tax provision: determining the financial statement impactnew_york... · recognized through...

TRANSCRIPT

Tax provision: determining the financial statement impact

Page 2 Ninth Annual International Tax Reporting Conference | New York | 30 May 2014

(M)odeling (P)rovision (C)ompliance (A)ttributes Disclaimer

► EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit www.ey.com.

► Ernst & Young LLP is a client-serving member firm of Ernst & Young Global Limited operating in the US.

► This presentation is © 2014 Ernst & Young LLP. All rights reserved. No part of this document may be reproduced, transmitted or otherwise distributed in any form or by any means, electronic or mechanical, including by photocopying, facsimile transmission, recording, rekeying, or using any information storage and retrieval system, without written permission from Ernst & Young LLP. Any reproduction, transmission or distribution of this form or any of the material herein is prohibited and is in violation of US and international law. Ernst & Young LLP expressly disclaims any liability in connection with use of this presentation or its contents by any third party.

► Views expressed in this presentation are not necessarily those of Ernst & Young LLP.

Page 3 Ninth Annual International Tax Reporting Conference | New York | 30 May 2014

(M)odeling (P)rovision (C)ompliance (A)ttributes Circular 230 disclaimer

► Any US tax advice contained herein was not intended or written to be used, and cannot be used, for the purpose of avoiding penalties that may be imposed under the Internal Revenue Code or applicable state or local tax law provisions.

► These slides are for educational purposes only and are not intended, and should not be relied upon, as accounting advice.

Page 4 Ninth Annual International Tax Reporting Conference | New York | 30 May 2014

Today’s presenters

Jon Baronowski Ernst & Young LLP Stamford, CT

Peter Amster Ernst & Young LLP Milwaukee, WI

Eric Sapperstein Ernst & Young LLP New York, NY

Page 5 Ninth Annual International Tax Reporting Conference | New York | 30 May 2014

(M)odeling (P)rovision (C)ompliance (A)ttributes

► C. A. M. P. ► Compliance

► Forms 5471, 8865 and 8858, 1118, white paper disclosure statements ► Attributes

► Earnings and profits (E&P), tax pools, basis, foreign tax credit (FTC) limitation/carryover, dual consolidated losses (DCLs), overall foreign loss (OFL)

► Modeling ► Planning ► Tax reform

► Provision ► Financial statement impact

Key elements of quantitative analysis

Page 6 Ninth Annual International Tax Reporting Conference | New York | 30 May 2014

(M)odeling (P)rovision (C)ompliance (A)ttributes Overall considerations with

provision

► Impact of tax accounting on intercompany tax planning transactions

► Deferred tax accounting for outside basis differences and impacts on global planning strategy

► Tax accounting treatment of transaction may be less clear than tax treatment! ► Application of accounting guidance potentially subject to greater

interpretation than tax rules ► Inappropriate to conclude here on appropriate tax accounting

guidance to these transactions without specific facts and circumstances

► Intent here is to highlight the tax accounting issues that need follow-up and assessment

Page 7 Ninth Annual International Tax Reporting Conference | New York | 30 May 2014

(M)odeling (P)rovision (C)ompliance (A)ttributes Provision tax accounting rules

to consider

► Accounting Research Bulletin (ARB) 51 – ASC 740-10-25-3(e) and Accounting Standards Codification (ASC) 810-10-45-8 and consolidated financial statements ► For financial statement (F/S) purposes, intercompany transactions

and carrying value increases/decreases are eliminated in consolidation. ARB 51 deals with accounting for the tax effects on intercompany sales of property between F/S group members.

► For transactions covered by ARB 51, the current tax expense/benefit is treated as a prepaid expense/benefit. Prepaid is recognized through generally accepted accounting principles (GAAP) income statement (I/S) as the intercompany property leaves the F/S group or is depreciated/amortized.

► Deferred taxes on new basis differentials created from intercompany transactions are not recognized.

Page 8 Ninth Annual International Tax Reporting Conference | New York | 30 May 2014

(M)odeling (P)rovision (C)ompliance (A)ttributes Provision tax accounting rules

to consider (ARB 51)

► ARB 51 commonly applied to intercompany sales of: ► Inventory ► Property, plant and equipment ► Intangible property

► ARB 51 Less commonly applied to intercompany transfers of: ► Shares/stock of consolidated group members ► Intercompany debt ► Transaction involving losses

Page 9 Ninth Annual International Tax Reporting Conference | New York | 30 May 2014

(M)odeling (P)rovision (C)ompliance (A)ttributes Provision tax accounting rules

to consider

► Accounting Principles Board (APB) 23 – ASC 740-30 and outside basis differences ► General presumption is that the excess of financial reporting

amounts over tax basis in an investment in a subsidiary will reverse and that such difference requires deferred tax accounting.

► ASC 740-30-25-18 rebuts the general presumption that the excess of financial reporting amount of an investment in a foreign subsidiary or foreign corporate joint venture will reverse. Under this exception, the excess GAAP value over tax basis is viewed as being essentially permanent in duration – APB 23 assertion ► Sufficient evidence is required to support the notion that subsidiary

has invested or will invest undistributed earnings indefinitely or that the earnings will be remitted in a tax-free liquidation.

Page 10 Ninth Annual International Tax Reporting Conference | New York | 30 May 2014

(M)odeling (P)rovision (C)ompliance (A)ttributes Provision tax accounting rules

to consider

► ASC 740-30-25-9 and prohibition on recognition of deferred tax assets (DTAs) on outside basis difference ► A DTA is recognized for an excess of tax basis over financial

reporting amount of an investment in a subsidiary or corporate joint venture only if it is apparent that such difference will reverse in the foreseeable future ► Prohibits recognition of DTAs for outside basis differences for foreign

subsidiaries/joint ventures (JVs) in many instances

► Valuation allowance ► DTAs require measurement that it is “more likely than not” that it

will be realized in full. Where the more likely than not (MLTN) standard is not met, a valuation allowance reserve is required to state the DTA at its realizable value.

Page 11 Ninth Annual International Tax Reporting Conference | New York | 30 May 2014

(M)odeling (P)rovision (C)ompliance (A)ttributes Provision components

► US tax provision on domestic operations ► DTA and deferred tax liability (DTL) for inside basis difference

► US tax provision on foreign operations ► Current tax on income from foreign operation subject to tax in the

US currently – dividends (deemed and actual), foreign tax credit ► Deferred taxes on outside basis differences on investment in

foreign subsidiaries and other foreign investments

Page 12 Ninth Annual International Tax Reporting Conference | New York | 30 May 2014

(M)odeling (P)rovision (C)ompliance (A)ttributes Thoughts about transactions

► Key transactions for discussion ► Section 304 ► Section 368(a)(1)(D) reorganization with check-the-box election

► Other transactions/variations ► Section 351 transfers ► Aspects of parent-subsidiary versus brother-sister (304(a)(1) vs

304(a)(2)) ► US-to-foreign and foreign-to-foreign transactions ► Transactions with boot

► Assume the following slides are not a part of purchase accounting transactions as it could result in a number of different outcomes

Page 13 Ninth Annual International Tax Reporting Conference | New York | 30 May 2014

(M)odeling (P)rovision (C)ompliance (A)ttributes

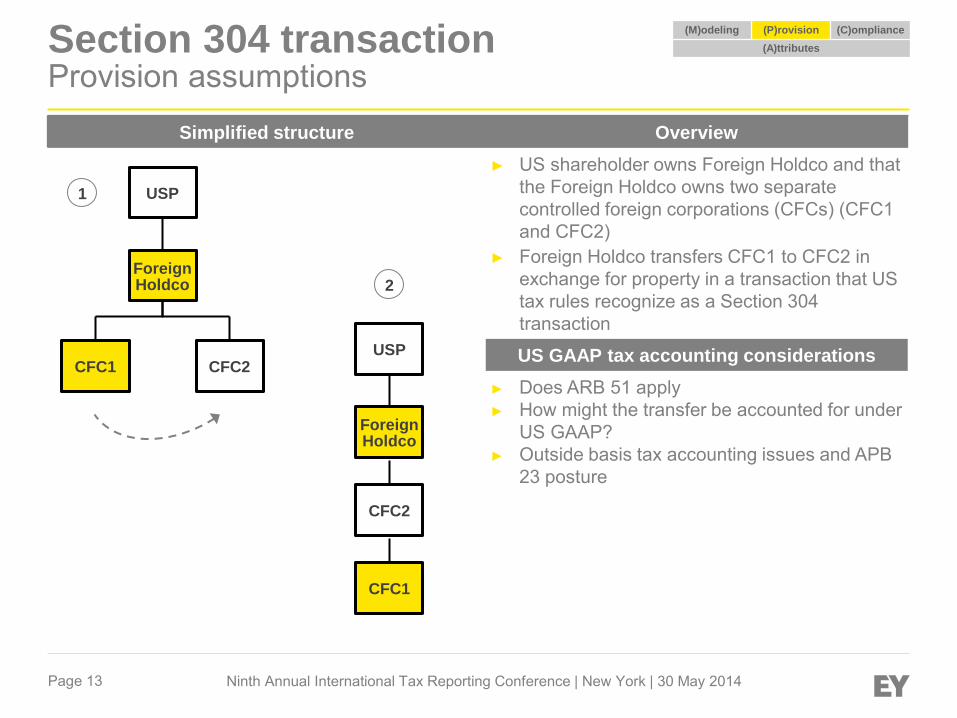

Simplified structure Overview ► US shareholder owns Foreign Holdco and that

the Foreign Holdco owns two separate controlled foreign corporations (CFCs) (CFC1 and CFC2)

► Foreign Holdco transfers CFC1 to CFC2 in exchange for property in a transaction that US tax rules recognize as a Section 304 transaction

US GAAP tax accounting considerations ► Does ARB 51 apply ► How might the transfer be accounted for under

US GAAP? ► Outside basis tax accounting issues and APB

23 posture

Section 304 transaction Provision assumptions

USP

Foreign Holdco

CFC2 CFC1 USP

Foreign Holdco

CFC2

CFC1

1

2

Page 14 Ninth Annual International Tax Reporting Conference | New York | 30 May 2014

(M)odeling (P)rovision (C)ompliance (A)ttributes Section 304 transaction:

tax accounting issues

► Is the transaction treated as an intercompany sale subject to ARB 51? ► Gain or loss recognized by Foreign Holdco on separate company basis is

eliminated in consolidation. ► Current tax expense/benefit recognized by Foreign Holdco treated as

prepaid item ► Gain/loss and current tax impact not recognized in income statement

in year of transfer ► No deferred taxes recognized on new outside basis differential

► Buyer gets fair market value tax basis, carryover GAAP basis ► Need to determine period over which gain and current tax impact is

recognized through income statement ► ARB 51 generally applies to sale of inventory and property, plant and

equipment (PP&E). Usually no similar intent to sell subsidiary shares outside of the group.

Page 15 Ninth Annual International Tax Reporting Conference | New York | 30 May 2014

(M)odeling (P)rovision (C)ompliance (A)ttributes Section 304 transaction:

tax accounting issues

► If Section 304 transaction (i.e., transfer of shares) is not subject to ARB 51 ► Non-application of ARB 51 more often the case for GAAP since

there really is not a “natural” recognition period like depreciation/amortization life for recognizing tax effects that get put up on the balance sheet

► Recognize current tax impact in year of Section 304 transaction ► Elimination of intercompany gain/loss in F/S consolidation results

in permanent tax rate impact ► Can be a positive or negative impact

Page 16 Ninth Annual International Tax Reporting Conference | New York | 30 May 2014

(M)odeling (P)rovision (C)ompliance (A)ttributes Section 304 transaction:

tax accounting issues

► Does the transfer of CFC1 to CFC2 change the overall APB 23 posture? ► Was Foreign Holdco asserting APB 23 with respect to outside basis difference in

CFC1 before the transfer and will this still be the case after the transfer of CFC1 to CFC2?

► Should there be a change in the assertion for CFC2 if the 304 dividend is sourced out of its E&P?

► Does Foreign Holdco’s GAAP basis in CFC2 change? Does Foreign Holdco’s tax basis in CFC2 change? ► US views the Section 304 transaction as a capital contribution of CFC1’s shares to CFC2

followed by a dividend distribution and/or return of capital. ► What is the impact of a change in CFC Holdco’s outside basis differential?

► Transaction consideration may reduce GAAP carrying value ► What happens to tax basis from a local jurisdiction perspective?

► What if one of the CFCs was in a tax> than book basis differential position before and was precluded from recognizing DTA. Does that “DTA” get recognized now as a reduction of the other’s DTL?

Page 17 Ninth Annual International Tax Reporting Conference | New York | 30 May 2014

(M)odeling (P)rovision (C)ompliance (A)ttributes Section 304 transaction:

tax accounting issues

► Does the transfer of CFC1 to CFC2 change the APB 23 posture? ► If transfer results in a change to outside basis difference and

deferred tax needs, x, need to recognize such impact through income statement

► Determination that subsidiary is no longer permanently reinvested usually is made before the transaction. In what period is it appropriate to recognize such change in assertion impact – period decision is made to do transaction or period in which transaction is completed?

Page 18 Ninth Annual International Tax Reporting Conference | New York | 30 May 2014

(M)odeling (P)rovision (C)ompliance (A)ttributes Section 304 transaction:

tax accounting issues

► Does the transfer of CFC1 to CFC2 result in a Subpart F recognition? ► Transaction may be a dividend from CFC2 to Foreign Holdco for

US tax purposes to extent of CFC2’s E&P or a dividend from CFC1 to Foreign Holdco. With the expiration of CFC look-through rules, is such a dividend Subpart F at the CFC Holdco level?

► Current tax recognition at USP level? ► Subpart F exceptions like high tax, same country? ► What if USP is asserting permanent reinvestment at the Foreign

Holdco shareholding level? ► If CFC2 cannot/does not assert APB 23 for CFC1, does expected

reversal of outside basis difference via dividend distribution from CFC1 to CFC2 result in Subpart F income at CFC2?

Page 19 Ninth Annual International Tax Reporting Conference | New York | 30 May 2014

(M)odeling (P)rovision (C)ompliance (A)ttributes

Type “D” reorganization with check- the-box Provision assumptions

Simplified structure Overview ► US shareholder owns Foreign Holdco and

Foreign Holdco owns CFC subsidiaries in two separate ownership chains, CFC1 and CFC2.

► Foreign Holdco transfers CFC1 to CFC2 in exchange for shares/additional equity and/or cash after which/as a part of which CFC1 is checked as a disregarded entity (DRE) for US tax purposes in a transaction that is meant to be a “D” reorganization.

US GAAP tax accounting considerations ► Outside basis tax accounting issues and APB

23 posture ► Transaction with boot ► Risks if transaction is a Section 351 transfer

and Section 332 liquidation

USP

Foreign Holdco

CFC2 CFC1 USP

Foreign Holdco

CFC2

DRE1

1

2

Page 20 Ninth Annual International Tax Reporting Conference | New York | 30 May 2014

(M)odeling (P)rovision (C)ompliance (A)ttributes Type “D” reorganization: tax

accounting issues

► Does the transfer of CFC1 to CFC2 change the overall outside basis posture? ► Was Foreign Holdco asserting APB 23 with respect to outside basis

difference in CFC1 before the transfer and will this still be the case after the transfer?

► Should there be a change in the assertion for CFC2? ► Does Foreign Holdco’s GAAP basis in CFC2 change? Does Foreign

Holdco’s tax basis in CFC2 change? ► US views the “D” reorganization as a transfer of CFC1’s assets to CFC2 in

exchange for CFC2 shares after which CFC1 is deemed to liquidate into Foreign Holdco

► What is the impact of a change in Foreign Holdco’s outside basis differential? ► What if one of the CFCs was in a tax> than book basis differential position

before and was precluded from recognizing DTA. Does that DTA get recognized now as a reduction of the other’s DTL?

Page 21 Ninth Annual International Tax Reporting Conference | New York | 30 May 2014

(M)odeling (P)rovision (C)ompliance (A)ttributes Type “D” reorganization: tax

accounting issues

► If transfer results in a change to outside basis difference and deferred tax needs, need to recognize such impact through the income statement.

► Determination that subsidiary is no longer reinvested usually is made before the transaction. In what period is it appropriate to recognize such change in assertion impact: period decision is made to do transaction or period in which transaction is completed?

Page 22 Ninth Annual International Tax Reporting Conference | New York | 30 May 2014

(M)odeling (P)rovision (C)ompliance (A)ttributes Questions and conference

close

► Questions? ► Closing remarks

Page 23 Ninth Annual International Tax Reporting Conference | New York | 30 May 2014

Contacts

Jon Baronowski Ernst & Young LLP | Stamford, CT +1 203 674 3448 [email protected]

Peter Amster Ernst & Young LLP | Milwaukee, WI +1 414 223 7226 [email protected]

Eric Sapperstein Ernst & Young LLP | New York, NY +1 212 773 3353 [email protected]