systemic risk caused by synchronization

TRANSCRIPT

Systemic Risk caused by Synchronization

SYstemic Risk TOmography:

Signals, Measurements, Transmission Channels, and Policy Interventions

Jorgen Vitting Andersen, CNRS, Centre d´Economie de la Sorbonne, Université Paris 1 Panthéon-Sorbonne Collaborators: L. Bellenzier, P. Dellaportas, S. Galam, A Nowak, P. de Peretti, M. Roszczynska, G. Rotundo, R. Savona, S. Stefani, and I. Vrontos SYRTO Project Final Conference, Paris – February 19, 2016

“Socio-Finance: price formation

is a sociological phenomenon.

“Will consider human decision making to happen in

two different ways

i) direct communication between people

or

ii) indirect communication between people through

a medium, say price index (Finance)

-1st level: communication between individuals

- 2nd level: communication between groups of

individuals

Dynamics of indirect communication

of individuals through a price/index

“

Indirect decision making through a medium:

people trading a financial market index

The “symphony” of the market

(complexity theory applied to financial markets)

Synchronization of markets: “price-quakes”

Integrate-and-fire (IAF) oscillators: fireflies

Integrate-and-fire oscillators

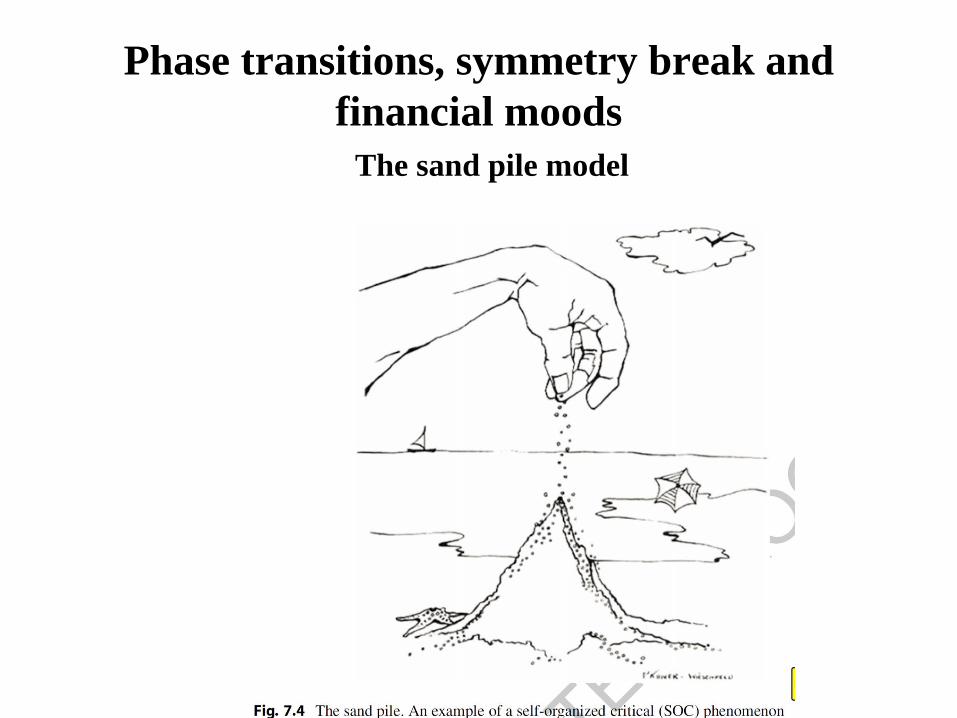

Phase transitions, symmetry break and

financial moods

The sand pile model

Understanding Excessive Risk Taking Seen in

Experiments on Financial Markets

• Jørgen Vitting Andersen, CNRS,

Centre d’Economie de la Sorbonne,

University of Paris 1.

• Research in progress, collaborators:

Yifang Liu, Philippe de Peretti, Maxim

Frolov, Roberto Savona, Hayette Gatfaoui,

Rania Kaffel

Individual versus collective risk taking

• Individual risks: Men are known to be more risk loving

compared to women. For real market traders see e.g. :

“Endogenous steroids and financial risk on a London

trading floor”, J. M. Coates and J. Herbert, PNAS, V.105,

16, 6167-72 (2008); “A note on trader Sharpe Ratios”, J.

M. Coates and L. Page, PLoSONE, V.4, 11, e8036 (2009)

• Collective risks: how does a group of traders with

heterogeneous risk profiles influence the formation of

market risks?

Setup of experiments

• Before each experiments individual risk profiles of participants were

obtained from lotteries (C. A. Holt, S. Laury, The American Economic

Review, V. 92, 1644 (2002)

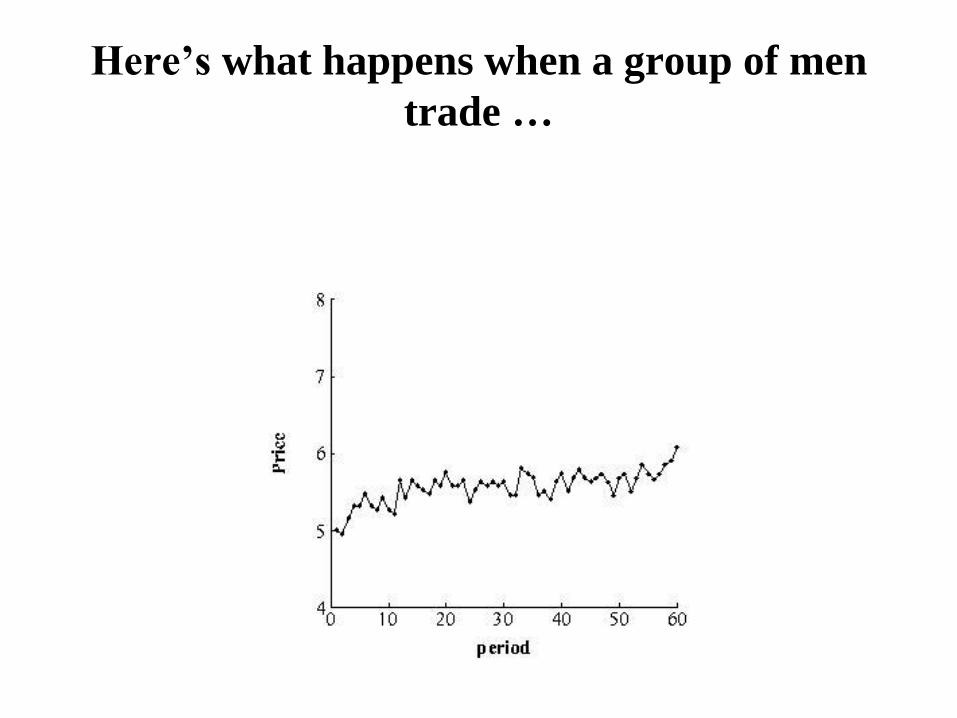

Here’s what happens when a group of men

trade …

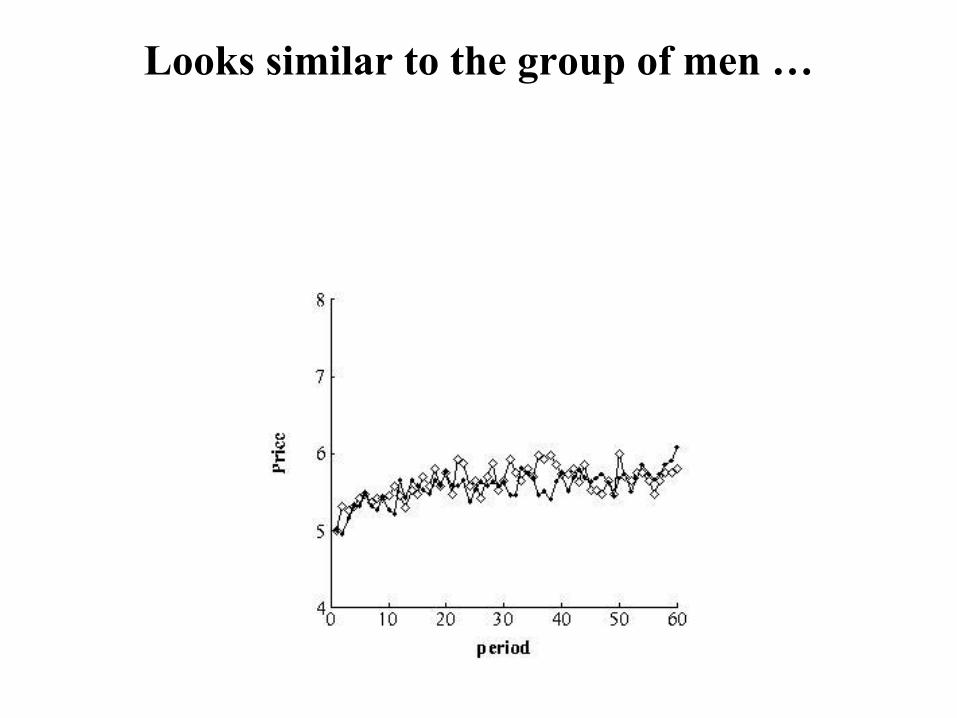

Next we let a group of women trade …

Looks similar to the group of men …

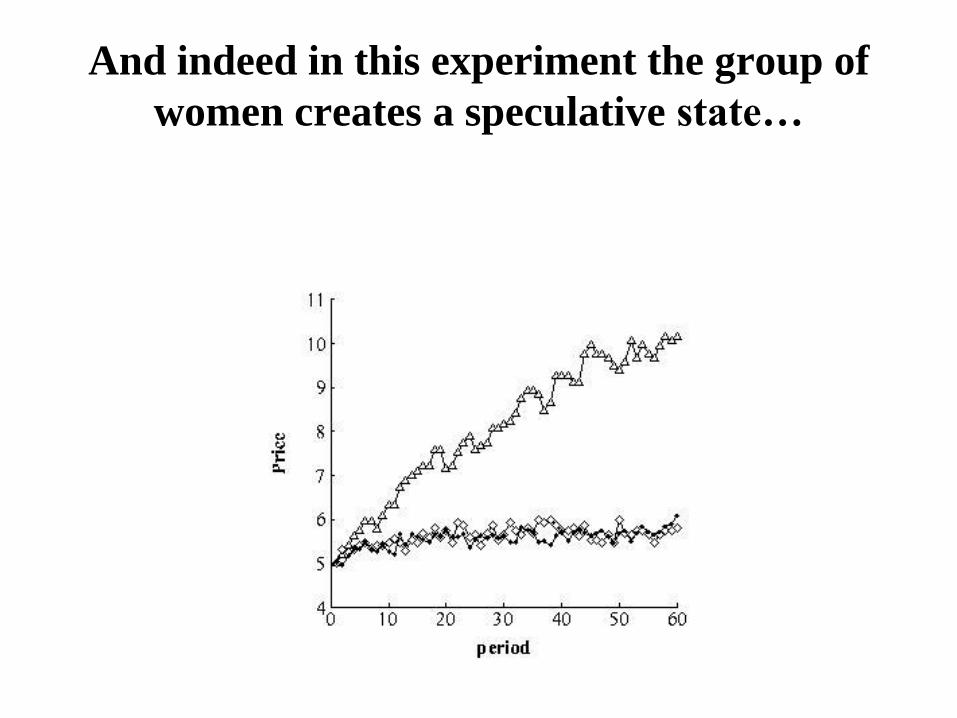

Then another group of women … initially this

group of women seem to trade differently…

And indeed in this experiment the group of

women creates a speculative state…

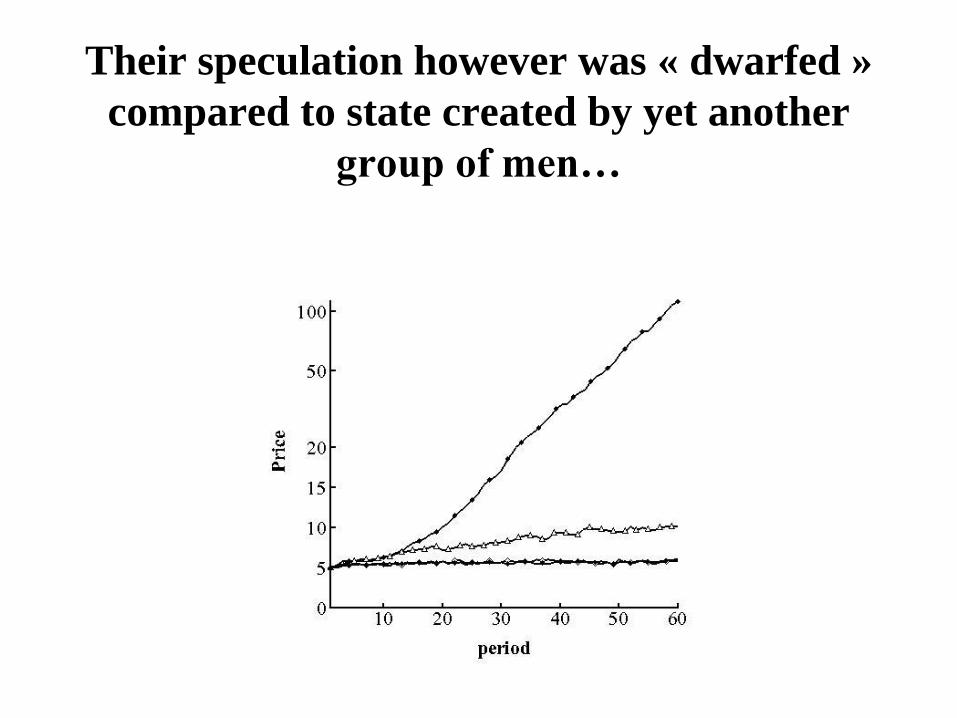

Their speculation however was « dwarfed »

compared to state created by yet another

group of men…

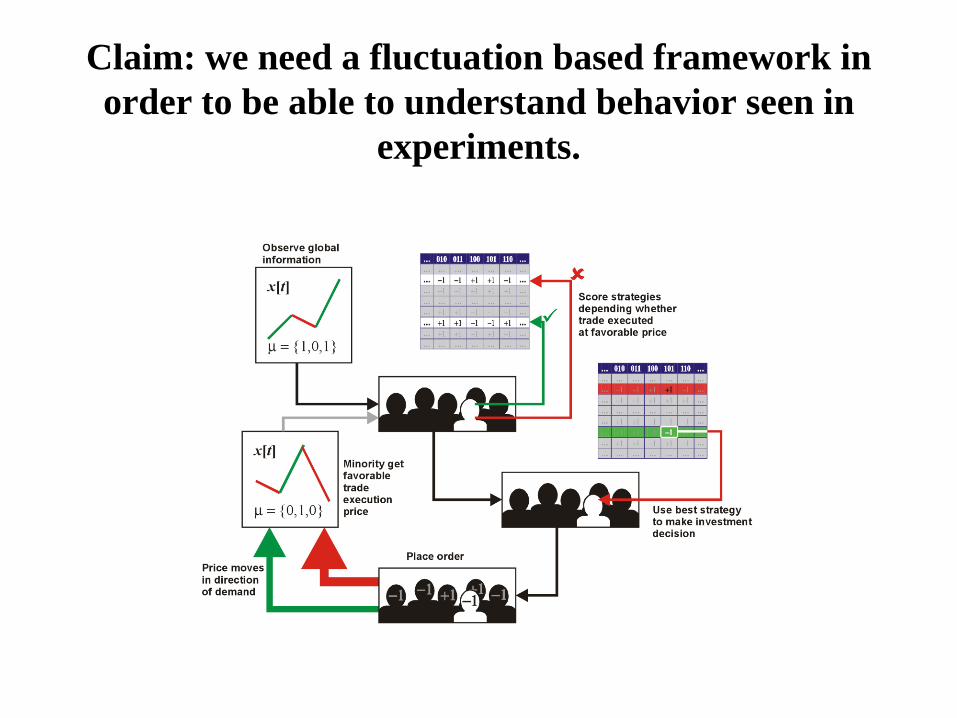

Claim: we need a fluctuation based framework in

order to be able to understand behavior seen in

experiments.

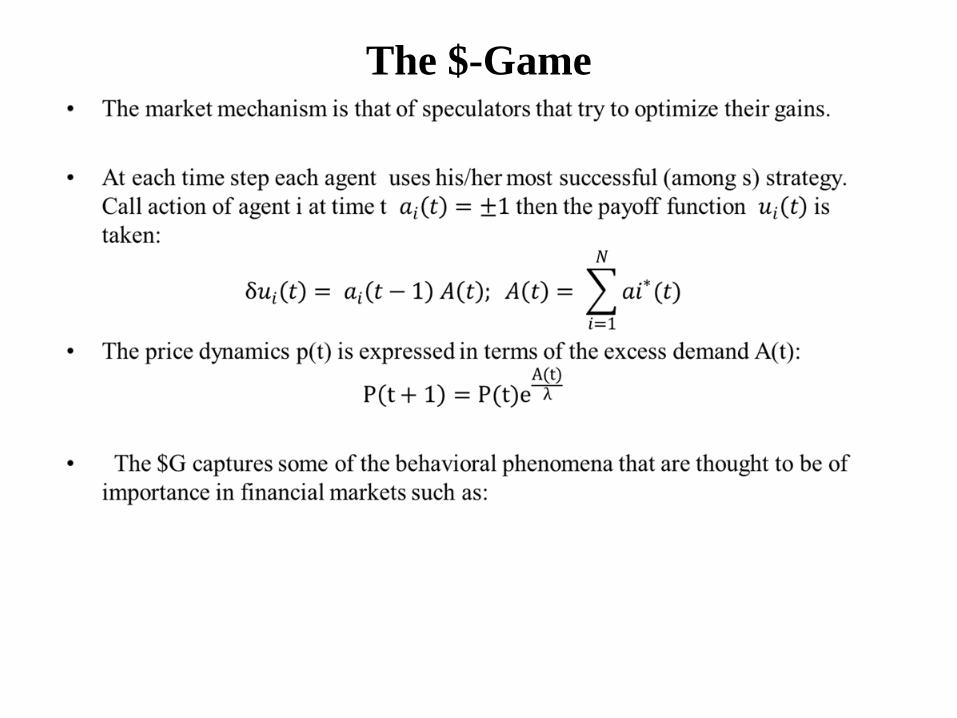

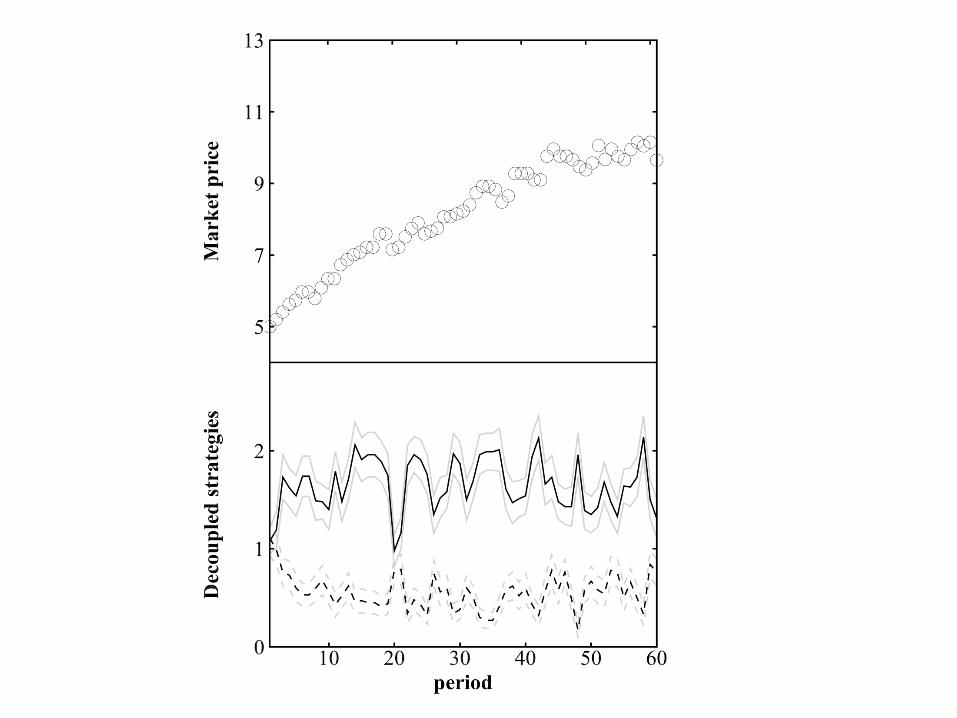

The $-Game

The $-Game

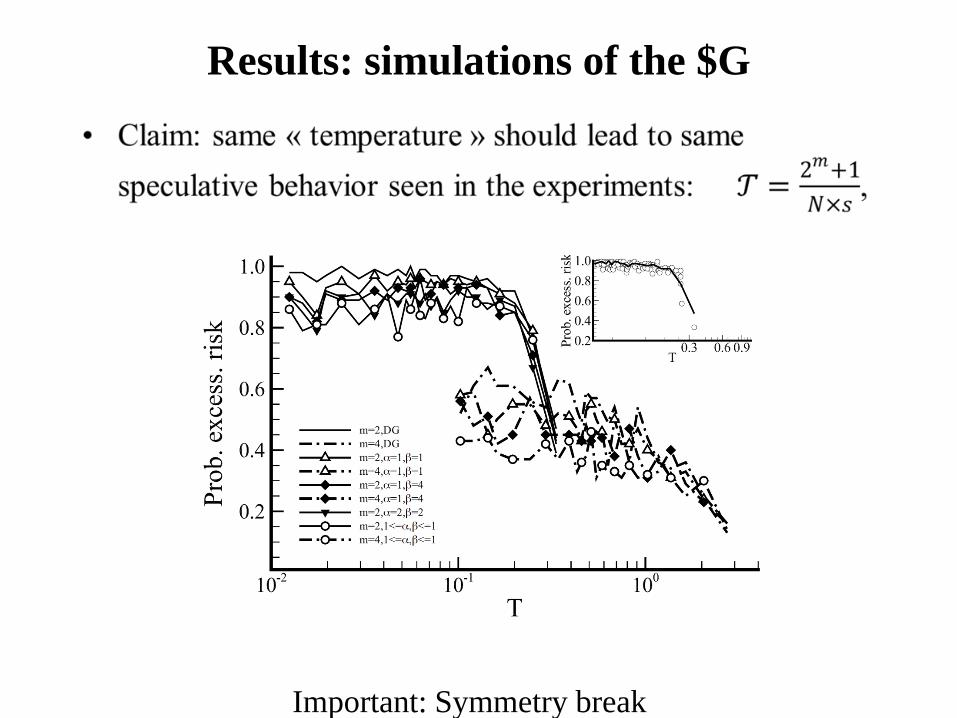

Results: simulations of the $G

Important: Symmetry break

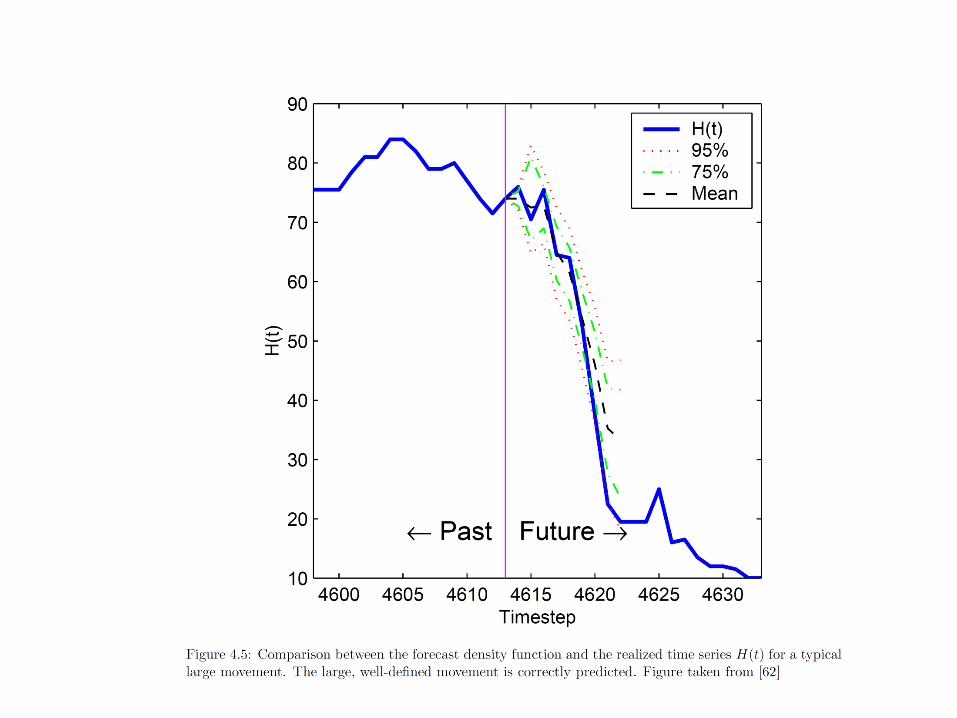

Taking the «temperature» of the market: predicting big

price «swings »

• Internal state of water? Insert a thermometer into the

liquid.

• Internal state of market? «slave » an agent based model to

the price evolution.

• Market in a “hot” or “cold” state.

ACTION

0000 0

0000

0001 0

0100 1

1010

0101 1

0101

0110 1

1011

0111 1

Dynamics of direct communication

between individuals

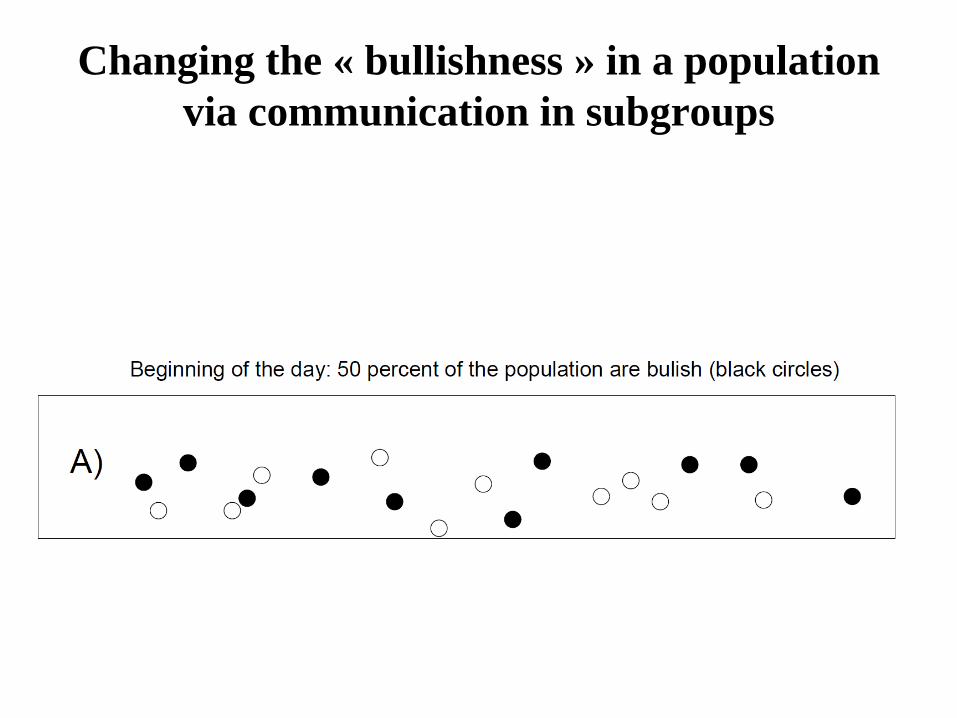

Changing the « bullishness » in a population

via communication in subgroups

During the day communication takes place in

random subgroups

During the day communication takes place in

random subgroups

During the day communication takes place in

random subgroups

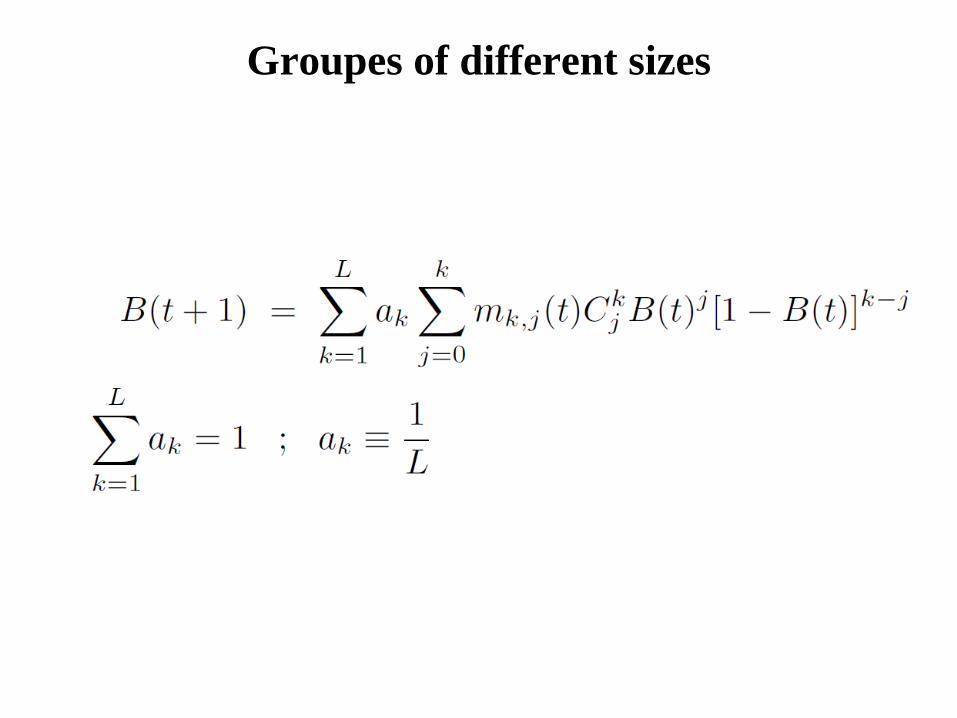

Quantitative description of model

Groupe of size k

Groupes of different sizes

Link between communication and its impact

on the markets

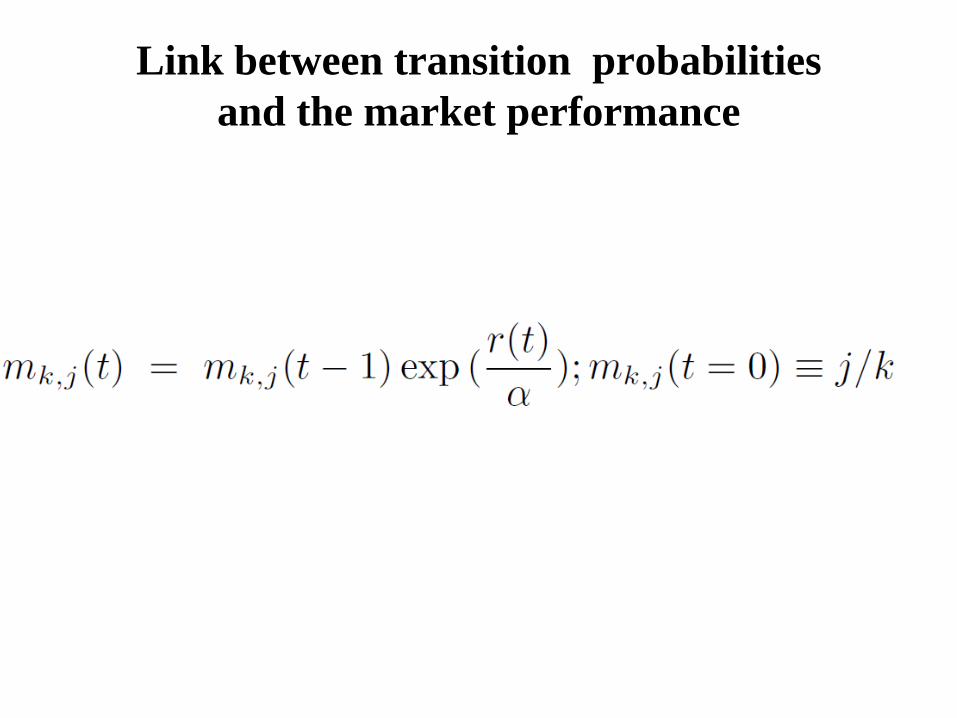

• r(t) the return of the market, RB(t)=[B(t)-

B(t-1)]/B(t), and η(t) Gaussian distributed

with zero mean and std. dev.:

Link between transition probabilities

and the market performance

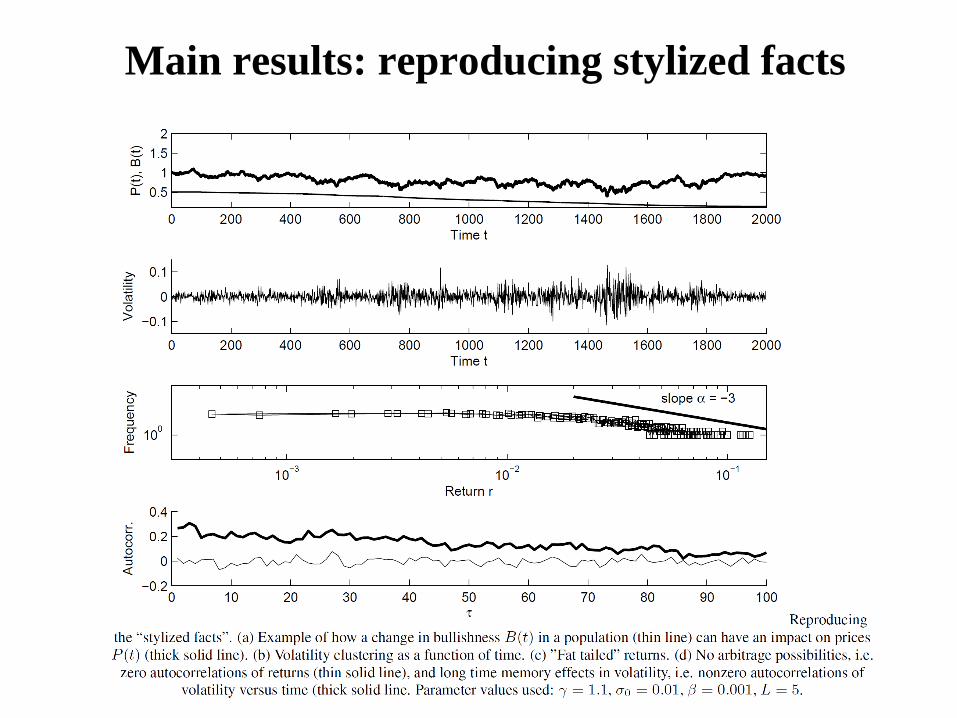

Main results: reproducing stylized facts

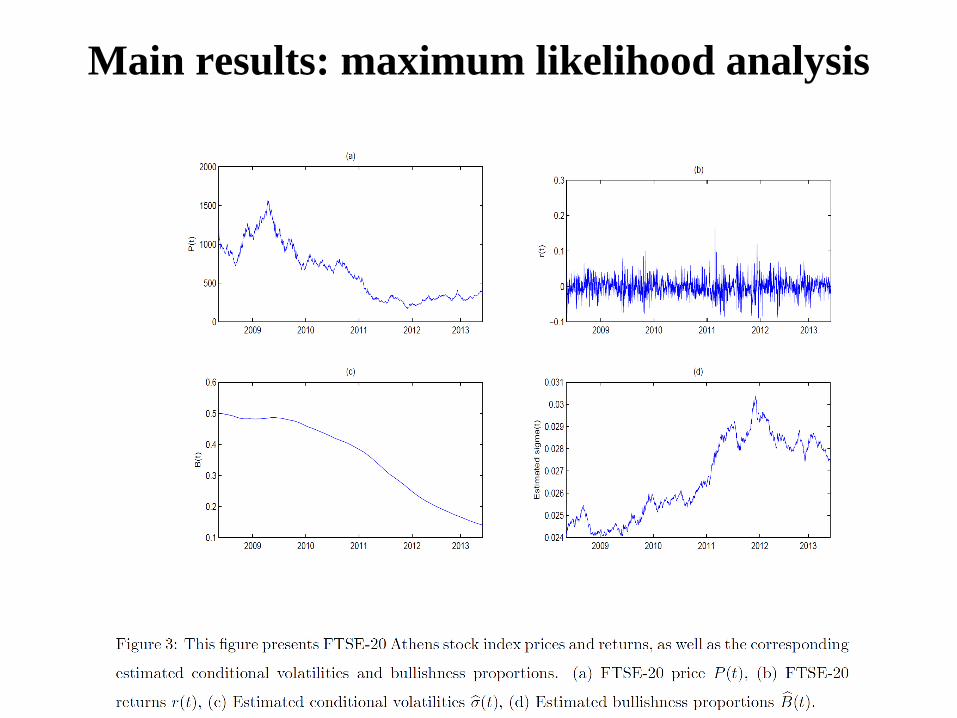

Main results: maximum likelihood analysis

Main results: maximum likelihood analysis

This project has received funding from the European Union’s

Seventh Framework Programme for research, technological

development and demonstration under grant agreement n° 320270

www.syrtoproject.eu

This document reflects only the author’s views.

The European Union is not liable for any use that may be made of the information contained therein.