tax policy in the 114th congress (and beyond)€¦ · source: congressional budget office, an...

TRANSCRIPT

Tax Policy in the 114th Congress (and Beyond)

Alex Brosseau, Deloitte Tax LLP

The fiscal backdrop –

long-term challenges remain

Tax Policy in the 114th Congress (and Beyond) Copyright © 2016 Deloitte Development LLC. All rights reserved.

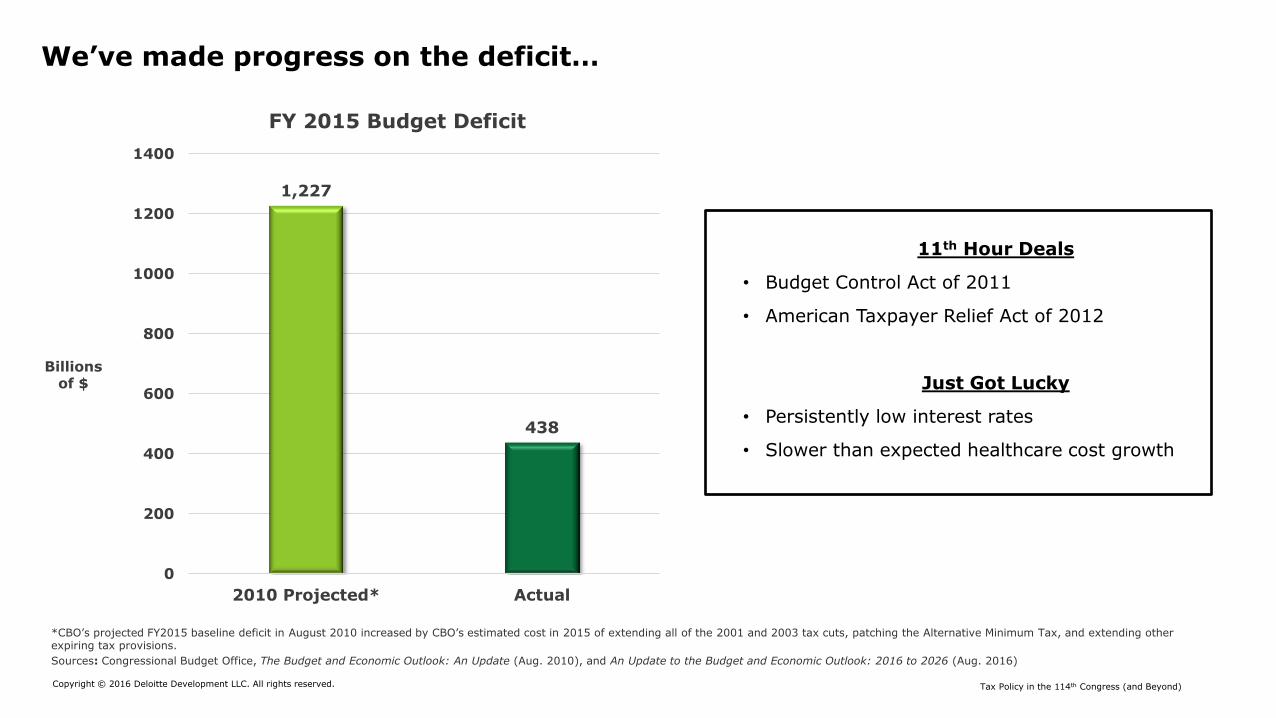

We’ve made progress on the deficit…

1,227

438

0

200

400

600

800

1000

1200

1400

2010 Projected* Actual

FY 2015 Budget Deficit

Billions of $

*CBO’s projected FY2015 baseline deficit in August 2010 increased by CBO’s estimated cost in 2015 of extending all of the 2001 and 2003 tax cuts, patching the Alternative Minimum Tax, and extending other expiring tax provisions.

Sources: Congressional Budget Office, The Budget and Economic Outlook: An Update (Aug. 2010), and An Update to the Budget and Economic Outlook: 2016 to 2026 (Aug. 2016)

11th Hour Deals

• Budget Control Act of 2011

• American Taxpayer Relief Act of 2012

Just Got Lucky

• Persistently low interest rates

• Slower than expected healthcare cost growth

Tax Policy in the 114th Congress (and Beyond) Copyright © 2016 Deloitte Development LLC. All rights reserved.

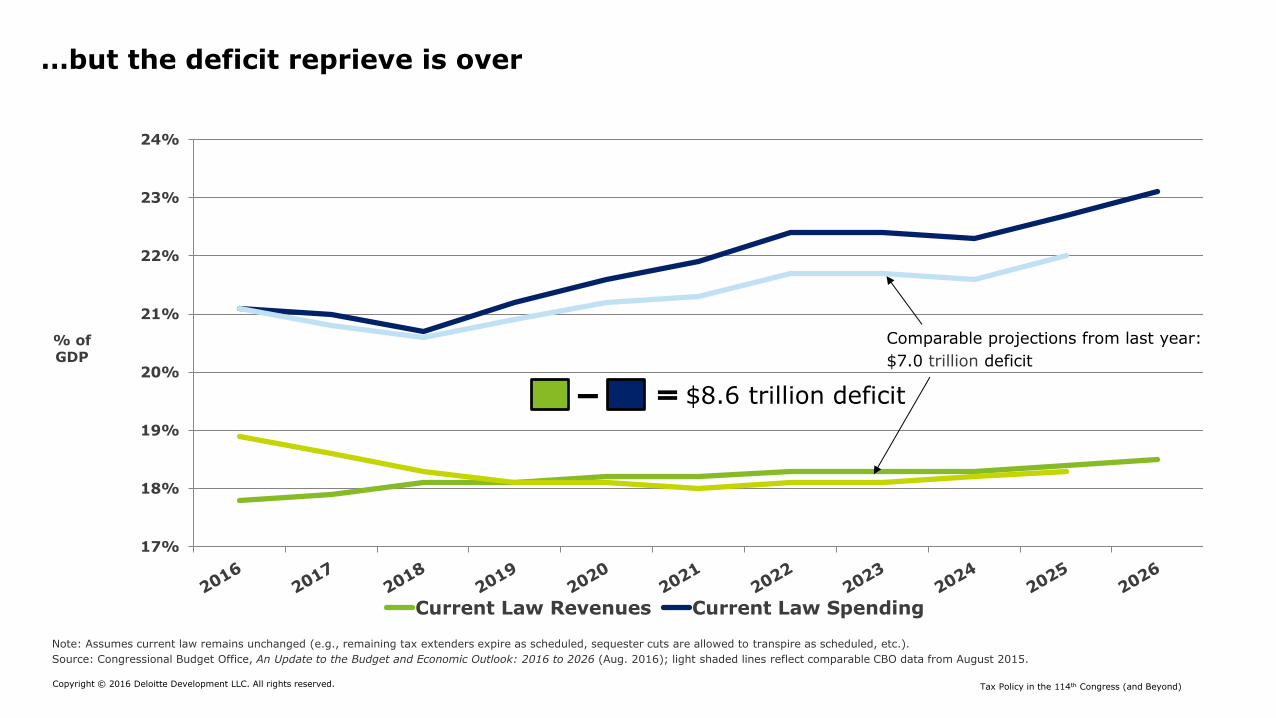

17%

18%

19%

20%

21%

22%

23%

24%

Current Law Revenues Current Law Spending

…but the deficit reprieve is over

Note: Assumes current law remains unchanged (e.g., remaining tax extenders expire as scheduled, sequester cuts are allowed to transpire as scheduled, etc.).

Source: Congressional Budget Office, An Update to the Budget and Economic Outlook: 2016 to 2026 (Aug. 2016); light shaded lines reflect comparable CBO data from August 2015.

% of GDP

Comparable projections from last year:

$7.0 trillion deficit

$8.6 trillion deficit

Tax Policy in the 114th Congress (and Beyond) Copyright © 2016 Deloitte Development LLC. All rights reserved.

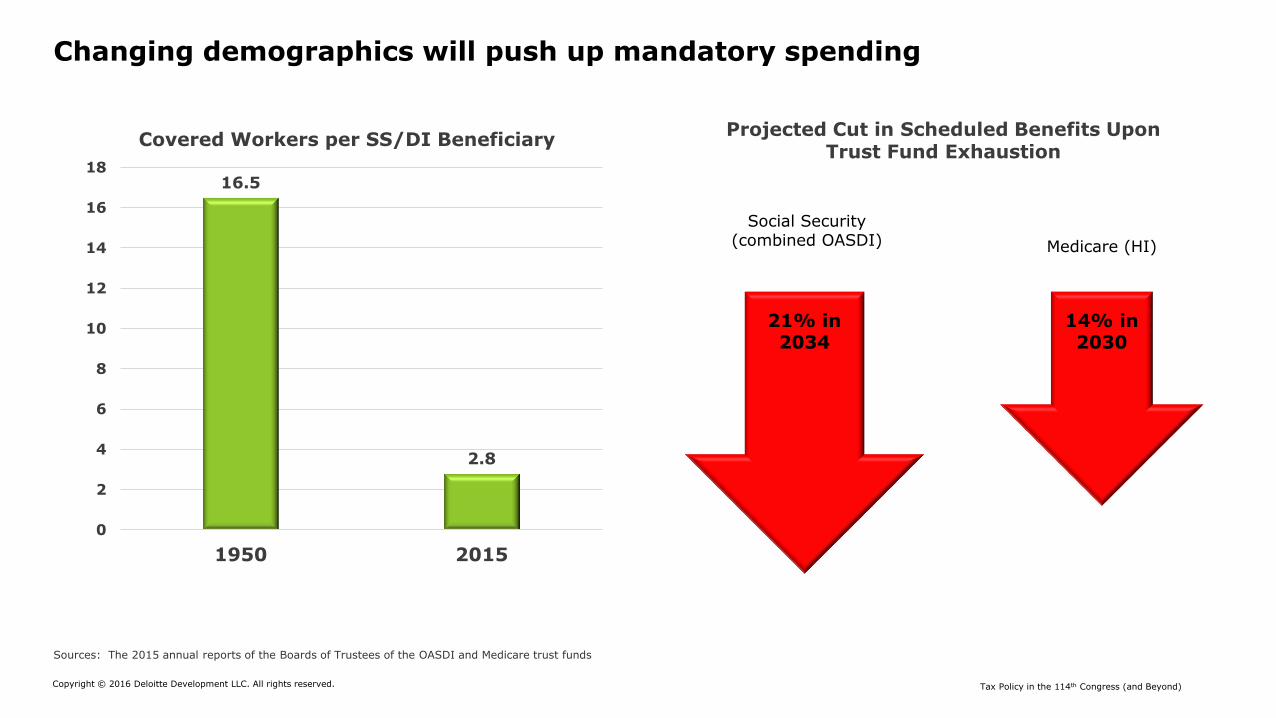

Changing demographics will push up mandatory spending

16.5

2.8

0

2

4

6

8

10

12

14

16

18

1950 2015

Covered Workers per SS/DI Beneficiary Projected Cut in Scheduled Benefits Upon

Trust Fund Exhaustion

Social Security (combined OASDI) Medicare (HI)

14% in 2030

21% in 2034

Sources: The 2015 annual reports of the Boards of Trustees of the OASDI and Medicare trust funds

Tax Policy in the 114th Congress (and Beyond) Copyright © 2016 Deloitte Development LLC. All rights reserved.

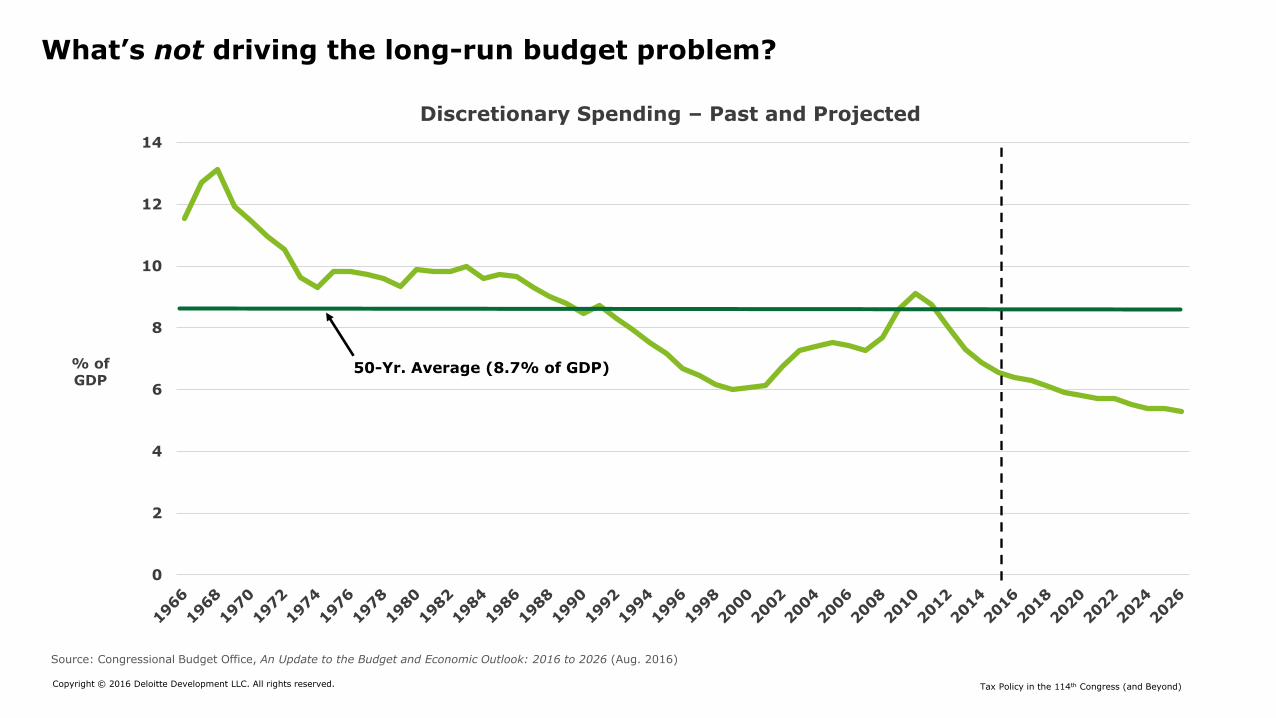

What’s not driving the long-run budget problem?

0

2

4

6

8

10

12

14

Discretionary Spending – Past and Projected

% of GDP

Source: Congressional Budget Office, An Update to the Budget and Economic Outlook: 2016 to 2026 (Aug. 2016)

Yr. Average (8.7% of GDP)-50

Tax Policy in the 114th Congress (and Beyond) Copyright © 2016 Deloitte Development LLC. All rights reserved.

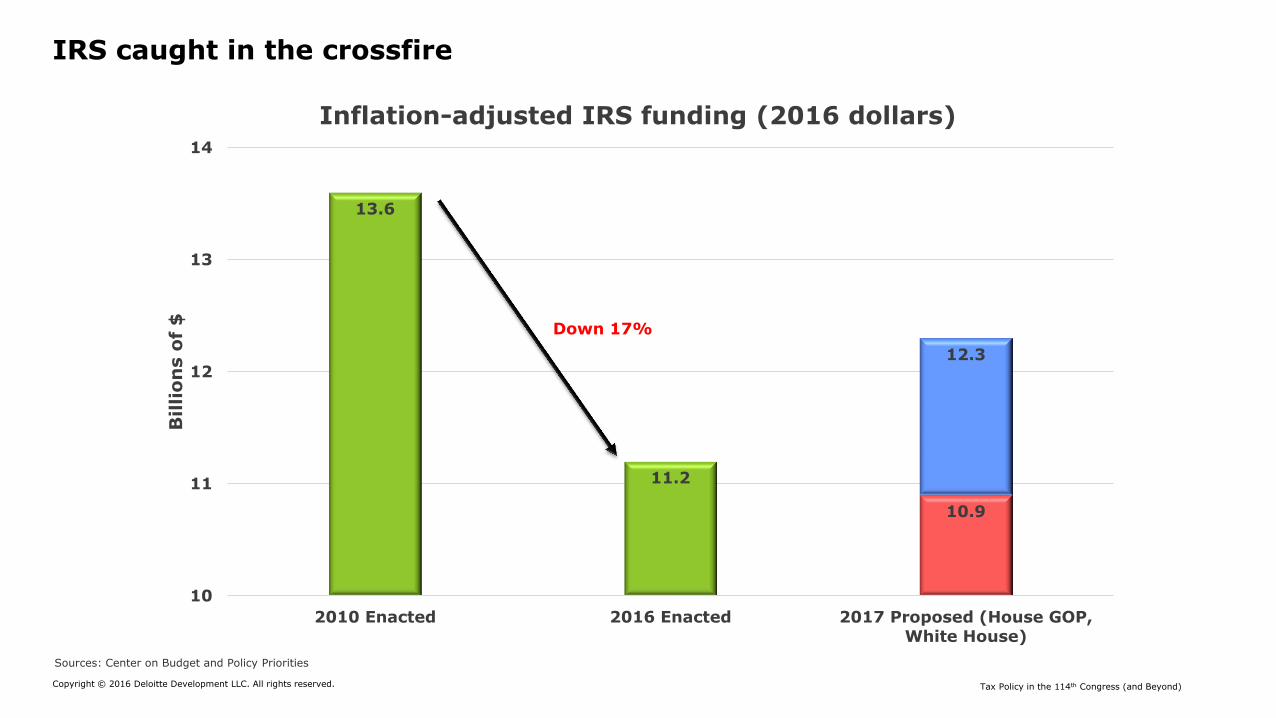

IRS caught in the crossfire

13.6

11.2

10.9

12.3

10

11

12

13

14

2010 Enacted 2016 Enacted 2017 Proposed (House GOP,White House)

Billio

ns o

f $

Inflation-adjusted IRS funding (2016 dollars)

Sources: Center on Budget and Policy Priorities

Down 17%

Political landscape –

more gridlock, or time for action?

Tax Policy in the 114th Congress (and Beyond) Copyright © 2016 Deloitte Development LLC. All rights reserved.

Different Speaker, same challenges?

Under Speaker Boehner

247 Size of House GOP Conference

218 Votes to pass bills in the House

~40 Approximate size of House Freedom Caucus

54 Size of Senate GOP Conference

60 Votes to overcome a Senate filibuster

290/67 Votes to override a President’s veto in the House/Senate

Under Speaker Ryan

247

218

~40

54

60

290/67

Tax Policy in the 114th Congress (and Beyond) Copyright © 2016 Deloitte Development LLC. All rights reserved.

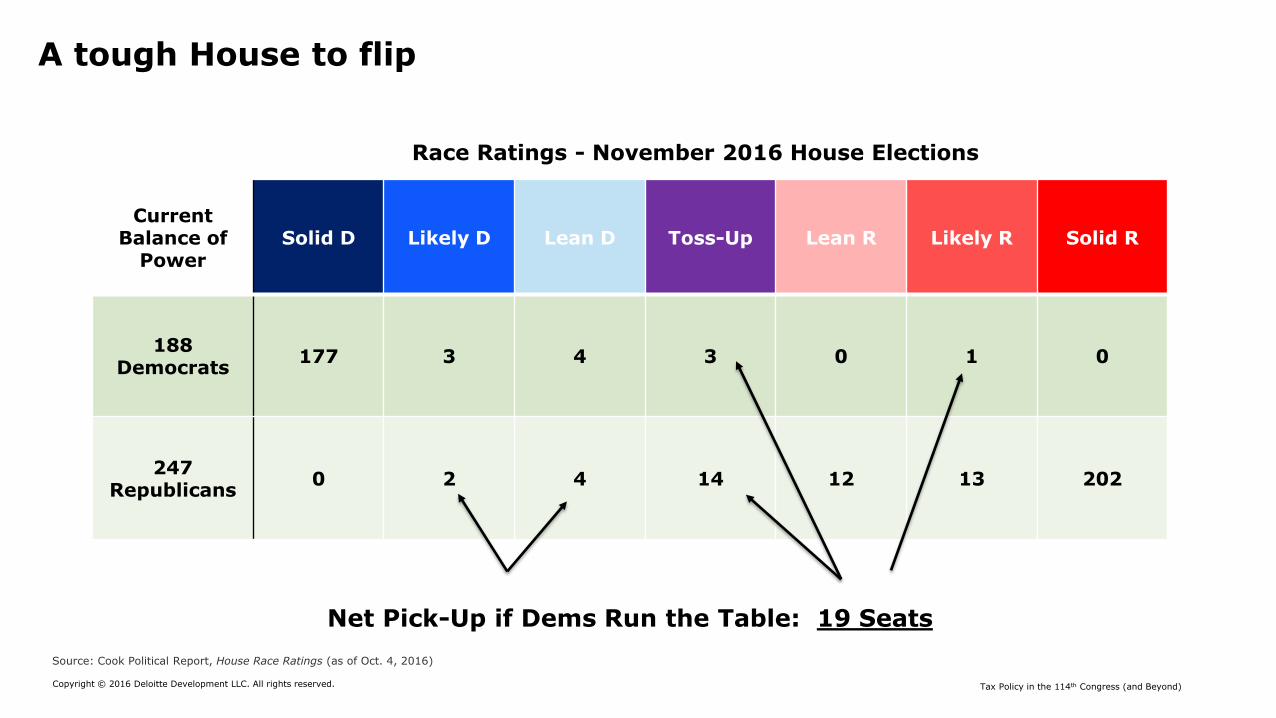

A tough House to flip

Current Balance of

Power Solid D Likely D Lean D Toss-Up Lean R Likely R Solid R

188 Democrats

177 3 4 3 0 1 0

247 Republicans

0 2 4 14 12 13 202

Net Pick-Up if Dems Run the Table: 19 Seats

Source: Cook Political Report, House Race Ratings (as of Oct. 4, 2016)

Race Ratings - November 2016 House Elections

Tax Policy in the 114th Congress (and Beyond) Copyright © 2016 Deloitte Development LLC. All rights reserved.

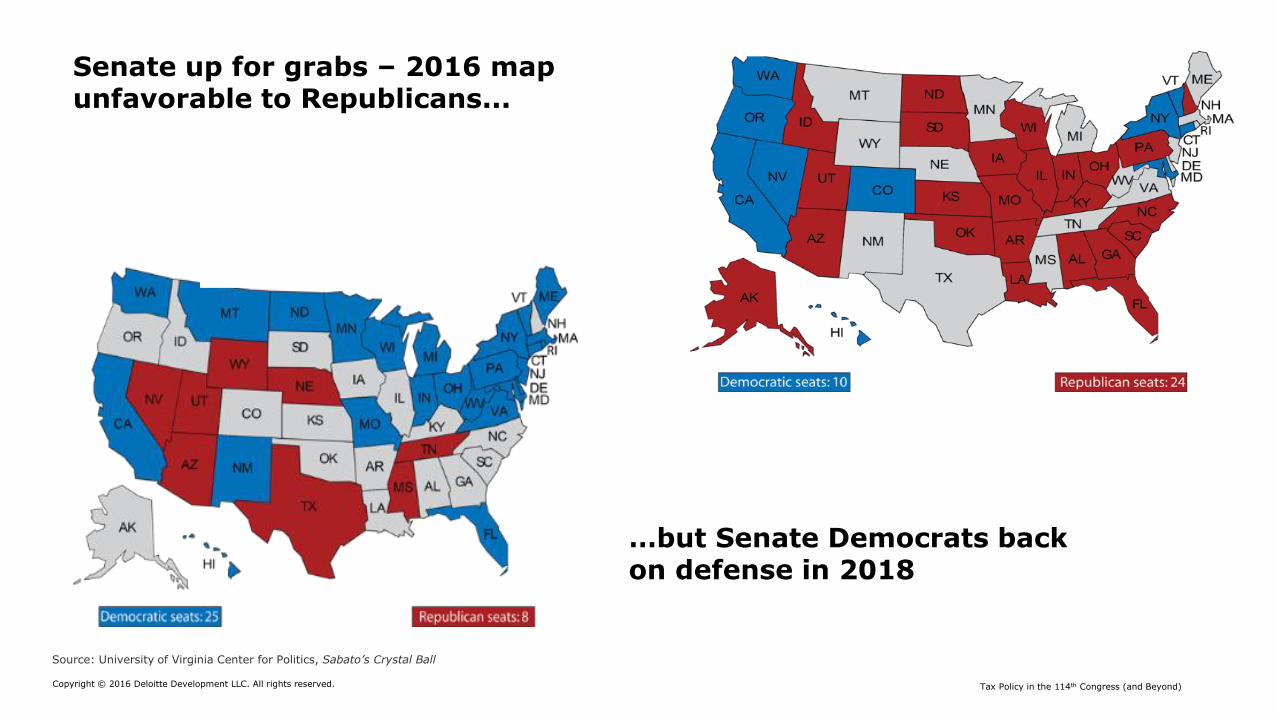

Senate up for grabs – 2016 map unfavorable to Republicans...

Source: University of Virginia Center for Politics, Sabato’s Crystal Ball

…but Senate Democrats back on defense in 2018

Tax Policy in the 114th Congress (and Beyond) Copyright © 2016 Deloitte Development LLC. All rights reserved.

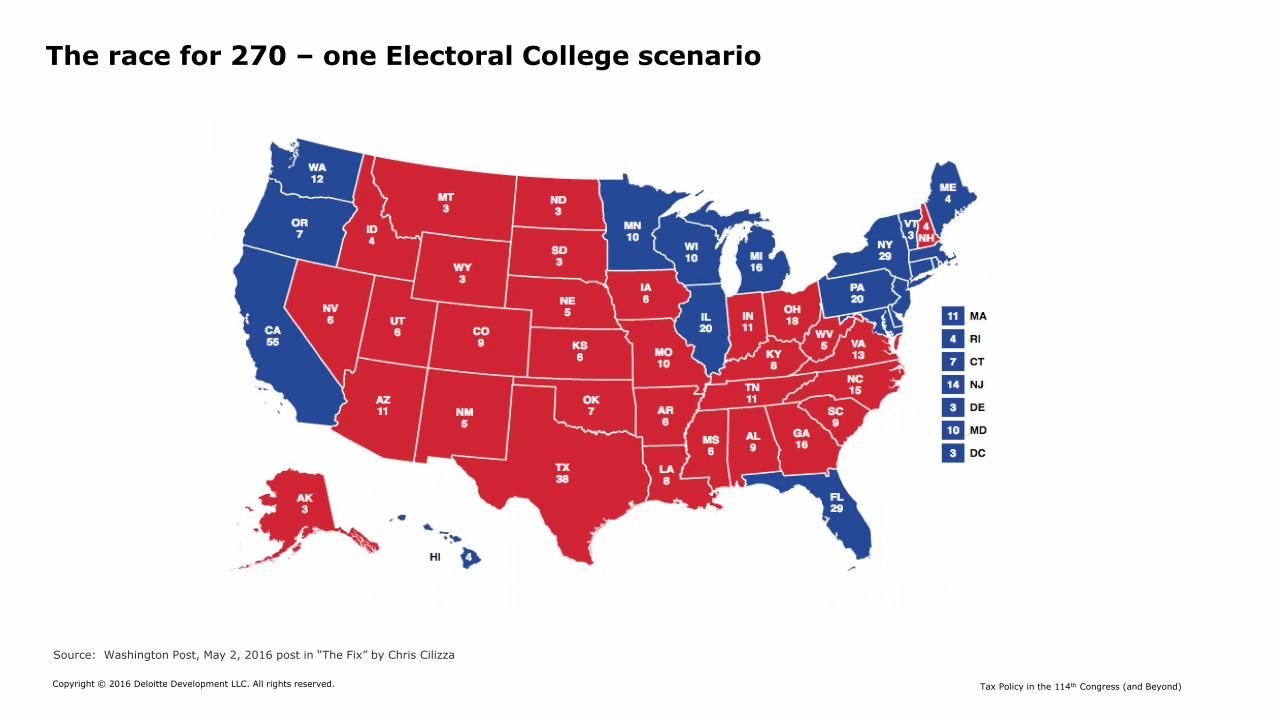

The race for 270 – one Electoral College scenario

Source: Washington Post, May 2, 2016 post in “The Fix” by Chris Cilizza

Presentation title [To edit, click View > Slide Master > Slide master1]

Copyright © 2016 Deloitte Development LLC. All rights reserved. 13

Can history help predict future tax changes?

Tax Policy in the 114th Congress (and Beyond)

Signed Economic Recovery Tax Act on August 13, 1981

Signed Omnibus Budget Reconciliation Act on November 5, 1990

Signed Omnibus Budget Reconciliation Act on August 10, 1993

Signed Economic Growth and Tax Relief Reconciliation Act on June 7, 2001

Signed American Recovery and Reinvestment Act on February 17, 2009

Act Fast Tailwinds Help

Economic recession

Projected budget deficits

Projected budget deficits

Projected budget surpluses

Financial crisis

Tax reform in 2015:

lots of talk, little action

Tax Policy in the 114th Congress (and Beyond) Copyright © 2016 Deloitte Development LLC. All rights reserved.

Tax reform in 2015 – missed opportunities and lessons learned

The parties can’t agree on how much revenue is enough and whether to use tax reform to make the system more (or less) progressive than it is today

Pass-through supporters indicated to Congress that if C Corps get a rate reduction that there is no other benefit, short of a rate cut, that will work for them

First idea Second idea Last idea

Comprehensive tax reform

How about business only tax reform?

Can we pair international tax reform with more money to help pay for highways?

Political toxicity of raising the gas tax, along with inversions, foreign acquisitions, BEPS, and European Commission cases created a perfect storm for this approach, but talks ostensibly fell apart due to disagreement over highway spending levels

Tax Policy in the 114th Congress (and Beyond) Copyright © 2016 Deloitte Development LLC. All rights reserved.

“Corporate-only” tax reform – tough optics

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Share of Net Income by Entity Type

C Corporations

Source: Deloitte analysis of IRS Statistics of Income data (Integrated Business Data, Table 1)

S Corporations

Partnerships

Sole Proprietorships

C Corp returns as a share of all business returns

(right axis)

Tax Policy in the 114th Congress (and Beyond) Copyright © 2016 Deloitte Development LLC. All rights reserved.

Populist tax sentiment hard for policymakers to ignore

0%

10%

20%

30%

40%

50%

60%

70%

80%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Percentage of Americans Who Feel these Groups Pay “Too Little” in Taxes

Middle-Income Individuals

Lower-Income Individuals

Source: Gallup, More Americans Say Low-Income Earners Pay Too Much in Taxes, Justin McCarthy (April 15, 2015)

Corporations

Upper-Income Individuals

Tax Policy in the 114th Congress (and Beyond) Copyright © 2016 Deloitte Development LLC. All rights reserved.

The year-end 2015 tax extenders deal – a recap

Made Permanent Medium-Term Extension Two-Year Extension (‘15-16)

R&D Credit Active

Financing

Exception from

Subpart F

Enhanced Sec.

179 Expensing 15-year straight-line

recovery for qualified

leasehold

improvements

Tax-free IRA

distributions for

charitable

purposes Itemized deduction for

state/local sales tax

Stimulus-era enhancements

to EITC, CTC, and AOTC

Bonus depreciation

(phased-out thru 2019) CFC “Look-

Through” Rule

(thru 2019)

Work

Opportunity

Tax Credit

(thru 2019) New Markets

Tax Credit

(thru 2019)

PTC for Wind

Energy

(phased-out

thru 2019)

Enhanced ITC

for Solar Energy

(phased-out

thru 2021)

Most other alternative

energy & energy

efficiency provisions Itemized deduction for

mortgage insurance

premiums

Exclusion for certain

forgiven mortgage

debt Other, often

parochial,

provisions

Non-Extender Policies

2-year suspension of

medical device tax

(‘16-’17) 2-year delay of

“Cadillac” tax

(‘18-’19)

The case for tax reform remains strong…

Tax Policy in the 114th Congress (and Beyond) Copyright © 2016 Deloitte Development LLC. All rights reserved.

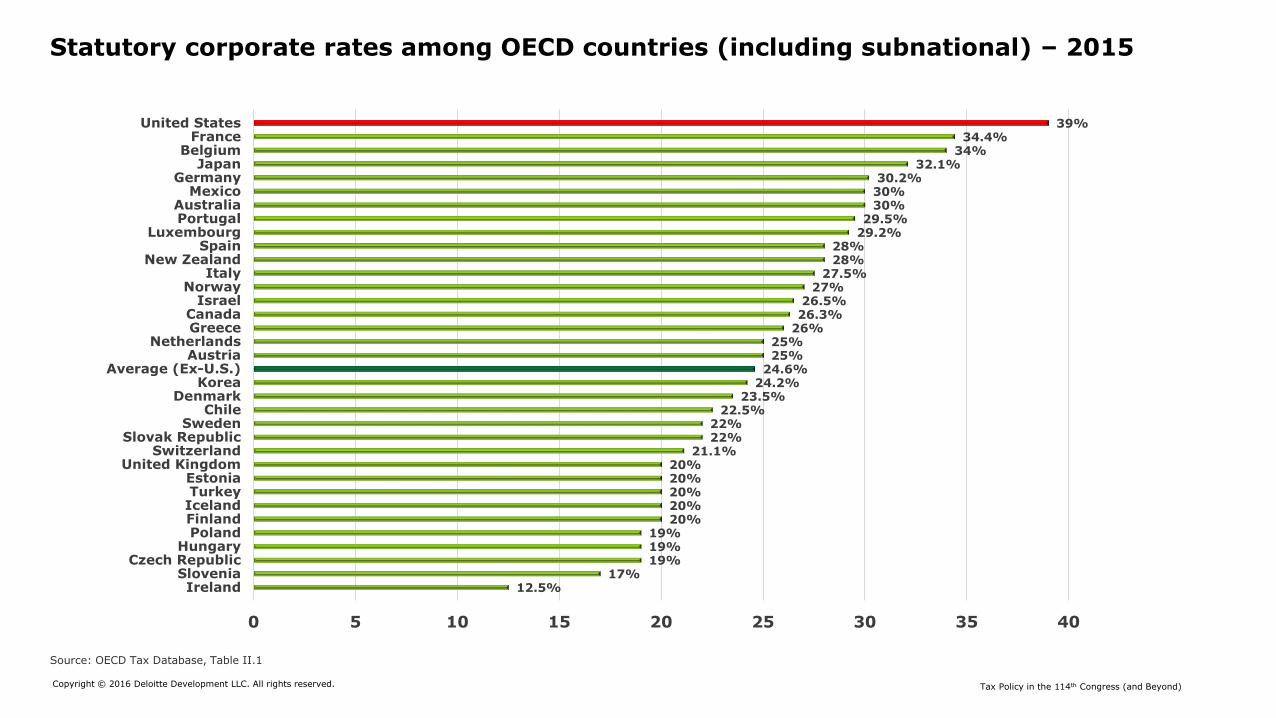

Statutory corporate rates among OECD countries (including subnational) – 2015

12.5% 17%

19% 19% 19%

20% 20% 20% 20% 20%

21.1% 22% 22%

22.5% 23.5%

24.2% 24.6% 25% 25%

26% 26.3% 26.5%

27% 27.5%

28% 28%

29.2% 29.5%

30% 30% 30.2%

32.1% 34%

34.4% 39%

0 5 10 15 20 25 30 35 40

IrelandSlovenia

Czech RepublicHungary

PolandFinlandIcelandTurkeyEstonia

United KingdomSwitzerland

Slovak RepublicSweden

ChileDenmark

KoreaAverage (Ex-U.S.)

AustriaNetherlands

GreeceCanada

IsraelNorway

ItalyNew Zealand

SpainLuxembourg

PortugalAustralia

MexicoGermany

JapanBelgium

FranceUnited States

Source: OECD Tax Database, Table II.1

Tax Policy in the 114th Congress (and Beyond) Copyright © 2016 Deloitte Development LLC. All rights reserved.

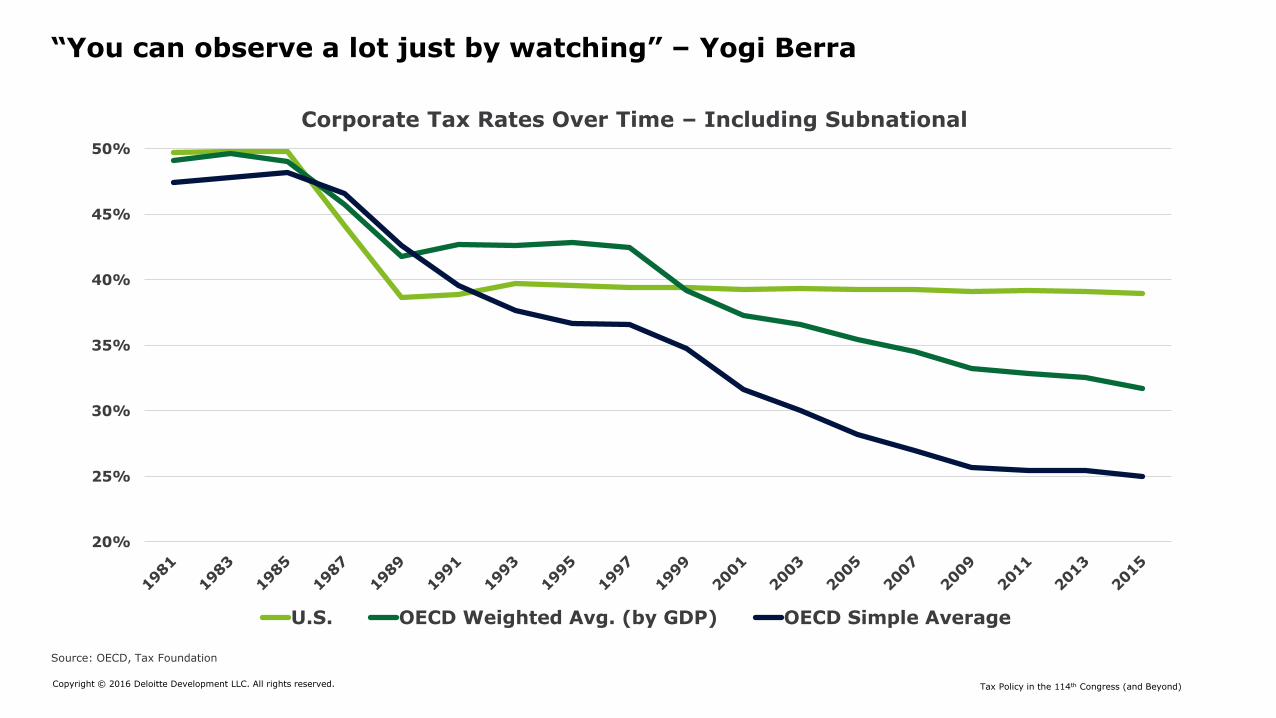

“You can observe a lot just by watching” – Yogi Berra

20%

25%

30%

35%

40%

45%

50%

Corporate Tax Rates Over Time – Including Subnational

U.S. OECD Weighted Avg. (by GDP) OECD Simple Average

Source: OECD, Tax Foundation

Tax Policy in the 114th Congress (and Beyond) Copyright © 2016 Deloitte Development LLC. All rights reserved.

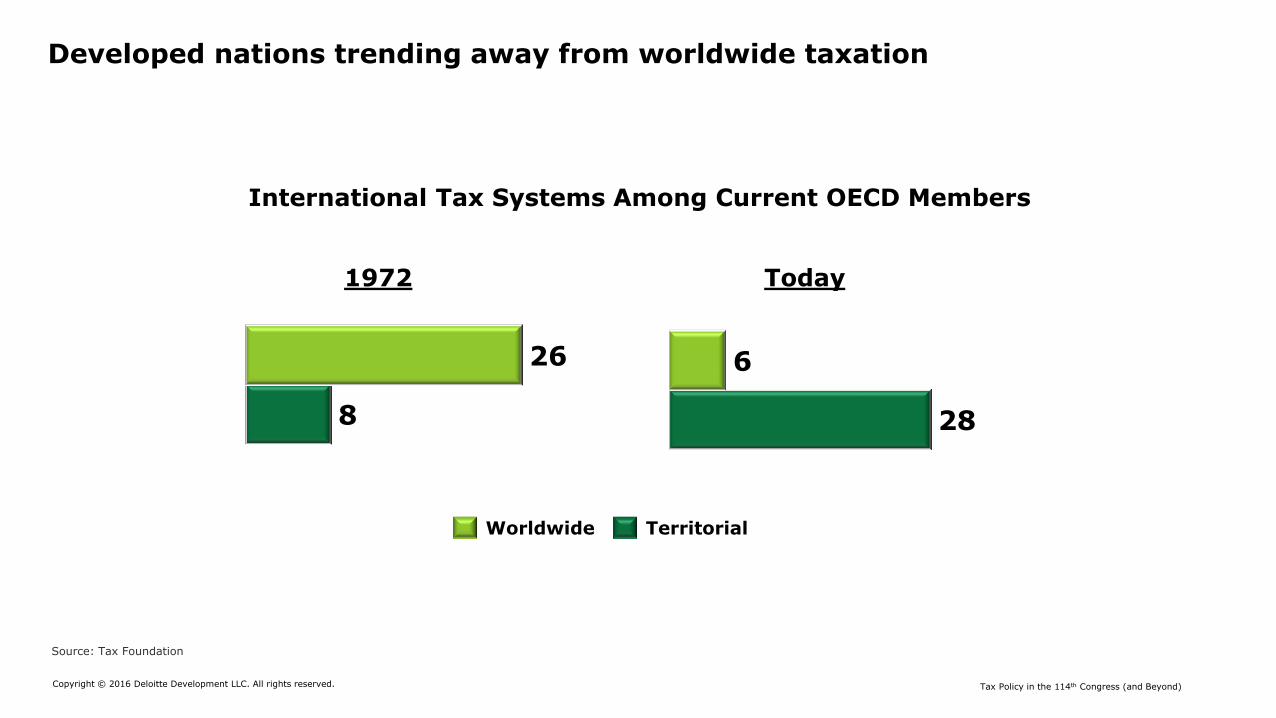

Developed nations trending away from worldwide taxation

8

26

28

6

Source: Tax Foundation

International Tax Systems Among Current OECD Members

Territorial Worldwide

1972 Today

…but threshold issues remain unresolved

Tax Policy in the 114th Congress (and Beyond) Copyright © 2016 Deloitte Development LLC. All rights reserved.

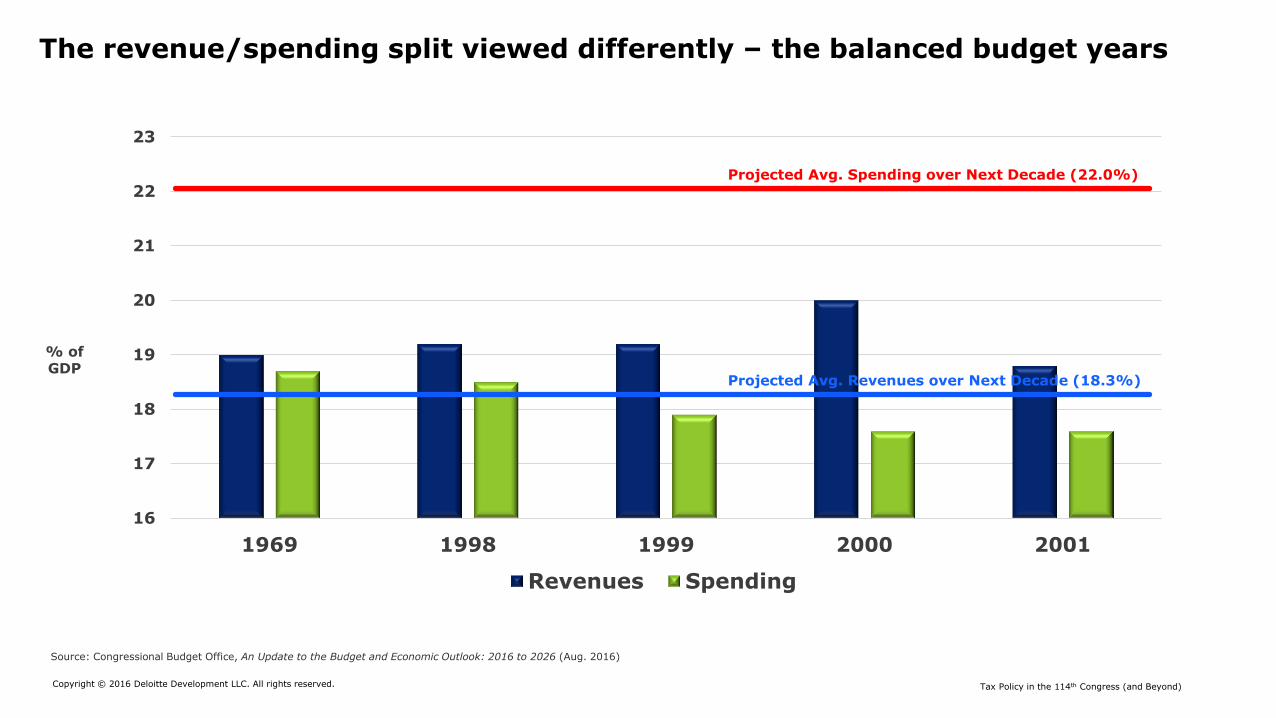

The revenue/spending split viewed differently – the balanced budget years

16

17

18

19

20

21

22

23

1969 1998 1999 2000 2001

Revenues Spending

% of GDP

Source: Congressional Budget Office, An Update to the Budget and Economic Outlook: 2016 to 2026 (Aug. 2016)

Projected Avg. Spending over Next Decade (22.0%)

Projected Avg. Revenues over Next Decade (18.3%)

Tax Policy in the 114th Congress (and Beyond) Copyright © 2016 Deloitte Development LLC. All rights reserved.

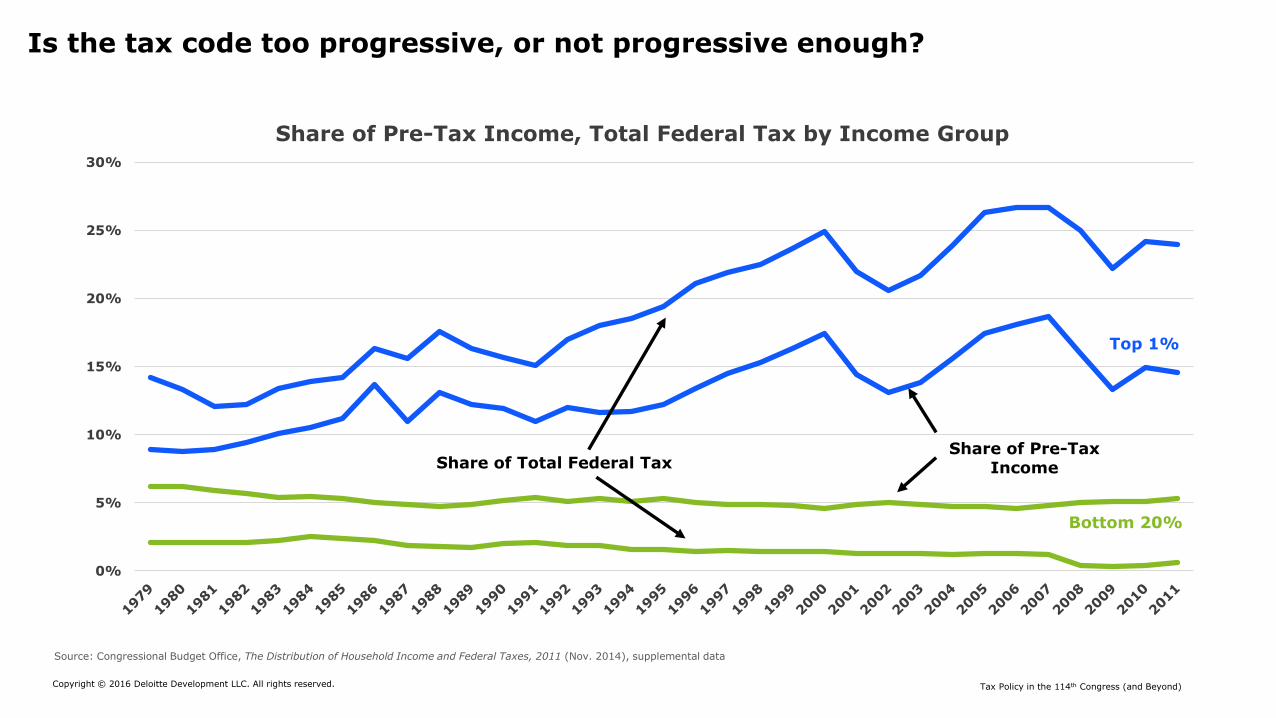

Is the tax code too progressive, or not progressive enough?

0%

5%

10%

15%

20%

25%

30%

Share of Pre-Tax Income, Total Federal Tax by Income Group

Source: Congressional Budget Office, The Distribution of Household Income and Federal Taxes, 2011 (Nov. 2014), supplemental data

Top 1%

Bottom 20%

Share of Pre-Tax Income Share of Total Federal Tax

Tax Policy in the 114th Congress (and Beyond) Copyright © 2016 Deloitte Development LLC. All rights reserved.

Broadening the base – easier said than done

Largest Corporate Tax Expenditures - 2014 Billions

of $

Deferral of active CFC income 83.4

Accelerated depreciation (w/o bonus) 24.0

§199 deduction 12.2

Deferral on like-kind exchanges 11.7

Exclusion for muni bond interest 9.3

Deferral of gain on installment sales 6.9

Low-income housing tax credit 6.8

Expensing of R&E expenditures 4.6

Reduced rates on corporate TI below $10M 3.8

Inventory property sales source rule exception 3.0

Top 10 as a % of total corporate ~80%

Largest Individual Tax Expenditures - 2014 Billions

of $

Exclusion of employer-provided health benefits 143.0

Reduced rates on LT cap gains/dividends 96.5

Tax-preferred retirement plans 88.8

Earned Income Tax Credit 69.2

Mortgage interest deduction 67.8

Child tax credit 57.3

State and local tax deduction 56.5

Exclusion of Social Security benefits 37.4

Charitable contribution deduction 34.8

Exclusion for cafeteria plan benefits 34.5

Top 10 as a % of total individual ~66%

Source: Senate Budget Committee Print 113-32, Tax Expenditures: Compendium of Background Material on Individual Provisions (Dec. 2014)

Tax Policy in the 114th Congress (and Beyond) Copyright © 2016 Deloitte Development LLC. All rights reserved.

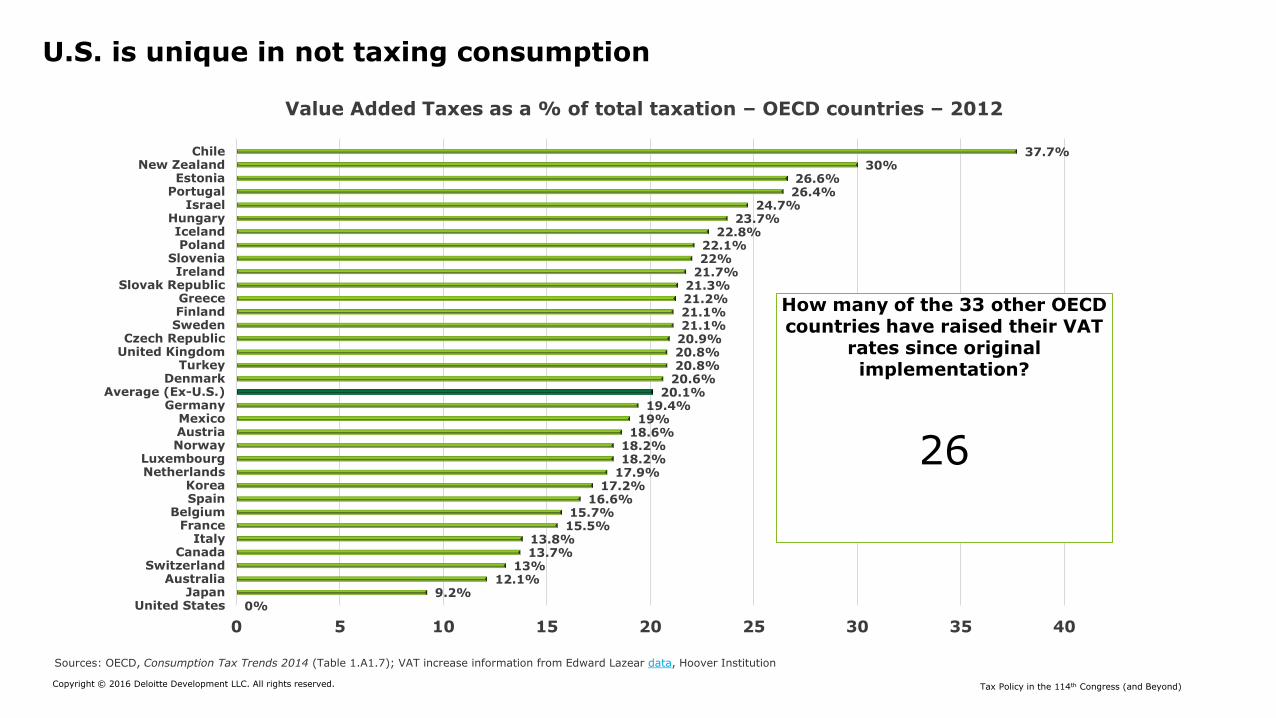

U.S. is unique in not taxing consumption

0% 9.2%

12.1% 13%

13.7% 13.8%

15.5% 15.7%

16.6% 17.2%

17.9% 18.2% 18.2%

18.6% 19%

19.4% 20.1%

20.6% 20.8% 20.8% 20.9% 21.1% 21.1% 21.2% 21.3%

21.7% 22% 22.1%

22.8% 23.7%

24.7% 26.4% 26.6%

30% 37.7%

0 5 10 15 20 25 30 35 40

United StatesJapan

AustraliaSwitzerland

CanadaItaly

FranceBelgium

SpainKorea

NetherlandsLuxembourg

NorwayAustriaMexico

GermanyAverage (Ex-U.S.)

DenmarkTurkey

United KingdomCzech Republic

SwedenFinlandGreece

Slovak RepublicIreland

SloveniaPoland

IcelandHungary

IsraelPortugalEstonia

New ZealandChile

Sources: OECD, Consumption Tax Trends 2014 (Table 1.A1.7); VAT increase information from Edward Lazear data, Hoover Institution

How many of the 33 other OECD countries have raised their VAT

rates since original implementation?

26

Value Added Taxes as a % of total taxation – OECD countries – 2012

Presidential nominees and top lawmakers pushing widely divergent approaches

Tax Policy in the 114th Congress (and Beyond) Copyright © 2016 Deloitte Development LLC. All rights reserved.

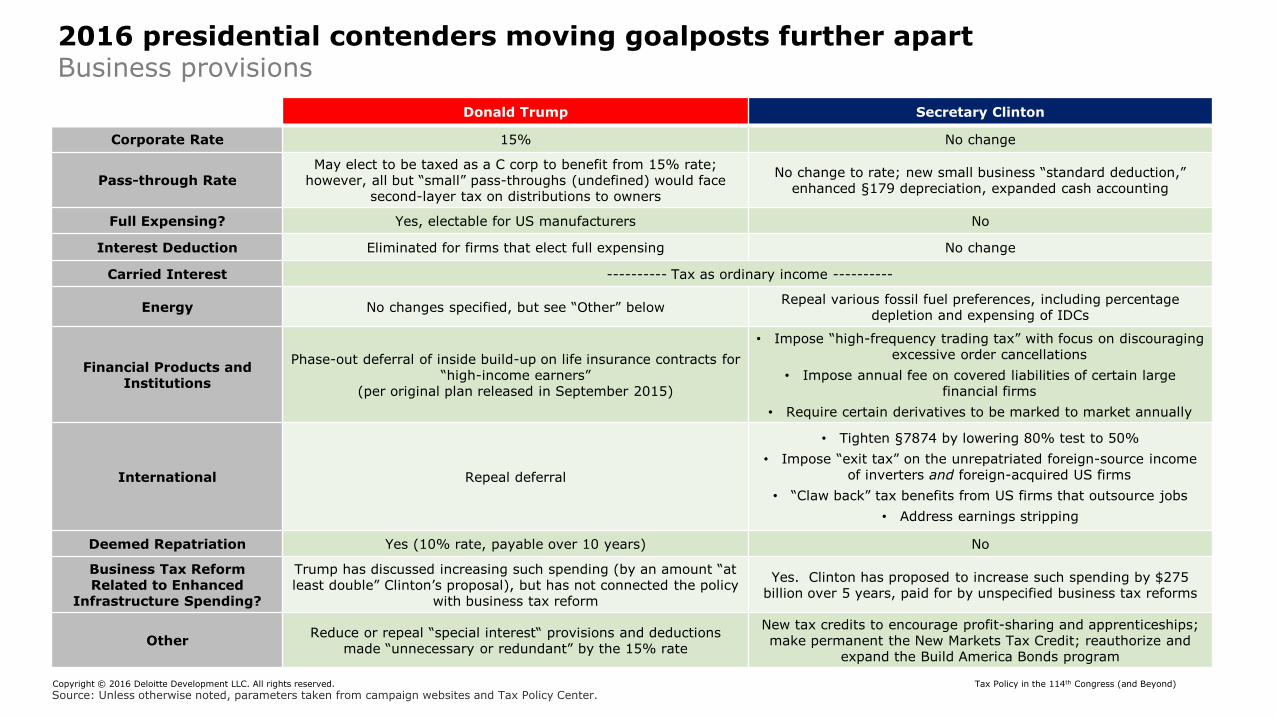

2016 presidential contenders moving goalposts further apart Business provisions

Donald Trump Secretary Clinton

Corporate Rate 15% No change

Pass-through Rate May elect to be taxed as a C corp to benefit from 15% rate;

however, all but “small” pass-throughs (undefined) would face second-layer tax on distributions to owners

No change to rate; new small business “standard deduction,” enhanced §179 depreciation, expanded cash accounting

Full Expensing? Yes, electable for US manufacturers No

Interest Deduction Eliminated for firms that elect full expensing No change

Carried Interest ---------- Tax as ordinary income ----------

Energy No changes specified, but see “Other” below Repeal various fossil fuel preferences, including percentage

depletion and expensing of IDCs

Financial Products and Institutions

Phase-out deferral of inside build-up on life insurance contracts for “high-income earners”

(per original plan released in September 2015)

• Impose “high-frequency trading tax” with focus on discouraging excessive order cancellations

• Impose annual fee on covered liabilities of certain large financial firms

• Require certain derivatives to be marked to market annually

International Repeal deferral

• Tighten §7874 by lowering 80% test to 50%

• Impose “exit tax” on the unrepatriated foreign-source income of inverters and foreign-acquired US firms

• “Claw back” tax benefits from US firms that outsource jobs

• Address earnings stripping

Deemed Repatriation Yes (10% rate, payable over 10 years) No

Business Tax Reform Related to Enhanced

Infrastructure Spending?

Trump has discussed increasing such spending (by an amount “at least double” Clinton’s proposal), but has not connected the policy

with business tax reform

Yes. Clinton has proposed to increase such spending by $275 billion over 5 years, paid for by unspecified business tax reforms

Other Reduce or repeal “special interest“ provisions and deductions

made “unnecessary or redundant” by the 15% rate

New tax credits to encourage profit-sharing and apprenticeships; make permanent the New Markets Tax Credit; reauthorize and

expand the Build America Bonds program

.Source: Unless otherwise noted, parameters taken from campaign websites and Tax Policy Center

Tax Policy in the 114th Congress (and Beyond) Copyright © 2016 Deloitte Development LLC. All rights reserved.

2016 presidential contenders moving goalposts further apart Individual provisions

Donald Trump Secretary Clinton

Top Individual Rate 33% (begins at $225k for joint filers) 43.6% (after new 4 percent surcharge on income over $5 million)

“Buffett Rule” No Yes. Minimum 30% rate on income over $1 million.

Capital Gains and Dividends 20% top rate (repeal 3.8% net investment income tax) Raise top capital gains rate to 43.4% (holding period ≤ 2 years),

gradually reduced to 23.8% (holding period > 6 years); no specified changes to dividend rates

Alternative Minimum Tax Repeal (both individual and corporate) No change

Itemized Deductions Dollar cap on total itemized deductions

($200k for joint filers, $100k for single filers)

Except for charitable contributions, limit tax benefit to 28 cents on the dollar (28% limit would also apply to excluded employer-

provided health benefits, tax exempt interest, etc.)

Standard Deduction $15,000 (single) / $30,000 (joint), indexed No change

Retirement No changes specified Limit additional contributions for taxpayers with high-balance,

tax-deferred retirement accounts

Estate and Gift Tax Repeal, but tax capital gains at death in excess of $10 million

• Increase rate to 45% on estate value > $3.5m; 50% on estates > $10m; 55% on estates > $50m;

65% on estates > $500m • Keep exemption portability, but no inflation adjustment

• Eliminate “step-up basis” at death • Unindexed $1m lifetime gift tax exemption

• Tighten grantor trust rules

Personal Exemptions Repeal No change

New Tax Benefits New above-the-line deduction for child care costs + new

Dependent Care Savings Accounts New tax credits for family caregivers and high out-of-pocket

health costs, expanded Child Tax Credit

10-Year Revenue Effect (Individual AND Business)

Loses $6.2 trillion

Raises $1.4 trillion

.Source: Unless otherwise noted, parameters and revenue impact taken from campaign websites and Tax Policy Center

Tax Policy in the 114th Congress (and Beyond) Copyright © 2016 Deloitte Development LLC. All rights reserved.

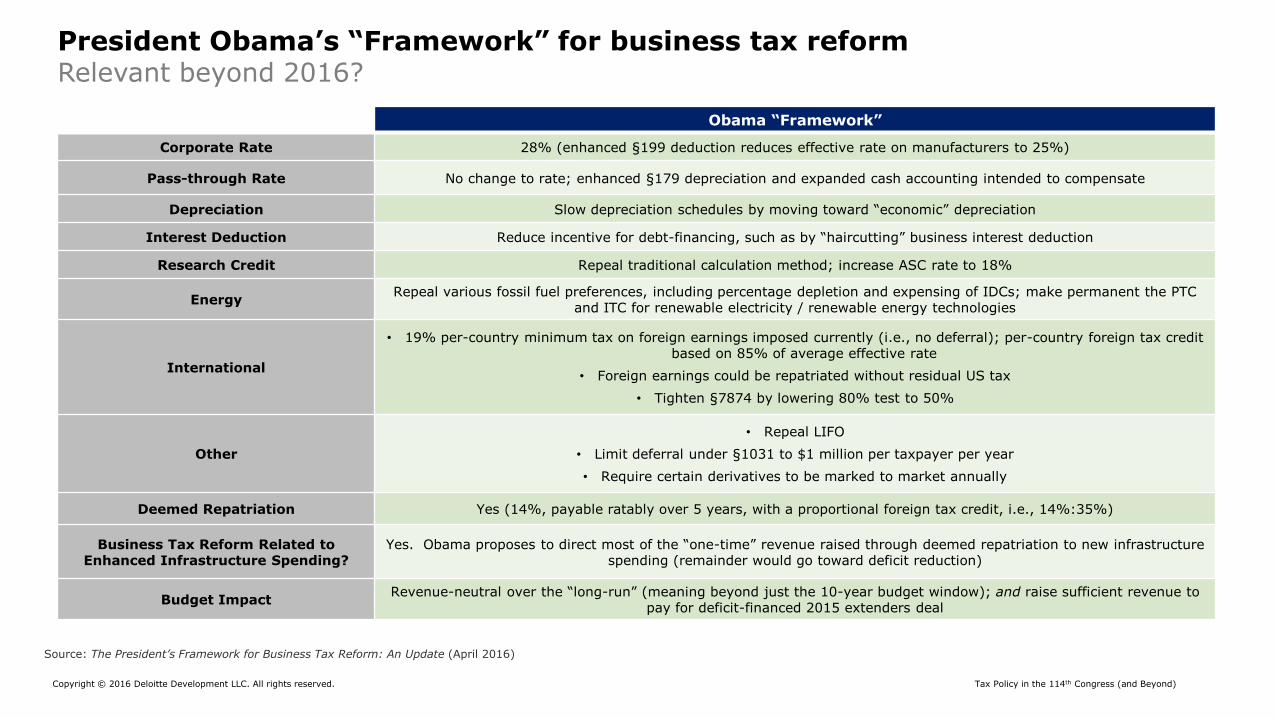

President Obama’s “Framework” for business tax reform Relevant beyond 2016?

Obama “Framework”

Corporate Rate 28% (enhanced §199 deduction reduces effective rate on manufacturers to 25%)

Pass-through Rate No change to rate; enhanced §179 depreciation and expanded cash accounting intended to compensate

Depreciation Slow depreciation schedules by moving toward “economic” depreciation

Interest Deduction Reduce incentive for debt-financing, such as by “haircutting” business interest deduction

Research Credit Repeal traditional calculation method; increase ASC rate to 18%

Energy Repeal various fossil fuel preferences, including percentage depletion and expensing of IDCs; make permanent the PTC

and ITC for renewable electricity / renewable energy technologies

International

• 19% per-country minimum tax on foreign earnings imposed currently (i.e., no deferral); per-country foreign tax credit based on 85% of average effective rate

• Foreign earnings could be repatriated without residual US tax

• Tighten §7874 by lowering 80% test to 50%

Other

• Repeal LIFO

• Limit deferral under §1031 to $1 million per taxpayer per year

• Require certain derivatives to be marked to market annually

Deemed Repatriation Yes (14%, payable ratably over 5 years, with a proportional foreign tax credit, i.e., 14%:35%)

Business Tax Reform Related to Enhanced Infrastructure Spending?

Yes. Obama proposes to direct most of the “one-time” revenue raised through deemed repatriation to new infrastructure spending (remainder would go toward deficit reduction)

Budget Impact Revenue-neutral over the “long-run” (meaning beyond just the 10-year budget window); and raise sufficient revenue to

pay for deficit-financed 2015 extenders deal

Source: The President’s Framework for Business Tax Reform: An Update (April 2016)

Tax Policy in the 114th Congress (and Beyond) Copyright © 2016 Deloitte Development LLC. All rights reserved.

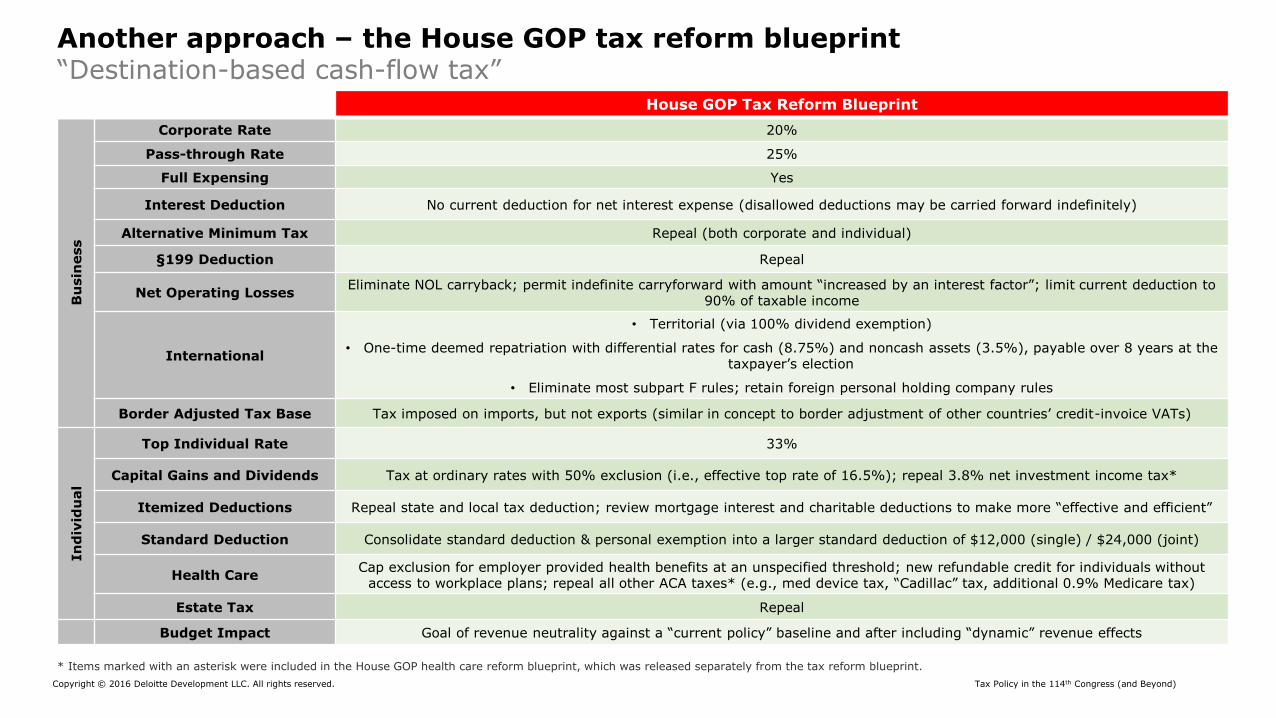

Another approach – the House GOP tax reform blueprint “Destination-based cash-flow tax”

House GOP Tax Reform Blueprint

Bu

sin

ess

Corporate Rate 20%

Pass-through Rate 25%

Full Expensing Yes

Interest Deduction No current deduction for net interest expense (disallowed deductions may be carried forward indefinitely)

Alternative Minimum Tax Repeal (both corporate and individual)

§199 Deduction Repeal

Net Operating Losses Eliminate NOL carryback; permit indefinite carryforward with amount “increased by an interest factor”; limit current deduction to

90% of taxable income

International

• Territorial (via 100% dividend exemption)

• One-time deemed repatriation with differential rates for cash (8.75%) and noncash assets (3.5%), payable over 8 years at the taxpayer’s election

• Eliminate most subpart F rules; retain foreign personal holding company rules

Border Adjusted Tax Base Tax imposed on imports, but not exports (similar in concept to border adjustment of other countries’ credit-invoice VATs)

In

div

idu

al

Top Individual Rate 33%

Capital Gains and Dividends Tax at ordinary rates with 50% exclusion (i.e., effective top rate of 16.5%); repeal 3.8% net investment income tax*

Itemized Deductions Repeal state and local tax deduction; review mortgage interest and charitable deductions to make more “effective and efficient”

Standard Deduction Consolidate standard deduction & personal exemption into a larger standard deduction of $12,000 (single) / $24,000 (joint)

Health Care Cap exclusion for employer provided health benefits at an unspecified threshold; new refundable credit for individuals without

access to workplace plans; repeal all other ACA taxes* (e.g., med device tax, “Cadillac” tax, additional 0.9% Medicare tax)

Estate Tax Repeal

Budget Impact Goal of revenue neutrality against a “current policy” baseline and after including “dynamic” revenue effects

.Items marked with an asterisk were included in the House GOP health care reform blueprint, which was released separately from the tax reform blueprint *

Tax Policy in the 114th Congress (and Beyond) Copyright © 2016 Deloitte Development LLC. All rights reserved.

Across the Capitol – senators have even more tax reform ideas

The yet unreleased corporate integration plan from Senate Finance Committee Chairman Orrin Hatch, R-Utah, is expected to call for a dividends paid deduction in order to reduce effective corporate tax rates, equalize the tax treatment of C corporations and pass-throughs, and reduce incentives for debt financing. In order keep the budget impact in check, all dividend recipients would be subject to full tax (i.e., not at preferred rates) by way of a withholding regime. To avoid favoring debt over equity, withholding is also expected to apply to interest payments on corporate debt.

Senate Finance Committee Ranking Democrat Ron Wyden of Oregon has been laying the groundwork for a possible return to the chairmanship in 2017 by releasing legislative discussion drafts: so far, (1) replacing asset-by-asset depreciation under MACRS with “pooling” approach (2) mark-to-market for speculative derivatives, and (3) changes affecting high-balance Roth accounts and inherited retirement accounts. Wyden historically has supported the policy of repealing deferral of active foreign source income as a means to help finance a reduction in the corporate rate.

Senate Finance Committee member Ben Cardin, D-Md., released legislation in 2014 that would impose a 10% credit-invoice Value Added Tax on most purchases of goods and services as part of a broader plan that would reduce the corporate rate to 17% and the top individual rate to 28%, while retaining most current law tax benefits. Cardin is expected to reintroduce an updated bill this fall.

Tax Policy in the 114th Congress (and Beyond) Copyright © 2016 Deloitte Development LLC. All rights reserved.

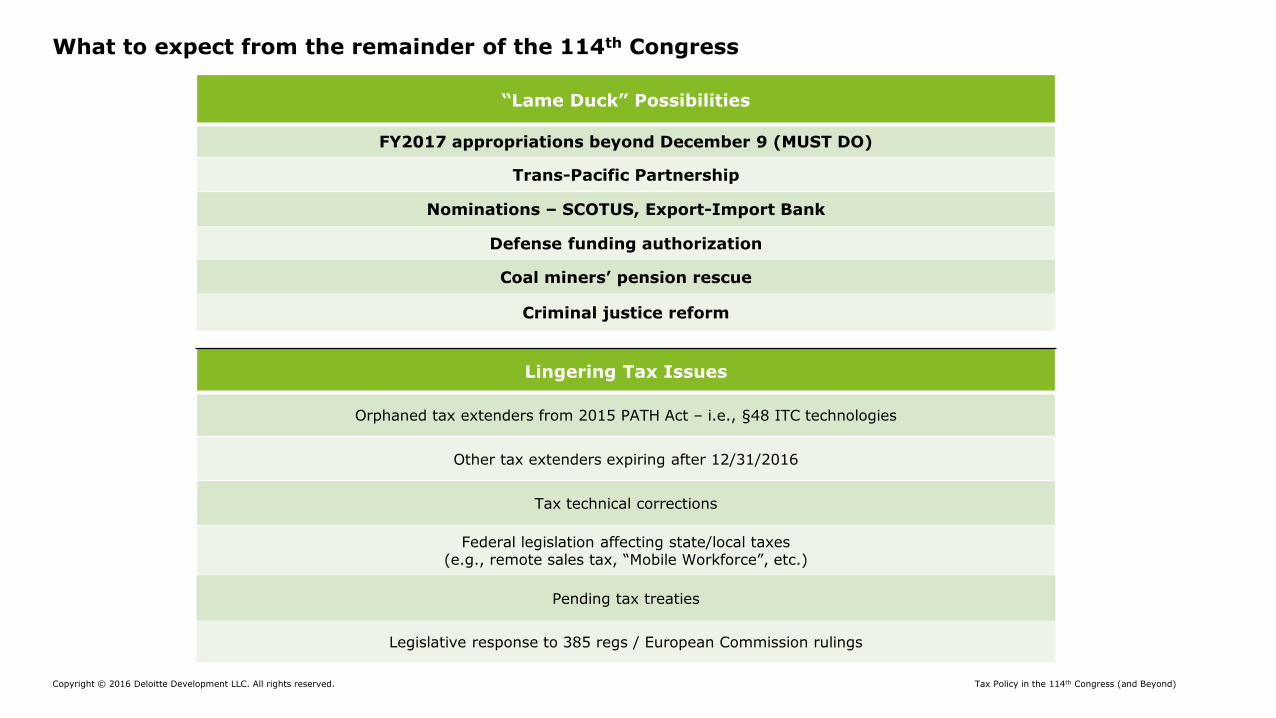

What to expect from the remainder of the 114th Congress

“Lame Duck” Possibilities

FY2017 appropriations beyond December 9 (MUST DO)

Trans-Pacific Partnership

Nominations – SCOTUS, Export-Import Bank

Defense funding authorization

Coal miners’ pension rescue

Criminal justice reform

Lingering Tax Issues

Orphaned tax extenders from 2015 PATH Act – i.e., §48 ITC technologies

Other tax extenders expiring after 12/31/2016

Tax technical corrections

Federal legislation affecting state/local taxes (e.g., remote sales tax, “Mobile Workforce”, etc.)

Pending tax treaties

Legislative response to 385 regs / European Commission rulings

Tax Policy in the 114th Congress (and Beyond) Copyright © 2016 Deloitte Development LLC. All rights reserved.

Questions?

Alex Brosseau

202.661.4532

Tax Policy in the 114th Congress (and Beyond) Copyright © 2016 Deloitte Development LLC. All rights reserved.

This presentation contains general information only and Deloitte is not, by means of this presentation, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This presentation is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Deloitte shall not be responsible for any loss sustained by any person who relies on this presentation.

About this presentation

About Deloitte

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL

and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see

www.deloitte.com/about for a detailed description of DTTL and its member firms. Please see www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte LLP

and its subsidiaries. Certain services may not be available to attest clients under the rules and regulations of public accounting.

Copyright © 2016 Deloitte Development LLC. All rights reserved.

36 USC 220506