for union representation, as it is more effective and democratic.

In short, Brazil needs effective labor laws and regulations that stops wast-ing workforce and making economic development hard, in an attempt to in-crease employment and income levels and the country’s sustained growth.

THE RESPONDENTS’ ROLE AND THEIR DEFICIENCIES IN BRAZIL

Brazil’s deficiencies in some areas prevent the country from getting a better position in the Doing Business ranking, used by governments to guide their actions and by businessmen to assess the places where they intend to invest. Indeed, as noticed, Brazil is poorly evaluated in some items due to bureau-cratic obstacles and internal issues, such as overregulation, difficulty in pay-ing taxes and labor charges. However, the country’s position in the ranking is not consistent with its reality, as respondents’ lack of knowledge, most of them acting in the legal field, ends up hindering the assessment. It was evi-denced that respondents are not duly aware of the best way to answer the questionnaires and to allocate adequate resources.

ANSWERS GIVEN TO THE qUESTIONNAIRES HAVE A MAjOR INfLUENCE ON THE fINAL RESULT. fOR BRAZIL, THEY END UP REVEALING AN ENVIRONMENT THAT DIffERS fROM THE REALITY

38 THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES

National respondents chosen by the World Bank and the IFC are professionals that frequently face the regulatory and legal requirements addressed in each Doing Business topic. Given this focus on legal and regulatory provisions, most respondents are legal professional, such as lawyers and attorneys. The survey on credit information is answered by officers in charge of credit regis-tries or bureaus. Freight forwarders, accountants, architects and other pro-fessionals answer the surveys related to trading across borders, paying taxes and construction permits.

However, answers provided in the ranking questionnaires by consultancy ser-vices, frequently on a formal basis, and sometimes by advisors other than the managers of inquired offices themselves, have a major influence on the final result. For Brazil, they end up revealing an environment that differs from the reality of the national entrepreneurship. That is, paying more attention to the answers may correct this deficiency and place the country in a more realistic position, less distant from the leaders.

Obviously, BRAiN is not assigning respondents exclusive responsibility for the current situation. But it is impossible to deny that, with no false information and just by paying more attention to the questionnaire, such respondents may contribute to improve Brazil’s position. By replacing a superficial and bureaucratic answer for a based and correct one about our development will allow improvements in the level of perception by foreign authorities and in-vestors, and help Brazil to achieve its deserved level of reliability and oppor-tunities, even though, on the other hand, governmental authorities also need to get involved and make the adjustments the country really needs.

To change this situation, BRAiN is requesting that the World Bank and IFC change the criteria for selection of respondents in order to allow compa-nies, professional associations and more accountants acting in the Brazilian market, therefore closest to the reality of the domestic business environ-ment, to form part of the group. Accordingly, we expect answers to be more consistent with reality.

ANSWERS GIVEN TO THE qUESTIONNAIRES HAVE A MAjOR INfLUENCE ON THE fINAL RESULT. fOR BRAZIL, THEY END UP REVEALING AN ENVIRONMENT THAT DIffERS fROM THE REALITY

THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES 41

THE NEW BRAZIL: PRESENT AND fUTURE

REALITY VERSUS IMAGE OF BRAZIL IN THE wORLD

Unfortunately, Brazil is not as good in showing the world its qualities as it is when showing its flaws, such as political scandals and violence. Regarding the economy, for example, there is a huge lack of information about several sec-tors, forcing international analysts to adopt a material amount of subjectivity in their studies, mistakenly assessing the risks that our laws pose to invest-ments in the country.

The global financial market opinion on how hard it is to recover credit in Bra-zil, whether due to bureaucracy, quality of laws or credibility of the Judiciary Branch, has a direct influence on the cost of loans and credit facilities granted to Brazilian companies, making it difficult, as a result, to increase investment, generate new jobs and even pay taxes.

Six major Brazilian companies have already obtained the Investment Grade, thirty-one local corporations have their shares listed on the New York Stock Exchange, the currency remains reliable since 1994, the balance of trade shows steady positive balances, the Brazilian democracy remains strong, with the population highly represented through direct and electronic vote (one of the world’s most advanced vote system), and our economy repre-sents 50 % of the economy of Latin America as a whole. This evidences that the extremely critic perspective of Brazil results more from its incapacity to properly present itself abroad than from a remote research work that does not take into account all material aspects.

SIx MAjOR BRAZILIAN COMPANIES HAVE ALREADY OBTAINED THE INVESTMENT GRADE

42 THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES 43

To illustrate this situation, it is worth to study the case of bankruptcy pro-ceedings in Brazil. Indeed, the former bankruptcy law (Decree-Law no. 7,661, 1945) was created in a time when family and little specialized businesses used to prevail. After adjudication of bankruptcy and appointment of a trustee, the company used to be shut off as a way, available at the time, to protect creditors’ interests. Such procedure for collection and safekeeping of properties might have made sense for small business, but did not make sense anymore for large business, whose managers are persons different from partners, and these are also persons separated from the company. The former bankruptcy system did not ensure effective control of the trustee’s acts, did not preserve production or jobs, nor prevented the deterioration of the business’ assets over time.

Also, bankruptcy proceedings in Brazil were not monitored by creditors, mak-ing easier to perpetrate a series of frauds. The main reason for the indiffer-ence of creditors in monitoring the bankruptcy process was the fact that, in the majority of the cases, they had no perspective to recover their credit, due to the unlimited priority granted by law to labor and tax credits. As the com-pany’s first and simplest alternative to tackle with its financial problems is to stop paying its taxes and social security contributions, usually there was not much left after adjudication of bankruptcy to pay other creditors.

However, since 2003, Brazil has been adopting effective measures with re-spect to ethical standards, modernization and expedition of proceedings and valuation of contractual guarantees, especially with the approval of the new Bankruptcy Law (Law 11,101/2005) and the reform of the Judici-ary Branch, which also introduced important progresses with respect to protection of creditors’ interests. The current bankruptcy law amended the legal sequence of payments in bankruptcy, limiting the priority of la-bor debts and giving preference to the payment of secured credits instead of tax credits, pursuant to more evolved systems adopted by countries as Germany, Sweden and England, and staying ahead of countries as the Unit-ed States, Italy and Spain, which bankruptcy laws still give priority to tax over secured credits.

However, such evolutions were preceded by deplorable scandals led by politi-cians, judges and other authorities, which significantly affected the country’s image and the Judiciary Branch’s credibility, resulting in a major popular de-mand for changes. All of this, together with scandals involving a very large number of legislators and the potential absolution of them all, only made the country’s image and its institutions’ credibility strongly unstable.

ONGOING CHANGES: THE BRAZILIAN BUSINESS ENVIRONMENT

The financial sector

Brazil starts from an actual outstanding position in the financial sector. De-spite the impact of recent crises on the financial services industry of devel-oped countries, this segment has been delivering increasing expansion and achieving new levels of prominence in Brazil and in the region. The country’s growth over the last few years has been supported by a robust financial seg-ment undergoing an expansion and internationalization process.

The regulation of the Brazilian financial system is internationally recognized. The reason why Brazil did resist well to the 2008 financial crisis was basically the strength of its banking infrastructure. The stability of the regulation sys-tem as a whole is greater than those of traditional countries as the United States and the United Kingdom in competitiveness ranking, as those prepared by the World Economic Forum and by IMD, an the regulation and supervision of specific segments, such as derivatives – with centralized trading and reg-istration – serve as a reference to other countries. Additionally, the Brazilian financial system shows positive profitability in a context of crisis.

44 THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES 45

Developing countries Developed countries

IndonesIa

coloMBIa

chIle

MexIco

IndIa

brazil

sIngaPore

chIna

hong kong

russIa

unIted states

unIted kIngdoM

gerMany

france

JaPan

20.2

14.1

10.3

10.2

6.2

6.2

- 23.5

- 21.3

- 19.4

- 16.3

- 13.8

- 5.9

- 5.5

- 4.5

- 0.3

BRAZIL ALREADY HAS A STRONG fINANCIAL SYSTEM AND IT IS RANkED WELL IN RELATION TO DEVELOPED ECONOMIES

Stock Market with the highest returns since 2004, main economies

TSR2 2007-2011 p.y. (%)

Change in share Market value³

1. Among the main global banking systems assessed by the BCG research Creating Value in Banking 2. TSR: Total Shareholder Return is comprised by capital gains and dividens 3. In US$ / Note: All TSRs calculated in local currency / Source: BCG 2012 Creating Value in Banking Report; UIV; BIS; World Bank; Standard & Poors; World Federation of exchanges; BCG research

100

200

300

400

2005 2006 2007 2008 2009 2010 20112004

unIted states

russIa

MexIcoIndIa

chIna

BrazIl

JaPan

index 2004=100

Bank shareholder returns are higher than in developed economies1

Some examples of Brazilian reference regulations are:

• Financial transactions are registered on behalf of the final beneficiary rather than the finder, which ensures the safety of the former in case of insolvency of the latter;

• Investment funds are required to disclose their holdings to regula-tory agencies at least on a quarterly basis. Such regulation ensures that fraudulent pyramid schemes, such as the Madoff case, become harder and harder in the country;

• The internalization of orders is forbidden, ensuring greater liquidity in the central market and a more accurate reflection of the assets actual price;

• All derivative transactions in Brazil are registered in the same place, the Derivatives Exposure Center – CED, controlled by the Interbank Payment Chamber (CIP), which allows financial agents to have access to the companies’ holdings in derivatives, upon their authorization, before closing transactions, avoiding overexposure. Countries as the United States and the United Kingdom have being trying to create simi-lar systems, but these are still being designed or under development;

• The transfer of funds for settlement of transaction in Brazil is protect-ed against finders’ insolvency risk: it is made in bank reserve currency at the Central Bank (settlement in central bank line) and the amounts, including guarantees, while still on finders’ hands, are not included in any bankrupt estate;

• All transactions in a stock exchange in Brazil have a central counter-party, which ensures the safety of the transaction to those involved;

• The country already requires, from its banks, the 11 % minimum Capital Adequacy Ratio, higher than the 8 % international requirement. In April 2012, the average of this ratio for Brazil was 16 %, showing a good position. Additionally, the Central Bank indicated the country is in a good position to implement the Basel III rules beginning in 2013, which define stricter criteria for composition of capital requirements and increase the ratio level to 13 %.

Thus, the Brazilian financial system is strong and shows very positive num-bers regarding returns, both bank structural returns and returns on invest-ments in the stock market.

46 THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES

Bank credit, considering non-earmarked funds and earmarked facilities granted by the Brazilian National Bank for Economic and Social Develop-ment – BNDES, grew 15 % per annum in real terms since 2004, more than doubling during the period. The Brazilian stock market also grew fast in the last decade, both in terms of capitalization and amount of transactions and is, by far, the largest in Latin America. The Brazilian stock market total capi-talization was of approximately 55 % of GDP in 2011, reaching a level close to France and higher than Germany, with a highly diversified base of investors, which includes individuals, institutional investors, financial institutions and foreign investors.

This growth was triggered by a combination of strong performance of the market and a consistent increase in the total amount of shares offered. The introduction of Novo Mercado (New Market), which encourages companies to adopt higher standards of corporate governance, transparency and pro-tection of minority shareholders as listing requirements, also contributed to the development of the stock market.

In order to mention some numbers, in the first six months of 2012, the Brazil-ian stock exchange (BM&FBOVESPA) presented a daily average of 5,202 mil-lion of shares traded and an average daily volume of US$3.7 billion only in local deals within Latin America. Currently, Brazil concentrates 85 % of the liquidity of all stock exchanges in Latin America (including Mexico) and 90 % of the volume of derivative contracts traded.

Regarding debentures, today the ongoing reduction in the real interest rate is expected to boost this financing alternative, which is still little used in Brazil. Additionally, Law no. 12,431 was published in June 2011, as a result from the conversion of the Provisional Measure no. 517 of 2012, aiming at encouraging long-term financing. This sets an important milestone in the development of debt securities in Brazil and in the increase of liquidity in its secondary mar-ket. The main regulatory changes were:

• Reduction of the Income Tax rate applied to foreign investments in Brazilian private securities to zero;

• 30-day exemption from the Tax on Financial Transactions (IOF) levied on private debt securities transactions;

• Possibility to repurchase debentures by the issuer for an amount higher than the face value, in case of appreciation;

THE BRAZILIAN STOCk MARkET ALSO GREW fAST IN THE LAST DECADE, BOTH IN TERMS Of CAPITALIZATION AND AMOUNT Of TRANSACTIONS, AND IS, BY fAR, THE LARGEST IN LATIN AMERICA

48 THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES 49

• Possibility of monetary adjustment as frequent as that stipulated for the periodic payment of interests, even if more than once a year;

• Amendment to the Brazilian Corporation Law in order to allow the issuance of bonds in amounts higher than the issuer’s capital stock. Thus, special purpose entities (SPEs) are not required to be capitalized in order to issue debentures;

• Possibility of simultaneous debenture issuances by the same issuer, as to provide issuers greater opportunities to take advantage of more favorable market conditions.

Changes made by this law removed most regulatory barriers to liquidity. Ad-ditionally, in 2012, more than 40 representatives of the commercial, indus-trial and financial sectors met with the Finance Minister and the president of BNDES to present a joint proposal to eliminate the remaining obstacles and further improve the framework required to develop this type of financing. Accordingly, the market, by trying to repeat and apply the Novo Mercado successful initiative of self-regulation to private debt issuance, organized and established additional benefits for the adoption of this type of financing.

IN THE fIRST SIx MONTHS Of 2012, THE BRAZILIAN STOCk ExCHANGE (BM&fBOVESPA) HAD AN AVERAGE Of 5,202 MILLION SHARES TRADED ON A DAILY BASIS

Non-earmarked credit

Earmarked credit (BNDES)

Brazilian corporate credit stock (R$B reais¹)

2004 2005 2006 2007 2008 2009 2010 2011

+ 15 %

414476

543

635

789

898

961

1,073

38 %37 %

35 %

32 %

30 %37 %

39 %39 %

62 % 63 %65 %

68 %70 % 63 % 61 % 61 %

1. Base amounts Dec./2011, adjusted by the General Market Price Index – IGPM 2. Considering the last busi-ness day of the year / Source: Brazil’s Central Bank; BIS; Central Banks and other institutions of the individual countries; Bloomberg

Debentures are also growing, however in a slower pace Brazilian corporate credit stock (R$B reais¹)

2004 2005 2006 2007 2008 2009 2010 2011

16 15 17 18 19 20 19 20

+ 4 %

The Exchange Value grew up to 2007 with a slight drop since thenMarket value of businesses listed on BM&FBOVESPA¹ (R$B reais²)

8461,073

1,512

2,488

1,362

2,3352,398

2,225+ 43 %

- 3 %

2004 2005 2006 2007 2008 2009 2010 2011

Corporate credit has been delivering a significant growth in Brazil

CORPORATE fINANCE HAS SIGNIfICANTLY ExPANDED IN BRAZIL OVER THE LAST fEW YEARS

50 THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES 51

Additionally, it is worth to mention private efforts to create self-regulation rules for the fixed income market in 2011, similar to the Novo Mercado suc-cessful model for the issuance of shares, with higher transparency and gov-ernance standards to attract investors, as: provide a minimum number of 10 investors with a maximum individual share of 20 % of the offer, obtain an annually updated credit risk assessment and adopt mechanisms that ensures, in the first 12 months of issuance, periodic disclosure by research analysts on the asset assessed.

As to the Brazilian insurance market, despite being still underpenetrated if compared to the global standard, it has room to double its size, taking into consideration the participation of premiums in the national GDP. Especially, there was already a big change in the reinsurance market after the break in the monopoly of IRB-Brasil (Brazilian Reinsurance Institute) in 2008. Current-ly, the country has more than 100 registered reinsurers and, according to the National Federation of the Reinsurance Companies, the market is expected to growth more than 15 % in the next five years (from approximately R$ 5.7 billion in 2011).

Therefore, the Brazilian financial sector currently has several strong points, especially its prudent regulation and solid and profitable financial institu-tions. The supervision of transactions carried out is appropriate, balancing the flexibility required by the market with the safety necessary for the system to continue. Additionally, the main Brazilian banks are healthy and provide positive returns to shareholders. This is important, given the crisis context, in which most of Brazil’s international peers showed significant declines. Fi-nally, with the current scenario of falling interest, the Brazilian government, through recent legislative changes, signs an interest in increasing the avail-ability of instruments capable of meeting the market needs.

The retail and services sector

Global economies went through, over the last few years, a process of produc-tive restructuring, which triggered transformations in the technological field and employment market, impacting all sectors of economy. In this process, the tertiary sector started to provide important contributions to the econom-ic development of the countries.

In Brazil, the retail and services sectors are responsible for about two thirds of the country’s Gross Domestic Product (GDP) and, consequently, of the workforce absorption. Urbanization, technological development and changes to household consumption pattern were the drivers to the evolution of the segment after the institution of important milestones as trade liberalization, the Real Plan and the process of income distribution.

The change to the household consumption pattern is linked to two essen-tial factors: price stability and the sustained global economic growth cycle. The increase in middle-class families’ income was possible thanks to the eco-nomic stability, expansion of employment, income and credit combined with government social welfare policies.

Over the past decade, the Brazilian economy moved towards reducing in-come inequality. This dynamic explained the greater access to credit by fami-lies that, before that moment, were kept out of the market and, also, the rep-resentative increase in the purchase of durable consumer goods and services.

Equally, it is important to notice that over the last few years Brazil experi-enced two very important demographic events: accelerated decrease in the birth rate and, at the same time, a significant increase in life expectancy.

Currently, the country has a contingent of more than 130 million people in working age and, by 2020, this mass will reach more than 144 million, i.e., the largest historical contingent in working age. This grants, strictly speaking, a demographic bonus to Brazil.

52 THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES 53

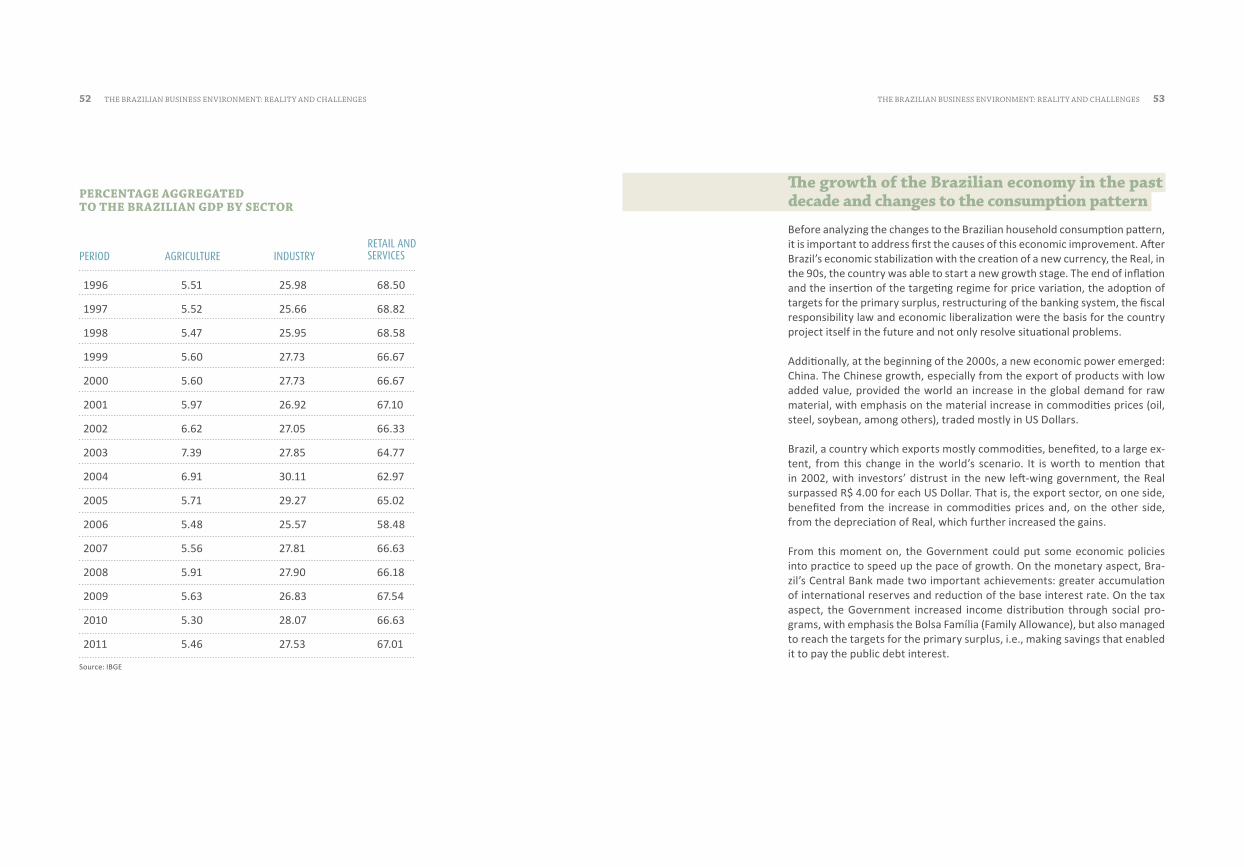

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

5.51

5.52

5.47

5.60

5.60

5.97

6.62

7.39

6.91

5.71

5.48

5.56

5.91

5.63

5.30

5.46

25.98

25.66

25.95

27.73

27.73

26.92

27.05

27.85

30.11

29.27

25.57

27.81

27.90

26.83

28.07

27.53

68.50

68.82

68.58

66.67

66.67

67.10

66.33

64.77

62.97

65.02

58.48

66.63

66.18

67.54

66.63

67.01

PERCENTAGE AGGREGATED TO THE BRAZILIAN GDP BY SECTOR

agrIculture IndustryPerIodretaIl and servIces

Source: IBGE

The growth of the Brazilian economy in the pastdecade and changes to the consumption pattern

Before analyzing the changes to the Brazilian household consumption pattern, it is important to address first the causes of this economic improvement. After Brazil’s economic stabilization with the creation of a new currency, the Real, in the 90s, the country was able to start a new growth stage. The end of inflation and the insertion of the targeting regime for price variation, the adoption of targets for the primary surplus, restructuring of the banking system, the fiscal responsibility law and economic liberalization were the basis for the country project itself in the future and not only resolve situational problems.

Additionally, at the beginning of the 2000s, a new economic power emerged: China. The Chinese growth, especially from the export of products with low added value, provided the world an increase in the global demand for raw material, with emphasis on the material increase in commodities prices (oil, steel, soybean, among others), traded mostly in US Dollars.

Brazil, a country which exports mostly commodities, benefited, to a large ex-tent, from this change in the world’s scenario. It is worth to mention that in 2002, with investors’ distrust in the new left-wing government, the Real surpassed R$ 4.00 for each US Dollar. That is, the export sector, on one side, benefited from the increase in commodities prices and, on the other side, from the depreciation of Real, which further increased the gains.

From this moment on, the Government could put some economic policies into practice to speed up the pace of growth. On the monetary aspect, Bra-zil’s Central Bank made two important achievements: greater accumulation of international reserves and reduction of the base interest rate. On the tax aspect, the Government increased income distribution through social pro-grams, with emphasis the Bolsa Família (Family Allowance), but also managed to reach the targets for the primary surplus, i.e., making savings that enabled it to pay the public debt interest.

54 THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES 55

In addition to these measures by the Government, the private sector realized larger gains given the strong growth of the global economy, which enabled it to increase the level of investments in the country through the most diverse sectors of economy (agriculture, retail and services and industry). Joint actions of government and private sector stimulated the national economy, which led to records in job creation, increasing the average income of Brazilian citizens.

Another factor that had an influence on the population income was the credit. The solid banking system and increased investments in new branches throughout the country enabled the insertion of Brazilian families in this seg-ment. People could open new bank accounts and acquire credit cards, which are now considered an affordable property.

Given the new framework of Brazilian social classes, families could increase their income, which provided them both growth in their spending and im-provement in the quality of that spending.

The evolution of the middle class in Brazil

The deep changes in the Brazilian socio-economic framework during the last decade happened in such a pace and magnitude that surprised the most opti-mistic forecasts until then. It was thought that to initiate a process of reversal and equalization of Brazil’s most severe and chronic problem – the huge and increasing income inequality –, the country would have to remain for decades in a virtuous and sustained growth cycle. It was believed that, nevertheless, this would happen at a gradual and slow pace, requiring more than a decade to deliver results that would actually impact income distribution.

The new middle class has been gaining, throughout the years, more and more space in the Brazilian consumer market. There are thousands of people who now have access to a variety of products and services. The economic stability and the expansion of employment, income and credit, combined with gov-ernment social welfare policies, were the main factors that provided families the possibility to rise to the new middle class.

Nevertheless, it is necessary to consider that such positive factors could only occur due to the existence of two primary circumstances, without which none of the causes pointed out would deliver the results observed:

price stability (inflation) and the unprecedented and sustained global economic growth cycle.

In order to demonstrate the magnitude of economic data that supported the improvement in Brazilian social conditions, only over the past decade, the total amount of credit for individuals and legal entities, with non-earmarked funds, grew 212 % in real terms, which means an average real growth of 12 % per annum. In 2009, the amount of credit had already surpassed R$ 1 trillion, i.e., virtually the total consumption potential of the Brazilian middle class, as we will discuss later.

The average real income, by its turn, grew 4.9 % between 2002 and 2010, and the unemployment rate, which was 11.7 % in 2002, reached 6.7 % in 2010. Real salaries grew around 30 % in the same period.

The scenario described was so important to the constitution of a Brazilian middle class in a more structured way that nor even the 2008 international financial crisis, that restricted consumption as a whole, was enough to break the virtuous cycle of reduction in social inequalities.

According to a survey conducted by FecomercioSP, based on data from the House-hold Budget Survey – POF (2009) of IBGE, there are a little more than 57 million families in Brazil. Of this total, more than half of the families are in the middle class (52 %). Other income classes are divided as follows: class E (22 %), class D (17 %), class B (5 %) and class A (4 %). In this study, class C is the so called middle class.

Comparing data from the previous POF (2002), an even clearer scenario of rise of the middle class throughout the years can be observed. In 2002, the middle class represented only 19 million of families (39 % of the total). In six years, what we see is the insertion of 11 million families into the middle class, amounting to 30 million.

A migration process from the lower income families to the middle class can also be noticed, evidencing that, with a stable economic scenario, families man-aged to change their social level. A direct evidence of this is that between 2002 and 2008 there was a decrease in the number of families belonging to classes D and E. The average household income of the new middle class is R$ 2,857.00 per month, i.e., virtually the same verified in the aggregate of Brazilian families (R$ 2,928.00). Accordingly, when analyzing the annual consumption potential of the Brazilian families (R$ 2.03 trillion), it can be noticed that the middle class corresponds virtually to half of such amount (R$ 1.03 trillion).

56 THE BRAZILIAN BUSINESS ENVIRONMENT: REALITY AND CHALLENGES

The transformations brought to the Brazilian scenario by social changes

The consumption potential of middle class families is so significant that is even higher than that registered by the other classes, opening a range of business opportunities for Brazilian companies. The retail segment was one of the sec-tors which benefited the most from the change in the Brazilian population so-cial status. From 2004 to 2010, the average growth rate of the retail segment in Brazil was 9 % per annum, providing an real increase of 82 % of sales during the period. That is, in six years, the retail segment almost doubled in size.