tesla motors, inc.(tsla) - jefferies · respondents considering alternative fuel vehicles and 7%...

TRANSCRIPT

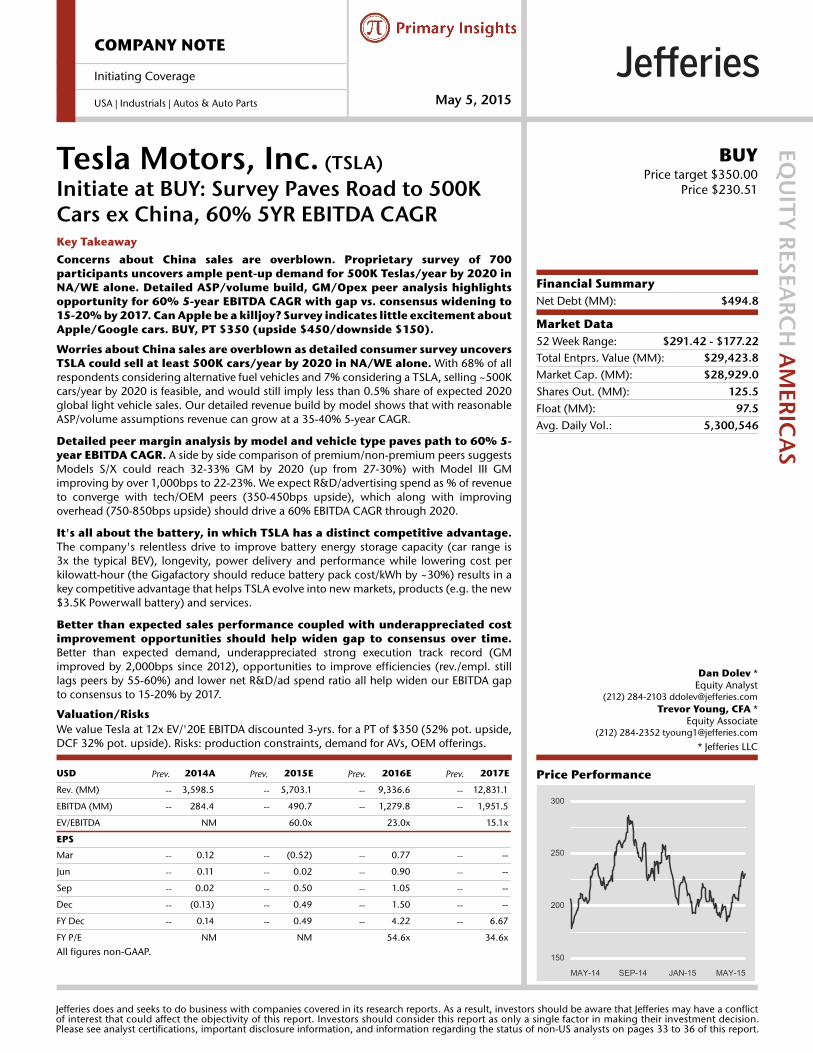

USD Prev. 2014A Prev. 2015E Prev. 2016E Prev. 2017E

Rev. (MM) -- 3,598.5 -- 5,703.1 -- 9,336.6 -- 12,831.1

EBITDA (MM) -- 284.4 -- 490.7 -- 1,279.8 -- 1,951.5

EV/EBITDA NM 60.0x 23.0x 15.1x

EPS

Mar -- 0.12 -- (0.52) -- 0.77 -- --

Jun -- 0.11 -- 0.02 -- 0.90 -- --

Sep -- 0.02 -- 0.50 -- 1.05 -- --

Dec -- (0.13) -- 0.49 -- 1.50 -- --

FY Dec -- 0.14 -- 0.49 -- 4.22 -- 6.67

FY P/E NM NM 54.6x 34.6x

All figures non-GAAP.

Price Performance

MAY-14 SEP-14 JAN-15 MAY-15

300

250

200

150

COMPANY NOTE

Initiating Coverage

USA | Industrials | Autos & Auto Parts May 5, 2015

Tesla Motors, Inc. (TSLA)Initiate at BUY: Survey Paves Road to 500KCars ex China, 60% 5YR EBITDA CAGR

EQU

ITY R

ESEARC

H A

MERIC

AS

BUYPrice target $350.00

Price $230.51

Financial SummaryNet Debt (MM): $494.8

Market Data52 Week Range: $291.42 - $177.22Total Entprs. Value (MM): $29,423.8Market Cap. (MM): $28,929.0Shares Out. (MM): 125.5Float (MM): 97.5Avg. Daily Vol.: 5,300,546

Dan Dolev *Equity Analyst

(212) 284-2103 [email protected] Young, CFA *

Equity Associate(212) 284-2352 [email protected]

* Jefferies LLC

Key TakeawayConcerns about China sales are overblown. Proprietary survey of 700participants uncovers ample pent-up demand for 500K Teslas/year by 2020 inNA/WE alone. Detailed ASP/volume build, GM/Opex peer analysis highlightsopportunity for 60% 5-year EBITDA CAGR with gap vs. consensus widening to15-20% by 2017. Can Apple be a killjoy? Survey indicates little excitement aboutApple/Google cars. BUY, PT $350 (upside $450/downside $150).

Worries about China sales are overblown as detailed consumer survey uncoversTSLA could sell at least 500K cars/year by 2020 in NA/WE alone. With 68% of allrespondents considering alternative fuel vehicles and 7% considering a TSLA, selling ~500Kcars/year by 2020 is feasible, and would still imply less than 0.5% share of expected 2020global light vehicle sales. Our detailed revenue build by model shows that with reasonableASP/volume assumptions revenue can grow at a 35-40% 5-year CAGR.

Detailed peer margin analysis by model and vehicle type paves path to 60% 5-year EBITDA CAGR. A side by side comparison of premium/non-premium peers suggestsModels S/X could reach 32-33% GM by 2020 (up from 27-30%) with Model III GMimproving by over 1,000bps to 22-23%. We expect R&D/advertising spend as % of revenueto converge with tech/OEM peers (350-450bps upside), which along with improvingoverhead (750-850bps upside) should drive a 60% EBITDA CAGR through 2020.

It's all about the battery, in which TSLA has a distinct competitive advantage.The company's relentless drive to improve battery energy storage capacity (car range is3x the typical BEV), longevity, power delivery and performance while lowering cost perkilowatt-hour (the Gigafactory should reduce battery pack cost/kWh by ~30%) results in akey competitive advantage that helps TSLA evolve into new markets, products (e.g. the new$3.5K Powerwall battery) and services.

Better than expected sales performance coupled with underappreciated costimprovement opportunities should help widen gap to consensus over time.Better than expected demand, underappreciated strong execution track record (GMimproved by 2,000bps since 2012), opportunities to improve efficiencies (rev./empl. stilllags peers by 55-60%) and lower net R&D/ad spend ratio all help widen our EBITDA gapto consensus to 15-20% by 2017.

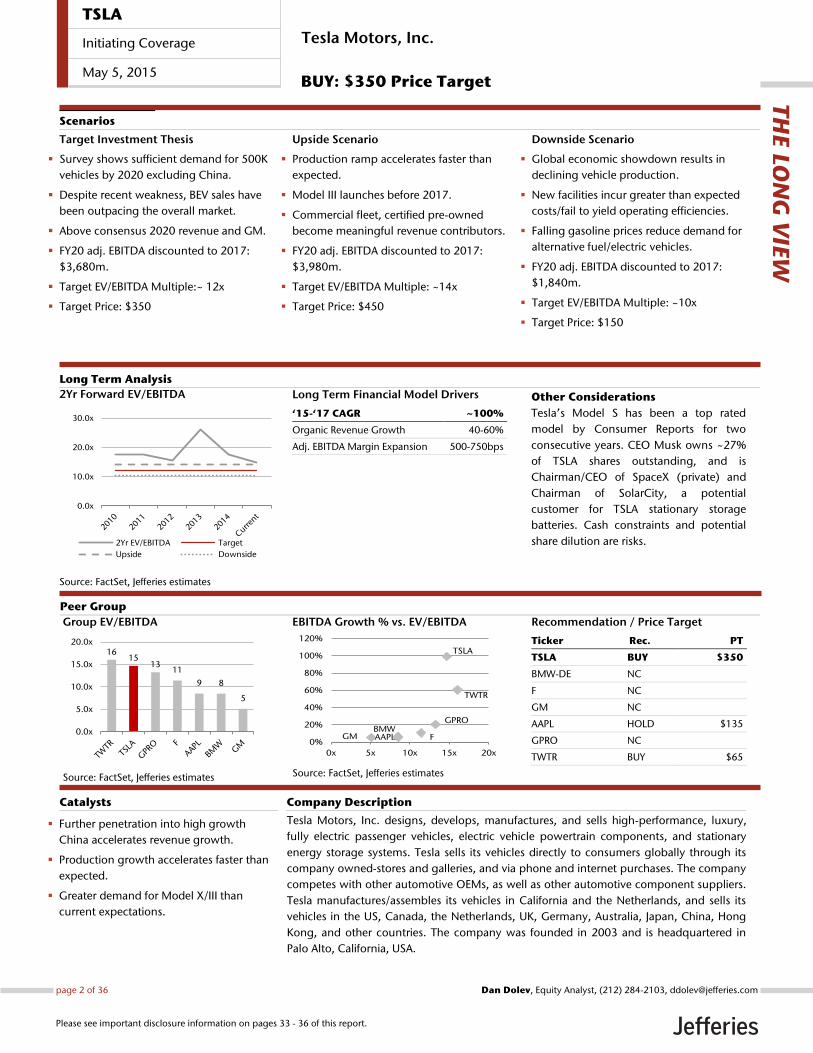

Valuation/RisksWe value Tesla at 12x EV/'20E EBITDA discounted 3-yrs. for a PT of $350 (52% pot. upside,DCF 32% pot. upside). Risks: production constraints, demand for AVs, OEM offerings.

Jefferies does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that Jefferies may have a conflictof interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.Please see analyst certifications, important disclosure information, and information regarding the status of non-US analysts on pages 33 to 36 of this report.

Long Term Financial Model Drivers

‘15-‘17 CAGR ~100%

Organic Revenue Growth 40-60%

Adj. EBITDA Margin Expansion 500-750bps

Other Considerations

Tesla’s Model S has been a top rated

model by Consumer Reports for two

consecutive years. CEO Musk owns ~27%

of TSLA shares outstanding, and is

Chairman/CEO of SpaceX (private) and

Chairman of SolarCity, a potential

customer for TSLA stationary storage

batteries. Cash constraints and potential

share dilution are risks.

2Yr Forward EV/EBITDA

Source: FactSet, Jefferies estimates

0.0x

10.0x

20.0x

30.0x

2Yr EV/EBITDA Target

Upside Downside

Tesla Motors, Inc. designs, develops, manufactures, and sells high-performance, luxury,

fully electric passenger vehicles, electric vehicle powertrain components, and stationary

energy storage systems. Tesla sells its vehicles directly to consumers globally through its

company owned-stores and galleries, and via phone and internet purchases. The company

competes with other automotive OEMs, as well as other automotive component suppliers.

Tesla manufactures/assembles its vehicles in California and the Netherlands, and sells its

vehicles in the US, Canada, the Netherlands, UK, Germany, Australia, Japan, China, Hong

Kong, and other countries. The company was founded in 2003 and is headquartered in

Palo Alto, California, USA.

Further penetration into high growth

China accelerates revenue growth.

Production growth accelerates faster than

expected.

Greater demand for Model X/III than

current expectations.

Catalysts

Target Investment Thesis

Survey shows sufficient demand for 500K

vehicles by 2020 excluding China.

Despite recent weakness, BEV sales have

been outpacing the overall market.

Above consensus 2020 revenue and GM.

FY20 adj. EBITDA discounted to 2017:

$3,680m.

Target EV/EBITDA Multiple:~ 12x

Target Price: $350

Upside Scenario

Production ramp accelerates faster than

expected.

Model III launches before 2017.

Commercial fleet, certified pre-owned

become meaningful revenue contributors.

FY20 adj. EBITDA discounted to 2017:

$3,980m.

Target EV/EBITDA Multiple: ~14x

Target Price: $450

Downside Scenario

Global economic showdown results in

declining vehicle production.

New facilities incur greater than expected

costs/fail to yield operating efficiencies.

Falling gasoline prices reduce demand for

alternative fuel/electric vehicles.

FY20 adj. EBITDA discounted to 2017:

$1,840m.

Target EV/EBITDA Multiple: ~10x

Target Price: $150

Long Term Analysis

Scenarios

Group EV/EBITDA

Source: FactSet, Jefferies estimates

1615

1311

9 8

5

0.0x

5.0x

10.0x

15.0x

20.0x

EBITDA Growth % vs. EV/EBITDA

Source: FactSet, Jefferies estimates

TWTR

TSLA

GPRO

FBMWAAPLGM

0%

20%

40%

60%

80%

100%

120%

0x 5x 10x 15x 20x

Recommendation / Price Target

Ticker Rec. PT

TSLA BUY $350

BMW-DE NC

F NC

GM NC

AAPL HOLD $135

GPRO NC

TWTR BUY $65

Company Description

TH

E LO

NG

VIE

W

Peer Group

Tesla Motors, Inc.

BUY: $350 Price Target

TSLA

Initiating Coverage

May 5, 2015

page 2 of 36 , Equity Analyst, (212) 284-2103, [email protected] Dolev

Please see important disclosure information on pages 33 - 36 of this report.

Executive Summary Worries about China sales are overblown as detailed consumer survey

uncovers TSLA could sell at least 500K cars/year by 2020 in NA/WE alone.

With 68% of all respondents considering alternative fuel vehicles and 7% considering a

TSLA, selling ~500K cars/year by 2020 is feasible and even conservative given an

aggressive ~80% haircut to NA/WE 2020E TAM of ~35m vehicles. Our detailed revenue

build by model shows that with reasonable ASP/volume assumptions revenue can grow

at a 35-40% 5-year CAGR.

Detailed peer margin analysis by model and vehicle type paves path to 60%

5-year EBITDA CAGR. A side by side comparison of premium/non-premium peers

suggests Models S/X could reach 32-33% GM by 2020 (up from 27-30%) with Model III

GM improving by over 1,000bps to 22-23%. We expect R&D/advertising spend as % of

revenue to converge with tech/OEM peers (350-450bps upside), which along with

improving overhead (750-850bps upside) should drive a 60% EBITDA CAGR through

2020.

It's all about the battery, in which TSLA has a distinct competitive advantage.

The company's relentless drive to improve battery energy storage capacity (car range is

3x the typical BEV), longevity, power delivery and performance while lowering cost per

kilowatt-hour (the Gigafactory should reduce battery pack cost/kWh by ~30%) results in a

key competitive advantage that helps TSLA evolve into new markets, products (e.g. the

new $3.5K Powerwall battery) and services.

Better than expected sales performance coupled with underappreciated cost

improvement opportunities should help widen gap to consensus over time.

Better than expected demand, underappreciated strong execution track record (GM

improved by 2,000bps since 2012), opportunities to improve efficiencies (rev./empl. still

lags peers by 55-60%) and lower net R&D/ad spend ratio all help widen our EBITDA gap

to consensus to 15-20% by 2017.

Growing BEV penetration suggests 500K/year is still conservative. TSLA

accounts for an estimated 25% of current US BEV sales (65K). Assuming the BEV category

slows to a 65% CAGR (vs. 85% between ’11-’14, ~4x faster than overall AVs), implies

~800K BEVs by 2020, so that simply maintaining TSLA’s current share implies ~215K

Teslas in North America, or over 430K including Western Europe. Plus, our estimate of

~500K Teslas by 2020 would still imply less than 0.5% share of expected global light

vehicle sales by 2020.

Valuation We value Tesla at ~12x EV/'20E EBITDA discounted three years for a PT of $350 (+52%

potential upside, DCF +32% potential upside).

Risks Key downside risks to our thesis include: 1) Tesla unable to ramp production/meet

timelines for new models, 2) legal issues selling cars directly in many US states persist, 3)

large OEM competitors develop comparable BEV vehicles with similar performance

attributes, 4) global economic slowdown results in declining vehicle demand, 5) falling

gasoline prices reduce demand for alternative fuel/electric vehicles, and 6) cash

constraints from sizeable CapEx demands result in potential share dilution.

TSLA

Initiating Coverage

May 5, 2015

page 3 of 36 , Equity Analyst, (212) 284-2103, [email protected] Dolev

Please see important disclosure information on pages 33 - 36 of this report.

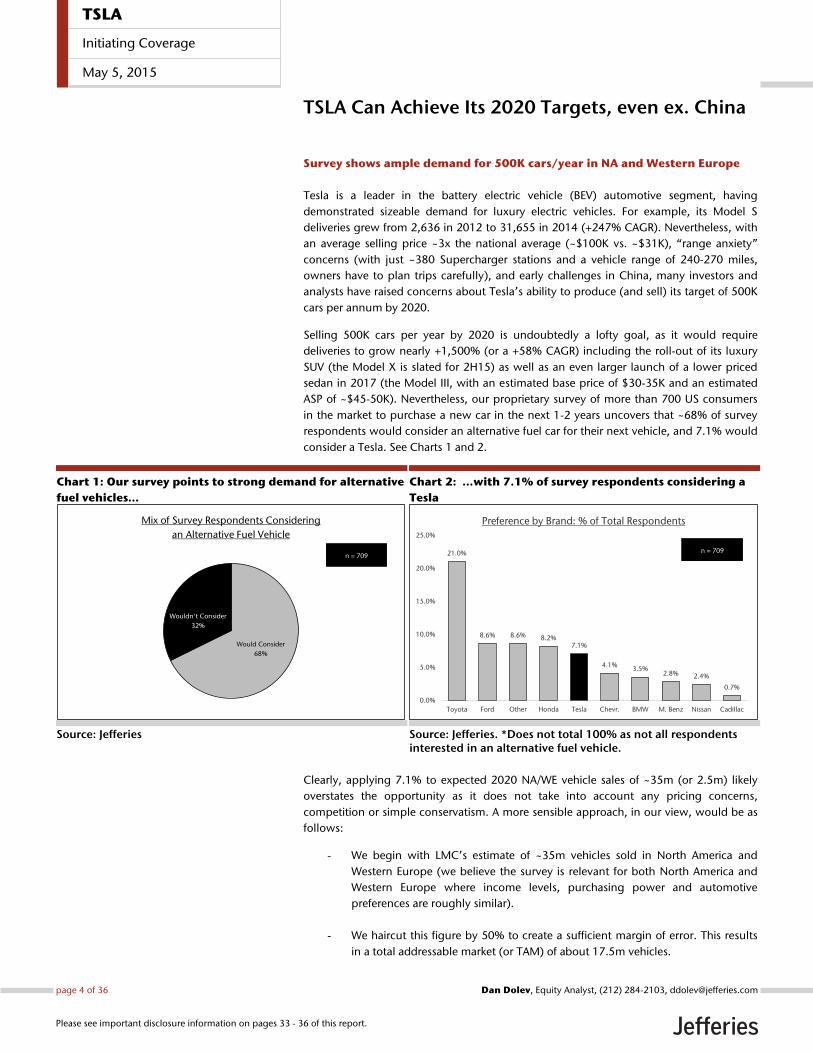

TSLA Can Achieve Its 2020 Targets, even ex. China

Survey shows ample demand for 500K cars/year in NA and Western Europe

Tesla is a leader in the battery electric vehicle (BEV) automotive segment, having

demonstrated sizeable demand for luxury electric vehicles. For example, its Model S

deliveries grew from 2,636 in 2012 to 31,655 in 2014 (+247% CAGR). Nevertheless, with

an average selling price ~3x the national average (~$100K vs. ~$31K), “range anxiety”

concerns (with just ~380 Supercharger stations and a vehicle range of 240-270 miles,

owners have to plan trips carefully), and early challenges in China, many investors and

analysts have raised concerns about Tesla’s ability to produce (and sell) its target of 500K

cars per annum by 2020.

Selling 500K cars per year by 2020 is undoubtedly a lofty goal, as it would require

deliveries to grow nearly +1,500% (or a +58% CAGR) including the roll-out of its luxury

SUV (the Model X is slated for 2H15) as well as an even larger launch of a lower priced

sedan in 2017 (the Model III, with an estimated base price of $30-35K and an estimated

ASP of ~$45-50K). Nevertheless, our proprietary survey of more than 700 US consumers

in the market to purchase a new car in the next 1-2 years uncovers that ~68% of survey

respondents would consider an alternative fuel car for their next vehicle, and 7.1% would

consider a Tesla. See Charts 1 and 2.

Chart 1: Our survey points to strong demand for alternative

fuel vehicles…

Source: Jefferies

Chart 2: …with 7.1% of survey respondents considering a

Tesla

Source: Jefferies. *Does not total 100% as not all respondents interested in an alternative fuel vehicle.

Clearly, applying 7.1% to expected 2020 NA/WE vehicle sales of ~35m (or 2.5m) likely

overstates the opportunity as it does not take into account any pricing concerns,

competition or simple conservatism. A more sensible approach, in our view, would be as

follows:

- We begin with LMC’s estimate of ~35m vehicles sold in North America and

Western Europe (we believe the survey is relevant for both North America and

Western Europe where income levels, purchasing power and automotive

preferences are roughly similar).

- We haircut this figure by 50% to create a sufficient margin of error. This results

in a total addressable market (or TAM) of about 17.5m vehicles.

Would Consider

68%

Wouldn't Consider

32%

Mix of Survey Respondents Considering

an Alternative Fuel Vehicle

n = 709 21.0%

8.6% 8.6% 8.2%7.1%

4.1%3.5%

2.8% 2.4%

0.7%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Toyota Ford Other Honda Tesla Chevr. BMW M. Benz Nissan Cadillac

Preference by Brand: % of Total Respondents

n = 709

TSLA

Initiating Coverage

May 5, 2015

page 4 of 36 , Equity Analyst, (212) 284-2103, [email protected] Dolev

Please see important disclosure information on pages 33 - 36 of this report.

- Applying our survey’s 7.1% penetration rate to 17.5m results in ~1.2m vehicles.

- The survey shows that only about ~42% of potential TSLA buyers are also willing

to pay ~$40K+ for a TSLA (approximately representative of Tesla’s estimated

base price for the upcoming Model III), implying ~520K cars/year.

We note that our view is likely conservative given that it does not account for any sales

outside NA/WE (see discussion below of the China opportunity). See Charts 3 and 4.

Chart 3: Only 42% of respondents interested in a Tesla are

willing to pay more than $40K…

Source: Jefferies

Chart 4: …which suggests selling ~520K cars by 2020 is

conceivable and perhaps even conservative

Source: LMC, Jefferies

Achieving 500K cars/year is feasible given that:

1. BEVs are gaining share within the alternative category

Although total US light vehicle sales have rebounded following the financial crisis,

reaching a CAGR of ~9% over the last four years, sales of alternative fuel vehicles have

grown more than 2x that rate (22.7% CAGR). Interestingly, while the alternative fuel

vehicle segment has historically consisted of predominantly hybrid vehicles (in 2011,

hybrids were ~70% of the alternative fuel vehicle sales in the US) sales of BEVs have far

outgrown the segment. In fact, US sales data suggests that BEV sales have grown at an

~85% CAGR since 2011, reaching just over 63K vehicles sold in 2014 (with an estimated

~17,400 cars delivered in North America, we estimate TSLA likely accounted for one-

quarter of US BEVs). As such, it is no surprise that BEVs as a percent of total alternative

vehicle sales have nearly quadrupled in just four years (from 2.6% in 2011 to 8.9% in

2014). See Chart 5.

16%

42%

22%

12%

8%

0%

10%

20%

30%

40%

50%

Less than $20K $20K - $40K $40K - $60K $60K - $80K $80K+

Tesla Respondents Targeted Purchase Price

n = 50

42%

~35.0m

~17.5m

~1.2m

~520K

...of which 7.1%

interested in TLSA,

...of which ~42% agree

to price range

Tesla Hypothetical NA/WE Demand Analysis based on

2020 Production and Survey Results

...of which 50% for

Conservatism,

2020E NA/WE

Production Estimate

TSLA

Initiating Coverage

May 5, 2015

page 5 of 36 , Equity Analyst, (212) 284-2103, [email protected] Dolev

Please see important disclosure information on pages 33 - 36 of this report.

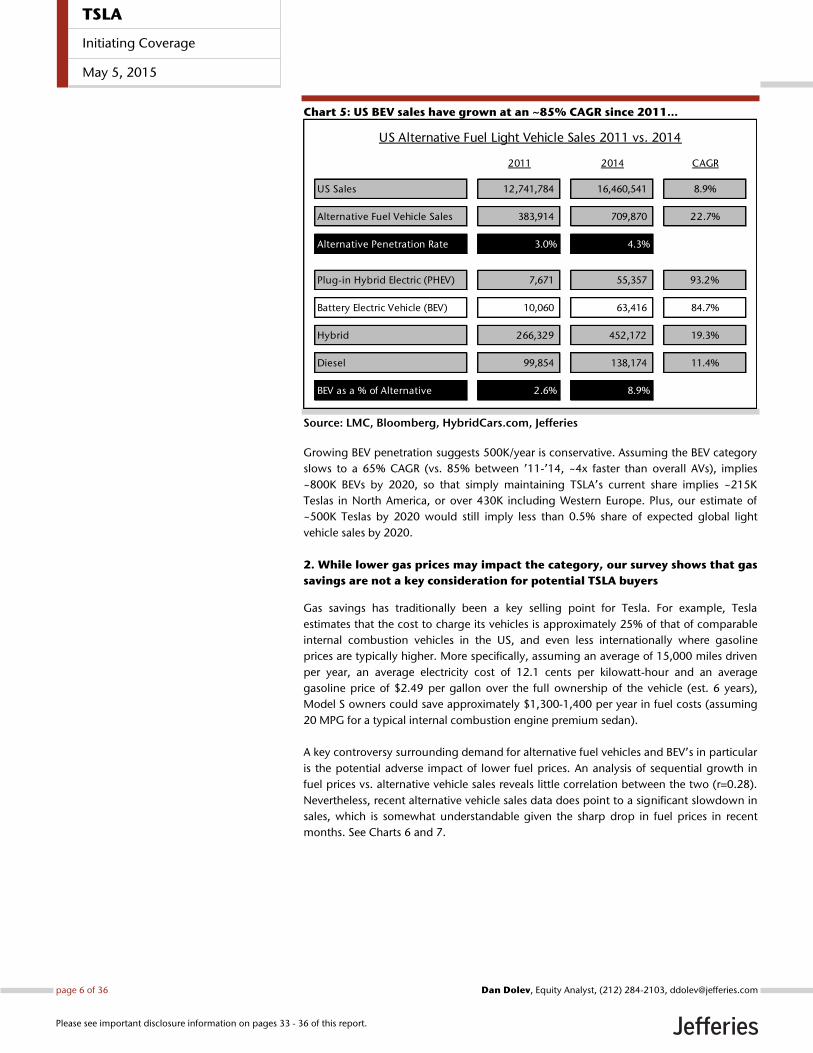

Chart 5: US BEV sales have grown at an ~85% CAGR since 2011…

Source: LMC, Bloomberg, HybridCars.com, Jefferies

Growing BEV penetration suggests 500K/year is conservative. Assuming the BEV category

slows to a 65% CAGR (vs. 85% between ’11-’14, ~4x faster than overall AVs), implies

~800K BEVs by 2020, so that simply maintaining TSLA’s current share implies ~215K

Teslas in North America, or over 430K including Western Europe. Plus, our estimate of

~500K Teslas by 2020 would still imply less than 0.5% share of expected global light

vehicle sales by 2020.

2. While lower gas prices may impact the category, our survey shows that gas

savings are not a key consideration for potential TSLA buyers

Gas savings has traditionally been a key selling point for Tesla. For example, Tesla

estimates that the cost to charge its vehicles is approximately 25% of that of comparable

internal combustion vehicles in the US, and even less internationally where gasoline

prices are typically higher. More specifically, assuming an average of 15,000 miles driven

per year, an average electricity cost of 12.1 cents per kilowatt-hour and an average

gasoline price of $2.49 per gallon over the full ownership of the vehicle (est. 6 years),

Model S owners could save approximately $1,300-1,400 per year in fuel costs (assuming

20 MPG for a typical internal combustion engine premium sedan).

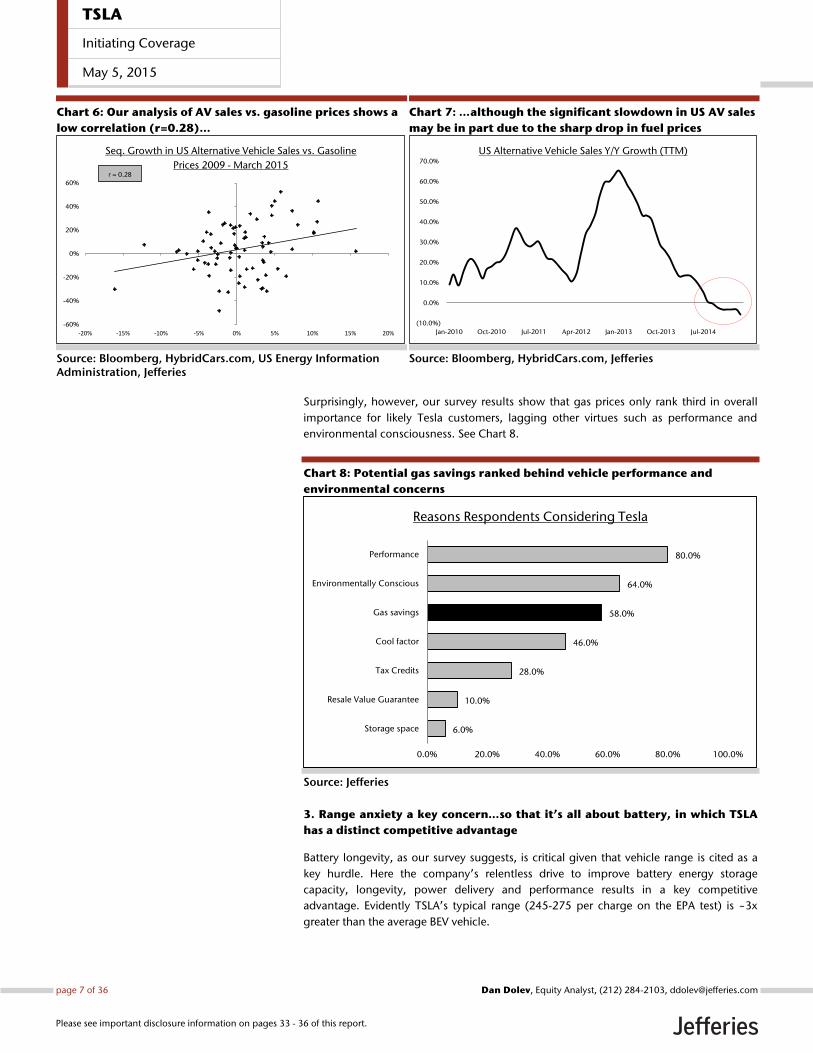

A key controversy surrounding demand for alternative fuel vehicles and BEV’s in particular

is the potential adverse impact of lower fuel prices. An analysis of sequential growth in

fuel prices vs. alternative vehicle sales reveals little correlation between the two (r=0.28).

Nevertheless, recent alternative vehicle sales data does point to a significant slowdown in

sales, which is somewhat understandable given the sharp drop in fuel prices in recent

months. See Charts 6 and 7.

US Alternative Fuel Light Vehicle Sales 2011 vs. 2014

2011 2014 CAGR

US Sales 12,741,784 16,460,541 8.9%

Alternative Fuel Vehicle Sales 383,914 709,870 22.7%

Alternative Penetration Rate 3.0% 4.3%

Plug-in Hybrid Electric (PHEV) 7,671 55,357 93.2%

Battery Electric Vehicle (BEV) 10,060 63,416 84.7%

Hybrid 266,329 452,172 19.3%

Diesel 99,854 138,174 11.4%

BEV as a % of Alternative 2.6% 8.9%

TSLA

Initiating Coverage

May 5, 2015

page 6 of 36 , Equity Analyst, (212) 284-2103, [email protected] Dolev

Please see important disclosure information on pages 33 - 36 of this report.

Chart 6: Our analysis of AV sales vs. gasoline prices shows a

low correlation (r=0.28)…

Source: Bloomberg, HybridCars.com, US Energy Information Administration, Jefferies

Chart 7: …although the significant slowdown in US AV sales

may be in part due to the sharp drop in fuel prices

Source: Bloomberg, HybridCars.com, Jefferies

Surprisingly, however, our survey results show that gas prices only rank third in overall

importance for likely Tesla customers, lagging other virtues such as performance and

environmental consciousness. See Chart 8.

Chart 8: Potential gas savings ranked behind vehicle performance and

environmental concerns

Source: Jefferies

3. Range anxiety a key concern…so that it’s all about battery, in which TSLA

has a distinct competitive advantage

Battery longevity, as our survey suggests, is critical given that vehicle range is cited as a

key hurdle. Here the company’s relentless drive to improve battery energy storage

capacity, longevity, power delivery and performance results in a key competitive

advantage. Evidently TSLA’s typical range (245-275 per charge on the EPA test) is ~3x

greater than the average BEV vehicle.

-60%

-40%

-20%

0%

20%

40%

60%

-20% -15% -10% -5% 0% 5% 10% 15% 20%

Seq. Growth in US Alternative Vehicle Sales vs. Gasoline

Prices 2009 - March 2015r = 0.28

(10.0%)

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

Jan-2010 Oct-2010 Jul-2011 Apr-2012 Jan-2013 Oct-2013 Jul-2014

US Alternative Vehicle Sales Y/Y Growth (TTM)

6.0%

10.0%

28.0%

46.0%

58.0%

64.0%

80.0%

0.0% 20.0% 40.0% 60.0% 80.0% 100.0%

Storage space

Resale Value Guarantee

Tax Credits

Cool factor

Gas savings

Environmentally Conscious

Performance

Reasons Respondents Considering Tesla

TSLA

Initiating Coverage

May 5, 2015

page 7 of 36 , Equity Analyst, (212) 284-2103, [email protected] Dolev

Please see important disclosure information on pages 33 - 36 of this report.

However, despite its above average range, the survey also cites availability of charging

stations as a key hurdle. Fortunately, TSLA is addressing this problem by offering a

network of charging stations (e.g. Supercharger stations) free of charge to owners of

Model S vehicles with the 85 kWh battery pack. More specifically:

- TSLA’s Supercharger stations grew from 90 in February 2012 in North America

and in Europe to 380+ stations by year-end 2014 globally, including in Asia.

Earlier this year, TLSA noted that it plans to grow its Supercharger network by

over 50% in 2015. Using the stations, Model S vehicles with a new battery pack

can replenish 170 miles of range in 30 minutes for free.

- In addition, TSLA currently partners with ~1,000 locations (e.g. hotels) in Asia

and North America, where ~1,800 free connectors are available.

We note that Model S also incorporates a modular battery pack in the floor of the vehicle,

enabling it to be rapidly swapped out at certain of its service centers and specialized

commercial battery exchange facilities that are likely to be available in the future. See

Chart 9.

Chart 9: Vehicle range and the availability of charging stations are key

concerns, which Tesla is addressing

Source: Jefferies

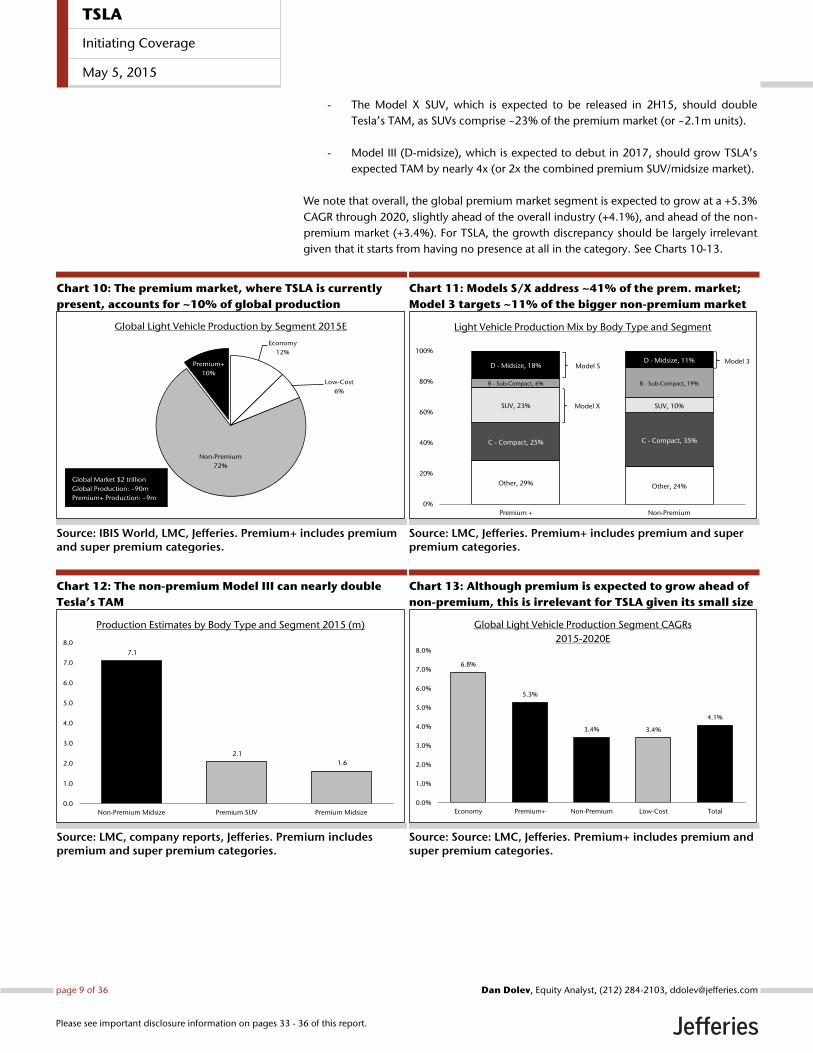

4. Model III helps double Tesla’s addressable market

Tesla’s Model S (and likely upcoming Model X) competes with offerings from Audi, BMW,

Lexus, Mercedes-Benz and Porsche, among others, in the estimated $500bn+

premium/luxury segment (~10% of global production). The segment is loosely defined by

cost (we estimate that vehicles in the category cost in excess of $50,000), performance

(e.g., the Model S can accelerate 0-60mph in under 4 seconds), and high quality

features/finishes (e.g., Tesla’s Model S features a 17-inch touchscreen with internet

connectivity, while some models feature Nappa leather seats). A detailed analysis of

market segment by vehicle body type reveals that:

- Tesla’s Model S sedan currently addresses just ~18% of the midsize premium

market (or a 1.6m unit TAM per annum).

18.3%

23.7%

24.6%

48.5%

71.5%

80.5%

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0% 70.0% 80.0% 90.0%

Battery Decay over Time

Type of Models Available

Charging Time

Cost of Vehicle

Vehicle Range

Availability of Charging Stations

Reasons Respondents Not Considering an Electric Vehicle

TSLA

Initiating Coverage

May 5, 2015

page 8 of 36 , Equity Analyst, (212) 284-2103, [email protected] Dolev

Please see important disclosure information on pages 33 - 36 of this report.

- The Model X SUV, which is expected to be released in 2H15, should double

Tesla’s TAM, as SUVs comprise ~23% of the premium market (or ~2.1m units).

- Model III (D-midsize), which is expected to debut in 2017, should grow TSLA’s

expected TAM by nearly 4x (or 2x the combined premium SUV/midsize market).

We note that overall, the global premium market segment is expected to grow at a +5.3%

CAGR through 2020, slightly ahead of the overall industry (+4.1%), and ahead of the non-

premium market (+3.4%). For TSLA, the growth discrepancy should be largely irrelevant

given that it starts from having no presence at all in the category. See Charts 10-13.

Chart 10: The premium market, where TSLA is currently

present, accounts for ~10% of global production

Source: IBIS World, LMC, Jefferies. Premium+ includes premium and super premium categories.

Chart 11: Models S/X address ~41% of the prem. market;

Model 3 targets ~11% of the bigger non-premium market

Source: LMC, Jefferies. Premium+ includes premium and super premium categories.

Chart 12: The non-premium Model III can nearly double

Tesla’s TAM

Source: LMC, company reports, Jefferies. Premium includes premium and super premium categories.

Chart 13: Although premium is expected to grow ahead of

non-premium, this is irrelevant for TSLA given its small size

Source: Source: LMC, Jefferies. Premium+ includes premium and super premium categories.

Economy

12%

Low-Cost

6%

Non-Premium

72%

Premium+

10%

Global Light Vehicle Production by Segment 2015E

Global Market $2 trillion

Global Production: ~90m

Premium+ Production: ~9m

Other, 29% Other, 24%

C - Compact, 25% C - Compact, 35%

SUV, 23% SUV, 10%

B - Sub-Compact, 6% B - Sub-Compact, 19%

D - Midsize, 18%D - Midsize, 11%

0%

20%

40%

60%

80%

100%

Premium + Non-Premium

Light Vehicle Production Mix by Body Type and Segment

Model X

Model SModel 3

7.1

2.1

1.6

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

Non-Premium Midsize Premium SUV Premium Midsize

Production Estimates by Body Type and Segment 2015 (m)

6.8%

5.3%

3.4% 3.4%

4.1%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

Economy Premium+ Non-Premium Low-Cost Total

Global Light Vehicle Production Segment CAGRs

2015-2020E

TSLA

Initiating Coverage

May 5, 2015

page 9 of 36 , Equity Analyst, (212) 284-2103, [email protected] Dolev

Please see important disclosure information on pages 33 - 36 of this report.

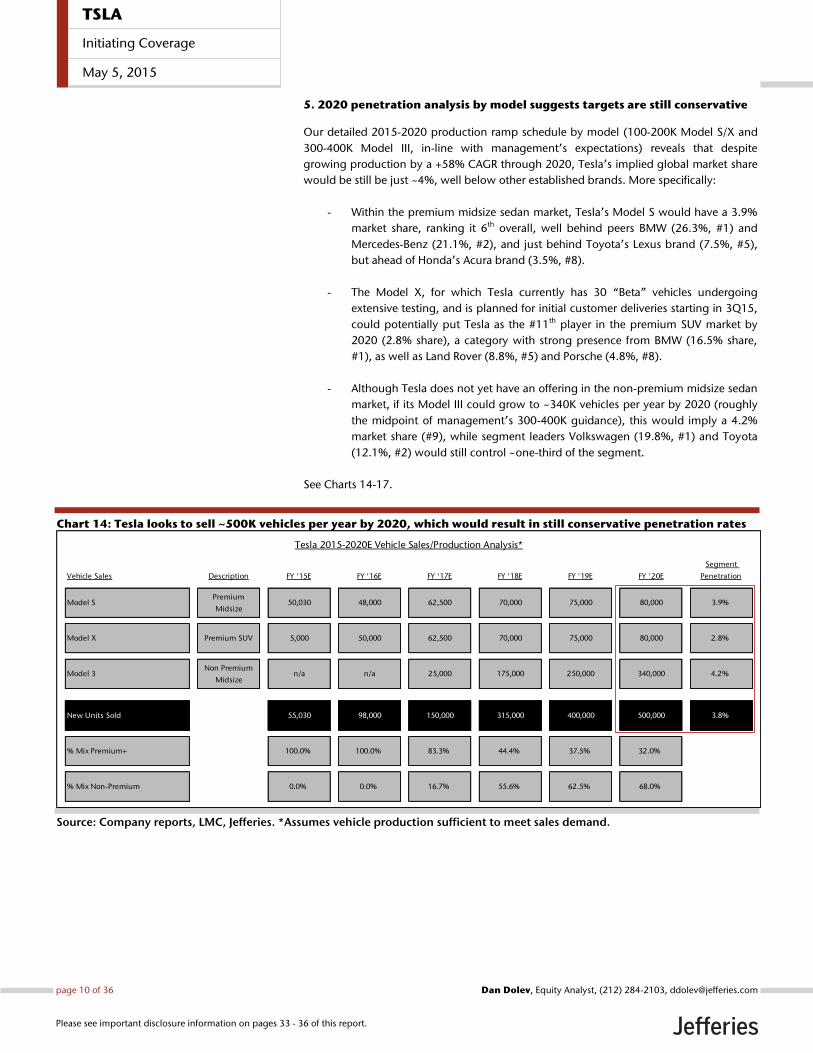

5. 2020 penetration analysis by model suggests targets are still conservative

Our detailed 2015-2020 production ramp schedule by model (100-200K Model S/X and

300-400K Model III, in-line with management’s expectations) reveals that despite

growing production by a +58% CAGR through 2020, Tesla’s implied global market share

would be still be just ~4%, well below other established brands. More specifically:

- Within the premium midsize sedan market, Tesla’s Model S would have a 3.9%

market share, ranking it 6th overall, well behind peers BMW (26.3%, #1) and

Mercedes-Benz (21.1%, #2), and just behind Toyota’s Lexus brand (7.5%, #5),

but ahead of Honda’s Acura brand (3.5%, #8).

- The Model X, for which Tesla currently has 30 “Beta” vehicles undergoing

extensive testing, and is planned for initial customer deliveries starting in 3Q15,

could potentially put Tesla as the #11th player in the premium SUV market by

2020 (2.8% share), a category with strong presence from BMW (16.5% share,

#1), as well as Land Rover (8.8%, #5) and Porsche (4.8%, #8).

- Although Tesla does not yet have an offering in the non-premium midsize sedan

market, if its Model III could grow to ~340K vehicles per year by 2020 (roughly

the midpoint of management’s 300-400K guidance), this would imply a 4.2%

market share (#9), while segment leaders Volkswagen (19.8%, #1) and Toyota

(12.1%, #2) would still control ~one-third of the segment.

See Charts 14-17.

Chart 14: Tesla looks to sell ~500K vehicles per year by 2020, which would result in still conservative penetration rates

Source: Company reports, LMC, Jefferies. *Assumes vehicle production sufficient to meet sales demand.

Tesla 2015-2020E Vehicle Sales/Production Analysis*

Vehicle Sales Description FY '15E FY '16E FY '17E FY '18E FY '19E FY '20E

Segment

Penetration

Model SPremium

Midsize50,030 48,000 62,500 70,000 75,000 80,000 3.9%

Model X Premium SUV 5,000 50,000 62,500 70,000 75,000 80,000 2.8%

Model 3Non Premium

Midsizen/a n/a 25,000 175,000 250,000 340,000 4.2%

New Units Sold 55,030 98,000 150,000 315,000 400,000 500,000 3.8%

% Mix Premium+ 100.0% 100.0% 83.3% 44.4% 37.5% 32.0%

% Mix Non-Premium 0.0% 0.0% 16.7% 55.6% 62.5% 68.0%

TSLA

Initiating Coverage

May 5, 2015

page 10 of 36 , Equity Analyst, (212) 284-2103, [email protected] Dolev

Please see important disclosure information on pages 33 - 36 of this report.

Chart 15: …including an implied 3.9%

share of the premium+ midsize market

Source: LMC, company reports, Jefferies. Premium also includes super premium.

Chart 16: …a 2.8% share of the

premium+ SUV market…

Source: LMC, company reports, Jefferies Premium also includes super premium

Chart 17: …and 4.2% of the non-prem.

midsize market as still conservative

Source: LMC, company reports, Jefferies

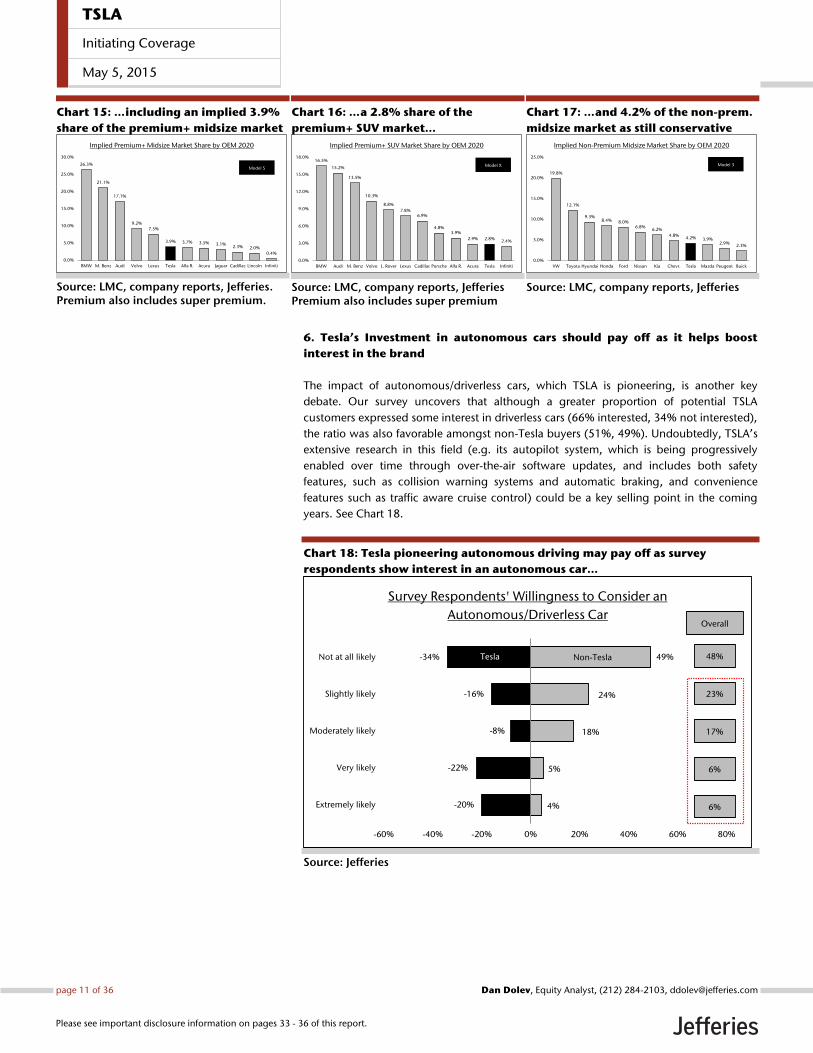

6. Tesla’s Investment in autonomous cars should pay off as it helps boost

interest in the brand

The impact of autonomous/driverless cars, which TSLA is pioneering, is another key

debate. Our survey uncovers that although a greater proportion of potential TSLA

customers expressed some interest in driverless cars (66% interested, 34% not interested),

the ratio was also favorable amongst non-Tesla buyers (51%, 49%). Undoubtedly, TSLA’s

extensive research in this field (e.g. its autopilot system, which is being progressively

enabled over time through over-the-air software updates, and includes both safety

features, such as collision warning systems and automatic braking, and convenience

features such as traffic aware cruise control) could be a key selling point in the coming

years. See Chart 18.

Chart 18: Tesla pioneering autonomous driving may pay off as survey

respondents show interest in an autonomous car…

Source: Jefferies

26.3%

21.1%

17.1%

9.2%

7.5%

3.9% 3.7% 3.5% 3.1% 2.3% 2.0%

0.4%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

BMW M. Benz Audi Volvo Lexus Tesla Alfa R. Acura Jaguar Cadillac Lincoln Infiniti

Implied Premium+ Midsize Market Share by OEM 2020

Model S

16.5%

15.2%

13.5%

10.3%

8.8%

7.8% 6.9%

4.8% 3.9%

2.9% 2.8% 2.4%

0.0%

3.0%

6.0%

9.0%

12.0%

15.0%

18.0%

BMW Audi M. Benz Volvo L. Rover Lexus Cadillac Porsche Alfa R. Acura Tesla Infiniti

Implied Premium+ SUV Market Share by OEM 2020

Model X

19.8%

12.1%

9.3% 8.4% 8.0%

6.8% 6.2%

4.8% 4.2% 3.9%

2.9% 2.3%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

VW Toyota Hyundai Honda Ford Nissan Kia Chevr. Tesla Mazda Peugeot Buick

Implied Non-Premium Midsize Market Share by OEM 2020

Model 3

-20%

-22%

-8%

-16%

-34%

4%

5%

18%

24%

49%

-60% -40% -20% 0% 20% 40% 60% 80%

Extremely likely

Very likely

Moderately likely

Slightly likely

Not at all likely

Survey Respondents' Willingness to Consider an

Autonomous/Driverless Car

Tesla Non-Tesla 48%

Overall

23%

17%

6%

6%

TSLA

Initiating Coverage

May 5, 2015

page 11 of 36 , Equity Analyst, (212) 284-2103, [email protected] Dolev

Please see important disclosure information on pages 33 - 36 of this report.

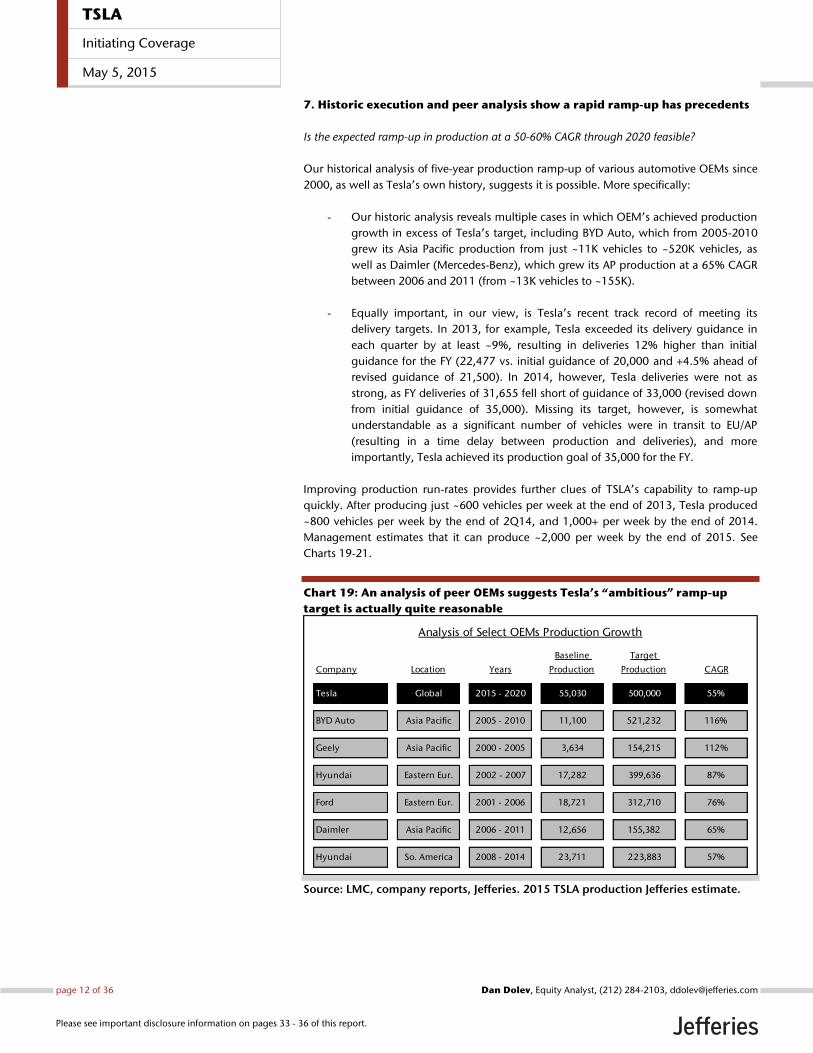

7. Historic execution and peer analysis show a rapid ramp-up has precedents

Is the expected ramp-up in production at a 50-60% CAGR through 2020 feasible?

Our historical analysis of five-year production ramp-up of various automotive OEMs since

2000, as well as Tesla’s own history, suggests it is possible. More specifically:

- Our historic analysis reveals multiple cases in which OEM’s achieved production

growth in excess of Tesla’s target, including BYD Auto, which from 2005-2010

grew its Asia Pacific production from just ~11K vehicles to ~520K vehicles, as

well as Daimler (Mercedes-Benz), which grew its AP production at a 65% CAGR

between 2006 and 2011 (from ~13K vehicles to ~155K).

- Equally important, in our view, is Tesla’s recent track record of meeting its

delivery targets. In 2013, for example, Tesla exceeded its delivery guidance in

each quarter by at least ~9%, resulting in deliveries 12% higher than initial

guidance for the FY (22,477 vs. initial guidance of 20,000 and +4.5% ahead of

revised guidance of 21,500). In 2014, however, Tesla deliveries were not as

strong, as FY deliveries of 31,655 fell short of guidance of 33,000 (revised down

from initial guidance of 35,000). Missing its target, however, is somewhat

understandable as a significant number of vehicles were in transit to EU/AP

(resulting in a time delay between production and deliveries), and more

importantly, Tesla achieved its production goal of 35,000 for the FY.

Improving production run-rates provides further clues of TSLA’s capability to ramp-up

quickly. After producing just ~600 vehicles per week at the end of 2013, Tesla produced

~800 vehicles per week by the end of 2Q14, and 1,000+ per week by the end of 2014.

Management estimates that it can produce ~2,000 per week by the end of 2015. See

Charts 19-21.

Chart 19: An analysis of peer OEMs suggests Tesla’s “ambitious” ramp-up

target is actually quite reasonable

Source: LMC, company reports, Jefferies. 2015 TSLA production Jefferies estimate.

Analysis of Select OEMs Production Growth

Company Location Years

Baseline

Production

Target

Production CAGR

Tesla Global 2015 - 2020 55,030 500,000 55%

BYD Auto Asia Pacific 2005 - 2010 11,100 521,232 116%

Geely Asia Pacific 2000 - 2005 3,634 154,215 112%

Hyundai Eastern Eur. 2002 - 2007 17,282 399,636 87%

Ford Eastern Eur. 2001 - 2006 18,721 312,710 76%

Daimler Asia Pacific 2006 - 2011 12,656 155,382 65%

Hyundai So. America 2008 - 2014 23,711 223,883 57%

TSLA

Initiating Coverage

May 5, 2015

page 12 of 36 , Equity Analyst, (212) 284-2103, [email protected] Dolev

Please see important disclosure information on pages 33 - 36 of this report.

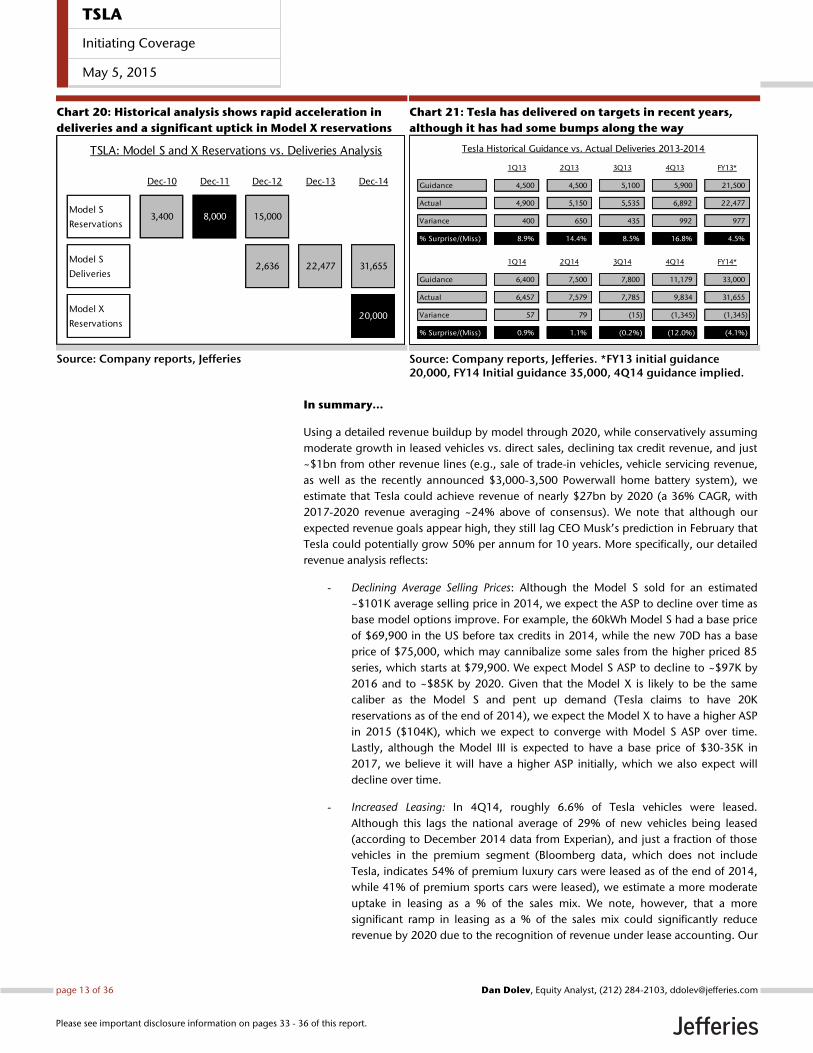

Chart 20: Historical analysis shows rapid acceleration in

deliveries and a significant uptick in Model X reservations

Source: Company reports, Jefferies

Chart 21: Tesla has delivered on targets in recent years,

although it has had some bumps along the way

Source: Company reports, Jefferies. *FY13 initial guidance 20,000, FY14 Initial guidance 35,000, 4Q14 guidance implied.

In summary…

Using a detailed revenue buildup by model through 2020, while conservatively assuming

moderate growth in leased vehicles vs. direct sales, declining tax credit revenue, and just

~$1bn from other revenue lines (e.g., sale of trade-in vehicles, vehicle servicing revenue,

as well as the recently announced $3,000-3,500 Powerwall home battery system), we

estimate that Tesla could achieve revenue of nearly $27bn by 2020 (a 36% CAGR, with

2017-2020 revenue averaging ~24% above of consensus). We note that although our

expected revenue goals appear high, they still lag CEO Musk’s prediction in February that

Tesla could potentially grow 50% per annum for 10 years. More specifically, our detailed

revenue analysis reflects:

- Declining Average Selling Prices: Although the Model S sold for an estimated

~$101K average selling price in 2014, we expect the ASP to decline over time as

base model options improve. For example, the 60kWh Model S had a base price

of $69,900 in the US before tax credits in 2014, while the new 70D has a base

price of $75,000, which may cannibalize some sales from the higher priced 85

series, which starts at $79,900. We expect Model S ASP to decline to ~$97K by

2016 and to ~$85K by 2020. Given that the Model X is likely to be the same

caliber as the Model S and pent up demand (Tesla claims to have 20K

reservations as of the end of 2014), we expect the Model X to have a higher ASP

in 2015 ($104K), which we expect to converge with Model S ASP over time.

Lastly, although the Model III is expected to have a base price of $30-35K in

2017, we believe it will have a higher ASP initially, which we also expect will

decline over time.

- Increased Leasing: In 4Q14, roughly 6.6% of Tesla vehicles were leased.

Although this lags the national average of 29% of new vehicles being leased

(according to December 2014 data from Experian), and just a fraction of those

vehicles in the premium segment (Bloomberg data, which does not include

Tesla, indicates 54% of premium luxury cars were leased as of the end of 2014,

while 41% of premium sports cars were leased), we estimate a more moderate

uptake in leasing as a % of the sales mix. We note, however, that a more

significant ramp in leasing as a % of the sales mix could significantly reduce

revenue by 2020 due to the recognition of revenue under lease accounting. Our

TSLA: Model S and X Reservations vs. Deliveries Analysis

Dec-10 Dec-11 Dec-12 Dec-13 Dec-14

Model S

Reservations3,400 8,000 15,000

Model S

Deliveries2,636 22,477 31,655

Model X

Reservations20,000

Tesla Historical Guidance vs. Actual Deliveries 2013-2014

1Q13 2Q13 3Q13 4Q13 FY13*

Guidance 4,500 4,500 5,100 5,900 21,500

Actual 4,900 5,150 5,535 6,892 22,477

Variance 400 650 435 992 977

% Surprise/(Miss) 8.9% 14.4% 8.5% 16.8% 4.5%

1Q14 2Q14 3Q14 4Q14 FY14*

Guidance 6,400 7,500 7,800 11,179 33,000

Actual 6,457 7,579 7,785 9,834 31,655

Variance 57 79 (15) (1,345) (1,345)

% Surprise/(Miss) 0.9% 1.1% (0.2%) (12.0%) (4.1%)

TSLA

Initiating Coverage

May 5, 2015

page 13 of 36 , Equity Analyst, (212) 284-2103, [email protected] Dolev

Please see important disclosure information on pages 33 - 36 of this report.

analysis further assumes ~36 month leases on average and an estimated residual

value of 47%.

- Decreasing Tax Credits: Although Tesla generated $216m in tax credit revenue in

2014, our 2020 revenue build assumes tax credit revenue declines to ~$95m in

2015, and declines to just $15-20m by 2020. Given uncertainty around the

continued marketability of tax credits, despite increasingly difficult emission

standards, our estimates decline over time for conservatism.

- Modest Increase in Service & Other Revenue: To align with new reporting

segments, we combine powertrain sales, vehicle services, trade-in sales, and

stationary storage sales into the Service & Other revenue segment. Historical

restatements are not yet available, but we estimate that the segment will

comprise just 5-10% of revenue over time, starting at ~$350m in 2015 (helped

by new Powerwall home battery sales), growing to ~$1.1bn by 2020. We note

that this includes ~$500m in stationary storage revenue by 2020.

- Powerwall opportunity: Just last week, Tesla announced its Powerwall

home/industrial stationary storage system, and we believe that it is far too early

to determine demand (deliveries are slated for summer 2015). For example, if

the entire ~600K US homes and businesses with solar panels were to purchase

the battery, the estimated market opportunity would near ~$2bn (although we

note that TSLA aims to market the battery to homes without solar panels, as well

as internationally…so that the market opportunity is arguably even larger).

Overall, our analysis points to FY15 revenue of ~$5.7bn (roughly in-line with consensus),

with the divergence growing over time. See Chart 22.

TSLA

Initiating Coverage

May 5, 2015

page 14 of 36 , Equity Analyst, (212) 284-2103, [email protected] Dolev

Please see important disclosure information on pages 33 - 36 of this report.

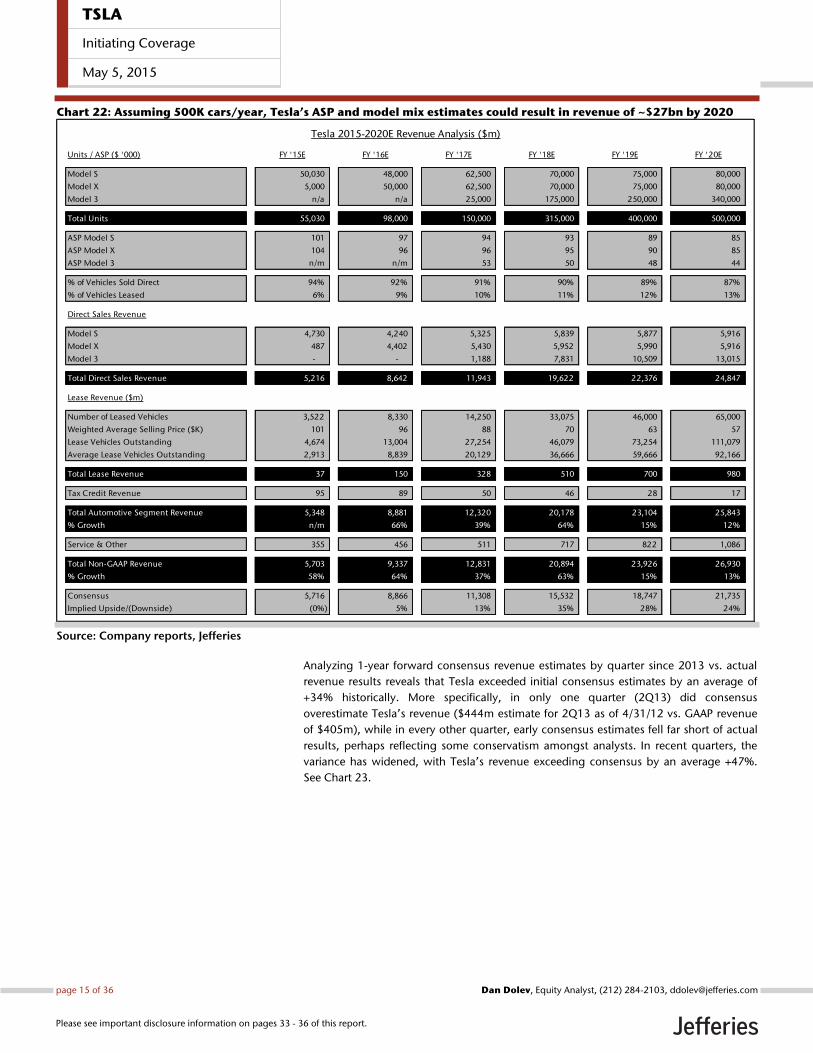

Chart 22: Assuming 500K cars/year, Tesla’s ASP and model mix estimates could result in revenue of ~$27bn by 2020

Source: Company reports, Jefferies

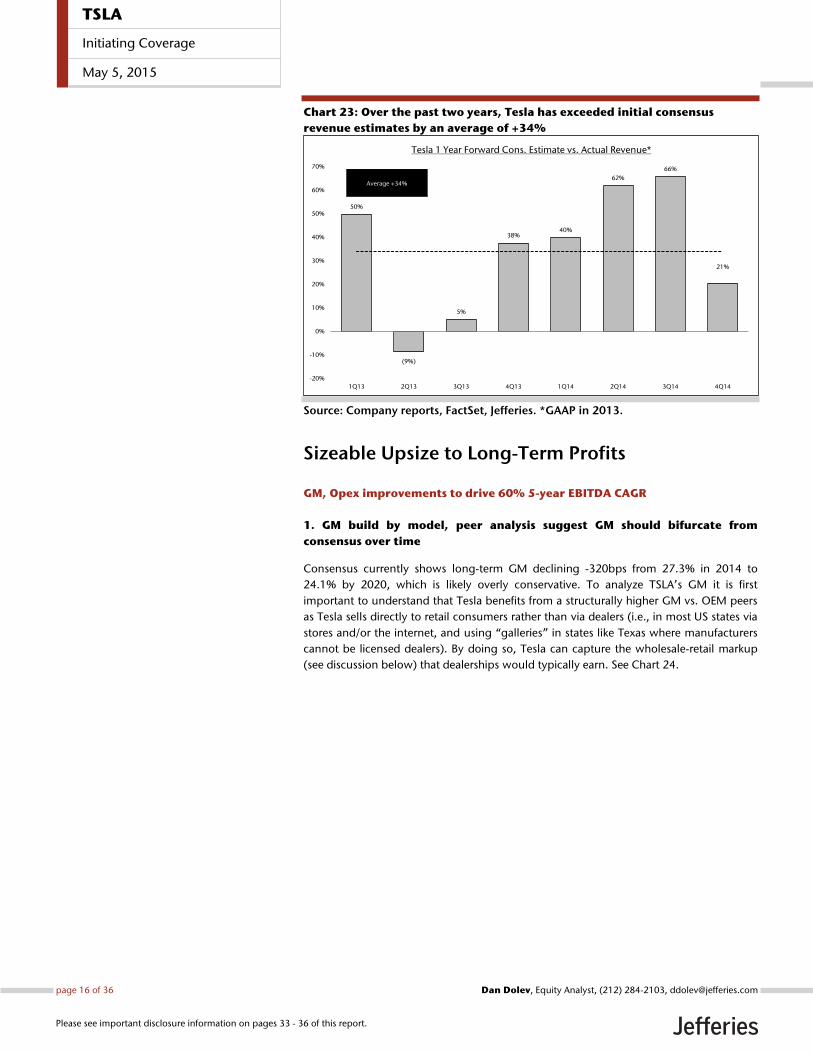

Analyzing 1-year forward consensus revenue estimates by quarter since 2013 vs. actual

revenue results reveals that Tesla exceeded initial consensus estimates by an average of

+34% historically. More specifically, in only one quarter (2Q13) did consensus

overestimate Tesla’s revenue ($444m estimate for 2Q13 as of 4/31/12 vs. GAAP revenue

of $405m), while in every other quarter, early consensus estimates fell far short of actual

results, perhaps reflecting some conservatism amongst analysts. In recent quarters, the

variance has widened, with Tesla’s revenue exceeding consensus by an average +47%.

See Chart 23.

Tesla 2015-2020E Revenue Analysis ($m)

Units / ASP ($ '000) FY '15E FY '16E FY '17E FY '18E FY '19E FY '20E

Model S 50,030 48,000 62,500 70,000 75,000 80,000

Model X 5,000 50,000 62,500 70,000 75,000 80,000

Model 3 n/a n/a 25,000 175,000 250,000 340,000

Total Units 55,030 98,000 150,000 315,000 400,000 500,000

ASP Model S 101 97 94 93 89 85

ASP Model X 104 96 96 95 90 85

ASP Model 3 n/m n/m 53 50 48 44

% of Vehicles Sold Direct 94% 92% 91% 90% 89% 87%

% of Vehicles Leased 6% 9% 10% 11% 12% 13%

Direct Sales Revenue

Model S 4,730 4,240 5,325 5,839 5,877 5,916

Model X 487 4,402 5,430 5,952 5,990 5,916

Model 3 - - 1,188 7,831 10,509 13,015

Total Direct Sales Revenue 5,216 8,642 11,943 19,622 22,376 24,847

Lease Revenue ($m)

Number of Leased Vehicles 3,522 8,330 14,250 33,075 46,000 65,000

Weighted Average Selling Price ($K) 101 96 88 70 63 57

Lease Vehicles Outstanding 4,674 13,004 27,254 46,079 73,254 111,079

Average Lease Vehicles Outstanding 2,913 8,839 20,129 36,666 59,666 92,166

Total Lease Revenue 37 150 328 510 700 980

Tax Credit Revenue 95 89 50 46 28 17

Total Automotive Segment Revenue 5,348 8,881 12,320 20,178 23,104 25,843

% Growth n/m 66% 39% 64% 15% 12%

Service & Other 355 456 511 717 822 1,086

Total Non-GAAP Revenue 5,703 9,337 12,831 20,894 23,926 26,930

% Growth 58% 64% 37% 63% 15% 13%

Consensus 5,716 8,866 11,308 15,532 18,747 21,735

Implied Upside/(Downside) (0%) 5% 13% 35% 28% 24%

TSLA

Initiating Coverage

May 5, 2015

page 15 of 36 , Equity Analyst, (212) 284-2103, [email protected] Dolev

Please see important disclosure information on pages 33 - 36 of this report.

Chart 23: Over the past two years, Tesla has exceeded initial consensus

revenue estimates by an average of +34%

Source: Company reports, FactSet, Jefferies. *GAAP in 2013.

Sizeable Upsize to Long-Term Profits

GM, Opex improvements to drive 60% 5-year EBITDA CAGR

1. GM build by model, peer analysis suggest GM should bifurcate from

consensus over time

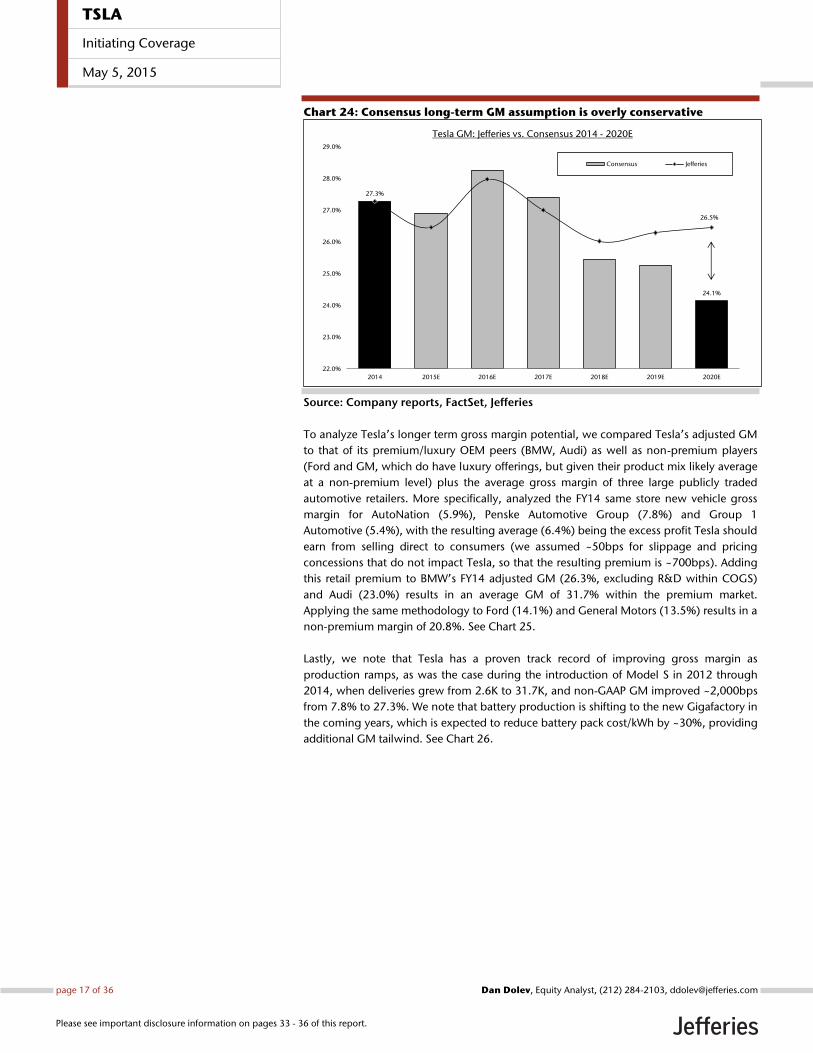

Consensus currently shows long-term GM declining -320bps from 27.3% in 2014 to

24.1% by 2020, which is likely overly conservative. To analyze TSLA’s GM it is first

important to understand that Tesla benefits from a structurally higher GM vs. OEM peers

as Tesla sells directly to retail consumers rather than via dealers (i.e., in most US states via

stores and/or the internet, and using “galleries” in states like Texas where manufacturers

cannot be licensed dealers). By doing so, Tesla can capture the wholesale-retail markup

(see discussion below) that dealerships would typically earn. See Chart 24.

50%

(9%)

5%

38% 40%

62%

66%

21%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14

Tesla 1 Year Forward Cons. Estimate vs. Actual Revenue*

Average +34%

TSLA

Initiating Coverage

May 5, 2015

page 16 of 36 , Equity Analyst, (212) 284-2103, [email protected] Dolev

Please see important disclosure information on pages 33 - 36 of this report.

Chart 24: Consensus long-term GM assumption is overly conservative

Source: Company reports, FactSet, Jefferies

To analyze Tesla’s longer term gross margin potential, we compared Tesla’s adjusted GM

to that of its premium/luxury OEM peers (BMW, Audi) as well as non-premium players

(Ford and GM, which do have luxury offerings, but given their product mix likely average

at a non-premium level) plus the average gross margin of three large publicly traded

automotive retailers. More specifically, analyzed the FY14 same store new vehicle gross

margin for AutoNation (5.9%), Penske Automotive Group (7.8%) and Group 1

Automotive (5.4%), with the resulting average (6.4%) being the excess profit Tesla should

earn from selling direct to consumers (we assumed ~50bps for slippage and pricing

concessions that do not impact Tesla, so that the resulting premium is ~700bps). Adding

this retail premium to BMW’s FY14 adjusted GM (26.3%, excluding R&D within COGS)

and Audi (23.0%) results in an average GM of 31.7% within the premium market.

Applying the same methodology to Ford (14.1%) and General Motors (13.5%) results in a

non-premium margin of 20.8%. See Chart 25.

Lastly, we note that Tesla has a proven track record of improving gross margin as

production ramps, as was the case during the introduction of Model S in 2012 through

2014, when deliveries grew from 2.6K to 31.7K, and non-GAAP GM improved ~2,000bps

from 7.8% to 27.3%. We note that battery production is shifting to the new Gigafactory in

the coming years, which is expected to reduce battery pack cost/kWh by ~30%, providing

additional GM tailwind. See Chart 26.

27.3%

24.1%

26.5%

22.0%

23.0%

24.0%

25.0%

26.0%

27.0%

28.0%

29.0%

2014 2015E 2016E 2017E 2018E 2019E 2020E

Tesla GM: Jefferies vs. Consensus 2014 - 2020E

Consensus Jefferies

TSLA

Initiating Coverage

May 5, 2015

page 17 of 36 , Equity Analyst, (212) 284-2103, [email protected] Dolev

Please see important disclosure information on pages 33 - 36 of this report.

Chart 25: We believe Tesla can exceed peer GM given its

direct-to-consumer sales model

Source: Company Reports, Jefferies

Chart 26: Tesla grew its GM from 7.8% to 27.3% as it

ramped production from 2,636 to 31,655 Model S vehicles

Source: Company Reports, Jefferies

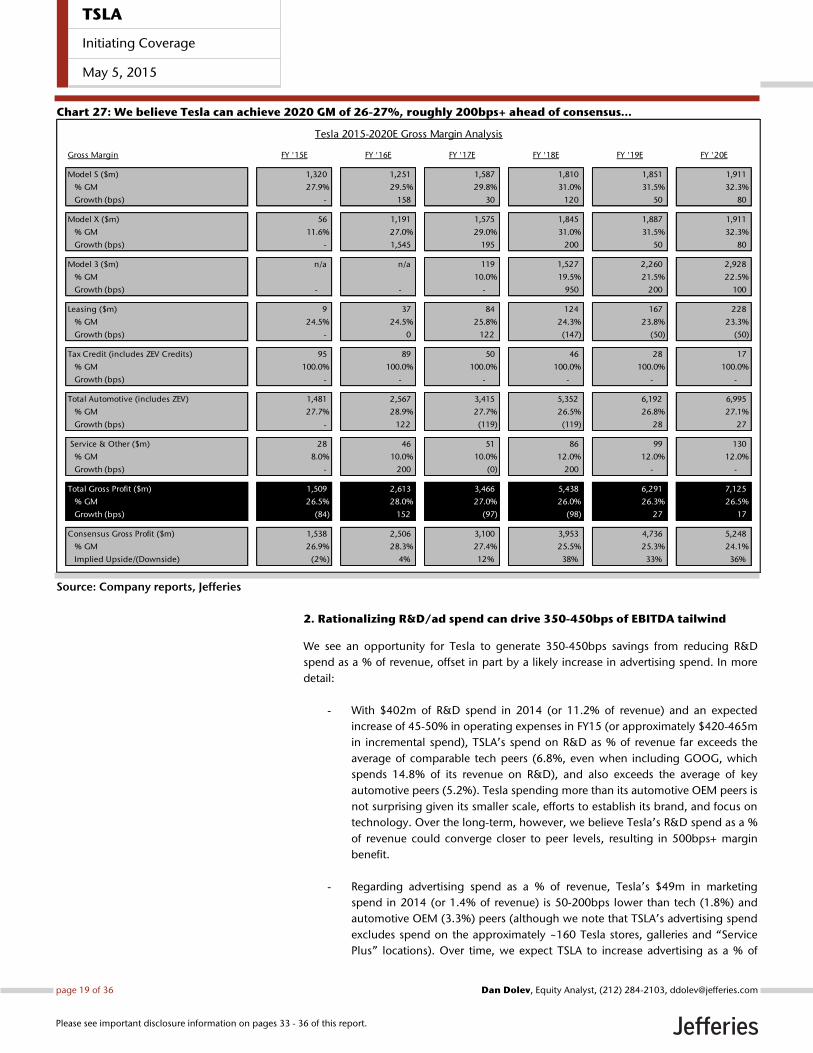

We therefore believe that it is reasonable to expect Tesla to achieve a gross margin of 32-

33% by 2020 for its Model S/X (in-line with the pro-forma Audi/BMW estimates) and

upwards of 22% for its Model III. Although the non-premium peers imply 20.8%, we

believe Tesla can exceed this given that Ford and GM also have significant lower-margin

economy offerings. More specifically, smaller cars, particularly subcompact/compact

models, tend to have lower margin as they have nearly as much content as larger/up-

market models, yet have much lower average selling prices than non-premium models.

Hence, assuming Tesla’s Model III is only in-line with the pro-forma adjusted GM of Ford

and General Motors would likely be too conservative.

In summary…

Our detailed margin by model analysis below shows that while the initial dilution from

Model X (for which deliveries are expected to begin in 3Q/4Q 2015) and Model III (which

is expected to begin deliveries in 2017) should suppress GM in FY17 (27.0% vs. 28.0% in

FY16) and FY18 (26.0%), GM is expected to recover in the outer years reaching 32-33%

for the Model S/X (in-line with the aforementioned premium OEMs) and 22-23% for

Model 3 (slightly above the non-premium OEMs), helped by a higher average ASP for

Model 3 (~$40-50K) vs. Ford’s $22K or General Motor’s $19K ASP. Consequently, we see

2020 GM of 26-27% (vs. consensus’ ~24%). See Chart 27.

26.3% 23.0%

14.1% 13.5%

33.3%

30.0%

27.3%

21.1% 20.5%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

BMW Audi Tesla Ford General Motors

Automotive Pro-Forma Retail & Wholesale Gross Margin of

Select OEMs 2014Adj. GM

Pro-Forma Retail GM

Premium

Non Premium

7.8%

21.9%

27.3%

2,636

22,477

31,655

0%

5%

10%

15%

20%

25%

30%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2012 2013 2014

% G

M

Veh

icle

s

Tesla 2012-2014 Model S Deliveries vs. GM %

GM (non-GAAP)

Model S Deliveries

TSLA

Initiating Coverage

May 5, 2015

page 18 of 36 , Equity Analyst, (212) 284-2103, [email protected] Dolev

Please see important disclosure information on pages 33 - 36 of this report.

Chart 27: We believe Tesla can achieve 2020 GM of 26-27%, roughly 200bps+ ahead of consensus…

Source: Company reports, Jefferies

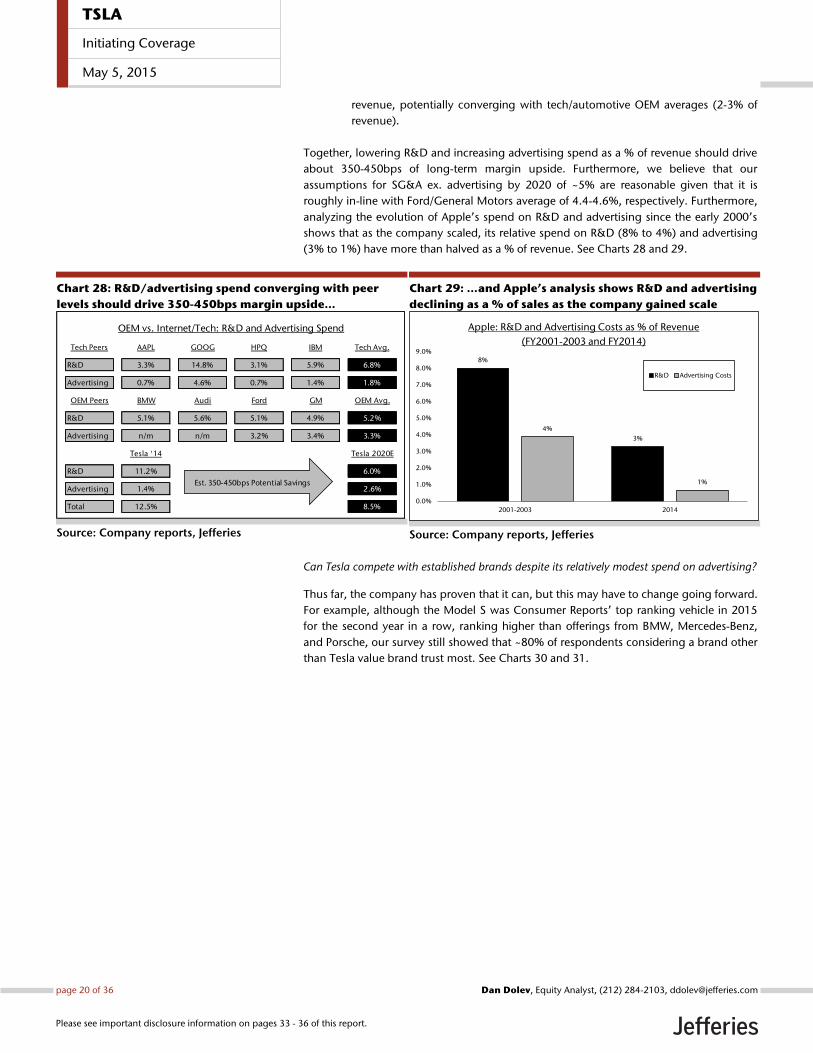

2. Rationalizing R&D/ad spend can drive 350-450bps of EBITDA tailwind

We see an opportunity for Tesla to generate 350-450bps savings from reducing R&D

spend as a % of revenue, offset in part by a likely increase in advertising spend. In more

detail:

- With $402m of R&D spend in 2014 (or 11.2% of revenue) and an expected

increase of 45-50% in operating expenses in FY15 (or approximately $420-465m

in incremental spend), TSLA’s spend on R&D as % of revenue far exceeds the

average of comparable tech peers (6.8%, even when including GOOG, which

spends 14.8% of its revenue on R&D), and also exceeds the average of key

automotive peers (5.2%). Tesla spending more than its automotive OEM peers is

not surprising given its smaller scale, efforts to establish its brand, and focus on

technology. Over the long-term, however, we believe Tesla’s R&D spend as a %

of revenue could converge closer to peer levels, resulting in 500bps+ margin

benefit.

- Regarding advertising spend as a % of revenue, Tesla’s $49m in marketing

spend in 2014 (or 1.4% of revenue) is 50-200bps lower than tech (1.8%) and

automotive OEM (3.3%) peers (although we note that TSLA’s advertising spend

excludes spend on the approximately ~160 Tesla stores, galleries and “Service

Plus” locations). Over time, we expect TSLA to increase advertising as a % of

Tesla 2015-2020E Gross Margin Analysis

Gross Margin FY '15E FY '16E FY '17E FY '18E FY '19E FY '20E

Model S ($m) 1,320 1,251 1,587 1,810 1,851 1,911

% GM 27.9% 29.5% 29.8% 31.0% 31.5% 32.3%

Growth (bps) - 158 30 120 50 80

Model X ($m) 56 1,191 1,575 1,845 1,887 1,911

% GM 11.6% 27.0% 29.0% 31.0% 31.5% 32.3%

Growth (bps) - 1,545 195 200 50 80

Model 3 ($m) n/a n/a 119 1,527 2,260 2,928

% GM 10.0% 19.5% 21.5% 22.5%

Growth (bps) - - - 950 200 100

Leasing ($m) 9 37 84 124 167 228

% GM 24.5% 24.5% 25.8% 24.3% 23.8% 23.3%

Growth (bps) - 0 122 (147) (50) (50)

Tax Credit (includes ZEV Credits) 95 89 50 46 28 17

% GM 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

Growth (bps) - - - - - -

Total Automotive (includes ZEV) 1,481 2,567 3,415 5,352 6,192 6,995

% GM 27.7% 28.9% 27.7% 26.5% 26.8% 27.1%

Growth (bps) - 122 (119) (119) 28 27

Service & Other ($m) 28 46 51 86 99 130

% GM 8.0% 10.0% 10.0% 12.0% 12.0% 12.0%

Growth (bps) - 200 (0) 200 - -

Total Gross Profit ($m) 1,509 2,613 3,466 5,438 6,291 7,125

% GM 26.5% 28.0% 27.0% 26.0% 26.3% 26.5%

Growth (bps) (84) 152 (97) (98) 27 17

Consensus Gross Profit ($m) 1,538 2,506 3,100 3,953 4,736 5,248

% GM 26.9% 28.3% 27.4% 25.5% 25.3% 24.1%

Implied Upside/(Downside) (2%) 4% 12% 38% 33% 36%

TSLA

Initiating Coverage

May 5, 2015

page 19 of 36 , Equity Analyst, (212) 284-2103, [email protected] Dolev

Please see important disclosure information on pages 33 - 36 of this report.

revenue, potentially converging with tech/automotive OEM averages (2-3% of

revenue).

Together, lowering R&D and increasing advertising spend as a % of revenue should drive

about 350-450bps of long-term margin upside. Furthermore, we believe that our

assumptions for SG&A ex. advertising by 2020 of ~5% are reasonable given that it is

roughly in-line with Ford/General Motors average of 4.4-4.6%, respectively. Furthermore,

analyzing the evolution of Apple’s spend on R&D and advertising since the early 2000’s

shows that as the company scaled, its relative spend on R&D (8% to 4%) and advertising

(3% to 1%) have more than halved as a % of revenue. See Charts 28 and 29.

Chart 28: R&D/advertising spend converging with peer

levels should drive 350-450bps margin upside…

Source: Company reports, Jefferies

Chart 29: …and Apple’s analysis shows R&D and advertising

declining as a % of sales as the company gained scale

Source: Company reports, Jefferies

Can Tesla compete with established brands despite its relatively modest spend on advertising?

Thus far, the company has proven that it can, but this may have to change going forward.

For example, although the Model S was Consumer Reports’ top ranking vehicle in 2015

for the second year in a row, ranking higher than offerings from BMW, Mercedes-Benz,

and Porsche, our survey still showed that ~80% of respondents considering a brand other

than Tesla value brand trust most. See Charts 30 and 31.

OEM vs. Internet/Tech: R&D and Advertising Spend

Tech Peers AAPL GOOG HPQ IBM Tech Avg.

R&D 3.3% 14.8% 3.1% 5.9% 6.8%

Advertising 0.7% 4.6% 0.7% 1.4% 1.8%

OEM Peers BMW Audi Ford GM OEM Avg.

R&D 5.1% 5.6% 5.1% 4.9% 5.2%

Advertising n/m n/m 3.2% 3.4% 3.3%

Tesla '14 Tesla 2020E

R&D 11.2% 6.0%

Advertising 1.4% 2.6%

Total 12.5% 8.5%

Est. 350-450bps Potential Savings

8%

3%

4%

1%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

2001-2003 2014

Apple: R&D and Advertising Costs as % of Revenue

(FY2001-2003 and FY2014)

R&D Advertising Costs

TSLA

Initiating Coverage

May 5, 2015

page 20 of 36 , Equity Analyst, (212) 284-2103, [email protected] Dolev

Please see important disclosure information on pages 33 - 36 of this report.

Chart 30: Tesla’s Model S was ranked #1 by Consumer

Reports for the 2nd consecutive year

Source: Consumer Reports, Jefferies

Chart 31: Survey respondents considering brands other

than Tesla noted that brand trust is paramount…

Source: Jefferies. *Does not total 100% as respondents could select multiple responses.

3. Despite progress, peer comparison shows ample opportunity to improve

efficiency

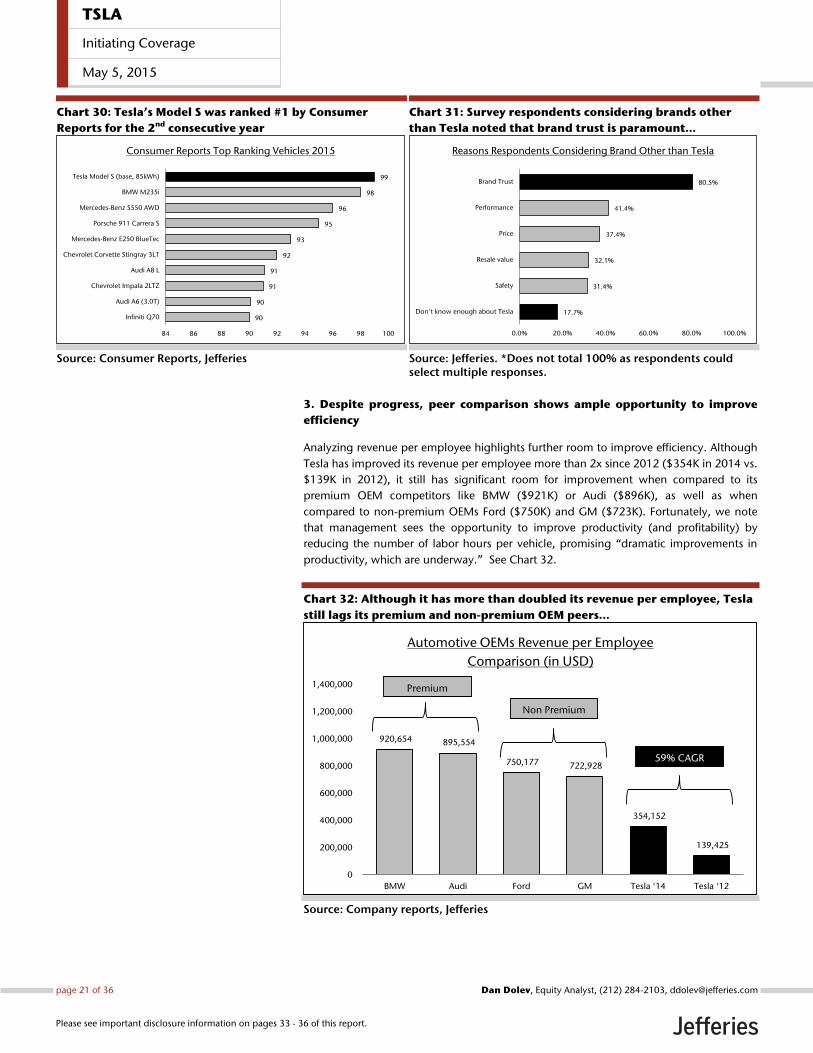

Analyzing revenue per employee highlights further room to improve efficiency. Although

Tesla has improved its revenue per employee more than 2x since 2012 ($354K in 2014 vs.

$139K in 2012), it still has significant room for improvement when compared to its

premium OEM competitors like BMW ($921K) or Audi ($896K), as well as when

compared to non-premium OEMs Ford ($750K) and GM ($723K). Fortunately, we note

that management sees the opportunity to improve productivity (and profitability) by

reducing the number of labor hours per vehicle, promising “dramatic improvements in

productivity, which are underway.” See Chart 32.

Chart 32: Although it has more than doubled its revenue per employee, Tesla

still lags its premium and non-premium OEM peers…

Source: Company reports, Jefferies

90

90

91

91

92

93

95

96

98

99

84 86 88 90 92 94 96 98 100

Infiniti Q70

Audi A6 (3.0T)

Chevrolet Impala 2LTZ

Audi A8 L

Chevrolet Corvette Stingray 3LT

Mercedes-Benz E250 BlueTec

Porsche 911 Carrera S

Mercedes-Benz S550 AWD

BMW M235i

Tesla Model S (base, 85kWh)

Consumer Reports Top Ranking Vehicles 2015

17.7%

31.4%

32.1%

37.4%

41.4%

80.5%

0.0% 20.0% 40.0% 60.0% 80.0% 100.0%

Don't know enough about Tesla

Safety

Resale value

Price

Performance

Brand Trust

Reasons Respondents Considering Brand Other than Tesla

920,654 895,554

750,177 722,928

354,152

139,425

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

BMW Audi Ford GM Tesla '14 Tesla '12

Automotive OEMs Revenue per Employee

Comparison (in USD)

Premium

Non Premium

59% CAGR

TSLA

Initiating Coverage

May 5, 2015

page 21 of 36 , Equity Analyst, (212) 284-2103, [email protected] Dolev

Please see important disclosure information on pages 33 - 36 of this report.

In summary…

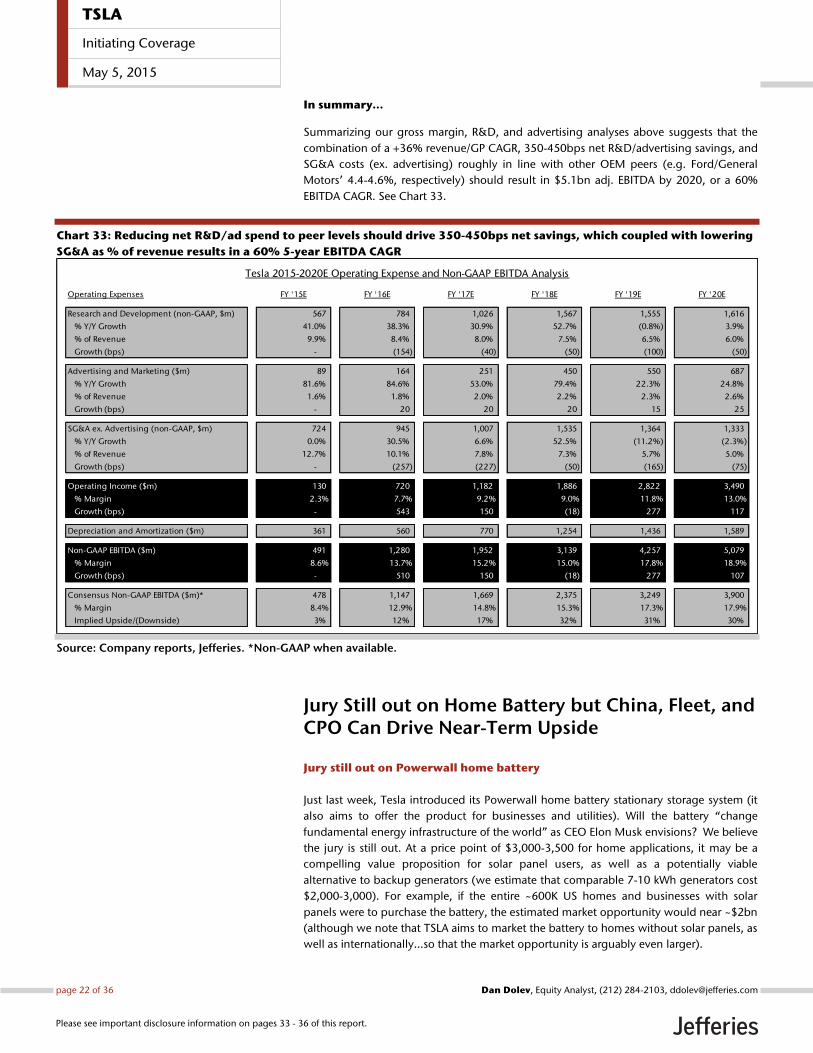

Summarizing our gross margin, R&D, and advertising analyses above suggests that the

combination of a +36% revenue/GP CAGR, 350-450bps net R&D/advertising savings, and

SG&A costs (ex. advertising) roughly in line with other OEM peers (e.g. Ford/General

Motors’ 4.4-4.6%, respectively) should result in $5.1bn adj. EBITDA by 2020, or a 60%

EBITDA CAGR. See Chart 33.

Chart 33: Reducing net R&D/ad spend to peer levels should drive 350-450bps net savings, which coupled with lowering

SG&A as % of revenue results in a 60% 5-year EBITDA CAGR

Source: Company reports, Jefferies. *Non-GAAP when available.

Jury Still out on Home Battery but China, Fleet, and CPO Can Drive Near-Term Upside

Jury still out on Powerwall home battery

Just last week, Tesla introduced its Powerwall home battery stationary storage system (it

also aims to offer the product for businesses and utilities). Will the battery “change

fundamental energy infrastructure of the world” as CEO Elon Musk envisions? We believe

the jury is still out. At a price point of $3,000-3,500 for home applications, it may be a

compelling value proposition for solar panel users, as well as a potentially viable

alternative to backup generators (we estimate that comparable 7-10 kWh generators cost

$2,000-3,000). For example, if the entire ~600K US homes and businesses with solar

panels were to purchase the battery, the estimated market opportunity would near ~$2bn

(although we note that TSLA aims to market the battery to homes without solar panels, as

well as internationally…so that the market opportunity is arguably even larger).

Tesla 2015-2020E Operating Expense and Non-GAAP EBITDA Analysis

Operating Expenses FY '15E FY '16E FY '17E FY '18E FY '19E FY '20E

Research and Development (non-GAAP, $m) 567 784 1,026 1,567 1,555 1,616

% Y/Y Growth 41.0% 38.3% 30.9% 52.7% (0.8%) 3.9%

% of Revenue 9.9% 8.4% 8.0% 7.5% 6.5% 6.0%

Growth (bps) - (154) (40) (50) (100) (50)

Advertising and Marketing ($m) 89 164 251 450 550 687

% Y/Y Growth 81.6% 84.6% 53.0% 79.4% 22.3% 24.8%

% of Revenue 1.6% 1.8% 2.0% 2.2% 2.3% 2.6%

Growth (bps) - 20 20 20 15 25

SG&A ex. Advertising (non-GAAP, $m) 724 945 1,007 1,535 1,364 1,333

% Y/Y Growth 0.0% 30.5% 6.6% 52.5% (11.2%) (2.3%)

% of Revenue 12.7% 10.1% 7.8% 7.3% 5.7% 5.0%

Growth (bps) - (257) (227) (50) (165) (75)

Operating Income ($m) 130 720 1,182 1,886 2,822 3,490

% Margin 2.3% 7.7% 9.2% 9.0% 11.8% 13.0%

Growth (bps) - 543 150 (18) 277 117

Depreciation and Amortization ($m) 361 560 770 1,254 1,436 1,589

Non-GAAP EBITDA ($m) 491 1,280 1,952 3,139 4,257 5,079

% Margin 8.6% 13.7% 15.2% 15.0% 17.8% 18.9%

Growth (bps) - 510 150 (18) 277 107

Consensus Non-GAAP EBITDA ($m)* 478 1,147 1,669 2,375 3,249 3,900

% Margin 8.4% 12.9% 14.8% 15.3% 17.3% 17.9%

Implied Upside/(Downside) 3% 12% 17% 32% 31% 30%

TSLA

Initiating Coverage

May 5, 2015

page 22 of 36 , Equity Analyst, (212) 284-2103, [email protected] Dolev

Please see important disclosure information on pages 33 - 36 of this report.

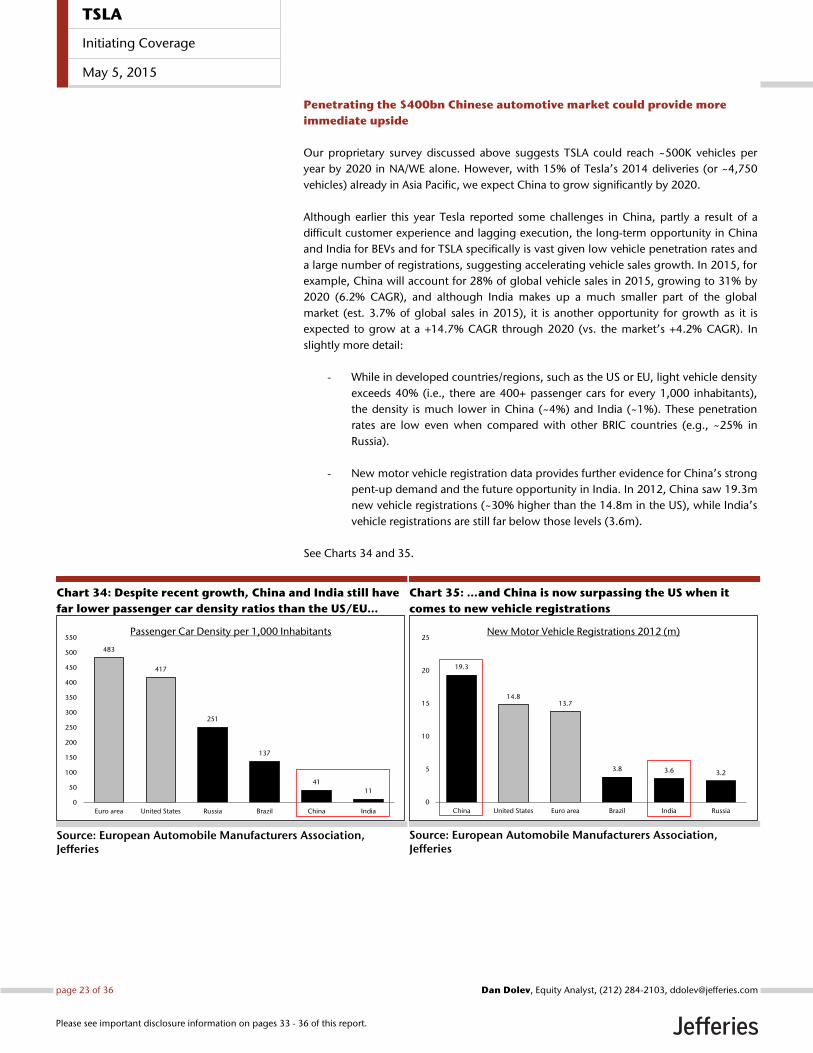

Penetrating the $400bn Chinese automotive market could provide more

immediate upside

Our proprietary survey discussed above suggests TSLA could reach ~500K vehicles per

year by 2020 in NA/WE alone. However, with 15% of Tesla’s 2014 deliveries (or ~4,750

vehicles) already in Asia Pacific, we expect China to grow significantly by 2020.

Although earlier this year Tesla reported some challenges in China, partly a result of a

difficult customer experience and lagging execution, the long-term opportunity in China

and India for BEVs and for TSLA specifically is vast given low vehicle penetration rates and

a large number of registrations, suggesting accelerating vehicle sales growth. In 2015, for

example, China will account for 28% of global vehicle sales in 2015, growing to 31% by

2020 (6.2% CAGR), and although India makes up a much smaller part of the global

market (est. 3.7% of global sales in 2015), it is another opportunity for growth as it is

expected to grow at a +14.7% CAGR through 2020 (vs. the market’s +4.2% CAGR). In

slightly more detail:

- While in developed countries/regions, such as the US or EU, light vehicle density

exceeds 40% (i.e., there are 400+ passenger cars for every 1,000 inhabitants),

the density is much lower in China (~4%) and India (~1%). These penetration

rates are low even when compared with other BRIC countries (e.g., ~25% in

Russia).

- New motor vehicle registration data provides further evidence for China’s strong

pent-up demand and the future opportunity in India. In 2012, China saw 19.3m

new vehicle registrations (~30% higher than the 14.8m in the US), while India’s

vehicle registrations are still far below those levels (3.6m).

See Charts 34 and 35.

Chart 34: Despite recent growth, China and India still have

far lower passenger car density ratios than the US/EU…

Source: European Automobile Manufacturers Association, Jefferies

Chart 35: …and China is now surpassing the US when it

comes to new vehicle registrations

Source: European Automobile Manufacturers Association, Jefferies

483

417

251

137

41

11

0

50

100

150

200

250

300

350

400

450

500

550

Euro area United States Russia Brazil China India

Passenger Car Density per 1,000 Inhabitants

19.3

14.813.7

3.8 3.6 3.2

0

5

10

15

20

25

China United States Euro area Brazil India Russia

New Motor Vehicle Registrations 2012 (m)

TSLA

Initiating Coverage

May 5, 2015

page 23 of 36 , Equity Analyst, (212) 284-2103, [email protected] Dolev

Please see important disclosure information on pages 33 - 36 of this report.

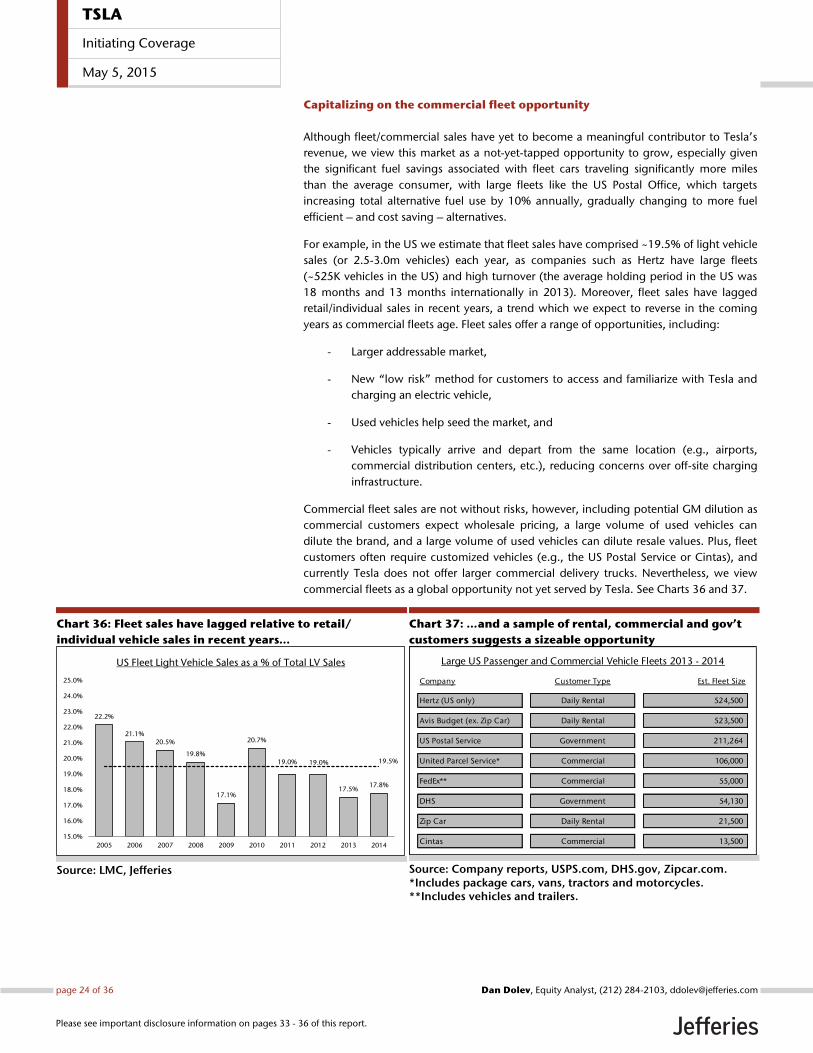

Capitalizing on the commercial fleet opportunity

Although fleet/commercial sales have yet to become a meaningful contributor to Tesla’s

revenue, we view this market as a not-yet-tapped opportunity to grow, especially given

the significant fuel savings associated with fleet cars traveling significantly more miles

than the average consumer, with large fleets like the US Postal Office, which targets

increasing total alternative fuel use by 10% annually, gradually changing to more fuel

efficient – and cost saving – alternatives.

For example, in the US we estimate that fleet sales have comprised ~19.5% of light vehicle

sales (or 2.5-3.0m vehicles) each year, as companies such as Hertz have large fleets

(~525K vehicles in the US) and high turnover (the average holding period in the US was

18 months and 13 months internationally in 2013). Moreover, fleet sales have lagged

retail/individual sales in recent years, a trend which we expect to reverse in the coming

years as commercial fleets age. Fleet sales offer a range of opportunities, including:

- Larger addressable market,

- New “low risk” method for customers to access and familiarize with Tesla and

charging an electric vehicle,

- Used vehicles help seed the market, and

- Vehicles typically arrive and depart from the same location (e.g., airports,

commercial distribution centers, etc.), reducing concerns over off-site charging

infrastructure.

Commercial fleet sales are not without risks, however, including potential GM dilution as

commercial customers expect wholesale pricing, a large volume of used vehicles can

dilute the brand, and a large volume of used vehicles can dilute resale values. Plus, fleet

customers often require customized vehicles (e.g., the US Postal Service or Cintas), and

currently Tesla does not offer larger commercial delivery trucks. Nevertheless, we view

commercial fleets as a global opportunity not yet served by Tesla. See Charts 36 and 37.

Chart 36: Fleet sales have lagged relative to retail/

individual vehicle sales in recent years…

Source: LMC, Jefferies

Chart 37: …and a sample of rental, commercial and gov’t

customers suggests a sizeable opportunity

Source: Company reports, USPS.com, DHS.gov, Zipcar.com. *Includes package cars, vans, tractors and motorcycles. **Includes vehicles and trailers.

22.2%

21.1% 20.5%

19.8%

17.1%

20.7%

19.0% 19.0%

17.5% 17.8%

19.5%

15.0%

16.0%

17.0%

18.0%

19.0%

20.0%

21.0%

22.0%

23.0%

24.0%

25.0%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

US Fleet Light Vehicle Sales as a % of Total LV Sales Large US Passenger and Commercial Vehicle Fleets 2013 - 2014

Company Customer Type Est. Fleet Size

Hertz (US only) Daily Rental 524,500

Avis Budget (ex. Zip Car) Daily Rental 523,500

US Postal Service Government 211,264

United Parcel Service* Commercial 106,000

FedEx** Commercial 55,000

DHS Government 54,130

Zip Car Daily Rental 21,500

Cintas Commercial 13,500

TSLA

Initiating Coverage

May 5, 2015

page 24 of 36 , Equity Analyst, (212) 284-2103, [email protected] Dolev

Please see important disclosure information on pages 33 - 36 of this report.

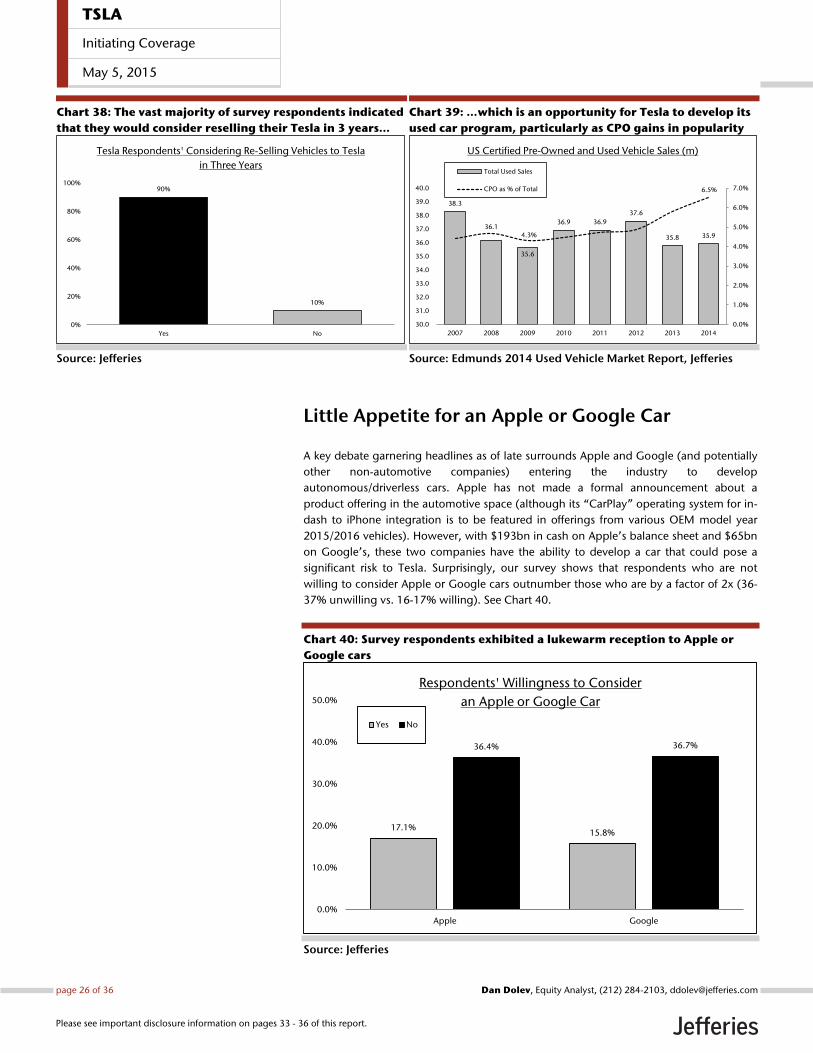

Customers value the ability to trade-in their Tesla…which is an opportunity

for a Certified Pre-Owned program

Of the 50 respondents interested in a Tesla (out of 700+ survey respondents), the vast

majority (90%) indicated that they would be interested in reselling their Tesla back to the

company after three years.

According to data from Edmunds.com, the US used vehicle market is ~2x the size of the

new car market in terms of volume (35.9m used vs. 16.4m new vehicles in 2014).

Moreover, the mix of Certified Pre-Owned (a manufacturer-specific program in which

used vehicles are inspected and “certified,” typically by way of a warranty and roadside

assistance, among other features) has grown from just 4.3% of used vehicle sales in 2009

(~1.5m vehicles) to 6.5% in 2014 (~2.3m vehicles), suggesting that consumers are

increasingly favoring the benefits of a CPO vehicle, despite the added cost. In fact,

according to KBB.com, the premium cost for a CPO vehicle is $1,000+ for large, non-

luxury vehicles, while the CPO premium for a luxury car can be several thousand dollars.

Although Tesla does not currently have a robust CPO/used vehicle sales program, we

anticipate that it will implement a program as more Model S vehicles age and the Model

X grows in popularity. We would view a more meaningful CPO program positively, as it

would allow Tesla to:

- Control the number and condition of used Teslas on the market, supporting

resale prices,

- Create an opportunity for more consumers to get into a Tesla at a lower price

point ahead of the 2017 release of the Model III

- Capture the majority of the secondary market that will inevitably arise as more

Teslas are on the road, and

- Generate incremental revenue/gross profit from existing service centers, better

leveraging fixed/sunk costs.

Nevertheless, repurchasing used Teslas is not without risks as it could potentially require

significant cash. For example, if 25% of the estimated ~60K Teslas that have been

delivered to customers were repurchased at ~$50K (or ~50% of the ASP in 2014) and not

replaced by another Tesla (e.g., the customer does not trade-in for a new vehicle at a

~$100K ASP), then Tesla could hypothetically have to spend ~$750m to repurchase these

vehicles. With ~$1.9bn in cash on its balance sheet as of 4Q14, these repurchases could

consume ~40% of Tesla’s cash. Although this simplistic analysis ignores the likelihood that

repurchases would not happen all at once, so that some vehicles would likely be sold

before others are repurchased, it demonstrates that Tesla could potentially have further

cash demands in the coming years as it addresses the used vehicle opportunity. See

Charts 38 and 39.

TSLA

Initiating Coverage

May 5, 2015

page 25 of 36 , Equity Analyst, (212) 284-2103, [email protected] Dolev

Please see important disclosure information on pages 33 - 36 of this report.

Chart 38: The vast majority of survey respondents indicated

that they would consider reselling their Tesla in 3 years…

Source: Jefferies

Chart 39: …which is an opportunity for Tesla to develop its

used car program, particularly as CPO gains in popularity

Source: Edmunds 2014 Used Vehicle Market Report, Jefferies

Little Appetite for an Apple or Google Car

A key debate garnering headlines as of late surrounds Apple and Google (and potentially

other non-automotive companies) entering the industry to develop

autonomous/driverless cars. Apple has not made a formal announcement about a

product offering in the automotive space (although its “CarPlay” operating system for in-

dash to iPhone integration is to be featured in offerings from various OEM model year

2015/2016 vehicles). However, with $193bn in cash on Apple’s balance sheet and $65bn

on Google’s, these two companies have the ability to develop a car that could pose a

significant risk to Tesla. Surprisingly, our survey shows that respondents who are not

willing to consider Apple or Google cars outnumber those who are by a factor of 2x (36-

37% unwilling vs. 16-17% willing). See Chart 40.

Chart 40: Survey respondents exhibited a lukewarm reception to Apple or

Google cars

Source: Jefferies

90%

10%

0%

20%

40%

60%

80%

100%

Yes No

Tesla Respondents' Considering Re-Selling Vehicles to Tesla

in Three Years

38.3

36.1

35.6

36.9 36.9

37.6

35.8 35.94.3%

6.5%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

30.0

31.0

32.0

33.0

34.0

35.0

36.0

37.0

38.0

39.0

40.0

2007 2008 2009 2010 2011 2012 2013 2014

US Certified Pre-Owned and Used Vehicle Sales (m)

Total Used Sales

CPO as % of Total

17.1% 15.8%

36.4% 36.7%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

Apple Google

Respondents' Willingness to Consider

an Apple or Google Car

Yes No

TSLA

Initiating Coverage

May 5, 2015

page 26 of 36 , Equity Analyst, (212) 284-2103, [email protected] Dolev

Please see important disclosure information on pages 33 - 36 of this report.

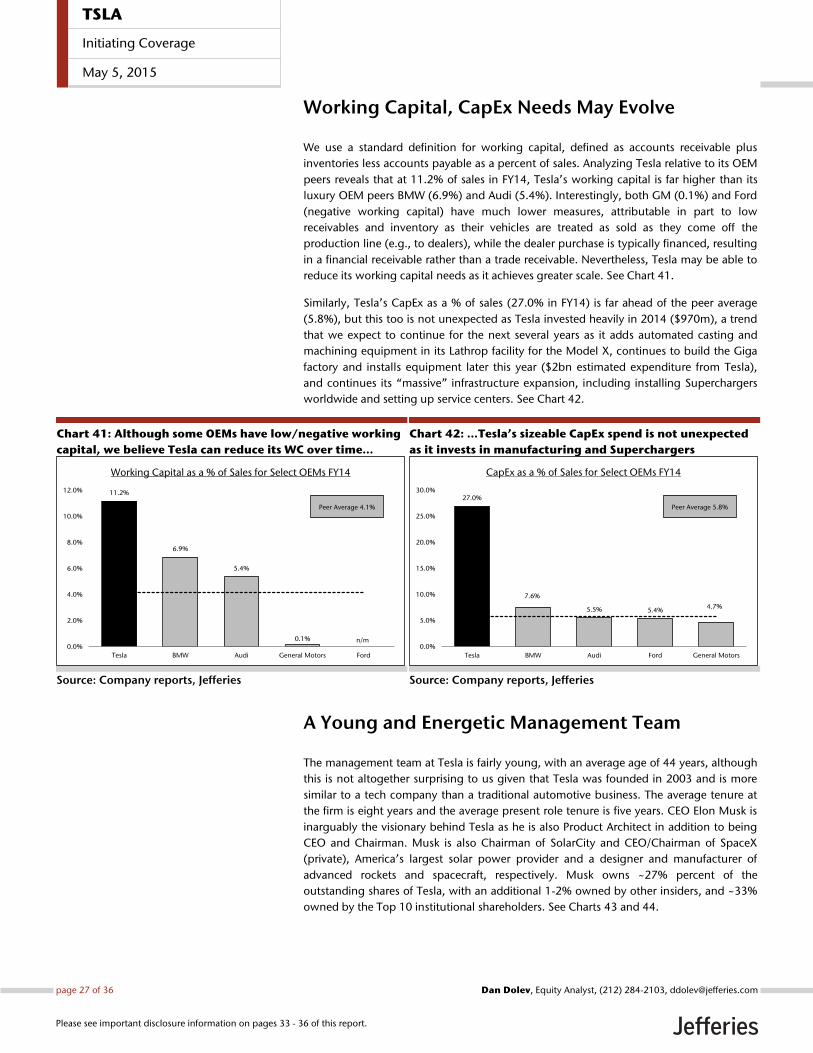

Working Capital, CapEx Needs May Evolve

We use a standard definition for working capital, defined as accounts receivable plus

inventories less accounts payable as a percent of sales. Analyzing Tesla relative to its OEM

peers reveals that at 11.2% of sales in FY14, Tesla’s working capital is far higher than its

luxury OEM peers BMW (6.9%) and Audi (5.4%). Interestingly, both GM (0.1%) and Ford

(negative working capital) have much lower measures, attributable in part to low

receivables and inventory as their vehicles are treated as sold as they come off the

production line (e.g., to dealers), while the dealer purchase is typically financed, resulting

in a financial receivable rather than a trade receivable. Nevertheless, Tesla may be able to

reduce its working capital needs as it achieves greater scale. See Chart 41.

Similarly, Tesla’s CapEx as a % of sales (27.0% in FY14) is far ahead of the peer average

(5.8%), but this too is not unexpected as Tesla invested heavily in 2014 ($970m), a trend

that we expect to continue for the next several years as it adds automated casting and

machining equipment in its Lathrop facility for the Model X, continues to build the Giga

factory and installs equipment later this year ($2bn estimated expenditure from Tesla),

and continues its “massive” infrastructure expansion, including installing Superchargers

worldwide and setting up service centers. See Chart 42.

Chart 41: Although some OEMs have low/negative working

capital, we believe Tesla can reduce its WC over time…

Source: Company reports, Jefferies

Chart 42: …Tesla’s sizeable CapEx spend is not unexpected

as it invests in manufacturing and Superchargers

Source: Company reports, Jefferies

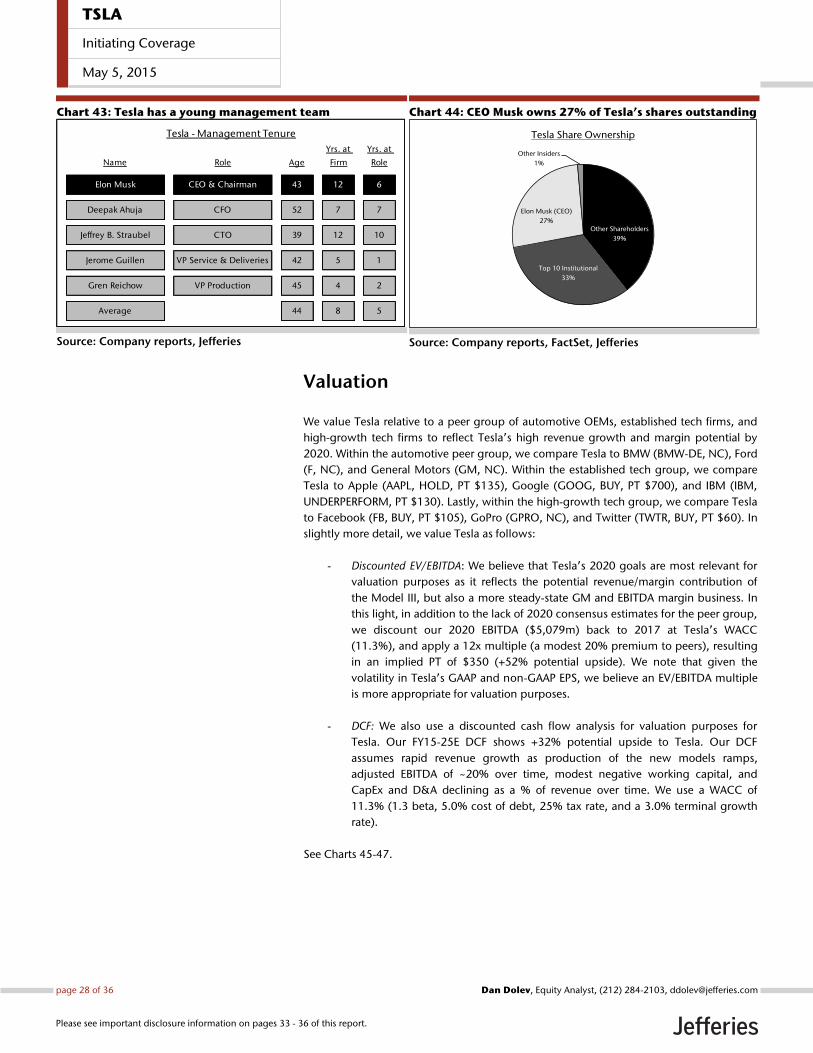

A Young and Energetic Management Team

The management team at Tesla is fairly young, with an average age of 44 years, although

this is not altogether surprising to us given that Tesla was founded in 2003 and is more

similar to a tech company than a traditional automotive business. The average tenure at

the firm is eight years and the average present role tenure is five years. CEO Elon Musk is

inarguably the visionary behind Tesla as he is also Product Architect in addition to being

CEO and Chairman. Musk is also Chairman of SolarCity and CEO/Chairman of SpaceX

(private), America’s largest solar power provider and a designer and manufacturer of

advanced rockets and spacecraft, respectively. Musk owns ~27% percent of the

outstanding shares of Tesla, with an additional 1-2% owned by other insiders, and ~33%

owned by the Top 10 institutional shareholders. See Charts 43 and 44.

11.2%

6.9%

5.4%

0.1% n/m 0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

Tesla BMW Audi General Motors Ford

Working Capital as a % of Sales for Select OEMs FY14

Peer Average 4.1%

27.0%

7.6%

5.5% 5.4% 4.7%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

Tesla BMW Audi Ford General Motors

CapEx as a % of Sales for Select OEMs FY14

Peer Average 5.8%

TSLA

Initiating Coverage

May 5, 2015

page 27 of 36 , Equity Analyst, (212) 284-2103, [email protected] Dolev

Please see important disclosure information on pages 33 - 36 of this report.

Chart 43: Tesla has a young management team

Source: Company reports, Jefferies

Chart 44: CEO Musk owns 27% of Tesla’s shares outstanding

Source: Company reports, FactSet, Jefferies

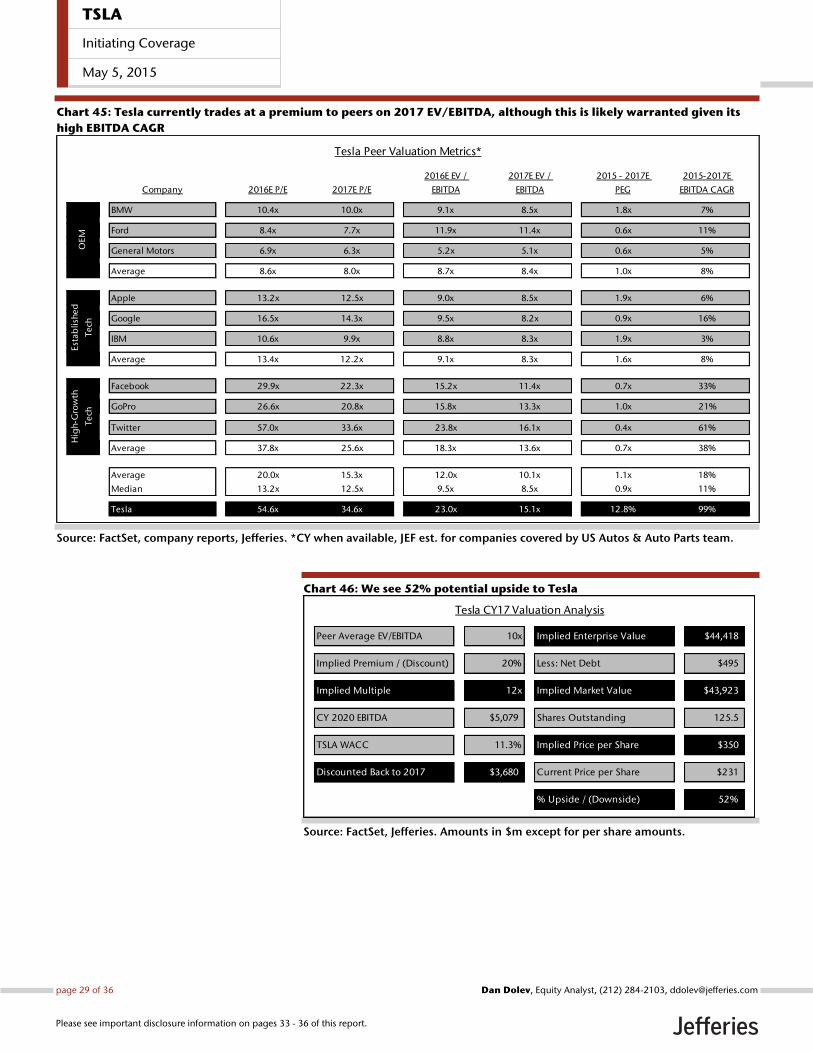

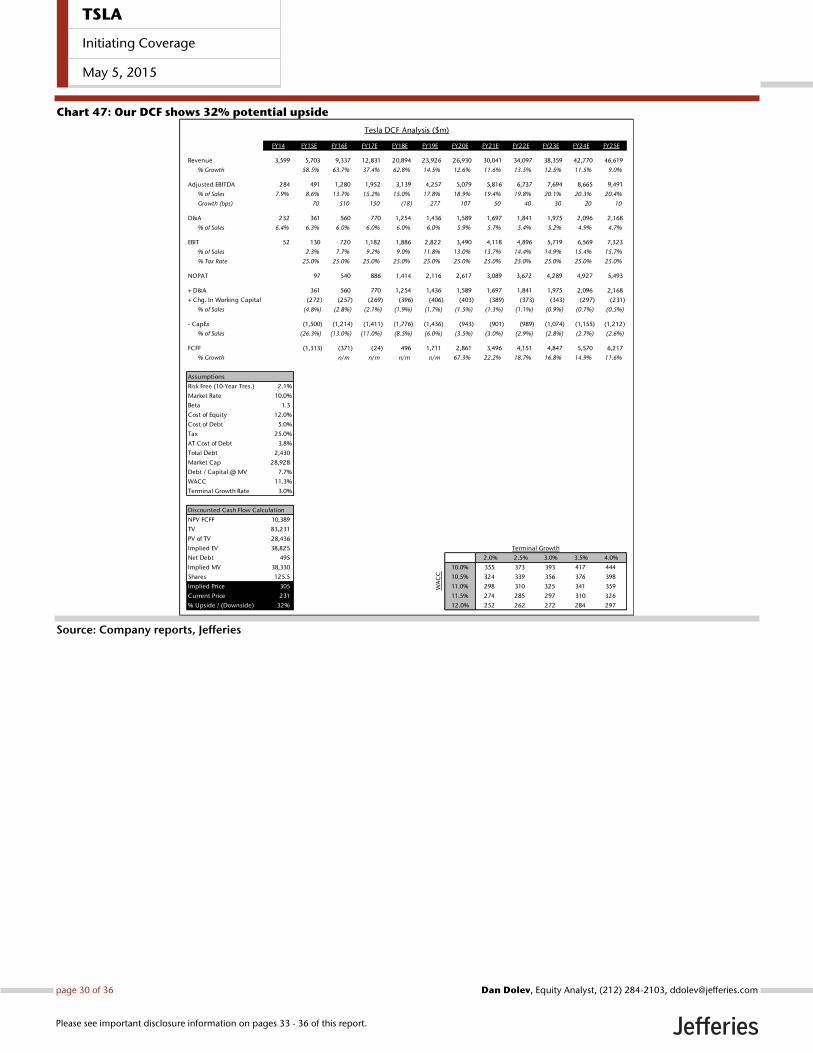

Valuation

We value Tesla relative to a peer group of automotive OEMs, established tech firms, and

high-growth tech firms to reflect Tesla’s high revenue growth and margin potential by